Post-Quantum Cryptography Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

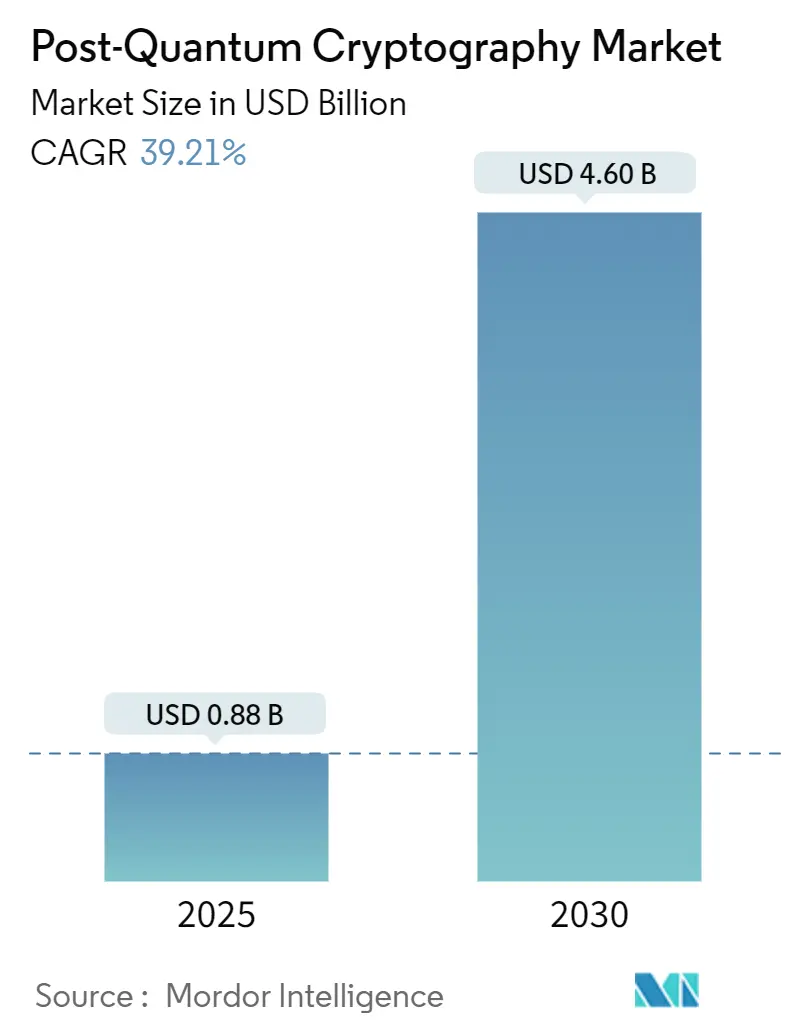

| Market Size (2025) | USD 0.88 Billion |

| Market Size (2030) | USD 4.60 Billion |

| Growth Rate (2025 - 2030) | 39.21% CAGR |

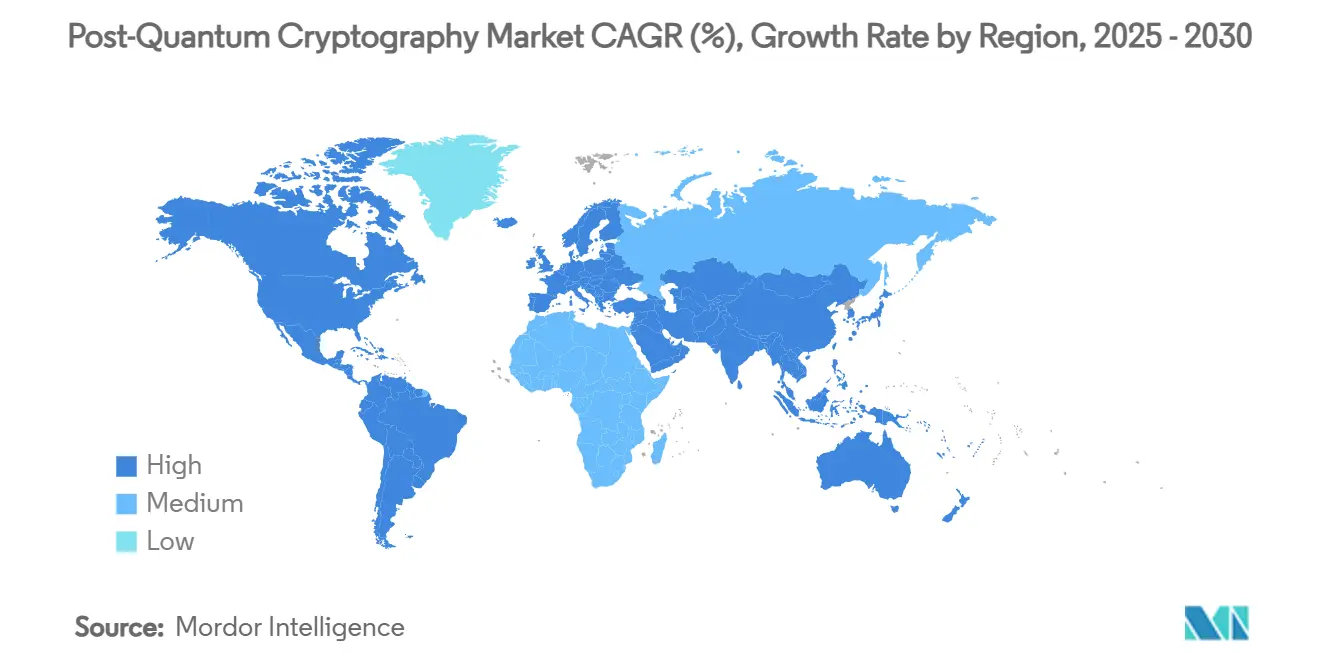

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Post-Quantum Cryptography Market Analysis by Mordor Intelligence

The post-quantum cryptography market size stands at USD 0.88 billion in 2025 and is forecast to reach USD 4.60 billion by 2030, advancing at a 39.27% CAGR.[1]Martyn Warwick, “NIST Issues First Three Quantum-Secure Encryption Standards,” TelecomTV, telecomtv.com Heightened regulatory urgency, the first three NIST standards, and rapid federal budget allocations are accelerating procurement cycles across government, defense, and critical-infrastructure operators. Cloud hyperscale’s are embedding quantum-safe controls as managed services, shrinking adoption barriers for enterprises that lack deep cryptography skills. Meanwhile, hardware security module (HSM) refresh cycles and the need to future-proof 5G-to-6G networks are creating predictable replacement demand. A parallel rise in venture funding for specialist vendors indicates sustained innovation, yet implementation risk remains as organizations juggle algorithm stability, performance overhead, and brown-field migration hurdles.

Key Report Takeaways

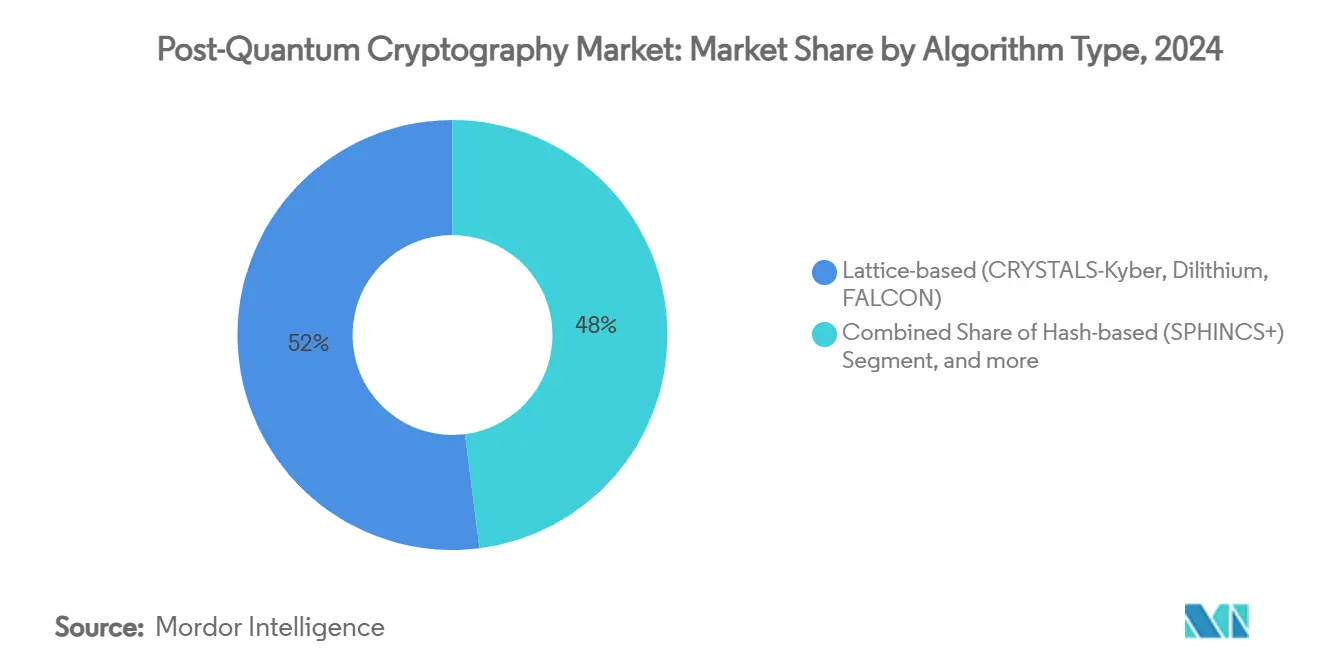

- By algorithm type, lattice-based schemes held 52% revenue share in 2024; code-based cryptography is projected to grow at a 45.31% CAGR through 2030.

- By deployment mode, on-premises solutions accounted for 46% of the post-quantum cryptography market share in 2024, while cloud-hosted deployments are set to expand at a 44.85% CAGR up to 2030.

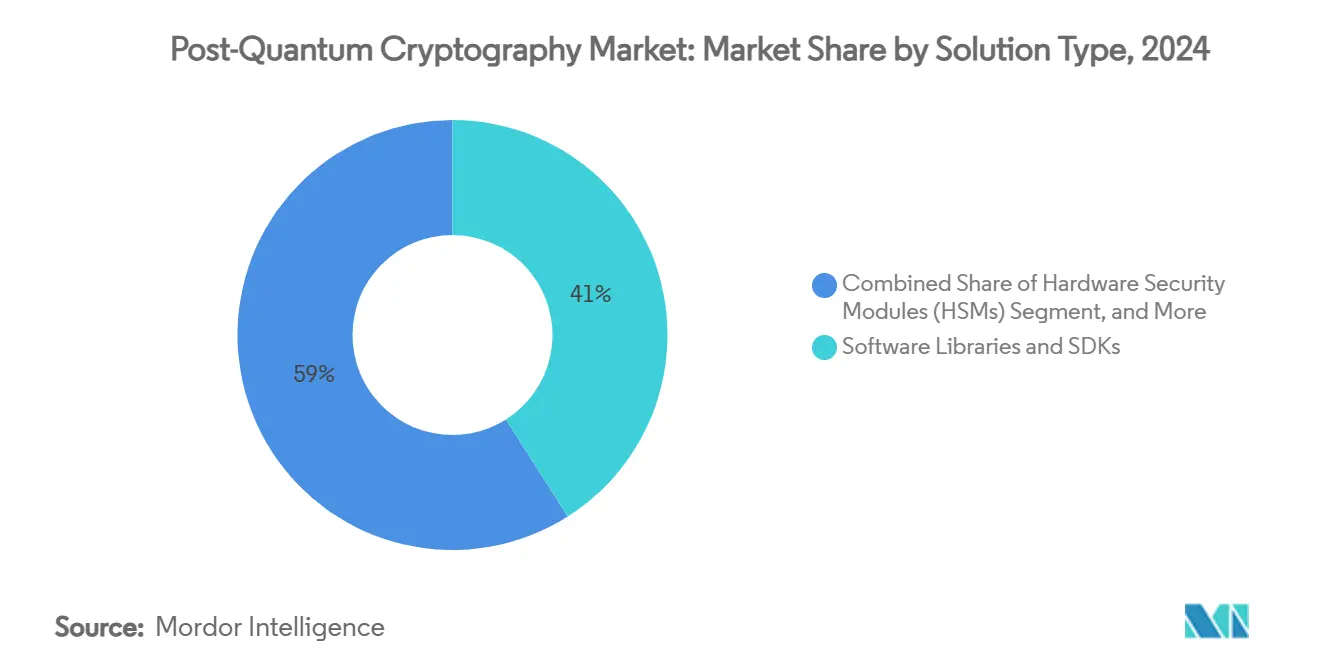

- By solution type, software libraries and SDKs captured 41% of the post-quantum cryptography market size in 2024; services represent the fastest trajectory with a 46.03% CAGR to 2030.

- By end-user industry, government and defense led with 30% share in 2024; telecommunications and IT are positioned for the highest growth at a 44.07% CAGR through 2030.

- By geography, North America commanded 38% of 2024 revenue, whereas Asia-Pacific is forecast to climb at a 46.55% CAGR during 2025-2030.

Market Trends and Insights

Drivers Impact Analysis of Post-Quantum Cryptography Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mainstream rapid federal-level compliance mandates | +8.50% | North America and EU, spill-over to APAC | Short term (≤ 2 years) |

| Routine refresh cycles of HSMs and TLS stacks | +6.20% | Global, concentrated in financial hubs | Medium term (2-4 years) |

| Cloud-native PQC integration by hyperscalers | +7.80% | Global, led by North America and Europe | Medium term (2-4 years) |

| Standard-driven vendor consolidation | +4.10% | Global, accelerated in mature markets | Long term (≥ 4 years) |

| Automotive and IoT firmware-signing urgency | +5.90% | APAC core, expansion to North America | Medium term (2-4 years) |

| Quantum-safe VPN demand in critical infra | +3.80% | Global, priority in government sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Mainstream Rapid Federal-Level Compliance Mandates

Federal procurement rules are compressing adoption timelines. The White House earmarked USD 7.1 billion for agency-wide migrations, mandating asset inventories and transition plans by 2026. Comparable directives from the European Commission set synchronized milestones for 18 member states, requiring quantum-safe controls in critical infrastructure by 2030.[2]European Commission, “EU Reinforces Its Cybersecurity with Post-Quantum Cryptography,” digital-strategy.ec.europa.eu Contractors that fail to comply risk disqualification from government tenders, producing a multiplier effect across defense supply chains. The clarity of legislative timetables reduces budget uncertainty and pushes projects into active execution phases. Collectively, these mandates lift short-term deployment volumes across the post-quantum cryptography market.

Routine Refresh Cycles of HSMs and TLS Stacks

Organizations replacing hardware security modules are discovering that firmware patches cannot meet post-quantum performance thresholds. New HSM lines from Thales and Utimaco feature enlarged key stores and optimized arithmetic to handle ML-KEM and Dilithium workloads. Parallel TLS-stack upgrades necessitate simultaneous certificate-authority changes, application rewrites, and network reconfigurations, driving multi-year consulting engagements. Financial institutions such as JPMorgan Chase have adopted hybrid key-agreement models to maintain backward compatibility during phased rollouts. Hardware refresh budgeting therefore dovetails neatly with post-quantum migration funding, sustaining global demand through 2029.

Cloud-Native PQC Integration by Hyperscale’s

Google Cloud added ML-KEM to its Key Management Service API, while AWS released quantum-safe VPN endpoints for site-to-site tunnels, shifting cryptographic heavy lifting onto platform layers. Microsoft’s SymCrypt upgrade embeds the entire first wave of NIST algorithms across Azure workloads. Customers benefit from zero-touch updates, mitigating skills gaps that might otherwise stall adoption. The model also deepens dependency on platform tooling, locking in workloads and creating durable revenue streams inside the post-quantum cryptography market.

Standard-Driven Vendor Consolidation

NIST’s definitive standards-FIPS 203, 204, 205-reduce algorithm uncertainty and shrink the list of credible product suppliers. Incumbent security vendors with certified code bases are partnering to accelerate time-to-market rather than pursuing outright acquisitions, as seen in PQShield’s USD 37 million Series B round led jointly by strategic investors. Consolidation streamlines procurement for conservative buyers but intensifies feature competition, especially around crypto-agility and performance optimizations. The pattern points to long-run margin expansion for companies that secure early certification.

Restraints Impact Analysis of Post-Quantum Cryptography Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Migration complexity of brown-field systems | -4.20% | Global, acute in mature markets | Medium term (2-4 years) |

| Performance overhead versus classical crypto | -3.10% | Global, critical in latency-sensitive apps | Short term (≤ 2 years) |

| Algorithm-break uncertainty after SIKE incident | -2.80% | Global, heightened in risk-averse sectors | Long term (≥ 4 years) |

| Short-term budget diversion to Gen-AI security | -1.90% | North America and EU, emerging in APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Migration Complexity of Brown-Field Systems

Legacy banking cores, healthcare EMRs, and SCADA platforms embed cryptographic routines deep inside business logic, making rip-and-replace infeasible. Partial upgrades risk interoperability failures and security gaps, yet full rewrites can disrupt mission-critical operations. The resulting analysis-to-implementation loops lengthen project timelines and depress short-term volume in the post-quantum cryptography market.

Performance Overhead Versus Classical Crypto

Initial benchmarks show Dilithium signatures demanding roughly 10 × the compute cycles of RSA-2048, while ML-KEM key exchanges enlarge handshake packets by up to 3 KB. Latency-sensitive environments-high-frequency trading and time-critical IoT-therefore perceive an immediate performance tax. Hardware accelerators are closing the gap, yet perceived risk slows procurement until performance parity is validated under production loads.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Post-Quantum Cryptography Market Segment Analysis

By Algorithm Type:

Lattice-Based Dominance Faces Code-Based ChallengeLattice schemes accounted for 52% of 2024 revenue in the post-quantum cryptography market, driven by FIPS-203 Kyber and FIPS-204 Dilithium certifications. The mathematical hardness of lattice problems, relatively compact key sizes, and availability of open-source reference code accelerated uptake across public-sector networks and hyperscale datacentres. Adoption momentum is reinforced by dedicated lattice cores appearing in next-generation HSM silicon, which reduce latency penalties that once discouraged performance-sensitive users.

Code-based cryptography is advancing at a 45.31% CAGR to 2030, moving from academic niche to commercial deployment as Classic McEliece gains tooling support. Long-established cryptanalytic scrutiny boosts buyer confidence, making the scheme attractive for archival storage, secure email gateways, and satellite command links where decapsulation speed outweighs key size constraints. The SIKE failure shifted demand away from isogeny-based options and highlighted the importance of mature algebraic foundations. HQC’s 2025 selection for standardization further diversifies algorithm portfolios.[4]Hans Martin Lauridsen, “HQC Chosen for NIST’s Post-Quantum Cryptography Standardization,” Cryptomathic, cryptomathic.com

By Deployment Mode:

Cloud Migration Accelerates Despite On-Premises LeadershipOn-premises deployments retained 46% share in 2024, reflecting regulatory demands for sovereign key custody among defense, finance, and healthcare players. These users value deterministic control over key material, rigorous audit trails, and air-gapped disaster-recovery designs. Vendors supply hardened appliances that slot directly into existing data-center racks, easing certification.

Cloud-hosted models are expanding at a 44.85% CAGR as Google, AWS, and Microsoft deliver quantum-safe primitives as managed functions within their platforms. Enterprises migrate less-sensitive workloads first, taking advantage of automatic key rotations and SLA-backed security patches. Hybrid designs-local keys for crown-jewel data, cloud keys for peripheral workloads—are emerging as the default architecture. This strategy balances regulatory compliance with the operational agility promised by the post-quantum cryptography market.

By Solution Type:

Services Growth Reflects Implementation ComplexitySoftware libraries and SDKs comprised 41% of 2024 spend, supplying developer-friendly wrappers around cryptographic kernels. OpenSSL, BoringSSL, and LibOQS releases containing Kyber and Dilithium serve as the connective tissue linking applications to quantum-safe primitives. Early adopters leverage these libraries for pilot deployments and proof-of-concept sprints.

Professional services, however, grow fastest at 46.03% CAGR. Enterprises discover that post-quantum migrations require asset discovery, risk modelling, change-management, and staff retraining. Consulting practices that merge cryptographic depth with sector expertise command premium rates. Integrators build bespoke migration runbooks, certify crypto-agile DevSecOps pipelines, and orchestrate multi-vendor rollouts, driving sustained billings across the post-quantum cryptography industry.

By End-User Industry:

Government Leadership Drives Private Sector AdoptionGovernment and defense entities delivered 30% of 2024 revenue, underpinned by statutory mandates and long procurement cycles that lock in multiyear contracts. Federal agencies fund reference implementations, sponsor open-source audits, and set interoperability baselines that ripple through supplier ecosystems. Their purchases de-risk technology for commercial buyers and create economies of scale for component vendors.

Telecommunications and IT services display the highest momentum, advancing at a 44.07% CAGR. 5G core upgrades, edge MEC nodes, and in-flight 6G research incorporate quantum-safe key management from inception to avoid forklift upgrades mid-decade. Banks, insurers, and capital-market platforms follow closely, motivated by the extended archival requirements for financial records and systemic-risk regulation. Healthcare adopts more cautiously because of strict data-integrity certifications, yet once projects launch, they encompass entire hospital networks, driving lumpy but sizeable deals inside the post-quantum cryptography market.

Geography Analysis

North America Post-Quantum Cryptography Market

North America held a 38% revenue share in 2024, buoyed by NIST stewardship, abundant venture capital, and the White House’s multibillion-dollar migration budget. Silicon Valley firms collaborate with federal research labs, yielding rapid algorithm maturation and early hardware accelerators for Kyber and Dilithium workloads. Mandatory compliance timelines force federal agencies and their contractors onto synchronized implementation paths, generating predictable pipeline visibility for suppliers. Canada follows the U.S. roadmap through CSE guidance, aligning public-sector requirements and stimulating cross-border procurement synergies.

APAC Post-Quantum Cryptography Market

Asia-Pacific is the fastest-growing region at a 46.55% CAGR. China’s national quantum strategy funds both computing hardware and quantum-resistant cryptography, pushing domestic vendors to embed Kyber alternatives inside telecom gear exported under the Belt and Road framework. Japan’s NEDO initiative dedicates USD 15 million to post-quantum pilots across finance and manufacturing, partnering with PQShield to supply reference libraries.[3]Cath Firmin, “PQShield Announces Participation in NEDO Program to Implement Post-Quantum Cryptography Across Japan,” pqshield.com Singapore’s financial-hub status draws regional banks into early migration programs, while South Korea seeds research grants to integrate quantum-safe protocols into 6G base-station silicon.

EMEA Post-Quantum Cryptography Market

Europe coordinates adoption through an EU-level roadmap ratified by 18 member states, targeting critical-infrastructure compliance no later than 2030. Germany’s BSI issues technical guidelines, France and the Netherlands co-chair working groups, and pan-European utilities pilot quantum-safe VPNs for cross-border energy grids. Middle East and Africa represent emerging demand pockets driven by sovereign-digital initiatives-Saudi Arabia’s Vision 2030 and the UAE’s federal cloud frameworks embed quantum-safe requirements at the architectural blueprint stage.

Competitive Landscape

The post-quantum cryptography market remains moderately fragmented, with traditional security vendors, quantum-native start-ups, and hyperscale cloud providers converging on overlapping value propositions. Thales, Entrust, and Utimaco translate certification expertise into updated HSM lines that slot into regulated industries. Quantum specialists such as PQShield and Quantinuum focus on lightweight algorithm implementations and formal verification, gaining traction in automotive firmware and IoT silicon. AWS, Microsoft Azure, and Google Cloud integrate FIPS-203/204 primitives natively, positioning managed services as the simplest path for enterprises lacking cryptography talent.

Strategic partnerships eclipse outright acquisitions. IBM collaborates with universities for algorithm research while embedding lattice accelerators in its z-Systems mainframes. Cisco aligns with QuSecure to retrofit routers via software only, reducing customer disruption. Funding flows heavily toward seed and Series B rounds-PQShield’s USD 37 million raise confirms investor appetite for pure-play suppliers. The SIKE collapse reiterates demand for crypto-agility, encouraging vendors to market pluggable algorithm frameworks rather than single-method offerings. Over the forecast window, supplier consolidation is expected through alliances that pool certification costs, while customer lock-in will hinge on performance benchmarks and key-management ergonomics.

Post-Quantum Cryptography Industry Leaders

IBM Corporation

Microsoft Corporation

Thales Group

Quantinuum Ltd.

PQShield Ltd.

- *Disclaimer: Major Players sorted in no particular order

Post-Quantum Cryptography Market Companies Covered in this Report

- IBM Corporation

- Microsoft Corporation

- Thales Group

- Quantinuum Ltd.

- PQShield Ltd.

- Infineon Technologies AG

- Huawei Technologies Co., Ltd.

- Samsung Electronics Co., Ltd.

- Crypto4A Technologies Inc.

- SandboxAQ Inc.

- Cisco Systems, Inc.

- AWS (Amazon Web Services, Inc.)

- Google LLC

- Eviden (Atos SE)

- Securosys SA

- Nokia Corporation

- Entrust Corporation

- ISARA Corporation

- Keyfactor Inc.

- DigiCert Inc.

Recent Industry Developments in Post-Quantum Cryptography Market

- July 2025: NIST selected HQC during its fourth-round process, with draft standards slated for 2026 and final text in 2027.

- June 2025: The European Commission issued a coordinated quantum-safe roadmap endorsed by 18 EU states, fixing 2030 as the final compliance deadline for critical infrastructure.

- June 2025: QuSecure launched QuProtect Core Security to harden Cisco routers without hardware changes.

- April 2025: Keyfactor expanded certificate lifecycle management to cover FIPS-203, 204, and 205 inside its PKI platform.

Global Post-Quantum Cryptography Market Report Scope

Segmentation Overview

| Lattice-based (CRYSTALS-Kyber, Dilithium, FALCON) |

| Hash-based (SPHINCS+) |

| Code-based (Classic McEliece) |

| Multivariate-based (Rainbow, GeMSS) |

| Isogeny-based (SIKE, CSIDH) |

| On-premises |

| Cloud / Hosted |

| Hybrid |

| Software Libraries and SDKs |

| Hardware Security Modules (HSMs) |

| Services (Consulting, Integration, Audits) |

| Government and Defense |

| Banking, Financial Services and Insurance (BFSI) |

| Telecom and IT |

| Healthcare and Life Sciences |

| Critical Infrastructure and Energy |

| Other Industries (Manufacturing, Retail, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| Segmentation by Algorithm Type | Lattice-based (CRYSTALS-Kyber, Dilithium, FALCON) | |

| Hash-based (SPHINCS+) | ||

| Code-based (Classic McEliece) | ||

| Multivariate-based (Rainbow, GeMSS) | ||

| Isogeny-based (SIKE, CSIDH) | ||

| Segmentation by Deployment Mode | On-premises | |

| Cloud / Hosted | ||

| Hybrid | ||

| Segmentation by Solution Type | Software Libraries and SDKs | |

| Hardware Security Modules (HSMs) | ||

| Services (Consulting, Integration, Audits) | ||

| Segmentation by End-User Industry | Government and Defense | |

| Banking, Financial Services and Insurance (BFSI) | ||

| Telecom and IT | ||

| Healthcare and Life Sciences | ||

| Critical Infrastructure and Energy | ||

| Other Industries (Manufacturing, Retail, etc.) | ||

| Segmentation by Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the post-quantum cryptography market by 2030?

The post-quantum cryptography market size is set to reach USD 4.60 billion by 2030, growing at a 39.27% CAGR.

Which algorithm family holds the largest revenue share?

Lattice-based schemes, led by Kyber and Dilithium, commanded 52% of 2024 revenue.

Which deployment mode is expanding fastest?

Cloud-hosted implementations are advancing at a 44.85% CAGR as hyperscalers embed quantum-safe services.

Why are government mandates influential in adoption?

Statutory deadlines require agencies and contractors to migrate by 2026, guaranteeing early-stage demand and shaping vendor roadmaps.

Which region is expected to grow most rapidly?

Asia-Pacific is forecast to expand at a 46.55% CAGR, driven by China’s quantum investments and Japan’s NEDO program.

How does performance overhead affect adoption?

Post-quantum algorithms increase compute cycles and packet sizes, posing challenges for latency-sensitive workloads until hardware accelerators close the gap.

Page last updated on: