Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

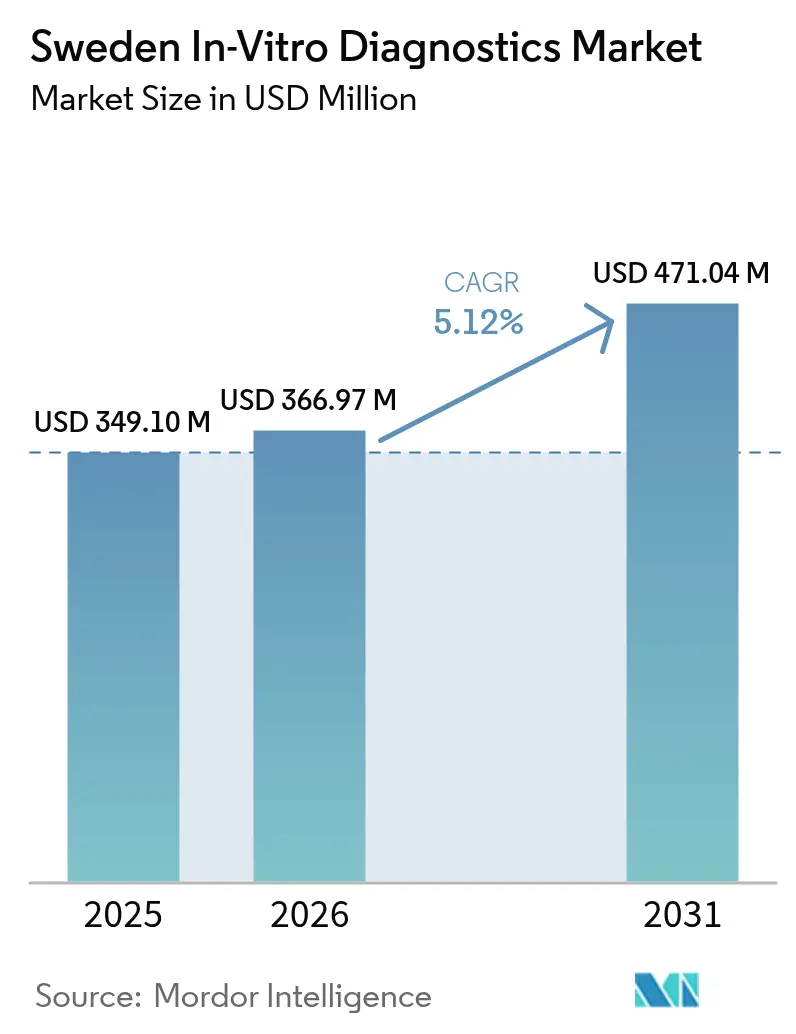

| Base Year Market Size (2025) | USD 349.1 Million |

| Market Size (2026) | USD 366.97 Million |

| Market Size (2031) | USD 471.04 Million |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sweden In-Vitro Diagnostics Market Analysis by Mordor Intelligence

The Sweden in-vitro diagnostics market size was valued at USD 349.1 million in 2025 and estimated to grow from USD 366.97 million in 2026 to reach USD 471.04 million by 2031, at a CAGR of 5.12% during the forecast period (2026-2031). The favorable trajectory reflects robust public-sector health spending, strategic precision-medicine programs, and rapid digitalization across care settings. Heavy investments channeled through the 11.2% of GDP health budget continue to enlarge testing volumes, while the SciLifeLab precision-medicine roadmap and Genomic Medicine Sweden funding spur biomarker discovery, accelerating adoption of molecular and companion diagnostics. Industry leaders are embedding artificial-intelligence algorithms in pathology and sequencing workflows, improving analytical speed and accuracy. Parallel growth of point-of-care systems reduces diagnostic delays in remote northern regions, a priority for regional health authorities responding to workforce shortages and harsh winter logistics. Against this backdrop, competitive intensity centers on assay innovation, regulatory readiness under IVDR, and service models that address an aging, multimorbid population whose 55% prevalence of five-plus chronic conditions necessitates frequent laboratory monitoring.

Key Report Takeaways

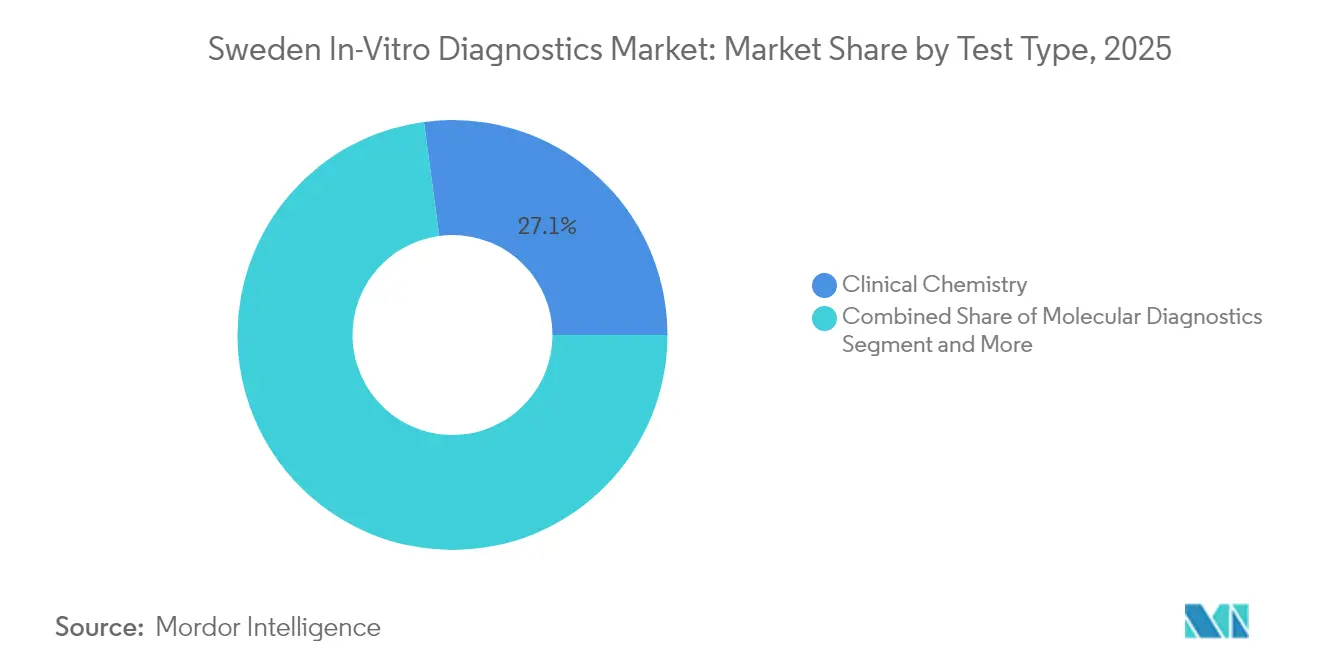

- By test type, clinical chemistry led with 27.12% revenue share in 2025; molecular diagnostics is projected to expand at a 7.29% CAGR to 2031.

- By product, reagents accounted for 64.72% share of the Sweden in-vitro diagnostics market size in 2025 while instruments are advancing at a 6.72% CAGR through 2031.

- By usability, reusable devices dominated with an 81.35% share in 2025; disposable devices are forecast to grow at a 6.54% CAGR to 2031.

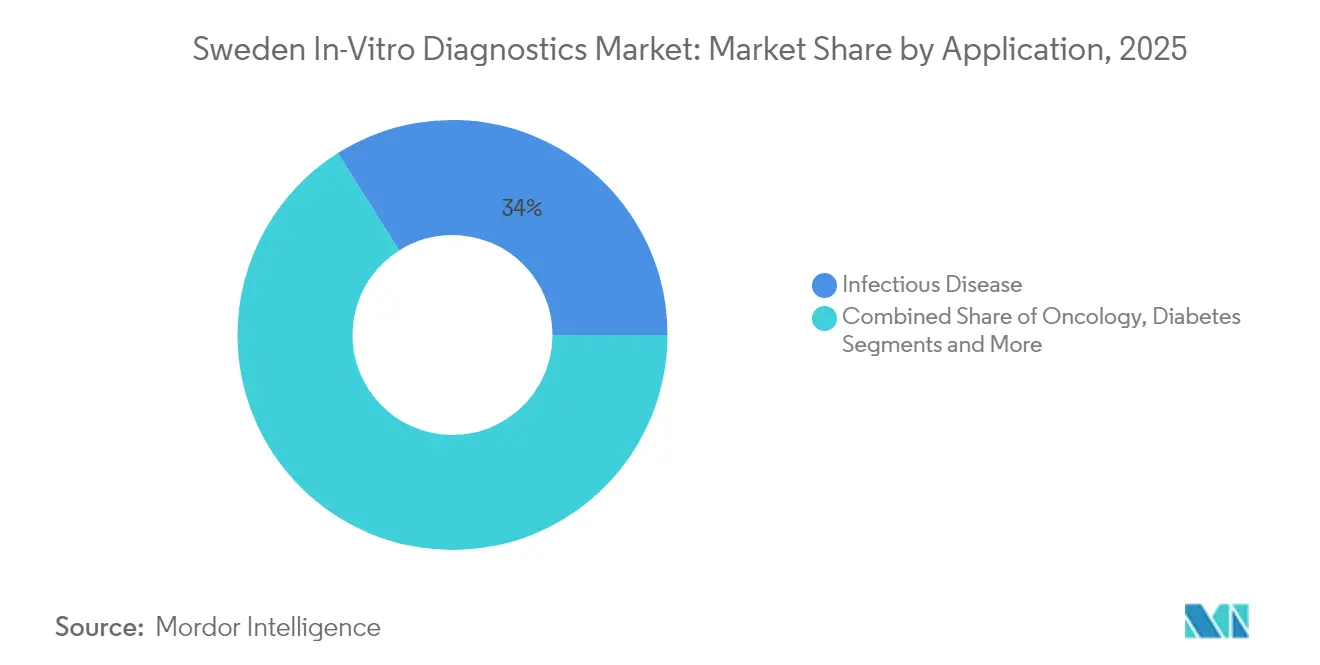

- By application, infectious disease captured 33.95% of Sweden in-vitro diagnostics market share in 2025 and cancer/oncology is rising at an 7.96% CAGR through 2031.

- By end-user, diagnostic laboratories held 55.92% of the Sweden in-vitro diagnostics market size in 2025 while hospitals & clinics are expanding at a 6.37% CAGR to 2031.

- By test location, central laboratory testing commanded 68.74% share in 2025; point-of-care testing is accelerating at a 8.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Sweden In-Vitro Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic diseases coupled with growing aging population | +1.4% | National, higher in urban centers | Long term (≥ 4 years) |

| Technological advancements in IVD devices | +1.2% | Stockholm–Uppsala & Gothenburg corridors | Medium term (2-4 years) |

| Increasing adoption of point-of-care testing | +0.9% | Remote northern regions | Medium term (2-4 years) |

| Government initiatives and funding for healthcare improvements | +0.8% | National | Medium term (2-4 years) |

| Expansion of diagnostic laboratories and infrastructure | +0.5% | Large urban counties | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Diseases Coupled with Growing Aging Population

Home-care recipients aged ≥85 exhibit a 66% multimorbidity rate, driving hospitalizations for infections, injuries, and heart failure that demand frequent biochemical and molecular tests. The Sweden in-vitro diagnostics market responds with assays capable of earlier detection and longitudinal monitoring, particularly within molecular platforms tuned to cardiac biomarkers and pathogen panels. Digital laboratory connectivity now transmits results directly to community nurses, shrinking turnaround time and enabling proactive therapy adjustments. Public payers view such diagnostics as cost-effective tools for curbing readmissions, reinforcing demand curves well into the next decade. Rising chronic-care caseloads in metropolitan Stockholm and Gothenburg further concentrate test volumes, incentivizing laboratories to automate high-throughput chemistry lines for metabolic and renal profiles.

Technological Advancements in IVD Devices

Swedish pathology suites are integrating over 20 artificial-intelligence algorithms—including prostate-grade and breast-mitosis classifiers—inside Roche’s Digital Pathology Open Environment, elevating diagnostic confidence and workflow capacity[1]Roche Diagnostics, “Roche Advances AI-Driven Cancer Diagnostics,” roche.com. The EU AI Act, effective 2024, classifies these models as high-risk, prompting manufacturers to secure CE marking and traceable data governance—a hurdle that favors early movers able to fuse regulatory and engineering skillsets. Convergence with next-generation sequencing amplifies precision-oncology gains; INFORM registry data show actionable targets in 88% of pediatric tumors profiled, catalyzing broader clinician reliance on gene-panel assays. Continuous instrument automation, cloud analytics, and middleware interoperability now extend from central labs to mobile hematology counters, solidifying technology adoption beyond university centers.

Increasing Adoption of Point-of-Care Testing

Sweden’s remote interior counties deploy tele-supervised POCT devices that deliver troponin, CRP, and influenza results within minutes, sparing patients 4- to 6-hour winter journeys to the nearest regional hospital. A Stockholm pediatric emergency study highlighted POCT’s dual value in clinical decision support and parental reassurance, though clinicians still request training modules on analytic limitations. Sponsor-led clinical trials harness POCT-enabled single-visit enrollment protocols, trimming screen-failure rates and bolstering patient retention. These operational efficiencies fuel the 9.1% CAGR forecast for POCT, positioning decentralized testing as a strategic complement rather than competitor to central laboratories across the Sweden in-vitro diagnostics market.

Government Initiatives and Funding for Healthcare Improvements

The 2025 federal allocation to Genomic Medicine Sweden funds nationwide tumor-molecular profiling networks and rare-disease sequencing, embedding reimbursement pathways for high-complexity assays[2]Genomic Medicine Sweden, “Government Provides Significant New Funding,” genomicmedicine.se. Parallel PROMISE investments channel multi-omics research into real-world care, generating longitudinal datasets that accelerate biomarker validation and regulatory submissions. Cross-sector partnerships target streamlined trial startup and data-sharing, elevating Sweden’s appeal to multinational IVD sponsors. Combined, these programs underpin sustained assay demand, catalyze instrument refresh cycles, and anchor global clinical-evaluation studies within the Sweden in-vitro diagnostics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced IVD equipment | -0.7% | National, heavier for small sites | Medium term (2-4 years) |

| Stringent regulatory approvals and compliance | -0.6% | Nationwide, IVDR-aligned | Short term (≤ 2 years) |

| Lack of skilled laboratory personnel | -0.5% | Rural counties | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced IVD Equipment

Whole-genome sequencing for acute leukemia tallies EUR 3,472 per patient versus EUR 2,465 for standard protocols, presenting a 41% premium that budget-constrained district hospitals struggle to absorb. Limited public test lists shift expenses to patients and charities, dampening uptake despite clinical superiority. Capital acquisition hurdles intensify when only 1% of Sweden’s health spend flows to in-vitro diagnostics even though test results influence 70% of clinical decisions. Leasing models and reagent-rental contracts partially alleviate upfront outlays, yet smaller providers still defer upgrades, tempering instrument growth within segments of the Sweden in-vitro diagnostics market.

Stringent Regulatory Approvals and Compliance

IVDR implementation multiplies documentation demands and Notified-Body fees, with 70% of manufacturers reporting higher administrative spend that diverts resources from R&D[3]MedTech Europe, “Report on Administrative Burden under IVDR,” medtecheurope.org. Parliamentary calls for legislative fine-tuning underscore certification bottlenecks that threaten test availability for niche conditions. Swedish trade groups urge proportional oversight and accelerated reviews, warning that prototype assays may languish outside market access windows, particularly for small and mid-size innovators. These headwinds slow portfolio refreshes, although larger multinational firms leverage in-house regulatory affairs teams to fast-track CE certifications, potentially widening competitive gaps within the Sweden in-vitro diagnostics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Molecular Diagnostics Revolutionizing Precision Care

Molecular platforms currently represent 20.88% of assay revenues yet register the fastest 7.29% CAGR as genomic profiling becomes routine in oncology, rare-disease, and infection workups. Sweden in-vitro diagnostics market size expansion for molecular panels aligns with the INFORM and PROMISE programs that reimburse gene panels and companion tests tethered to targeted therapies. Clinical chemistry still accounts for 27.12% of 2025 billings by covering metabolic, renal, and electrolyte baselines essential for chronic-disease management. Automation upgrades such as Boule Diagnostics’ compact analyzers improve throughput for primary-care clinics and free specialist labs to pivot toward high-value genomic assays. Immuno-diagnostics capture steady autoimmune and respiratory demand, while hematology benefits from AI-enhanced smear interpretation reducing manual review variance. Collectively, these categories reinforce balanced volume streams that stabilize reagent demand across the Sweden in-vitro diagnostics market.

Molecular growth also rides the country’s strong biobank network, which stores over 200 million samples linked to electronic health records. This infrastructure shortens validation cycles for novel NGS assays and attracts external sponsors seeking Nordic trial populations with homogeneous follow-up. Sequencing cost curves descending below USD 200 per gene panel further democratize access, prompting community oncology centers to procure benchtop sequencers under reagent-rental plans. As result-turnaround expectations tighten, central labs integrate cloud-based variant-calling pipelines that flag actionable mutations within hours, boosting clinician confidence and reinforcing adoption momentum throughout the Sweden in-vitro diagnostics market.

By Product: Reagents Sustain Market While Instruments Innovate

Reagents contribute 64.72% of 2025 billings, their recurring consumption pattern making them the profit backbone for both global and local suppliers. Multi-year vendor contracts lock in volume commitments, creating forecast visibility that underwrites manufacturing scale economies. Simultaneously, the instruments segment is projected to post a 6.72% CAGR as sites replace legacy analyzers with AI-ready, middleware-enabled platforms capable of auto-verification and auto-reflex testing. Hospital mergers seeking consolidated service lines push for open-channel chemistry and immuno-chemistry systems that accommodate third-party kits, spurring instrument refresh cycles in Tier-2 counties. Software and middleware—grouped under “other products”—add incremental revenue by bridging LIS, EHR, and data-lake environments, supporting national interoperability mandates.

Reagent suppliers are also embedding sustainability metrics—such as reduced hazardous solvent volumes and recyclable primary packaging—aligning with Sweden’s circular-economy targets. Instruments now ship with energy-efficiency dashboards that report kWh consumption per test, a growing procurement criterion for carbon-budgeted county councils. Net effect: product-level innovation dovetails with policy priorities, reinforcing value propositions and widening moats around incumbents operating in the Sweden in-vitro diagnostics market.

By Usability: Disposable Devices Gain Momentum Despite Reusable Dominance

Reusable analyzers and cartridge-free devices hold an 81.35% volume share due to Sweden’s tradition of minimizing single-use plastics and maximizing life-cycle cost savings. Nevertheless, disposable test kits post a 6.54% CAGR as POCT stations proliferate in ambulances, rural clinics, and home-care pathways. Manufacturers now adopt plant-based polymers and modular housings to cut carbon footprints, making disposables more palatable to sustainability-minded purchasers. During winter months, disposable swab-to-answer respiratory panels enable quick triage in remote villages where courier service to central labs can take days, underscoring convenience-driven demand.

Emerging reimbursement codes that cover POCT influenza and respiratory syncytial virus assays further accelerate uptake. Meanwhile, reusable platforms adapt by offering auto-clean and UV-sterilization cycles that reduce manual labor, appealing to busy hospital core labs. Balancing infection-control, cost-containment, and environmental stewardship, procurement committees increasingly deploy hybrid strategies that combine reusable high-volume analyzers with disposable near-patient kits, ensuring the Sweden in-vitro diagnostics market accommodates diverse clinical settings.

By Application: Cancer Diagnostics Accelerate Amid Infectious-Disease Prevalence

Infectious-disease testing retains 33.95% share given sustained surveillance needs for respiratory pathogens, tuberculosis, and healthcare-associated infections. Government-funded respiratory panels capable of detecting up to 23 targets remain cornerstone tools in central labs, especially after RISE’s designation as an EU reference laboratory for virus diagnostics. However, oncology drives the steepest 7.96% CAGR as precision-therapy eligibility hinges on detailed tumor genomics. National guidelines now recommend multi-gene panels for colorectal, lung, breast, and pediatric cancers, creating predictable volumes that laboratories leverage for batching efficiency.

Diabetes monitoring constitutes a stable slice of demand, with HbA1c and micro-albumin assays regularly ordered in primary care. Cardiac biomarkers see incremental growth tied to rising heart-failure prevalence among the elderly, whereas autoimmune profiles leverage chemiluminescence platforms to cut assay times. Thyroid and coagulation tests round out the application matrix, ensuring diversified revenue streams that help labs cushion cyclical swings. Confluence of pathogen vigilance and precision-oncology imperatives therefore keeps the Sweden in-vitro diagnostics market resilient across economic and epidemiological cycles.

By End-User: Diagnostic Laboratories Lead While Hospitals Expand Capabilities

Specialist diagnostic-service providers account for 55.92% of 2025 receipts, leveraging robotic track systems and consolidated purchasing power to drive reagent costs down. University-affiliated mega-labs in Karolinska and Sahlgrenska process over 20,000 samples daily, freeing regional hospitals to concentrate on acute care. Yet hospital laboratories grow at 6.37% CAGR as integrated care models mandate same-day results to expedite discharge planning. Investments in compact immunoassay, hematology, and syndromic molecular platforms allow emergency departments to act on results during the same patient encounter.

Research institutes and pharma sponsors constitute a nimble but growing customer base, propelled by surge in precision-oncology trials that require companion diagnostic workflows embedded within academic facilities. Home-care providers pilot dried-blood-spot and remote-phlebotomy solutions for frail seniors, a niche predicted to scale with aging demographics. The distributed yet interconnected lattice of end-users thus bolsters assay volumes across the Sweden in-vitro diagnostics market while spreading risk across payer types.

By Test Location: Point-of-Care Testing Accelerates Despite Central-Lab Dominance

Central labs maintain a 68.74% share by offering economies of scale, high-throughput platforms, and extensive test menus spanning routine chemistries to esoteric molecular panels. Automation tracks reduce manual touches by up to 85%, containing labor costs amid technologist shortages. Concurrently, POCT’s 8.74% CAGR embodies Sweden’s digital-health vision, delivering actionable data at mountain clinics, ferries serving archipelagos, and even patient homes via nurse-operated kits. Integration middleware now ports POCT results into regional EHRs within seconds, enabling clinicians to view comprehensive lab histories irrespective of collection site.

Public health authorities use POCT to shorten antibiotic-prescribing windows, thereby curbing antimicrobial resistance. In tertiary centers, cardiac troponin POCT halves emergency department dwell times, freeing bed capacity. The symbiosis of centralized and decentralized modalities ensures broad population coverage, reinforcing the Sweden in-vitro diagnostics market’s adaptability to geography, seasonality, and resource constraints.

Geography Analysis

Regional funding differences and population density gradients shape testing demand profiles. Stockholm and Uppsala counties jointly account for nearly one-third of national assay volumes, driven by high tertiary-care concentration and research-hospital clustering. Laboratories here pioneer molecular-oncology projects, pulling advanced instrument installations forward in the procurement cycle. West-coast Gothenburg–Västra Götaland similarly commands a substantial share, fueled by aging urban populations and active life-science corridors that host multinational device makers.

Northern Norrbotten and Västerbotten record the fastest year-on-year POCT uptake as sparsely populated municipalities adopt digital-first models to compensate for long travel distances. The Swedish in-vitro diagnostics market size attributable to north-of-the-Arctic-Circle counties is currently modest but posts double-digit growth in POCT consumables, a trend likely to continue as telemedicine networks widen fiber coverage. Southern Skåne leverages cross-Öresund proximity to Danish biotech clusters, fostering collaborative clinical-validation studies that import reference samples and analytic expertise, diversifying local test portfolios.

County councils apply value-based procurement frameworks that weigh total cost of ownership and sustainability metrics, influencing supplier success. Carbon-priced logistics incentivize local reagent distribution centers, squeezing lead times and supporting temperature-sensitive molecular kits. Collectively, Sweden’s decentral-governance model creates a patchwork of procurement cadences yet ensures nationwide testing access, sustaining consistent reagent demand across the Sweden in-vitro diagnostics market.

Regulatory Landscape

In Sweden, in-vitro diagnostic (IVD) products are governed by the EU In Vitro Diagnostic Regulation (IVDR, EU 2017/746), which has applied since May 26, 2022, and requires CE marking plus strengthened clinical evidence, post-market surveillance, and vigilance. Läkemedelsverket (the Swedish Medical Products Agency, MPA) is the competent authority for IVD market access oversight, surveillance and vigilance, and supervision of performance studies, alongside national implementing provisions such as Law (2021:600) and Ordinance (2021:631).

IVD performance studies require notification or authorization via Läkemedelsverket. The published fees range from 16,000 SEK to 60,000 SEK depending on the IVDR pathway, including routes aligned to Articles 66 and 70. Sweden also tracks EU-level updates that adjusted IVDR transition timelines through Regulation (EU) 2024/1860 (adopted June 13, 2024) and the phased roll-out of Eudamed, with Swedish legislative updates proposed to take effect by May 26, 2025. These changes affect how manufacturers and economic operators manage registration and legacy-to-IVDR transition activities.

Competitive Landscape

Global majors—Abbott, Danaher Corporation, and Becton, Dickinson, and Company—anchor the market with broad assay menus, advanced automation, and deep regulatory resources. Roche’s AI-powered pathology suite exemplifies strategy to bundle instrumentation with digital analytics, locking customers into ecosystem workflows. Abbott leverages its glucose-monitoring and rapid-immunoassay franchises to cross-sell molecular panels, while Siemens drives adoption of high-throughput chemistry systems within county mega-labs. Local champion Boule Diagnostics maintains foothold through hematology and compact chemistry analyzers tailored for Sweden’s mid-size hospitals.

Strategic alliances surge as firms navigate IVDR complexity; multinationals partner with RISE for verification studies, tapping the institute’s newly awarded reference-lab status for respiratory diagnostics. Start-ups flock to university incubators, focusing on AI-driven sepsis markers and microfluidic PCR cartridges but face capital-intensity and regulatory hurdles. Workforce shortages spur co-development of workflow automation solutions that promise reduced hands-on time, an appealing differentiator for procurement committees.Price competition remains moderate as quality and compliance overshadow pure cost metrics. Vendors differentiate via training, uptime guarantees, and environmental-impact reporting.

Sweden In-Vitro Diagnostics Industry Leaders

Abbott Laboratories

Becton, Dickinson, and Company

Bio-Rad Laboratories, Inc.

Thermo Fisher Scientific Inc.

Danaher Corporation (Beckman Coulter, Cepheid)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

In Sweden, the most concrete opportunities are linked to scaling clinically validated precision diagnostics backed by national genomics and multi-omics infrastructure. Genomic Medicine Sweden funding in 2025 supports nationwide tumor profiling and rare-disease sequencing workflows, which in turn increases demand for molecular and companion diagnostic menus in oncology and rare disease. It also raises requirements for interoperable software, sample logistics, and quality systems that can operate across county-run care pathways.

Another opportunity area is compliant AI-enabled diagnostics embedded into routine laboratory and pathology workflows. The Vinnova-backed AIDx AI Diagnostics Excellence Cluster (Oct 2025 to Mar 2026), involving the National Genomics Platform (NGP), points to active efforts to standardize AI use in clinical genomic diagnostics under overlapping EU AI Act, GDPR, and IVDR constraints. With Sweden continuing digitalization across care settings, suppliers that can provide auditable AI, data governance, and IVDR-ready documentation alongside instruments and reagents have a clearer route into county procurement and university-hospital reference environments.

Recent Industry Developments

- April 2026: Devyser Diagnostics completed the acquisition of Cybergene AB, expanding its portfolio in the aneuploidy testing area. The deal strengthens a Sweden-based specialist supplier with additional assays and capabilities that support cytogenetics and genetic testing workflows in clinical laboratories.

- May 2025: Abbott reported REFLECT real-world retrospective findings using the Swedish National Diabetes Register, linking FreeStyle Libre continuous glucose monitoring use with reduced hospitalizations for heart complications among people with diabetes in Sweden. The use of national registry evidence supports payer and provider discussions around broader adoption and integration of connected diagnostics in chronic disease pathways.

- April 2025: The Swedish government provided additional funding to Genomic Medicine Sweden to accelerate precision-medicine infrastructure. The program-level financing supports wider access to sequencing and tumor profiling, increasing downstream demand for molecular IVD assays, reagents, and associated laboratory automation.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the Sweden in vitro diagnostics market includes in-scope lab and point-of-care tests that analyze human samples outside the body, along with the related instruments and consumables. Revenue is counted at the manufacturer selling price within Sweden.

Scope exclusions: Standalone laboratory service fees and general health IT that are not sold as IVD products are excluded.

Segmentation Overview

- By Test Type

- Clinical Chemistry

- Molecular Diagnostics

- Immuno-Diagnostics

- Hematology

- Other Test Types

- By Product

- Instruments

- Reagents

- Other Products

- By Usability

- Disposable IVD Devices

- Reusable IVD Devices

- By Application

- Infectious Disease

- Diabetes

- Cancer / Oncology

- Cardiology

- Autoimmune Disease

- Other Applications

- By End-User

- Diagnostic Laboratories

- Hospitals & Clinics

- Other End-Users

- By Test Location

- Point-of-Care Testing

- Central Laboratory Testing

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set a starting point for Sweden, so the model builds on consistent definitions and publicly checkable signals. We typically review Sweden health and population indicators, such as Sweden national health statistics, OECD health data, and Eurostat series, to track demand direction and where testing intensity is likely to be concentrated.

To keep the IVD scope aligned with how products are classified, we also check EU IVDR references published by the European Commission and supporting public guidance from national bodies. In parallel, company annual reports, investor presentations, and reputable press releases are used to understand product mix and pricing movement, while patent databases help indicate the pace of assay and platform development. Where useful, a paid subscription for company financials and intelligence is used for screening and cross-checking reported exposure, and an import-export shipment-level database is used selectively to sanity-check supply patterns for key IVD categories. The sources listed above are illustrative, and many other public references are also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to verify assumptions that are harder to read from public Sweden-only datasets, especially around utilization, tender behavior, and price realization. We speak with a mix of manufacturers and distributors, hospital and diagnostic lab procurement roles, laboratory leaders, and clinicians familiar with testing pathways, which helps validate the desk signals and fill gaps.

For Sweden, discussions also focus on central laboratory versus point-of-care testing mix, the practical impact of IVDR transitions on portfolio availability, and how procurement cycles can shift analyzer placements and reagent demand.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 20% | |

| Mid tier: 43% | Functional/Unit leaders: 35% | |

| Smaller Players: 20% | Managers: 45% |

Market-Sizing & Forecasting

Sizing begins with a top-down demand pool reconstruction that links Sweden testing need to measurable healthcare signals and then converts that need into IVD product revenue. We build the chain from population and aging mix, to diagnosed and monitored cohorts, to testing rates by key care settings, and then apply a price logic for instruments and consumables that is checked against real procurement and supplier commentary.

Inputs that commonly matter in Sweden IVD include chronic disease monitoring frequency, infectious disease testing intensity during seasonal peaks, the split between central laboratories and near-patient settings, procurement and tender timing that affects placements, and the expected mix shift toward molecular diagnostics and immunoassays. Pricing is handled in local currency first, and then translated to USD using the applicable period average, which reduces distortion from one-off currency swings.

For forecasting, scenario analysis is used to reflect different adoption speeds for higher value assays, the timing of portfolio transitions under IVDR, and the pace of decentralization into point-of-care. We then corroborate the result with selective bottom-up approximations using sampled supplier splits and channel checks, and where data is incomplete the gap is handled with conservative fill rules that are re-tested during validation.

Data Validation & Update Cycle

Validation is done in a few passes so the total stays consistent with observable market signals. We compare outputs against independent indicators like health spending direction, testing activity proxies, and procurement behavior, then investigate any abrupt shifts that do not match the underlying drivers.

Before sign-off, another analyst reviews the full model chain to confirm scope application is consistent across instruments and consumables and that currency handling does not inflate growth. Reports are refreshed annually, with interim updates when material events occur such as regulatory shifts, reimbursement changes, or supply constraints. Right before delivery, a fresh pass is completed so clients receive the latest aligned assumptions and outputs.

Mordor Intelligence's Vitro Diagnostics Sweden Market Size Compared With Other Published Estimates

Published values for Sweden IVD often differ because the scope boundary is not drawn the same way across sources, and the year can be valued using different price bases and currency conversion timing. Another reason is the choice of demand anchor, since some estimates start from broad healthcare spend ratios and others start from testing activity and product mix.

Tender award patterns, disclosed analyzer placements, and test volume direction checks are the evidence that keeps Mordor Intelligence tied to Sweden product-only revenue (reagents, consumables, and instruments), rather than totals that also fold in broader lab service fees or adjacent software lines.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 349.10 M (2025) | |

| Industry Publisher A | USD 913.60 M (2024) | This figure appears to use a wider revenue capture that can include data management software and services, which expands the market beyond the core IVD product basket counted here. |

| Strategy Consultancy B | USD 629.43 M (2023) | This number is anchored to an earlier base year and may apply higher assumed testing intensity or a different average price progression for higher value test areas, which can lift modeled revenue totals. |

The spread across the table is mainly explained by what gets counted and how pricing and timing assumptions are applied, not by a disagreement that Sweden has meaningful IVD demand. By keeping the inputs tied to repeatable demand signals and clear product categories, the total is easier to reconcile when assumptions are updated.

Key Questions Answered in the Report

What is the current value of the Sweden in-vitro diagnostics market?

The Sweden in-vitro diagnostics market is valued at USD 366.97 million in 2026 and is set to grow to USD 471.04 million by 2031.

Which test category shows the fastest growth in Sweden?

Molecular diagnostics leads with a 7.29% CAGR due to nationwide precision-medicine funding and the wider adoption of genomic panels.

How significant is point-of-care testing in Swedish healthcare?

POCT is the fastest-expanding test location, advancing at a 8.74% CAGR, especially in northern remote regions where on-site results reduce travel burdens.

Why do reagents dominate revenue over instruments?

Reagents account for 64.72% of spending because they are consumed with every test, ensuring steady, recurring revenue streams for suppliers.

What regulatory framework governs IVD products in Sweden?

All IVDs must comply with the European Union IVDR, which imposes rigorous clinical-evidence and Notified-Body certification requirements.

Page last updated on: