Paper Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 20.63 Billion |

| Market Size (2031) | USD 27.92 Billion |

| Growth Rate (2026 - 2031) | 6.24 % CAGR |

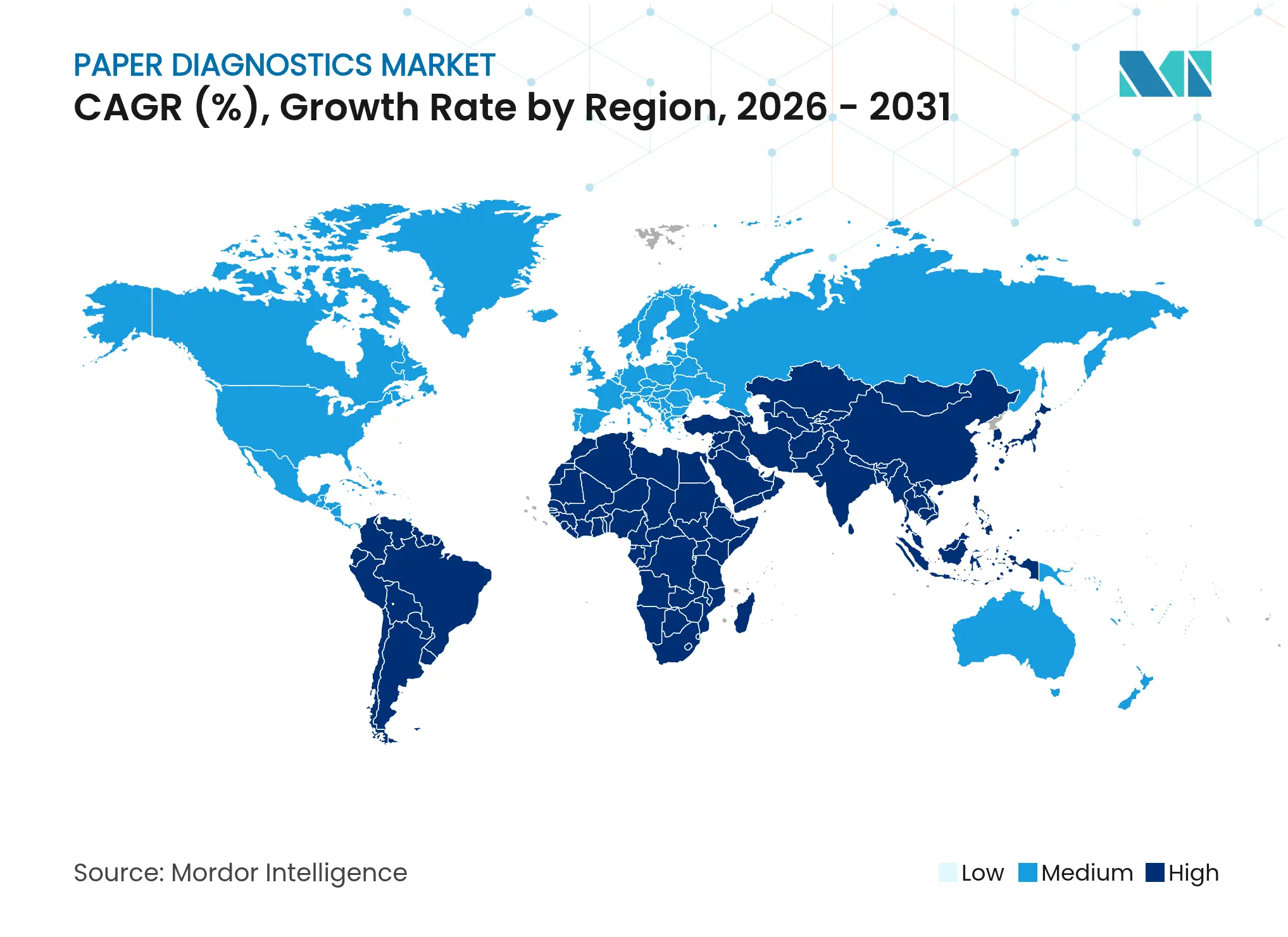

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Paper Diagnostics Market Analysis by Mordor Intelligence

The paper diagnostics market size was valued at USD 19.42 billion in 2025 and estimated to grow from USD 20.63 billion in 2026 to reach USD 27.92 billion by 2031, at a CAGR of 6.24% during the forecast period (2026-2031). The progression signals the sector’s successful pivot from pandemic-era volume toward longer-term demand built on public health investments and technology upgrades. Growth momentum comes from the rollout of CRISPR-enabled paper microfluidics that lift analytical sensitivity above traditional lateral flow formats, the spread of artificial-intelligence-guided point-of-care testing, and sustained funding for genomic surveillance programs in low- and middle-income countries. Asia-Pacific leads in expansion pace while North America continues to anchor early adoption, supported by clear regulatory pathways and entrenched supplier relationships. Competitive intensity stays moderate; large firms preserve scale advantages yet face rising niche entrants that apply specialty optics, cellulose engineering, and smartphone analytics to capture emerging use cases.

Key Report Takeaways

- By product category, lateral flow assays held 60.92% of 2025 revenue, whereas paper-based microfluidics are projected to compound at 9.58% through 2031.

- By type, diagnostic devices commanded 69.05% share of the paper diagnostics market size in 2025, while monitoring devices are on track for a 10.18% CAGR to 2031.

- By sample type, blood testing accounted for 45.84% of the paper diagnostics market share in 2025; saliva-based platforms exhibit an 8.86% CAGR over 2026-2031.

- By technology, colorimetric assays led with 56.10% share in 2025, and SERS-enhanced assays are expected to expand at 9.34% CAGR.

- By application, clinical diagnostics delivered 48.18% of segment revenue in 2025; environmental monitoring is the fastest-growing application at 9.98% CAGR.

- By end user, hospitals and clinics controlled 52.94% of 2025 demand, while home healthcare solutions record a 10.52% CAGR through 2031.

- By geography, North America contributed 31.88% of 2025 sales, whereas Asia-Pacific exhibits the highest regional CAGR of 8.81% during the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Paper Diagnostics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Burden of infectious and chronic

diseases

Burden of infectious and chronic

diseases

| +1.8% | Global focus on Sub-Saharan Africa and South Asia | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

+1.8%

|

Geographic Relevance

:

Global focus on Sub-Saharan Africa

and South Asia

|

Impact Timeline

:

Long term (≥ 4 years)

|

Demand for low-cost POC testing

Demand for low-cost POC testing

| +1.2% | Asia-Pacific core, spill-over to Latin America and MEA | Medium term (2-4 years) | |||

Government and NGO surveillance

funding

Government and NGO surveillance

funding

| +0.9% | Worldwide, priority in LMICs | Medium term (2-4 years) | |||

CRISPR-enabled paper microfluidics

CRISPR-enabled paper microfluidics

| +0.7% | North America and EU, expanding to Asia-Pacific | Long term (≥ 4 years) | |||

Biodegradable biosensors and plastic

bans

Biodegradable biosensors and plastic

bans

| +0.5% | EU primary, North America secondary | Medium term (2-4 years) | |||

Anti-counterfeit drug-quality

testing

Anti-counterfeit drug-quality

testing

| +0.4% | Global pharmaceutical supply chains | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Burden of Infectious & Chronic Diseases

Global morbidity tied to infectious agents and non-communicable conditions continues to underpin adoption of paper diagnostics. WHO channelled USD 2 million to ten surveillance projects in 2024, demonstrating institutional faith in scalable, paper-based platforms for field epidemiology.[1]World Health Organization, “International Pathogen Surveillance Network Announces First Recipients of Grants,” WHO, who.intWastewater tracking among refugee settlements and point-of-care HbA1c screening in urban China show the format’s ability to serve both outbreak control and chronic care at sustainable cost levels.[2]Shao Q. et al., “Point-of-Care Testing HbA1c Screening for Type 2 Diabetes in Urban and Rural China,” Frontiers in Public Health, frontiersin.org Saliva testing for viral infections now equals blood-based sensitivity while improving patient acceptance, further broadening deployment scenarios.

Demand for Low-Cost POC Testing

Hospitals and payors prioritize decentralized diagnostics that cut lab queues and deliver rapid answers in community settings. Smartphone-linked fluorescence readers processing 20 μL samples in 30 minutes illustrate how consumer electronics shrink instrumentation budgets.[3]Chonghui Yang et al., “Low-Cost Microfluidic Biomarker Detection on a Smartphone,” PubMed, pubmed.ncbi.nlm.nih.gov China’s willingness-to-pay analyses confirm that instant HbA1c results fall well below national ICER thresholds, validating economic rationale for widespread rollout. United States home-testing growth underscores consumer appetite for convenience, pushing suppliers to refine kit usability and logistics.

Government & NGO Surveillance Funding

Multilateral grants strengthen laboratory networks and reserve procurement for rapid paper platforms. The US CDC awarded WHO USD 20 million in 2024 as part of a five-year, USD 100 million plan dedicated to high-quality field detection tools. In Laos, avian-flu tracing with paper strips shows how grant-funded diagnostics leapfrog infrastructure gaps, while Chembio Diagnostics attracted foundation support to accelerate tropical disease tests.

CRISPR-Enabled Paper Microfluidics

CRISPR-Cas13a assays embedded on cellulose reach 14.4 copies/mL sensitivity, rivaling lab PCR without bulky hardware. Multiplex panels targeting 23 pathogens achieve same-visit answers in under 30 minutes and can be rapidly re-programmed for new threats. Rolling circle amplification coupled with Cas12a gains attomolar limits within half an hour, broadening use for metabolic biomarkers.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Non-harmonized regulatory standards

Non-harmonized regulatory standards

| -0.8% | Global, strongest in emerging markets | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

-0.8%

|

Geographic Relevance

:

Global, strongest in emerging

markets

|

Impact Timeline

:

Medium term (2-4 years)

|

Sensitivity limits for multiplex

assays

Sensitivity limits for multiplex

assays

| -0.6% | Global clinical settings | Long term (≥ 4 years) | |||

Specialty cellulose supply

volatility

Specialty cellulose supply

volatility

| -0.4% | Worldwide, Nordic supply hubs | Short term (≤ 2 years) | |||

IP fragmentation and licensing

hurdles

IP fragmentation and licensing

hurdles

| -0.3% | North America and EU innovation clusters | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Non-Harmonized Regulatory Standards

Divergent rules create duplicated testing and higher compliance bills. The FDA Laboratory Developed Tests final rule could cost laboratories up to USD 3.56 billion per year, concentrating volume with firms that sustain large quality-assurance budgets. Europe’s Medical Device Regulation extensions reduce immediate disruption yet prolong uncertainty for mid-sized manufacturers. Asian regulators pursue alignment yet retain country-specific filings that slow simultaneous launches.

Sensitivity Limits for Multiplex Assays

Paper formats struggle when many low-abundance targets must be read on one strip. CRISPR-based respiratory panels reached full concordance for common viruses yet showed drop-offs when viral load dipped below detection thresholds. Chemical enhancement can lift signals but adds cost and workflow complexity, curbing uptake outside specialized labs.

Segment Analysis

By Product: Microfluidics Drive Innovation Beyond Traditional Assays

Lateral flow assays captured 60.92% of 2025 revenue, underlining their maturity within the paper diagnostics market. Paper-based microfluidics now post a 9.58% CAGR, reflecting clinician demand for multi-step processing on a single slip without added equipment. Roll-to-roll nanoimprint lithography scales chip output while keeping per-test costs competitive, supporting volume programs in infectious disease and food safety. Dipsticks still serve high-throughput screening where qualitative results suffice, particularly in urinalysis and pesticide detection.

Advances in nitrocellulose-cotton composites reduce reagent bleed and raise wicking speed, bringing hybrid membranes in line with commercial standards while cutting reliance on synthetic plastics. Optoelectronic microfluidic rigs that read blood plasma viscosity in 3 minutes widen application reach into cardiovascular risk triage. The integration of CRISPR readers onto microfluidic paper further positions the format as a reconfigurable platform for pathogen-agnostic panels.

Note: Segment shares of all individual segments available upon report purchase

By Type: Monitoring Devices Capitalize on Chronic Disease Management

Diagnostic devices retained 69.05% share in 2025 on strength of established clinical protocols and reimbursement pathways. Monitoring devices, advancing at 10.18% CAGR, respond to chronic disease prevalence and the shift to home-based care. Remote HbA1c cassette readers and electrical-sensing blood analyzers support physician-supervised self-testing programs that ease outpatient workloads.

Smartphone connectivity lets monitoring devices stream data to cloud dashboards, enabling care teams to adjust medication without in-person visits. Diagnostic devices hold regulatory advantages but must evolve toward automated sample handling and multiplex capability to counter rising household kits. Convergence of telehealth services with paper sensors further elevates monitoring solutions in regions facing clinician shortages.

By Sample Type: Saliva Testing Gains Clinical Acceptance

Blood remained the dominant matrix at 45.84% of 2025 sales, upheld by broad biomarker validation. Saliva testing, growing at 8.86% CAGR, benefits from painless collection and lower infection risk during outbreaks. Clinical studies now confirm saliva assays can equal plasma sensitivity for many viral and hormonal markers, making them attractive for mass screening in schools and worksites.

Urine dipsticks stay popular for pregnancy and narcotics tests due to established cut-offs and regulatory familiarity. Stool diagnostics gain traction in colorectal cancer programs using paper-based immunochemical cards mailed to patients. Emerging matrices such as exhaled breath condensate are under evaluation but require stability improvements before commercial rollout.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Technology: SERS Enhancement Transforms Optical Detection

Colorimetric readouts maintained 56.10% share in 2025 through low equipment needs and long heritage. Surface-enhanced Raman spectroscopy systems integrate nano-gold islands onto cellulose, lifting limit of detection close to lab PCR and propelling a 9.34% CAGR. Fluorescence assays profit from LED cost decline, while electrochemical sensors carve space in cardiometabolic monitoring for exact quantitation.

CRISPR-integrated paper strips sit in the “others” category yet command high strategic value for next-wave panels that multiplex dozens of pathogens on one ticket. Manufacturers balance performance gains against added reagent complexity and the need for robust mobile phone analytics in field use.

By Application: Environmental Monitoring Emerges as Growth Driver

Clinical diagnostics still generated 48.18% of turnover in 2025, but environmental monitoring outpaces with a 9.98% CAGR. Governments raise water-quality enforcement, prompting utilities to add microfluidic paper kits for on-site heavy-metal and microbial checks. AI-enabled platforms pair sensor results with geolocation data to model pollution plumes in real time.

Food safety programs deploy paper diagnostics to screen for Salmonella, aflatoxins, and pesticide residues at processing lines, shortening recall windows. Liver disorder panels leveraging enhanced fibrosis scores demonstrate the format’s move into chronic disease staging within gastroenterology clinics.

Note: Segment shares of all individual segments available upon report purchase

By End User: Home Healthcare Transforms Patient Management

Hospitals and clinics contributed 52.94% of purchases in 2025, yet home healthcare exhibits the fastest growth at 10.52% CAGR as aging populations seek convenient chronic-care solutions. Insurers endorse home-based test packs that lower readmission rates and flag complications earlier. Diagnostic centers invest in automation to preserve throughput but face competition from point-of-care kits that bypass centralized labs.

Retail pharmacies and workplace wellness programs emerge as supplementary channels offering preventive screens during daily errands, widening consumer touchpoints and normalizing at-home sampling kits.

Geography Analysis

North America supplied 31.88% of 2025 revenue owing to robust reimbursement networks, established supplier frameworks, and early adoption of CRISPR-enabled formats. National contingency plans call for pre-event contracts with paper test makers to secure surge capacity, anchoring demand during public-health emergencies. Canadian modernization funding and Mexican cross-border manufacturing further reinforce regional supply integrity.

Europe pursues balanced expansion as regulatory harmonization coexists with strong sustainability drivers. The impending Packaging Waste Regulation encourages healthcare buyers to favor cellulose substrates, and digital instruction mandates simplify compliance paperwork, accelerating timetable to clinic shelves. Research clusters in Germany, the United Kingdom, and France pilot biodegradable sensors, while Eastern members leverage EU cohesion funds to upgrade diagnostic networks.

Asia-Pacific represents the fastest-growing territory at 8.81% CAGR, propelled by China’s point-of-care reimbursement reforms and India’s Make-in-India incentives that crowd in local manufacturing capacity. Japan’s regulatory sandbox fosters AI-linked diagnostics, and Australia partners with Korean institutes on cellulose membrane research. Southeast Asian nations receive WHO and CDC grants to bolster surveillance, positioning paper diagnostics as a first-line tool in remote provinces.

Emerging uptake in Middle East & Africa and South America is tied to multilateral development loans earmarked for primary care infrastructure. Progress depends on regulatory capacity building and supply-chain resilience to guard against pulp price swings that hamper kit affordability.

Competitive Landscape

Market Concentration

The paper diagnostics market shows moderate concentration shaped by the interplay of global incumbents and specialist challengers. Abbott’s diagnostics revenue slipped 7.2% in Q1 2025 as post-pandemic testing volumes normalized, prompting shifts toward core lab automation and portable immunoassay platforms. Siemens Healthineers posted 1.6% growth in the same period, aided by efficiency programs and broader geographic spread.

Acquisitions remain a favored path to technology infusion; bioMérieux’s purchase of SpinChip Diagnostics adds a 10-minute whole-blood immunoassay platform and underscores the premium placed on time-critical acute-care tools. Start-ups such as BugSeq secure BARDA funding for AI-assisted metagenomic reporting, signaling government backing for next-generation, pathogen-agnostic workflows.

Smaller players navigate financing hurdles, illustrated by Chembio Diagnostics’ going-concern warnings even as it gains philanthropic support for tropical-disease projects. Market leaders expand automated roll-to-roll fabrication to defend cost positions, while entrants differentiate through niche optics, specialty cellulose, and integrated mobile apps aimed at underserved testing needs.

Paper Diagnostics Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Trividia Health TRUE METRIX blood glucose systems became preferred on all Medicaid plans in Pennsylvania.

- February 2025: CellMade launched a comprehensive mycotoxin testing suite combining ELISA, rapid strips, and reference materials.

- January 2025: bioMérieux acquired SpinChip Diagnostics, adding a 10-minute immunoassay platform for acute-care blood tests.

Table of Contents for Paper Diagnostics Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Burden Of Infectious & Chronic Diseases

- 4.2.2Demand For Low-Cost POC Testing

- 4.2.3Government & NGO Surveillance Funding

- 4.2.4CRISPR-Enabled Paper Microfluidics

- 4.2.5Biodegradable Biosensors & Plastic Bans

- 4.2.6Anti-Counterfeit Drug-Quality Testing

- 4.3Market Restraints

- 4.3.1Non-Harmonized Regulatory Standards

- 4.3.2Sensitivity Limits For Multiplex Assays

- 4.3.3Specialty Cellulose Supply Volatility

- 4.3.4IP Fragmentation & Licensing Hurdles

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technology Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size and Growth Forecasts (Value-USD)

- 5.1By Product

- 5.1.1Lateral Flow Assays

- 5.1.2Dipsticks

- 5.1.3Paper-based Microfluidics

- 5.2By Type

- 5.2.1Monitoring Devices

- 5.2.2Diagnostic Devices

- 5.3By Sample Type

- 5.3.1Blood

- 5.3.2Urine

- 5.3.3Saliva

- 5.3.4Stool

- 5.3.5Others

- 5.4By Technology

- 5.4.1Colorimetric Assays

- 5.4.2Fluorescence-based Assays

- 5.4.3Electrochemical Sensors

- 5.4.4SERS-enhanced Assays

- 5.4.5Others

- 5.5By Application

- 5.5.1Clinical Diagnostics

- 5.5.1.1Cancer

- 5.5.1.2Infectious Diseases

- 5.5.1.3Liver Disorders

- 5.5.1.4Others

- 5.5.2Food Quality Testing

- 5.5.3Environmental Monitoring

- 5.6By End User

- 5.6.1Hospitals & Clinics

- 5.6.2Diagnostic Centers

- 5.6.3Home Healthcare

- 5.6.4Others

- 5.7By Geography

- 5.7.1North America

- 5.7.1.1United States

- 5.7.1.2Canada

- 5.7.1.3Mexico

- 5.7.2Europe

- 5.7.2.1Germany

- 5.7.2.2United Kingdom

- 5.7.2.3France

- 5.7.2.4Italy

- 5.7.2.5Spain

- 5.7.2.6Rest of Europe

- 5.7.3Asia-Pacific

- 5.7.3.1China

- 5.7.3.2Japan

- 5.7.3.3India

- 5.7.3.4Australia

- 5.7.3.5South Korea

- 5.7.3.6Rest of Asia-Pacific

- 5.7.4Middle East and Africa

- 5.7.4.1GCC

- 5.7.4.2South Africa

- 5.7.4.3Rest of Middle East and Africa

- 5.7.5South America

- 5.7.5.1Brazil

- 5.7.5.2Argentina

- 5.7.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1Abbott Laboratories

- 6.3.2Siemens Healthineers AG

- 6.3.3Bio-Rad Laboratories Inc.

- 6.3.4ACON Laboratories Inc.

- 6.3.5Chembio Diagnostic Systems Inc.

- 6.3.6Arkray Inc.

- 6.3.7Abcam plc

- 6.3.8Creative Diagnostics

- 6.3.9Micro Essential Laboratories Inc.

- 6.3.10R-Biopharm AG

- 6.3.11Danaher

- 6.3.12OraSure Technologies Inc.

- 6.3.13QuidelOrtho Corp.

- 6.3.14F. Hoffmann-La Roche Ltd.

- 6.3.15Qiagen NV

- 6.3.16Eiken Chemical Co.

- 6.3.17NG Biotech

- 6.3.18Lumos Diagnostics

- 6.3.19Truelab-Molbio

- 6.3.20Fujifilm Wako

- 6.3.21Chongqing Biospes Co.

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global Paper Diagnostics Market Report Scope

As per the report's scope, paper diagnostics are devices made of paper and cellulosic materials that recognize and quantify biomolecules and chemical agents that affect health. This technology was developed as a revolutionary point-of-care approach to employing high-performance, cheap, and disposable electronics to improve the quality of inexpensive tests, especially in remote settings where digitalization is minimal.

The paper diagnostics market is segmented by product, type, application, end user, and geography. The product segment is further divided into lateral flow assays, dipsticks, and paper-based microfluidics. The type segment is further divided into monitoring devices and diagnostic devices. The application segment is further divided into clinical diagnostics, food quality testing, and environmental monitoring. By end user, the market is further divided into hospitals and clinics, diagnostic centers, home healthcare, and others. The geography segment is further divided into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (USD) for all the above segments.