Saudi Arabia Architectural Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

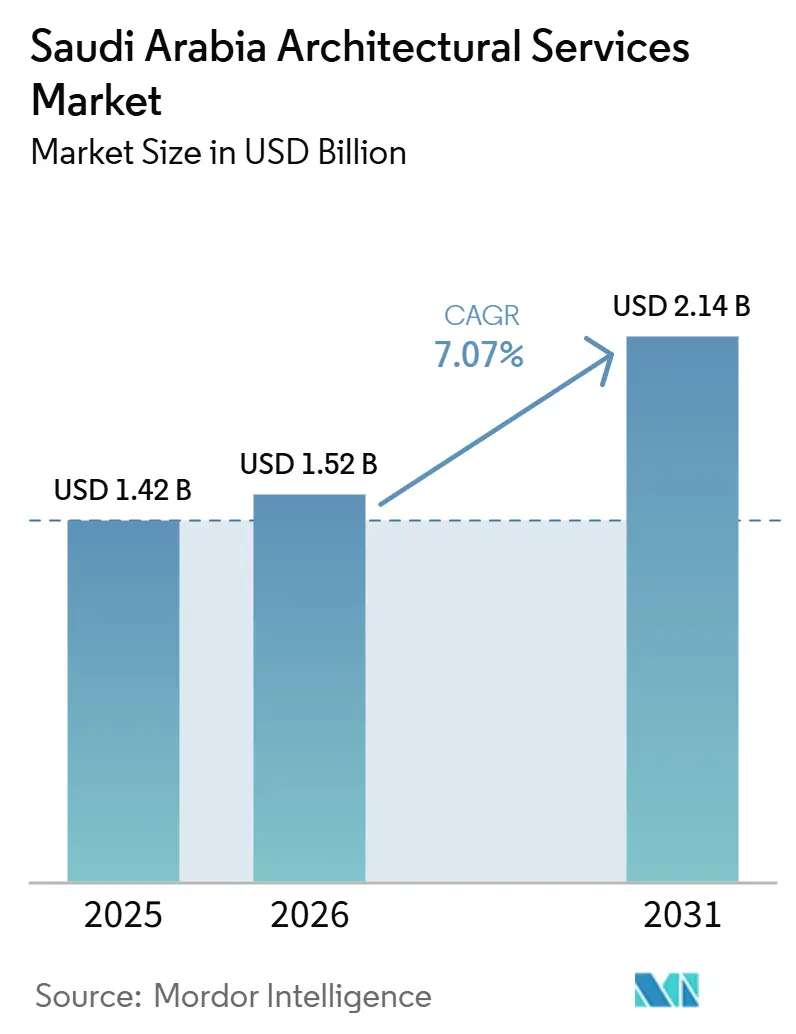

| Base Year Market Size (2025) | USD 1.42 Billion |

| Market Size (2026) | USD 1.52 Billion |

| Market Size (2031) | USD 2.14 Billion |

| Growth Rate (2026 - 2031) | 7.07% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Architectural Services Market Analysis by Mordor Intelligence

The Saudi Arabia Architectural Services Market size was valued at USD 1.42 billion in 2025 and is estimated to grow from USD 1.52 billion in 2026 to reach USD 2.14 billion by 2031, at a CAGR of 7.07% during the forecast period (2026-2031). The Saudi Arabia architectural services market is being shaped by a government-led capital cycle that continues to direct large design mandates to Riyadh, Diriyah, NEOM, the Red Sea coast, and other Vision 2030 locations. Public capital remained the main source of fee generation in 2025, although private investment is now scaling faster as hotel, logistics, branded residential, and workplace projects move from intent to execution. The Saudi Arabia architectural services market is also moving toward bundled procurement, where clients seek architecture, engineering, supervision, and digital delivery under a single mandate, which favors large, multidisciplinary firms and strong local partnerships[1]AECOM, “AECOM Selected to Deliver Project Management and Engineering Services for The Avenues Riyadh Phase II,” AECOM, aecom.com. Regulatory change is widening the competitive field because Saudization, municipal design controls, and Saudi architecture guidelines are pushing more delivery capacity and advisory work into the kingdom itself. A second stream of opportunity is forming around retrofit, repositioning, and compliance-led redesign as early Vision 2030 assets move into operational review and updated thermal, cultural, and sustainability requirements shape later design phases.

Key Report Takeaways

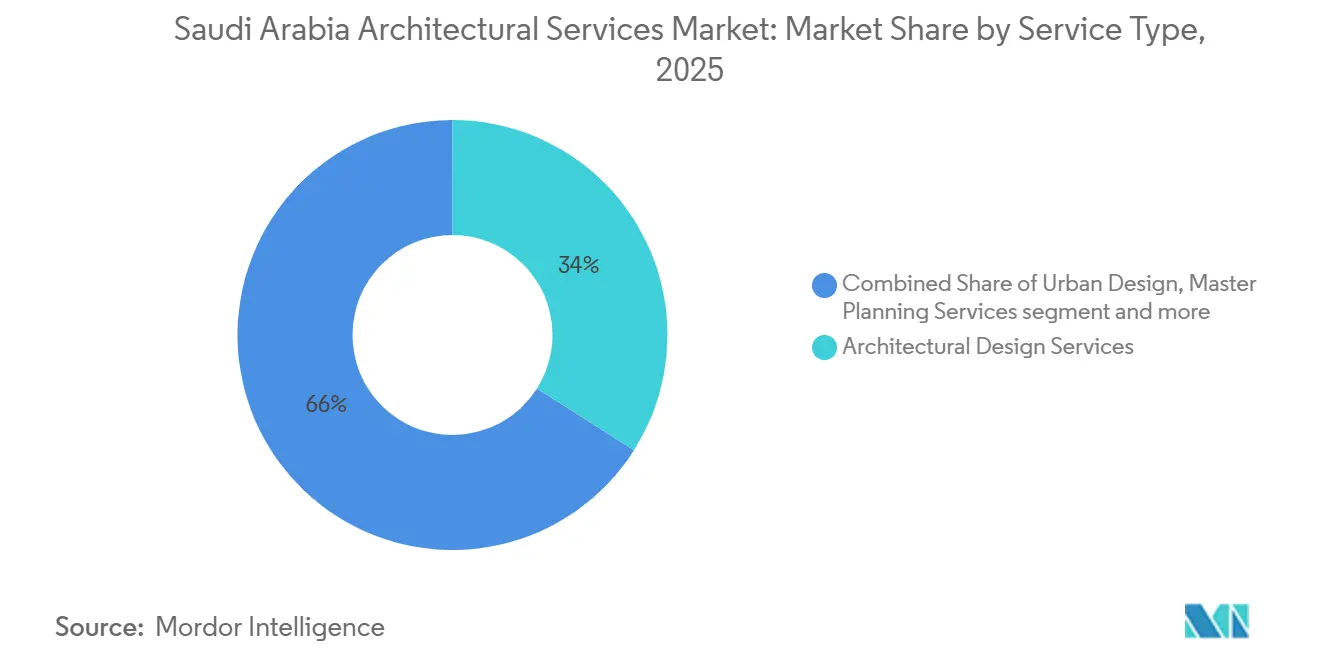

- By service type, architectural design services held 34% of the Saudi Arabia architectural services market size in 2025, while urban design and master planning services recorded the highest projected CAGR at 9.4% through 2031.

- By project type, new construction accounted for 79% of the Saudi Arabia architectural services market size in 2025, while renovation is forecast to expand at a 10.2% CAGR to 2031.

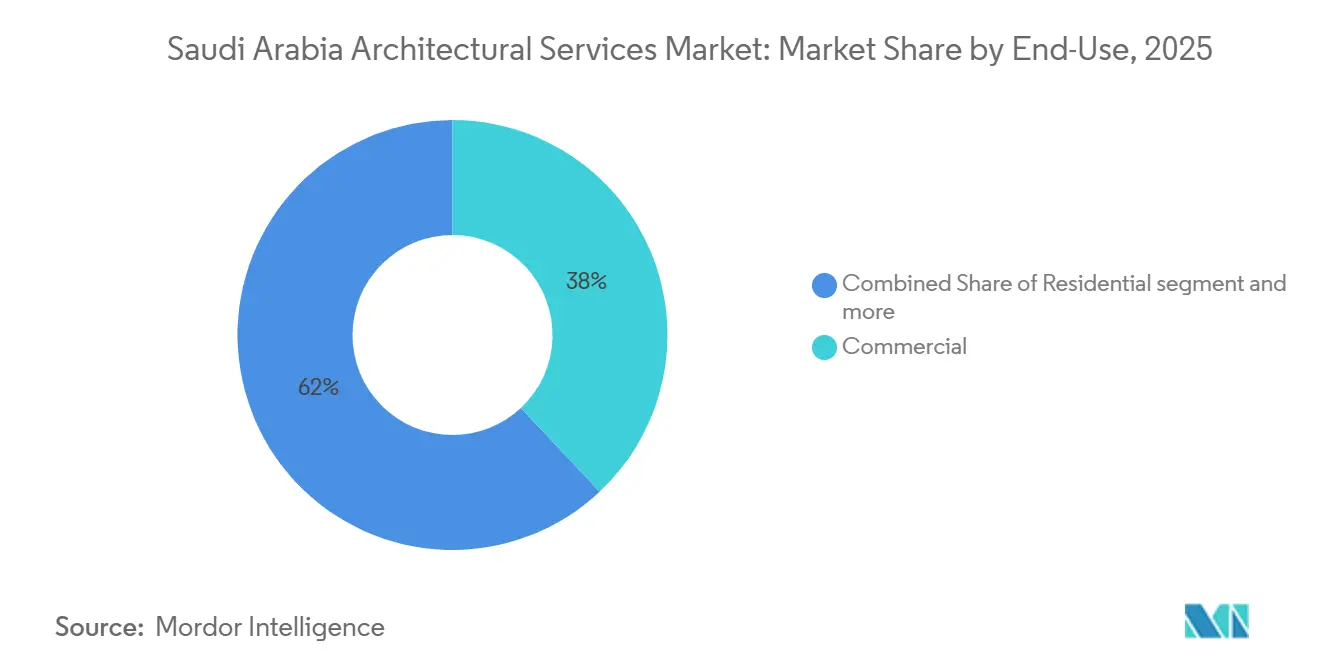

- By end use, commercial buildings led with 38% revenue share in 2025, while infrastructure-linked buildings are projected to grow at an 11% CAGR through 2031.

- By investment source, public investment held 63% of the Saudi Arabia architectural services market share in 2025, while private investment is set to record the highest CAGR at 9.1% through 2031.

- By city, Riyadh held 36% of the Saudi Arabia architectural services market share in 2025, while Rest of Saudi Arabia is forecast to expand at a 9.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Architectural Services Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 Mega-Project Pipeline | +2.4% | National, concentrated delivery in Riyadh, the NEOM corridor, and the Red Sea coast | Medium term (2-4 years) |

| Rising Demand for Destination-Led Tourism and Hospitality Design | +1.2% | Red Sea coast, AlUla, Diriyah, and Medina | Medium term (2-4 years) |

| Public Sector Demand for Integrated Design and Delivery | +1.0% | National, primarily Riyadh and secondary cities | Short term (≤ 2 years) |

| Smart City and Sustainability Mandates Expanding Design Scope | +0.8% | NEOM, Riyadh, and DMA | Medium term (2-4 years) |

| Retrofit and Repositioning Demand for Public and Commercial Assets | +0.7% | Riyadh, Jeddah, and DMA | Long term (≥ 4 years) |

| Localization Requirements Favoring In-Country Delivery Capability | +0.6% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Mega-Project Pipeline

The steady release of giga-project design mandates remains the largest source of architectural fee revenue in Saudi Arabia. In November 2025, AECOM and Jacobs, through a joint venture, were appointed by New Murabba Development Company to deliver design services for The Mukaab in north Riyadh, covering infrastructure, road tunnels, core podium areas, and public realm. In August 2025, AECOM was also selected as project management consultant and engineer for The Avenues Riyadh Phase II, a USD 4 billion-plus development with 1.87 million sq m of built-up area and 370,000 sq m of leasable space. This pattern shows that large Saudi developments are no longer assigning design work to a single lead architect. Multi-firm consortia are becoming more common, which is opening access to the Saudi fee pool for more mid-tier international firms and reducing the concentration of advantage among only the largest players.

Rising Demand for Destination-Led Tourism and Hospitality Design

Saudi Arabia’s target of attracting 150 million annual tourists by 2030 is creating a distinct and higher-value category of hospitality architecture that functions as destination infrastructure. Red Sea Global’s USD 23.6 billion Red Sea Project targets 50 resorts across 22 islands and 6 inland sites, and multiple properties are already operational, including Shebara Resort and Desert Rock, which opened in January 2025. In May 2025, AlUla Development Company unveiled the NUMAJ Autograph Collection Hotel concept, targeting LEED Gold certification and reinforcing sustainability as a standard design requirement rather than an optional add-on. This category also extends the revenue cycle for design firms because it creates follow-on work in conservation planning, operational design review, and sustainability certification. As a result, project award data alone does not fully capture the value of hospitality-led architectural demand in Saudi Arabia.

Public Sector Demand for Integrated Design and Delivery

Public sector clients, led by PIF, its giga-project subsidiaries, and municipal development authorities, are increasingly awarding contracts that combine architectural design with supervision, cost management, and digital delivery. In 2025, Diriyah Company awarded Omrania a USD 113.6 million architecture and design contract for the Diriyah Boulevard District. It also commissioned Parsons for a USD 56 million, 5-year mandate for public realm design and construction supervision for Diriyah Phase 2 GULFBUSINESS. These bundled procurement models favor firms with integrated delivery platforms rather than pure-play design studios. The result is a market structure that rewards firms with broad execution capability, while narrowing the share of work that remains available as stand-alone architectural mandates.

Smart City and Sustainability Mandates Expanding Design Scope

The King Salman Charter for Architecture and Urbanism has shifted municipal planning from general guidance toward a more enforceable framework tied to performance and identity. New projects must now demonstrate alignment with core values such as authenticity, continuity, human-centricity, livability, innovation, and sustainability. At the same time, climate-specific thermal-efficiency rules are discouraging expansive glass facades and pushing architects to incorporate shading devices, passive cooling strategies, and climate-responsive building envelopes into their design submissions. These requirements are increasing the amount of early-stage technical documentation and design coordination needed before permits are approved. That broader scope is already reflected in the strong growth outlook for urban design and master planning, where climate performance and planning compliance are becoming central parts of the work.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multi-Agency Approval Complexity | -0.8% | National, amplified in mega-project and heritage zones | Short term (≤ 2 years) |

| Shortage of Specialized Local Design Talent | -0.7% | National | Medium term (2-4 years) |

| Competitive Fee Pressure in Tender-Led Procurement | -0.5% | National | Short term (≤ 2 years) |

| Dependence on Imported Design Inputs and Technical Specifications | -0.4% | National, especially outside core metro areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Multi-Agency Approval Complexity

Approval delays remain a clear restraint on architectural delivery in Saudi Arabia, as large projects still require clearances from several agencies operating on separate timelines. Mega-projects and heritage-linked developments often move through the Architecture and Design Commission, Civil Defense, the Ministry of Environment, Water and Agriculture, the Heritage Commission, and utilities authorities before design packages can fully advance. A 2026 study in the Journal of Project Management found that legal complexity and overlapping regulatory jurisdictions have a statistically significant effect on project schedule performance in Saudi Arabia’s construction sector. Digital permit systems such as Baladi have helped standard residential applications, but large and mixed-use developments still sit outside simple automated workflows. This extends validation cycles, increases compliance effort, and shifts design resources away from billable technical work. Firms with dedicated regulatory coordination capacity, therefore, hold a structural advantage in complex project environments.

Shortage of Specialized Local Design Talent

The shortage of specialized local design talent is becoming more visible as regulatory requirements raise the need for qualified in-country staffing. Saudi Arabia enforced a 30% Saudization requirement for 46 engineering professions, including architecture, from 30 June 2026, and private-sector firms with 5 or more engineers must meet this quota while ensuring Saudi Council of Engineers accreditation and a minimum monthly salary of SAR 8,000 (USD 2,133), as per the supplied draft. A 2025 study also identified a mismatch between local architectural education and the technical requirements of internationally active firms, especially in BIM, computational design, and parametric documentation. This creates both wage pressure and a staffing bottleneck because demand for accredited Saudi architects is rising faster than the available specialist pool. The constraint is especially relevant for firms handling large and technically demanding mandates, where delivery standards are high and timelines are tight. Smaller private-sector projects are better placed to absorb this shift because staffing compliance is easier to manage at that scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Architectural Design Commands the Fee Pool

Architectural design services held the largest service-type share at 34% of the Saudi Arabia architectural services market in 2025, which reflects the value attached to concept, schematic, and lead-design work on large development programmes. The fee pool remains concentrated in these early phases because clients still place a premium on firms that can set design direction, coordinate complex briefs, and align projects with Saudi cultural and planning requirements. Urban design and master planning services are projected to grow at a 9.4% CAGR through 2031, the fastest pace among service sub-segments, because greenfield planning remains central to NEOM, Diriyah, airport-adjacent districts, and secondary city expansion. The rollout of Phase 3 Saudi architecture design guidelines to Jazan, Sakaka, and Buraydah in 2026 also widens the geographic base for formal master planning work[2]Architecture and Design Commission, “Salmani Architecture, Core Architectural Pillars and Compliance Framework,” Architecture and Design Commission, architsaudi.dasc.gov.sa . That shift means the Saudi Arabia architectural services market is not only deepening in Riyadh, it is also broadening into cities that now require more structured design governance.

Interior architecture and space planning continue to benefit from high-specification workplace, hospitality, and mixed-use projects across the kingdom. In practice, this service line gains when occupiers and developers want cultural identity, wellness, and operational efficiency resolved within the same interior brief. Architectural documentation and delivery services remain structurally necessary, but margins are tighter because compliance demands are rising even when unit pricing does not move at the same rate. The Saudi Arabia architectural services industry also includes specialty advisory work under the “others” category, such as heritage conservation architecture, acoustic input, and sustainability certification support. These activities are becoming more visible because recurrent review, restoration, and compliance work is growing around heritage destinations and high-profile cultural assets. The Saudi Arabia architectural services market also shows a clear split between design authorship and delivery intensity inside this segment. Lead design work captures attention and brand value, but documentation, technical coordination, and permit closure now consume a larger share of working hours than before. That is especially true where Salmani compliance, material controls, and climate-response evidence must be embedded in submissions. Firms with in-country licensing capacity therefore have an advantage because they can move between concept ambition and procedural closure with less friction. This is why service-line growth in the Saudi Arabia architectural services market is strongest where strategic planning and local compliance overlap.

By Project Type: Renovation Challenges New-Build Primacy

New construction commanded 79% of Saudi Arabia architectural services market revenues in 2025, which reflects the still-young development cycle of many Vision 2030 assets. Most flagship sites are still moving through design, documentation, supervision, and staged handover, so fee generation remains tied to first-cycle delivery rather than mature asset repositioning. Renovation is forecast to grow at a 10.2% CAGR through 2031, which makes it the fastest-growing project type in the Saudi Arabia architectural services market. This shift is supported by sports infrastructure, public assets, hospitality properties, and mixed-use developments that already require design updates, branding changes, sustainability recalibration, or code-led technical improvements. In May 2025, AECOM was appointed to provide site supervision consultancy services for the transformation of King Fahd International Stadium in Riyadh, which illustrates the scale of renovation mandates now entering the pipeline.

Renovation work will not displace new construction in absolute value during the forecast window, but it will widen the service mix. Retrofit commissions often carry lower individual construction values, yet they generate repeated technical reviews and strong follow-on advisory work when assets remain active during improvements. Government assets are also moving into updated thermal, cultural, and operational compliance cycles, which supports a recurring renovation stream rather than a one-time catch-up phase. For firms already embedded in supervision or as-built documentation, this creates a strong route into repeat appointments. That gives incumbents a practical edge in the Saudi Arabia architectural services market because they already understand the asset, the delivery history, and the approval pathway. A second implication is that project-type competition will become less dependent on who wins the first concept package. Firms that were not part of the original design team can still enter through asset repositioning, operational redesign, or venue modernization if they have the right technical credentials. The Saudi Arabia architectural services market therefore opens new space for specialist retrofit and adaptation firms even while mega-project new-build work stays dominant. This balance should keep the project mix broader than headline new-construction shares might suggest. It also reduces reliance on a single procurement moment for long-term client access.

By End-Use: Commercial Leads, Infrastructure-Linked Buildings Accelerate

Commercial buildings held a 38% share of 2025 revenues, which kept them as the largest end-use category in the Saudi Arabia architectural services market. The category is supported by headquarters demand, retail-led mixed-use projects, hospitality clusters, and premium office schemes that require strong design identity as well as practical fit-out efficiency. In January 2026, Gensler completed a 25,000 sq m, 12-story LEED Gold-certified workplace in Riyadh’s Laysen Valley, which captures the performance standard now expected in high-end corporate briefs. Infrastructure-linked buildings are projected to grow at an 11% CAGR through 2031, which makes them the fastest-growing end-use line in the Saudi Arabia architectural services market. Demand here is tied to metro-adjacent districts, aviation facilities, convention venues, exhibition complexes, and other assets where buildings and transport systems are designed as one development logic.

Residential work remains substantial in volume, but it usually carries lower fee intensity than flagship commercial or infrastructure-linked mandates. Its importance comes from scale, geographic spread, and the need to apply Saudi design criteria consistently across large communities rather than from unusually high fee rates per commission. Institutional, industrial, and logistics design is also becoming more visible in secondary cities where universities, healthcare facilities, logistics cities, and industrial clusters are moving into later design stages. These typologies require technical coordination that was less common in earlier phases of the Saudi Arabia architectural services market. That helps diversify fee generation beyond hotels and office towers.Commercial leadership in 2025 does not mean the category is simple or uniform. Office, retail, hospitality, and mixed-use schemes each move on different timing, different approval routes, and different delivery expectations. Infrastructure-linked buildings, by contrast, benefit from the kingdom’s wider capital build-out because every major transport or public venue investment tends to create a connected building programme. This is why the Saudi Arabia architectural services market is seeing growth shift toward more complex end-use combinations rather than a narrow rise in one building type. Firms that can link architecture with movement systems, public realm, and operational planning are best placed to benefit from that shift.

By Investment Source: Public Capital Anchors, Private Sector Scales

Public investment accounted for 63% of the Saudi Arabia architectural services market in 2025, so the market was still anchored by PIF and its associated development platforms. These clients shaped the scale and timing of the largest commissions, and they also influenced procurement standards because they frequently demanded integrated delivery and strong program-level accountability. Private investment is projected to grow at a 9.1% CAGR through 2031, which makes it the faster-moving capital source in the Saudi Arabia architectural services market. Hotel operators, logistics developers, branded residential builders, data center investors, and workplace developers are moving more actively as regulatory clarity improves and demand visibility strengthens. That growth does not replace public capital, but it does create a second engine of fee expansion that is less dependent on a small number of mega-platforms.

Private clients usually work on shorter time frames and with tighter commercial discipline, which changes how firms compete. Fees face more pressure, but decisions can move faster, and approval management is often more direct than on very large public schemes. At the same time, private projects still need to align with the same broad design and performance expectations that now shape new Saudi development more generally. This reduces the historic gap between public and private design documentation intensity. It also means the Saudi Arabia architectural services market is converging around similar technical standards even when the client type changes. The difference between the 63% public share and the higher private growth rate mainly reflects where each capital stream sits in its development cycle. Public programmes already captured very large first-wave mandates, while private capital is still expanding into more typologies and more cities. Over time, this should make the Saudi Arabia architectural services market more balanced, even if public institutions continue to set the tone for scale and procurement structure. Firms that can serve both client groups will have more stable pipelines than firms tied too closely to only one funding source. That strategic flexibility is becoming more valuable as the project base widens.

Geography Analysis

Riyadh accounted for 36% of the Saudi Arabia architectural services market size in 2025, and it remains the core revenue center because the capital hosts the densest concentration of administrative, residential, sports, transport, and mixed-use programs. The city’s role is changing as flagship projects move beyond concept design into documentation, construction supervision, and post-award design review work. That gives Riyadh a deeper fee base than a city that depends only on first-stage master planning. In November 2025, AECOM and Jacobs were appointed on The Mukaab, and in August 2025, AECOM also secured the project management consultant and engineering role for The Avenues Riyadh Phase II, which shows the scale of concurrent assignments active in the capital. Riyadh, therefore, remains the anchor of the Saudi Arabia architectural services market even as more growth shifts outward.

Jeddah generates the second-largest fee pool in the Saudi Arabia architectural services market because it combines aviation-linked work, commercial densification, and coastal tourism-related development. SOM’s appointment on the T3A West Terminal at King Abdulaziz International Airport highlights the scale of design work tied to the city’s gateway role. The city also supports engineering-adjacent design activity through large urban infrastructure programs, including long-duration resilience and drainage work that affects the built environment[3]WSP, “Transforming Flood Risks into Resilience, Jeddah Stormwater Drainage Programme,” WSP, wsp.com. DMA is smaller in revenue terms, but it matters because industrial, logistics, and port-adjacent development create technically specialized demand that is different from Riyadh and Jeddah.

Rest of Saudi Arabia is set to expand at a 9.8% CAGR through 2031, which gives it the fastest growth profile in the Saudi Arabia architectural services market. Medina benefits from the Rua Al Madina development, which targets 30 million pilgrims and visitors by 2030 and supports a sustained hospitality and mixed-use design pipeline. AlUla is gaining momentum through destination-led hospitality and heritage-sensitive development, including the NUMAJ concept unveiled in May 2025. The NEOM corridor and Jazan add a different mix of demand, centered on greenfield planning, climate-responsive design, and industrial or tourism expansion. This wider geographic spread means the Saudi Arabia architectural services market will increasingly reward firms that can operate beyond the three main metro areas.

Competitive Landscape

The Saudi Arabia architectural services market has a moderately concentrated top tier and a broad fragmented middle tier. Large global multidisciplinary firms hold the most visible mandates because clients often want architecture, engineering, supervision, and digital coordination in one platform. AECOM, Jacobs, SOM, and Gensler all secured prominent assignments in 2025 and 2026, often through joint ventures or locally anchored delivery structures. The Saudi Arabia architectural services market therefore favors firms that can combine design credibility with execution scale and local compliance capability. That still leaves room for regional specialists and Saudi-licensed firms in secondary commissions, residential typologies, and advisory niches.

One clear strategic move is portfolio bundling. AECOM’s roles on The Mukaab, The Avenues Riyadh Phase II, and King Fahd International Stadium show how firms are spreading across design, engineering, and supervision rather than competing for one package at a time. A second move is local scaling, where Saudi-anchored firms step into larger mandates, as shown by Omrania’s architecture and design contract for Diriyah Boulevard. A third move is specialization in premium design categories, which is visible in Gensler’s Riyadh workplace project and SOM’s airport terminal assignment. These examples show that competition in the Saudi Arabia architectural services market is being shaped by breadth, local access, and technical specialization at the same time.

There is still open space in BIM-first delivery, heritage conservation architecture, and sustainability certification support because these areas demand local capacity and technical depth together. The 30% Saudization requirement for engineering professions is also changing the way international practices build teams, which makes consortium structures and Saudi hiring pipelines more important than before. Market access is no longer defined only by winning a design brief. It is increasingly defined by whether a firm can satisfy accreditation, staffing, and documentation expectations inside Saudi Arabia. That keeps the Saudi Arabia architectural services market competitive, but it also raises the practical barriers to entry for firms without a durable local base.

Saudi Arabia Architectural Services Industry Leaders

AECOM

Jacobs Solutions Inc.

Gensler

Perkins and Will

HOK

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Saudi Arabia enforced a 30% Saudization requirement for 46 engineering professions, including architecture, effective 30 June 2026. Private-sector firms employing 5 or more engineers must maintain a 30% Saudi national quota, with each qualifying professional accredited by the Saudi Council of Engineers and earning a minimum of SAR 8,000 per month (USD 2,133.3 per month).

- January 2026: Gensler completed a 25,000 sq m, 12-story LEED Gold-certified workplace in Riyadh's Laysen Valley for a leading professional services client, establishing a new benchmark for culturally integrated, sustainability-accredited corporate interiors in the Kingdom.

- November 2025: AECOM and Jacobs, in a joint venture, were appointed by New Murabba Development Company to provide design services for The Mukaab — the 247-acre centerpiece of Riyadh's New Murabba development — covering infrastructure, road tunnels, the Mukaab Core, and public realm, in support of Saudi Arabia's Vision 2030 urban transformation program.

- August 2025: AECOM was selected as Project Management Consultant and engineer for The Avenues Riyadh Phase II, a USD 4 billion-plus, 1.87 million sq m mixed-use development in North Riyadh City encompassing a luxury shopping mall and five multi-use towers.

Saudi Arabia Architectural Services Market Report Scope

| Architectural Design Services |

| Architectural Documentation and Delivery Services |

| Interior Architecture and Space Planning Services |

| Urban Design and Master Planning Services |

| Others |

| New Construction |

| Renovation |

| Residential | |

| Commercial | Office |

| Retail | |

| Institutional | |

| Industrial and Logistics | |

| Others | |

| Infrastructure-linked Buildings |

| Public |

| Private |

| Riyadh |

| Jeddah |

| DMA ( Dammam Metropolitan Area) |

| Rest of Saudi Arabia |

| By Service Type | Architectural Design Services | |

| Architectural Documentation and Delivery Services | ||

| Interior Architecture and Space Planning Services | ||

| Urban Design and Master Planning Services | ||

| Others | ||

| By Project Type | New Construction | |

| Renovation | ||

| By End-Use | Residential | |

| Commercial | Office | |

| Retail | ||

| Institutional | ||

| Industrial and Logistics | ||

| Others | ||

| Infrastructure-linked Buildings | ||

| By Investment Source | Public | |

| Private | ||

| By City | Riyadh | |

| Jeddah | ||

| DMA ( Dammam Metropolitan Area) | ||

| Rest of Saudi Arabia | ||

Key Questions Answered in the Report

What is the 2031 outlook for architectural services in Saudi Arabia?

The Saudi Arabia architectural services market is projected to reach USD 2.1 billion by 2031 from USD 1.5 billion in 2026, growing at a 7.1% CAGR.

Which service line is growing the fastest in Saudi Arabia?

Urban design and master planning services are expected to grow the fastest, at a 9.4% CAGR through 2031, supported by greenfield planning and wider design governance.

Why is renovation becoming more important for firms in Saudi Arabia?

Renovation is projected to grow at a 10.2% CAGR as early Vision 2030 assets move into repositioning, sustainability upgrades, and technical compliance work.

Which end-use segment offers the strongest growth potential?

Infrastructure-linked buildings are forecast to grow at an 11% CAGR through 2031, driven by transport, aviation, convention, and exhibition development.

Page last updated on: