Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

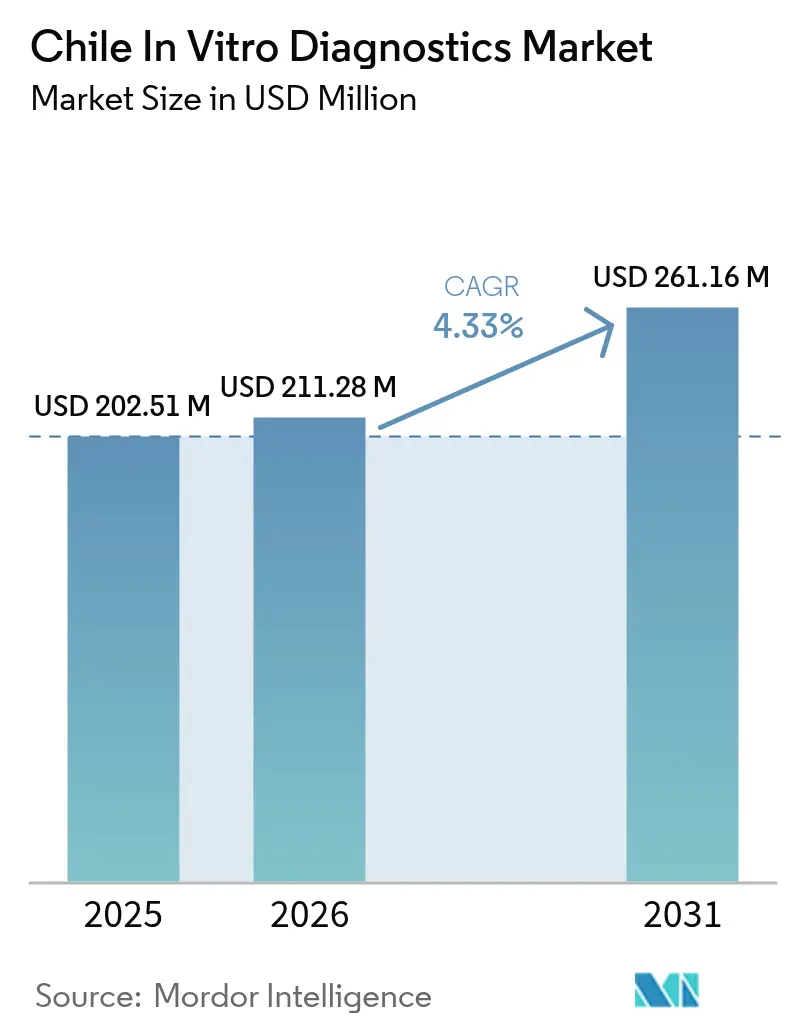

| Base Year Market Size (2025) | USD 202.51 Million |

| Market Size (2026) | USD 211.28 Million |

| Market Size (2031) | USD 261.16 Million |

| Growth Rate (2026 - 2031) | 4.33% CAGR |

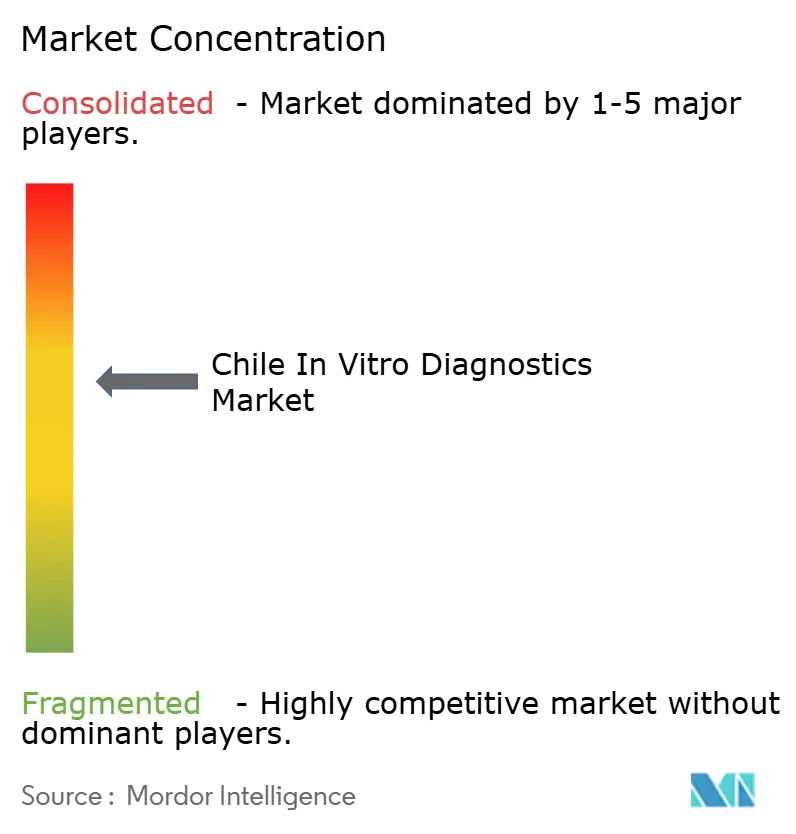

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chile In Vitro Diagnostics Market Analysis by Mordor Intelligence

The Chile In Vitro Diagnostics Market size is projected to be USD 202.51 million in 2025, USD 211.28 million in 2026, and reach USD 261.16 million by 2031, growing at a CAGR of 4.33% from 2026 to 2031.

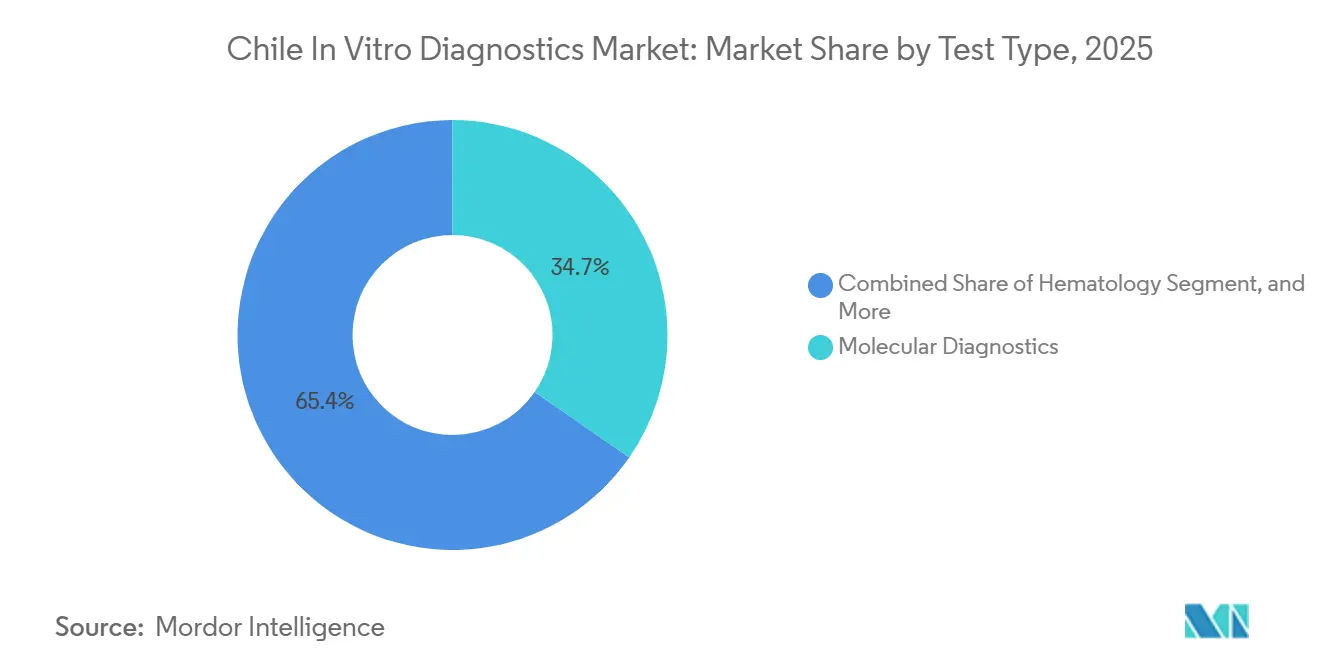

The structural shift in Chile's healthcare system is evident, with 78% of citizens now dependent on the FONASA public payer and only 13% utilizing private ISAPRE plans. This transition is driving laboratories to prioritize flexible reagent contracts over significant capital investments. The Instituto de Salud Pública (ISP) is set to release a consultation in November 2025, introducing sanitary controls on 39 IVD categories. While this will increase documentation costs, it is expected to standardize quality across Chile's in-vitro diagnostics market. Molecular diagnostics dominated 2025 revenue, contributing 34.65%. However, hospitals are increasingly adopting chemiluminescence platforms, which provide high-throughput thyroid and tumor marker panels without requiring PCR-grade clean rooms. In 2024, private networks such as ILC/RedSalud processed 8.3 million tests, highlighting how economies of scale are reshaping supplier negotiations within Chile's in-vitro diagnostics market.

Key Report Takeaways

- By test type, molecular diagnostics led with 34.65% of Chile in-vitro diagnostics market share in 2025; immunodiagnostics are projected to expand at a 6.75% CAGR through 2031.

- By product, reagents and kits commanded 57.43% share of the Chile in-vitro diagnostics market size in 2025, while software and services are forecast to advance at a 6.89% CAGR.

- By usability, disposable devices accounted for 61.64% of the Chile in-vitro diagnostics market size in 2025; re-usable equipment is growing at 7.88% as centralized labs amortize analyzers.

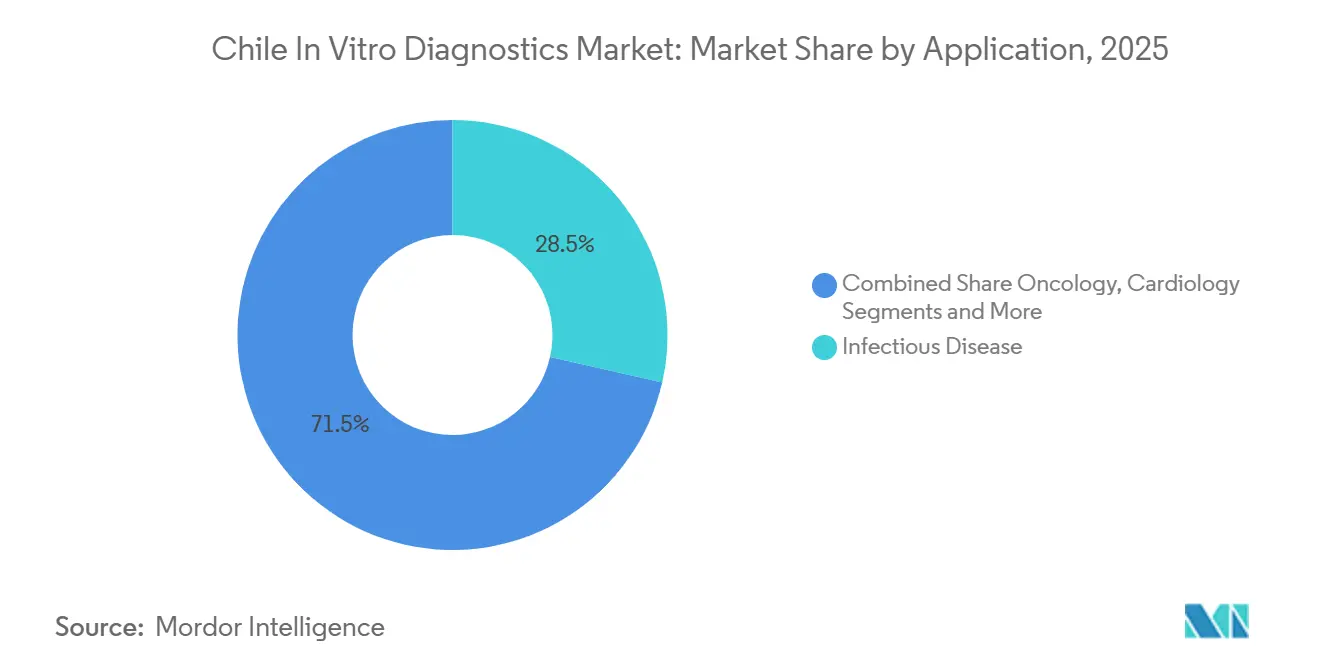

- By application, infectious diseases led with 28.54% revenue in 2025, whereas oncology diagnostics are on track for a 7.54% CAGR to 2031.

- By end user, hospital laboratories captured 48.54% of revenue in 2025; home-care and self-testing segments are rising at 5.43% amid pharmacy distribution of continuous glucose monitors.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Chile In Vitro Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing prevalence of chronic and infectious diseases | +1.2% | National, with concentration in Santiago, Valparaíso, Concepción | Medium term (2-4 years) |

| Expansion of public and private healthcare expenditure | +0.9% | National, stronger in Metropolitan and urban regions | Long term (≥ 4 years) |

| Technological advancements in molecular and point-of-care testing | +1.0% | National, early adoption in private hospital networks | Short term (≤ 2 years) |

| Favorable government reimbursement and screening programs | +0.7% | National, prioritizing GES/AUGE pathologies | Medium term (2-4 years) |

| Growing private laboratory consolidation and outreach | +0.5% | Metropolitan Santiago, expanding to regional capitals | Medium term (2-4 years) |

| Rising demand for personalized medicine and oncology diagnostics | +0.6% | National, concentrated in tertiary-care centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of Chronic and Infectious Diseases

Noncommunicable disorders caused 86% of deaths in 2024, yet tuberculosis incidence held at 15 cases per 100,000—triple the OECD mean—forcing laboratories to support chemistry analyzers for diabetes monitoring and PCR systems for TB detection simultaneously. WHO’s 2024 guidance recommends Xpert MTB/RIF Ultra as the first-line TB test, but 60% of rural clinics still rely on smear microscopy, elongating diagnosis by 14 days. Cancer incidence is forecast to rise 18% by 2030, yet only 12 of 29 regional services operate molecular pathology units for tumor profiling, underscoring unmet demand in the Chile in-vitro diagnostics market[1]Pan American Health Organization, “Health in the Americas 2025,” paho.org.

Expansion of Public and Private Healthcare Expenditure

Chile devoted 9.8% of GDP to health in 2021, but real public capital budgets have been flat since 2024, directing funds toward point-of-care HbA1c and lipid testing in 1,500 community centers under the National Health Strategy 2024-2030[2]OECD, “Chile Economic Survey 2025,” oecd.org. Private ISAPRE enrollees, though only 13% of the population, generate 40% of diagnostic revenue because of faster turnaround services, sustaining premium segments of the Chile in-vitro diagnostics industry.

Technological Advancements in Molecular and Point-of-Care Testing

Eighteen hospitals adopted BD MAX and GeneXpert platforms for respiratory panels since 2024, cutting turnaround from 48 hours to 90 minutes and proving the clinical value of rapid molecular testing. A 2024 Pontificia Universidad Católica study showed emergency departments that use 15-minute troponin and D-dimer assays lowered observation bed occupancy by 22%, reinforcing hospital interest in decentralized immunodiagnostics.

Favorable Government Reimbursement and Screening Programs

GES/AUGE mandates seven-day cervical cancer reporting and now reimburses circulating tumor DNA liquid biopsy at up to CLP 350,000 per test, a step expected to boost oncology throughput in the Chile in-vitro diagnostics market. HPV primary screening replaced cytology in 2024, shifting 600,000 annual tests toward molecular vendors and reducing per-test cost by 18%.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory approval timelines and compliance costs | -0.8% | National, affecting all IVD suppliers | Medium term (2-4 years) |

| Currency fluctuations impacting import-dependent supply chain | -0.6% | National, acute in public procurement | Short term (≤ 2 years) |

| Shortage of skilled laboratory workforce in regional areas | -0.5% | Regional provinces outside Santiago, Valparaíso, Concepción | Long term (≥ 4 years) |

| Fragmented health information systems limiting interoperability | -0.4% | National, most severe in public hospital networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Approval Timelines and Compliance Costs

ISP approval of novel Class III–IV assays averages 6-9 months, and the 2025 consultation adds ISO 27001 cybersecurity audits for middleware, pushing compliance outlays to USD 50,000-150,000 per device family[3]Instituto de Salud Pública de Chile, “Requisitos de Ciberseguridad 2025,” ispch.cl. Smaller vendors lacking regulatory staff may exit, tightening supplier diversity in the Chile in-vitro diagnostics market.

Currency Fluctuations Impacting Import-Dependent Supply Chain

The peso slipped from 800 to 870 CLP/USD during 2024, inflating reagent costs by 9% and forcing public buyers to cut volumes or extend contracts, a volatility pattern that erodes margins across the Chile in-vitro diagnostics industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Immunodiagnostics Outpace Molecular Despite Smaller Base

Molecular diagnostics accounted for 34.65% of revenue in 2025, but immunodiagnostics are forecast to grow 6.75%, driven by chemiluminescence analyzers such as cobas e 801, which lower reagent costs per test by 12%. Clinical chemistry held about 25% share, yet stagnant tariffs restrict sector expansion within the Chile in-vitro diagnostics market size.

Microbiology delivered 12% of sales, with BD and bioMérieux blood-culture systems gaining share as hospitals target faster sepsis identification. The strategic tilt toward immunodiagnostics reflects lower capital requirements and higher volumes relative to PCR, aligning with constrained public budgets.

By Product: Software and Services Gain as Laboratories Prioritize Connectivity

Reagents and kits captured 57.43% of 2025 revenue, yet software and services are climbing at 6.89% as middleware upgrades align with ISO 27001 mandates. Instruments now account for 30%, with replacement cycles stretching to nine years.

Roche’s cobas link generates recurring USD 12,000 per site, and private chains are bundling remote diagnostics contracts to lock predictable spend profiles within the Chile in-vitro diagnostics market. Interoperability remains challenging where 3-vendor fleets demand custom interfaces consuming a quarter of IT budgets.

By Usability: Disposable Devices Dominate but Re-Usable Equipment Gains in Centralized Labs

Disposable cartridges held 61.64% share during 2025 as BD Veritor and Abbott i-STAT enable 15-minute answers in point-of-care settings. However, re-usable analyzers show 7.88% CAGR as networks like ILC/RedSalud centralize high-throughput platforms, cutting per-test costs by 18%.

Public hospitals face a catch-22: low daily volumes cannot amortize re-usable analyzers, yet disposable strips exhaust budgets by mid-year, prompting pilot shared-service hubs that ferry samples to provincial capitals under a courier model.

By Application: Oncology Diagnostics Surge as GES Coverage Expands

Infectious diseases delivered 28.54% of revenue in 2025, but oncology assays are slated for 7.54% CAGR as liquid biopsy and EGFR testing secure reimbursement. Diabetes made up 22%, though CGM adoption is diverting some volumes away from laboratories.

Cardiology, autoimmune, and nephrology panels round out demand, and liquid biopsy pilots that detect recurrence six months earlier than CT are pushing tertiary centers to invest in serial ctDNA workflows inside the Chile in-vitro diagnostics market.

By End User: Home-Care and Self-Testing Users Expand as Pharmacies Distribute Devices

Hospital laboratories retained 48.54% of 2025 revenue, yet home and self-testing segments are growing 5.43% on the back of Abbott FreeStyle Libre sensors retailing at CLP 45,000 per 14-day pack.

Stand-alone private labs own 30% share, offering extended hours and mobile draws, while point-of-care sites carry 15% as rapid antigen testing normalizes emergency workflows across Chile in-vitro diagnostics market facilities.

Competitive Landscape

The top five suppliers—Roche, Abbott, Siemens Healthineers, BD, and bioMérieux—together held about 60% of 2025 revenue, confirming moderate concentration in the Chile in-vitro diagnostics market. Roche’s cobas footprint spans 42 hospitals; Abbott treats Chile as a satellite yet benefits from Latin America scale effects. Siemens Atellica wins chemistry-immunoassay consolidations, though fragmented distributors blunt service levels in provinces.

Multinationals bundle multi-year reagent-rental deals, shifting income toward subscriptions, while local distributors win rural share via same-day service and peso-denominated payment terms. ISP’s 24-36-month compliance window on 39 IVD categories favors established dossiers, creating a moat against small entrants.

Technology remains a differentiator: cobas link middleware reduced report delays 35% at Clínica Alemana but costs 15-20% more than generic LIS bridges, restricting adoption to well-integrated private hospitals. Start-ups offering vendor-neutral cloud LIS at 40% lower price lack cybersecurity credentials, yet could appeal if they pass ISO 27001 audits by 2027.

Chile In Vitro Diagnostics Industry Leaders

Thermo Fischer Scientific Inc.

QIAGEN N.V.

Abbott Laboratories

Siemens Healthcare GmbH

F. Hoffmann-La Roche AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: MINSAL launched a public consultation to include new medical and in vitro diagnostic devices under Chile’s mandatory sanitary control regime, based on existing health regulations.

- October 2024: The Instituto de Salud Pública in Chile became the first agency in the Americas to implement an automated vaccine-safety surveillance system using HL7 FHIR technology. This innovative system enables integrated reporting of diagnostic data for better public health monitoring.

Chile In Vitro Diagnostics Market Report Scope

As per the scope of this report, in vitro diagnostics involves medical devices and consumables that are utilized to perform in vitro tests on various biological samples.

The Chile in-vitro diagnostic market is segmented by Test Type (Clinical Chemistry, Molecular Diagnostics, Immuno Diagnostics, Hematology, and Other Test Types) Product (Instrument, Reagent, Other Products), Usability (Disposable IVD Devices, Reusable IVD Devices), Application (Infectious Disease, Diabetes, Cancer/Oncology, Cardiology, Autoimmune Disease, and Other Applications), and End User (Diagnostic Laboratories, Hospitals and Clinics, and Other End-Users). The report offers the value (in USD million) for the above segments.

By Test Type

| Clinical Chemistry |

| Immuno-Diagnostics |

| Molecular Diagnostics |

| Hematology |

| Coagulation |

| Microbiology |

| Other Test Types |

By Product

| Instruments |

| Reagents & Kits |

| Software & Services |

By Usability

| Disposable IVD Devices |

| Re-Usable Equipment |

By Application

| Infectious Diseases |

| Diabetes |

| Oncology |

| Cardiology |

| Auto-Immune Disorders |

| Nephrology |

| Other Applications |

By End User

| Stand-Alone Laboratories |

| Hospital-Based Laboratories |

| Point-Of-Care Settings |

| Home-Care & Self-Testing Users |

| By Test Type | Clinical Chemistry |

| Immuno-Diagnostics | |

| Molecular Diagnostics | |

| Hematology | |

| Coagulation | |

| Microbiology | |

| Other Test Types | |

| By Product | Instruments |

| Reagents & Kits | |

| Software & Services | |

| By Usability | Disposable IVD Devices |

| Re-Usable Equipment | |

| By Application | Infectious Diseases |

| Diabetes | |

| Oncology | |

| Cardiology | |

| Auto-Immune Disorders | |

| Nephrology | |

| Other Applications | |

| By End User | Stand-Alone Laboratories |

| Hospital-Based Laboratories | |

| Point-Of-Care Settings | |

| Home-Care & Self-Testing Users |

Key Questions Answered in the Report

How fast is the Chile in-vitro diagnostics market expected to grow through 2031?

It is projected to expand from USD 0.21 billion in 2026 to USD 0.26 billion by 2031 at a 4.33% CAGR.

Which test type is growing fastest in Chile?

Immunodiagnostics are forecast to grow 6.75% yearly as chemiluminescence analyzers replace manual ELISA.

What share do reagents and kits hold in overall spending?

Reagents and kits accounted for 57.43% of 2025 revenue, the largest slice of spending.

Why is oncology testing gaining momentum?

GES reimbursement now covers EGFR liquid biopsy and broader molecular profiling under the National Cancer Plan 2024-2030.

Which regions dominate diagnostic spending?

Santiago, Valparaíso, and Biobío together captured 72% of 2025 market revenue.

How are currency swings affecting suppliers?

An 8% peso depreciation in 2024 raised reagent costs 9%, squeezing margins and delaying public-sector analyzer upgrades.

Page last updated on: