Saudi Arabia Residential Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

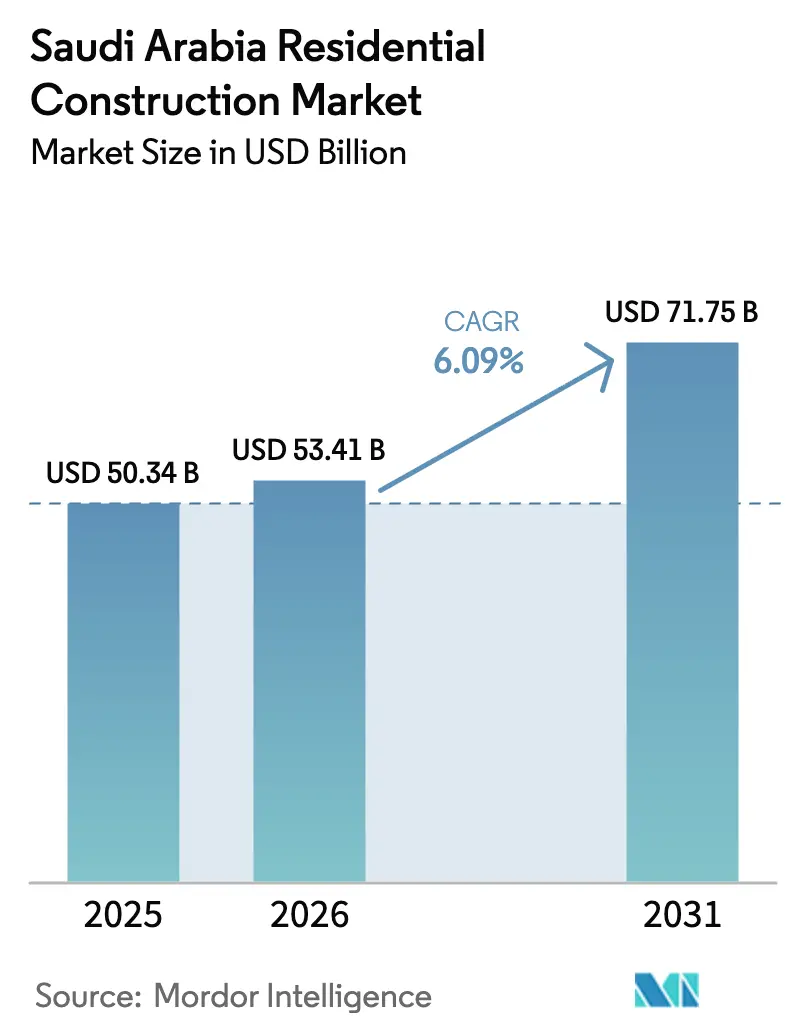

| Base Year Market Size (2025) | USD 50.34 Billion |

| Market Size (2026) | USD 53.41 Billion |

| Market Size (2031) | USD 71.75 Billion |

| Growth Rate (2026 - 2031) | 6.09% CAGR |

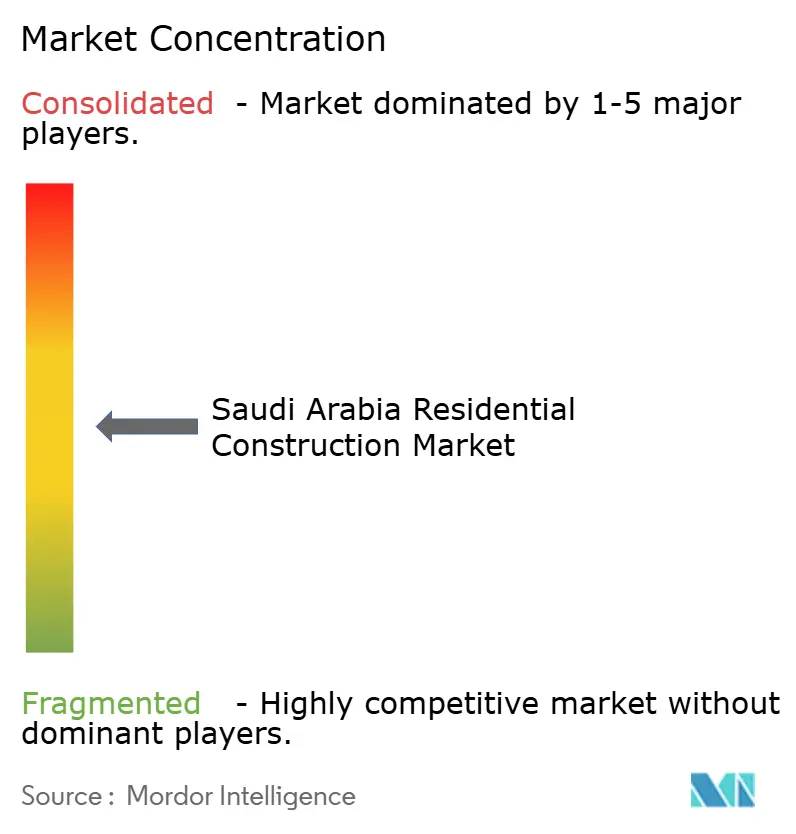

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Residential Construction Market Analysis by Mordor Intelligence

The Saudi Arabia Residential Construction Market size is projected to be USD 50.34 billion in 2025, USD 53.41 billion in 2026, and reach USD 71.75 billion by 2031, growing at a CAGR of 6.09% from 2026 to 2031.

Strong government backing through Vision 2030 keeps annual housing demand around 300,000 units, a target that pushes developers toward off-site construction to avoid site-capacity bottlenecks. Faster mortgage growth, a rising share of private capital, and streamlined permits on the Etmam digital platform shorten development cycles and spur fresh launches. Contractor pipelines are filling quickly as Public Investment Fund (PIF) subsidiaries pre-book capacity, while modular suppliers carve out a niche on giga-project sites. Input-cost inflation and slow utility hookups temper near-term growth yet also encourage prefabrication and early-stage infrastructure commitments by sponsors.

Key Report Takeaways

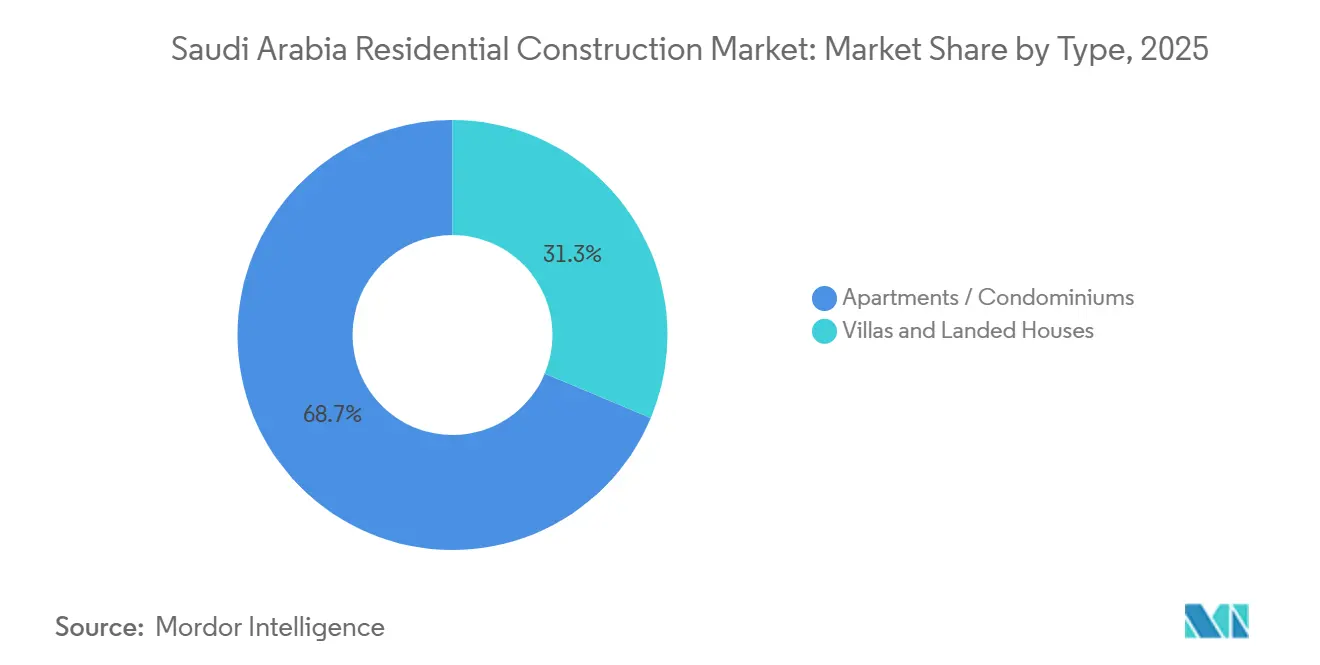

- By type, apartments and condominiums led with 68.7% of the Saudi Arabia residential construction market share in 2025, while villas and landed houses are projected to expand at a 6.35% CAGR through 2031.

- By construction type, new-build schemes captured 84.5% of the Saudi Arabia residential construction market share in 2025, whereas renovation activity is forecast to grow at a 6.41% CAGR to 2031.

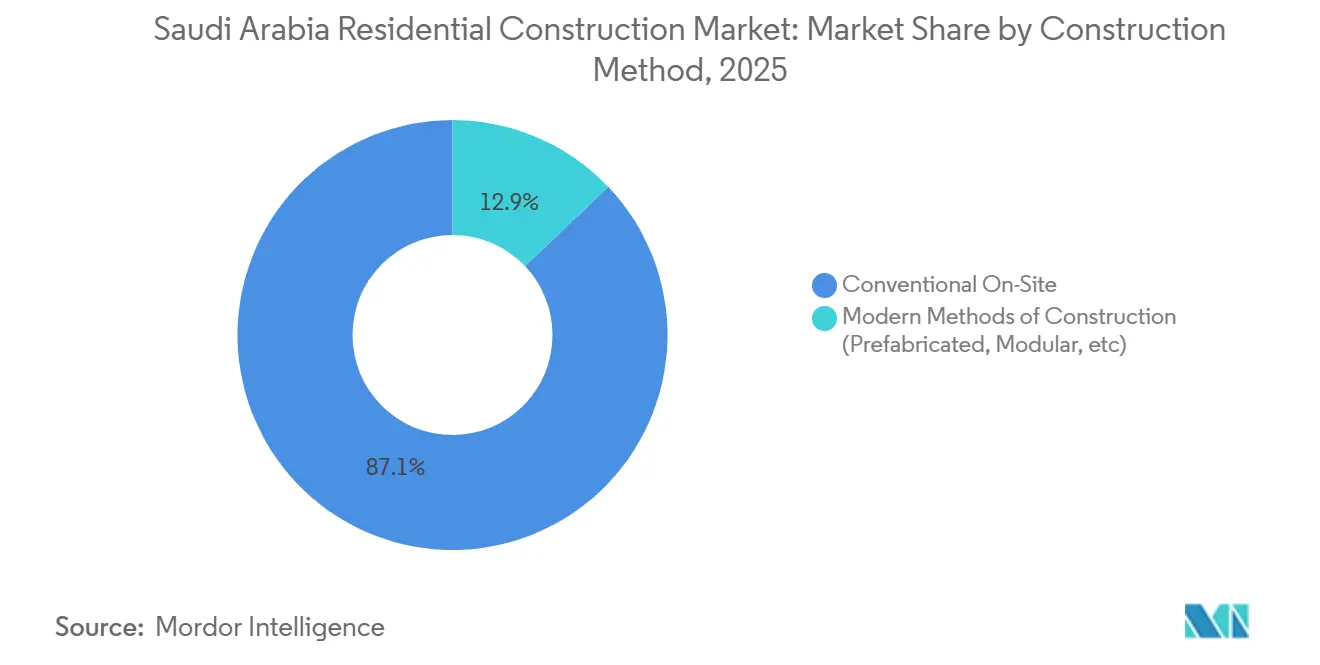

- By construction method, conventional on-site work retained 87.1% of the Saudi Arabia residential construction market share in 2025, but modern modular systems are expected to post a 6.55% CAGR over 2026-2031.

- By investment source, private capital accounted for 70.1% of 2025 spending, whereas public-sector programs financed by REDF and PIF are set to rise at a 6.31% CAGR to 2031.

- By city, Riyadh commanded 41.3% of the Saudi Arabia residential construction market size in 2025, while the Dammam Metropolitan Area is projected to register the fastest 6.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Residential Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 housing targets accelerating community-scale projects | +1.8% | Kingdom-wide, strongest in Riyadh and Jeddah, plus giga-project zones | Medium term (2–4 years) |

| Mortgage uptake and developer financing support | +1.5% | National, the highest in Riyadh and Jeddah | Short term (≤ 2 years) |

| Strong population growth and urbanization | +1.2% | National, with peak pressure in Riyadh, Jeddah, and Eastern Province | Long term (≥ 4 years) |

| Giga-projects driving employee housing demand | +1.0% | NEOM (Tabuk), Diriyah, Red Sea, Qiddiya corridors | Medium term (2–4 years) |

| Rising off-site and modular construction adoption | +0.7% | Early uptake at NEOM, ROSHN, and NHC sites | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Housing Targets: Accelerating Community-Scale Projects

Homeownership stood at 65.4% in 2024, leaving a gap of 4.6 percentage points to the 70% goal by 2030. ROSHN’s 20 km² Riyadh community alone will house more than 30,000 families once complete. In January 2026, ROSHN let SAR 1.5 billion (USD 400 million) of Phase 4-5 contracts and secured SAR 2.1 billion (USD 560 million) of new land, signaling durable capital flows. National Housing Company (NHC) now oversees 134,000 units across 17 cities under joint-venture terms that reduce state outlays while speeding delivery. Ministry-level oversight through MOMRAH ties every masterplan to Saudi Building Code 2024 requirements, locking sustainability into project baselines[1]Ministry of Municipal, Rural Affairs and Housing, “Etmam Platform Cuts Approval Durations,” momrah.gov.sa.

Mortgage Uptake and Developer Financing Support Increasing Launches

Real Estate Development Fund (REDF) subsidies dropped effective mortgage rates by up to 3 percentage points in 2025, lifting loan-to-value ratios to 85% for first-time buyers. This financing safety net helped Dar Al Arkan push Shams Ar Riyadh and launch the Etoile by Elie Saab tower, both scheduled to finish before the end of 2026. Retal Urban Development signed SAR 1.39 billion (USD 370 million) and SAR 252 million (USD 67 million) deals with NHC that let the developer recycle presale proceeds into successive phases. Stable overnight rates at the Saudi Central Bank prevent debt-service spikes and encourage banks to widen mortgage books[2]Saudi Central Bank, “Quarterly Mortgage Report 2025,” sama.gov.sa .

Strong Population Growth and Urbanization Sustaining Supply Needs

Saudi Arabia’s population surpassed 32 million in 2025, with urbanization above 84%. Riyadh alone could hit 8.5 million residents by 2030, implying 50,000-60,000 new homes each year. Jeddah’s role as the Red Sea gateway couples religious tourism with permanent migration, while petrochemical hiring in Dammam and Jubail fuels Eastern Province demand. The White-Land Tax policy pressures landowners to build or sell, accelerating site releases and helping apartments claim 68.7% of 2025 volume[3]General Authority for Statistics, “Construction Cost Index 2025,” gastat.gov.sa.

Expansion of Giga-Projects Driving Employee Housing Demand

Peak labor across NEOM, Diriyah, Red Sea Global, and Qiddiya may top 1.8 million by 2028. NEOM’s SAR 2.8 billion (USD 746 million) Phase II deal with Homagic covers 12,000 permanent modular units built to 50-year durability and LEED Gold standards. Diriyah Gate and Qiddiya are adding downstream residential clusters for managers and service staff, while Red Sea Global resorts raise villa demand in Yanbu and Umluj. These hubs anchor entire micro-economies that sustain housing even after construction winds down.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising construction costs and contractor capacity constraints are pressuring project timelines | -1.2% | National, with the highest impact in Riyadh and Jeddah, where demand concentration strains labor and material supply | Short term (≤ 2 years) |

| Land servicing and utility connections are delaying handovers in new communities | -0.9% | National, particularly in greenfield masterplans (ROSHN, NHC communities, giga-project peripheries) | Medium term (2–4 years) |

| Regulatory approvals and compliance requirements are extending project development cycles | -0.6% | National, with more pronounced impact in secondary cities where Etmam digital platform adoption lags behind Riyadh and Jeddah | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Construction Costs and Capacity Constraints

The GASTAT construction-cost index advanced 0.7-1.0% year-on-year in 2025 as cement, steel, and skilled-labor prices climbed. Turner & Townsend pegged average Riyadh build costs at USD 3,112 per m², up on worker shortages created by concurrent giga-projects. Large contractors like Al Bawani and Shapoorji Pallonji hit bandwidth ceilings even after topping USD 800 million in annual Saudi revenue, forcing developers to embed inflation clauses and pre-order materials months ahead.

Land-Servicing and Utility Connections Slowing Handover

Before occupancy permits are issue, communities need water mains, substations, and fiber. National Water Company tie-ins for ROSHN’s Sedra project added 6-12 months despite early excavation and right-of-way clearances. Saudi Electricity Company faces similar load-upgrade queues, while traffic-impact studies push highway access approvals to a further 3-6 months. Developers are now front-loading infrastructure—ROSHN bundled utilities into a SAR 1.9 billion (USD 507 million) Sedra contract—to cut these critical-path risks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Apartments Dominate, Villas Accelerate

Apartments and condominiums held 68.7% of the Saudi Arabia residential construction market in 2025, illustrating the land-efficiency imperative in core Riyadh and Jeddah districts. Premium schemes such as Abdul Latif Jameel Land’s J|ONE in Jeddah delivered 242 units in 19.5 months, showing why high-rise formats remain popular among young professionals. Villas are forecast to post the segment-best 6.35% CAGR through 2031 as suburban masterplans and giga-project executive housing lift demand for larger footprints and private outdoor space. ROSHN’s Sedra phases mix three-bedroom townhouses with four-bedroom villas and market them to families that value privacy yet still want quick airport access.

Apartment affordability benefits from mortgage limits that reach 85% LTV, whereas villa finance typically caps at 75%, skewing younger buyers toward vertical living. Supply also dovetails with Saudi Building Code energy goals; shared walls reduce cooling loads in a climate where air-conditioning commands up to 60% of household electricity use. Conversely, villa builders differentiate through energy-saving façades and low-flow plumbing that cut utility bills by 18% and 17% respectively, versus older stock, as proven under Shapoorji Pallonji’s Sedra contract. Design choice, lifestyle preferences, and financing terms, therefore, keep both formats in play, but apartments maintain the numerical edge while villas outpace in growth.

By Construction Type: New Build Dominates, Renovation Rises

New schemes captured 84.5% share of the Saudi Arabia residential construction market in 2025 on the back of Vision 2030’s 300,000-unit annual target. Digital Etmam permitting slashed average approval cycles to 45 days, letting ROSHN award SAR 1.5 billion (USD 400 million) of fresh Sedra work in January 2026. Renovations are emerging at a 6.41% CAGR because 1980s-1990s stock in Riyadh’s Al Malaz and Jeddah’s Al Salamah faces SBC 601 energy-retrofit deadlines. Landlords now weigh USD 1,500-2,000 per m² refurbishment against USD 3,112 per m² for a replacement build, often choosing upgrades that extend asset life and lift rents through better insulation and new HVAC systems.

Renovation also receives a policy boost: projects meeting LEED or Estidama standards enjoy fast-track permits and utility rebates, improving the return profile. In tight districts where raw land is scarce, rehab stays the only path to supply growth. Meanwhile, greenfield demand still rules new build, especially in giga-project satellite towns and public-private housing schemes that bundle infrastructure and vertical components to compress schedules.

By Construction Method: Conventional Leads, Modular Gains Speed

Conventional on-site work controlled 87.1% of 2025 output thanks to deep contractor familiarity with cast-in-place concrete and blockwork. CSCEC’s 1,092-unit Dammam South project topped out a month early, even using standard flow-line sequencing, proving traditional methods still deliver when optimized. Modular solutions, however, are growing 6.55% CAGR as NEOM and ROSHN place bulk orders for factory-made units that meet 50-year durability and net-zero carbon targets. Homagic’s 12,000-unit NEOM Phase II package runs 90% off-site fabrication, slices on-site waste by 80% and trims program time nearly by half.

Saudi authorities now publish modular approval guides, easing municipal skepticism and paving the way for China Harbour Engineering’s domestic prefab plant. Hybrid models also emerge; Shapoorji Pallonji drops completed bathroom pods and kitchen modules into conventionally cast structures, compressing critical paths by four to six months without full design overhauls.

By Investment Source: Private Funds Predominate, Public Capital Expands

Private developers supplied 70.1% of 2025 spending, a vote of confidence in mortgage uptake and mid-market demand. Dar Al Arkan’s luxury towers, Retal’s SAR 1.39 billion (USD 370 million) PPP with NHC, and Abdul Latif Jameel Land’s turnkey complexes all rely on presales plus bank debt, allowing quick recycling of capital. Public contributions, though smaller at 29.9%, are forecast to grow 6.31% CAGR through 2031 as REDF low-rate mortgages and PIF balance sheets underwrite affordable housing and major infrastructure.

State funding often shoulders off-site utilities, lowering entry barriers for private vertical developers. Saudization quotas of 30-40% on public jobs additionally anchor employment goals, turning housing into an economic-diversification lever that attracts bipartisan support.

Geography Analysis

Riyadh’s dominance stems from its role as the Kingdom’s political and business center; the city alone accounted for 41.3% of the 2025 budget and continues to attract mega-community investments such as ROSHN’s multi-phase Sedra. High absorption rates, REDF-backed mortgages, and proximity to giga-projects like Diriyah Gate sustain forward sales even with construction costs at USD 3,112 per m². Builders mitigate inflation risk by early material procurement and integration of modular components for bathrooms and façades.

Jeddah ranks second yet differs in the demand mix. Tourism and pilgrimage flows boost serviced-apartment formats, while luxury towers target high-net-worth expatriates returning under the Premium Residency scheme. Land prices run 20-30% below comparable Riyadh zones, giving developers wider margin cushions. Fast-tracked permits on Etmam shorten project gestation, and mixed-use waterfront schemes increase liveability metrics that elevate unit pricing.

The DMA posts the fastest 6.81% CAGR because industrial expansion out east adds continuous white- and blue-collar inflows. New highways and King Abdulaziz Port upgrades enhance logistics appeal, while lower land costs—roughly 40% under Riyadh prime sites—make entry-level villas attainable for first-time buyers. Modular adoption grows here too; CSCEC’s zoned flow-line approach in Dammam South met structure deadlines a month early, proving the value of digital scheduling and central procurement in cut-throat timelines.

Competitive Landscape

Competition remains moderate; about half of the 2025 project value lies with the top ten players, giving a mid-table concentration score. PIF entities like ROSHN, NHC, and Saudi Entertainment Ventures now bundle multi-year deals to lock contractor capacity and curb inflation exposure. ROSHN alone placed SAR 1.5 billion (USD 400 million) Sedra work in January 2026, then signed SAR 2.1 billion (USD 560 million) of land deals—moves that crowd out smaller rivals on prime plots.

International entrants lift technical standards. CSCEC dominates modular segments with Homagic after securing NEOM’s 12,000-unit order. Shapoorji Pallonji uses hybrid build models and bundled infrastructure to win repeat ROSHN contracts, while China Harbour Engineering’s planned prefab plant marks a commitment to localize supply and meet Saudization quotas. Digital tools are widespread: BIM adoption at Dammam South reduced rework, and Etmam integration lets developers track permit status in real time, smoothing cash-flow planning.

Niche specialists still find room. Mid-tier contractors focus on retrofit work in aging Riyadh and Jeddah cores where 1980s towers need MEP and façade upgrades for SBC 601 compliance. Al Bawani pivots toward leisure-anchored housing via the USD 293.3 million Seven Yanbu entertainment hub, diversifying beyond plain residential blocks. Financing creativity—from land-for-equity swaps to sharia-compliant bonds—adds another layer of differentiation as firms chase capital-light structures that fit Vision 2030 social mandates.

Saudi Arabia Residential Construction Industry Leaders

Saudi Cyprian Construction Co. Ltd.

Saudi Constructioneers Ltd. (Saudico)

Nesma & Partners

Jabal Omar Development Co.

Sedco Development

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: ROSHN let SAR 1.5 billion (USD 400 million) of Sedra Phase 4-5 contracts and closed SAR 2.1 billion (USD 560 million) in land at Restatex, locking pipeline capacity for its 30,000-unit Riyadh scheme.

- January 2026: CSCEC topped out Dammam South 30 days early, finishing structural works on 1,092 units across 39 buildings.

- November 2025: NEOM issued Homagic a SAR 2.8 billion (USD 746 million) deal for 12,000 net-zero modular homes, the region’s largest single MiC award.

- November 2025: King Salman Park Foundation, Ajdan Real Estate, and SEDCO Capital launched a SAR 3.8 billion (USD 1 billion) mixed-use fund for a 600-unit urban precinct inside the park.

Saudi Arabia Residential Construction Market Report Scope

| Apartments / Condominiums |

| Villas / Landed Houses |

| New Construction |

| Renovation |

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc.) |

| Public |

| Private |

| Riyadh |

| Jeddah |

| DMA (Dammam Metropolitan Area) |

| Rest of Saudi Arabia |

| By Type | Apartments / Condominiums |

| Villas / Landed Houses | |

| By Construction Type | New Construction |

| Renovation | |

| By Construction Method | Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc.) | |

| By Investment Source | Public |

| Private | |

| By City | Riyadh |

| Jeddah | |

| DMA (Dammam Metropolitan Area) | |

| Rest of Saudi Arabia |

Key Questions Answered in the Report

How large is the Saudi Arabia residential construction market today?

The sector reached USD 50.34 billion in 2025 and is forecast to grow to USD 71.75 billion by 2031.

What CAGR is expected for Saudi housing construction up to 2031?

The market is projected to register a 6.09% CAGR during 2026-2031.

Which city accounts for the biggest share of new housing projects?

Riyadh led with 41.3% of the 2025 value, driven by mega-communities like ROSHN’s Sedra.

Why is modular construction gaining ground in Saudi projects?

Prefabrication cuts delivery time by up to 45% and meets strict 50-year durability and net-zero targets, as shown in NEOM's 12,000-unit contract.

How are mortgages influencing residential demand?

REDF subsidies and higher loan-to-value ratios have lowered borrower costs, encouraging developers to launch and pre-sell more units.

What is the main risk facing developers over the next two years?

Rising input costs and limited contractor capacity could squeeze margins and extend build schedules unless mitigated by bulk procurement or modular tactics.

Page last updated on: