Transplant Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

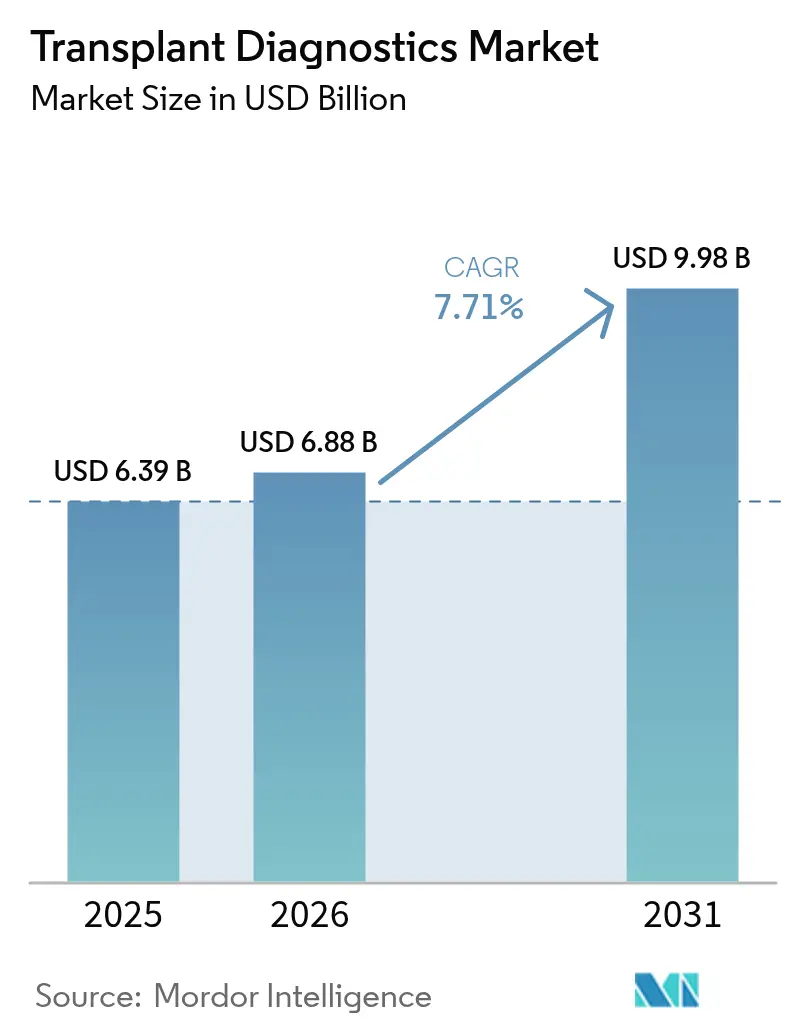

| Market Size (2026) | USD 6.88 Billion |

| Market Size (2031) | USD 9.98 Billion |

| Growth Rate (2026 - 2031) | 7.71% CAGR |

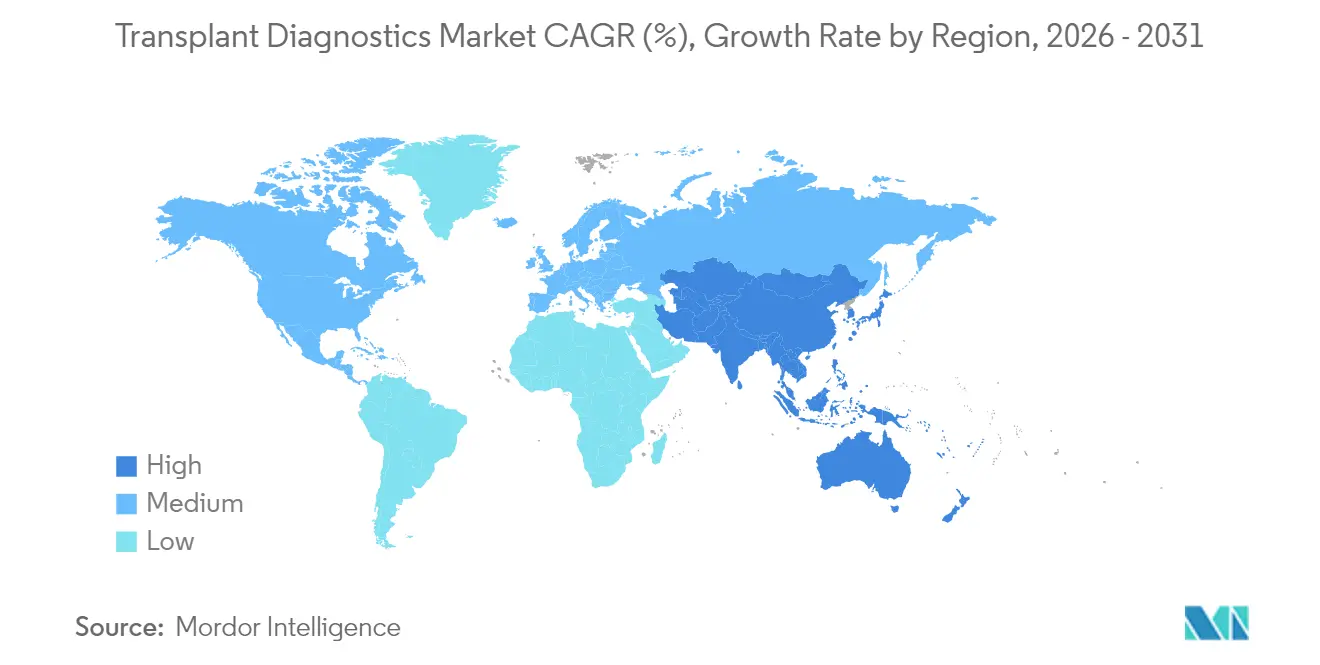

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Transplant Diagnostics Market Analysis by Mordor Intelligence

Transplant diagnostics market size in 2026 is estimated at USD 6.88 billion, growing from 2025 value of USD 6.39 billion with 2031 projections showing USD 9.98 billion, growing at 7.71% CAGR over 2026-2031. Robust transplant volumes, rapid NGS adoption, AI-driven decision support, and payer recognition of precision medicine collectively sustain double-digit revenue momentum across major laboratories and kit suppliers. High-resolution HLA sequencing delivers decisive gains in turnaround times and allelic resolution, encouraging pay-per-use procurement models that lower capital barriers for smaller programs. Reagent pull-through remains strong because NGS workflows require validated library kits, while predictive dd-cfDNA surveillance is displacing invasive biopsies in routine follow-up. Competitive intensity is rising as diagnostics majors and transplant-focused specialists race to integrate analytics, automation, and digital pathology into unified offerings.

Key Report Takeaways

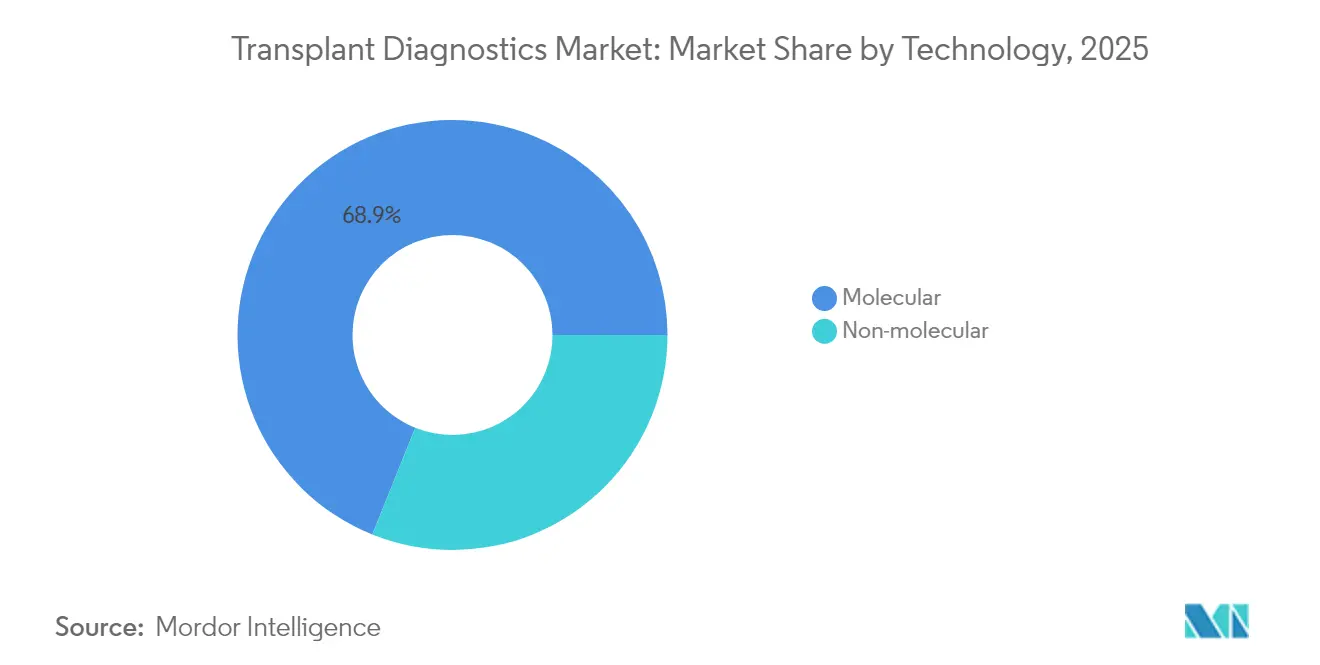

- By technology, molecular platforms led with 68.92% of transplant diagnostics market share in 2025.

- By product, reagents and consumables accounted for 64.93% revenue in 2025; software and analytics is expanding at a 13.58% CAGR through 2031.

- By transplant type, solid organs held 76.12% share in 2025 while stem cell procedures are growing at 10.29% CAGR.

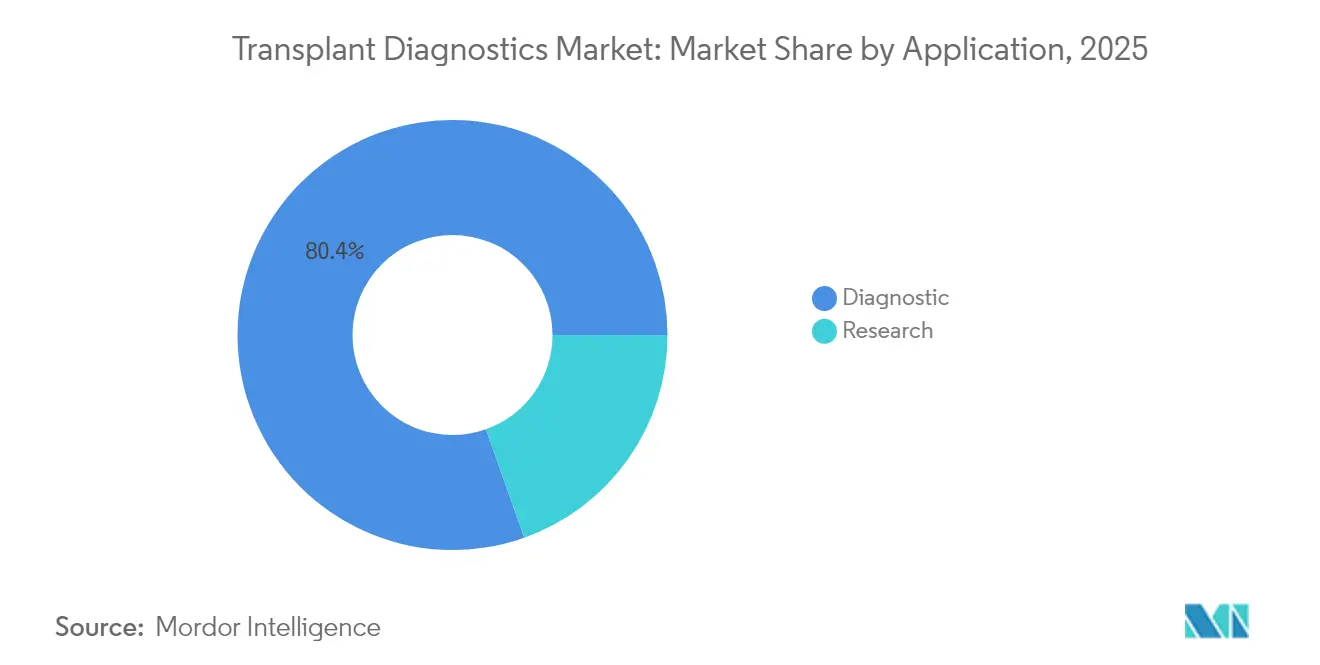

- By application, diagnostic segment accounted for 80.42% of 2025 revenue; research segment is forecast to rise at an 11.34% CAGR to 2031.

- By end user, hospitals and transplant centers captured 54.48% revenue in 2025; academic and research institutes post the quickest gains at 12.28% CAGR.

- By geography, North America dominated with 42.42% share in 2025, while Asia-Pacific advances at 11.36% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Transplant Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Transplant Volumes (Solid-Organ & Cell Therapy) | +2.1% | Global, with strongest impact in North America & Asia-Pacific | Medium term (2-4 years) |

| Shift To NGS-Based HLA & Ccfdna Surveillance | +1.8% | Global, led by North America & Europe | Short term (≤ 2 years) |

| Reagent Rental + Pay-Per-Use Pricing By Vendors | +0.9% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| AI-Assisted Histocompatibility Matching | +1.2% | Global, with early adoption in North America | Long term (≥ 4 years) |

| 3-D Printed Micro-Organs As Reference Controls | +0.4% | North America & Europe, research-focused | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Transplant Volumes (Solid Organ & Cell Therapy)

US hospitals performed 48,000-plus organ transplants in 2024, a 3.3% rise that mirrors broader global gains. Donation-after-circulatory-death grafts now contribute 36% of deceased-donor procedures, expanding the recipient pool. Parallel momentum in hematopoietic stem-cell transplants is linked to high-resolution HLA typing that validates partially mismatched donors, especially benefitting ethnically diverse patients. Continuous distribution for lungs has already lifted transplant rates 16% within 12 months[1]Organ Procurement and Transplantation Network, “Organ Transplants Exceeded 48,000 in 2024,” optn.transplant.hrsa.gov. Each increment in procedure volume converts into higher demand for compatibility assays, post-operative monitoring, and longitudinal rejection surveillance. Consequently, the transplant diagnostics market records sustained reagent pull-through and greater installed-base utilization.

Shift to NGS-Based HLA & dd-cfDNA Surveillance

NGS platforms provide simultaneous high-resolution typing of multiple HLA loci via sample barcoding, boosting throughput while cutting cost per allele. dd-cfDNA assays now flag graft injury earlier than histology, with hazard ratios of 2.56 for elevated signals in heart recipients. National payers increasingly recognize the downstream savings from fewer biopsy complications, accelerating reimbursement approvals. Laboratories gain flexibility through reagent-rental contracts that bundle sequencers, software, and consumables into predictable per-sample fees, propelling wider NGS adoption across mid-tier centers.

AI-Assisted Histocompatibility Matching

Machine-learning algorithms outperform conventional scoring in predicting cellular rejection, achieving 98% donor-recipient matching accuracy in kidney cohorts. Cardiac biopsy image classifiers covering 2,900 patients deliver higher diagnostic precision than manual review methods. Platforms such as Smart Match integrate IoT telemetry with predictive analytics to update allocation decisions in real time. AI integration embeds software subscriptions into every assay order, opening recurring revenue channels and reinforcing vendor lock-in across the transplant diagnostics market.

Reagent-Rental & Pay-Per-Use Pricing

Lower upfront capital encourages smaller centers to adopt advanced assays. Vendors replicate gene-therapy subscription models by bundling consumables, service, and analytics into flat monthly fees for unlimited tests. This arrangement smooths budget spikes and ensures reagent certainty during surge periods. As laboratories scale test menus, per-sample economics improve, making precision diagnostics accessible beyond top-tier institutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Assay Costs & Capital Outlay | -1.4% | Global, particularly affecting emerging markets | Short term (≤ 2 years) |

| Patchwork Global Reimbursement | -1.1% | Global, with varying regional impact | Medium term (2-4 years) |

| Data-Privacy Hurdles In Cross-Border Registries | -0.7% | Europe & Asia-Pacific primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Assay Costs & Capital Outlay

Comprehensive NGS systems can exceed USD 500,000 before validation, while premium reagents reach USD 400 per sample aruplab.com. FDA oversight of Laboratory-Developed Tests adds compliance expenditures near USD 1.29 billion over 10 years[2]Food and Drug Administration, “Laboratory-Developed Tests Regulatory Impact Analysis,” fda.gov. Laboratories with limited throughput struggle to amortize these expenses, prompting consolidation toward high-volume reference centers. Cost pressure also affects dd-cfDNA assays where payer fee schedules lag analytical complexity, delaying widespread roll-out in low-income settings.

Patchwork Global Reimbursement

Medicare’s adjudication of AlloSure and AlloMap underscored how coverage swings can reset demand trajectories overnight. Europe requires multi-year clinical dossiers for new tests, extending market entry timelines and raising evidence-generation costs. GDPR restrictions have already reduced registry-based studies by 46.9%, slowing biomarker validation that underpins reimbursement submissions. These discrepancies fragment the global commercial roadmap and inhibit uniform scaling of transplant diagnostics market offerings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Molecular Platforms Extend Dominance

Molecular assays captured 68.92% of transplant diagnostics market share in 2025 owing to unrivaled allelic resolution and multiplex capacity. The segment’s 7.63% CAGR through 2031 benefits from lab automation that consolidates extraction, library prep, and sequencing on unified decks, shortening hands-on time. Complementary non-molecular tests such as flow-cytometric crossmatch remain indispensable for urgent deceased-donor allocation, growing 12.02% CAGR on specialized use cases.

Platform enhancements now merge NGS reads with AI-based imputation to reconcile ambiguous alleles, raising call confidence in under-sequenced regions. dd-cfDNA kits layered on the same sequencers raise reagent consumption per patient episode, lifting the transplant diagnostics market size for molecular workflows. External proficiency programs covering 19 years of benchmarking show genotype concordance steadily increasing, underscoring technology maturity.

By Product: Digital Analytics Accelerates

Reagents and consumables remained the revenue anchor with 64.93% share in 2025 because every NGS run consumes barcoded primers, polymerases, and capture probes. Yet software and analytics is expected to post 13.58% CAGR, expanding the transplant diagnostics market size for digital services as algorithms automate QC, phasing, and clinical reporting.

Cloud-native platforms reduce on-premise infrastructure needs and support real-time variant databases that update with each global allele submission. Instruments shift toward usage-based leases, reallocating capex to operating budgets and dampening hardware growth. Vendors bundle AI licenses with reagent kits, embedding data subscriptions into every assay cycle to capture recurring revenue.

By Transplant Type: Stem Cell Procedures Surge

Solid organ programs represented 76.12% of global revenue in 2025, anchored by kidney and liver caseloads that demand high-frequency monitoring. Stem cell transplantation, however, displays a 10.29% CAGR through 2031 as mismatched unrelated donors achieve survival parity with fully matched sources.

Expanded criteria intensify testing volumes because every partial match requires deeper allelic interrogation plus chimerism surveillance. Xenotransplantation successes, including 10-day pig-liver function without rejection, herald new compatibility assays that will diversify the transplant diagnostics market.

By Application: Research Pipelines Propel Innovation

Clinical diagnostics generated 80.42% of revenue in 2025, encompassing pre-implant typing, virtual crossmatch, and longitudinal rejection monitoring. Research use is rising 11.34% CAGR as bioprinted tissue models, organoids, and extracellular vesicle analytics demand ultra-sensitive sequencing for immune profiling.

Grant-funded projects increasingly purchase multi-omic workflows that integrate single-cell RNA-seq with HLA genotyping. These studies drive incremental consumable demand and incubate biomarkers that eventually transition into clinical panels, continually enlarging the transplant diagnostics market.

By End User: Academic Centers Lead Adoption Curves

Hospitals and dedicated transplant centers retained 54.48% share in 2025 because point-of-care decisions hinge on in-house labs. Academic and research institutes are expanding at 12.28% CAGR as they combine care delivery with precision-medicine trials that require high-complexity assays.

Independent reference labs collect overflow samples and satisfy regulatory complexity for smaller community hospitals, reinforcing consolidation trends. Fully automated “dark labs” running 24/7 with robotic sample loading are emerging at leading institutions, signaling the next productivity leap for the transplant diagnostics market.

Geography Analysis

North America held 42.42% of global revenue in 2025 due to comprehensive Medicare policies, 48,000 transplant procedures, and dense center networks that routinely deploy dd-cfDNA monitoring. Widespread adoption of AI analyzers and early reimbursement decisions support mid-single-digit unit price premiums. FDA regulation of LDTs may pinch smaller facilities, provoking outsourcing to national reference laboratories that command scale efficiencies.

Europe presents mature infrastructure with harmonized quality schemes; however, GDPR limits rare-allele data exchange, complicating multicenter study design and slowing biomarker validation. Health-technology-assessment bodies often request extended clinical outcome data, extending payback periods for vendors. Nonetheless, population aging and rising solid-organ waitlists sustain steady test volumes.

Asia-Pacific registers the fastest expansion at 11.36% CAGR as Japan pioneers gene-edited xenograft readiness and India scales transplant capacity with 85-90% one-year survival benchmarks. Governments invest in local bioprinting and NGS manufacturing to mitigate import dependence, amplifying reagent accessibility. Diverse HLA profiles across large populations further elevate demand for high-resolution genotyping, expanding the transplant diagnostics market.

Competitive Landscape

The sector exhibits moderate concentration with diagnostics conglomerates and transplant-focused specialists tussling for share. Abbott, Roche, and Thermo Fisher leverage multi-segment portfolios to supply instruments, reagents, and informatics bundles that embed them across hospital labs. CareDx and Natera maintain transplant exclusivity, posting 30% revenue growth in 2024 on expanded AlloSure indications and payer wins.

Strategic acquisitions intensify: Werfen purchased Omixon for USD 25 million to widen its NGS franchise, while Quest Diagnostics bought Fresenius kidney-testing assets to increase hospital outreach. Vendors differentiate by coupling consumables with AI dashboards that interpret immunological risk and link directly to electronic health records. Bioinformatics portfolios generate incremental subscription revenue and raise switching costs.

Impending reshuffles loom as Becton Dickinson explores divestiture of its USD 3.4 billion diagnostics arm, potentially enabling niche players to consolidate specialized assay lines. White-space opportunities persist in emerging economies, AI-enhanced personalized immunology, and xenotransplant compatibility testing. Vendors that harmonize sequencing, digital pathology, and predictive analytics within secure cloud frameworks are poised to accelerate share gains across the transplant diagnostics market.

Transplant Diagnostics Industry Leaders

Abbott Laboratories

Biomérieux SA

Qiagen NV

F Hoffman La Roche AG

Bio-Rad Laboratories, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: CareDx launched pediatric AlloSure Heart and kidney-plus-pancreas AlloSure Kidney assays after New York approval, broadening its dd-cfDNA portfolio.

- February 2025: Quest Diagnostics agreed to acquire Fresenius Medical Care kidney-testing assets, reinforcing its transplant diagnostics reach.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the transplant diagnostics market covers revenue earned from reagent kits, instruments, and dedicated software used to type HLA antigens, detect donor-specific antibodies, and track molecular markers before and after solid organ, stem cell, and soft-tissue transplants. Testing carried out in hospital labs, transplant centers, and independent reference laboratories is valued at manufacturer invoice levels.

Scope Exclusion: We exclude therapeutic drugs, organ-preservation devices, and generic molecular tools that are not purpose built for transplant compatibility.

Segmentation Overview

- By Technology

- Molecular

- PCR-based Molecular Assays

- Sequencing-based Molecular Assays

- Non-Molecular

- Molecular

- By Product

- Instruments

- Reagents & Consumables

- Software / Analytics

- By Transplant Type

- Solid Organ

- Stem Cell / Bone Marrow

- Soft Tissue

- By Application

- Diagnostic

- Research

- By End User

- Independent Reference Laboratories

- Hospital & Transplant Centres

- Academic & Research Institutes

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with laboratory directors, transplant immunologists, and procurement managers across North America, Europe, and eight fast-growing Asian markets. Those conversations clarified test-mix shifts, average selling prices, and reimbursement nuances, helping us reconcile data pulled from public sources.

Desk Research

We reviewed high-credibility public databases such as the Global Observatory on Donation and Transplantation, UNOS, Eurotransplant, and China COTDF to map graft volumes. Our team pulled assay approvals from FDA 510(k) and EMA listings, tapped UN Comtrade for reagent shipment trends, and scanned journals like the American Journal of Transplantation for rejection incidence. Company 10-Ks, investor presentations, and reputable press added pricing clues, while D&B Hoovers and Dow Jones Factiva supplemented paywalled financial details. Many additional secondary sources informed gap checks, though they are not all listed here.

Market-Sizing & Forecasting

A top-down build starts with country transplant counts, multiplies them by tests per procedure and blended ASPs, and then layers surveillance testing frequency. Supplier roll-ups and sampled invoices act as our bottom-up cross-check to fine-tune totals. Key variables include graft volume growth, sequencing assay penetration, reagent price erosion, lab accreditation expansion, and turnaround time benchmarks. Five-year forecasts rely on multivariate regression that links those drivers with macro indicators such as health-care spending and private insurance coverage. Regional analogues bridge smaller market gaps before experts re-validate outputs.

Data Validation & Update Cycle

Our analysts run variance scans against historical rejection rates and import data, followed by two peer reviews and a senior audit. We refresh models annually and push interim updates when regulation or reimbursement shifts materially affect inputs.

Why Mordor's Transplant Diagnostics Baseline Commands Reliability

Published estimates often diverge because firms bundle different products, freeze price curves, or refresh models infrequently.

We document scope, update drivers each cycle, and triangulate volumes and ASPs, giving decision makers a balanced baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.39 B (2025) | Mordor Intelligence | - |

| USD 6.39 B (2024) | Global Consultancy A | Broader basket includes routine molecular diagnostics, inflating value |

| USD 7.80 B (2024) | Industry Association B | Uses list prices and ignores 7-10 % annual ASP decline |

| USD 4.40 B (2022) | Global Consultancy C | Base year outdated; transplant growth applied uniformly across regions |

The comparison underscores that when volumes, pricing dynamics, and product scope are consistently framed, Mordor's disciplined approach delivers the most transparent and reproducible market baseline.

Key Questions Answered in the Report

What is the current value of the transplant diagnostics market?

The transplant diagnostics market size is USD 6.88 billion in 2026 and is projected to hit USD 9.98 billion by 2031 at a 7.71% CAGR.

Which technology segment leads revenue?

Molecular assays dominate with 68.92% market share in 2025 due to the clinical precision of next-generation sequencing.

Why are stem cell diagnostics growing faster than solid organ testing?

Expanded HLA matching criteria now validate partially mismatched donors, driving a 10.29% CAGR for stem cell transplant diagnostics.

Which region is expanding the fastest?

Asia-Pacific posts the quickest growth at 11.36% CAGR thanks to rapid transplant program expansion and government investment in precision medicine.

How are vendors lowering capital barriers for smaller centers?

Reagent-rental and pay-per-use models bundle sequencers, consumables, and software into predictable operating fees, enabling mid-tier hospitals to adopt NGS workflows without large upfront purchases.

Page last updated on: