Cloud-Based Quantum Computing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

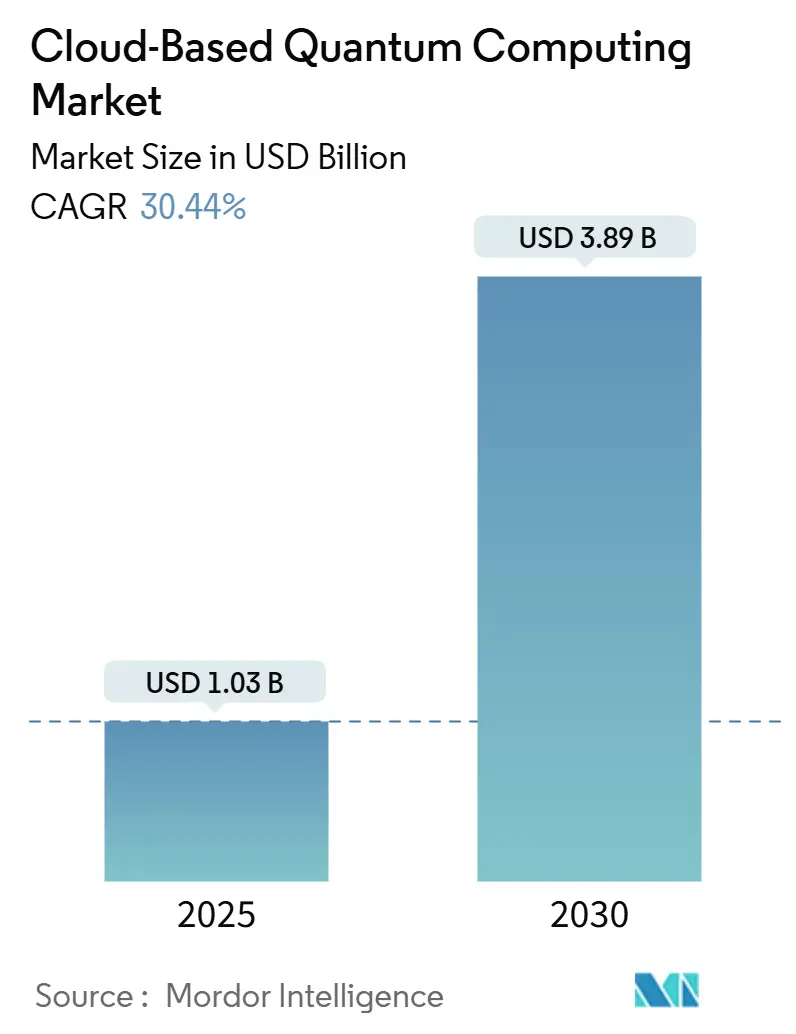

| Market Size (2025) | USD 1.03 Billion |

| Market Size (2030) | USD 3.89 Billion |

| Growth Rate (2025 - 2030) | 30.44% CAGR |

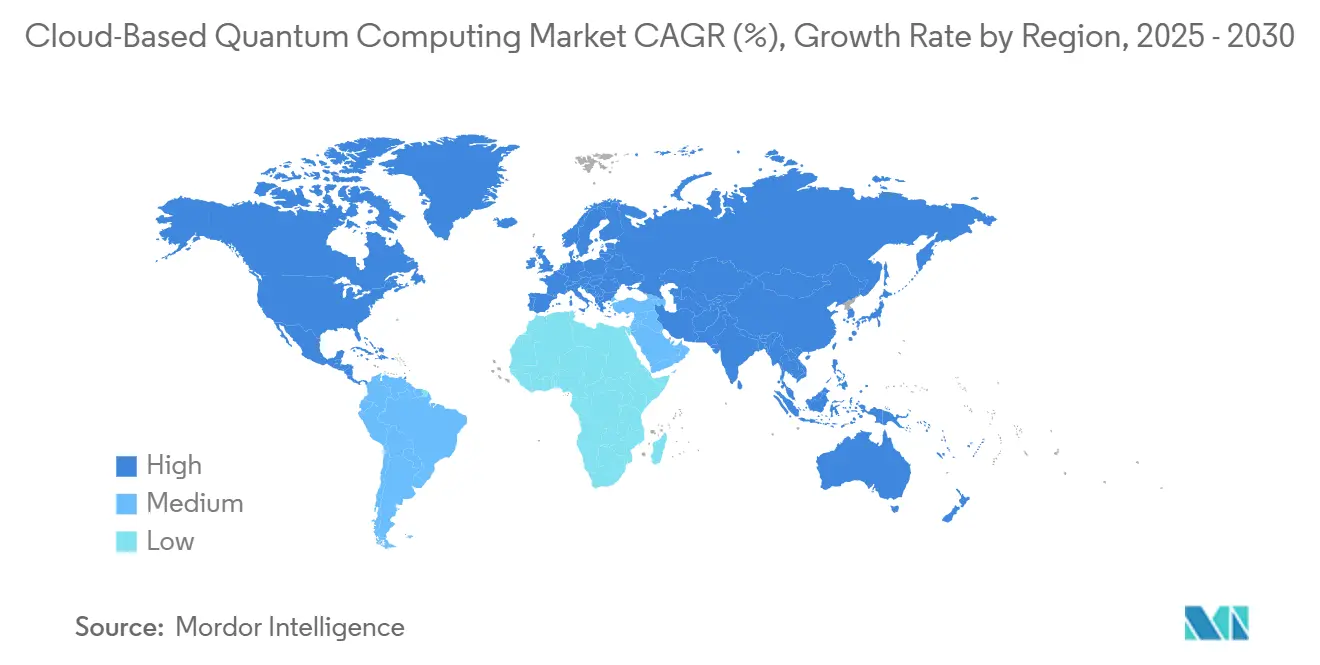

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

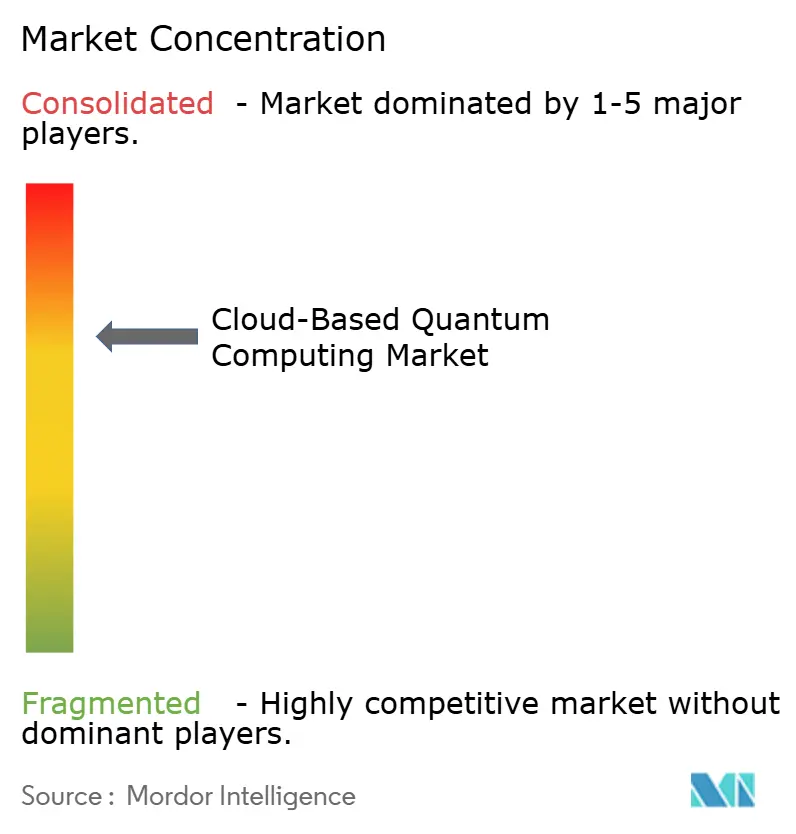

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud-Based Quantum Computing Market Analysis by Mordor Intelligence

The cloud-based quantum computing market size reached USD 1.03 billion in 2025 and is forecast to post a 30.44% CAGR, lifting value to USD 3.89 billion by 2030. Demand accelerates as enterprises tap quantum capacity through hyperscaler platforms instead of financing cryogenic hardware, while government grants such as the United States’ USD 998 million National Quantum Initiative and the European Union’s EUR 1 billion (USD 1.13 billion) Quantum Flagship sustain long-range R&D. Public cloud dominates early adoption thanks to instant accessibility, yet hybrid architectures advance fastest because regulated industries keep sensitive data on-premises while still running quantum jobs remotely. Superconducting systems currently lead deployments, but photonic qubits gain momentum as room-temperature operation promises lower operating costs. Sector use cases expand from portfolio optimization to drug-molecule simulation, and the looming post-quantum cryptography deadline intensifies enterprise experimentation. Competition remains moderate: large cloud vendors integrate multiple hardware partners, raising entry barriers for stand-alone quantum startups while simultaneously widening market reach for niche hardware specialists.

Key Report Takeaways

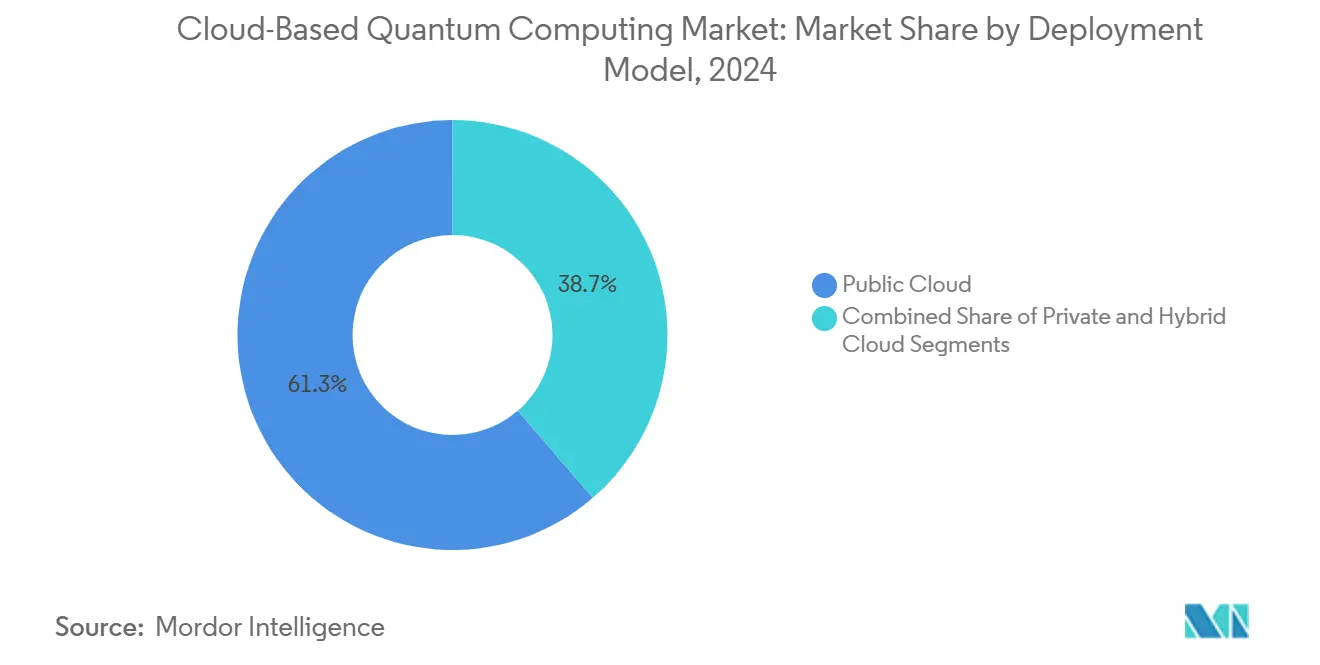

- By deployment model, public cloud held 61.32% of the cloud-based quantum computing market share in 2024, whereas hybrid cloud is projected to expand at a 31.23% CAGR through 2030.

- By technology, superconducting qubits commanded 47.86% share of the cloud-based quantum computing market size in 2024 and photonic qubits are forecast to rise at a 30.68% CAGR to 2030.

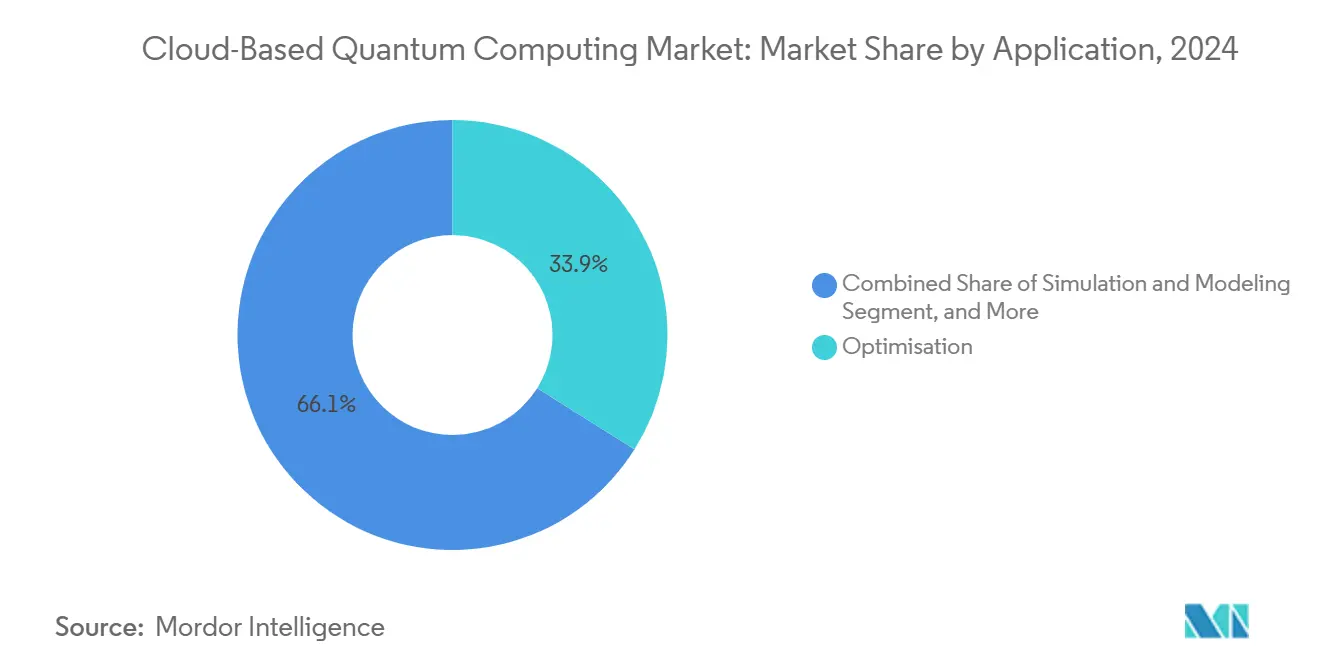

- By application, optimization captured 33.92% of the cloud-based quantum computing market size in 2024; machine learning is advancing at a 30.91% CAGR through 2030.

- By end-user industry, BFSI led with 26.41% revenue share in 2024, while healthcare and life sciences is expected to register the fastest 30.53% CAGR to 2030.

- By geography, North America controlled 39.84% of the cloud-based quantum computing market share in 2024 and Asia-Pacific is set to grow at a 30.74% CAGR over the same horizon.

Global Cloud-Based Quantum Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising enterprise demand for QCaaS for complex optimization problems | +6.2% | Global, with concentration in North America and EU | Medium term (2-4 years) |

| Growing investments by hyperscalers in quantum resources | +4.8% | North America and EU primary, Asia-Pacific secondary | Short term (≤ 2 years) |

| Government funding initiatives for quantum research | +3.1% | US, EU, China leading, spillover to allied nations | Long term (≥ 4 years) |

| Urgency for post-quantum cryptography adoption | +2.7% | Global, regulatory-driven in US and EU first | Medium term (2-4 years) |

| Quantum-enabled AI for real-time fraud detection | +1.9% | BFSI sectors globally, concentrated in financial hubs | Short term (≤ 2 years) |

| Expansion of open-source quantum SDK ecosystems | +1.2% | Global, developer-community driven | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Enterprise Demand for QCaaS Optimization

Organizations now treat access to quantum capacity as a strategic lever rather than a research curiosity. Portfolio managers, logistics operators, and energy traders report order-of-magnitude speed improvements in solving combinatorial problems once reserved for supercomputers. The ability to spin up cloud instances on demand removes the capital burden of dilution refrigerators and vibration-free labs. Early proof points in container routing and derivative pricing validate tangible ROI, pushing board-level mandates to pilot quantum workloads during the planning cycle that begins in 2025. Procurement teams increasingly embed quantum credits inside multiyear cloud contracts, ensuring that usage scales as algorithm libraries mature. [1]Alexander Megrant and Yu Chen, “Scaling up Superconducting Quantum Computers,” Nature Electronics, nature.com

Hyperscaler Infrastructure Investments

Large cloud providers are racing to secure supply of advanced quantum processors and to deepen platform integration. Proprietary chips such as Google’s Willow and IBM’s Heron demonstrate lower logical error rates, supporting longer algorithm depth without catastrophic decoherence. At the same time, multi-vendor gateways in Microsoft Azure Quantum and AWS Braket let enterprises benchmark superconducting, trapped-ion, and photonic hardware inside one console, simplifying procurement review cycles. These moves tighten customer lock-in by coupling quantum credits to broader cloud spend commitments, and they signal that future roadmap differentiation will hinge on uptime SLAs, error-corrected qubit density, and regional availability zones rather than raw qubit counts.

Government Funding Accelerates Research Translation

Public-sector money underwrites high-risk research that private investors deem too remote from commercialization. Grant-supported university consortia produce novel materials, better error-correction codes, and energy-efficient cryogenics that gradually appear in commercial cloud roadmaps three to five years later. Defense agencies explicitly treat quantum advantage as a national-security asset, shaping export-control lists and driving domestic pilot projects for secure communications, traffic routing, and energy-grid optimization. These policies enlarge the innovation funnel, yet they also heighten compliance costs for cross-border cloud customers who must verify that compute jobs do not violate technology-transfer rules.

Urgency for Post-Quantum Cryptography

Standards issued by NIST in 2024 obligate enterprises to migrate away from vulnerable encryption before 2035. CISOs thus confront a dual mandate: test quantum-safe algorithms while also exploring quantum processors to stress-test new keys. Financial regulators warn that custodians must preserve transaction confidentiality for decades, catalyzing early adoption among banks, insurance carriers, and clearinghouses. Cloud providers respond by adding quantum-safe VPN tunnels and secure enclaves to reassure clients that sensitive payloads remain protected even when traversing quantum back-ends. Vendors able to deliver both compute power and compliant security tooling win preferred-supplier status at the RFP stage. [2]Financial Industry Regulatory Authority, “Quantum Computing and the Future of Finance,” finra.org

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High error rates and limited qubit coherence times | -2.3% | Global, affecting all quantum technologies | Medium term (2-4 years) |

| Shortage of skilled quantum talent | -1.8% | Global, acute in developed markets | Long term (≥ 4 years) |

| Data-localisation rules restricting cross-border quantum processing | -1.4% | EU, China, regulated sectors globally | Short term (≤ 2 years) |

| Carbon-footprint concerns of cryogenic quantum data centres | -0.9% | Global, regulatory pressure in EU and California | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Error Rates and Limited Coherence

Most commercial superconducting qubits hold quantum states for only tens of microseconds, forcing algorithms to finish before decoherence dominates. Error-correction schemes like surface codes require thousands of physical qubits per logical qubit, inflating cost and power budgets. Photonic or trapped-ion devices exhibit longer coherence but slower gate speeds or lower integration density, creating trade-offs that limit universal applicability. Consequently, cloud vendors curate narrow algorithm catalogs targeting optimization or simulation tasks that tolerate noisy intermediate-scale quantum constraints. This technical ceiling will restrain broad enterprise deployment until research lifts coherence times into the millisecond range and reduces gate error below 0.1%. [3]Mikko Tuokkola et al., “Near-Millisecond Energy Relaxation in a Superconducting Transmon Qubit,” arxiv.org

Shortage of Skilled Quantum Talent

Industry postings outnumber qualified applicants at a ratio near 3:1. While universities expand graduate programs, the pipeline lags market demand. Scarcity inflates salary offers, favoring large technology firms able to fund premium compensation packages and stock incentives. Startups respond with equity-heavy recruitment or acquisition exits, reducing independent competition. The gap extends beyond physicists to encompass quantum software engineers who can convert domain problems into hardware-friendly circuits, slowing time-to-value for enterprise pilots.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid solutions bridge quantum and classical resources

Hybrid deployments accounted for a 31.23% CAGR from 2025-2030, reflecting the balance enterprises strike between data sovereignty and experimentation flexibility. Public instances still contribute 61.32% of the cloud-based quantum computing market size in 2024, but financial institutions and governments increasingly route sensitive workloads through private gateways that link on-premises data stores to remote quantum hardware. This architecture minimizes regulatory risk while preserving access to the latest qubit generations. Providers now bundle low-latency fiber connections and dedicated VPN endpoints so that batch execution times approach those of native public-cloud jobs. The approach helps customers avoid stranded capital in nascent hardware while still exploiting quantum speed-ups in scheduling, pricing, or supply-chain simulation.

Vendor roadmaps reveal growing investment in regional availability zones designed for sovereign-cloud compliance. Operators install shielded racks adjacent to classical HPC clusters, allowing shared identity management, unified billing, and integrated DevOps tooling. As a result, CIOs view hybrid quantum adoption as a natural extension of existing multi-cloud strategies, and procurement teams structure service-level agreements using the same governance models that cover container orchestration and GPU reservation. This architectural convergence underpins sustained demand for connectivity software and orchestration APIs that schedule circuits across local and remote back-ends without manual intervention.

By Technology: Photonic qubits challenge superconducting dominance

Superconducting qubits held 47.86% of the cloud-based quantum computing market share in 2024, but photonic approaches are set to multiply at a 30.68% CAGR through 2030. Cryogenic vacuum chambers give superconducting processors excellent gate speeds, yet cooling overhead drives high energy consumption and expensive infrastructure. Photonic chips operate near room temperature, reducing total cost of ownership and enabling deployment inside conventional data centers. Investment momentum is evident in strategic funding rounds that exceeded USD 750 million in 2025, accelerating fabrication scale-up and supply-chain localization.

The heterogeneous landscape benefits buyers because each technology aligns with different problem sets. Superconducting architectures favor short-depth variational algorithms, while photonic architectures hold promise for longer algorithm chains that require sustained coherence. Trapped-ion and neutral-atom systems address high-fidelity requirements at smaller qubit counts and serve as proving grounds for advanced error-correction codes. Cloud providers position themselves as neutral marketplaces, offering developers the option to target any supported hardware from a single SDK, thereby absorbing technology-risk on the customer’s behalf.

By Offering: SDK ecosystems spur developer adoption

Quantum software and development kits are expanding at a 31.12% CAGR, underscoring a shift from hardware obsession to problem-centric adoption. Self-service portals present drag-and-drop workflow builders that compile user algorithms into gate sequences optimized for specific back-ends. This abstraction boosts engineering productivity and sidesteps the scarcity of deep quantum expertise. Hardware access still formed 44.67% of 2024 revenue because compute minutes remain the transaction unit, yet the margin structure tilts toward platform subscriptions that bundle priority queue slots, managed simulators, and code libraries.

Consulting and integration services provide crucial bridge capacity for enterprises lacking in-house quantum architects. Engagements typically focus on opportunity identification workshops, algorithm feasibility studies, and proof-of-concept pilots. As in classical cloud history, many professional-services contracts include joint intellectual-property clauses, creating annuity revenue around proprietary quantum workflows.

By Application: Machine learning integration boosts enterprise interest

Optimization retained 33.92% of the cloud-based quantum computing market size in 2024, but machine-learning workloads are on track to surge at 30.91% CAGR thanks to the synergy between quantum kernels and classical neural networks. Quantum feature maps lift model accuracy on small, noisy data sets by embedding complex correlations into Hilbert space with fewer parameters. Fraud-detection pilots inside card-payment networks already report double-digit precision gains while cutting inference latency, sparking follow-on projects in anomaly detection for manufacturing quality control and network-security threat hunting.

Simulation and material-discovery users capitalize on quantum chemistry solvers that replicate electron interactions without invoking heavy classical approximations, cutting lead times in catalyst formulation and battery design. Cryptography workloads exploit quantum back-ends to benchmark post-quantum algorithms under realistic threat models, supporting compliance reports required by financial regulators. Demand diversity stabilizes revenue across economic cycles because each vertical tends to prioritize a different workload family, buffering providers against dependency on any single killer app.

By End-User Industry: Healthcare leads the growth curve

BFSI kept 26.41% revenue share during 2024, anchored by use cases in risk optimization, asset-liability management, and real-time fraud screening. Healthcare and life sciences, however, stand as the fastest riser with projected 30.53% CAGR, propelled by quantum-enabled molecular modeling that slashes early-stage screening costs in drug pipelines. Quantum imaging sensors under development promise higher spatial resolution at lower radiation doses, opening new revenue around diagnostic equipment as well.

Aerospace and defense agencies pilot quantum route planning to minimize fuel burn, while automotive manufacturers feed quantum computers with battery-chemistry data to stretch electric-vehicle range. Energy utilities deploy quantum algorithms for grid stability under high renewable penetration, and chemicals producers simulate polymer properties to accelerate formulation cycles. Government bodies treat quantum services as force multipliers for public-sector priorities such as traffic decongestion and climate modeling, allocating dedicated budget lines within digital-transformation plans.

Geography Analysis

North America generated 39.84% of 2024 revenue as hyperscaler headquarters and strong federal funding create a dense cluster of research talent, venture capital, and early adopters. Federal grants totaling USD 998 million in fiscal 2025 sustain university labs that feed intellectual property into commercial roadmaps, while Canadian pioneers supply complementary annealing services. Multinational corporations headquartered in the United States treat domestic cloud regions as the default venue for quantum pilots, reinforcing volume leadership and justifying continuous capacity expansion.

Asia-Pacific is projected to clock a 30.74% CAGR through 2030, driven by sovereign quantum programs in China, India, Japan, South Korea, and Australia. India’s National Mission on Quantum Technology aims to lift national spending to USD 7 billion by 2032, spurring joint ventures that co-locate cloud nodes near pharma hubs in Bengaluru and Hyderabad. Chinese cloud conglomerates embed in-house quantum teams to sidestep export-control exposure, while Japanese industrial groups bundle quantum compute slots with semiconductor manufacturing alliances. The region’s growth profile benefits from a young developer base eager to upskill on open-source SDKs.

Europe pursues strategic autonomy through the EUR 1 billion Quantum Flagship and rigorous privacy frameworks such as GDPR. Providers respond with region-locked quantum zones and sovereign-cloud options that keep telemetry inside EU borders. Germany, the United Kingdom, and France anchor the ecosystem with national testbeds and consortium projects in mobility and materials science. At the same time, tighter export licensing from the United States complicates transatlantic supply chains, prompting European hardware startups to seek domestic fabrication capacity for cryogenic components.

Competitive Landscape

The market exhibits moderate concentration: the top five vendors collectively command slightly under 70% of 2024 revenue, assigning a market concentration score of 7. IBM leads the patent race and offers tiered cloud subscriptions that bundle quantum compute with classical accelerators. Google extends its Tensor Processing Unit ecosystem by offloading quantum-classical hybrid workloads to dedicated co-processors. Microsoft leverages Azure’s footprint to pre-install SDKs inside visual-studio templates, while Amazon unifies procurement under existing cloud-spend commitments. Partnerships remain the dominant go-to-market route for hardware specialists such as IonQ, Rigetti, and Quantinuum, who gain enterprise reach without duplicating salesforce overhead.

Strategic moves highlight differentiation around error-corrected qubit delivery, regional datacenter presence, and low-latency interconnect. Recent acquisitions skew toward quantum networking and cryptography start-ups, signaling that security add-ons may become table stakes. The next battleground lies in workload orchestration software that automatically routes jobs to the lowest-cost, highest-fidelity back-end in real time.

Cloud-Based Quantum Computing Industry Leaders

International Business Machines Corporation

Alphabet Inc.

Microsoft Corporation

Amazon Web Services, Inc.

D-Wave Quantum Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Google reported Willow chip achievements that pushed logical error rates below physical error rates, a crucial threshold for scalable fault-tolerant systems.

- January 2025: NVIDIA committed USD 750 million to PsiQuantum to accelerate photonic hardware production lines.

- December 2024: IonQ closed the USD 250 million purchase of ID Quantique, adding quantum key distribution capability to its cloud portfolio.

- November 2024: IBM deployed Heron processors with coherence times near 500 microseconds, expanding circuit depth potential.

Global Cloud-Based Quantum Computing Market Report Scope

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Superconducting Qubits |

| Trapped-Ion Qubits |

| Photonic Qubits |

| Quantum Annealing |

| Topological Qubits |

| Hardware Access (Quantum Processors-as-a-Service) |

| Software / SDK and APIs |

| Quantum Consulting and Integration Services |

| Optimisation |

| Simulation and Modelling |

| Machine Learning / AI |

| Cryptography and Security |

| Material Discovery |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Aerospace and Defence |

| Automotive and Transportation |

| Energy and Utilities |

| Chemicals and Materials |

| Government and Public Sector |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Deployment Model | Public Cloud | ||

| Private Cloud | |||

| Hybrid Cloud | |||

| By Technology | Superconducting Qubits | ||

| Trapped-Ion Qubits | |||

| Photonic Qubits | |||

| Quantum Annealing | |||

| Topological Qubits | |||

| By Offering | Hardware Access (Quantum Processors-as-a-Service) | ||

| Software / SDK and APIs | |||

| Quantum Consulting and Integration Services | |||

| By Application | Optimisation | ||

| Simulation and Modelling | |||

| Machine Learning / AI | |||

| Cryptography and Security | |||

| Material Discovery | |||

| By End-User Industry | Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | |||

| Aerospace and Defence | |||

| Automotive and Transportation | |||

| Energy and Utilities | |||

| Chemicals and Materials | |||

| Government and Public Sector | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the cloud-based quantum computing market in 2025?

The cloud-based quantum computing market size is USD 1.03 billion in 2025 and is set to grow to USD 3.89 billion by 2030.

Which deployment model is expanding fastest in quantum cloud computing?

Hybrid cloud is forecast at a 31.23% CAGR because it lets firms combine on-premises data control with public-cloud quantum processors.

What drives enterprise interest in quantum computing right now?

Urgency to optimize complex problems, impending post-quantum cryptography deadlines, and hyperscaler investments that simplify access are the primary catalysts.

Which region is projected to grow quickest for quantum cloud adoption?

Asia-Pacific leads with a projected 30.74% CAGR through 2030, bolstered by government programs in China, India, Japan, and South Korea.

What is the main technical hurdle limiting broader quantum use?

High gate error rates and short qubit coherence times restrict circuit depth, delaying fully fault-tolerant applications.

How concentrated is the competitive landscape?

The top five providers hold just under 70% of revenue, producing a moderate concentration score of 7 that still allows room for niche innovators.

Page last updated on: