Confidential Computing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

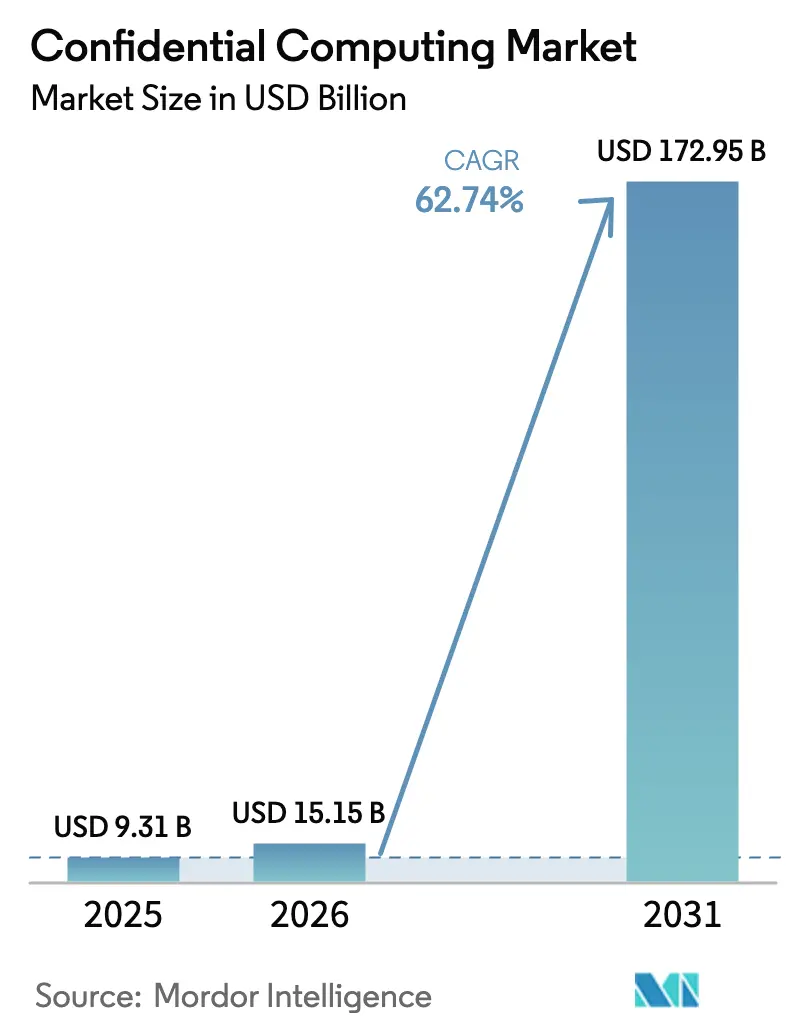

| Market Size (2026) | USD 15.15 Billion |

| Market Size (2031) | USD 172.95 Billion |

| Growth Rate (2026 - 2031) | 62.74% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Confidential Computing Market Analysis by Mordor Intelligence

The confidential computing market size is expected to grow from USD 9.31 billion in 2025 to USD 15.15 billion in 2026 and is forecast to reach USD 172.95 billion by 2031 at 62.74% CAGR over 2026-2031. Demand is fueled by the sharp rise in cyber-attack sophistication, the spread of sovereign-cloud mandates, and the steady fall in performance overhead for running encrypted workloads in production settings. Enterprises that already encrypt data at rest and in transit are now extending protection to data-in-use through hardware-rooted Trusted Execution Environments (TEEs), homomorphic encryption accelerators, and secure multiparty computation. Hyperscale cloud providers are productizing these capabilities across mainstream instance families, making confidential computing a default option rather than a specialist add-on. With regulators tightening breach-notification windows and imposing steeper penalties, confidential computing market adoption is moving from early pilots to large-scale deployments in banking, healthcare, and public-sector workloads.

Key Report Takeaways

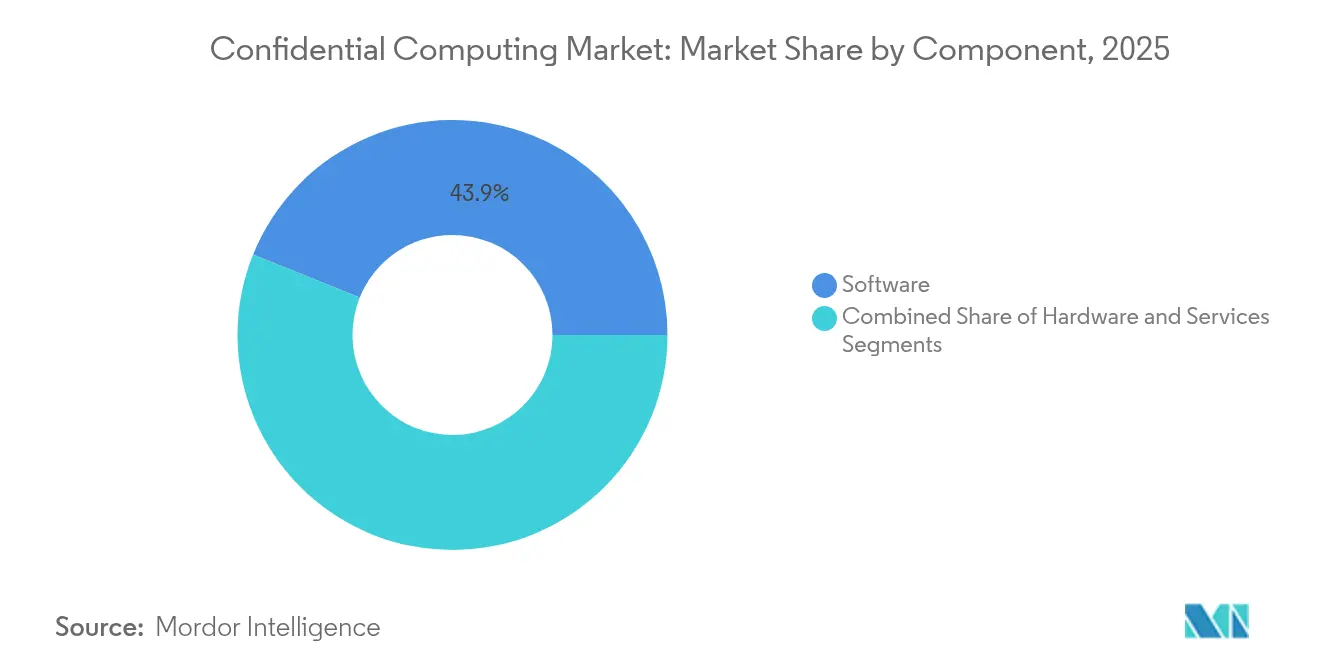

- By component, software captured 43.90% of confidential computing market share in 2025, while hardware is forecast to expand at a 64.90% CAGR to 2031.

- By deployment mode, on-premise held 54.30% of the confidential computing market share in 2025; cloud deployments record the fastest trajectory at 66.50% CAGR through 2031.

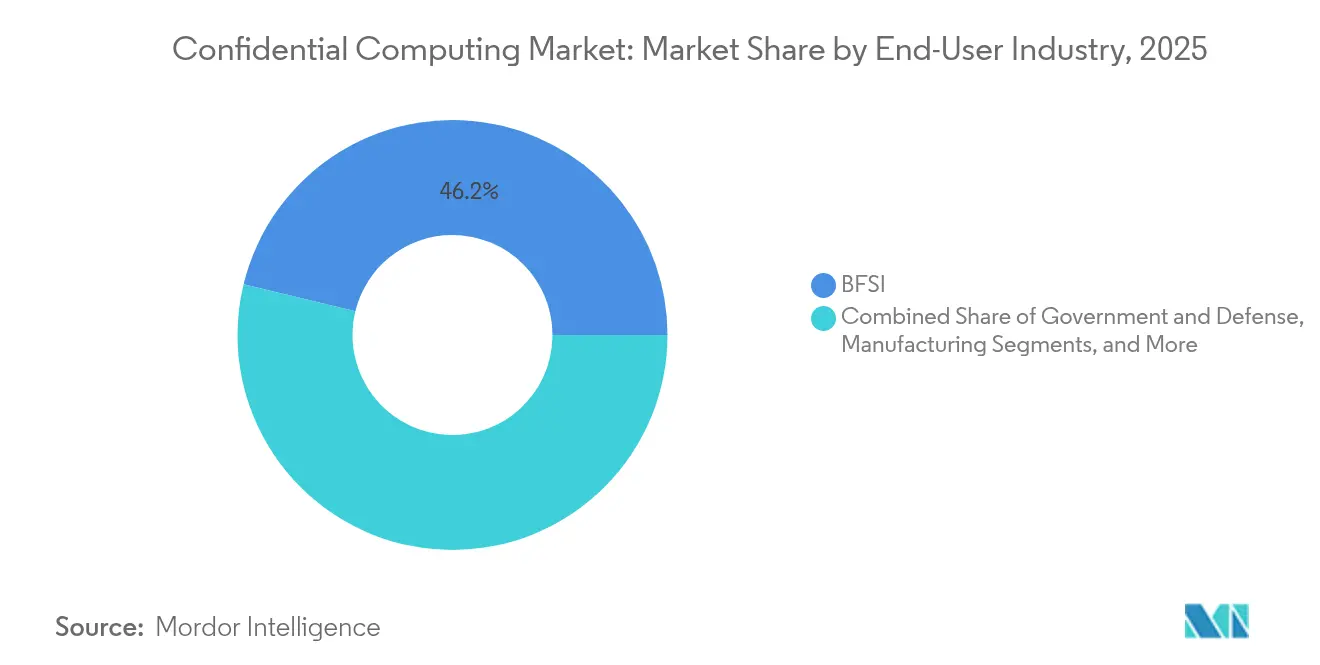

- By end-user industry, BFSI led with 46.20% revenue share in 2025, whereas retail and e-commerce is projected to grow at a 64.60% CAGR to 2031.

- By security mechanism, TEEs accounted for a 50.10% share of the confidential computing market size in 2025, and homomorphic encryption accelerators are advancing at a 66.90% CAGR.

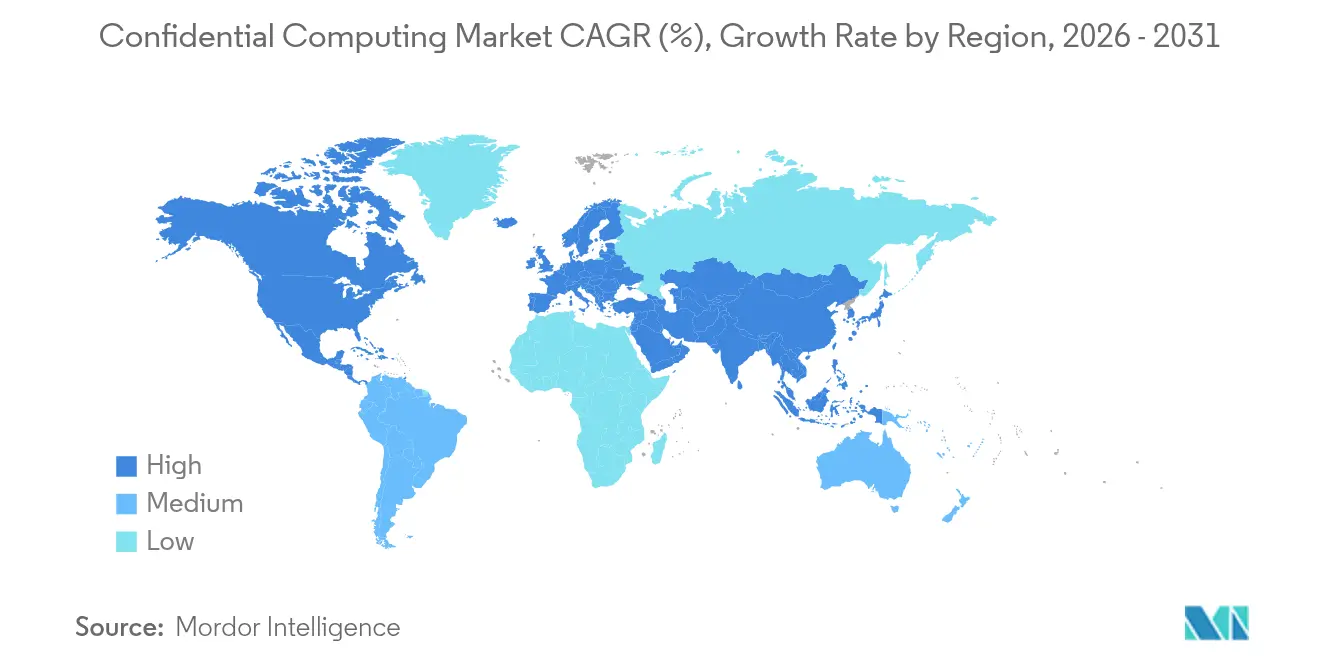

- By geography, North America dominated with 41.70% revenue share in 2025, while Asia-Pacific is expanding at a 66.10% CAGR during the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Confidential Computing Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in data-breach frequency and cost | +12.5% | Global, with heightened impact in North America and EU | Short term (≤ 2 years) |

| Multi-cloud adoption demanding in-use encryption | 11.2% | Global, particularly North America and Asia-Pacific | Medium term (2-4 years) |

| GPU-grade TEEs unlocking "Confidential AI" use-cases | 15.8% | North America and Asia-Pacific core, spill-over to EU | Medium term (2-4 years) |

| Federated analytics in regulated sectors | 8.7% | Global, with early gains in North America and EU | Long term (≥ 4 years) |

| Sovereign-cloud initiatives mandate CC | 10.3% | EU and Asia-Pacific core, emerging in MEA | Medium term (2-4 years) |

| Decentralised AI and blockchain need trusted off-chain compute | 6.9% | Global, with concentration in North America and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Data-Breach Frequency and Cost

The Oracle Cloud Infrastructure breach that exposed more than 6 million records proved perimeter defenses can be bypassed even in well-managed clouds. Confidential computing gives organizations a final shield by encrypting data while it is processed, ensuring adversaries gain nothing usable even when they obtain root access. AI-driven attack automation amplifies the threat, pushing financial institutions and healthcare providers to adopt hardware-rooted TEEs that resist both present-day and post-quantum exploits. Regulators now fine firms more for compliance failures than for remediation expenses, so encrypted-in-use protection is becoming compulsory in heavily regulated verticals.

Multi-Cloud Adoption Demanding In-Use Encryption

Enterprises spreading workloads across several clouds struggle to maintain consistent data-sovereignty controls. Azure Confidential Compute nodes equipped with NVIDIA H100 GPUs let organizations move sensitive AI jobs among regions without decrypting data. Google Cloud widened its confidential offering to C3D, C3, and N2D families, turning in-use encryption into a table-stakes feature rather than a boutique SKU [1]Google Cloud, “Expanding Confidential VMs to C3, C3D, and N2D,” cloud.google.com. When paired with Confidential GKE Nodes, firms can lift-and-shift Kubernetes clusters while preserving enclave-level guarantees.

GPU-Grade TEEs Unlocking “Confidential AI” Use-Cases

NVIDIA’s general release of confidential computing on H100 Tensor Core GPUs enables LLM training on private datasets with under 7% overhead, erasing the traditional performance trade-off. Apple’s Private Cloud Compute uses Secure Enclaves for device-to-cloud AI privacy, illustrating consumer-scale potential. Secure GPU enclaves now underpin confidential federated learning, where hospitals merge radiology images across borders without exposing patient identifiers, accelerating disease-classification accuracy while maintaining compliance.

Federated Analytics in Regulated Sectors

Swift and Google Cloud run federated fraud-detection models that keep every bank’s transaction stream encrypted, improving anomaly-detection speed by 29% while honoring data-sharing restrictions. Healthcare consortiums employ TEEs for multi-center genomic pipelines, pooling small rare-disease cohorts to reach statistical power without moving raw patient files. Early policy drafts in the EU and Japan reference federated analytics as a best-practice for sensitive cross-border research.

Restraints Impact Analysis of Confidential Computing Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Up-front hardware and integration cost | -8.4% | Global, particularly impacting SMEs in emerging markets | Short term (≤ 2 years) |

| Performance overhead / limited workload fit | -6.2% | Global, with higher impact in latency-sensitive applications | Medium term (2-4 years) |

| Absent cross-vendor attestation standards | -4.1% | Global, with particular challenges in multi-cloud environments | Long term (≥ 4 years) |

| Supply-chain trust gaps and side-channel disclosures | -3.7% | Global, with heightened concerns in government and defense sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Up-front Hardware and Integration Cost

Quantum-safe servers priced near USD 12.5 million remain out of reach for most SMEs, driving a pause in on-premise refresh plans. Intel’s data-center division saw a 3% revenue dip in Q4 2024 as buyers deferred confidential computing upgrades during economic turbulence [2]Intel Corporation, “2024 Q4 Earnings Release,” intel.com. Cloud “confidential-as-a-service” offerings reduce CapEx barriers by charging per-second usage, allowing pilot projects without owning the silicon.

Performance Overhead / Limited Workload Fit

High-frequency trading desks and real-time industrial controllers cannot tolerate even single-digit latency spikes introduced by encryption during PCIe transfers. Firms increasingly deploy hybrid stacks that route only highly sensitive functions through enclaves while keeping milliseconds-critical code on standard nodes. Start-ups such as RISC Zero report 4× speed gains for zero-knowledge VMs, hinting that today’s constraints may ease before 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Confidential Computing Market Segment Analysis

By Component:

Software Dominance Drives IntegrationSoftware accounted for 43.90% of confidential computing market share in 2025, reflecting its ease of overlaying enclave capabilities atop existing hypervisors and container orchestrators. This layer lets enterprises deploy incremental protections without forklift upgrades. However, hardware revenue is scaling fastest at a 64.90% CAGR as Intel, AMD, and NVIDIA embed TEEs directly into CPUs and GPUs, collapsing encryption overheads and closing side-channel gaps.

Hardware vendors now bundle firmware-level attestation and encrypted PCIe links, shifting the spend mix toward silicon by 2030. Services capture the remaining slice, covering integration, managed attestation, and audit extensions. As the confidential computing market size for hardware widens, chipmakers are packaging dedicated MACsec lanes and on-die key managers to harden accelerators against cold-boot attacks.

By Deployment Mode:

On-Premise Leadership Faces Cloud AccelerationOn-premise installations held 54.30% of confidential computing market share in 2025 because defense, intelligence, and critical-infrastructure operators insist on local custody of cryptographic keys. Yet cloud is climbing at a 66.50% CAGR as hyperscalers guarantee regional data residency, offer pay-as-you-go enclaves, and integrate ledger-backed attestation logs.

Broadcom’s 2025 survey shows 69% of CIOs plan to repatriate some workloads, driving hybrid blueprints that tether enclave keys across private and public clouds. The confidential computing market size for cloud services is expected to surpass on-premise outlays by 2028 as providers roll out auto-scaling encrypted clusters controlled through policy engines rather than BIOS settings.

By End-User Industry:

BFSI Dominance Meets Retail AccelerationBFSI contributed 46.20% revenue in 2025 after early adopters used enclaves for algorithmic trading and secure regulatory reporting. Stringent compliance frameworks, such as PCI DSS 4.0 and Basel III, make data-in-use encryption a board-level mandate among global banks.

Retail and e-commerce’s 64.60% CAGR stems from privacy-preserving analytics that let merchants segment shoppers without exposing raw purchase histories. Unattended point-of-sale devices now ship with integrated secure enclaves, shielding tokenized card data from edge attackers. The confidential computing industry also sees rising adoption in healthcare where TEEs enable AI-assisted diagnostics on encrypted images.

By Security Mechanism:

TEE Leadership Faces Homomorphic DisruptionTEEs maintained 50.10% share in 2025 thanks to mature Intel SGX, AMD SEV, and ARM TrustZone implementations that require minimal code change. They remain favored for low-latency operations such as key-management services.

Homomorphic encryption accelerators, however, are posting a 66.90% CAGR as photonic co-processors process ciphertext at near plaintext speeds. The confidential computing market size devoted to homomorphic silicon is forecast to eclipse USD 21.35 billion by 2031, pushed by privacy legislation that prizes algebraic proof over isolation. Secure multiparty computation lags in revenue but is essential for consortium-style risk-scoring across distrustful counterparties in capital markets and life-sciences collaborations.

Geography Analysis

North America Confidential Computing Market

North America captured 41.70% of confidential computing market share in 2025, propelled by the U.S. Department of Defense awarding IBM USD 576 million for secure chip foundry expansion and NIST’s Provenance Chain Network to harden microelectronics supply chains . Federal buying power signals long-term demand, while private-sector moves such as HP’s quantum-resistant PCs prime the broader ecosystem for post-quantum readiness. Major cloud platforms headquartered in the region keep releasing enclave enhancements that quickly ripple through global deployments.

APAC Confidential Computing Market

Asia-Pacific is progressing at a 66.10% CAGR through 2031, lifted by state-backed quantum initiatives in China, Japan’s METI cybersecurity rules for semiconductor fabs, and Taiwan’s post-quantum cryptography migration guide. India’s financial-sector digitization and Australia’s critical-infrastructure act also encourage enclave adoption for cross-border data flows. Governments fund pilot projects that pair TEEs with blockchain-style ledgers to certify export-controlled design files.

Europe Confidential Computing Market

Europe combines GDPR enforcement with sovereign-cloud mandates that require in-region compute and attestation services. Microsoft completed its EU sovereign cloud in February 2025, while Google partners with T-Systems and S3NS for French data-residency controls. The proposed Cloud and AI Development Act aims to triple secure data-center capacity within seven years. Financial institutions such as HSBC already operate quantum-secured metro networks, reinforcing confidential computing as a compliance accelerator rather than a cost overhead.

Competitive Landscape

Market concentration is moderate: Intel, AMD, and NVIDIA supply most enclave-capable processors, while Microsoft Azure, Google Cloud, and Amazon Web Services dominate managed confidential services. Intel’s 2025 10-K highlights confidential computing as a strategic differentiator in x86 roadmaps Intel. AMD counters with SEV-SNP on EPYC, promising lower performance overhead, and NVIDIA extends attestation across PCIe fabrics to include GPUs.

Cloud providers differentiate through depth of integration. Microsoft bundles policy-based key governance, Google offers Confidential Space for collaborative AI, and AWS Nitro Enclaves targets payment tokenization workloads. All three contribute to the Confidential Computing Consortium, balancing cooperation on standards with competitive feature velocity.

Specialist entrants target white-space niches. Zama raised USD 57 million to commercialize fully homomorphic encryption at blockchain scale, while Arcium’s acquisition of Inpher brings multi-party computation IP into decentralized protocols. Optalysys races to deliver photonic homomorphic accelerators, and RISC Zero optimizes zero-knowledge systems for roll-ups. These challengers exploit gaps in cross-vendor attestation and workload-specific optimizations that incumbents cannot address rapidly.

Confidential Computing Industry Leaders

Microsoft Corporation

IBM Corporation

Intel Corporation

Amazon Web Services, Inc.

Google LLC (Alphabet Inc.)

- *Disclaimer: Major Players sorted in no particular order

Confidential Computing Market Companies Covered in this Report

- Microsoft Corporation

- IBM Corporation

- Intel Corporation

- Google LLC (Alphabet Inc.)

- Advanced Micro Devices, Inc.

- Amazon Web Services, Inc.

- Alibaba Cloud (Alibaba Group Holding Ltd.)

- Fortanix Inc.

- Swisscom AG

- American Megatrends International LLC (AMI)

- Arm Holdings plc

- NVIDIA Corporation

- Oracle Corporation

- Red Hat, Inc.

- VMware LLC (Broadcom Inc.)

- Thales Group

- Edgeless Systems GmbH

- Anjuna Security, Inc.

- Cosmian SA

- R3 LLC

Recent Industry Developments in Confidential Computing Market

- June 2025: Zama secured USD 57 million in Series B funding, unveiling its confidential blockchain protocol and public testnet for building encrypted decentralized applications on Ethereum.

- March 2025: HP launched printers and PCs with quantum-resistant ASICs, aligning with U.S. federal mandates for post-quantum secure devices by 2027.

- February 2025: Intel enabled TDX Connect on Xeon 6 processors, extending encrypted communication between confidential virtual machines and PCIe devices.

- November 2024: Arcium acquired Inpher’s technology and talent to boost decentralized confidential computing via advanced multi-party computation.

Global Confidential Computing Market Report Scope

Confidential computing is a cloud computing technology that safeguards data by isolating it within a protected central processing unit (CPU) during processing. This means that both the data being processed and the methods employed to process it are secured within the CPU's environment.

The study tracks the revenue accrued through the sale of the confidential computing market by various players across the globe. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The confidential computing market is segmented by component (hardware, software, and services), deployment mode (on-premises and cloud), vertical (BFSI, government & defense, healthcare & life sciences, IT & telecommunications, manufacturing, retail & consumer goods, and other verticals), and geography (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

Segmentation Overview

| Hardware |

| Software |

| Services |

| Cloud |

| On-premise |

| BFSI |

| Government and Defense |

| Healthcare and Life Sciences |

| IT and Telecommunications |

| Manufacturing |

| Retail and E-Commerce |

| Other Verticals |

| Trusted Execution Environments (TEE) |

| Confidential Virtual Machines |

| Homomorphic Encryption Accelerators |

| Secure Multiparty Computation Platforms |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Deployment Mode | Cloud | ||

| On-premise | |||

| By End-user Industry | BFSI | ||

| Government and Defense | |||

| Healthcare and Life Sciences | |||

| IT and Telecommunications | |||

| Manufacturing | |||

| Retail and E-Commerce | |||

| Other Verticals | |||

| By Security Mechanism | Trusted Execution Environments (TEE) | ||

| Confidential Virtual Machines | |||

| Homomorphic Encryption Accelerators | |||

| Secure Multiparty Computation Platforms | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is driving the rapid growth of the confidential computing market?

The surge stems from stricter data-protection regulations, the spread of sovereign-cloud mandates, and hardware advances that cut performance overhead to below 7% for AI workloads, propelling a 62.74% CAGR through 2031.

Which segment currently generates the most revenue?

Software led with 43.90% revenue share in 2025 because virtualization-layer tools overlay easily on existing infrastructure.

Why is Asia-Pacific the fastest-growing region?

Massive public funding for quantum-safe technologies and aggressive digital-transformation programs push Asia-Pacific to a 66.10% CAGR.

How do homomorphic encryption accelerators differ from TEEs?

TEEs isolate runtime memory on standard CPUs or GPUs, while homomorphic accelerators compute directly on ciphertext, enabling collaboration without decrypting data.

Page last updated on: