Rapid Diagnostic Kits Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 25.16 Billion |

| Market Size (2031) | USD 37.42 Billion |

| Growth Rate (2026 - 2031) | 8.27% CAGR |

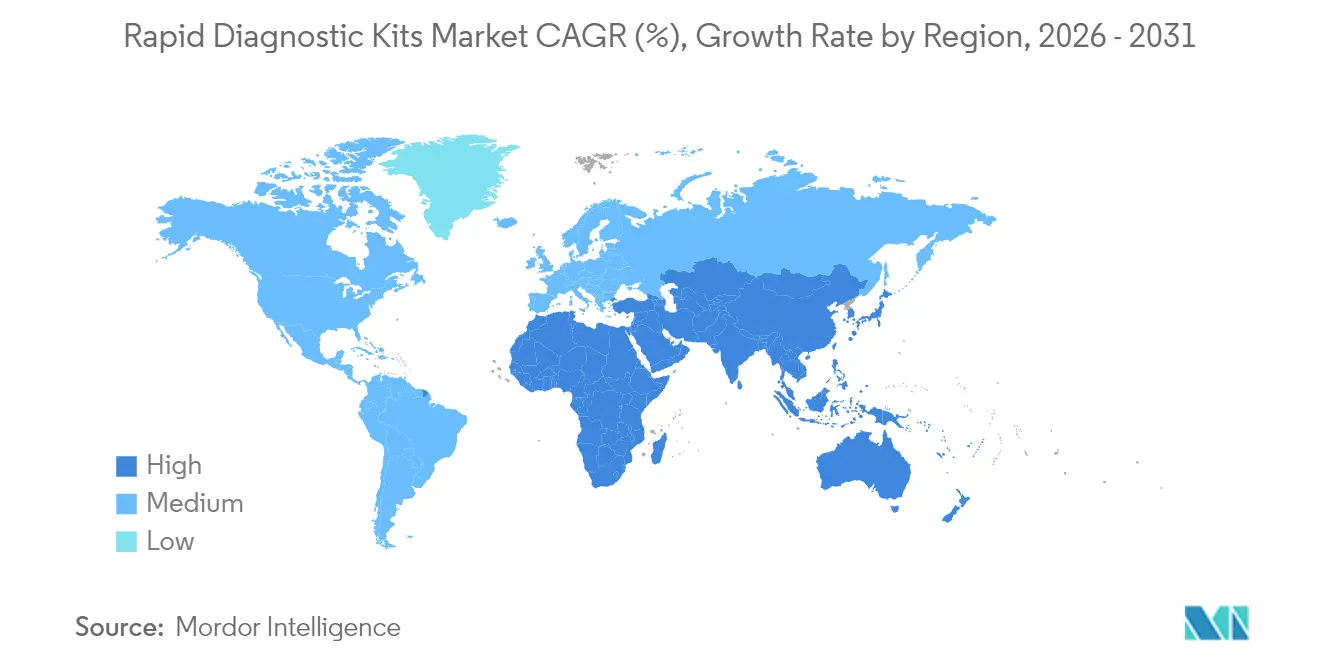

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

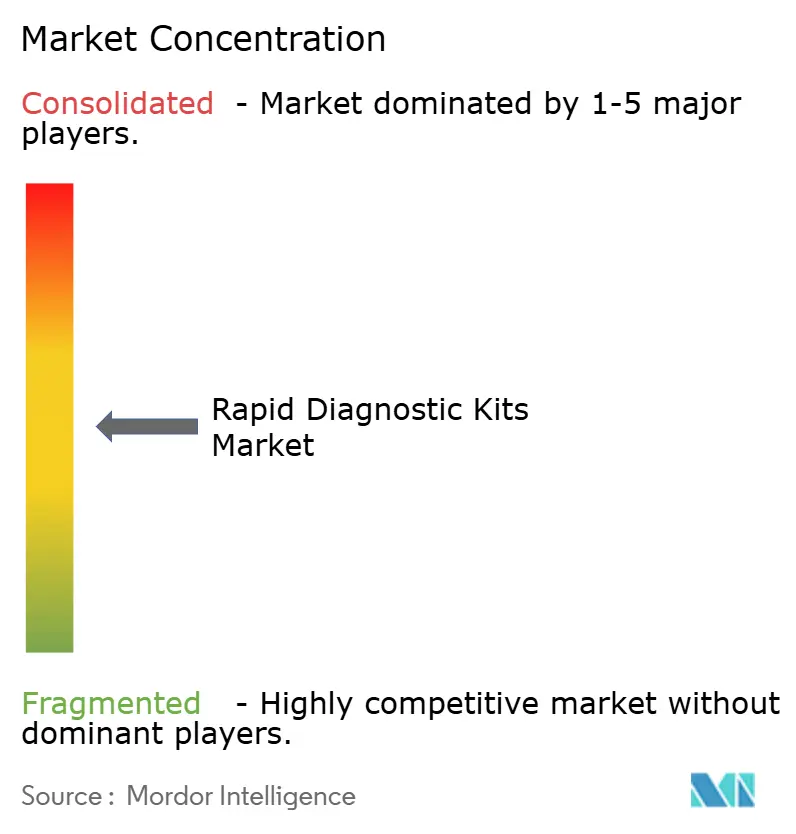

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rapid Diagnostic Kits Market Analysis by Mordor Intelligence

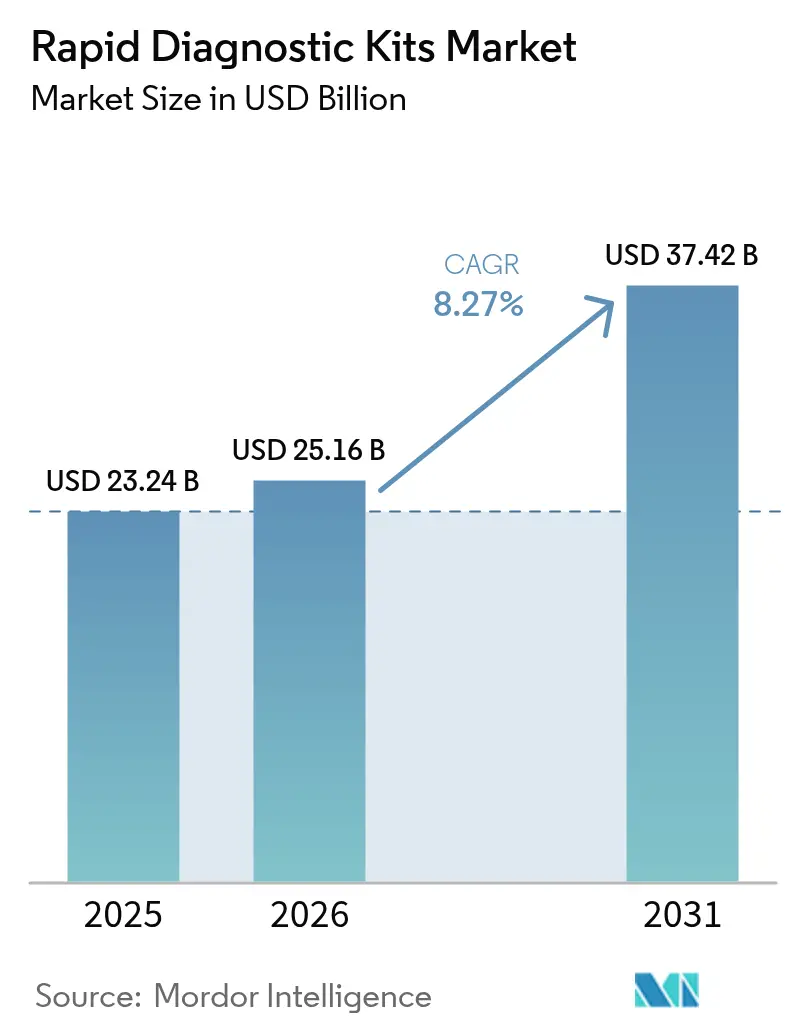

The Rapid Diagnostic Kits market size is expected to grow from USD 23.24 billion in 2025 to USD 25.16 billion in 2026 and is forecast to reach USD 37.42 billion by 2031 at 8.27% CAGR over 2026-2031.

The expansion reflects rising point-of-care adoption, tighter hospital budgets, and the global shift from episodic to preventive care. Technology upgrades that allow multiplex detection, alongside supportive reimbursement for chronic disease monitoring, keep demand elevated even after the acute pandemic wave. Manufacturers benefit from government funding that de-risks R&D, while ageing populations increase test volumes across primary and home-care settings. Competitive strategies now focus on scale, vertical integration, and data connectivity as hospitals and consumers both expect seamless integration with electronic health records.

Key Report Takeaways

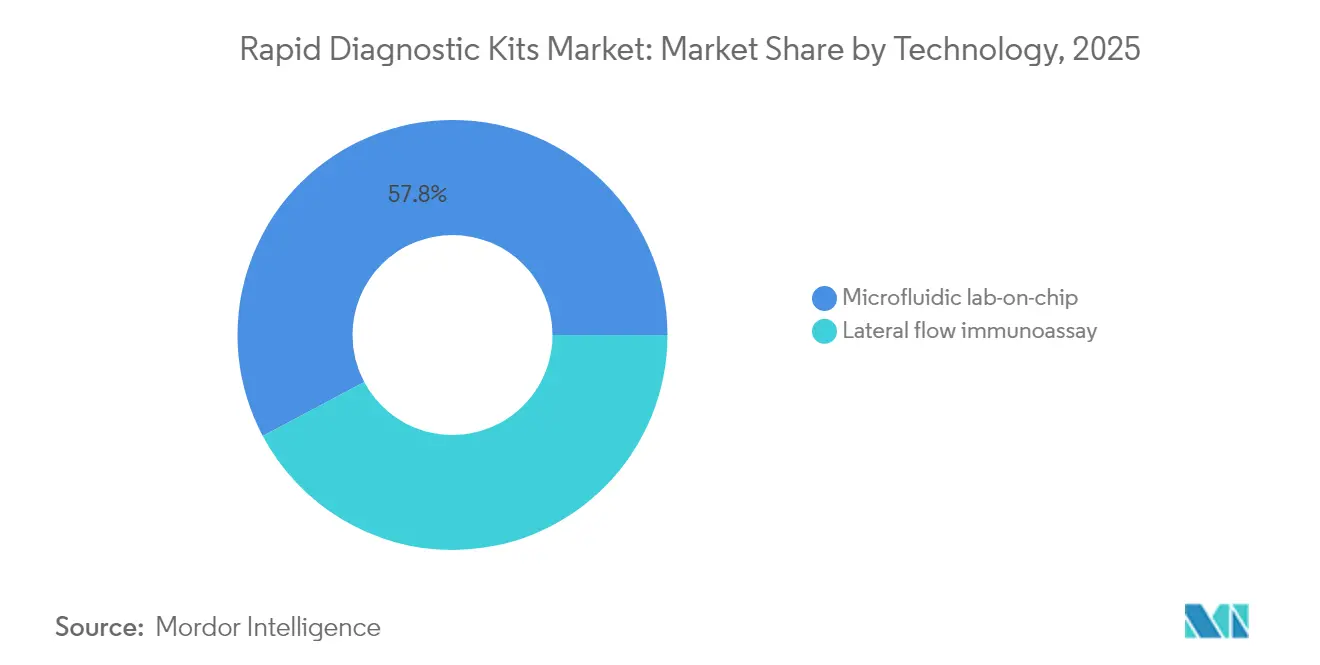

- By technology, lateral flow immunoassay held 42.21% of the rapid diagnostics kits market share in 2025 and immuno-chromatography is projected to expand at a 8.84% CAGR through 2031 within the rapid diagnostics kits market size.

- By application, infectious diseases led with 35.62% revenue share in 2025, while oncology markers is poised for the fastest 9.02% CAGR to 2031 in the rapid diagnostics kits market.

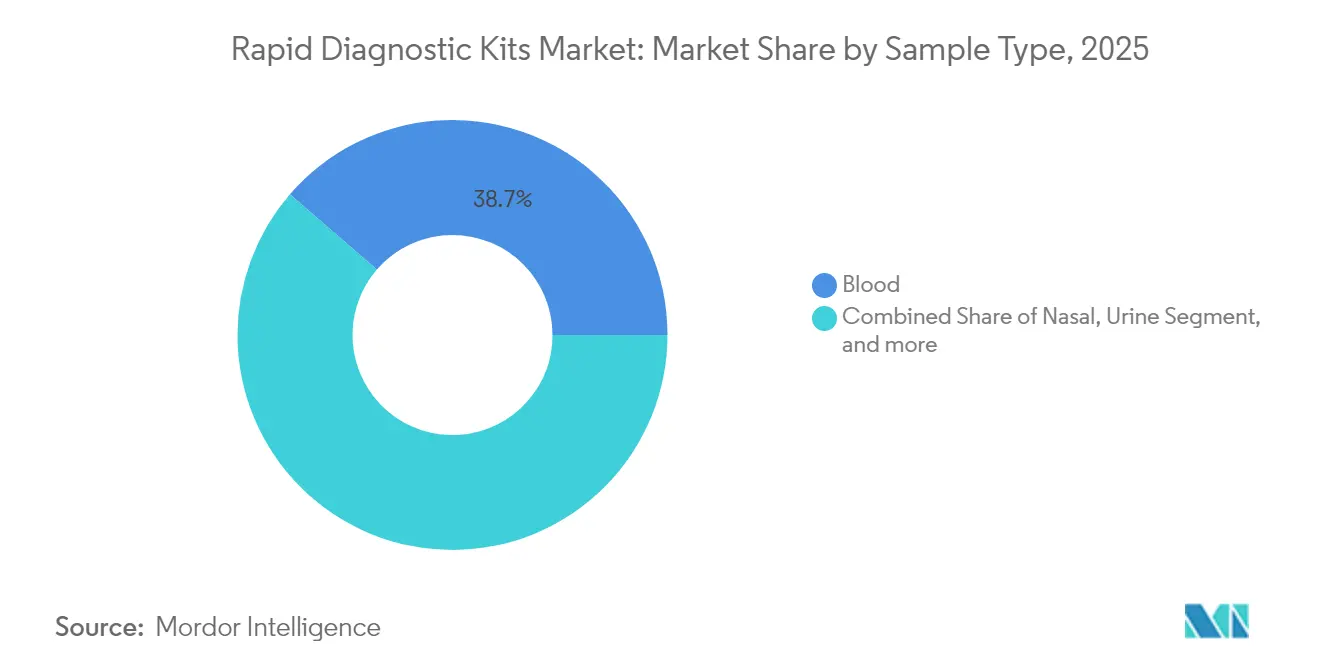

- By sample type, blood accounted for 38.65% of 2025 testing volume; saliva is the fastest mover at a 9.87% CAGR through 2031 in the rapid diagnostics kits market size.

- By end user, hospitals & clinics retained 35.31% of 2025 revenue, whereas home-care settings are forecast to grow at 8.55% CAGR to 2031 within the rapid diagnostics kits market.

- By geography, North America commanded 37.88% of 2025 sales, and Asia-Pacific is set to post the highest 10.74% CAGR to 2031 in the rapid diagnostics kits market size.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Rapid Diagnostic Kits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Funding Surge for Multiplex Respiratory Panels | +1.8% | North America & EU, spill-over to APAC | Medium term (2-4 years) |

| Rising Consumer Adoption of Self-Testing for Chronic Diseases | +1.5% | Global, with early gains in North America, Europe | Long term (≥ 4 years) |

| Expansion of Decentralized Molecular PoC Platforms in LMICs | +1.2% | APAC core, Sub-Saharan Africa, Latin America | Long term (≥ 4 years) |

| Integration of AI-Enabled Readers Improving Test Accuracy | +0.9% | Global, led by North America & EU | Medium term (2-4 years) |

| Emergence of CRISPR-Based Ultra-Rapid Assays | +0.7% | North America & EU, gradual APAC adoption | Long term (≥ 4 years) |

| Increasing Awareness of Diseases Driving Screening Demand | +0.6% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Funding Surge for Multiplex Respiratory Panels

Public agencies continue to bankroll multiplex respiratory panels that test for SARS-CoV-2, influenza A/B, and RSV in one cartridge, giving suppliers firm multiyear order books. BARDA’s outlays have accelerated prototype-to-market timelines, exemplified by Roche’s 20-minute cobas liat triple assay cleared in May 2024.[1]Roche Diagnostics, “cobas liat respiratory triple test EUA,” roche.com Hospitals embrace the syndromic model because a single swab trims sample handling, shortens isolation decisions, and conserves personal protective equipment. Laboratories capture operational savings, while manufacturers secure volume commitments that justify further platform miniaturization. The model is now migrating to emerging pathogen panels, widening the rapid diagnostics kits market scope and solidifying a revenue floor for molecular suppliers.

Rising Consumer Adoption of Self-Testing for Chronic Diseases

Self-testing has moved beyond pregnancy kits into cardiometabolic and infectious disease monitoring. Labcorp’s First-to-Know syphilis kit, the first FDA-authorized over-the-counter blood test for a bacterial STI, validated consumer readiness for capillary sampling at home. Digital health platforms that curate results for care teams reduce clinic visits and enable medication titration without laboratory delays. Payers also gain, as direct-pay kits lower claims associated with repeated phlebotomy. Regulatory draft guidance on digital detection of prediabetes underscores official support for non-invasive screening, and suppliers respond by embedding Bluetooth or NFC connectivity for instant data upload. The behavioural shift cements home-care as the fastest end-user channel in the rapid diagnostics kits market.

Expansion of Decentralized Molecular PoC Platforms in LMICs

Resource-constrained regions favor rugged devices that deliver lab-quality results without continuous power or specialized staff. FIND pegs annual LMIC demand at 63.6 million tests, a sizable white space for tuberculosis, hepatitis B, and HIV assays.[2]FIND, “Target product profiles for LMIC diagnostics,” finddx.org Cepheid’s 36-minute Mpox cartridge, distributed across district clinics after the WHO emergency declaration, demonstrates rapid deployment potential. Governments view molecular PoC as essential for antimicrobial stewardship because real-time results curb empirical prescriptions. Local manufacturing partnerships and donor-backed procurement de-risk currency and logistics exposure, enhancing supplier competitiveness in the rapid diagnostics kits market.

Integration of AI-Enabled Readers Improving Test Accuracy

AI algorithms now analyze faint lines or optical signals imperceptible to human eyes, transforming long-standing lateral flow devices into semi-quantitative tools. FDA re-classification of acute febrile illness detectors into Class II special controls provides a clear route for algorithm-powered readers.[3]U.S. Food and Drug Administration, “Class II special controls for febrile illness agents,” fda.gov Chronus Health’s microfluidic sensor array couples electrical detection with machine learning to convert a finger-prick sample into multiplexed outputs in minutes. Consistency across operators reduces false negatives, augments epidemiological confidence, and builds value for providers who reimburse based on clinical outcomes. The convergence of AI and hardware thus raises performance benchmarks and reinforces premium pricing in the rapid diagnostics kits market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-Chain Fragility for Critical Reagents | -1.4% | Global, acute in APAC manufacturing hubs | Short term (≤ 2 years) |

| Regulatory Uncertainty for Home-Use Multiplex Kits | -0.8% | North America & EU regulatory jurisdictions | Medium term (2-4 years) |

| Reader-Device Data-Privacy Concerns | -0.5% | Global, heightened in EU under GDPR | Medium term (2-4 years) |

| Sustainability Pressure on Single-Use Plastics | -0.4% | EU & North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Fragility for Critical Reagents

Specialized antibodies, enzymes, and buffers are often produced in single-facility clusters across East Asia. Trade friction or pandemics quickly halt exports, forcing allocation protocols that lengthen delivery times and inflate costs. The COVID-19 crisis exposed these choke points when enzyme shortages limited PCR kit output. Manufacturers now dual-source or internalize reagent production, but capital outlays lengthen payback horizons and squeeze smaller firms. Disruptions can starve public clinics of essential diagnostics, especially in low-income regions that lack inventory buffers, restraining the rapid diagnostics kits market until redundancy plans mature.

Regulatory Uncertainty for Home-Use Multiplex Kits

The July 2024 FDA rule that ends enforcement discretion for laboratory-developed tests places home-use multiplex kits under device regulations. Developers must undertake extensive clinical validation to secure CLIA waiver, raising cost and time to market. Europe adds complexity through country-specific implementation of the IVDR, and data privacy statutes such as GDPR impose strict controls on cloud-connected readers. As compliance budgets balloon, start-ups may defer launches or pivot to single-analyte formats. The regulatory cloud tempers the rapid diagnostics kits market momentum in the home segment until clear cross-border standards emerge.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Lateral Flow Dominance Faces Molecular Challenge

Lateral flow immunoassay generated the largest slice of the rapid diagnostics kits market in 2025 with 42.21% revenue, underpinned by mature supply chains, low unit costs, and the ability to scale quickly during pandemic surges. The segment continues to thrive in resource-limited clinics, humanitarian missions, and mass-screening programs because it tolerates ambient temperatures and requires minimal training. Advances such as nanoparticle labels and improved membrane porosity are lifting analytical sensitivity, allowing lateral flow to defend share even as laboratory expectations rise. Immuno-chromatography, though smaller, logs the fastest 8.84% CAGR, fueled by growing physician demand for semi-quantitative output and by AI-assisted readers that unlock richer data layers. Microfluidic lab-on-chip systems inch forward in endocrinology and neonatal screening where microlitre volumes and high precision matter. Molecular rapid assays employing isothermal amplification or CRISPR editing record double-digit growth, capitalizing on syndromic panels that bundle respiratory and gastrointestinal targets. Biosensor platforms leverage electrochemical detection to capture continuous glucose or cardiac biomarker trends, expanding the total addressable rapid diagnostics kits market.

A steady pipeline of combination systems blends lateral flow cartridges with integrated nucleic-acid capture modules. Such hybrids promise lower reagent use, three-target detection in one strip, and smartphone readouts that sync to cloud dashboards. FDA’s January 2025 validation guidance for emerging pathogen panels accelerates clearance of these designs. As hospitals rationalize suppliers, technology differentiation now hinges on throughput, sample type versatility, and embedded connectivity rather than solely on detection chemistry. Manufacturers that pair proprietary reagents with open-analytics software carve durable footholds within the rapid diagnostics kits market.

By Application: Infectious Diseases Leadership Challenged by Oncology Growth

Infectious diseases contributed 35.62% of 2025 revenue, buoyed by perpetual influenza, RSV, and antimicrobial resistance surveillance. Yet oncology markers is advancing fastest at a 9.02% CAGR because policy makers back early detection to curb treatment costs. Point-of-care FIT tests, liquid biopsy cartridges for methylated DNA, and nucleosome assays such as VolitionRx’s sepsis indicator keep oncology in the spotlight. Cardio-metabolic Monitoring gains as hypertension and diabetes management migrate to pharmacies and homes. Pregnancy & Fertility kits sustain baseline volume, expanded by later-life pregnancies and tele-reproductive services. Toxicology & Drugs-of-Abuse panels evolve in step with shifting opioid policies and upcoming federal workplace rule revisions.

Veterinary & zoonotic screening, though small today, benefits from One Health frameworks that integrate animal and human disease vigilance. The overall rapid diagnostics kits market size for infectious disease testing in LMICs is buttressed by multilateral grants, while oncology-focused start-ups secure venture capital to refine epigenetic targets. Application diversification thus cushions suppliers against cyclical demand swings and positions multipurpose platforms for cross-sector revenue.

By Sample Type: Blood Dominance Challenged by Saliva Innovation

Whole-blood and finger-stick samples represented 38.65% of 2025 test volumes, thanks to entrenched workflows and the broad menu of analytes validated for this matrix. Standardization of micro-collection tubes and anticoagulants eases integration with automation such as Siemens Healthineers’ Atellica line, which reduces manual steps by 75%. Nonetheless, Saliva registers the swiftest 9.87% CAGR as consumers prefer painless collection for hormonal, genetic, and respiratory panels. Nasal swabs stay relevant because they align with respiratory virus tropism and clinician familiarity, while Urine dominates in toxicology and pregnancy contexts for its stability and large analyte library. Stool sampling, though cumbersome, becomes indispensable for colorectal cancer screening.

Technology cross-pollination continues. Glyconics’ fingernail infrared analysis hints at bodily materials other than blood or saliva serving as diagnostic goldmines. Each matrix influences cartridge design, reagent stability, and reader optics, so platform adaptability becomes a source of competitive edge in the rapid diagnostics kits market. Manufacturers develop interchangeable sample modules that snap onto a core analyzer, permitting hospitals to minimize training and inventory. Multi-sample versatility will likely dictate future formulary listings as payers tighten reimbursement thresholds tied to cost per reportable result.

By End User: Home-Care Acceleration Disrupts Traditional Channels

Hospitals & clinics still generated the largest 35.31% slice in 2025, driven by high patient throughput and bundled reagent contracts covering inpatient and outpatient wings. Yet home-care Settings are sprinting at an 8.55% CAGR, energized by direct-to-consumer marketing and insurer support for telehealth. CLIA-waived urgent care centers and retail pharmacies install compact analyzers to dispense treatment during a single visit, trimming readmission risk. Diagnostic laboratories feel share erosion as decentralized kits bypass traditional specimen logistics; they counter by offering validation services for emerging pathogens and complex pharmacogenomic panels. Workplace testing, mobile vans, and school screening round out the “Other” bracket, expanding total addressability of the rapid diagnostics kits market.

Integration with telemedicine platforms lets home-care users transmit results to clinicians who adjust therapy in real time, aligning with value-based care mandates. Siemens Healthineers’ Atellica peripherals illustrate how legacy in-lab systems now pair with cloud APIs to share data across care sites. Manufacturers redesign packaging for e-commerce fulfillment, adding tamper-evident seals and multilingual QR-code instructions. The channel mix will influence pricing tiers, with B2C kits commanding premiums for convenience while hospital volumes drive cost-plus contracts.

Geography Analysis

North America retained 37.88% of 2025 revenue, aided by favorable reimbursement codes, high digital literacy, and the BARDA pipeline that continuously seeds innovation. The United States accounts for a majority share, where CLIA waivers for Roche’s 20-minute STI assays open wide deployment across 12,000 retail clinics. Canada follows through national tender programs for First Nations communities, adding HIV and hepatitis-C cartridges to primary-care tool kits. The region also leads in AI-reader pilots that integrate with electronic health records, creating first-mover advantages for early adopters within the rapid diagnostics kits market.

Asia-Pacific records the strongest 10.74% CAGR, spurred by public insurance expansion and government incentives for domestic IVD production. China’s push for self-reliance lifted local suppliers who reverse-engineer reagents to undercut imports, while tier-2 city hospitals procure portable PCR analyzers to meet new respiratory surveillance mandates. India scales telemedicine through its Ayushman Bharat Digital Mission, embedding rapid metabolic panels into community health worker kits. Southeast Asian ministries deploy combination dengue-COVID cartridges during monsoon seasons, and Japanese geriatric clinics pilot saliva-based dementia biomarkers. The region’s heterogeneity drives diverse demand patterns yet converges on a common need for low-maintenance, cloud-connected systems.

Europe sustains steady mid-single-digit growth undergirded by harmonized IVDR rules that assure cross-border device acceptance. Germany finances AI-assisted lateral flow platforms in nursing homes, while France subsidizes pharmacy-based cardiometabolic screens to shorten cardiologist queues. The Middle East & Africa sees accelerated tender activity for tuberculosis and mpox detection as petro-states upgrade lab infrastructure, though distribution remains hampered in remote zones. Latin America tackles arbovirus co-circulation with multiplex assays that differentiate dengue, Zika, and chikungunya. Cross-regional donor programs, such as the Global Fund, aggregate demand and smooth currency volatility, anchoring the rapid diagnostics kits market size across emerging geographies.

Regulatory Landscape

Regulatory pathways for rapid diagnostic kits are tightening across major markets, raising the bar for clinical evidence, quality systems, and post-market controls, particularly for decentralized and home-use formats. In the United States, the FDA issued a final rule in May 2024 to treat laboratory-developed tests (LDTs) as medical devices and phase out enforcement discretion over several years, which increases validation and QMS obligations for test developers that previously operated under lab frameworks. The FDA also finalized guidance in September 2025 on enforcement policies for unapproved in vitro diagnostic tests during declared emergencies, shaping how emerging-pathogen panels move from emergency conditions into routine commercialization.

In Europe, implementation of the In Vitro Diagnostic Regulation (IVDR) continues to reconfigure conformity assessment timelines and operational readiness, with EUDAMED milestones becoming material for market access workflows, including actor and device registration for new IVDs from May 28, 2026. For global health procurement, the World Health Organization (WHO) expanded prequalification mechanics, including announcing in December 2025 the prequalification of the first two rapid antigen detection tests for COVID-19 and implementing a revised approach from January 2026 that separates product performance evaluation as a prerequisite step for prequalification assessment. These changes affect launch sequencing and documentation strategies for suppliers serving both high-income regulatory jurisdictions and donor-funded tender channels.

Competitive Landscape

The rapid diagnostics kits market is moderately concentrated, with household names capturing share through vertical integration and M&A. Becton Dickinson’s USD 17.5 billion Waters combination broadens reagent and instrument portfolios, giving BD analytical chemistry capabilities previously missing from its point-of-care arsenal. Roche’s USD 295 million LumiraDx purchase grants it microfluidic expertise that complements the cobas franchise and accelerates market entry for digital readers. BioMérieux’s USD 138 million SpinChip deal locks in proprietary microfluidic nozzle technology that shortens nucleic-acid extraction.

Tier-one players exploit scale to mitigate reagent shortages and negotiate long-term governmental contracts, but nimble start-ups chip away niches through AI, CRISPR, or sample-agnostic platforms. Cepheid leverages early pathogen panels alongside distribution into 180 countries, whereas Abbott builds recurrent revenue via consumable strips embedded in chronic care pathways. Digital health alliances such as Siemens Healthineers syncing Atellica results to population-level dashboards offer differentiation beyond unit economics. Sustained R&D pipelines, global regulatory proficiency, and localized manufacturing dictate competitive edge in an era where time-to-market influences pandemic response funding.

White-space opportunities surface in antimicrobial stewardship, oncology epigenetics, and neurodegenerative disease biomarkers. Firms that co-develop reagents with pharma partners attain companion-diagnostic premiums. Meanwhile, sustainability drives packaging innovations that replace polystyrene with biodegradable polymers, aiming to pre-empt EU single-use restrictions. The competitive outlook thus hinges on merging chemistry, automation, connectivity, and environmental stewardship to win formulary tiering and public grants within the rapid diagnostics kits market.

Rapid Diagnostic Kits Industry Leaders

ACON Laboratories Inc.

Abbott Laboratories

Alfa Scientific Designs Inc.

Artron Laboratories Inc.

F. Hoffmann-La Roche AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regional manufacturing localization is creating a more practical whitespace in supply assurance and tender competitiveness, especially where public-sector buyers prioritize import substitution and continuity of supply. In June 2026, Abbott began local production of HIV, syphilis, and hepatitis rapid test kits in Nigeria through a partnership tied to the Presidential Initiative for Unlocking the Healthcare Value Chain and Afrimedical, and NASENI highlighted the NASENI-Troment Diagnostics Factory with stated capacity to produce up to 600 million rapid diagnostic test kits annually (July 2026). Alongside India capacity additions such as Lord's Mark Industries opening a new IVD manufacturing facility in June 2026, these moves give kit makers scope to combine localized assembly or upstream steps with regional distribution, faster replenishment cycles, and participation in ministry-led procurement programs.

Compliance-driven redesign and connectivity-ready products are also creating another opportunity pocket as rules converge on stronger quality systems and traceability. The EU's May 2026 EUDAMED requirements, the US FDA's QMSR alignment with ISO 13485:2016 taking effect in 2026, and the UK's shift away from CTDA toward conformity assessment against Common Specifications for COVID-19 tests are pushing manufacturers to upgrade design controls, labeling, and post-market data flows. Suppliers that embed secure reader connectivity, strengthen cybersecurity and data handling for home and pharmacy settings, and standardize technical documentation across jurisdictions can reduce friction in multi-country launches, especially for multiplex respiratory and STI panels already moving into CLIA-waived and CE-marked point-of-care footprints.

Recent Industry Developments

- March 2026: Roche launched the cobas eplex respiratory pathogen panel 3 (RP3) in CE-mark countries, expanding syndromic respiratory testing to detect up to 25 viral and bacterial targets. The launch reinforces the shift toward broader multiplex menus in decentralized and near-patient workflows, supporting faster differential diagnosis from a single sample.

- December 2025: Roche received FDA 510(k) clearance and a CLIA waiver for a cobas liat point-of-care molecular test for Bordetella (whooping cough) infections with results in about 15 minutes. The combined clearance and waiver expands the addressable POC footprint in urgent care and retail clinic settings where rapid respiratory triage and immediate treatment decisions are operational priorities.

- April 2024: Abbott received FDA clearance for the i-STAT TBI whole-blood test cartridge to support assessment of suspected concussion at the bedside, delivering results in about 15 minutes. This broadens rapid testing beyond infectious disease into acute-care decision support, bringing lab-grade biomarkers into emergency and urgent care workflows without central-lab turnaround times.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers rapid diagnostic kits that provide quick test results, used to identify diseases or health conditions in clinical and non-clinical settings. We size the market in value terms based on kit sales across key testing needs such as infectious disease, diabetes, and pregnancy.

Scope exclusions: Capital lab analyzers and routine laboratory services are excluded when they are not sold as rapid kit-based solutions.

Segmentation Overview

- By Technology

- Lateral Flow Immunoassay

- Microfluidic Lab-on-Chip

- Immuno-chromatography

- Agglutination & Latex Tests

- Biosensor-Based Rapid Tests

- Molecular Rapid Tests

- By Application

- Infectious Diseases

- Cardio-metabolic Monitoring

- Pregnancy & Fertility

- Toxicology & Drugs-of-Abuse

- Oncology Markers

- Veterinary & Zoonotic Screening

- By Sample Type

- Blood

- Nasal

- Urine

- Saliva

- Stool

- By End User

- Hospitals & Clinics

- Physician Offices & Urgent Care

- Home-care Setting

- Diagnostic Laboratories

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting structure for the model, with focus on test adoption patterns and healthcare system capacity. We relied on public sources such as the World Health Organization, the US CDC, and the US FDA (including approvals and safety notices), along with databases and publications from the World Bank and OECD for comparable health spend and access indicators.

To avoid sizing the market in isolation, we also reviewed annual reports and investor presentations of relevant manufacturers, along with association websites, peer-reviewed journals on rapid testing performance and use cases, and reputable press coverage of outbreaks and screening programs. When needed, we used paid subscriptions for company financials and intelligence, patent databases, and shipment-level import and export tracking to sanity-check volumes and the direction of pricing. These examples are not exhaustive, and additional public and paid sources were also referenced for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was carried out with a mix of kit manufacturers, distributors, hospital and clinic stakeholders, and diagnostic center buyers, so we could test what we saw in desk research and close information gaps. Because this is a global market, we also checked assumptions across APAC, EMEA, and the Americas to reflect differences in disease burden, point-of-care testing access, and procurement cycles.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 17% | APAC: 37% |

| Mid tier: 45% | Functional/Unit leaders: 24% | EMEA: 36% |

| Smaller Players: 17% | Managers: 59% | Americas: 27% |

Market-Sizing & Forecasting

Our sizing starts with a top-down demand pool build that ties rapid testing to healthcare delivery realities, then it is pressure-tested with selective bottom-up approximations such as sampled ASP multiplied by implied testing volumes in key use settings. For this market, the model is mainly guided by variables like infectious disease incidence signals, testing frequency assumptions in hospitals and clinics, growth in homecare testing uptake, the mix shift between lateral flow and other rapid technologies, and average selling price movement by kit category.

Where public data does not spell out kit volumes cleanly, gaps are handled using bounded ranges that are then narrowed using interview feedback on typical reorder rates, channel markups, and procurement seasonality. Forecasts are built using scenario analysis, since outbreaks, regulatory actions, and reimbursement changes can shift the demand curve in short cycles. Scenario weights are then aligned to expert consensus gathered during primary discussions.

Data Validation & Update Cycle

Validation is done through triangulation across multiple signals, so totals are compared against independent indicators like healthcare spend direction, regulatory approval cadence, and trade movement in relevant kit categories. Outliers are flagged early, and the assumptions behind them are reviewed in a second pass before the numbers are signed off.

Reports are refreshed annually, and interim updates are triggered when material events occur, such as large policy changes, major outbreaks, or sudden pricing shifts that show up in channel checks. Before delivery, an analyst runs a fresh review pass so clients receive the latest updated view rather than an older locked version.

Mordor Intelligence's Rapid Diagnostic Kits Market Estimate Compared With Other Published Estimates

Published market sizes for rapid diagnostic kits can look far apart even when they describe similar use cases, because the counted items and the pricing basis are not always the same. Differences typically come from what is treated as a kit versus a broader rapid diagnostics bundle, how home testing is counted, and whether values are captured at manufacturer level or closer to retail.

The benchmark table shows a wide spread that is largely explained by scope and revenue recognition choices. In Mordor Intelligence's model, value is focused on rapid diagnostic kits across key technologies and end users, rather than folding in adjacent items like instruments, software, and broader point-of-care service revenues. Some published figures also use different base years or longer forecast horizons, and currency conversion timing and ASP progression assumptions can shift the current-year value.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 25.16 B (2026) | |

| Global Consultancy A | USD 32.01 B (2024) | Uses a broader rapid diagnostics frame that can include kits plus related product types and associated service revenues, which typically pushes the total above a kits-only view, and it is anchored to a different base year. |

| Industry Research Group B | USD 32.70 B (2024) | Positions the market as rapid medical diagnostic kits with wide category coverage, and the public summary does not clarify how pricing is treated across channels, which can inflate values when retail-level pricing is mixed with manufacturer pricing. |

Taken together, the table suggests that scope clarity is the biggest lever, followed by pricing basis and the chosen starting year. By tying the total to observable demand indicators and then checking the result with practical supplier and channel inputs, the estimate stays more traceable and easier to replicate when assumptions are updated.

Key Questions Answered in the Report

What is the current size of the rapid diagnostics kits market?

The rapid diagnostics kits market size reached USD 25.16 billion in 2026 and is projected to rise to USD 37.42 billion by 2031 at an 8.27% CAGR.

Which technology holds the largest share of the rapid diagnostics kits market?

Lateral flow immunoassay led with 42.21% market share in 2025, thanks to low cost and ease of use.

Why is Asia-Pacific the fastest-growing regional market?

Government healthcare investment, domestic manufacturing incentives, and expanded telemedicine programs give Asia-Pacific an 10.74% CAGR forecast through 2031.

What are the main restraints on market growth?

Supply-chain fragility for critical reagents and regulatory uncertainty surrounding home-use multiplex kits are the leading constraints, together shaving 2.2 percentage points off forecast CAGR.

How are AI-enabled readers improving diagnostic accuracy?

Machine-learning algorithms analyze faint visual or optical signals, reduce operator variation, and extend detection range, making rapid tests more reliable in decentralized settings.

Which end-user channel is expanding fastest?

Home-care settings show the quickest rise with an 8.55% CAGR, fueled by consumer demand for self-testing and insurer support for remote monitoring.

Page last updated on: