North America Formwork Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.59 Billion |

| Market Size (2026) | USD 1.64 Billion |

| Market Size (2031) | USD 2.02 Billion |

| Growth Rate (2026 - 2031) | 4.26% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Formwork Market Analysis by Mordor Intelligence

The North America Formwork Market size was valued at USD 1.59 billion in 2025 and is estimated to grow from USD 1.64 billion in 2026 to reach USD 2.02 billion by 2031, at a CAGR of 4.26% during the forecast period (2026-2031).

The North America formwork market is supported by a multi-year infrastructure pipeline because the Infrastructure Investment and Jobs Act committed USD 275 billion in highway and bridge formula funds across more than 120,860 projects as of April 2026. The regional demand base is also strengthened by the Federal Transit Administration’s FY2026 public transportation funding of USD 20.6 billion, which supports fixed-guideway capital projects, state-of-good-repair work, and bus facility expansion across urban networks. This overlap among bridge, transit, and public works execution keeps procurement activity active across multiple project categories simultaneously, which benefits suppliers with broad rental fleets, engineering support, and national depot coverage. Labor shortages remain a structural issue in the North America formwork market because 92% of contractors reported difficulty filling open positions, which raises the appeal of engineered systems that reduce field dependence on skilled carpentry labor. At the same time, raw material volatility and tariff-related cost uncertainty continue to slow capacity expansion decisions, which keeps the opportunity centered on reusable, engineered, and service-backed systems rather than low-value commodity panels.

Key Report Takeaways

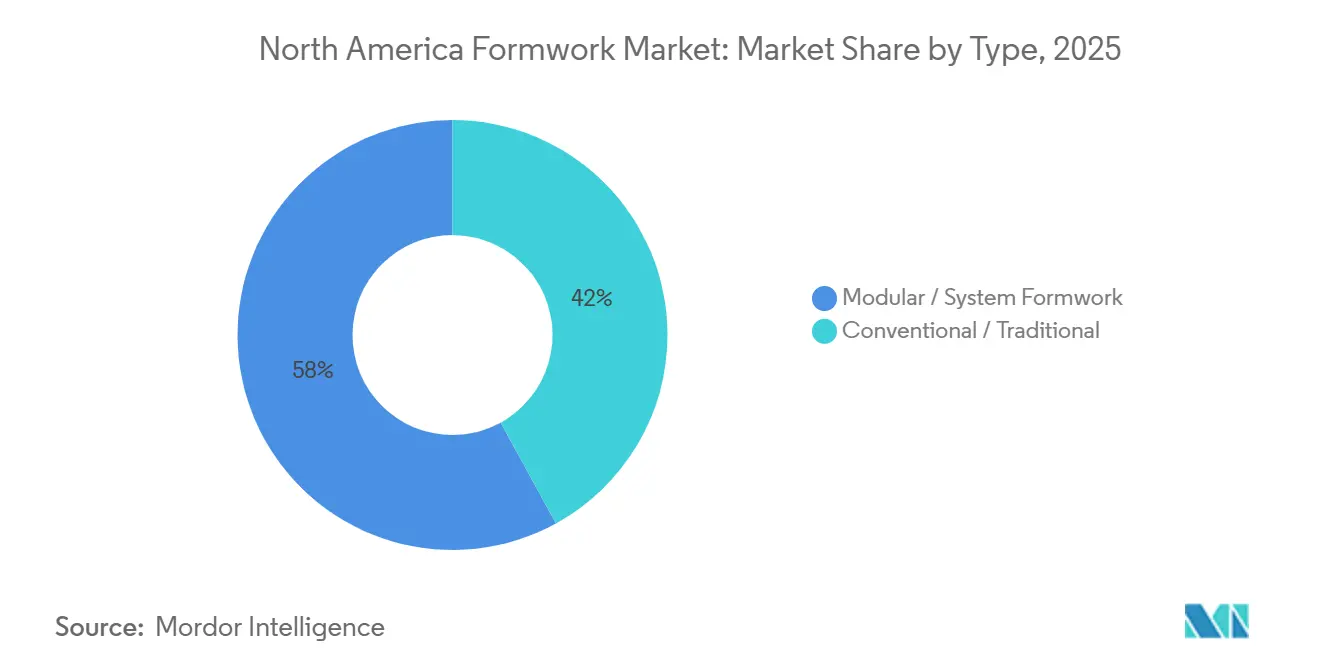

- By type, modular / system formwork held 58% of the North America formwork market size in 2025, and it is also the fastest-growing type at a 5.40% CAGR through 2031.

- By configuration, static formwork led with 46% of the North America formwork market share in 2025, while climbing formwork is projected to expand at a 4.56% CAGR through 2031.

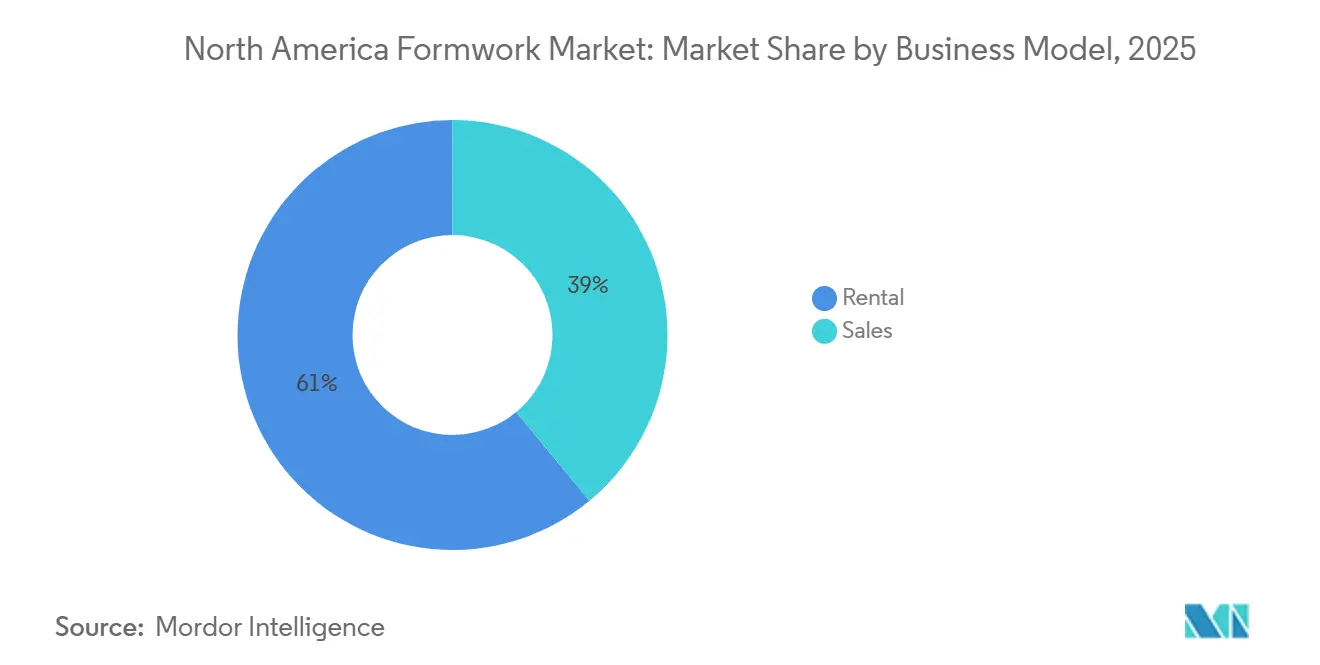

- By business model, rental held a 61% of the North America formwork market share in 2025 and is also the fastest-growing model, with a 5.20% CAGR through 2031.

- By sector, infrastructure accounted for a 39% share in 2025 and is also the fastest-growing sector, with a 5.23% CAGR through 2031.

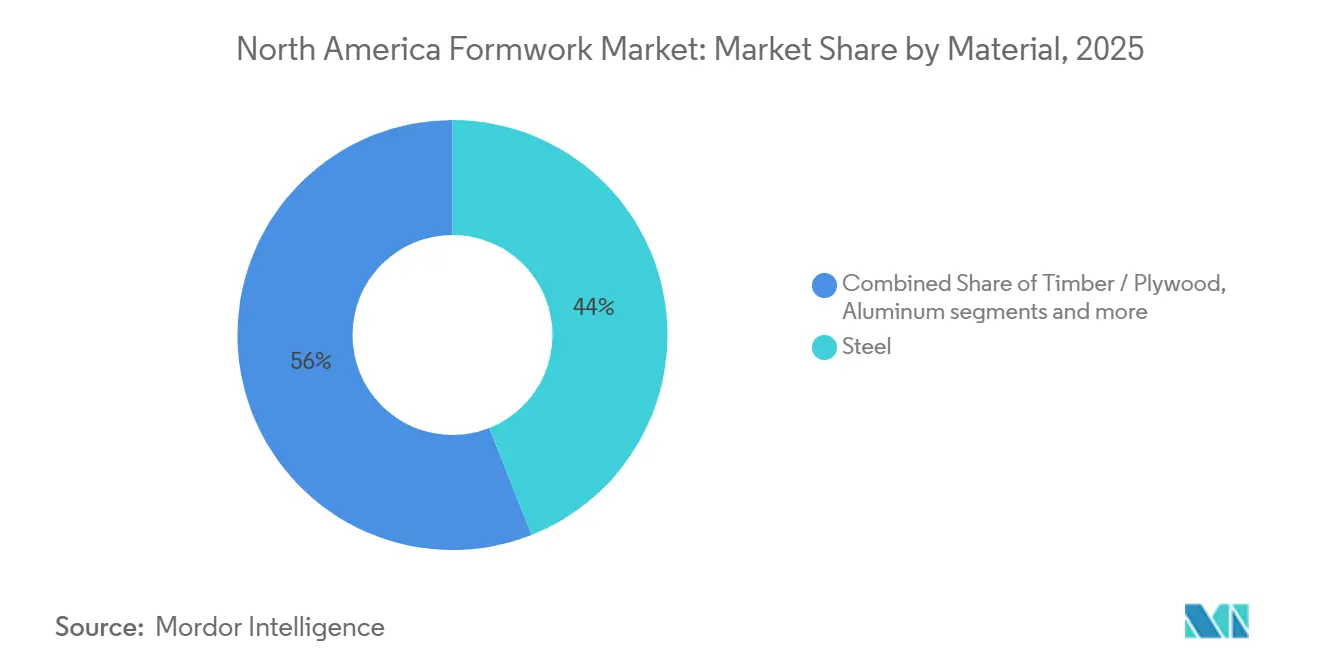

- By material, steel held 44% of the North America formwork market share in 2025, while aluminum is projected to grow at a 5.60% CAGR through 2031.

- By geography, the United States held 85% share in 2025, while Mexico is forecast to record the highest country CAGR at 5.10% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Formwork Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Infrastructure Spend on Bridges, Transit, and Public Works | +1.2% | United States, Canada, with spill-over to Mexico | Long term (≥ 4 years) |

| Shift Toward Rental and Reuse Models to Reduce Project CAPEX | +0.8% | United States and Canada core, emerging in Mexico | Medium term (2-4 years) |

| Adoption of Engineered and Modular Systems for Faster Cycle Times | +0.7% | United States core, accelerating in Mexico | Medium term (2-4 years) |

| Demand for Safer Forming Solutions in High-Rise and Deep Foundation Work | +0.4% | United States, especially major metro corridors | Medium term (2-4 years) |

| Digital Takeoff, BIM, and Prefabrication Integration | +0.3% | United States and Canada, especially tech-forward markets | Short term (≤ 2 years) |

| Reuse Economics Under Carbon and Waste Reporting Pressure | +0.2% | United States and Canada, especially corporate-mandated projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Infrastructure Spend on Bridges, Transit, and Public Works

Federal infrastructure spending remains the most direct demand driver for the North America formwork market over the forecast period[1]American Road & Transportation Builders Association, “Highway Dashboard – IIJA,” ARTBA, artba.org . Through April 2026, states had committed USD 275 billion in the Infrastructure Investment and Jobs Act (IIJA) highway and bridge formula funds across more than 120,860 projects, including 19,000 bridge upgrades. The same cycle is reinforced by the Federal Transit Administration’s FY2026 apportionment of USD 20.6 billion for transit capital work, state-of-good-repair projects, and bus facility upgrades. The Federal Highway Administration also states that every USD 1 billion in highway and bridge investment supports around 13,000 jobs across the United States economy, which keeps contractor activity and project mobilization broad-based. As these bridge, roadway, and transit projects move deeper into execution during 2026 and 2027, the North America formwork market continues to benefit from stronger rental utilization and a firmer replacement cycle for engineered systems.

Shift Toward Rental and Reuse Models to Reduce Project CAPEX

Rental has become the preferred access model across a large part of the North America formwork market because it reduces upfront ownership risk and aligns better with uneven project schedules. This shift is strongest among mid-sized contractors that manage several projects at once and prefer to keep capital free for labor, materials, and working capital needs. The model also gives contractors access to newer system designs, engineering support, and faster mobilization without the need to build internal maintenance capacity. As rental fleet ownership becomes more concentrated among large operators, pricing power and service differentiation increasingly move toward players with deeper depot networks and stronger field support. That is why recent moves by suppliers such as MEVA, ULMA, PERI, and Doka point to a service-led playbook in the North America formwork market, where rental depth and engineering support matter as much as the hardware itself.

Adoption of Engineered and Modular Systems for Faster Cycle Times

Engineered and modular systems are now central to the productivity case in the North America formwork market because contractors are under pressure to shorten cycle times and reduce field dependence on experienced carpentry crews. PERI USA’s January 2025 launch of SKYFLEX and LEVO demonstrated how suppliers are tailoring systems to local site needs through lightweight panels, early-strike features, and assembly methods that reduce handling complexity. This matters because 57% of contractors reported that available candidates lacked the required skills or licenses, making simpler, more standardized systems easier to deploy on active jobs. The Occupational Safety and Health Administration (OSHA) concrete and masonry construction standards also favor documented, engineered systems because they include defined load tables and established safety procedures. The result is that the North America formwork market is moving away from site-built timber methods and toward systems that combine speed, repeatability, and compliance support.

Demand for Safer Forming Solutions in High-Rise and Deep Foundation Work

High-rise cores and deep foundation applications are pushing the North America formwork market toward more advanced climbing and safety-focused systems. Doka’s March 2026 launch of the Shear Wall Climber SCP with FormDrive in the United States market reflects this shift through its crane-independent setup, 20-foot forming height, and 90-kip hydraulic lifting capacity. These features help address a recurring site constraint because tower crane time is often shared across several trades on dense urban projects. EFCO’s POWER TOWER PT-100 example also showed the value of more efficient climbing solutions by supporting 4-day floor cycles with fewer workers and lower equipment demand. In these applications, procurement decisions in the North America formwork market are moving beyond upfront price and toward technical assurance, controlled lifting, and better monitoring during concrete placement.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost of Engineered Formwork Systems | -0.5% | United States and Canada core, moderate impact in Mexico | Medium term (2-4 years) |

| Skilled Labor Shortages for Safe Assembly and On-Site Engineering | -0.4% | National in the United States, concentrated in Texas, Georgia, and California | Medium term (2-4 years) |

| Project Delays From Permitting, Weather, and Seasonal Construction Windows | -0.3% | Canada, northern U.S. states, and markets facing permitting backlogs | Short term (≤ 2 years) |

| Inventory Fragmentation Across Rental Fleets and Job Sites | -0.2% | United States and Canada, especially among multi-site contractors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Engineered Formwork Systems

The higher initial cost of engineered systems remains a clear brake on adoption in the North America formwork market. The cost case improves over many reuse cycles, but smaller contractors and single-project users often lack the capital visibility to justify an outright purchase. This is one reason rental remains strong even when contractors prefer the long-run economics of ownership. Tariff-related pressures also add cost risk, as 41% of construction firms raised prices in response to tariffs and 39% accelerated purchases ahead of expected increases. Engineering design, supervision requirements, and shoring compliance add another cost layer to complex jobs, concentrating ownership among larger fleets and well-capitalized operators.

Skilled Labor Shortages for Safe Assembly and On-Site Engineering

Labor scarcity remains one of the most persistent restraints on the North America formwork market because it affects both project speed and safe assembly conditions. The AGC survey showed that 92% of firms had difficulty filling open positions, 88% had openings for craft workers, and 75% saw inexperienced skilled labor as a direct safety concern. The Home Builders Institute estimated that skilled labor shortages created an annual economic impact of USD 10.8 billion in the residential sector alone, including USD 2.7 billion in carrying costs and USD 8.1 billion in lost output. In formwork operations, this matters because complex climbing and shoring setups can fail if crews lack enough site engineering supervision during concrete loading. The North America formwork market, therefore, sees a dual effect where labor shortages delay work in the short term but also strengthen the long-term case for safer, more standardized, and easier-to-assemble systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Modular Dominance Accelerates as Legacy Timber Erodes

Modular / system formwork held 58% of the North America formwork market in 2025 and is projected to grow at a 5.4% CAGR through 2031. This made it both the largest and fastest-growing type, which shows that the North America formwork market is moving through a structural shift rather than a short-cycle preference change. The appeal of modular systems lies in repeatability, shorter setup time, and greater control over labor-intensive activities on active jobs. These systems also fit well with the demand for documented safety performance and more standardized execution on public and institutional work. PERI USA’s SKYFLEX and LEVO launch in January 2025 reflected this direction through lightweight handling, imperial sizing, and assembly methods designed for the United States jobsite conditions[2]PERI USA, “PERI USA to Launch SKYFLEX, LEVO at World of Concrete 2025,” PERI USA, peri-usa.com.

Conventional / traditional formwork still serves custom foundations, low-repetition work, and smaller residential pours where contractors rely on familiar timber-based practices. In those settings, the setup cost of modular equipment can still outweigh the productivity gain from system adoption. The segment, therefore, remains relevant where repetition is low and design variation is high. Even so, the North America formwork market is steadily shifting away from carpenter-built methods as trained crews, engineering desks, and Building Information Modeling (BIM)-ready component libraries make modular adoption easier across more project types. Within this transition, modular and system formwork continues to anchor the North America formwork market size at the type level because it already leads on both scale and future growth.

By Configuration: Climbing Systems Emerge as the High-Value Growth Vector

Static formwork held 46% of the North America formwork market in 2025, which kept it in the lead across slabs, walls, columns, and foundation work. It remains the default configuration because a large share of commercial, residential, and civil pours still do not require highly specialized movement systems. In simple geometric conditions, static systems offer familiarity, broad availability, and easier crew deployment. This keeps them central to the day-to-day execution base of the North America formwork market. At the same time, climbing formwork is forecast to grow at a 4.56% CAGR through 2031, which makes it the fastest-growing configuration.

The growth case for climbing systems comes from high-rise cores, dense urban sites, and jobs where crane independence can protect schedules. Doka’s 2026 United States launch of the Shear Wall Climber SCP with FormDrive showed how this product class is evolving through hydraulic lifting, remote monitoring, and faster repositioning. Slipform remains essential in silos, tanks, and utility structures where continuous casting is required. Tunnel formwork also plays a practical role, as transit and utility projects continue to drive demand for efficient, repetitive lining work. In this segment, the North America formwork market share is still anchored by static systems, while the growth premium is shifting toward climbing technology in higher-value urban applications.

By Business Model: Rental Economics Consolidate Around Fleet Scale

Rental held 61% of the North America formwork market in 2025 and is projected to expand at a 5.20% CAGR through 2031. That combination made rental both the largest and fastest-growing business model in the North America formwork market. The model works because it reduces ownership risk, shortens the time needed to mobilize equipment, and transfers maintenance responsibility to fleet operators. It also helps contractors respond to uneven project starts without carrying idle stock between pours. For mid-sized contractors, especially, rental provides access to advanced systems and engineering support that would be harder to fund internally.

The sales channel still represented 39% of the 2025 market and remains relevant for large Engineering, Procurement, and Construction (EPC) contractors and self-performing concrete specialists with high annual reuse rates. These buyers can justify ownership when they run repeated project cycles or use proprietary forms over long programs. Hünnebeck by BrandSafway’s August 2025 agreement with Alkus AG showed how component specialization is becoming deeper across both rental and sales channels. That deeper supplier integration tends to raise switching costs and strengthen customer retention over time. For this reason, the North America formwork industry is not moving away from sales. Still, the strongest commercial momentum in the North America formwork market remains with large, service-backed rental fleets.

By Sector: Infrastructure Pipeline Sustains Demand Across the Market Cycle

Infrastructure accounted for 39% of the North America formwork market in 2025 and is projected to grow at a 5.23% CAGR through 2031. This made infrastructure both the largest sector and the fastest-growing one in the North America formwork market. The demand is directly linked to bridge, roadway, transit, retaining wall, and tunnel work funded through federal programs. The Federal Highway Administration’s Bridge Formula Program and the Bridge Investment Program continue to support rehabilitation and replacement activity across a large installed base of aging structures. This creates a steady need not only for standard systems but also for custom shoring, falsework, and project-specific engineering support.

Residential construction remains important, especially where repetitive concrete-frame housing and multifamily development favor the use of reusable systems. Commercial demand remains strong in institutional buildings and large concrete-intensive structures, though project timing varies by subcategory. Industrial and logistics activity supports the North America formwork market through reshoring, tilt-wall construction, and cast-in-place structures tied to manufacturing and warehouse expansion. The practical difference is that infrastructure work usually offers longer visibility and more specialized engineering needs than short-cycle building projects. That is why infrastructure continues to hold the largest share of the North America formwork market size at the sector level while also setting the pace for future expansion.

By Material: Steel’s Volume Position Tested by Aluminum’s Weight-Efficiency Gains

Steel held 44% of the North America formwork market share in 2025, which kept it as the largest material segment in the region. Steel remains strong because it offers durability, high load capacity, and broad suitability for heavy civil work such as bridge decks, tunnel linings, retaining walls, and large gang wall panels. Contractors also know how to maintain and adapt steel systems on demanding jobs, which supports continued use in infrastructure-led applications. This gives steel a durable installed position across the North America formwork market. However, aluminum is forecast to grow at a 5.60% CAGR through 2031, which makes it the fastest-growing material category.

The growth of aluminum is linked to lower panel weight, easier handling, and greater suitability for repetitive residential and mid-rise building layouts. These features become more valuable when contractors are trying to stretch smaller crews across multiple pours and reduce physical strain on site teams. Timber and plywood still retain a role in custom work and residential foundations, but that addressable base is narrowing as reusable systems move further into smaller projects. Plastic and fiberglass remain niche, yet peer-reviewed sustainability work has strengthened their case on projects where circularity and lower waste matter. In material terms, the North America formwork market keeps its volume base in steel while its growth edge shifts toward lighter reusable systems.

Geography Analysis

The United States held 85% of the North America formwork market in 2025, which made it the clear regional anchor for demand, installed fleet depth, and engineering capability. The country’s lead reflects the size of its active construction base, its broader network of engineered formwork suppliers, and stronger procurement visibility from federal infrastructure funding. In 2026, IIJA-funded bridge and roadway work is at or near peak execution, which keeps demand active across highway, public works, and transit-linked civil construction[3]American Road & Transportation Builders Association, “Highway Dashboard – IIJA,” ARTBA, artba.org. High-rise activity in major coastal and Sun Belt metros also adds a separate demand layer for climbing systems, advanced slipform, and engineering-intensive solutions. This concentration keeps the United States at the center of the North America formwork market size and gives suppliers a large installed base from which to expand service models.

Canada remains a steady contributor to the North America formwork market through institutional, infrastructure, and energy-related projects. Its demand base is smaller than that of the United States, but it still supports the stable use of engineered systems that require certified load documentation and strong safety compliance. Energy infrastructure in Western Canada also creates demand for larger-format slipform and climbing configurations that differ from standard commercial building patterns. Multi-year public investment plans improve visibility for bridge and transit-related work, helping suppliers plan inventory and engineering support with longer lead times.

Mexico is projected to grow at a 5.10% CAGR through 2031, which makes it the fastest-growing country segment in the North America formwork market. The country’s demand profile stands out because it is more heavily weighted toward repetitive residential and social housing, where lighter, reusable systems can be more attractive than heavy-gauge steel panels. That structure gives European suppliers with experience in repetitive residential work a practical advantage as the market expands. It also means product mix in Mexico does not perfectly mirror the United States pattern, even though regional suppliers serve all 3 countries. Across the region, the North America formwork market combines the United States scale, Canadian stability, and Mexican growth, which creates a diversified but still infrastructure-led demand base.

Competitive Landscape

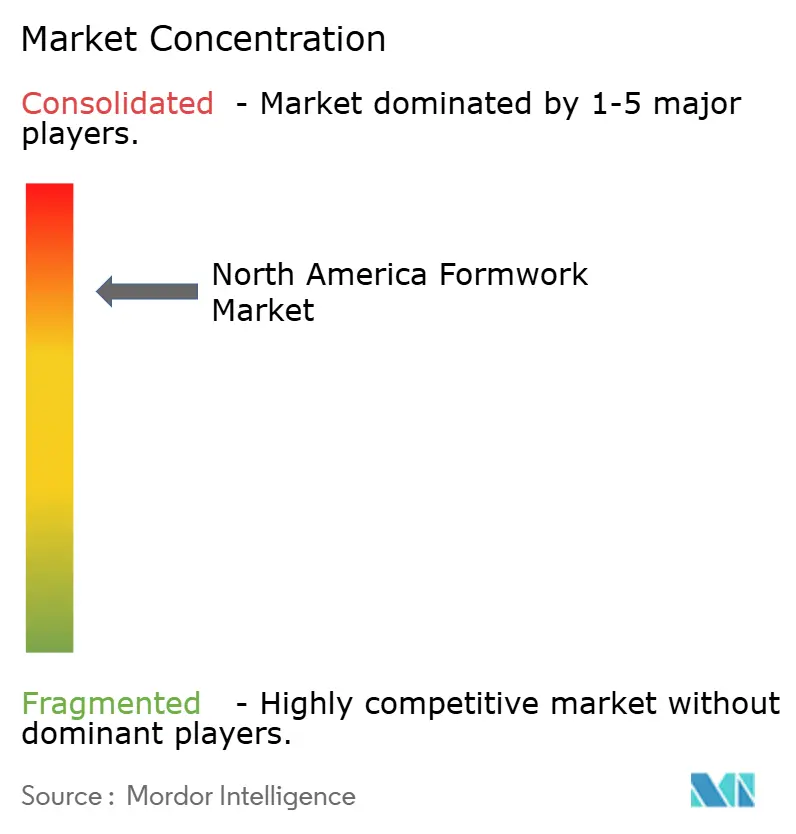

The North America formwork market is consolidated, with PERI Formwork Systems, Doka USA, BrandSafway (including Aluma Systems, Hünnebeck, and SGB), and EFCO Corp. accounting for a significant share of the market. Their leadership is built on extensive rental fleets, established distribution networks, engineering expertise, and integrated project support, making it difficult for smaller suppliers to compete on large and technically complex projects. As contractors increasingly prefer end-to-end solutions combining equipment, design, and field services, established providers continue to strengthen their market positions.

The leading companies are reinforcing their competitive advantage through product innovation and value-added services. PERI USA launched the SKYFLEX and LEVO systems in January 2025 to improve productivity and simplify manual handling, while Doka introduced the Shear Wall Climber SCP with FormDrive and the Xlife plastic recycling program in March 2026, strengthening its position in high-rise construction and sustainable formwork solutions. These developments demonstrate that innovation and technical capability remain key competitive differentiators.

BrandSafway continues to leverage its extensive operating network and integrated access solutions to serve infrastructure, industrial, and commercial projects across North America. At the same time, EFCO Corp. strengthens customer relationships through its manufacturing capabilities and contractor training programs. As a result, competition in the North America formwork market remains concentrated among a limited number of established providers that compete through scale, engineering expertise, service quality, and long-term customer relationships rather than price alone.

North America Formwork Industry Leaders

PERI Formwork Systems, Inc.

Doka USA Ltd.

BrandSafway

EFCO Corp.

ULMA Construction

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Doka launched the Shear Wall Climber SCP with FormDrive at CONEXPO in Las Vegas, extending its United States climbing formwork portfolio with a crane-independent system supporting 20-foot forming heights and 90-kip hydraulic lifting capacity. The system integrates real-time monitoring and remote troubleshooting, targeting dense urban high-rise projects in North America.

- March 2026: BrandSafway exhibited its full forming and shoring product portfolio at CONEXPO-CON/AGG, covering infrastructure, industrial, and commercial markets. With 340 locations across 25 countries and approximately 40,000 employees, the showcase highlighted the company's breadth in the North American market ahead of a critical execution year.

- August 2025: Hünnebeck by BrandSafway and Alkus AG deepened their collaboration, signing an agreement that expands Alkus' solid plastic panel supply to additional Hünnebeck and Aluma Systems formwork product lines, including the RONDA circular and PAX column formwork systems. The deal extends a partnership in place since 2013 and adds new product lines to the scope.

North America Formwork Market Report Scope

The North America Formwork Market is Segmented by Type (Conventional / Traditional and Modular / System Formwork), Configuration (Static, Climbing, Slipform, and Tunnel), Business Model (Sales and Rental), Sector (Residential, Commercial, Industrial & Logistics, and Infrastructure), Material (Timber / Plywood, and More), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| Conventional and Traditional |

| Modular and System Formwork |

| Static |

| Climbing |

| Slipform |

| Tunnel |

| Sales |

| Rental |

| Residential |

| Commercial |

| Industrial and Logistics |

| Infrastructure |

| Timber / Plywood |

| Steel |

| Aluminum |

| Plastic / Fibreglass |

| Others |

| United States |

| Canada |

| Mexico |

| By Type | Conventional and Traditional |

| Modular and System Formwork | |

| By Configuration | Static |

| Climbing | |

| Slipform | |

| Tunnel | |

| By Business Model | Sales |

| Rental | |

| By Sector | Residential |

| Commercial | |

| Industrial and Logistics | |

| Infrastructure | |

| By Material | Timber / Plywood |

| Steel | |

| Aluminum | |

| Plastic / Fibreglass | |

| Others | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the current outlook for North America formwork demand through 2031?

The market is valued at USD 1.64 billion in 2026 and is forecast to reach USD 2.02 billion by 2031 at a 4.26% CAGR. Growth is supported by infrastructure, transit, and bridge execution across the region.

Which product type leads regional demand?

Modular / system formwork led with 58% share in 2025 and is also the fastest-growing type at a 5.40% CAGR through 2031.

Why is rental so important in this space?

Rental held 61% share in 2025 and remains the fastest-growing business model at a 5.20% CAGR because contractors want flexible fleet access, less ownership risk, and stronger engineering support.

Which end-use sector creates the strongest opportunity?

Infrastructure is the largest and fastest-growing sector, with 39% share in 2025 and a 5.23% CAGR through 2031, supported by federal bridge and transit spending.

Which country drives most regional revenue?

The United States held 85% of regional share in 2025 because of its scale, active federal infrastructure pipeline, and mature engineered formwork ecosystem.

Page last updated on: