Quantum Computing In Automotive Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

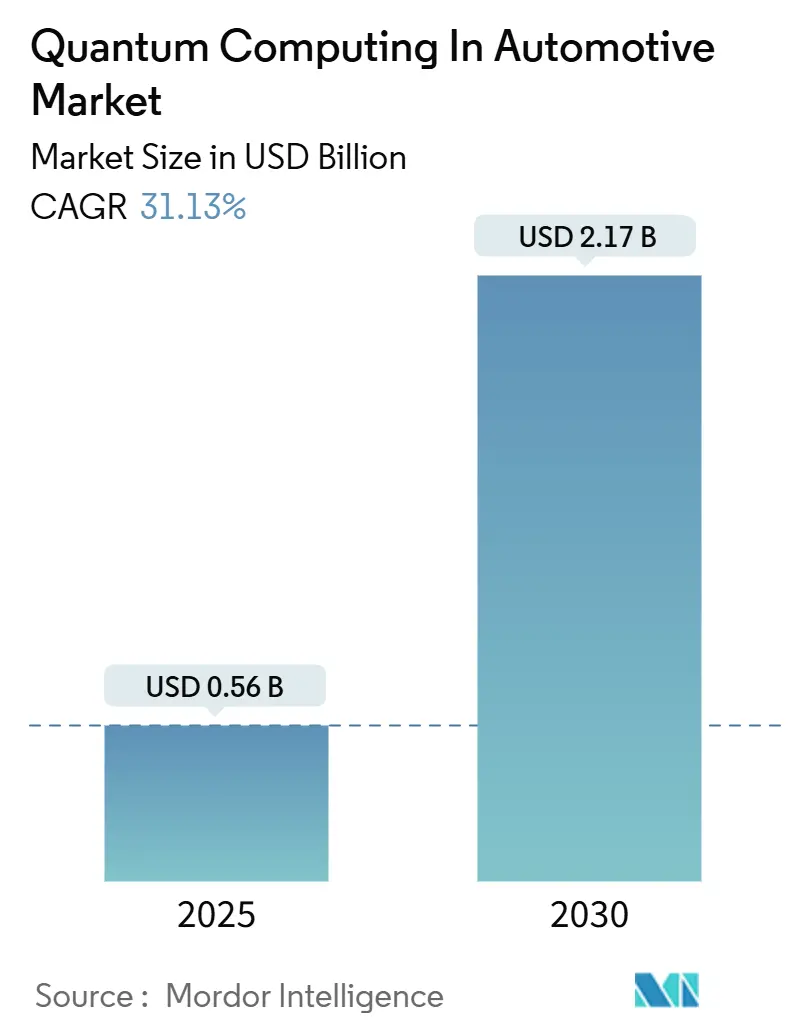

| Market Size (2025) | USD 0.56 Billion |

| Market Size (2030) | USD 2.17 Billion |

| Growth Rate (2025 - 2030) | 31.13% CAGR |

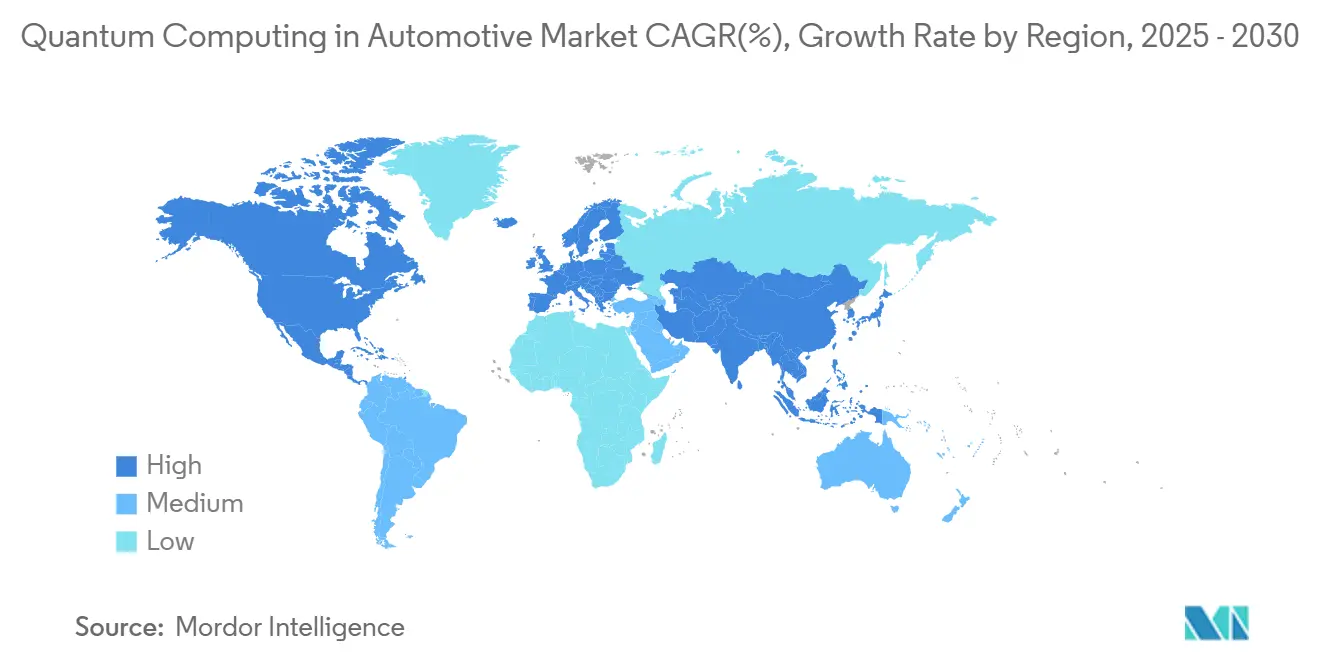

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Quantum Computing In Automotive Market Analysis by Mordor Intelligence

The quantum computing in the automotive market size reached USD 0.56 billion in 2025 and is projected to climb to USD 2.17 billion by 2030, expanding at a 31.13% CAGR. The upward trajectory is powered by the industry’s shift toward quantum-enhanced optimization, battery-chemistry simulation, and next-generation autonomous-driving workloads that classical infrastructure cannot handle efficiently. Commercial deployments have moved past proof-of-concept: Volkswagen, BMW, and Hyundai now run quantum algorithms within live production and R&D workflows, recording measurable throughput gains in paint-shop sequencing, metal-forming simulations, and perception model training. Cloud-based Quantum Computing-as-a-Service (QCaaS) lowers capital barriers and lets Tier-1 suppliers test multiple hardware modalities on demand. At the same time, hybrid quantum-classical algorithms deliver immediate ROI even on noisy intermediate-scale quantum (NISQ) machines. Regional growth patterns diverge: North America leverages mature quantum infrastructure and a deep startup pipeline, whereas Asia-Pacific accelerates on the back of government-funded national quantum programs and massive automotive production bases.

Key Report Takeaways

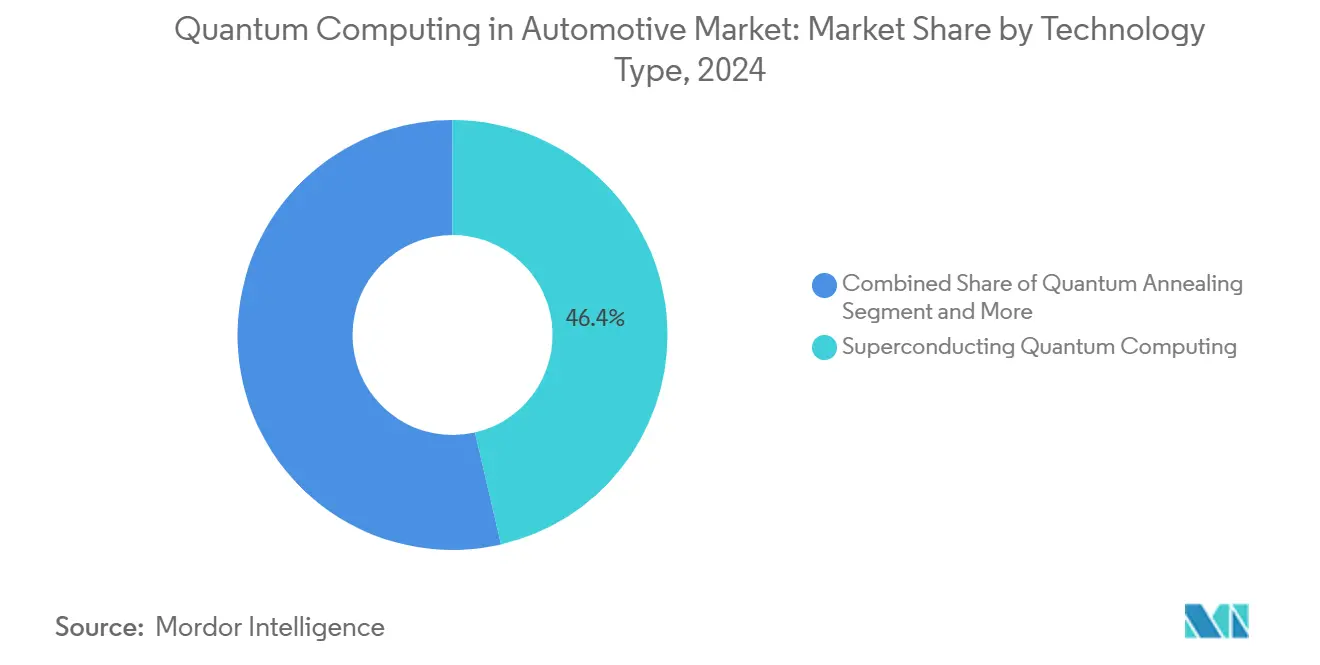

- By technology type, superconducting systems captured 46.37% of the quantum computing market share in 2024, while photonic platforms are forecast to post a 34.28% CAGR through 2030.

- By application, supply-chain and logistics optimization held 26.22% of the quantum computing market in the automotive industry in 2024; autonomous-driving algorithms are advancing at a 33.62% CAGR to 2030.

- By component, quantum processors commanded 41.28% of the quantum computing market share in 2024, whereas quantum software platforms are projected to expand at a 34.48% CAGR over 2025-2030.

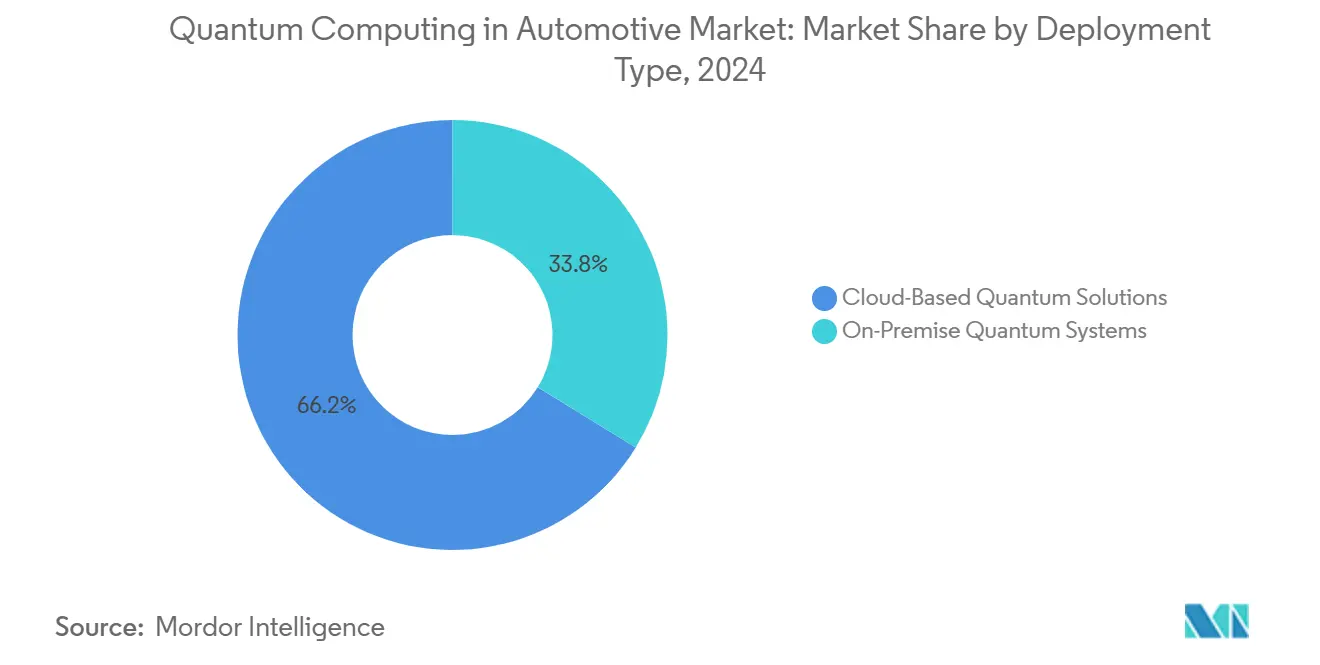

- By deployment, cloud-hosted solutions led with 66.23% of the quantum computing market share in 2024, yet on-premise systems are set to grow at a 32.66% CAGR as OEMs seek lower latency and IP protection.

- By end-user, original equipment manufacturers accounted for 41.28% of the quantum computing market share in 2024, but R&D institutions exhibit the fastest trajectory at 33.87% CAGR to 2030.

- By geography, North America represented 36.21% of the quantum computing market share in 2024, whereas Asia-Pacific is poised for the highest regional CAGR of 34.21% through 2030.

Market Trends and Insights

Drivers Impact Analysis of Quantum Computing In Automotive Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in AI-Driven Autonomous Workloads | +8.2% | Global, with concentration in North America and China | Medium term (2-4 years) |

| Urgent Push for EV Battery Breakthroughs | +6.8% | Global, with emphasis on Europe and Asia-Pacific | Long term (≥ 4 years) |

| OEM–Quantum Partnerships Scaling Post-2023 | +5.4% | North America & Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Hybrid Quantum Algorithms Showing Early ROI | +4.7% | Global | Short term (≤ 2 years) |

| Quantum-Safe V2X Rules Entering Regulations | +3.9% | North America and EU, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Cloud QCaaS Cutting CapEx for Tier-1s and Fleets | +2.3% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Boom in AI-Heavy Autonomous-Driving Workloads

Level 4 vehicles process several terabytes of lidar, radar, and camera data daily, and the combinatorial path-planning and object-recognition challenges outstrip the scaling curves of classical GPUs. Quantum machine-learning models run on trapped-ion and superconducting systems have demonstrated faster convergence and higher accuracy in sign-recognition and trajectory-optimization benchmarks, trimming inference latency without sacrificing safety margins. Early deployments with Hyundai and IonQ display shorter classification runtimes than best-in-class deep-learning accelerators. Automakers reallocate R&D budgets toward quantum algorithm design because conventional silicon improvements will not close the widening compute gap. This dynamic positions quantum acceleration as a critical enabler for broad Level 4 and Level 5 roll-outs during the forecast horizon.

Urgent Need to Accelerate EV Battery-Chemistry Discovery

Regulatory zero-emission deadlines push battery-material breakthroughs onto compressed timelines that standard density-functional theory cannot satisfy. Gate-based quantum simulators resolve electron-correlation effects in solid-state interfaces, letting chemists evaluate candidate cathode or electrolyte molecules in days rather than years. Ford and Quantinuum applied variational quantum eigensolver workflows to lithium-ion cell chemistries, uncovering stable phase combinations that classical supercomputer models could not converge. German OEMs have broadened the remit to cover metal-lattice distortion and battery thermal management, underlining quantum computing’s potential to cut physical prototyping cycles and boost energy density. Governments in Japan, Korea, and the European Union co-fund pilot lines that embed quantum simulations into the battery-design toolchain to maintain EV-export competitiveness.

OEM–Quantum Vendor Investments and Pilots Scaling Post-2023

Since 2023, partnerships have shifted from corporate-innovation showcases to operational deployments inside production systems. BMW’s “Quantum Computing for Automotive Challenges” contest on AWS transitioned into live-shop-floor workflows that reschedule robot paths in Dingolfing and Spartanburg plants. Toyota Tsusho built quantum supply-chain solvers on ion-trap hardware, optimizing multimodal parts routing across four continents. Capital flows mirror the operational pivot: Bosch Ventures took a strategic stake in Quantum Motion to align cryogenic-CMOS development with future ASIC needs, while Volkswagen’s software unit invested in hybrid-solver startups to secure algorithm IP. These moves create a reinforcing cycle in which demonstrated ROI accelerates board-level budget allocations for additional quantum use cases.

Hybrid Quantum-Inspired Algorithms Delivering Near-Term ROI

Automotive enterprises can monetize quantum techniques today by coupling classical pre-processing with quantum sub-routines that attack the most computationally intensive kernels. BMW’s production-planning model reduced cycle time 15% by delegating a million-variable constraint set to a D-Wave hybrid annealer that returned high-quality near-optimal schedules within maintenance-window limits[1]“Volkswagen Boosts Paint-Shop Throughput With Hybrid Quantum Annealing,”, D-Wave Systems Inc., dwavesys.com. Similar gains arise in paint-shop color-switch sequence optimization, dynamic vehicle routing, and parts-inventory minimization. The financial clarity of these wins lowers internal adoption barriers and cultivates quantum-skilled engineering cohorts, preparing organizations for a smooth transition to fault-tolerant processors later in the decade.

Restraints Impact Analysis of Quantum Computing In Automotive Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| NISQ Hardware: High Error Rates, Few Qubits | -7.3% | Global | Medium term (2-4 years) |

| Severe Shortage of Quantum Talent | -5.8% | Global, particularly acute in Europe and North America | Long term (≥ 4 years) |

| Cryo & Vibration Challenges for Vehicle-Grade QC | -4.2% | Global | Long term (≥ 4 years) |

| Hidden ESG/Energy Costs of Quantum Data Centers | -2.1% | Global, with emphasis on Europe due to ESG regulations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

NISQ-Era Hardware Error Rates and Limited Qubit Counts

Despite their advancements, superconducting and ion-trap quantum processors still grapple with elevated two-qubit error rates at their most advanced nodes. This limitation curtails the depth of logical circuits and restricts the scope of solvable problems. Such constraints are particularly challenging for automotive optimization tasks, which typically deal with vast variable sets. The limited physical qubits in quantum hardware fall short of handling this complexity. As a workaround, they often turn to coarse problem decomposition, a method that notably undermines the theoretical performance boosts that quantum computing promises. Error-mitigation and zero-noise-extrapolation techniques extend reach but add classical overhead and variable run-time. As a result, many near-term applications remain confined to proof-of-value scopes rather than plant-wide deployments. Vendors publish aggressive roadmaps toward million-qubit fault-tolerant architectures, but engineering realities underpin a multiyear lag that restrains growth momentum.

Severe Global Shortage of Quantum-Skilled Engineers

Automotive OEMs require talent fluent in quantum circuits and automotive control systems, a rare intersection that commands premium salaries unattainable for most Tier-2 suppliers. The talent gap forces companies to depend on external quantum vendors, diluting proprietary know-how and increasing vendor-lock-in risk. Joint degree programs and national training grants exist, but upskilling pipelines take years. Until the labor market equilibrates, staffing bottlenecks will impede large-scale internalization of quantum development and slow the adoption of quantum computing in the automotive market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Quantum Computing In Automotive Market Segment Analysis

By Technology Type:

Superconducting Systems Maintain Lead While Photonic Platforms AccelerateQuantum computing in the automotive market size for superconducting platforms equals 46.37% revenue share in 2024, propelled by readily available cloud access from IBM, Google, and Rigetti. Photonic hardware, in contrast, accounted for a smaller base but is forecast to exhibit the fastest 34.28% CAGR through 2030 as Xanadu and ORCA Computing ship room-temperature prototypes that remove cryogenic overhead. Superconducting gate fidelity improvements enable deeper algorithms for machine-learning inference and molecular simulation, functions highly prized by battery-research teams. Automotive IT architects appreciate these mature stacks' rich open-source tooling and robust calibration procedures, fostering rapid proof-of-concept deployment cycles.

The photonic surge introduces complementary strengths. Continuous-variable photonic qumodes excel in sampling and combinatorial optimization tasks pertinent to traffic-flow regulation and real-time vehicle-network management. Photon-based qubits demonstrate resilience to thermal vibration, which bodes well for eventual in-vehicle accelerators. Car makers are therefore hedging bets: Volkswagen is piloting photonic co-processors for secure V2X channels, while BMW maintains superconducting testbeds for simulation-heavy workloads. Quantum annealers remain niche but prove their worth in plant scheduling; D-Wave’s Advantage pipeline processes constraint-satisfaction problems with million-variable density unmatched by gate-based rivals, ensuring annealing retains a specialized but profitable foothold inside the quantum computing in automotive market.

By Application:

Autonomous-Driving Algorithms Overtake Supply-Chain OptimizationSupply-chain and logistics optimization generated 26.22% of 2024 revenue, reflecting quick wins from quantum routing, warehouse stacking, and global parts-order decomposition. Toyota’s distribution network quantifies a 12% freight-mile reduction after integrating annealing solvers into its nightly transport-planner runs, validating immediate economic returns. Yet autonomous-driving workloads are projected to leapfrog with a 33.62% CAGR to 2030 owing to the explosive data-processing demands of Level 4 perception and decision stacks. Quantum-accelerated feature-extraction and sensor-fusion networks shed milliseconds of latency, critical for safety envelopes in dense urban scenarios.

Given quantum simulation’s unrivaled ability to predict electron behavior in novel solid-state formulations, battery-chemistry modeling represents another breakout niche. Vehicle design digital twins and predictive-maintenance analytics round out the expanding menu of use cases, each drawing upon quantum optimization or sampling hooks that offer order-of-magnitude speedups over high-performance computing clusters. The diversity of adoption paths underscores why the quantum computing in the automotive market is widening beyond IT departments to touch material-science labs, plant-operations teams, and mobility-services divisions across the automotive value chain.

By Component:

Software Platforms Become the Primary Growth EngineQuantum processors still captured 41.28% of 2024 spend, reflecting hardware leasing fees embedded in QCaaS contracts. Nonetheless, quantum software platforms are on track for a 34.48% CAGR, outpacing every other component as OEMs realize that algorithm development and orchestration middleware dictate real differentiation. Compiler stacks like Qiskit, Cirq, and PennyLane integrate domain-specific libraries for routing, fluid dynamics, and battery simulation, letting automotive engineers code quantum routines using familiar Python interfaces.

Quantum sensors are entering pilot fleets for navigation drift correction and magnetic-field mapping. At the same time, revenue remains nascent, the long-term promise of centimeter-level positioning accuracy could reinvent ADAS road-map architecture. Meanwhile, turnkey algorithm libraries become proprietary assets: Volkswagen’s paint-shop sequencing solver and BMW’s body-panel formability kernel serve as reusable accelerators across multiple plants, anchoring sticky platform relationships with chosen quantum vendors. As solution depth increases, software royalties and maintenance contracts will form a larger slice of the quantum computing in the automotive market.

By Deployment Type:

Cloud Dominance Faces Rapid On-Premise UptakeCloud instances represented 66.23% of 2024 revenue because QCaaS offerings from AWS Braket, Azure Quantum, and IBM Quantum Network let users experiment on byte-metered tariffs instead of capitalizing on cryogenic racks. The pay-per-shot model suits Tier-1 suppliers that need intermittent access for scheduling runs or design-space exploration during program kickoff phases. Automotive CIOs also favor cloud because hardware upgrades happen transparently, ensuring continuous availability of the newest qubit topologies without procurement cycles.

However, the on-premise segment is accelerating at a 32.66% CAGR. IP-sensitive tasks like battery material discovery and autonomous-driving neural-net training entail confidential datasets whose transfer to external clouds triggers compliance and cybersecurity scrutiny. Latency-sensitive closed-loop manufacturing-execution algorithms also benefit from local qubit adjacency. BMW’s Munich campus and Toyota’s Aichi research center budget for modest on-premise pods by 2027, aiming to integrate quantum co-processors directly into high-performance compute backbones. Hybrid topologies that burst from private clusters to public clouds during capacity spikes will likely dominate operational best practice.

By End-User:

R&D Institutions Outpace OEM Spending GrowthOriginal equipment manufacturers booked 41.28% of total expenditure in 2024 as they chased competitive differentiation through proprietary algorithms and process optimization. Volkswagen, Hyundai, and Mercedes-Benz each operate cross-disciplinary quantum task forces that link manufacturing, AI safety, and battery science. Yet university laboratories and public-private research institutes are set for the steepest 33.87% CAGR, thanks to multibillion-dollar national quantum grants that underwrite algorithm and hardware prototyping missions tied to automotive use cases.

Tier-1 suppliers—Bosch, Continental, Denso—follow closely: their complex global supply chains invite quantum routing and inventory minimization, and they must co-innovate with OEM partners to keep pace. Fleet operators like DHL and UPS generate demand, focusing on route-mix optimization and energy-cost trimming for electrified logistics vans. The collaboratively networked nature of automotive R&D means know-how circulates between academia, suppliers, and automakers, expanding the breadth of skills feeding into quantum computing in the automotive market.

Geography Analysis

North America Quantum Computing In Automotive Market

North America held 36.21% of revenue in 2024, anchored by a dense constellation of quantum hardware pioneers—IBM, Google, IonQ, Rigetti—and a vibrant automotive R&D corridor stretching from Michigan to Silicon Valley. Federal research tax credits and the CHIPS and Science Act funnel grants toward quantum processor scaling, luring partnerships with Ford, General Motors, and Tesla. Canadian influence remains outsized through D-Wave’s annealing leadership and a conducive government-backed Quantum Strategy that subsidizes automotive-linked pilot studies. The cross-pollination between software startups and automaker innovation labs cements North America’s primacy in the early commercialization of quantum workloads.

APAC Quantum Computing In Automotive Market

Asia-Pacific, however, is the growth pacesetter with a 34.21% CAGR projected through 2030. Japan’s Toyota Tsusho and Nissan nurture trapped-ion and photonic collaborations supported by METI-funded quantum budgets. South Korea blends Samsung’s semiconductor acumen with Hyundai’s autonomous vehicle ambitions, creating an ecosystem where quantum R&D gains immediate scaling leverage inside global vehicle export platforms. China’s state-led Quantum Science Initiative finances fault-tolerant prototypes and offers automakers preferential access to national quantum centers, although IP-transfer regulations and export controls complicate international project structures. The region’s sheer vehicle production volume provides a vast sandbox for supply-chain and traffic optimization pilots, accelerating diffusion of best practices across domestic brands.

Europe Quantum Computing In Automotive Market

Europe retains strategic weight courtesy of heavyweight OEMs—Volkswagen, BMW, Mercedes-Benz—and a supranational quantum budget that mandates industrial applicability. Germany’s Quantum Technology and Application Consortium integrates Fraunhofer Institutes with Tier-1 suppliers to create reference architectures for in-plant quantum workloads. France’s Pasqal leads neutral-atom breakthroughs, attracting Stellantis and Renault for battery-electrolyte simulations. While venture capital remains less abundant than in the United States, public-sector co-funding offsets risk and ensures continuity of long-term hardware roadmaps. Compliance with emerging quantum-safe cybersecurity laws under UN Regulations R.155 and R.156 gives European OEMs a regulatory first-mover edge.

MEA and South America Quantum Computing In Automotive Market

The Middle East & Africa and South America presently contribute single-digit revenue shares but hold latent potential. Gulf states incorporate quantum initiatives into sovereign diversification plans, exploring traffic-flow optimizers for mega-urban development zones. Brazil’s EMBRAPII backs feasibility studies coupling ethanol supply chains with quantum modeling, setting the stage for future adoption once hardware cost curves decline. Cross-regional QCaaS access ensures that geographical entry barriers fall steadily, enabling global participation in quantum computing in the automotive market as connectivity infrastructure matures.

Competitive Landscape

The quantum computing in automotive market features a mosaic of co-opetition rather than head-to-head battles. Pure-play quantum firms focus on hardware maturity and algorithm libraries, partnering with automotive incumbents that possess domain expertise and systems-integration muscle. D-Wave’s Advantage annealer solves million-variable constraint sets for Volkswagen’s paint-shop color sequencing, delivering documented throughput gains. IonQ leverages trapped-ion coherence times for perception-model training with Hyundai, while Quantinuum collaborates with Ford on lithium-ion chemical-simulation kernels. Hardware differentiation—qubit count, error rate, gate connectivity—matters, but automotive partners increasingly evaluate vendors on integration roadmaps, safety certification support and adherence to emerging quantum-safe standards.

Automotive OEMs pursue equity stakes or long-term strategic-sourcing contracts to secure priority qubit access amid anticipated capacity shortages. Bosch Ventures’ investment in Quantum Motion illustrates the trend: large Tier-1s buy into hardware startups to align roadmap objectives. White space proliferates in middleware that marries shop-floor MES or ADAS toolchains with quantum backend schedulers. Multiverse Computing, Zapata and Riverlane position themselves as abstraction-layer specialists, providing domain-optimized APIs that insulate car makers from raw qubit management intricacies.

Regulation and cybersecurity emerge as competitive levers. Vendors offering certified post-quantum encryption modules under NIST SP 800-208 or British DfT guidelines gain favor as automakers must demonstrate compliance for over-the-air updates and V2X channels[2]“SP 800-208: Stateful Hash-Based Signatures,”, National Institute of Standards and Technology, nist.gov. Manufacturers also scrutinize vendors’ ESG credentials given the cooling-power footprint of dilution refrigerators[3]“Consultation on Automotive Cyber-Security Under UN R155–R156,”, UK Department for Transport, gov.uk. Firms pledging renewable-powered data-center operations or cryogenic-efficiency breakthroughs may secure differentiation as Scope 3 emissions accounting widens to include compute resources.

Quantum Computing In Automotive Industry Leaders

D-Wave Quantum Inc.

Quantinuum

Google Quantum AI

IonQ, Inc.

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Quantum Computing In Automotive Market Companies Covered in this Report

- D-Wave Quantum Inc.

- IBM Corporation

- Quantinuum

- Google Quantum AI

- IonQ, Inc.

- Rigetti & Co, LLC.

- Xanadu

- PASQAL

- Terra Quantum

- BosonQ Psi

- Microsoft Azure Quantum

- AWS Braket

- Volkswagen Group

- BMW Group

- Hyundai Motor Company

- Robert Bosch GmbH

- Mercedes-Benz

- Ford Motor Company

Recent Industry Developments in Quantum Computing In Automotive Market

- March 2025: Ford Otosan, a joint venture of Ford Motor Company and Koç Holding in Turkey, has rolled out a hybrid-quantum application in production, optimizing the manufacturing processes for its Ford Transit vehicles. This move comes in collaboration with D-Wave Quantum Inc., a frontrunner in quantum computing systems, software, and services.

- July 2024: planqc, Europe's frontrunner in digital atom-based quantum computing, has successfully secured EUR 50 million (USD 54.09 million) in financing. The funds will be directed towards launching a quantum computing cloud service and crafting quantum software tailored for sectors including chemistry, healthcare, climate-tech, automotive, and finance. Notably, planqc is harnessing quantum machine learning to enhance climate simulations and develop more efficient batteries for electric vehicles.

- June 2024: In a notable leap for quantum computing in the automotive realm, Classiq has teamed up with NVIDIA and the BMW Group to enhance mechatronic systems.

Global Quantum Computing In Automotive Market Report Scope

Segmentation Overview

| Superconducting Quantum Computing |

| Quantum Annealing |

| Photonic Quantum Computing |

| Autonomous Driving |

| Traffic Flow Optimization |

| Vehicle Design Simulation |

| Battery Chemistry Modeling |

| Predictive Maintenance |

| Supply Chain and Logistics Optimization |

| Quantum Processors |

| Quantum Software Platforms |

| Quantum Sensors |

| Quantum Algorithms |

| Cloud-Based Quantum Solutions |

| On-Premise Quantum Systems |

| OEMs (Original Equipment Manufacturers) |

| Tier 1 Suppliers |

| Fleet Operators |

| R&D Institutions |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East & Africa |

| By Technology Type | Superconducting Quantum Computing | |

| Quantum Annealing | ||

| Photonic Quantum Computing | ||

| By Application | Autonomous Driving | |

| Traffic Flow Optimization | ||

| Vehicle Design Simulation | ||

| Battery Chemistry Modeling | ||

| Predictive Maintenance | ||

| Supply Chain and Logistics Optimization | ||

| By Component | Quantum Processors | |

| Quantum Software Platforms | ||

| Quantum Sensors | ||

| Quantum Algorithms | ||

| By Deployment Type | Cloud-Based Quantum Solutions | |

| On-Premise Quantum Systems | ||

| By End-User | OEMs (Original Equipment Manufacturers) | |

| Tier 1 Suppliers | ||

| Fleet Operators | ||

| R&D Institutions | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East & Africa | ||

Key Questions Answered in the Report

What revenue growth is expected in quantum computing for automotive by 2030?

The quantum computing in automotive market size is forecast to reach USD 2.17 billion by 2030, expanding at a 31.13% CAGR.

Which technology platform currently leads adoption among automakers?

Superconducting systems hold the largest 46.37% share thanks to mature cloud access from IBM, Google and Rigetti.

Why are automakers investing in on-premise quantum hardware?

On-premise installations protect proprietary algorithms and cut latency for real-time manufacturing or ADAS workloads, driving a 32.66% CAGR for this deployment model.

How does quantum computing enhance autonomous driving?

Quantum machine-learning and optimization algorithms reduce sensor-fusion latency and optimize trajectory planning, supporting Level 4 and Level 5 performance targets.

What is the biggest challenge to scaling automotive quantum applications?

NISQ hardware limitations and a shortage of quantum-skilled engineers together constrain the complexity and rollout speed of commercial deployments.

Page last updated on: