Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

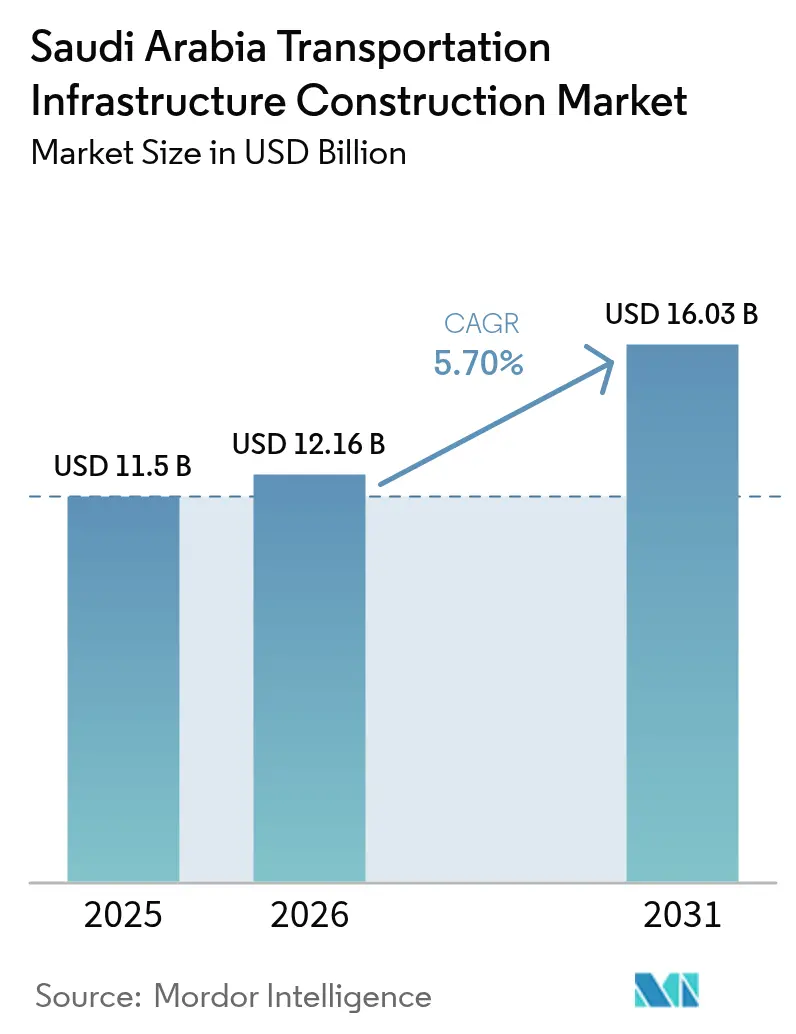

| Base Year Market Size (2025) | USD 11.5 Billion |

| Market Size (2026) | USD 12.16 Billion |

| Market Size (2031) | USD 16.03 Billion |

| Growth Rate (2026 - 2031) | 5.70% CAGR |

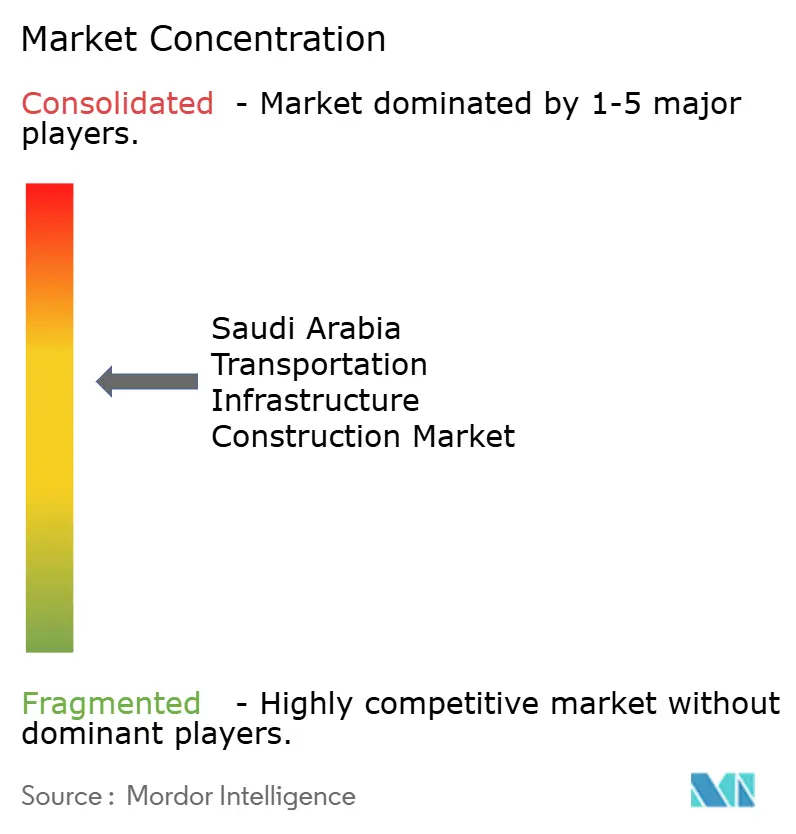

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Transportation Infrastructure Construction Market Analysis by Mordor Intelligence

Saudi Arabia transportation infrastructure construction market size in 2026 is estimated at USD 12.16 billion, growing from 2025 value of USD 11.5 billion with 2031 projections showing USD 16.03 billion, growing at 5.7% CAGR over 2026-2031. Capital deployed through the Public Investment Fund, Vision 2030-linked giga-projects, and a maturing public-private partnership framework stand out as the principal expansion catalysts. Road upgrades, metro build-outs, and port modernizations keep commissioning activity high, while the King Salman International Airport project underpins aviation infrastructure growth. Private capital is increasingly visible, aided by clearer risk-allocation rules and bankable project pipelines. The market also benefits from an ecosystem that rewards digital engineering, modular building, and green mobility solutions, helping contractors maintain cost discipline despite escalations in steel, cement, and imported equipment.

Key Report Takeaways

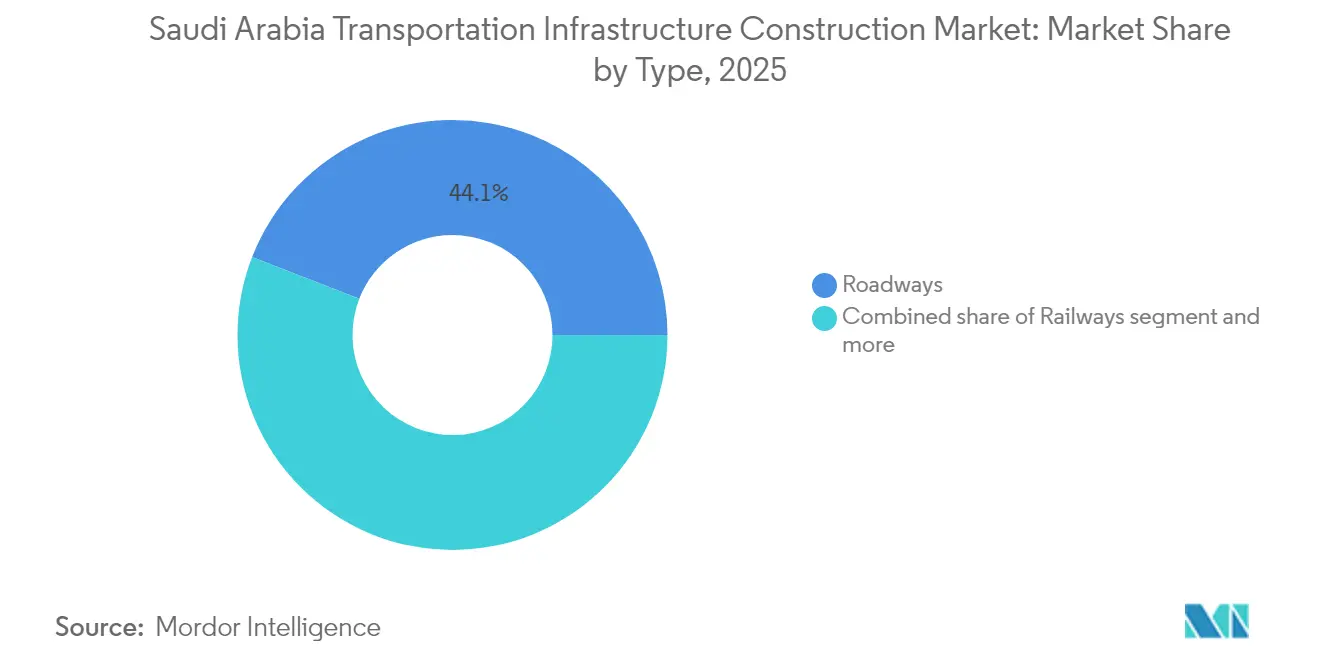

- By type, roadways held a 44.10% revenue share of the Saudi Arabia transportation infrastructure construction market in 2025. The Saudi Arabia transportation infrastructure construction market for railways is poised for the fastest 6.28% CAGR between 2026-2031.

- By construction type, new construction accounted for 78.25% of the Saudi Arabia transportation infrastructure construction market share in 2025. The Saudi Arabia transportation infrastructure construction market for renovation is projected to expand at a 6.05% CAGR between 2026-2031.

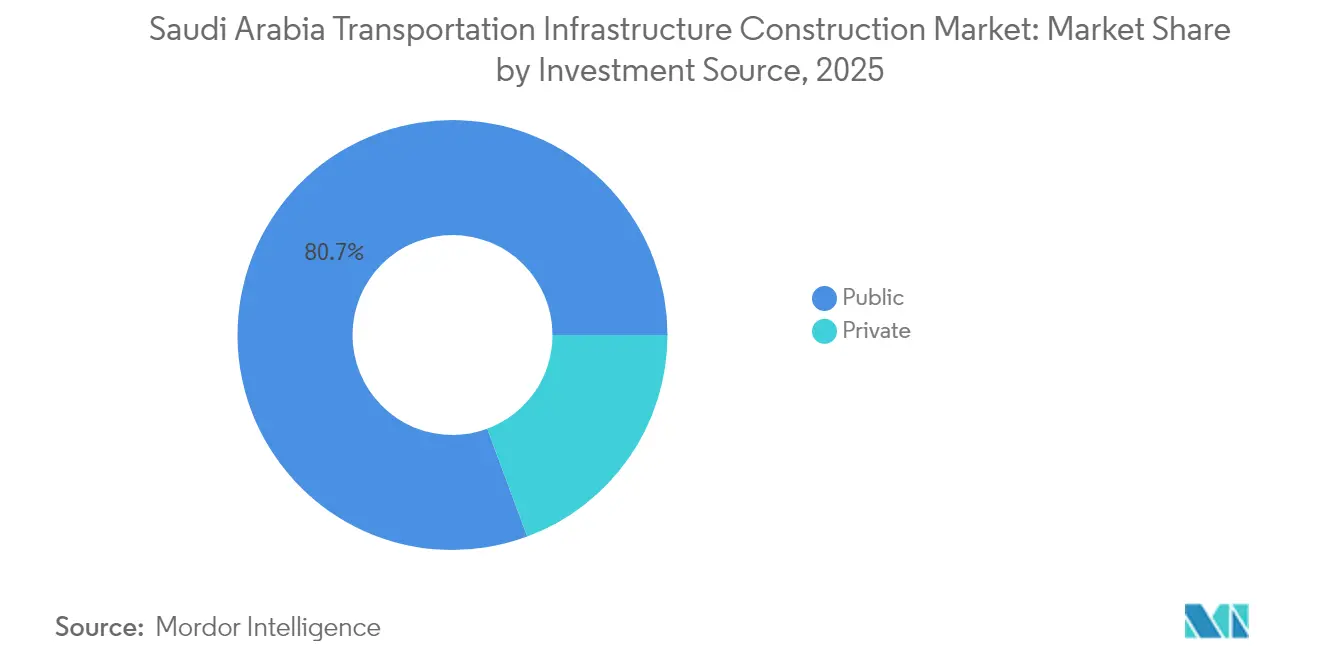

- By investment source, the public segment controlled 80.65% of the Saudi Arabia transportation infrastructure construction market in 2025. The Saudi Arabia transportation infrastructure construction market for private funding records the highest 6.52% CAGR between 2026-2031.

- By geography, Riyadh contributed 29.55% of the Saudi Arabia transportation infrastructure construction market total activity in 2025. The Saudi Arabia transportation infrastructure construction market for the Dammam Metropolitan Area is forecast to grow at 6.68% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Transportation Infrastructure Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030-linked mega projects continue to drive large-scale transport infrastructure needs | +1.8% | National, with concentration in NEOM, Riyadh, Red Sea regions | Long term (≥ 4 years) |

| Ongoing metro and high-speed rail construction is enhancing urban and intercity connectivity | +1.2% | Riyadh, Jeddah, Makkah corridor, future extensions to other cities | Medium term (2-4 years) |

| Expansion of port infrastructure is supporting national logistics and trade ambitions | +0.9% | Red Sea coast, Arabian Gulf ports, particularly Jeddah and Dammam | Medium term (2-4 years) |

| Development of integrated mobility hubs is strengthening airport, rail, and road linkages | +0.7% | Major urban centers: Riyadh, Jeddah, DMA | Medium term (2-4 years) |

| Strong PPP engagement and foreign investment are enabling faster project execution | +0.6% | National, with emphasis on high-value infrastructure projects | Long term (≥ 4 years) |

| Strategic focus on green and smart mobility is encouraging sustainable transport initiatives | +0.5% | Urban centers and new city developments like NEOM | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Mega Projects Anchor Demand

Vision 2030’s giga-projects lock in sustained order books for the Saudi Arabia transportation infrastructure construction market. NEOM’s USD 500 billion master plan entails a 170-kilometer high-speed spine, a 100% renewable port, and an on-demand urban transit grid. The Red Sea Project adds bespoke air, road, and maritime links for luxury tourism and logistics. Partnerships such as NEOM’s USD 347 million robotics joint venture with Samsung C&T show the premium placed on automated, productivity-enhancing methods. The multistage build program keeps procurement visibility strong well past 2030.

Metro and High-Speed Rail Expansion Strengthens Urban Mobility

The six-line Riyadh Metro entered service in 2024 after USD 25 billion of works, transporting up to 3.6 million daily passengers. A seventh line has been tendered, while the Makkah Metro’s USD 8 billion restart moves rail capability beyond the capital. The Haramain High-Speed Rail already links Makkah, Jeddah, and Madinah at 320 km/h. Future corridors to NEOM illustrate how railways will knit together new economic clusters, delivering the highest growth inside the Saudi Arabia transportation infrastructure construction market.

Port Infrastructure Expansion Fuels Logistics Ambitions

Jeddah Islamic Port’s USD 1.7 billion redevelopment and King Abdulaziz Port’s USD 1.86 billion expansion lift total box capacity to 15 million TEUs. The Port of NEOM, designed for full automation and renewable power, positions the Kingdom as a digital trade hub. Safer Red Sea anchorage and better hinterland highways amplify investment returns, solidifying a multimodal logistics platform[1]Saleh Al-Jasser, “National Transport and Logistics Strategy Overview,” Ministry of Transport, mot.gov.sa.

Integrated Mobility Hubs Link Transport Modes

King Salman International Airport’s USD 7.2 billion scheme embeds high-speed rail platforms and advanced ground-access roads, preparing for 185 million annual passengers by 2050[2]Young Tae Kim, “India-Middle East-Europe Economic Corridor: Implications for Gulf Connectivity,” International Transport Forum, itf-oecd.org. ACI reports King Abdulaziz International Airport processed 49.1 million passengers in 2024, underscoring demand for seamless terminal-to-city transfers[3]Stefano Baronci, “Saudi Airports Passenger Traffic 2024,” Airports Council International Asia-Pacific, aci-asiapac.aero. Such hubs elevate passenger experience while freeing capacity for cargo and e-commerce flows.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Contractor mobilization delays and labor sourcing issues are impacting project schedules | -0.8% | National, with particular challenges in remote mega-project locations | Short term (≤ 2 years) |

| Volatile oil-linked public spending is creating capital planning uncertainties | -0.6% | National, affecting all government-funded infrastructure projects | Medium term (2-4 years) |

| Lengthy regulatory approvals and land acquisition delays are affecting project starts | -0.5% | National, with complex procedures for large-scale developments | Short term (≤ 2 years) |

| Escalating input costs and logistics disruptions are pressuring budgets and delivery timelines | -0.4% | National, with particular impact from Red Sea shipping disruptions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Contractor Mobilization Challenges Trim Schedules

Long visa cycles, extreme-climate site conditions, and tight accommodation capacity slow workforce deployment. Firms juggling multiple billion-dollar jobs report overlapping peak-manpower curves that strain craft-labor availability. NEOM’s remoteness further enlarges logistics costs, nudging bids upward and stretching delivery calendars.

Oil-Price Volatility Clouds Fiscal Planning

Lower crude receipts periodically tighten budget ceilings, prompting scope deferrals such as the scaling of THE LINE’s first phase to 2.4 kilometers. Efforts to diversify revenues via taxes and PPP concessions temper this risk but do not eliminate funding cyclicality.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Railways Advance Despite Roadway Scale

Roadways continued to own the largest 44.10% share, owing to 73,000 kilometers of existing highways and fresh upgrades for freight corridors. Continuous resurfacing contracts, Hajj pilgrim routes, and smart-highway pilots keep baseline spending predictable. Railways will capture the steepest 6.28% CAGR through 2031 as urban metros, high-speed lines, and freight spurs move from design to notice-to-proceed. Elevated stations, cut-and-cover tunneling, and CBTC signaling enrich supplier opportunities. The rail build-out broadens the Saudi Arabia transportation infrastructure construction market by adding turnkey electromechanical packages and long-term O&M concessions.

Passenger experience standards adopted from the Haramain line influence rolling-stock specifications and depot design. Interoperability with ports and airports improves rolling asset utilization, lifting lifecycle returns, and sustaining contractors’ five-year backlogs. As public ridership targets rise, rolling capital allocations shield the Saudi Arabia transportation infrastructure construction market from cyclical pauses in highway procurement.

By Construction Type: Greenfield Dominates, Retrofit Gains Traction

In 2025, greenfield projects accounted for a significant share, making up 78.25% of Saudi Arabia's transportation infrastructure construction market. As part of the Vision 2030 initiative, city clusters like Qiddiya, Diriyah Gate, and the Red Sea resort zones are being developed from the ground up, necessitating new road grids, marinas, and intermodal stations. By employing design-build contracts with integrated value engineering, project timelines are shortened, and costs are kept within acceptable limits.

With legacy assets reaching capacity thresholds, renovation works are witnessing a growth rate of 6.05% CAGR. Contractors specializing in asset management are expanding their service offerings, undertaking airport terminal enlargements, bridge widenings, and ITS retrofits. Predictive maintenance, guided by digital twins of Riyadh Metro tunnels, is not only reducing life-cycle costs but also unlocking additional demand. As the post-2030 asset refresh cycles commence, the market for retrofit programs in Saudi Arabia's transportation infrastructure construction is poised for further growth.

By Investment Source: Public Wallet Still Largest, Private Money Accelerates

Public entities poured significant funding into projects, capturing 80.65% of Saudi Arabia's transportation infrastructure construction market. This sovereign backing not only reduces early-stage risks but also attracts master planners and global contractors.

Private investments are projected to grow at a 6.52% CAGR through 2031. This growth is bolstered by clarified PPP legislation, escrow arrangements, and step-in rights, all of which enhance lender confidence. Revenue streams are diversified through toll-based highway concessions, build-operate port terminals, and retail leases at stations. Additionally, road PPP pilots aiming for 5% network coverage by 2030 could further elevate the private sector's share. With strategic investors securing annuity-style cash flows, the outlook for Saudi Arabia's transportation infrastructure construction industry remains robust.

Geography Analysis

Riyadh’s 29.55% contribution underscores its role as Vision 2030’s command center. The completed six-line metro, 85 stations, and park-and-ride hubs form the region’s multimodal backbone. King Salman International Airport’s phased build catalyzes arterial highway and rail spurs, making the capital a transcontinental node. Intersection upgrades, pedestrian boulevards, and BRT corridors further sustain civil works tenders.

Jeddah remains the commercial hinge between Red Sea trade and religious tourism. King Abdulaziz International Airport’s 49.1 million passengers in 2024 highlight resilient visitor flows, while Jeddah Islamic Port’s redevelopment expands berth depth and yard automation. Dedicated Hajj access roads and service tunnels mitigate seasonal surges, keeping the Saudi Arabia transportation infrastructure construction market in the city robust.

The Dammam Metropolitan Area posts the quickest 6.68% CAGR, propelled by King Abdulaziz Port’s box-terminal enlargement and the King Salman Maritime Complex’s six-kilometer quay walls. Proximity to hydrocarbon plants feeds specialized heavy-haul road and rail demand. Integration of port, rail, and airport logistics platforms shortens delivery cycles for petrochemical exports, enhancing regional competitiveness. New interchange upgrades and ring-road extensions also reduce congestion in the growing conurbation.

Other provinces benefit from NEOM’s transformative spending. The Port of NEOM employs AI-driven crane timing, pushing the frontier of smart ports, while urban spine tunnels for THE LINE refine TBM deployment at scale. These works broaden supplier bases and funnel skills into previously underserved hinterlands, lifting nationwide standards and the overall Saudi Arabia transportation infrastructure construction market.

Competitive Landscape

Moderate fragmentation prevails, with top local and global contractors vying for multi-billion-dollar packages. Saudi Binladin Group and Almabani leverage deep government ties and local labor pools, while Bechtel, Parsons, and China Railway Construction Corporation bring mega-project governance and advanced design tools. Consortium bidding balances risk, ensures resource depth, and satisfies local content thresholds.

Digitalization, modular precast systems, and robotics become decisive factors. NEOM’s USD 347 million Samsung C&T robotics agreement aims for 80% manual-labor reduction, signaling future procurement preferences. Contractors adopting BIM level-3 standards and drone-aided progress tracking report faster payment certification cycles, promoting cash-flow stability.

Strategic moves in 2025 include Bechtel-Parsons’ airport win and DP World’s logistics park commitment, both cementing first-mover advantages in aviation and maritime verticals. Market entrants with smart-asset O&M capabilities find white space in post-handover service contracts, underlining a shift from build-only to build-operate mindsets across the Saudi Arabia transportation infrastructure construction market.

Saudi Arabia Transportation Infrastructure Construction Industry Leaders

Saudi Binladin Group

AL-AYUNI Company

Almabani

Nesma & Partners

Binyah

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Bechtel and Parsons secured the USD 7.2 billion King Salman International Airport expansion contract, targeting 120 million passengers by 2030.

- March 2025: Talaat Moustafa Group and Al Muhaidib Group formed a joint venture for the 10 million m² Banan City in Riyadh (Al Muhaidib Group).

- January 2025: King Khalid International Airport Terminal 1 expansion completed, lifting capacity to 7 million passengers annually.

- December 2024: NEOM and Samsung C&T formed a SAR 1.3 billion (USD 0.34 billion) construction-robotics joint venture to cut manual rebar work by 80%.

Saudi Arabia Transportation Infrastructure Construction Market Report Scope

Transportation infrastructure is referred to as the framework that facilitates the transportation system. Roads, railways, ports, and airports are all part of it. Daily, transportation infrastructure connects people to jobs, healthcare facilities, educational institutions, etc. It makes it easier to provide and receive goods and services worldwide. A complete background analysis of the Saudi Arabia Transportation Infrastructure Construction Market, including the assessment of the economy and contribution of sectors in the economy, a market overview, market size estimation for key segments, emerging trends in the market segments, market dynamics and geographical trends, and COVID-19 impact, is covered in the report.

The Saudi Arabia Transportation Infrastructure Construction Market is segmented by mode (roads, railways, airports, and waterways). The report offers market size and forecast values (USD) for all the above segments.

By Type

| Roadways |

| Railways |

| Airways |

| Ports and Inland Waterways |

By Construction Type

| New Construction |

| Renovation |

By Investment Source

| Public |

| Private |

By City

| Riyadh |

| Jeddah |

| DMA (Dammam metropolitan area) |

| Rest of Saudi Arabia |

| By Type | Roadways |

| Railways | |

| Airways | |

| Ports and Inland Waterways | |

| By Construction Type | New Construction |

| Renovation | |

| By Investment Source | Public |

| Private | |

| By City | Riyadh |

| Jeddah | |

| DMA (Dammam metropolitan area) | |

| Rest of Saudi Arabia |

Key Questions Answered in the Report

What is the current size of the Saudi Arabia transportation infrastructure construction market?

The market is worth USD 12.16 billion in 2026.

How fast is the Saudi Arabia transportation infrastructure construction market expected to grow?

A 5.70% CAGR is projected between 2026 and 2031, taking the value to USD 16.03 billion.

Which segment is expanding quickest within the market?

Railways post the fastest 6.28% CAGR through 2031, driven by metro extensions and high-speed corridors.

How significant is private sector participation?

Private capital funded 19.35% of 2025 spending and is growing at 6.52% CAGR as PPP pipelines mature.

Why is the Dammam Metropolitan Area a growth hotspot?

Port expansions, maritime-industrial complexes, and rising air traffic propel a 6.68% CAGR in the region.

Page last updated on: