Cloud Encryption Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 4.90 Billion |

| Market Size (2030) | USD 14.59 Billion |

| Growth Rate (2025 - 2030) | 24.38% CAGR |

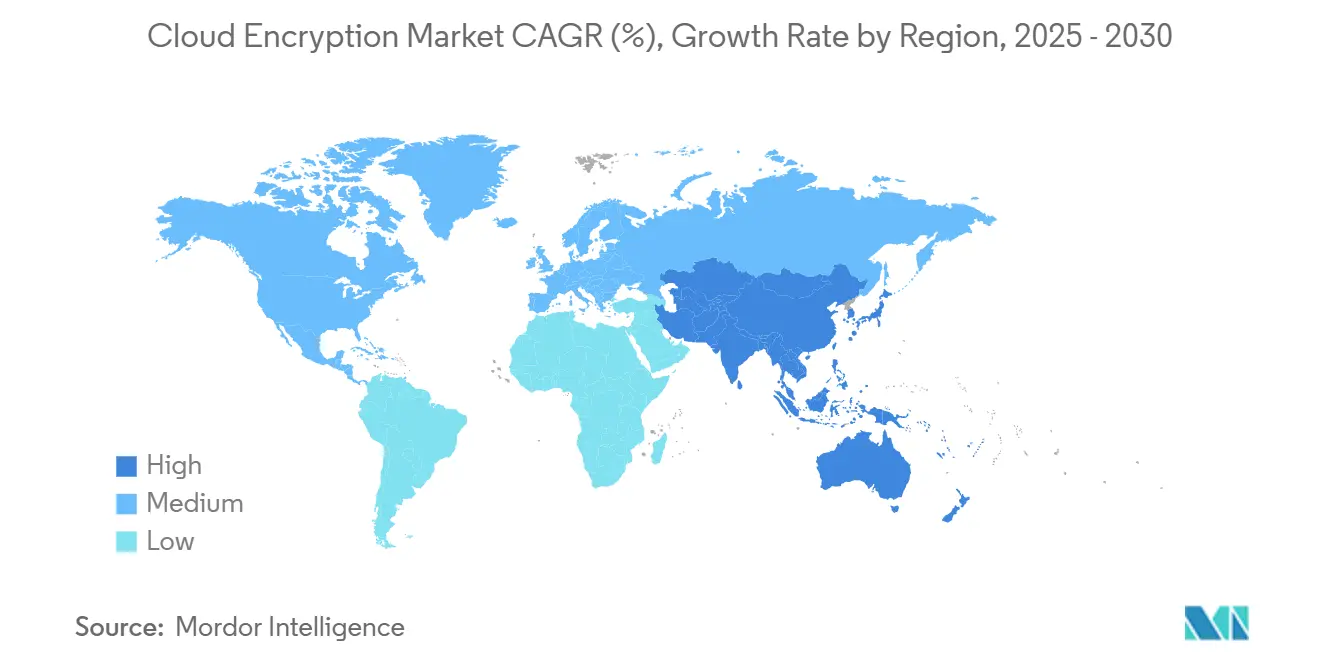

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

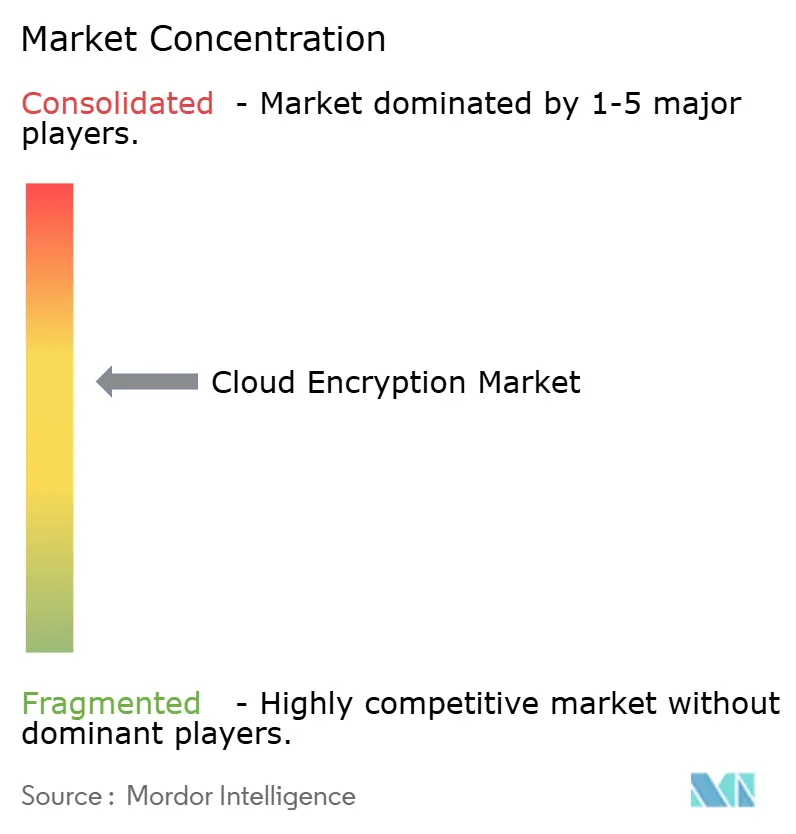

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Encryption Market Analysis by Mordor Intelligence

The cloud encryption market size is expected to reach USD 4.90 billion in 2025 and is projected to grow to USD 14.59 billion by 2030, expanding at a 24.38% CAGR. Accelerated uptake of multi-cloud strategies, rapid digital transformation among small and mid-sized enterprises, and intensifying regulatory oversight are the strongest growth catalysts. Software-defined encryption remains the architectural cornerstone; however, demand for managed services is rising quickly as organizations grapple with quantum-safe deployment, confidential computing integrations, and multi-cloud key orchestration. Regional dynamics are equally pronounced: North America maintains the largest revenue lead, while the Asia-Pacific region records the fastest expansion, driven by SME cloud migrations and evolving data-sovereignty regimes.[1]Cloud Security Alliance, “Global Data Sovereignty: A Comparative Overview,” cloudsecurityalliance.org Competitive positioning hinges on end-to-end key control, post-quantum readiness, and seamless policy enforcement across heterogeneous infrastructure.

Key Report Takeaways

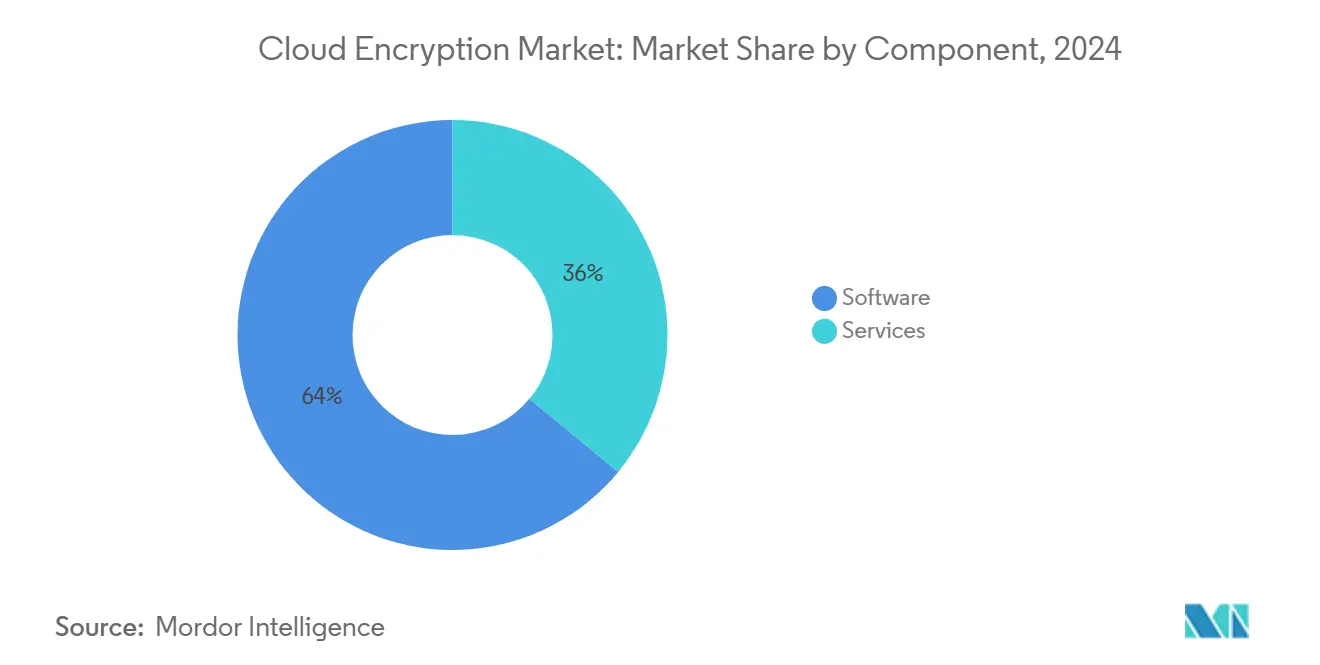

- By component, Software led with 64% of the cloud encryption market share in 2024; Services is projected to grow at a 29.10% CAGR to 2030.

- By service model, IaaS held 46% revenue share in 2024; SaaS solutions are forecast to rise at a 31.50% CAGR through 2030.

- By cloud type, Public Cloud accounted for 59% of the cloud encryption market size in 2024, while Hybrid Cloud is projected to advance at a 33.20% CAGR through 2030.

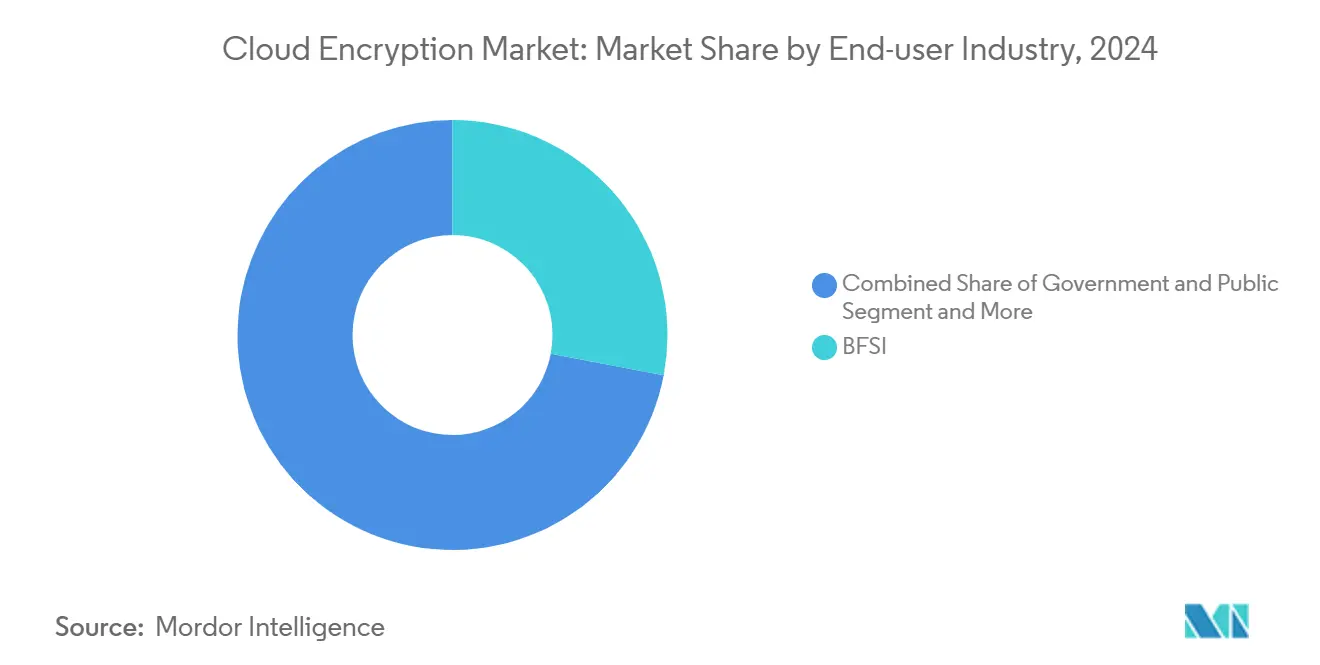

- By end-user industry, BFSI held 28% share of the cloud encryption market size in 2024; Healthcare and Life Sciences are expanding at a 28.40% CAGR through 2030.

- By enterprise size, large enterprises controlled 71% of the cloud encryption market in 2024, whereas the SME segment is projected to grow at a 27.30% CAGR to 2030.

- By geography, North America held a 34% market share in the cloud encryption market in 2024, whereas the Asia-Pacific segment is projected to grow at a 24% CAGR through 2030.

Global Cloud Encryption Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion of multi-cloud and edge workloads | +7.2% | Global (notably North America and Europe) | Medium term (2–4 years) |

| Tightening global data-sovereignty laws | +5.8% | Europe, Asia-Pacific, North America | Medium term (2–4 years) |

| SaaS proliferation across regulated verticals | +4.5% | Global (early adoption in North America) | Short term (≤ 2 years) |

| Quantum-safe encryption urgency | +2.9% | North America, Europe | Long term (≥ 4 years) |

| Confidential-computing integrations | +2.1% | North America, Europe | Medium term (2–4 years) |

| Gen-AI assisted key-management automation | +1.8% | Global (early adoption in North America) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Explosion of Multi-Cloud and Edge Workloads

Enterprises now spread applications across several public clouds and edge nodes, with 86% pursuing multi-cloud strategies in 2025. Dispersed workloads shatter the traditional perimeter, forcing teams to enforce uniform encryption policies across dissimilar control planes. Edge-first architectures intensify complexity because encryption must execute with minimal latency at the point of data creation. Deep observability and AI-driven anomaly detection are therefore being embedded into encryption workflows to sustain visibility across clouds while shielding sensitive workloads from lateral movement.

Tightening Global Data-Sovereignty Laws

Regulations such as GDPR, China’s PIPL, and Brazil’s LGPD stipulate that data remain subject to local jurisdiction, compelling multinational firms to rethink cloud placement and key custody. Centralized key management, coupled with location-aware encryption, has become an indispensable compliance tool, especially where the Digital Operational Resilience Act (DORA) requirements mandate demonstrable control over encryption keys held in third-party clouds. Organizations are increasingly weighing the repatriation of high-risk workloads to sovereign facilities while maintaining selective public-cloud utilization for scalability.

SaaS Proliferation Across Regulated Verticals

Healthcare, finance, and public-sector entities intensify their SaaS adoption to streamline core processes, yet they face strict mandates for record confidentiality, transaction integrity, and auditability. Encryption must extend from the application layer through transport and storage without degrading the end-user experience. Providers that secure SOC 2, ISO/IEC 27001, and CSA STAR certifications are gaining share, as customers demand verifiable cryptographic controls before onboarding mission-critical workloads.

Quantum-Safe Encryption Urgency

Advances in quantum hardware threaten to render RSA and ECC obsolete, prompting collaboration between cloud hyperscalers and standards bodies to finalize lattice- and code-based algorithms. Early adopters are integrating post-quantum suites into test environments, prioritizing migration paths that do not disrupt current TLS or VPN channels. ETSI’s 2025 Quantum Safe Cryptography Conference brought together AWS, Telefonica, and the ECB to accelerate the standardization of lattice-based algorithms.[2]ETSI, “ETSI/IQC Quantum Safe Cryptography Conference 2025,” etsi.org The shift is critical for the long-term confidentiality of data archived today, which must remain protected for decades, particularly in financial services, defense, and healthcare.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High performance overhead in low-latency apps | −3.2% | Global (notably North America and Asia-Pacific) | Short term (≤ 2 years) |

| Key escrow and lifecycle complexity | −2.8% | Global | Medium term (2–4 years) |

| Fragmented cloud-native security standards | −1.9% | Global (higher impact where regulations are strict) | Medium term (2–4 years) |

| Geo-sovereignty barriers to key export | −1.5% | Europe, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Performance Overhead in Low-Latency Apps

Real-time trading, industrial control, and immersive media demand millisecond responsiveness; yet encrypt-decrypt cycles add compute drag and jitter. Hardware offload cards and streamlined ciphers are easing the burden, but many enterprises still selectively bypass encryption in latency hotspots, exposing isolated data flows to risk. Until next-generation accelerators become ubiquitous, the tension between throughput and confidentiality will persist.

Key Escrow and Lifecycle Complexity

Generating, distributing, rotating, and revoking keys across multiple cloud strains operational resources. Fewer than 10% of enterprises encrypt 80% or more of cloud-resident data, underscoring sizable protection gaps. Unified key-management-as-a-service offerings are gaining traction, but heterogenous policy frameworks and provider-specific APIs still complicate true crypto agility, especially when incorporating post-quantum algorithms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominates While Services Accelerate

Software controlled 64% of 2024 revenue, underscoring its foundational role in deploying at-rest and in-transit ciphers across storage, VM, and container layers. Mature toolsets bundle granular policy engines, role-based access, and AES-256 support, enabling consistent enforcement throughout DevSecOps pipelines. Vendors continuously update libraries to accommodate emerging algorithms and to embed hardware offload for performance-sensitive paths.

Services expand at a 29.10% CAGR as organizations confront cloud-native sprawl. Third-party experts design, run, and audit encryption estates spanning confidential-compute clusters, hybrid gateways, and post-quantum testbeds. Engagement scope often covers crypto-agil,ity road mapping, and zero-trust alignment, filling workforce gaps, and accelerating compliance certification.

By Service Model: IaaS Foundations Support SaaS Growth

Infrastructure-layer encryption underpins every higher-order service, and IaaS retained a 46% share in 2024. Customers depend on provider-supplied boot-volume ciphers, block-storage key services, and encrypted object stores to secure core compute and network constructs. Integration with organization-owned hardware security modules enables regulated workloads to meet stringent audit requirements.

SaaS encryption outpaces the market at a 31.50% CAGR as application portfolios migrate to cloud subscription models. Each workload, customer relationship management, electronic health records, or treasury management, requires seamless data protection without altering user workflows. Providers embedding field-level encryption, bring-your-own-key frameworks, and strong certificate pinning win new customers in finance and healthcare.

By Cloud Type: Hybrid Deployments Outpace Public Cloud

Although public platforms still generated 59% of 2024 revenue, the hybrid approach advances at a 33.20% CAGR. Enterprises keep sensitive datasets in private or sovereign locations while bursting less sensitive analytics to hyperscale clusters. Unified policy planes maintain key custody across both realms, ensuring compliance with jurisdictional statutes while tapping public scalability for ephemeral workloads.

Hybrid success rides on consistent encryption orchestration that spans physical data centers and multiple public providers. Solutions exposing centralized key vault APIs, automation hooks, and hardware-rooted trust effectively neutralize inter-platform discrepancies, paving the way for smooth workload mobility and resilience.

By End-user Industry: BFSI Leads While Healthcare Accelerates

Financial services retained a 28% revenue share in 2024, underscoring the indispensability of encryption for transaction integrity, regulatory compliance, and zero-trust adoption. Sector standards stress continuous identity verification and dual-control key ceremonies, making comprehensive encryption non-negotiable.

Healthcare and Life Sciences are growing at the fastest rate, with a 28.40% CAGR, as electronic health record repositories expand and Internet of Medical Things devices proliferate. Attack surfaces enlarge, breach costs rise, and regulators tighten audit scope. Clinicians, therefore, roll out full-stack encryption, from sensor to cloud analytic cluster, coupled with strict role segregation and immutable audit logging.

By Enterprise Size: Large Enterprises Dominate While SMEs Catch Up

Large Enterprises commanded 71% of 2024 spending due to broad IT estates, high data classification complexity, and bigger compliance penalties. These firms deploy layered defenses including data-in-use protections through confidential computing, post-quantum pilots, and machine-learning monitoring of encrypted traffic.

SMEs close the gap at a 27.30% CAGR. Affordable pay-as-you-go key-management services and automated policy templates lower technical barriers, enabling smaller firms to safeguard their intellectual property and customer data without dedicated security staff. Adoption is especially strong across the Asia-Pacific’s SME ecosystem, where cloud services underpin digital-commerce expansion.

Geography Analysis

North America held 34% of the cloud encryption market in 2024, propelled by early cloud adoption, strict sectoral mandates, and hyperscaler innovation. Financial institutions, healthcare providers, and federal agencies advance zero-trust blueprints that place encryption at every trust boundary. Collaboration between large cloud providers and NIST on post-quantum cryptography accelerates standards convergence, further entrenching the region’s leadership.

The Asia-Pacific region delivers the fastest trajectory, with a 24% CAGR. SMEs, which constitute over 97% of businesses, are embracing cloud platforms to achieve operational agility. National data-residency laws in China, India, and Indonesia drive demand for sovereign-ready key-management deployments. Hyperscalers respond with region-specific availability zones and partner-run key vaults, enabling customers to comply without sacrificing scalability.

Europe faces stringent compliance requirements under the GDPR and the forthcoming Digital Operational Resilience Act rules. Organizations emphasize the importance of sovereign key ownership and the selective placement of workloads within EU-based data centers. Sovereign cloud initiatives with in-region hardware security modules gain traction, allowing enterprises to meet legal demands while leveraging elastic compute economics.

Competitive Landscape

The cloud encryption market exhibits moderate concentration, with the top five providers accounting for a significant share of the global revenue. Amazon Web Services, Microsoft Azure, and Google Cloud anchor this leadership by embedding default data-at-rest and data-in-transit ciphers, central key vaults, and hardware-rooted attestation into their platforms. Each hyperscaler keeps expanding encryption coverage. AWS now offers Bring-Your-Own-Key for 100+ services, Azure extends confidential-compute nodes across every region, and Google Cloud equips its External Key Manager with post-quantum options, so that customers can satisfy industry mandates without bolt-on tools.

Scale, however, is not the only differentiator. Thales, Fortanix, and Virtru win market share by focusing on data-centric policy engines, tokenization, and sovereign key custody that work consistently across multicloud estates. Thales recently added Hardware Security Module-as-a-Service nodes inside new EU sovereign zones, while Fortanix integrated Intel Trust Domain Extensions to seal keys inside processor enclaves for confidential analytics. Virtru, meanwhile, offers packaged client-side encryption software development kits that enable SaaS builders to insert field-level protection without rewriting application logic.

Innovation from emerging specialists further intensifies rivalry. Arqit Quantum combines lattice-based algorithms with confidential computing, ensuring that even cloud operators cannot access customer secrets. The company partnered with Dell Technologies in 2025 to co-sell the service to regulated banks.[3]Arqit Quantum Inc., “Arqit Delivers Quantum-Safe Protection Enhanced by Confidential Computing,” arqit.uk CrowdStrike folded real-time data-loss prevention into its Falcon platform to compete for unified endpoint and cloud encryption budgets. Cloudflare has pushed end-to-end post-quantum cryptography into Zero Trust Network Access, providing security teams with a low-friction on-ramp to quantum-safe connectivity ahead of formal NIST ratification.

Cloud Encryption Industry Leaders

IBM Corporation

Broadcom Inc. (Symantec Corporation)

Amazon Web Services

Microsoft Corporation

Google Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: CrowdStrike added Falcon Data Protection features to secure data across endpoints, cloud, GenAI, and SaaS applications.

- March 2025: Cohesity released NetBackup 11.0 with quantum-proof encryption and behavioral analytics for high-risk user activities.

- March 2025: Cloudflare expanded end-to-end post-quantum cryptography to its Zero Trust Network Access service, delivering immediate quantum-safe connectivity.

- November 2024: Echoworx launched a Google Workspace add-on that embeds email encryption natively for more than 6 million business users.

Global Cloud Encryption Market Report Scope

The Cloud Encryption Market Report is Segmented by Component (Software, and Services), Service Model (Infrastructure-As-A-Service (IaaS), Platform-As-A-Service (PaaS), and Software-As-A-Service (SaaS)), Cloud Type (Public Cloud, Private Cloud, and Hybrid Cloud), End-User Industry (BFSI, Government and Public Sector, Retail and e-Commerce, Healthcare and Life Sciences, Energy and Utilities, IT and Telecommunications, and Others), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), and Geography (North America, Europe, Asia Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) |

| Software-as-a-Service (SaaS) |

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| BFSI |

| Government and Public Sector |

| Retail and e-Commerce |

| Healthcare and Life Sciences |

| Energy and Utilities |

| IT and Telecommunications |

| Others (Media, Education) |

| Large Enterprises |

| Small and Medium Enterprises |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Service Model | Infrastructure-as-a-Service (IaaS) | ||

| Platform-as-a-Service (PaaS) | |||

| Software-as-a-Service (SaaS) | |||

| By Cloud Type | Public Cloud | ||

| Private Cloud | |||

| Hybrid Cloud | |||

| By End-user Industry | BFSI | ||

| Government and Public Sector | |||

| Retail and e-Commerce | |||

| Healthcare and Life Sciences | |||

| Energy and Utilities | |||

| IT and Telecommunications | |||

| Others (Media, Education) | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordics | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected CAGR for the cloud encryption market between 2025 and 2030?

The market is forecast to expand at a 24.38% CAGR over the 2025–2030 period.

Which component category currently holds the largest share?

Software holds 64% of revenue due to its critical role in implementing at-rest and in-transit encryption policies.

Why is Asia-Pacific the fastest-growing region?

Rapid SME cloud adoption, expanding digital-economy initiatives, and emerging data-sovereignty regulations fuel a 24% CAGR in Asia-Pacific.

How are organizations preparing for quantum threats?

Enterprises pilot post-quantum cryptography suites and confidential-computing platforms to safeguard data against future quantum decryption risks.

What drives the sharp growth in hybrid cloud encryption?

Enterprises balance compliance and scalability by keeping sensitive records on-premises while bursting other workloads to public clouds, pushing hybrid cloud encryption to a 33.20% CAGR.

Which industry shows the fastest growth in encryption spending?

Healthcare and Life Sciences is advancing at a 28.40% CAGR as digitized patient records and connected medical devices enlarge the threat surface.

Page last updated on: