Quantum Cryptography Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

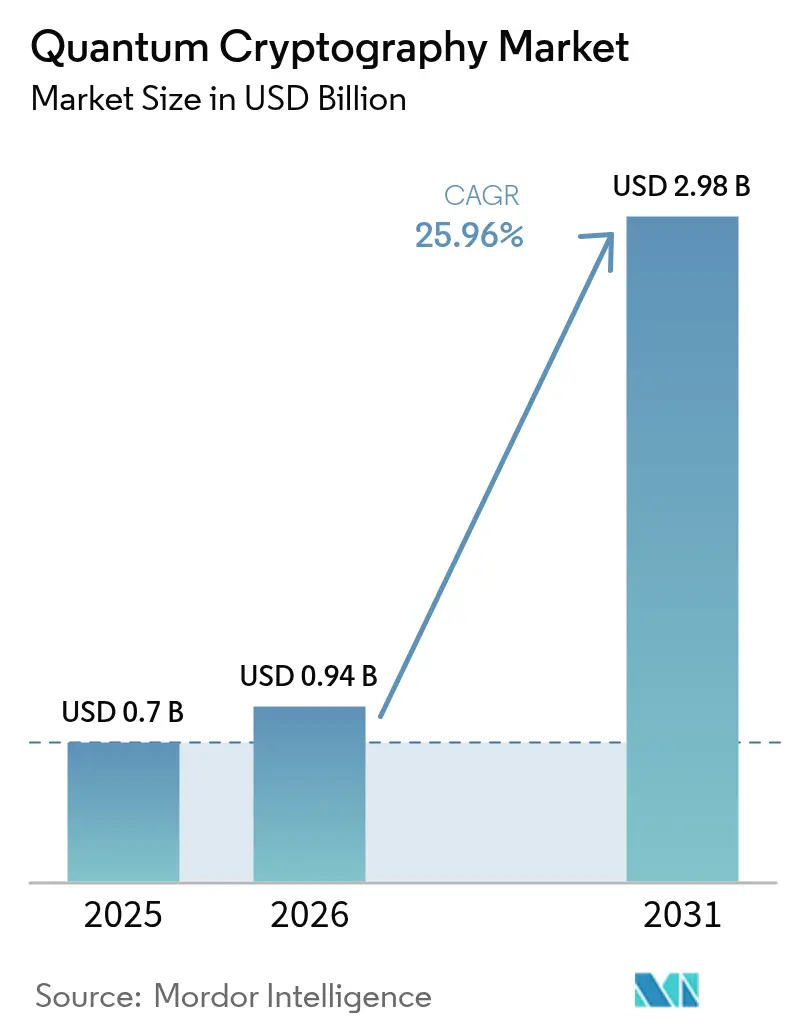

| Market Size (2026) | USD 0.94 Billion |

| Market Size (2031) | USD 2.98 Billion |

| Growth Rate (2026 - 2031) | 25.96% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Quantum Cryptography Market Analysis by Mordor Intelligence

The quantum cryptography market size is projected to expand from USD 0.70 billion in 2025 and USD 0.94 billion in 2026 to USD 2.98 billion by 2031, registering a CAGR of 25.96% between 2026 to 2031. This sharp growth reflects how fast post-quantum threats are pressuring enterprises to migrate from classical encryption to quantum-safe techniques. Government mandates for critical infrastructure, the commercialization of quantum key distribution (QKD) pilot networks, and sustained venture funding for photonic-component start-ups have combined to accelerate deployments. Hardware still dominates early budgets because dedicated single-photon sources and detectors remain the only proven way to defeat quantum-enabled code-breaking, yet service revenues are beginning to outpace products as integration complexity rises. Regional momentum is equally uneven: North America generated the largest portion of 2025 spending, but Asia-Pacific is scaling the most ambitious backbone projects, giving the region first-mover advantages in standard setting and vendor ecosystems.

Key Report Takeaways

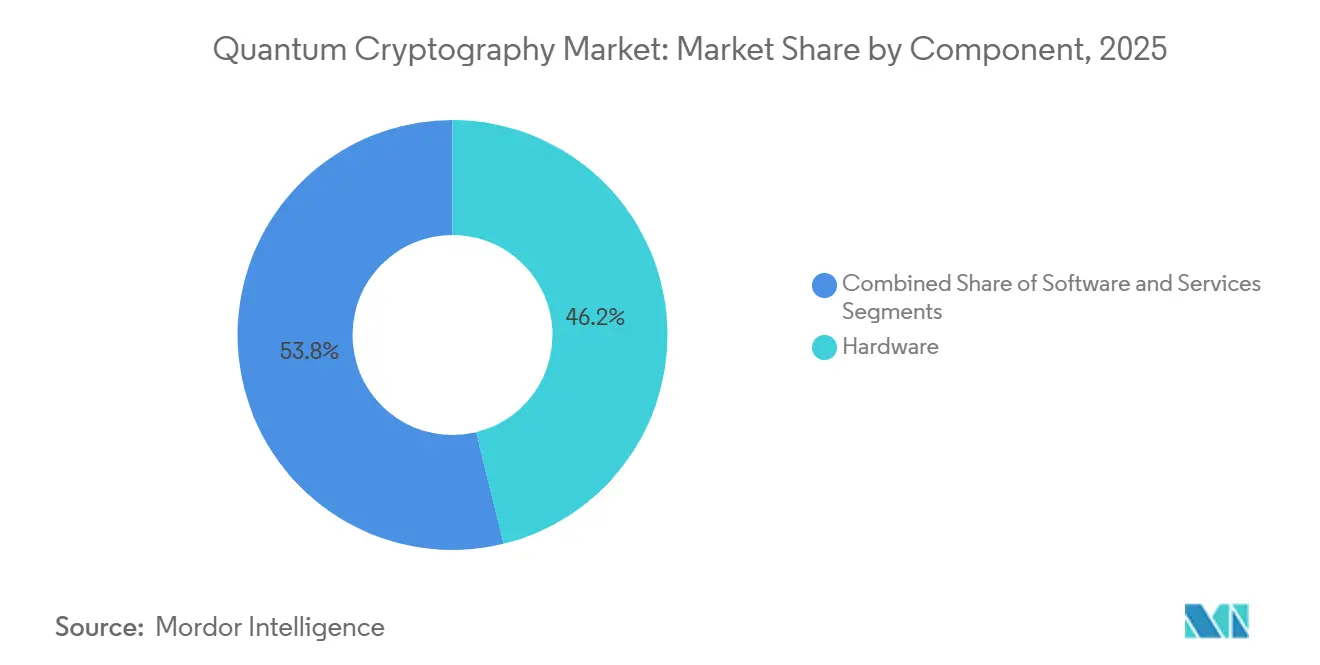

By component, hardware captured 46.19% of 2025 revenue, while services are advancing at a 26.67% CAGR through 2031 as enterprises outsource quantum-security operations.

- By technology, QKD held 54.16% of 2025 revenue, and quantum secure communications platforms are forecast to expand at a 26.91% CAGR to 2031.

- By deployment mode, on-premises architectures represented 57.58% of 2025 installations, whereas hybrid models are projected to grow at 26.48% through 2031.

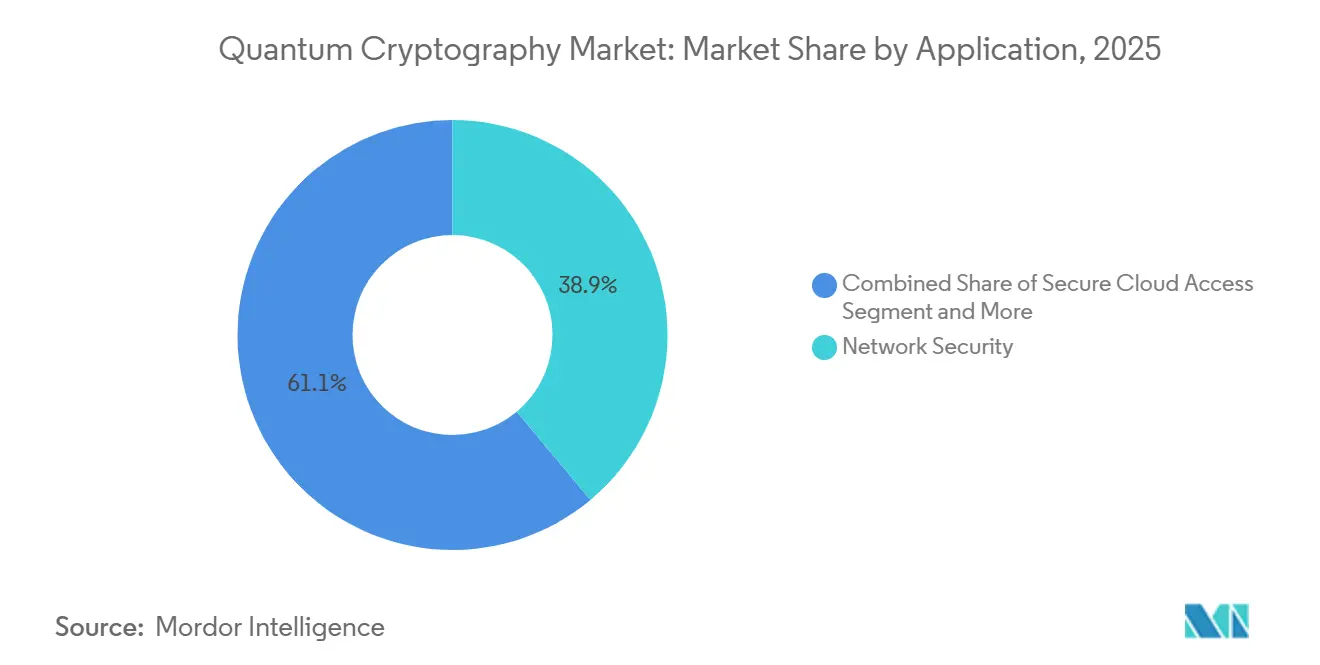

- By application, network security led with a 38.91% share in 2025, while secure cloud access is expected to grow at a 26.71% CAGR over 2026-2031.

- By end-user, IT and telecommunications commanded 31.78% of 2025 spend, but healthcare and life sciences is set to advance at a 26.83% CAGR to 2031.

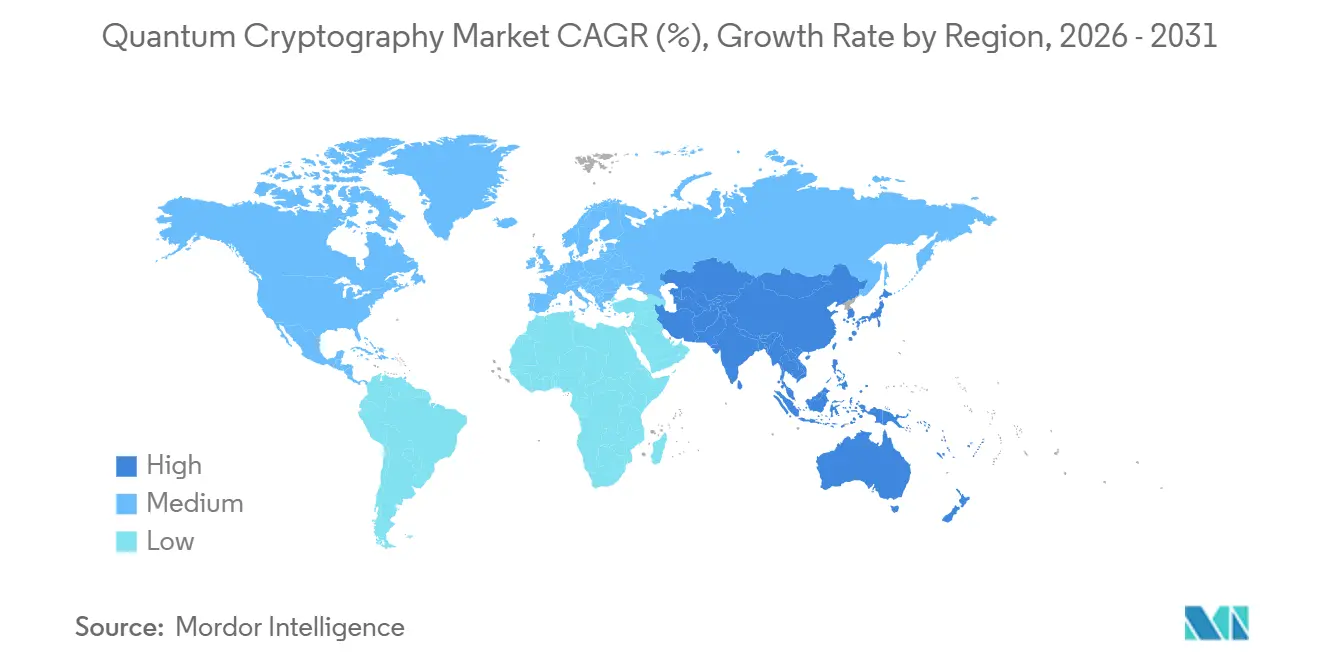

- By geography, North America accounted for 36.67% of 2025 revenue, yet Asia-Pacific is forecast to expand at 27.01% over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Quantum Cryptography Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Number of Quantum-Enabled Cyber-Attacks | +5.20% | Global, with acute exposure in North America and Europe | Short term (≤ 2 years) |

| Government Funding for Quantum Communication Infrastructure | +4.80% | APAC core (China, Japan, South Korea), spill-over to EU and North America | Medium term (2-4 years) |

| Need for Quantum-Safe Security in 5G and IoT Ecosystems | +4.10% | Global, concentrated in urban metro areas deploying 5G standalone networks | Medium term (2-4 years) |

| Standardization Progress at ETSI and ITU Enabling Interoperable QKD | +3.70% | Europe and North America, with gradual adoption in APAC | Long term (≥ 4 years) |

| Emergence of Quantum Network Testbeds Accelerating Commercial Pilots | +3.30% | North America, EU, China, Japan | Short term (≤ 2 years) |

| Convergence of QKD with Software-Defined Networking for Automated Key Orchestration | +2.90% | Global, led by cloud-native enterprises in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Number of Quantum-Enabled Cyber-Attacks

Incidents in which adversaries captured encrypted traffic for future decryption rose sharply during 2025, moving the discussion from theoretical to operational risk. Financial institutions, defense primes, and cloud providers reacted by accelerating roadmaps for both QKD and post-quantum cryptography.[1]U.S. Cybersecurity and Infrastructure Security Agency, “Quantum Threat Assessment 2025,” cisa.gov Boards are now briefed quarterly on “harvest-now-decrypt-later” exposures, pushing budgets for quantum-safe upgrades ahead of broader IT refresh cycles.[2]National Institute of Standards and Technology, “Post-Quantum Cryptography Standardization,” nist.gov Insurance carriers excluding quantum-related breaches from new cyber policies are amplifying the urgency. As a result, the quantum cryptography market is transitioning from proof-of-concept trials to enterprise-wide rollouts.

Government Funding for Quantum Communication Infrastructure

Public-sector capital reached USD 4.2 billion in 2025, underwriting nationwide backbones that de-risk private adoption. China’s 10 000-kilometer fiber network, the EU’s flagship cross-border links, U.S. defense satellite projects, and Japan’s metro deployments all created anchor tenants for domestic vendors.[3]Ministry of Science and Technology, China, “National Quantum Communication Infrastructure,” most.gov.cn These early networks validated performance over long haul and urban metro distances, demonstrating commercial service-level agreements. Subsidies also accelerated standards work because agencies demanded interoperable gear, indirectly lowering vendor lock-in fears for enterprises evaluating multi-supplier strategies.

Need for Quantum-Safe Security in 5G and IoT Ecosystems

Edge devices using 5G standalone architectures transmit telemetry and control signals that remain valuable well beyond a typical device lifecycle. Classical key-rotation intervals cannot mitigate future quantum decryption, so operators have begun embedding quantum random number generators in base stations and gateways. Industrial IoT endpoints with limited compute headroom increasingly rely on externally distributed quantum keys, avoiding expensive hardware swaps. The result is a structural pull for low-power QKD appliances and managed key orchestration services, expanding the addressable quantum cryptography market beyond core data-center links.

Standardization Progress at ETSI and ITU Enabling Interoperable QKD

Release of open APIs and authenticated channel protocols in 2024-2025 allowed multi-vendor integration inside existing network-management stacks. Large banks and telecom operators, previously wary of proprietary ecosystems, now issue tenders that mandate ETSI GS QKD-018 compliance. Certification blueprints like ISO/IEC 23837 are emerging in procurement checklists, providing smaller hardware manufacturers a clear path to qualification. Interoperability lowers switching costs, promotes price competition, and shortens deployment lead times, making the quantum cryptography market more approachable for midsize enterprises.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Deployment and Maintenance Costs of QKD Hardware | -3.40% | Global, most acute in cost-sensitive markets in South America and Africa | Short term (≤ 2 years) |

| Shortage of Skilled Quantum-Security Professionals | -2.80% | Global, with severe gaps in emerging markets | Medium term (2-4 years) |

| Photonic Component Supply-Chain Bottlenecks | -2.10% | Global, concentrated in regions dependent on East Asian semiconductor fabs | Short term (≤ 2 years) |

| Inconsistent Quantum Channel Certification Frameworks Across Jurisdictions | -1.60% | Cross-border deployments in multinational enterprises | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Deployment and Maintenance Costs of QKD Hardware

Per-node spending frequently exceeds USD 500 000 because single-photon detectors, precision lasers, and synchronization electronics remain niche components with limited manufacturing scale. Maintenance contracts add material operational expenditure because uptime requires tight environmental control. Currency volatility further inflates import prices in emerging markets, widening the affordability gap. Vendors are responding with compact 19-inch rack units that consume under 100 watts, but cost curves still trail conventional networking equipment by an order of magnitude, slowing the quantum cryptography market adoption in price-sensitive regions.

Shortage of Skilled Quantum-Security Professionals

Fewer than 5 000 certified practitioners worldwide maintain enterprise QKD networks, design post-quantum key hierarchies, or integrate quantum-safe stacks into security-information and event-management platforms. Hiring cycles stretch close to a year, and salary premiums exceed 60% over traditional cybersecurity roles. Regions without established quantum-engineering graduate programs import expatriate talent or outsource to vendors, adding both cost and operational risk. Managed-service models partially offset scarcity but introduce key-escrow concerns that regulators are only beginning to address.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain Ground as Complexity Rises

The quantum cryptography market size for components shows hardware leading with 46.19% of 2025 revenue, reflecting early network buildouts that required dedicated transmitters, receivers, and photonic switches. A growing share of enterprises, however, prefer opex-based engagements that bundle equipment, integration, and 24/7 monitoring. Services consequently are projected to grow at 26.67% through 2031, the fastest among components, supported by subscription models that mirror broader IT outsourcing trends.

Momentum toward services is also propelled by a lack of internal quantum talent and by regulators urging third-party audits of key management operations. Compact rackmount QKD nodes consuming under 100 watts simplify colocation, yet day-to-day tuning of single-photon detectors remains specialized. Software continues to mature as vendors expose APIs that link QKD sources to classical public-key-infrastructure platforms, but without managed orchestration, many enterprises still struggle to operationalize policies. As field experience accumulates, service catalogues now include quantum-risk assessments, automated key-lifecycle management, and compliance reporting, rounding out the quantum cryptography market offering.

By Technology: Platforms Outpace Stand-Alone QKD

Quantum key distribution commanded 54.16% of 2025 technology spend because it remains the only field-proven method for information-theoretic key exchange. Yet integrated quantum secure communications platforms should post the highest growth, 26.91% CAGR to 2031, as customers demand unified dashboards that merge QKD channels, post-quantum cryptography, and quantum random number generators. This platform approach reduces operational silos and matches how security teams already manage firewalls and VPN concentrators.

The quantum cryptography market share for post-quantum cryptography software is expanding following NIST algorithm standardization, especially where fiber distance or budget constraints preclude QKD. QRNG silicon is now embedded inside hardware security modules, closing entropy gaps exploited via side-channels. Finally, satellite QKD has moved from demonstrations to limited commercial pilots, offering global coverage for regions lacking fiber backbones. Together, these modalities reposition quantum security as an integrated feature rather than an exotic bolt-on.

By Deployment Mode: Hybrid Architectures Emerge as Default

On-premises installations represented 57.58% of revenue in 2025 because banks, defense agencies, and critical-infrastructure operators control latency-sensitive applications. However, hybrid models are the fastest-growing segment at 26.48% CAGR, balancing data-sovereignty demands with the elasticity of public clouds. Cloud providers now expose QRNG and post-quantum VPN gateways, allowing enterprises to extend quantum-safe channels into virtual private clouds without re-architecting applications.

A European financial institution illustrates the shift: its core banking systems remain on-premises with dedicated QKD links, but analytics workloads leverage cloud instances protected by lattice-based encryption and cloud-edge QKD nodes. This split deployment aligns security controls with workload sensitivity while preserving agility. As more industries adopt multi-cloud strategies, orchestrators that allocate quantum keys dynamically across on-premises, edge, and cloud domains will define the next phase of the quantum cryptography market evolution.

By Application: Secure Cloud Access Becomes Top Growth Engine

Network security dominated 38.91% of 2025 spend because perimeter defenses were first in line for quantum-safe hardening. Yet secure cloud access is projected to expand at a 26.71% CAGR as zero-trust architectures demand continuous authentication and encryption of every flow, independent of location. The quantum cryptography market size for secure cloud access will therefore accelerate as multinationals synchronize data across SaaS, platform-as-a-service, and on-premises assets.

Application security teams are embedding NIST-approved post-quantum algorithms in microservices meshes, while database administrators integrate QRNG-generated keys into encryption-at-rest policies. Healthcare providers already use quantum-safe cloud gateways to protect telemedicine sessions and genomic analytics pipelines. As a result, the quantum cryptography market share for cloud-oriented workloads is rising from a small 2025 base toward mainstream adoption by the decade’s end.

By End-User: Healthcare Moves from Pilot to Rapid Scale

IT and telecommunications generated 31.78% of revenue in 2025 because carriers both consume and resell quantum-secure connectivity. The next growth engine is healthcare and life sciences, forecast to grow at 26.83% CAGR through 2031, as hospitals protect immutable genomic data and telemedicine sessions. Regulatory bodies treat patient privacy breaches as existential threats, prompting rapid budgeting for quantum-safe upgrades.

Banks continue to extend QKD to interbank settlement paths, but many have already completed early metro links, shifting incremental spend toward managed services. Defense agencies remain strategic anchor customers, especially for satellite QKD. Energy utilities are now piloting lightweight QKD appliances for SCADA links, underscoring how operational-technology environments broaden the quantum cryptography market addressable pool.

Geography Analysis

North America led the quantum cryptography market with 36.67% of 2025 revenue owing to early financial-services and defense rollouts. Activity spans both metropolitan fiber corridors and experimental satellite links, anchored by federal funding and strong venture ecosystems. Europe follows closely, leveraging the EU Quantum Flagship to harmonize cross-border certification and subsidize regional vendor clusters. Performance benchmarks from Paris-Berlin-Vienna links have already fed back into procurement standards across the bloc.

Asia-Pacific is the fastest-growing region, projected at 27.01% CAGR, propelled by China’s national backbone, Japan’s Tokyo-Osaka metro buildouts, and South Korea’s QRNG-enabled 5G base-station networks. These projects create domestic supply chains, lowering component costs and accelerating local standardization bodies’ influence.

Middle East and Africa markets are nascent but strategically important as Gulf smart-city initiatives allocate sovereign wealth to secure financial hubs and critical infrastructure. Latin America is progressing unevenly; Brazil’s pilot government network has slipped schedules because of photonic-detector shortages, illustrating how supply-chain fragility still shapes regional rollouts.

Competitive Landscape

The quantum cryptography market exhibits moderate fragmentation, with the top three vendors controlling less than 40% of global revenue. ID Quantique, Toshiba, and QuantumCTek secure anchor projects through proven QKD performance, while challengers such as KETS Quantum Security and QuNu Labs differentiate with chip-scale QRNG modules and edge-friendly form factors. Incumbents are vertically integrating component suppliers to hedge detector shortfalls and lock in cost advantages, a trend likely to lift barriers to entry for pure-play software start-ups.

Patent filings exceeded 320 in 2025, covering photonic-integrated circuits and key-management protocols. Cloud hyperscalers have begun embedding quantum-safe services into broader platforms, commoditizing basic capabilities and forcing hardware specialists to develop value-added orchestration software.

Mergers and acquisitions therefore skew toward hardware-software convergence, as vendors seek to offer end-to-end stacks that satisfy enterprise desires for single-pane-of-glass management.

Quantum Cryptography Industry Leaders

QuintessenceLabs Pty Ltd

Crypta Labs Limited

ID Quantique SA

MagiQ Technologies, Inc.

Nucrypt Llc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: IBM, Tata Consultancy Services, and the Government of Andhra Pradesh unveiled plans to deploy India’s largest quantum computer featuring a 156-qubit Heron processor.

- April 2025: QuintessenceLabs secured USD 15 million from Australia’s National Reconstruction Fund Corporation to accelerate global expansion.

- March 2025: ETSI released TS 104 015 for efficient quantum-safe hybrid key exchanges.

- March 2025: Vodafone and IBM partnered to embed post-quantum security in mobile networks.

Global Quantum Cryptography Market Report Scope

The Quantum Cryptography Market Report is Segmented by Component (Hardware, Software, Services), Technology (Quantum Key Distribution, Post-Quantum Cryptography, Quantum Random Number Generation, Quantum Secure Communications Platforms), Deployment Mode (On-Premises, Cloud, Hybrid), Application (Network Security, Application Security, Database/Storage Security, Secure Cloud Access, Other Applications), End-User (IT and Telecommunications, BFSI, Government and Defense, Healthcare and Life Sciences, Energy and Utilities, Other End-Users), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Software |

| Services |

| Quantum Key Distribution (QKD) |

| Post-Quantum Cryptography (PQC) |

| Quantum Random Number Generation (QRNG) |

| Quantum Secure Communications Platforms |

| On-Premises |

| Cloud |

| Hybrid |

| Network Security |

| Application Security |

| Database/Storage Security |

| Secure Cloud Access |

| Other Applications |

| IT and Telecommunications |

| BFSI |

| Government and Defense |

| Healthcare and Life Sciences |

| Energy and Utilities |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Middle East | GCC |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Technology | Quantum Key Distribution (QKD) | |

| Post-Quantum Cryptography (PQC) | ||

| Quantum Random Number Generation (QRNG) | ||

| Quantum Secure Communications Platforms | ||

| By Deployment Mode | On-Premises | |

| Cloud | ||

| Hybrid | ||

| By Application | Network Security | |

| Application Security | ||

| Database/Storage Security | ||

| Secure Cloud Access | ||

| Other Applications | ||

| By End-User | IT and Telecommunications | |

| BFSI | ||

| Government and Defense | ||

| Healthcare and Life Sciences | ||

| Energy and Utilities | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East | GCC | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What CAGR will quantum cryptography record between 2026 and 2031?

The quantum cryptography market is projected to grow at 25.96% during 2026-2031.

Which region is forecast to grow fastest through 2031?

Asia-Pacific is expected to expand at 27.01% as China, Japan, and South Korea scale national backbones.

Which component segment will rise most quickly?

Services are set to expand at 26.67% CAGR because enterprises are outsourcing complex quantum-security operations.

Which application shows the highest growth potential?

Secure cloud access leads with a 26.71% CAGR due to zero-trust mandates across multicloud environments.

Why is healthcare accelerating adoption?

Genomic databases and telemedicine services require quantum-safe encryption to comply with strict privacy regulations, driving a 26.83% CAGR in healthcare spend.

How concentrated is vendor competition?

The top five players hold a little above 60% of global revenue, giving the market a concentration score of 6.

Page last updated on: