Quantum Computing In Drug Discovery Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

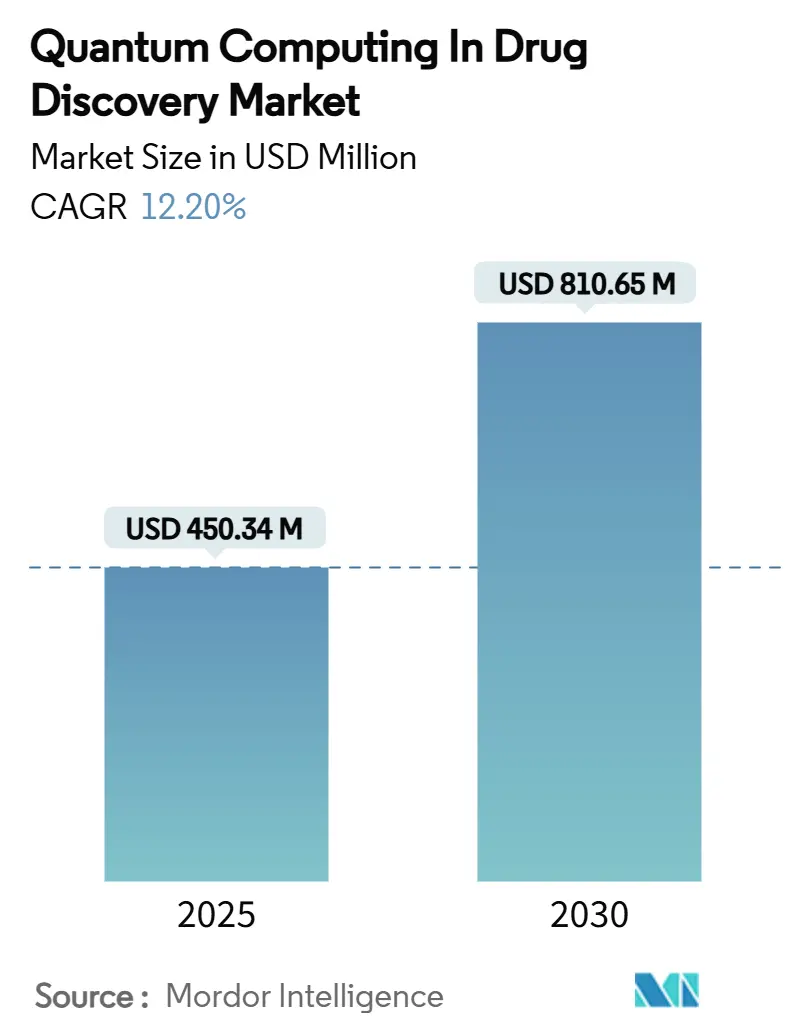

| Market Size (2025) | USD 450.34 Million |

| Market Size (2030) | USD 810.65 Million |

| Growth Rate (2025 - 2030) | 12.20% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Quantum Computing In Drug Discovery Market Analysis by Mordor Intelligence

The quantum computing in drug discovery market size reached USD 450.34 million in 2025 and, on its present trajectory, will enlarge to USD 810.65 million by 2030, producing a robust 12.20% CAGR over the forecast window. Rising cloud access to qubit resources, escalating pharmaceutical–quantum partnerships, and sustained government moon-shot funding converge as the primary accelerants behind this expansion. Pharmaceutical developers, under pressure to compress traditional 10- to 15-year research cycles, are adopting quantum molecular-simulation workflows to refine hit lists, optimize leads, and de-risk later-stage programs. Competitive dynamics remain fluid because the technology is still early-stage, yet the clear cost and time advantages are compelling enough that early movers expect meaningful productivity gains once logical-qubit counts surpass 1,000. Greater availability of quantum-ready application programming interfaces is also easing integration with legacy high-performance computing stacks, broadening the commercial reach of gate-model and photonic hardware.

Key Report Takeaways

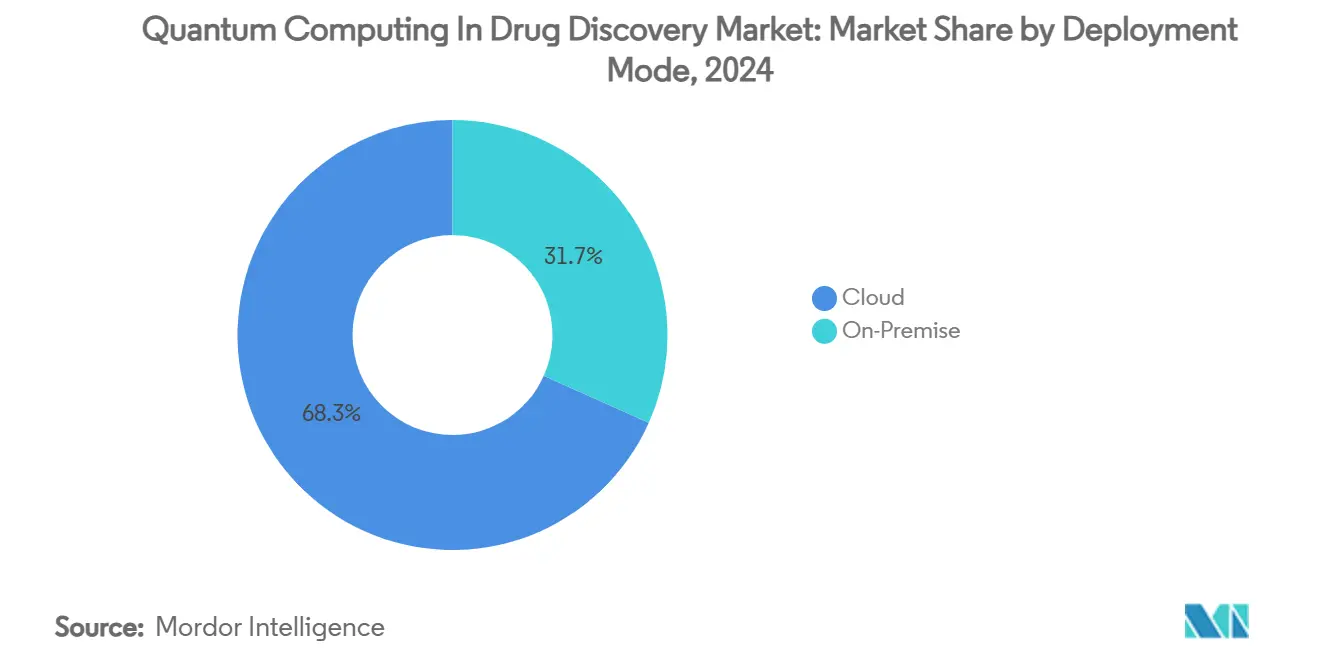

- By deployment mode, cloud solutions accounted for 68.3% of quantum computing in drug discovery market share in 2024, while on-premise installations are projected to expand at a 14.5% CAGR through 2030.

- By quantum processing type, gate-model processors led with 46.7% revenue share in 2024; photonic hardware is forecast to register the fastest 15.7% CAGR to 2030.

- By drug discovery stage, lead optimisation captured a 38.3% share of the quantum computing in drug discovery market size in 2024, whereas target identification and validation are advancing at a 16.6% CAGR through 2030.

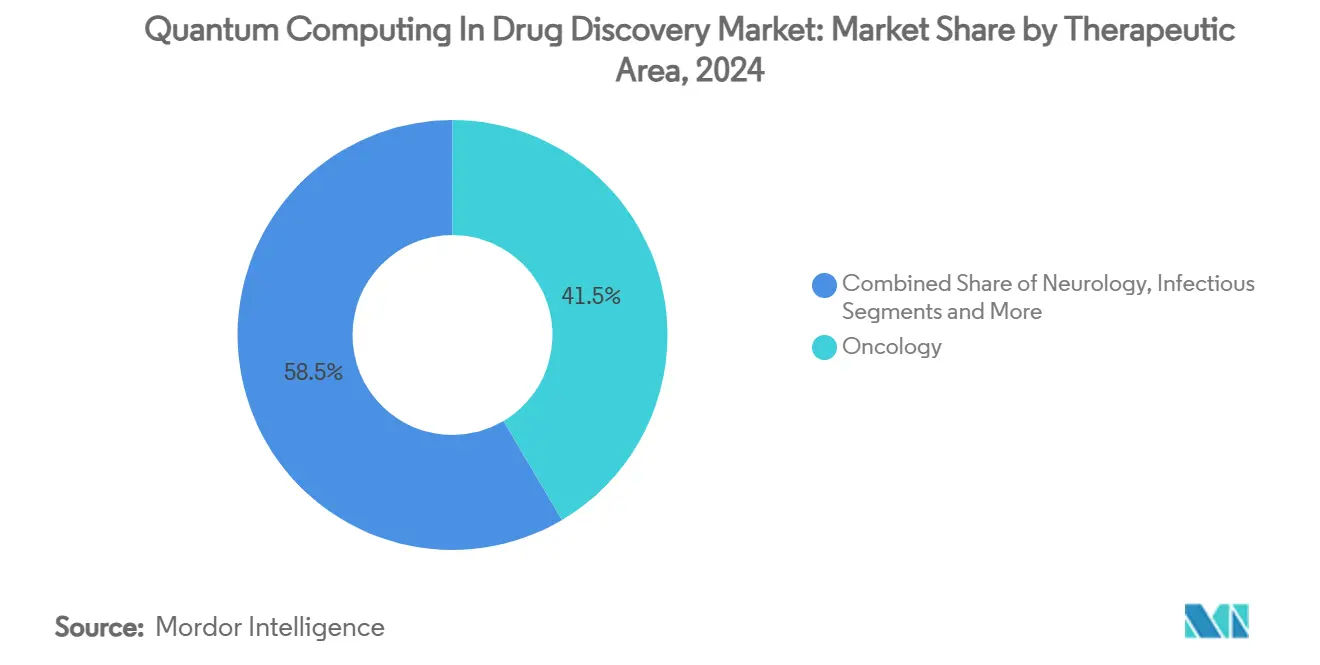

- By therapeutic area, oncology dominated with 41.5% share in 2024, while rare and orphan diseases are poised for the quickest growth at a 14.3% CAGR over the forecast period.

- By end user, pharmaceutical and biotech companies held 53.8% share in 2024; quantum drug-discovery start-ups are projected to post the highest 13.7% CAGR to 2030.

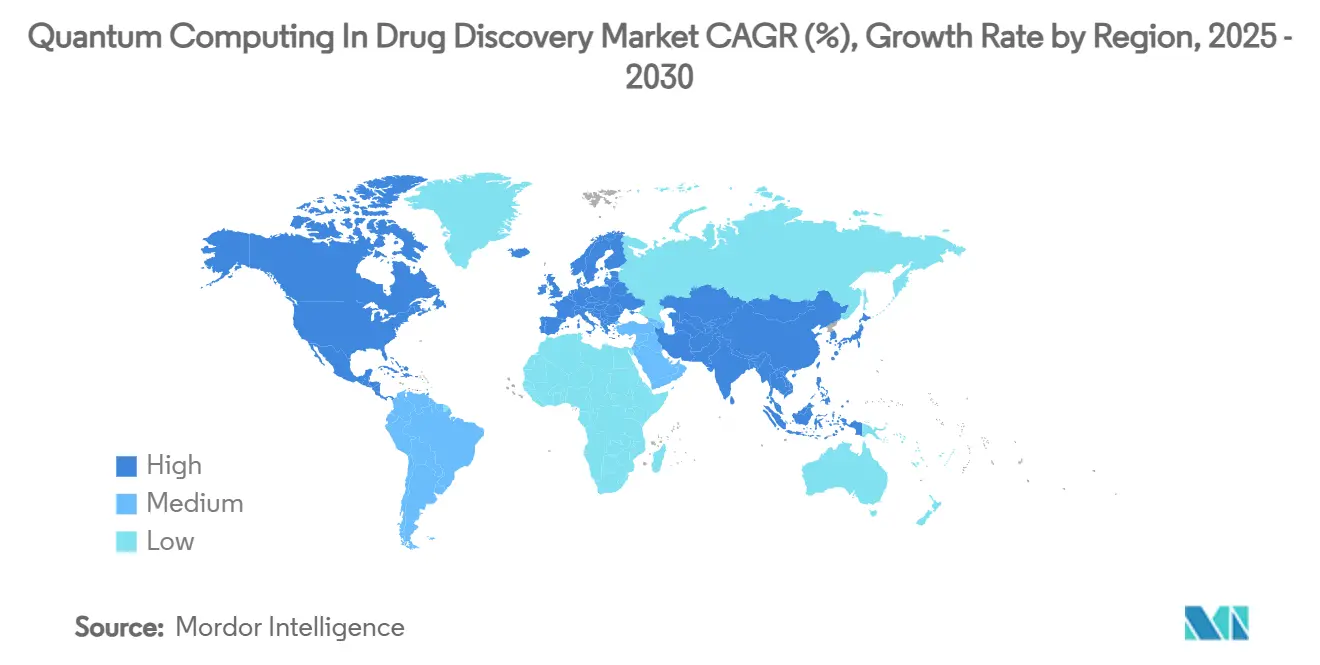

- By geography, North America remained the largest regional market with 51.1% share in 2024, whereas Asia-Pacific is expected to record the strongest 17.1% CAGR through 2030.

Global Quantum Computing In Drug Discovery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud accessibility democratising molecule simulation | +2.50% | North America, Europe early; Global diffusion | Medium term (2-4 years) |

| Pharma-quantum alliances accelerating VC funding | +1.80% | North America & EU core; APAC expanding | Short term (≤ 2 years) |

| Government quantum grants for biopharma use cases | +1.20% | US, UK, Germany, China, Australia | Long term (≥ 4 years) |

| Hybrid AI-QC platforms cutting computational cost | +1.50% | Silicon Valley, Boston, London hubs | Medium term (2-4 years) |

| Error-corrected logical qubits >1,000 | +1.30% | Global research centers | Long term (≥ 4 years) |

| Quantum-as-a-Service price competition | +0.90% | North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Exponential Growth in Quantum-Cloud Accessibility Democratizing Molecule Simulation

Cloud platforms remove the USD 15–50 million capital barrier that once restricted quantum access to elite labs. Microsoft’s Azure Quantum Elements introduced generative chemistry and accelerated density-functional-theory services in 2024, allowing mid-tier biotechs to screen millions of compounds via browser dashboards. Hybrid orchestration that pairs classical GPUs with gate-model qubits now returns property predictions in hours rather than weeks, trimming early drug-development cycles. University of Copenhagen researchers further boosted accuracy by publishing new mathematical “recipes” that reduce noise in quantum molecular algorithms[1]University of Copenhagen, “Quantum Researchers Come Up with a Recipe That Could Accelerate Drug Development,” scientedaily.com. Commercial pilots confirm these gains: IonQ, AstraZeneca, AWS, and NVIDIA publicly demonstrated quantum-accelerated lead-generation workflows able to process broader chemical spaces at lower compute cost. As a result, the quantum computing in drug discovery market is transitioning from isolated proofs-of-concept to repeatable, cloud-hosted production chores.

Pharma-Quantum Strategic Alliances Accelerating Venture-Capital Influx

Large drug makers are underwriting specialist quantum software vendors to secure first-mover access to custom algorithms. Eli Lilly’s USD 1 billion commitment to Creyon’s RNA-oriented quantum chemistry engine became the sector’s most significant single transaction in 2025. Zapata’s work with multiple pharma sponsors produced quantum-enhanced generative AI that generated viable KRAS inhibitors ahead of classical benchmarks, galvanizing fresh investor interest. Consortium models are emerging as capital-efficient vehicles: KT Consortium pools resources from Henkel, Mitsubishi Chemical, and others to co-fund foundational toolchains. Novo Holdings’ EUR 188 million (USD 219.72 million) allocation to establish a Danish quantum-life-science hub underscores that investment is moving beyond North America. These cash infusions accelerate hardware development and stimulate application-specific libraries, directly enlarging the quantum computing in the drug discovery market.

Government Quantum Moon-Shot Grants Targeting Biopharma Use Cases

Regulators are seeding national programs that expressly include drug discovery pilot studies. NIH’s Quantum Computing Challenge funds algorithm ideation for oncology and rare-disease targets[2]National Institutes of Health, “Quantum Computing Challenge,” nih.gov. Australia pledged AUD 940 million (USD 612.22 million) to PsiQuantum, with stated expectations of a USD 48 billion life-science GDP uplift by 2040. A Netherlands-France-Germany trilateral initiative placed more than EUR 30 million (USD 35.04 million) behind cross-border projects in 2025. The UK earmarked EUR 30 million (USD 35.04 million) for a broader EUR 45 million (USD 52.59 million) quantum package for healthcare applications[3]Department for Science, Innovation and Technology, “Unlocking the Potential of Quantum: £45 Million Investment to Drive Breakthroughs in Brain Scanners, Navigation Systems, and Quantum Computing,” gov.uk. This public-sector scaffolding mitigates risk for private sponsors and speeds readiness of national testbeds that will feed the quantum computing in the drug discovery industry over the long term.

Emergence of Hybrid AI-QC Drug-Discovery Platforms Cutting Computational Cost

Pairing deep-learning models with variational quantum circuits is yielding measurable speed-ups on compound-screening tasks. Model Medicines dubbed 2025 the “inflection year” for commercially viable hybrid stacks after validating rapid hit-to-lead pipelines. Insilico Medicine’s KRAS-focused project screened 100 million molecules on a combined classical–quantum workflow, illustrating scale advantages impossible for quantum or AI alone. SandboxAQ and Sanofi extended the paradigm into biomarker discovery, widening addressable applications. Research prototypes such as Q-Drug encode molecules into Ising-model objective functions, reducing compute time by nearly an order of magnitude. As hardware matures, these hybrid architectures will dominate quantum computing in the drug discovery market thanks to their practicality in the noisy-intermediate-scale-quantum era.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hardware decoherence limits deep circuits | -1.40% | Global variance by vendor | Medium term (2-4 years) |

| Scarcity of quantum-skilled drug-discovery talent | -0.80% | North America & Europe acute | Long term (≥ 4 years) |

| Regulatory uncertainty on quantum-generated data | -0.60% | Primarily US & EU | Long term (≥ 4 years) |

| High on-premise system cost for mid-tier pharma | -1.10% | Emerging markets hardest hit | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Hardware Decoherence Limiting Deep Circuits for Large Molecules

Current noisy-intermediate-scale devices cannot preserve coherent states long enough to execute the depth required for whole-protein simulations. University of Rochester findings show decoherence rises exponentially with molecular complexity, nullifying speed gains on larger targets. Tensor-network emulation studies confirm that required bond dimensions grow quickly, erasing runtime advantages once systems exceed a few hundred qubits. Protein-folding challenges remain chiefly classical, forcing practitioners to confine quantum work to fragment-based models or hybrid splits. Until fault-tolerant architectures arrive, this ceiling tempers near-term addressable revenue within the quantum computing in drug discovery market.

Scarcity of Quantum-Skilled Drug-Discovery Talent Inflating Project Timelines

Demand for scientists fluent in quantum mechanics and medicinal chemistry outstrips supply, slowing project ramp-ups. Interviews with leading pharma CTOs indicate budgets are available, but teams require six to nine months to secure essential staff, stretching pilot timetables. Academia is only now merging quantum computing and pharmacology syllabi, implying multiyear lags before a steady graduate pipeline appears. Large firms are launching in-house academies, yet smaller biotechs must often outsource algorithm development, increasing dependency on external vendors and squeezing margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Dominance Accelerates Access

Cloud environments accounted for 68.3% of quantum computing in drug discovery market share in 2024, cementing their place as the default entry route for most pharmaceutical users. On-demand contracts deliver qubit cycles without facility overhead, and fully managed stacks translate to minimal in-house quantum expertise. Microsoft’s Azure Quantum Elements and IBM’s Partner Program report monthly upticks in active pharma tenants, signalling a broadening customer base.

Nonetheless, on-premise footprints will post a 14.5% CAGR to 2030, driven by global pharma majors pursuing proprietary pipelines for competitive secrecy. These installations often integrate cryogenic gate-model rigs with in-house high-performance clusters, forming hybrid backbones that shorten data-sovereignty review cycles. Consequently, vendors that offer configurable deployment flexibility are poised to capture wider slices of the quantum computing in drug discovery market.

By Quantum Processing Type: Gate-Model Leadership Faces Photonic Challenge

Gate-model architectures led 2024 revenue with 46.7%, reflecting their compatibility with variational eigensolvers central to quantum chemistry. Yet photonic systems’ tolerance for room-temperature operation and lower decoherence positions them as the highest-growth class, advancing at 15.7% CAGR. Quantum annealers currently fill discrete optimization niches such as conformer clustering, holding 23.1% share, while simulator-oriented rigs carry 18.5% share by supporting time-evolution studies for mid-size molecules.

Hardware heterogeneity implies a pluralistic future: pharmaceutical teams will choose processing modalities best aligned to task-level requirements, thereby encouraging multi-vendor procurement strategies and broadening technical demands inside the quantum computing in drug discovery market.

By Drug Discovery Stage: Lead Optimization Dominance Shifts

Gate-model architectures led 2024 revenue with 46.7%, reflecting their compatibility with variational eigensolvers central to quantum chemistry. Yet photonic systems’ tolerance for room-temperature operation and lower decoherence positions them as the highest-growth class, advancing at 15.7% CAGR. Quantum annealers currently fill discrete optimization niches such as conformer clustering, holding 23.1% share, while simulator-oriented rigs carry 18.5% share by supporting time-evolution studies for mid-size molecules.

Hardware heterogeneity implies a pluralistic future: pharmaceutical teams will choose processing modalities best aligned to task-level requirements, thereby encouraging multi-vendor procurement strategies and broadening technical demands inside the quantum computing in drug discovery market.

By Therapeutic Area: Oncology Leadership Drives Innovation

Oncology commanded a 41.5% share in 2024, where complex mutational landscapes demand high-fidelity molecular dynamics well suited to quantum simulation. Life-time values of cancer therapies justify premium compute spending, making oncology a proving ground for early quantum ROI. Neurology held 19.2%, infectious diseases 15.8%, and metabolic-cardiovascular domains 13.7%. Rare and orphan conditions, though just 9.8% today, post the swiftest 14.3% CAGR because quantum-enabled precision can turn small-population economics favourable.

Quantum techniques in oncology already extend beyond simulation to diagnostic imaging enhancement through quantum neural networks, showing the breadth of clinical pathways available once hardware matures. This enriches the long-run prospects for quantum computing in the drug discovery market.

By End User: Pharma Dominance Enables Startup Growth

Pharmaceutical and Biotech Enterprises absorbed 53.8% of 2024 revenue, confirming their role as anchor clients. Contract research organizations followed with 21.7%, often white-labelling cloud quantum environments for fee-for-service engagements. Academia accounted for 15.4% through grant-funded algorithm development that feeds commercial pipelines. Start-ups captured 9.1% yet project a 13.7% CAGR, reflecting strong venture funding and lighter organizational inertia.

This mix shows double-sided momentum: entrenched pharma sponsors secure capacity, while agile newcomers push inventive algorithms faster. Their interaction advances the entire quantum computing in drug discovery market, establishing new tool chains and proof points.

Geography Analysis

North America retained 51.1% of 2024 revenue, leveraging its dense cluster of quantum hardware vendors and big-pharma headquarters. Federal initiatives such as NIH’s Quantum Computing Challenge funnel public grants directly into healthcare applications. Private-sector coupling exemplified by IBM and Cleveland Clinic’s dedicated healthcare quantum computer demonstrates institutional buy-in. Combined, these factors create a virtuous feedback loop in which research breakthroughs rapidly convert into commercial pilots and reinforce the region’s leadership.

Europe followed with a 28.4% slice, underpinned by coordinated multistate programs and corporate commitments exemplified by Boehringer Ingelheim’s quantum labs sited in Germany. The continent benefits from an integrated regulatory environment that can harmonize guidelines swiftly once standards emerge. Trilateral calls between the Netherlands, France, and Germany infuse capital into cross-border consortia, broadening the supplier ecosystem and supporting SMEs that feed specialized modules into large pharma workflows.

Asia-Pacific, although currently smaller, is the fastest-advancing geography, growing at a 17.1% CAGR. China’s Tencent Quantum Lab pursues proprietary circuit optimization for medicinal chemistry, while Japan’s Fujitsu and RIKEN progress superconducting hardware lines aimed explicitly at drug discovery workloads. Australia’s unprecedented AUD 940 million backing of PsiQuantum exemplifies government ambition to vault into forefront positions. Regional universities such as Hong Kong Polytechnic deliver quantum micro-processor research that filters rapidly into start-ups, creating a fresh pipeline of tools tailored to local pharma needs.

The rest of the world, including the Middle East and Latin America, remains to be explored. Their adoption curves depend on cloud-service rollouts that mitigate capital barriers; as platform vendors extend colocation facilities, uptake should accelerate, but sizable revenue contributions materialize mainly after 2027. Overall, regional variances reflect differing access to capital, talent, and policymaking agility, yet collectively, they ensure the quantum computing in the drug discovery market acquires genuinely global contours by decade’s end.

Competitive Landscape

Competition is moderate but intensifying as gate-model specialists, photonic pioneers, cloud hyperscalers, and pharma-backed labs vie for early reference wins. Strategic partnerships dominate because no single entity holds all required proficiencies. IBM aligns with Moderna on mRNA structure prediction, Google Quantum AI partners with Boehringer Ingelheim for molecular-dynamics work, and IonQ teams with AstraZeneca to integrate qubit services into existing AWS pipelines. Such alliances share risk, merge domain expertise, and accelerate time-to-validation for quantum algorithms.

Technology differentiation centers on three pillars: qubit stability, chemistry-specific libraries, and seamless API integration with legacy informatics. Photonic vendors argue their room-temperature operation removes a key obstacle, while superconducting incumbents tout higher gate fidelities. Software stack vendors, meanwhile, court developers with Pythonic toolkits and pre-calibrated kernels tuned to medicinal-chemistry Hamiltonians. Intellectual property filings are climbing, with Tencent’s quantum-circuit determination patent illustrating the race to lock in algorithmic optimization pathways.

White-space opportunities exist in compliance modules able to translate quantum output into regulator-ready formats, as well as in hybrid AI-QC frameworks tailor-made for rare-disease modelling where dataset paucity challenges conventional deep learning. Start-ups such as Menten AI, which achieved the first quantum-designed peptide therapeutic, show how focused vertical applications can disrupt niche pockets without competing head-to-head with hyperscalers. Over the next five years, M&A activity is expected to rise as large pharma’s acquire algorithm shops to internalize know-how, progressively consolidating the quantum computing in drug discovery market.

Quantum Computing In Drug Discovery Industry Leaders

IBM Quantum

Google Quantum AI

D-Wave Systems

Rigetti Computing

IonQ

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Fujitsu and RIKEN unveiled a 256-qubit superconducting quantum computer to strengthen hybrid drug-discovery workflows, with a 1,000-qubit roadmap for 2026.

- June 2025: IonQ, AstraZeneca, AWS, and NVIDIA demonstrated quantum-accelerated drug-development pipelines in production test environments.

- March 2025: Fujitsu released open-source quantum-operations software to broaden cloud accessibility.

- June 2024: Microsoft added Generative Chemistry and Accelerated DFT modules to Azure Quantum Elements for high-throughput screening.

Global Quantum Computing In Drug Discovery Market Report Scope

| Cloud-Based Quantum Computing |

| On-Premise Quantum Systems |

| Gate-Model Quantum Processors |

| Quantum Annealers |

| Photonic/Optical Quantum Computers |

| Quantum Simulators/Emulators |

| Target Identification & Validation |

| Hit Generation & Lead Discovery |

| Lead Optimisation |

| Pre-clinical Candidate Selection |

| Oncology |

| Neurology & CNS |

| Infectious Diseases |

| Metabolic & Cardiovascular Diseases |

| Rare & Orphan Diseases |

| Pharmaceutical & Biotech Companies |

| Contract Research Organisations (CROs) |

| Academic & Research Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Deployment Mode | Cloud-Based Quantum Computing | |

| On-Premise Quantum Systems | ||

| By Quantum Processing Approach | Gate-Model Quantum Processors | |

| Quantum Annealers | ||

| Photonic/Optical Quantum Computers | ||

| Quantum Simulators/Emulators | ||

| By Drug Discovery Stage | Target Identification & Validation | |

| Hit Generation & Lead Discovery | ||

| Lead Optimisation | ||

| Pre-clinical Candidate Selection | ||

| By Therapeutic Area | Oncology | |

| Neurology & CNS | ||

| Infectious Diseases | ||

| Metabolic & Cardiovascular Diseases | ||

| Rare & Orphan Diseases | ||

| By End User | Pharmaceutical & Biotech Companies | |

| Contract Research Organisations (CROs) | ||

| Academic & Research Institutes | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the quantum computing in drug discovery market?

The quantum computing in drug discovery market size stands at USD 450.34 million in 2025.

How fast is the quantum computing in drug discovery market expected to grow?

It is projected to register a 12.20% CAGR between 2025 and 2030.

Which deployment mode holds the largest share?

Cloud-based solutions dominate with 68.3% of quantum computing in drug discovery market share in 2024.

What hardware segment is growing the quickest?

Photonic quantum processors are forecast to expand at a 15.7% CAGR through 2030.

Which region is the fastest growing?

Asia-Pacific is advancing at a 17.1% CAGR, outpacing all other geographies due to heavy public funding and growing pharma demand.

What is the main technical barrier today?

Hardware decoherence limits the depth of quantum circuits for complex molecules, restraining near-term full-protein simulations.

Page last updated on: