Saudi Arabia Scaffolding Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

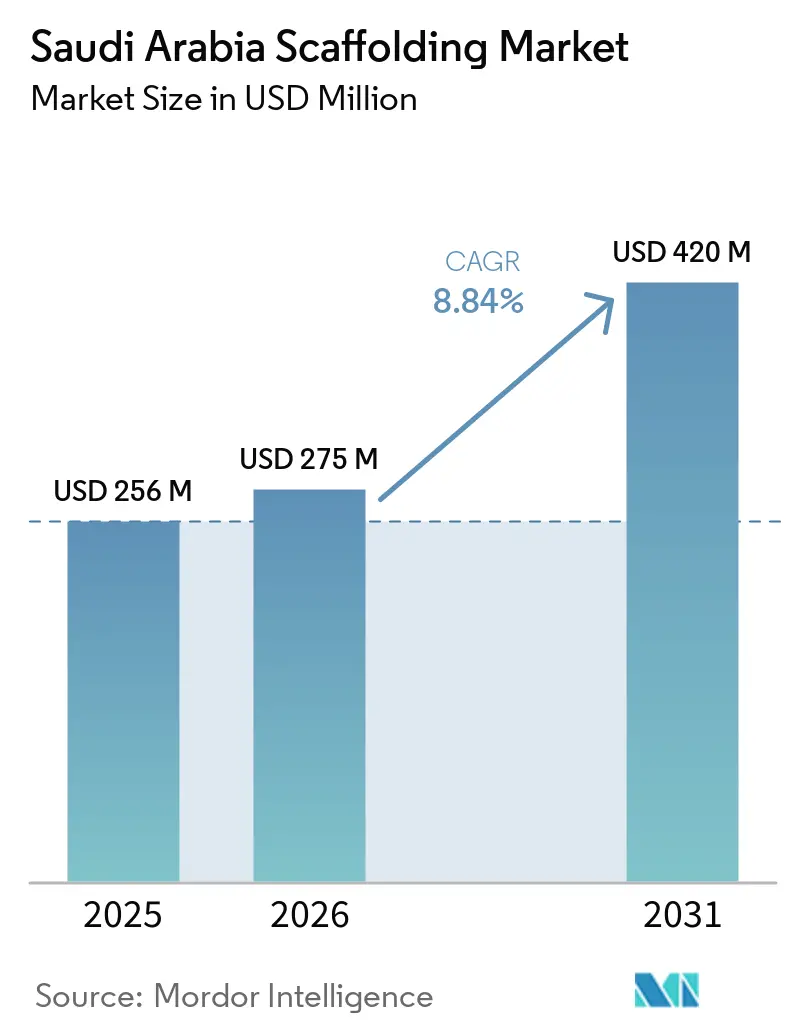

| Base Year Market Size (2025) | USD 256 Million |

| Market Size (2026) | USD 275 Million |

| Market Size (2031) | USD 420 Million |

| Growth Rate (2026 - 2031) | 8.84% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Scaffolding Market Analysis by Mordor Intelligence

The Saudi Arabia Scaffolding Market size is projected to expand from USD 256 million in 2025 and USD 275 million in 2026 to USD 420 million by 2031, registering a CAGR of 8.84% between 2026 to 2031.

The Saudi Arabia scaffolding market is being supported by demand that now extends across transport works, entertainment projects, mixed-use development, industrial expansion, and recurring oil and gas maintenance rather than a narrow set of flagship sites. Saudi Arabia’s construction sector Gross Domestic Product (GDP) grew 4% year over year in Q4 2025, indicating that activity remained broad-based across the Kingdom and provided contractors with a broader base of project work[1]DataSaudi, “Construction Sector Data,” DataSaudi, datasaudi.sa. The Saudi Arabia scaffolding market also benefits from recurring maintenance work on energy assets, where Saudi Aramco is guiding USD 50-55 billion in capital investment for 2026, after USD 52.2 billion in 2025. Demand is also moving toward modular systems, larger rental fleets, and lighter materials in project phases that need faster assembly, documented inspections, and repeated redeployment. Competition remains moderately fragmented, with Aramco-certified domestic firms and Saudi units of global suppliers competing on compliance, availability, design support, and mobilization speed.

Key Report Takeaways

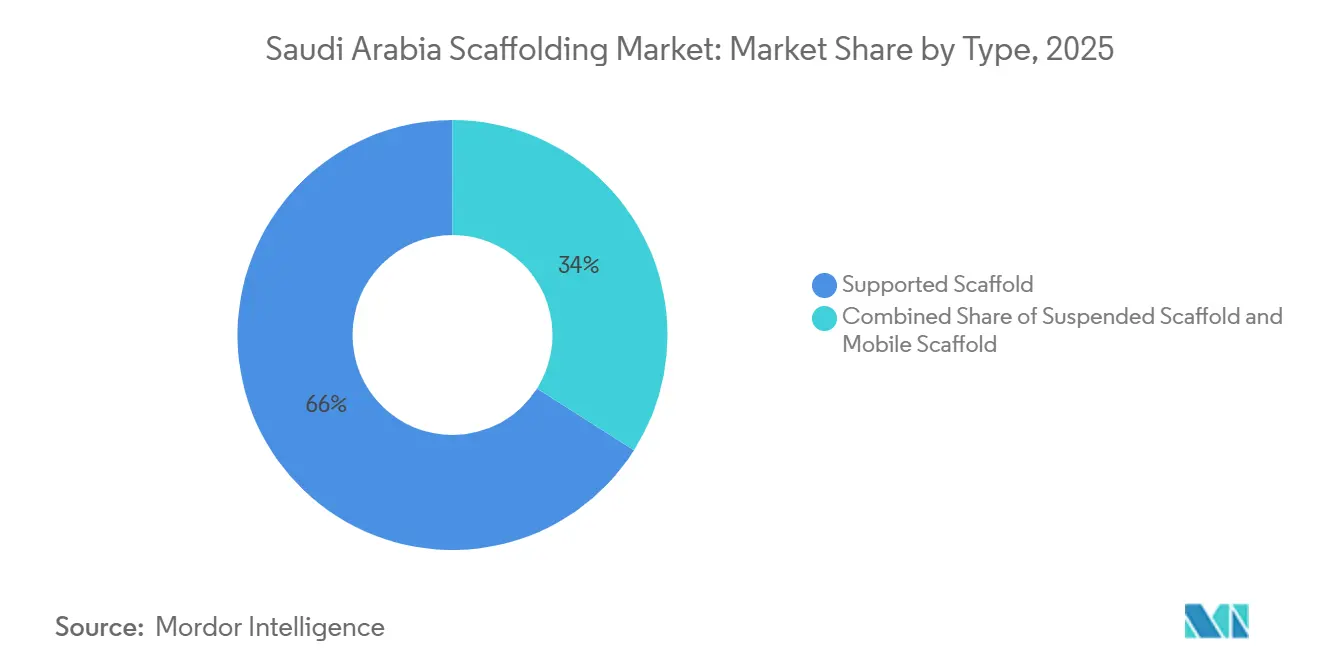

- By type, the supported scaffold is projected to lead with 66% of the Saudi Arabia Scaffolding market share in 2025, while the mobile scaffold is projected to grow fastest at 9.6% CAGR through 2031.

- By system, modular / ringlock held a 44% share in 2025 and recorded the highest forecast CAGR of 10.3% through 2031.

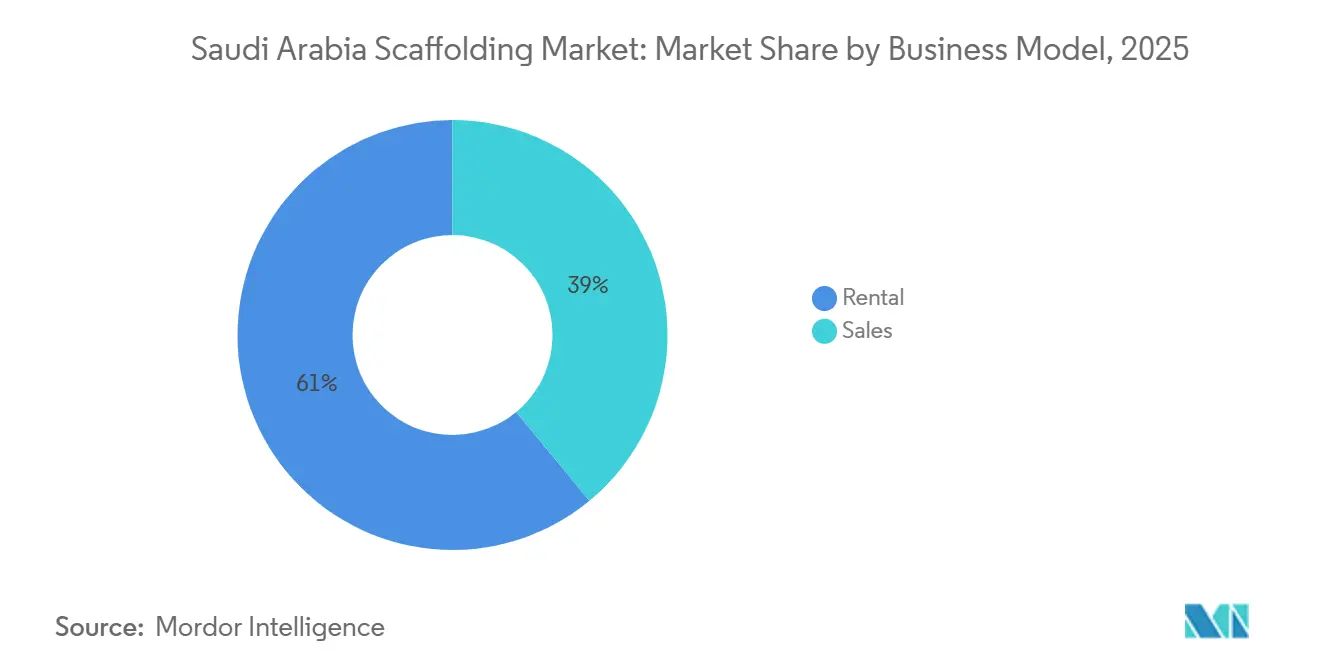

- By business model, rental held 61% share in 2025 and is advancing at 10.2% CAGR through 2031.

- By material type, steel accounted for 72% of Saudi Arabia scaffolding market share in 2025, while aluminum is forecast to expand at 10.5% CAGR through 2031.

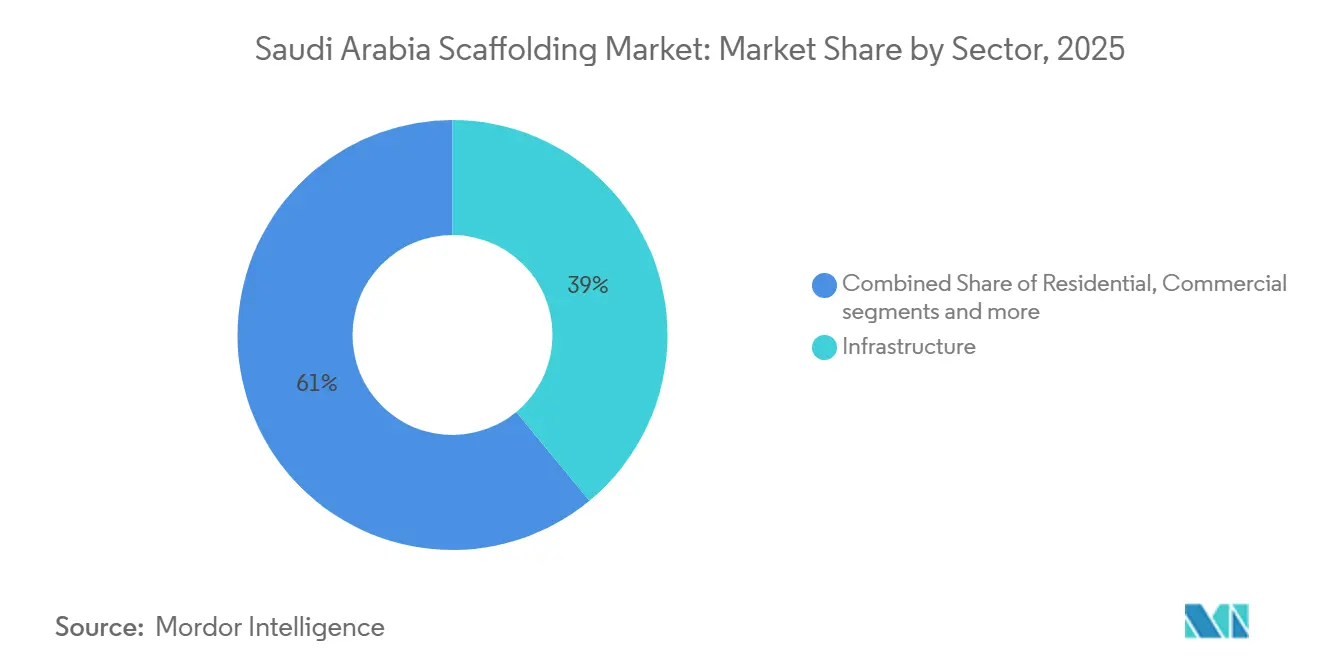

- By sector, infrastructure accounted for 39% share of the Saudi Arabia scaffolding market size in 2025, while industrial & logistics is forecast to grow at 10.6% CAGR through 2031.

- By city, Riyadh held 31% of Saudi Arabia scaffolding market share in 2025, while Eastern Province recorded the highest projected CAGR at 9.5% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Scaffolding Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 Construction Pipeline Drives Scaffolding Demand | +2.5% | Kingdom-wide, concentrated in Riyadh, the NEOM corridor, and Jeddah | Long term (≥ 4 years) |

| Oil and Gas Maintenance Activities Increase Scaffolding Utilization | +1.8% | Eastern Province, with spillover to Yanbu | Long term (≥ 4 years) |

| Growth in Industrial and Mega Projects Expands Scaffolding Requirements | +1.2% | Eastern Province, Jizan, and Yanbu industrial zones | Long term (≥ 4 years) |

| Shift Toward Modular and Reusable Systems Supports Market Growth | +1.0% | Kingdom-wide across major project types | Medium term (2-4 years) |

| Expansion of Infrastructure and Transportation Projects Boosts Scaffolding Deployment | +0.9% | Riyadh, Jeddah, and major transport corridors | Medium term (2-4 years) |

| Strong Safety Compliance Requirements Encourage Standardized Scaffolding Adoption | +0.8% | Kingdom-wide, strongest in oil and gas and heavy construction | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Construction Pipeline Drives Scaffolding Demand

The Saudi Arabia scaffolding market continues to draw strength from a construction pipeline that spans public transport, urban expansion, hospitality, and government-backed redevelopment. Construction sector GDP rose 4% year over year in Q4 2025, confirming that site activity was not limited to a few large schemes but was instead spread across the broader building base. Riyadh’s metro extension program and the wider list of national development projects under Vision 2030 keep work moving across multiple locations and asset classes. This spread lowers the risk that demand depends on a single project corridor or structure type. It also favors suppliers that can shift scaffold fleets and crews between cities as project phases change. As more projects move from structural works into finishing and operations support, the Saudi Arabia scaffolding market is likely to see more repeat deployment cycles across the same equipment base.

Oil and Gas Maintenance Activities Increase Scaffolding Utilization

The Saudi Arabia scaffolding market has a durable support layer in oil and gas maintenance, which behaves differently from one-time construction demand. Saudi Aramco reported capital investment of USD 52.2 billion in 2025 and guided USD 50-55 billion for 2026, which keeps major field and plant activity active in the Eastern Province[2]Saudi Aramco, “Fourth Quarter and Full-Year 2025 Results Press Release,” Aramco, aramco.com. KAEFER Saudi Arabia’s work on the Zuluf onshore oil facilities project showed the scale of access demand in this channel, with more than 200,000 square meters of suspended scaffolding, peak deployment of more than 1,200 tons of material, and 34 dedicated scaffold designs. Maintenance shutdowns and turnaround work also compress the timeline for erection and inspection, which raises the value of vendors that can mobilize certified crews quickly. This supports pricing for technically demanding projects even when more routine urban work remains price-sensitive. As a result, energy maintenance keeps the Saudi Arabia scaffolding market tied to a recurring service cycle rather than only new-build awards.

Growth in Industrial and Mega Projects Expands Scaffolding Requirements

The Saudi Arabia scaffolding market is seeing stronger demand as industrial expansion and large project execution continue across several parts of the Kingdom. Industrial & Logistics is projected to grow at a 10.6% CAGR through 2031, supported by Aramco field developments, downstream expansion, and industrial-city activity in Jubail and Yanbu, all of which need large volumes of access systems during construction and commissioning. Infrastructure remained the largest sector with a 39% share in 2025, indicating that transport, utility, and public works projects continue to drive a broad base of scaffold demand alongside the industrial pipeline. Riyadh and Eastern Province continue to account for a significant share of construction activity, as ongoing investments in industrial facilities, transportation infrastructure, energy projects, and urban development programs support a steady pipeline of scaffold-intensive work. The same pattern is visible in mega project sequencing, where spending is being redirected toward more executable industrial and event-linked developments such as OXAGON, Expo 2030 infrastructure, and the FIFA 2034 corridor, keeping scaffolding demand spread across multiple long-cycle worksites. This combination of new industrial assets, large infrastructure packages, and phased mega project delivery is expanding scaffold requirements across both heavy construction and later-stage maintenance-oriented work.

Shift Toward Modular and Reusable Systems Supports Market Growth

The Saudi Arabia scaffolding market is shifting toward modular, reusable systems because contractors need faster assembly, greater repeatability, and reduced handling complexity across large work sites. Modular/Ringlock already held a 44% share in 2025 and posted the highest forecast growth at a 10.3% CAGR, indicating that adoption is still expanding rather than leveling off. System-based designs can reduce the number of loose parts on site. They can improve reassembly speed after weather checks or layout changes, which is one reason this format is gaining favor in industrial and infrastructure work. PERI Saudi Arabia’s local branch network and its ability to provide engineering support, technical training, and timely equipment availability demonstrate how established suppliers are strengthening in-country capabilities to meet these system requirements. The use of standardized systems also makes it easier to tie equipment supply to documented engineering and inspection workflows. Over time, that shifts competition in the Saudi Arabia scaffolding market from simple product availability to broader service capabilities.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense Price Competition Pressures Contractor Margins | -1.2% | Kingdom-wide, most acute in Riyadh and Jeddah competitive bidding | Short term (≤ 2 years) |

| Skilled Labor and Erection Capacity Constraints Limit Project Execution Efficiency | -1.0% | Kingdom-wide, most severe in Makkah and Jubail industrial zones | Long term (≥ 4 years) |

| Dependence on Imported Materials and Components Increases Cost Exposure | -1.0% | National, elevated in Eastern Province and remote project sites | Medium term (2-4 years) |

| High Compliance and Certification Requirements Raise Operating Costs | -0.8% | Kingdom-wide, highest burden in oil and gas sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intense Price Competition Pressures Contractor Margins

The Saudi Arabia scaffolding market continues to face pricing pressure in routine construction activities, where numerous subcontractors compete for similar project scopes. Competition is particularly intense in standard tube-and-coupler applications, short-duration urban projects, and lower-complexity contracts, where procurement decisions are often driven by cost considerations rather than technical capabilities. While larger providers are generally better positioned to meet safety, compliance, and documentation requirements, they continue to compete with smaller operators that have lower operating costs. As a result, maintaining margins can be challenging outside industrial, infrastructure, and long-duration projects. This environment is encouraging suppliers to differentiate through integrated offerings that combine rental services, engineering support, inspections, and site mobilization rather than competing solely on price.

Skilled Labor and Erection Capacity Constraints Limit Project Execution Efficiency

The Saudi Arabia scaffolding market also faces labor pressure because compliant erection and inspection work cannot be scaled as easily as equipment inventory. Large industrial and transport sites need crews that can assemble, inspect, modify, and release scaffolds within tight windows and in accordance with formal site rules. When the same cities are handling transport, hospitality, mixed-use, and maintenance workloads simultaneously, trained crews can become a constraint even when materials are available. This slows turnover on some projects and can stretch mobilization time during busy construction periods. It also favors operators that already have stable supervision, training routines, and a multi-city labor base.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Infrastructure Workloads Anchor Supported Scaffolds Maintain Market Leadership

Supported scaffolds held a 66% share in 2025, keeping it well ahead of suspended and mobile formats in the Saudi Arabia scaffolding market. This lead reflected the structure of demand, since large transport works, industrial facilities, utilities, and broad horizontal construction programs rely on ground-supported access for stability and load-bearing needs. Supported systems are also easier to scale across long linear sites and multi-bay work fronts, which matters in transport corridors and large public projects. Suspended scaffold held a smaller share, but it remained important on technically demanding oil and gas jobs and on structures where vertical access needs are more specialized. KAEFER Saudi Arabia’s Zuluf deployment demonstrated how one energy project can achieve very high suspended scaffold intensity, with more than 200,000 square meters erected and supported through project-specific design.

Mobile scaffold is forecast to grow at the fastest 9.6% CAGR through 2031, aligning with the evolving project mix in the Kingdom. As major developments move from structural phases into fit-out, testing, maintenance preparation, and inspection, the need for fast-moving, frequently repositioned access is increasing. Retail, hospitality, airport, and mixed-use assets tend to create more of these shorter-cycle tasks than heavy civil work does. This part of the Saudi Arabia scaffolding industry is therefore widening, even while supported scaffold remains the largest revenue base. Vendors that can supply both heavy-supported systems and lighter mobile fleets are better positioned to follow projects through all phases rather than only during the early build stage. The same type split also reflects how buyers are weighing compliance and operating convenience. Larger projects now place more value on engineered layouts, documented inspections, and predictable assembly methods, which favor supported systems from established vendors. Mobile scaffolding still benefits from simpler deployment, but buyers increasingly want that convenience without sacrificing traceability or safety standards. This balance helps explain why leadership has stayed with supported scaffold while growth is shifting toward mobile formats. It also means the Saudi Arabia scaffolding market is not moving away from heavy systems. Still, it is adding more flexible access demand on top of a still-large structural core. Over the forecast period, the supported scaffold is likely to remain the base category, while mobile systems are expected to play a larger role in finishing and operational turnover work.

By System: Modular / Ringlock Systems Lead the Market and Continue to Gain Adoption

Modular / ringlock held a 44% share in 2025 and recorded the highest forecast growth at a 10.3% CAGR, making it the leading system in both current scale and forward momentum. That mix suggests the Saudi Arabia scaffolding market is still in the middle of a conversion toward more standardized system platforms rather than at the end of it. Contractors value these systems because they are easier to repeat across large sites, simpler to document, and better suited to planned assembly sequences. Standardized node geometry and lower loose-part dependence can also improve handling discipline on busy sites and speed up reconfiguration when the layout needs to change. PERI Saudi Arabia’s branch network and 35,000-square-meter yard also show that suppliers are building local support around system scaffolding rather than treating it as a niche line[3]PERI Saudi Arabia, “Company Overview,” PERI Saudi Arabia, peri.com.sa.

Tube-and-coupler systems remain relevant when geometry is irregular, budgets are tight, or site teams are more familiar with flexible component-based layouts. Cuplock also remains suitable for large working platforms and repetitive access patterns where a strong, well-known system is needed without moving fully to all-purpose modular platforms. H-frame continues to serve residential and light commercial work where floor heights are more standardized, and the engineering burden is lower. This part of the Saudi Arabia scaffolding industry is therefore not a simple one-system replacement story. It is a gradual shift in which standardized systems gain ground first on complex, higher-value, and better-documented projects. The system segment is also changing because equipment supply is becoming harder to separate from engineering support. Once scaffold design, inspection planning, and digital coordination are built around a system platform, switching suppliers mid-project is less practical. That improves contract stickiness for vendors with deeper inventories and stronger technical teams. Layher’s rollout of the Allround Lightweight system is one example of how suppliers are widening the appeal of standardized systems by improving handling and transport, as well as structural performance. As a result, the Saudi Arabia scaffolding market is seeing system leadership increasingly tied to service depth, site planning, and inventory reach rather than to equipment alone.

By Business Model: Rental Dominance Reinforces a Self-Strengthening Dynamic

Rental commanded a 61% share in 2025 and is also expected to grow fastest at a 10.2% CAGR through 2031, giving it a clear lead in the Saudi Arabia scaffolding market. Contractors who manage several active sites simultaneously often prefer not to lock capital into owned scaffold inventory when labor, logistics, and project guarantees also require funding. Rental also gives buyers more flexibility when project schedules shift or when equipment must be moved quickly between work fronts. For international Engineering, Procurement, and Construction (EPC) firms and their Saudi partners, rental is often the easier route because it aligns with group-wide procurement practices and reduces the need to build a country-specific asset base. This makes fleet availability, turnaround speed, and inspection support important selling points in addition to price.

The strength of the rental model also changes bargaining power during busy delivery periods. When shutdown campaigns, accelerated deadlines, or overlapping completion phases lift short-term demand, operators with large certified fleets can command firmer pricing and better contract terms. This is especially relevant in a market where project timings are increasingly layered across transport, hospitality, mixed-use, and industrial work. The Saudi Arabia scaffolding industry is therefore seeing rental grow not only because of lower upfront cost, but also because it offers schedule flexibility that owned fleets cannot always match. Vendors that combine rental with design, erection supervision, and inspection can turn that flexibility into a more complete service offer. Sales remained the smaller business model at 39% in 2025, but it still has a clear place in long-duration or high-utilization environments. Buyers with constant maintenance needs or fixed industrial access programs can justify ownership when the equipment remains on site for extended periods. That logic is strongest in some energy and plant maintenance channels, where utilization can be high and repeated mobilization costs are less attractive. Even so, ownership does not remove the need for design support, inspections, and trained labor. For that reason, the Saudi Arabia scaffolding market is likely to keep favoring rental at the overall level while preserving a strategic role for direct sales in selected industrial settings.

By Material Type: Steel Dominates but Aluminum Reshapes the Premium Tier

Steel held a 72% share in 2025, making it the primary material in the Saudi Arabia scaffolding market. That position is tied to the heavy-duty requirements of transport works, industrial plants, logistics facilities, and broad infrastructure packages where load-bearing strength and site familiarity matter most. Steel also fits the dominant supported scaffold format and large working platforms used across civil and industrial jobs. Aluminum, however, is forecast to grow fastest at a 10.5% CAGR through 2031, as projects in high-rise fit-out, hospitality, and lighter access work seek easier handling and faster installation. The Saudi Arabia scaffolding market still relies on steel, but material choice is becoming more segmented by end use rather than adhering to a single standard.

Aluminum’s growth also reflects operating conditions in locations where corrosion resistance and lower manual handling weight carry practical value. In coastal and humid settings, buyers increasingly weigh maintenance needs and service life rather than focusing solely on upfront material cost. Lighter systems can also help crews reposition equipment faster on dense urban and interior work scopes. This does not remove steel from the core of the market, but it does increase aluminum’s role in higher-specification and time-sensitive packages. Over time, that can raise the average value of premium access contracts even if steel remains dominant by volume. Other materials continue to serve narrower roles. Timber / plywood remain present in low-budget work, but they face tighter acceptance limits where buyers ask for better traceability and certified components. Plastic / fiberglass systems occupy small but important niches in utilities, electrical work, and chemical settings where non-conductive properties matter. Material choice is therefore becoming more application driven than before, with buyers matching system weight, durability, and safety requirements to the task. For suppliers, the best position is no longer to stock one main material only, but to maintain a mix that can serve both heavy industrial demand and lighter urban access needs.

By Sector: Infrastructure Leads as Industrial & Logistics Closes the Gap

Infrastructure accounted for a 39% share of the Saudi Arabia scaffolding market in 2025, making it the largest sector in the current mix. The scale of transport upgrades, urban public works, and associated utility construction gives this segment a broad and steady demand base. Large infrastructure jobs also tend to run across long timelines, which supports sustained equipment deployment rather than short spikes in use. Industrial & logistics is projected to grow fastest at a 10.6% CAGR through 2031, indicating the rising importance of plant construction, industrial expansion, and logistics-linked facilities in the Saudi Arabia scaffolding market. Saudi Aramco’s active upstream and downstream investment pipeline continues to support this shift, especially in the Eastern Province, where new assets add future maintenance needs on top of current construction.

The industrial growth pattern matters because it is not driven only by one-off buildouts. Once new facilities move into operation, they create recurring shutdown, inspection, and turnaround work that can keep scaffold demand active beyond the initial construction period. That gives industrial & logistics a more durable runway than sectors that depend only on new project awards. Infrastructure will remain the largest sector because its current base is broader and more geographically spread. Yet the faster industrial growth rate shows where premium work and recurring service demand are becoming more important. The commercial and residential sectors still account for a meaningful share of project count, even though they do not match the value per site of industrial or infrastructure projects. Commercial demand benefits from mixed-use and hospitality development, but it often faces tighter bidding pressure and lower-quality margins than industrial maintenance. Residential work is widespread across several sites, though unit project values are usually smaller and often centered on a supported scaffolds. This keeps a wide base of day-to-day demand in the Saudi Arabia scaffolding market, even outside large signature projects. The result is a sector mix in which infrastructure anchors current scale, while industrial & logistics adds momentum and recurring value through the forecast period.

Geography Analysis

Riyadh accounted for 31% of the Saudi Arabia scaffolding market in 2025, making it the leading city cluster in terms of current demand. The capital’s strength comes from a dense overlap of transport infrastructure, mixed-use development, entertainment projects, and public investment that keeps access needs active across multiple project types. Construction sector banking credit reached SAR 146.7 billion (USD 39.1 billion) in April 2026, up 9.8% year over year, which supports the view that project financing and activity remained firm. Point-of-sale activity in the construction sector also rose 6.5% year over year in April 2026, which matched the still-active delivery environment visible across Riyadh and other large urban centers. The January 2026 Red Line extension award added another long-duration urban transport project to Riyadh’s workload and reinforced the city’s lead in the Saudi Arabia scaffolding market.

Eastern Province is the fastest-growing city cluster, with a 9.5% CAGR through 2031, driven by both new asset creation and recurring industrial maintenance. Saudi Aramco’s capital program continues to support field development and facility activity across the province, providing scaffolding suppliers with exposure to both construction and plant service work. The Marjan and Berri project updates from 2025 matter because newly commissioned and expanded facilities feed future inspection and shutdown cycles as they move deeper into operations. This creates a denser and more recurring demand base than cities that rely mostly on one-time urban buildouts. For the Saudi Arabia scaffolding market, Eastern Province therefore combines strong growth with better long-run visibility than many purely construction-led geographies.

Makkah Region remains important because hospitality, mobility, and holy-site support work continue throughout the year rather than around a single project window. Madinah follows a similar pattern on a smaller scale, supported by ongoing religious, hospitality, and urban service development under the national project agenda. The rest of Saudi Arabia adds demand from industrial diversification corridors, secondary urban works, and project support outside the main metropolitan centers. This wider geographic spread helps the Saudi Arabia scaffolding market maintain utilization even when project timing shifts from one city to another.

Competitive Landscape

The Saudi Arabia scaffolding market remains moderately fragmented, but the competitive field is increasingly divided by certification depth, service capabilities, and fleet scale. Domestic specialists such as Saudi Scaffolding Factory, SGB Al-Dabal Co. Ltd, and Al Najm Al Thaqib Scaffolding Company operate alongside Saudi units or affiliates of global names such as BrandSafway, Layher, and PERI. At the broad market level, many smaller contractors still compete on price in standard urban work. In premium industrial and maintenance channels, the competitive set narrows because buyers place more weight on compliance, engineering support, and reliable mobilization. This makes the Saudi Arabia scaffolding market more concentrated in high-value subsegments than in the overall national total.

A clear line separates suppliers that provide only equipment from those that package engineered access support. KAEFER Saudi Arabia’s Zuluf project is a strong example of the second model, as it combined large material deployment with 3D-based design and structured execution on a major oil site. BrandSafway’s January 2026 launch of the Spider work-at-height system also shows that global operators are still adding differentiated products for constrained industrial and infrastructure environments. Layher’s introduction of the Allround Lightweight system points in the same direction, with product changes aimed at easier handling and a broader set of site conditions. These moves show that product design, engineering support, and documented safety performance are becoming more important in how the Saudi Arabia scaffolding market is contested.

PERI Saudi Arabia’s 3 branches and its engineering, inspection, and project support capabilities underscore the value of a strong in-country presence when projects are spread across several cities. Operators with local yards, trained crews, and inspection support can serve both long-duration contracts and urgent short-cycle demand more effectively than firms that rely on narrower local setups. The result is not a winner-takes-all structure, but a layered market where premium jobs are harder to enter than routine jobs. Over time, that should favor suppliers that can demonstrate compliance, multi-city availability, and engineering support in a single offer. This is why the Saudi Arabia scaffolding market is likely to stay fragmented in volume terms while becoming more selective in the highest-value channels.

Saudi Arabia Scaffolding Industry Leaders

Saudi Scaffolding Factory (SSF)

Al Najm Al Thaqib Scaffolding Company (NTC)

Najd Scaffolding & Formwork

PERI Saudi Arabia

SGB Al-Dabal Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Saudi Aramco released its full-year 2025 results and guided capital investment of USD 50-55 billion for 2026, following USD 52.2 billion in 2025. The spending outlook continues to support scaffolding demand in the Eastern Province, particularly for shutdown, maintenance, and field development activities.

- February 2026: ASMO, the Aramco–DHL Supply Chain joint venture, partnered with Arcapita in February 2026 to develop a 1.4 million square meters logistics facility at King Salman Energy Park (SPARK), including a 43,000 square meters Grade-A warehouse, chemical storage facilities, offices, and a 1.2 million square meters industrial yard; the large-scale development is expected to generate sustained demand for scaffolding and temporary access structures throughout the multi-year construction phase.

- January 2026: The Royal Commission for Riyadh City awarded contracts for the 8.4 km Red Line metro extension to Diriyah Gate, encompassing 7.1 km of deep underground tunnels, 1.3 km of elevated tracks, and 5 new stations; completion is scheduled in approximately 6 years, adding a multi-year structural scaffolding campaign to Riyadh's active construction workload.

Saudi Arabia Scaffolding Market Report Scope

The Saudi Arabia Scaffolding Market is Segmented by Type (Supported, Suspended, and Mobile), System (Tube & Coupler, Cuplock, Modular / Ringlock, H-Frame), Business Model (Sales and Rental), Material (Timber / Plywood, Steel, Aluminum, and More), Sector (Residential, Commercial, Industrial & Logistics, and Infrastructure), and By City (Riyadh, Eastern Province, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Supported Scaffold |

| Suspended Scaffold |

| Mobile Scaffold |

| Tube & Coupler |

| Cuplock |

| Modular / Ringlock |

| Frame / H-Frame |

| Sales |

| Rental |

| Timber / Plywood |

| Steel |

| Aluminum |

| Plastic / Fibreglass |

| Others |

| Residential |

| Commercial |

| Industrial & Logistics |

| Infrastructure |

| Riyadh |

| Eastern Province |

| Makkah Region |

| Madinah Region |

| Rest of Saudi Arabia |

| By Type | Supported Scaffold |

| Suspended Scaffold | |

| Mobile Scaffold | |

| By System | Tube & Coupler |

| Cuplock | |

| Modular / Ringlock | |

| Frame / H-Frame | |

| By Business Model | Sales |

| Rental | |

| By Material Type | Timber / Plywood |

| Steel | |

| Aluminum | |

| Plastic / Fibreglass | |

| Others | |

| By Sector | Residential |

| Commercial | |

| Industrial & Logistics | |

| Infrastructure | |

| By City | Riyadh |

| Eastern Province | |

| Makkah Region | |

| Madinah Region | |

| Rest of Saudi Arabia |

Key Questions Answered in the Report

What is the current size of Saudi Arabia scaffolding demand?

The Saudi Arabia scaffolding market size stands at USD 275 million in 2026 and is forecast to reach USD 420 million by 2031 at an 8.84% CAGR.

Which segment leads by scaffold type in Saudi Arabia?

Supported scaffold leads with 66% share in 2025 because large infrastructure, utility, and industrial sites still rely heavily on ground-supported access systems.

Why is rental growing faster than direct sales?

Rental held 61% share in 2025 and is also the fastest-growing business model at 10.2% CAGR because contractors want flexibility across multiple concurrent sites without tying up capital in owned fleets.

Which material is expanding fastest in Saudi projects?

Aluminum is growing fastest at 10.5% CAGR through 2031, helped by fit-out, hospitality, and lighter access needs where easier handling and corrosion resistance matter.

Which city cluster has the strongest growth outlook?

Eastern Province is projected to grow fastest at 9.5% CAGR through 2031 because it combines oil and gas construction, existing asset maintenance, and industrial expansion.

Page last updated on: