Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.76 Billion |

| Market Size (2031) | USD 17.35 Billion |

| Growth Rate (2026 - 2031) | 12.18% CAGR |

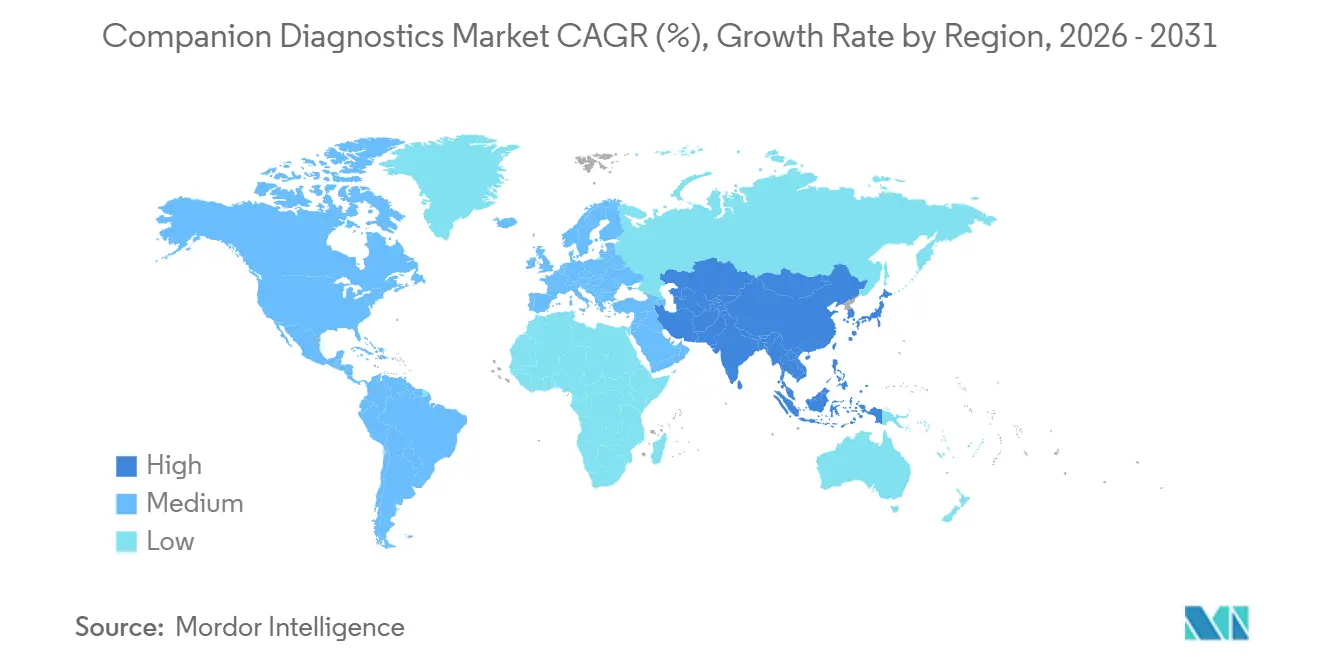

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

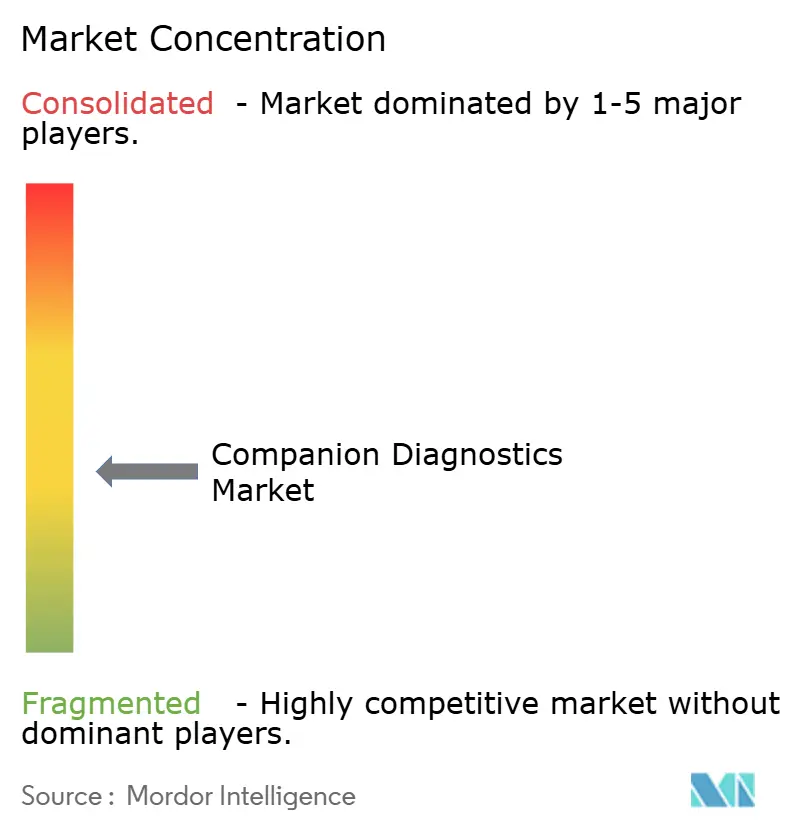

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Companion Diagnostics Market Analysis by Mordor Intelligence

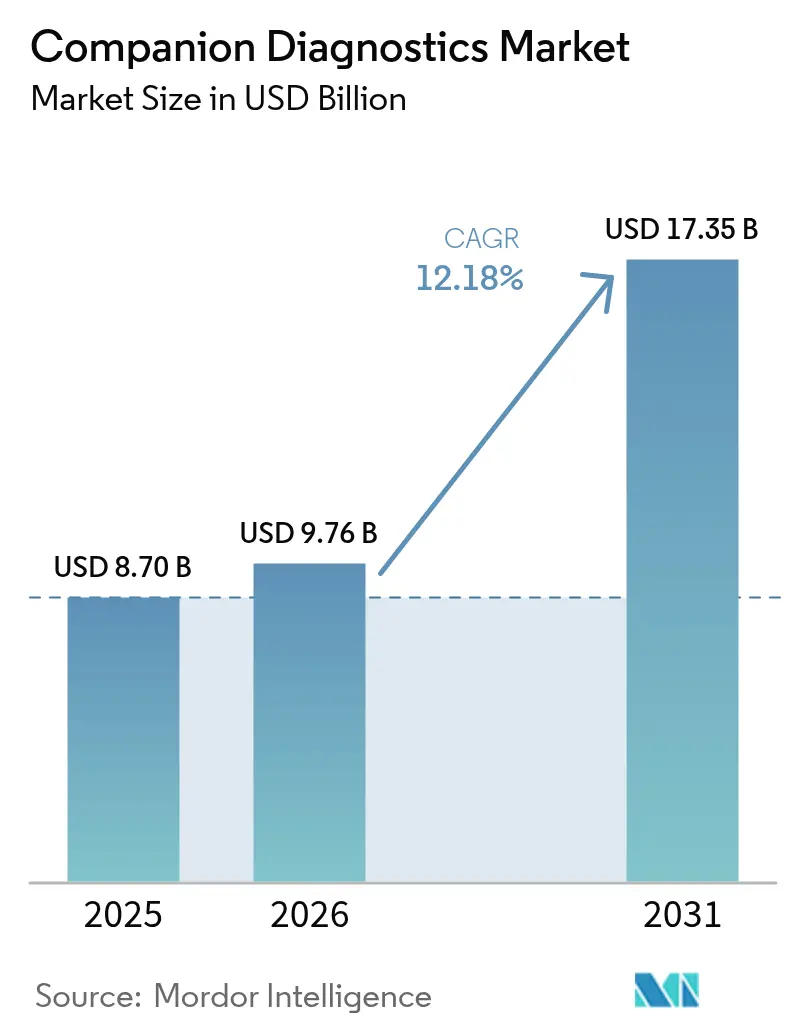

The Companion Diagnostics Market size was valued at USD 8.70 billion in 2025 and estimated to grow from USD 9.76 billion in 2026 to reach USD 17.35 billion by 2031, at a CAGR of 12.18% during the forecast period (2026-2031).

Companion diagnostics integrate molecular testing with targeted therapeutics, aligning diagnostic information with optimal therapy choices. The widening application of precision medicine is simultaneously shifting investment priorities for drug makers and reshaping payer reimbursement models as policy makers recognize diagnostics as pivotal cost-containment tools.

Key Report takeaways

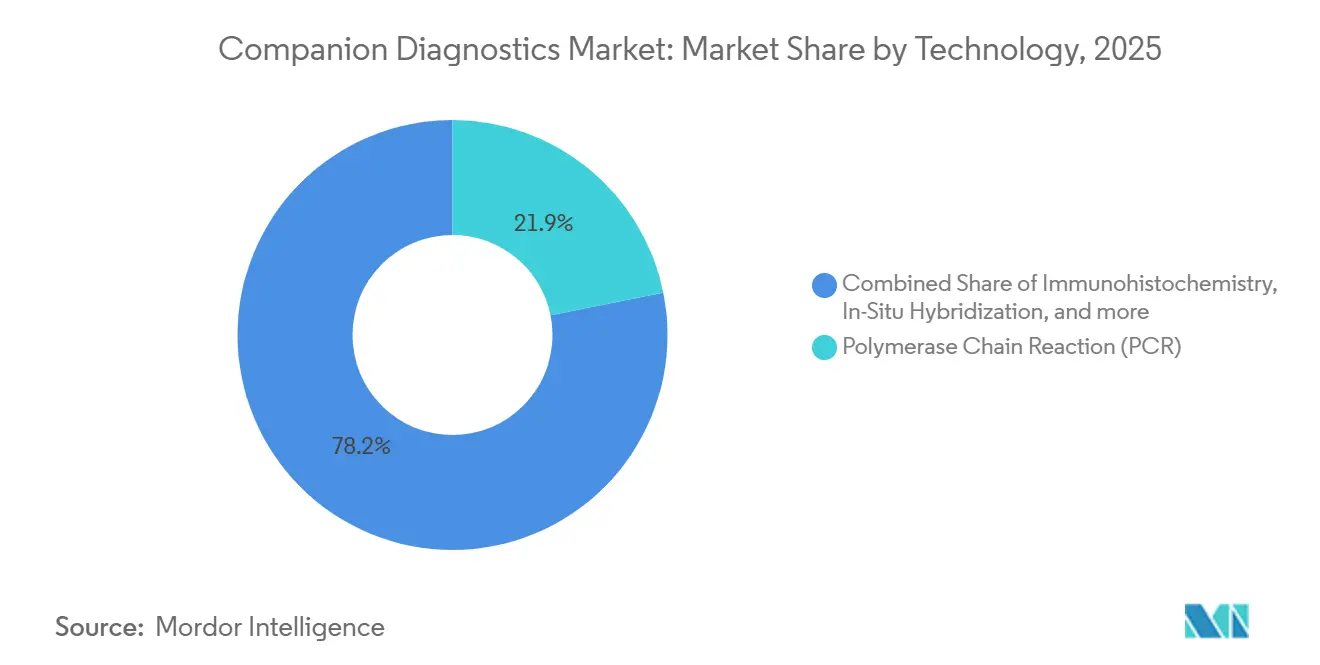

- By technology, PCR still holds the largest 2025 slice at 21.85% market share, whereas companion diagnostics is forecast to outpace PCR-based alternatives, expanding at a 13.85% CAGR between 2026-2031.

- By indication, melanoma is expected to grow with a CAGR of 13.22%, whereas lung cancer held 22.10% share in 2025.

- By product type, assays and kits accounted for 65.75% in 2025, driven by their one-to-one linkage with specific drug launches. However, software-driven interpretive platforms are the fastest-growing product category, with a 15.12% CAGR (2026-2031).

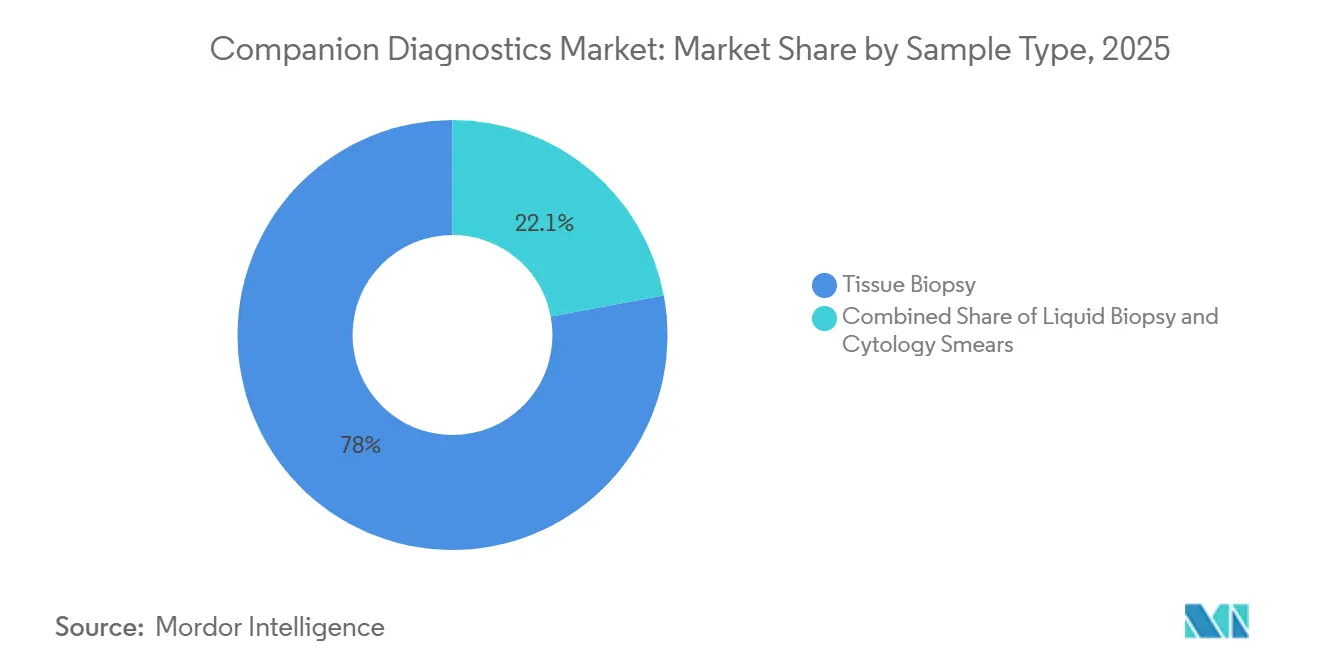

- By sample type, tissue biopsy still accounts for 77.95% of the companion diagnostic market volume in 2025, as confirmatory histology remains the regulatory gold standard. The liquid biopsy market is projected to expand at a 18.22% CAGR through 2031.

- By end user, CROs’ companion diagnostics market size is set to climb 12.85% CAGR (2026-2031) and pharmaceutical & biotechnology companies held 44.60% share in 2025.

- By geography, North America holds 39.95% of the companion diagnostic market share in 2025 and Asia-Pacific is projected to log a 12.45%. CAGR from 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Companion Diagnostics Market Trends and Insights

Driver Impact Analysis*

| Driver | Approximate % Impact on Overall CAGR (2025-2030) | Primary Regions Affected | Impact Timeline |

|---|---|---|---|

| Expansion of precision-medicine drug labels | ~+2.0 % | North America, Europe, Japan | Long term (≥4 years) |

| Rapid uptake of liquid biopsy | ~+1.6 % | Global urban oncology hubs; fastest in Asia-Pacific | Medium term (2-4 years) |

| ADC-focused oncology pipeline requiring multiplex CDx platforms | +0.8% | North America, Europe, Japan | Medium term (2-4 years) |

| Declining NGS cost curve | ~+1.3 % | Community cancer centers in North America and Western Europe | Long term (≥4 years) |

| Payer alignment with FDA-approved tests | ~+1.1 % | United States; spill-over to Canada and GCC | Short term (≤2 years) |

| Integration of AI for variant interpretation | ~+0.7 % | High-throughput reference labs worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Companion Diagnostics Market Trends & Insights Rapid Adoption of Liquid-Biopsy CDx in Oncology Practices

Liquid biopsy companion diagnostics are redefining cancer management by providing a minimally invasive route for repeat testing that captures tumor heterogeneity in real time. Clinicians now track disease evolution through circulating tumor DNA, dynamically adjusting therapy rather than relying on static tissue snapshots. A second-order implication is that hospital laboratories must recalibrate throughput and cold-chain logistics to accommodate larger volumes of blood-based assays, affecting capital-allocation timelines across the entire oncology service line. FoundationOne Liquid CDx, granted multiple FDA approvals in 2024, illustrates the regulatory momentum that is quickening market uptake [1]U.S. Food and Drug Administration – Companion Diagnostics Table . Yet liquid biopsy sensitivity still varies by cancer stage and by tumor shedding biology, meaning providers are pressured to adopt hybrid tissue-plus-blood strategies that preserve diagnostic accuracy while controlling test redundancy.

Advancements in Personalized Medicine and Precision Oncology

Companion diagnostics have moved beyond optional add-ons; they are codified prerequisites for access to many targeted drugs. The FDA lists 168 biomarker–drug pairings linked to approved tests, signaling that reimbursement agencies will progressively withhold payment for therapy courses lacking molecular confirmation. This linkage is steering pharmaceutical companies to co-develop tests earlier in Phase I trials, compressing total program timelines but increasing preclinical complexity. An immediate knock-on effect is that contract research organizations (CROs) are expanding biomarker-validation benches to secure multi-year strategic outsourcing contracts, positioning themselves as de facto molecular gatekeepers for biopharma pipelines.

Technological Innovations in Diagnostic Tools

Next-generation sequencing (NGS) is delivering comprehensive genomic insights in a single workflow, with its segment projected to grow 14.3% between 2025 and 2030. Laboratories are layering artificial-intelligence algorithms onto NGS output to triage the flood of variants, a move that subtly shifts diagnostic labor demand from wet-lab technologists toward data scientists. This workforce rebalancing, inferred from rising bioinformatics job postings, is influencing university curricula and venture-backed start-ups that provide automated annotation engines. Given that lung cancer NGS panels identify actionable mutations in up to 65% of patients, payers are already drafting variable reimbursement tiers linked to the number of clinically actionable findings, foreshadowing value-based pricing models for diagnostics.

Growing Prevalence of Chronic Diseases

Cancer incidence continues to climb, with the American Cancer Society projecting approximately two million new cases in the United States for 2024 [2]European Medicines Agency, “In Vitro Diagnostic Regulation Guidance,” European Medicines Agency, ema.europa.eu. The volume surge forces oncology centers to redesign patient-triage protocols, acknowledging that diagnostic turnaround time now directly influences time-to-treatment and, by extension, quality-metric reimbursements. Pharmaceutical sponsors respond by integrating companion diagnostics earlier to boost trial power, recognizing that enriched populations reduce statistical noise. This dynamic is prompting institutional review boards to update informed-consent language, as patients must now acknowledge that molecular profiling determines therapy eligibility—a subtle yet meaningful shift in autonomy discourse.

Restraint Impact Analysis*

| Restraint | (~) % Drag on Overall CAGR (2025-2030) | Primary Regions Affected | Impact Timeline |

|---|---|---|---|

| High development costs (USD 50-100 million) | ~-1.8 % | Universal; most acute in emerging markets | Long term (≥4 years) |

| IVDR regulatory bottlenecks | ~-1.3 % | European Union | Medium term (2-4 years) |

| Variable assay sensitivity in low-ctDNA tumors | ~-0.9 % | Global; highest impact in early-stage oncology programs | Short term (≤2 years) |

| Inconsistent reimbursement outside major markets | ~-0.8 % | Latin America, parts of ASEAN, Eastern Europe | Long term (≥4 years) |

| Bioinformatics workforce shortage | ~-0.4 % | Rapidly scaling labs in Asia-Pacific and MENA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Development Costs

Developing a companion diagnostic can require USD 50–100 million and 3–5 years, framing diagnostics as long-cycle capital projects. Smaller firms increasingly tie their fortunes to big-pharma alliances, trading equity stakes for developmental funding. The second-order consequence is a consolidation of intellectual-property portfolios: as large companies absorb device rights, freedom-to-operate for newcomers narrows. This tightening IP landscape nudges venture investors to favor platform companies with expandable assay menus rather than single-marker concepts, subtly migrating venture dollars away from niche biomarkers toward scalable informatics-driven solutions, these structural shifts are shaping the companion diagnostic market.

Stringent Regulatory Policies

The European Union’s In Vitro Diagnostic Regulation (IVDR) introduced mandatory notified-body and European Medicines Agency consultations for companion diagnostics in 2022 [3]American Cancer Society, “Cancer Facts & Figures 2024,” American Cancer Society, cancer.org. Because only a handful of bodies are fully designated, review queues are lengthening, compelling firms to divert launch sequencing toward the United States or Japan first. As a ripple effect, European oncologists may experience delayed access to novel tests, raising ethical debates about geographic equity in cancer care. In the United States, the FDA pilot that publicly posts test-performance characteristics has catalyzed transparency but simultaneously exposes under-performing assays, creating reputational risk for diagnostics firms and sharpening buyer scrutiny.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

NGS Disrupts Traditional Testing Paradigms

PCR still owns the largest 2025 slice at 21.8% of the companion diagnostic market share, yet NGS is expected to outpace all other technologies. NGS market size in companion diagnostics is forecast to outpace PCR-based alternatives, expanding at 13.85% CAGR between 2026-2031. Hospital procurement committees increasingly run total-cost-of-ownership analyses that reveal high sample throughput offsets higher NGS consumable costs over a three-year amortization window. Consequently, instrument vendors now bundle analytics software into reagent contracts, an arrangement that shifts revenue recognition from one-time hardware sales to recurring service streams—reshaping quarterly earnings visibility.

Melanoma Emerges as Growth Frontier

Melanoma companion diagnostics will capture a market share acceleration to 13.22% CAGR through 2031 as immunotherapy combinations proliferate. The downstream impact is that dermatology clinics must coordinate closely with molecular labs to ensure rapid reflex testing, effectively blending two historically separate clinical silos. This integration forces electronic medical record vendors to adapt order-entry modules to accommodate reflex molecular panels, an IT adjustment that, although minor on the surface, represents a notable administrative investment across health systems.

Software Solutions Accelerate Growth

Assays and kits account for 65.75% of 2025 spending, driven by their one-to-one linkage with specific drug launches. However, software-driven interpretive platforms are the fastest-growing product category, with a 15.12% CAGR (2026-2031). Diagnostic accuracy hinges on variant classification pipelines that are now subject to continuous machine-learning updates, prompting regulators to contemplate post-market algorithm change controls. A parallel business consequence is emerging: laboratories may incur liability if they decline software upgrades that could materially improve clinical calls, implicitly threading software-maintenance clauses into laboratory accreditation audits.

Liquid Biopsy Transforms Testing Paradigms

Tissue biopsy still accounted for 77.95% of volumes in 2025 because confirmatory histology remains the regulatory gold standard. The liquid biopsy market is projected to expand at a 18.22% CAGR through 2031. Oncology practices are already reallocating phlebotomy staff to accommodate the surge, subtly increasing demand for point-of-care blood-processing devices. Laboratories that historically specialized in tissue histopathology must now invest in plasma-DNA extraction systems, creating operating expense pressure that influences capital budget cycles.

CROs Emerge as Strategic Partners

CROs’ companion diagnostics market size is set to climb 12.85% CAGR (2026-2031). Their breadth of biomarker-validation experience allows smaller biotechs to access regulatory pathways that would otherwise be prohibitive. This positioning gives CROs leverage to negotiate risk-sharing fee models tied to trial milestones, shifting them from service vendors toward quasi-development partners—a nuance that alters revenue recognition and could improve margin stability.

Geography Analysis

North America holds 39.95% market share in 2025. UnitedHealthcare’s policy to cover FDA-approved companion diagnostics when matched with the corresponding drug signals payer endorsement that directly influences adoption velocity. An inferred outcome is that private insurers outside the UnitedHealthcare umbrella may emulate the policy to remain competitive, leading to a cascade that can stabilize test reimbursement rates industry-wide.

Asia-Pacific is projected to log a 12.45% CAGR from 2026-2031. Japan’s government-supported cancer genome profiling (CGP) program forecasts a 54 billion-yen CGP market by 2035, prompting domestic labs to scale sequencing capacity. This governmental commitment sets a precedent that neighboring countries may replicate, harmonizing regulatory expectations and spurring cross-border clinical-trial enrollment that accelerates data accumulation in under-studied Asian populations.

Europe’s In Vitro Diagnostic Regulation environment is prompting companies to reexamine launch strategies. The limited capacity of notified bodies amplifies time-to-market risk, causing diagnostic firms to consider centralized testing models as interim solutions. Such centralization may inadvertently strengthen select reference laboratories, creating a quasi-oligopoly that could sway pricing dynamics once test volumes peak.

Competitive Landscape

The competitive environment blends diversified players like Roche with agile specialists such as Guardant Health. Strategic co-development agreements remain pivotal: Roche’s portfolio of 200-plus pharmaceutical collaborations anchors its diagnostics in many clinical-trial protocols, ensuring near-automatic uptake at commercial launch. A subtle competitive vector is emerging around data ownership; companies that control large real-world genomic datasets can refine predictive algorithms faster, granting them an iterative advantage unlikely to be replicated by reagent-only competitors.

Companion Diagnostics Industry Leaders

Qiagen NV

Agilent Technologies Inc.

Abbott

Biomerieux

F. Hoffmann-La Roche Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Roche received FDA label expansion for PATHWAY anti-HER2/neu antibody to include HR-positive, HER2-ultralow metastatic breast cancer.

- December 2024: Agilent’s PD-L1 IHC 28-8 pharmDx secured EU IVDR certification.

- November 2024: Roche obtained CE mark for the VENTANA FOLR1 RxDx Assay.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the companion diagnostics market as the global revenue generated from regulatory-cleared in vitro tests that guide the safe and effective use of a specific therapeutic drug or biologic across oncology and selected non-oncology indications.

In line with the report's Table of Contents, our study tracks assay kits, instruments, software services, and their deployment in clinical laboratories, hospitals, CROs, and biopharma settings.

Scope Exclusions: genomic profiling panels sold only for research use, imaging-based markers, and veterinary tests are intentionally left outside the market boundary.

Segmentation Overview

- By Technology

- Immunohistochemistry (IHC)

- Polymerase Chain Reaction (PCR)

- Real-Time PCR (RT-PCR)

- In-Situ Hybridization (ISH)

- Next-Generation / Gene Sequencing (NGS)

- Other Technologies

- By Indication

- Lung Cancer

- Breast Cancer

- Colorectal Cancer

- Leukemia

- Melanoma

- Gastric Cancer

- Prostate Cancer

- Other Indications

- By Product & Service

- Assays & Kits

- Instruments & Analyzers

- Software & Services

- By Sample Type

- Tissue Biopsy

- Liquid Biopsy

- Cytology Smears

- By End-user

- Pharmaceutical & Biotechnology Companies

- Contract Research Organizations (CROs)

- Clinical Reference Laboratories

- Hospital & Cancer Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- GCC

- South Africa

- Rest of Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed laboratory directors, oncologists, payers, and CDx product managers across North America, Europe, Asia-Pacific, and the Gulf to validate adoption rates, price dispersion, and launch timelines, and to stress-test early assumptions drawn from secondary work.

Desk Research

Our analysts began with public data sets from agencies such as the US FDA (CDx approvals list), EMA, PMDA, the National Cancer Institute's SEER registry, and OECD health statistics.

Trade bodies, including EFPIA and AdvaMedDx, were mined for drug-diagnostic co-development pipelines, while patent activity was screened through Questel to spot emerging targets.

Company 10-Ks, investor decks, and peer-reviewed papers supplied pricing ranges and utilization clues.

Finally, curated news feeds from Dow Jones Factiva helped trace new launches and reimbursement decisions.

The sources named are illustrative; many additional materials were consulted to complete evidence gathering.

Market-Sizing & Forecasting

A top-down incidence-to-treatment pool build was applied: cancer prevalence, therapy eligibility ratios, test uptake rates, average selling prices, and retest frequencies produced the base value.

Selected bottom-up checks sampled supplier revenues and channel inventories to help tune totals.

Key variables include: 1) annual FDA CDx approvals, 2) share of targeted therapies in oncology drug sales, 3) NGS platform installed base, 4) average reimbursement per biomarker panel, and 5) liquid-biopsy penetration.

Forecasts leverage multivariate regression layered with scenario analysis to capture shifts in precision medicine funding.

Data gaps in supplier roll-ups were bridged using region-specific ASP proxies validated through expert calls.

Data Validation & Update Cycle

Outputs pass a three-tier analyst review, variance tests against independent indicators, and re-checks with respondents when anomalies arise.

The model is refreshed every 12 months; material events (for example, a major biomarker approval) trigger interim revisions before client delivery.

Why Mordor's Companion Diagnostics Baseline Commands Reliability

Published figures often diverge because firms pick dissimilar product mixes, geography cuts, base years, and refresh cadences.

Key gap drivers in our space include whether liquid biopsies are counted, how aggressively non-oncology indications are modeled, and the extent to which emerging-market volumes are verified before projection.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.70 B (2025) | Mordor Intelligence | - |

| USD 9.06 B (2024) | Global Consultancy A | Includes imaging-linked CDx and cardiovascular panels not in scope |

| USD 7.50 B (2024) | Industry Journal B | Excludes several high-growth Asia-Pacific markets and uses list, not net, ASPs |

| USD 9.38 B (2024) | Regional Consultancy C | Projects faster uptake by assuming immediate payer parity for liquid biopsy |

Taken together, the comparison shows that Mordor's disciplined scope choices, balanced adoption curves, and annual refresh cycle yield a dependable, traceable baseline that decision-makers can trust when sizing opportunities or benchmarking performance.

Key Questions Answered in the Report

How big is the Companion Diagnostics Market?

The Companion Diagnostics Market size is expected to reach USD 9.76 billion in 2026 and grow at a CAGR of 12.18% to reach USD 17.35 billion by 2031.

Who are the key players in Companion Diagnostics Market?

Qiagen NV, Agilent Technologies Inc., Abbott, Biomerieux and F. Hoffmann-La Roche Ltd are the major companies operating in the Companion Diagnostics Market.

Which is the fastest growing region in Companion Diagnostics Market?

Asia-Pacific is estimated to grow at the highest CAGR of 12.45% over the forecast period (2026-2031).

Which region has the biggest share in Companion Diagnostics Market?

In 2025, the North America accounts for the largest market share in ompanion Diagnostics Market.

Page last updated on: