Encryption Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

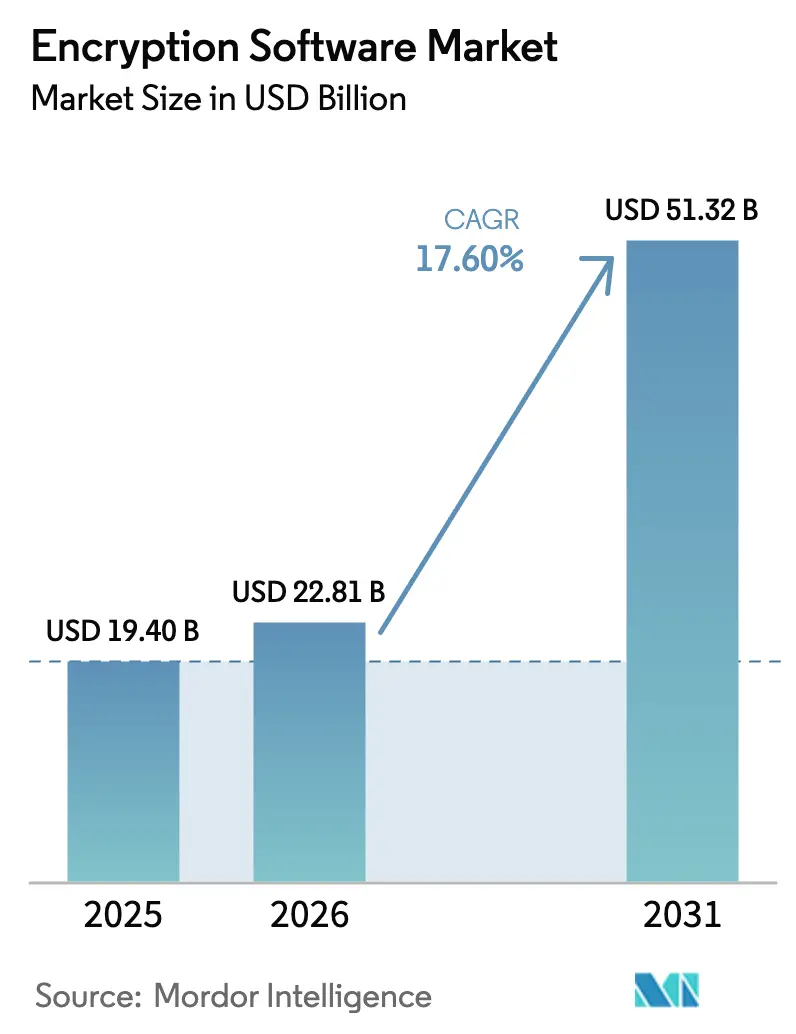

| Market Size (2026) | USD 22.81 Billion |

| Market Size (2031) | USD 51.32 Billion |

| Growth Rate (2026 - 2031) | 17.60% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Encryption Software Market Analysis by Mordor Intelligence

The encryption software market size was valued at USD 19.4 billion in 2025 and estimated to grow from USD 22.81 billion in 2026 to reach USD 51.32 billion by 2031, at a CAGR of 17.6% during the forecast period (2026-2031). Rapid adoption follows the August 2024 release of the first three NIST post-quantum cryptography (PQC) standards and a 2035 federal deadline for PQC implementation, which together de-risk procurement decisions and unlock budget allocations.[1]National Institute of Standards and Technology, “FIPS 203, 204, 205: First Post-Quantum Cryptography Standards,” nist.gov Enterprises are embedding encryption across zero-trust frameworks mandated by U.S. Executive Order 14028, while the permanent hybrid workforce pushes cloud-native deployment models and distributed key management. Competition is intensifying as incumbent security vendors race against quantum-cryptography start-ups, with acquisitions filling capability gaps and platform integration emerging as a key differentiator. APAC’s surge, healthcare’s regulatory urgency, and a pivot from perimeter to data-centric protection all reinforce sustained expansion opportunities across the encryption software market.

Key Report Takeaways

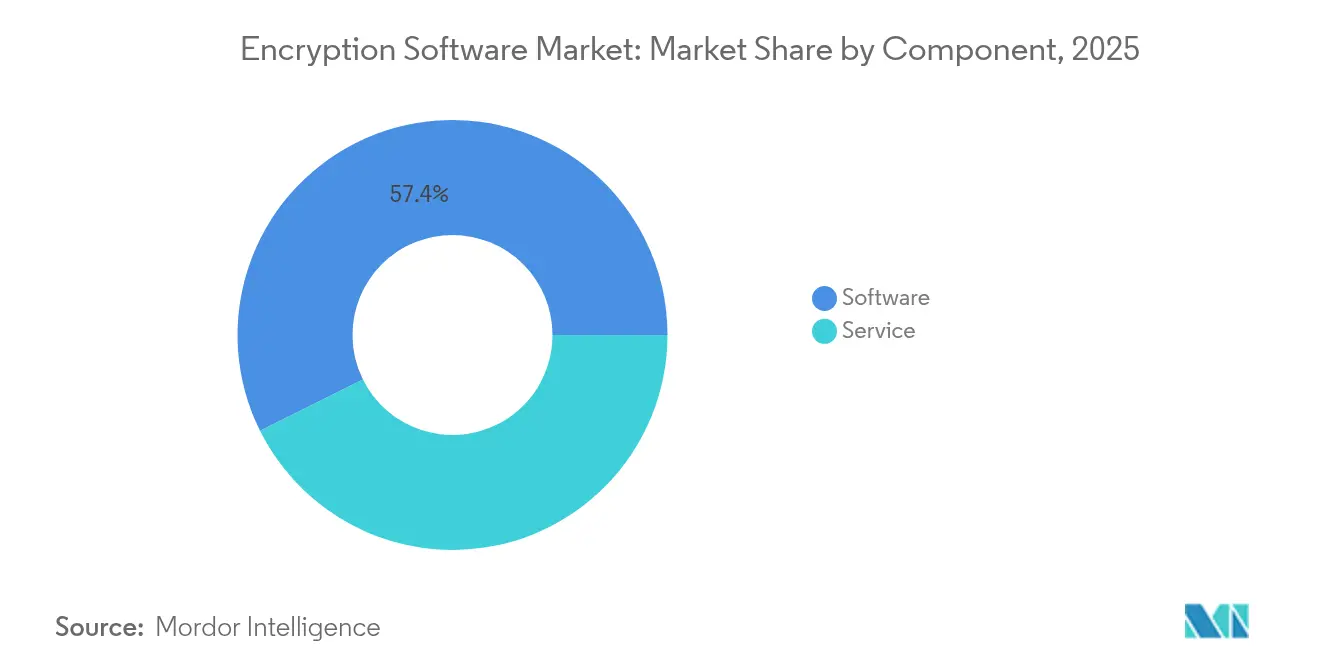

- By component, software maintained 57.35% of encryption software market share in 2025, while services are projected to grow fastest at 20.6% CAGR to 2031.

- By deployment model, on-premise held 61.28% of the encryption software market size in 2025; cloud deployment is forecast to expand at a 24.07% CAGR through 2031.

- By function, disk encryption accounted for 32.85% of encryption software market size in 2025; cloud encryption is advancing at a 26.85% CAGR.

- By vertical, BFSI led with 29.40% revenue share in 2025, while healthcare is poised to rise at a 20.55% CAGR.

- By geography, North America captured 42.60% of encryption software market share in 2025; APAC is set to climb at a 19.78% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Encryption Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent data-protection regulations | +4.2% | Global; EU & US lead | Medium term (2-4 years) |

| Rising cyber-attacks on cloud workloads | +3.8% | North America & APAC | Short term (≤ 2 years) |

| Remote & hybrid workforce needs | +3.1% | North America, EU | Medium term (2-4 years) |

| Homomorphic encryption uptake | +2.4% | North America, EU | Long term (≥ 4 years) |

| Quantum-resistant pilots | +2.1% | US & allies | Long term (≥ 4 years) |

| Hardware root-of-trust for IoT | +1.6% | APAC hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Data-Protection Regulations

Global watchdogs now require proactive encryption mandates that embed security into digital infrastructure rather than treat it as a check-box exercise. The U.K. Information Commissioner’s Office updated guidance in May 2025, mandating algorithm-strength oversight that directly steers procurement choices. In the United States, Cybersecurity Maturity Model Certification 2.0 compels contractors to encrypt Controlled Unclassified Information in transit and at rest, widening the addressable encryption software market among federal suppliers.[2]Cybersecurity and Infrastructure Security Agency, “Software Acquisition Guide for Government Enterprise Consumers,” cisa.gov The Department of Justice’s Civil Cyber-Fraud Initiative raises financial penalties for non-compliance, turning encryption into a material risk-management imperative. Financial institutions supervising USD 23 trillion in assets face overlapping GLBA, SOX, and PCI-DSS mandates, each specifying encryption requirements, reinforcing multi-layered adoption across front-, middle-, and back-office systems. Together, these statutes contribute a 4.2% uplift to the forecast CAGR.

Rising Volume & Sophistication of Cyber-Attacks on Cloud Workloads

Attacks have shifted from opportunistic data theft to systematic “harvest-now-decrypt-later” campaigns that bank encrypted datasets for future quantum decryption. Canada’s National Cyber Threat Assessment 2025-2026 flags state-sponsored actors escalating AI-assisted campaigns targeting critical infrastructure.[4]Canadian Centre for Cyber Security, “National Cyber Threat Assessment 2025-2026,” cyber.gc.ca Enterprises answer with defense-in-depth strategies layering multiple encryption protocols and unified key hierarchies. Cloud encryption’s 27.6% CAGR reflects the urgency to protect multi-tenant workloads as ransomware evolves into double and triple-extortion assaults. Consequently, encryption becomes the final shield once perimeter defenses fall, fuelling integrated solution demand across hybrid environments.

Remote & Hybrid Workforce Fueling Endpoint-Level Encryption Demand

Distributed work dissolves fixed perimeters, forcing encryption onto every endpoint. SMEs, in particular, cite security and privacy concerns among chief cloud adoption hurdles, prompting demand for user-friendly encryption tools. Bring-your-own-device culture expands the diversity of endpoints, requiring encryption solutions that operate agnostic of ownership or network context. Zero-trust policies treat each device as potentially compromised, making endpoint-level encryption non-negotiable. Healthcare provides a prominent example: 92% of providers now use TLS for data flows and 87% have multi-factor authentication in place to secure remote electronic health records iaeme. The trend drives steady advance in unified data-at-rest and data-in-motion protection.

Homomorphic Encryption Adoption in Privacy-Preserving Analytics

Homomorphic encryption moves from academic theory to enterprise pilots, allowing analytics on encrypted data without exposing the plaintext. Banks apply the technology to fraud-detection algorithms that span multiple institutions, preserving client confidentiality while improving risk models. Healthcare research groups carry out federated genomic studies across hospitals without leaking patient data. Performance barriers shrink thanks to hardware acceleration and algorithmic refinements, making real-time encrypted computation feasible for advertising-tech analytics within evolving privacy laws. Cloud providers now position homomorphic encryption as a managed service, lowering entry hurdles for firms lacking deep cryptographic talent.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High TCO of full-disk encryption at scale | −2.8% | Global; SMEs hardest hit | Short term (≤ 2 years) |

| Proliferation of open-source & pirated tools | −1.9% | APAC & emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High TCO of Full-Disk Encryption at Enterprise Scale

Total cost of ownership encompasses not just licensing but hardware upgrades, performance overhead, and specialist staffing. Post-quantum algorithms can impose 10-30% processing overhead, forcing infrastructure refresh cycles. Key management introduces further capital outlays for hardware security modules and segregated networks. Annual enterprise key-management budgets can range from USD 500,000 to USD 2 million, outstripping software fees. In latency-sensitive environments such as high-frequency trading, even microsecond delays translate into lost revenue, compelling expensive hardware acceleration. SMEs with limited budgets therefore delay or scale down broad encryption roll-outs, shaving 2.8% from the CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Surge Amid Quantum Transition

Services currently trail software yet register the steepest ascent as enterprises confront the 2035 PQC compliance horizon. The encryption software market size attributed to services will climb on a 20.6% CAGR, driven by demand for cryptographic asset inventories, algorithm migration roadmaps, and managed key-lifecycle oversight. Federal agencies earmark an estimated USD 7 billion for PQC transition services—an indicator of the consulting windfall in play. Software still secures recurrent revenue through subscriptions, but rising complexity favors turnkey managed offerings, especially within healthcare and finance where certified expertise and continuous compliance are mandatory.

At the same time, software vendors embed automated migration tooling, prompting vendors to bundle advisory services for differentiated value. This dual revenue track—license plus services—strengthens vendor lock-in, particularly where platform integration minimises operational friction. Over 60% of new deals scoped in 2025 combine software licenses with professional-service packages that cover discovery, remediation, and PQC-ready architecture validation. Consequently, partnerships between software publishers and global systems integrators are proliferating, helping both sides monetise the quantum shift inside the encryption software market.

By Deployment Model: Cloud Encryption Accelerates

Despite on-premise deployments commanding 61.28% of encryption software market size in 2025, cloud encryption climbs fastest at a 24.07% CAGR on the back of hybrid architectures and federal cloud-first mandates. Government agencies implementing zero-trust frameworks require scalable key management that spans public-, private-, and multi-cloud estates gsa. Small and mid-sized enterprises favour cloud subscriptions to sidestep capital outlays and access enterprise-grade security on demand, aligning with operational efficiency gains noted in 82% of SME studies businesses.

On-premise solutions retain appeal where data sovereignty or ultra-low latency demands prevail, such as regulated banking workloads and high-frequency trading platforms. Yet cloud providers now offer Hardware Security Module-as-a-Service and confidential-computing enclaves, eroding legacy objections to off-premise key custody. Cloud-native encryption enables rapid policy propagation across containers and serverless functions otherwise hard to cover with traditional disk encryption. As a result, the encryption software market witnesses a secular tilt towards flexible SaaS models while hybrid adoption ensures on-premise tools remain relevant, albeit at a slower growth pace.

By Enterprise Size: SMEs Embrace Cloud-First Encryption

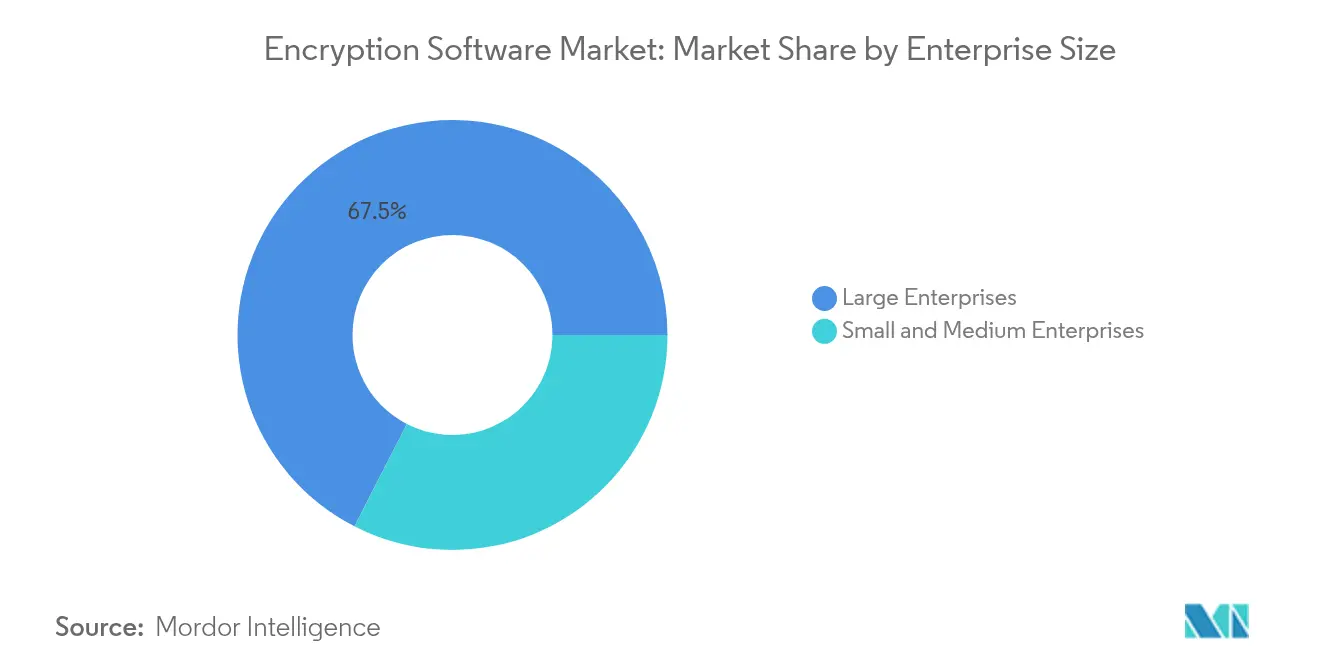

Large enterprises hold 67.46% revenue share, reflecting complex multi-layer deployments and deep compliance obligations. Still, SMEs are the fastest-expanding cohort at 22.5% CAGR, empowered by user-friendly cloud services that abstract cryptographic complexity. Surveyed SMEs highlight phishing, ransomware, and insider abuse as top threats, with encryption cited among preferred safeguards to fulfil customer trust commitments jis.

However, cost and skills gaps persist. Providers therefore package encryption with managed detection and response, automating key rotation and audit reporting. Vendors targeting the SME channel emphasise rapid onboarding, subscription pricing, and compliance templates aligned to PCI-DSS and HIPAA. Meanwhile, large enterprises drive custom integration projects that stitch encryption into legacy ERP and data-warehouse environments, leveraging vendor professional services at scale. The two-speed demand underscores why portfolio breadth—from entry-level SaaS to bespoke on-premise modules—remains pivotal for capturing share across the encryption software market.

By Function: Cloud Encryption Leads Innovation

Disk encryption continues to top revenue at 32.85%, yet its share will erode as organisations pivot to the cloud. Cloud-specific encryption is forecast to outstrip every other function at a 26.85% CAGR, buoyed by containerised workloads and the need for granular, data-centric protection. Communication encryption supports remote work, while database encryption advances steadily under zero-trust mandates. Vendors increasingly bundle multi-function capabilities under a unified management plane, curbing console sprawl and easing compliance audits.

Emerging homomorphic encryption and secure multi-party computation modules extend functional scope, letting users process encrypted datasets without decrypting them. Demand is strongest in regulated analytics—fraud scoring, collaborative healthcare research—where data sensitivity precludes plaintext sharing. Consequently, R&D pipelines concentrate on performance optimisation to make advanced encryption practical for latency-intensive use cases, cementing function-level diversification as a growth catalyst within the encryption software market.

By Industry Vertical: Healthcare Drives Regulatory Compliance

BFSI retains the largest wallet share, but healthcare records the highest trajectory at 20.55% CAGR. HIPAA revisions and telehealth expansion require end-to-end protection of electronic health information, boosting TLS adoption to 92% and MFA usage to 87% within provider networks. Hospitals also gravitate toward homomorphic encryption for multi-institutional research in genomics and drug discovery, safeguarding patient privacy while enabling large-scale analytics.

Government adoption rises alongside PQC mandates, while IT-telecom sectors pioneer edge-to-cloud encryption for 5G rollout. Retail and education display steady uptake as e-commerce and digital-learning channels widen attack surfaces. Vertical demand therefore aligns to the regulatory burden and digital-transformation velocity, not the fundamental need for confidentiality, underscoring a broadening opportunity pool for vendors across the encryption software market.

Geography Analysis

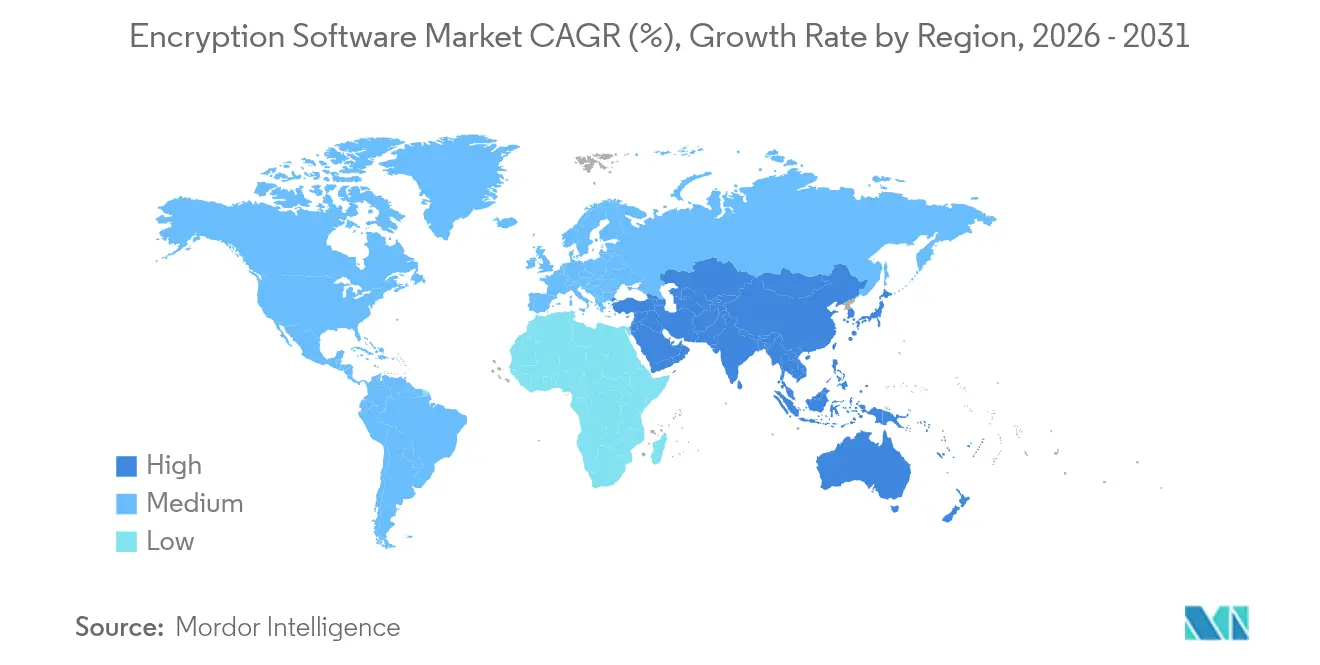

North America leads at 42.60% market share, fortified by early zero-trust adoption and a robust vendor ecosystem. The region benefits from the National Quantum Strategy, which allocates CAD 360 million (USD 267 million) to post-quantum cryptography R&D and aims to deliver a secure quantum communication network. State legislatures are equally active, with 75 cybersecurity bills enacted in 2024 alone, driving encryption procurement within the public sector.

APAC, climbing at 19.78% CAGR, reflects rapid digitisation in manufacturing, finance, and healthcare plus accelerating regulatory frameworks in Japan, South Korea, and Singapore. The region’s semiconductor dominance advances hardware-root-of-trust shipments yet also reveals supply-chain fragility, spurring interest in software-only encryption that mitigates component shortages. Europe grows at a steady clip under GDPR compliance and new U.K. guidance that stresses algorithm-strength governance, reinforcing encryption’s role in digital sovereignty. Collectively, these trends map a geographic landscape where leadership in policy, supply chains, and cloud adoption determines regional momentum within the encryption software market.

Europe’s trajectory aligns to data localization and privacy priorities. Renewed focus on homomorphic encryption facilitates cross-border analytics without breaching GDPR. Member states coordinate quantum-safe pilot projects to protect critical infrastructure, driving procurement of PQC-enabled email gateways and VPNs. Brexit imposes data-transfer complexity, making encryption essential for U.K.–EU commerce. Fragmented national regulations create opportunity for vendors offering policy-aware key management capable of adapting to differing retention and disclosure rules.

Competitive Landscape

Encryption remains a moderately fragmented field where established giants and nimble specialists collide. IBM, Microsoft, and Broadcom leverage existing customer footprints and broad security suites, cross-selling encryption modules bolstered by cloud, identity, and analytics offerings. Quantum-specialist start-ups such as Arqit advance differentiated intellectual property on symmetric key-agreement protocols, drawing interest from defense and telco clients. Patent filings around hybrid PQC algorithms and quantum-secure communication channels underscore mounting barriers to entry.

Acquisition momentum reflects strategic gaps: Arqit’s May 2025 purchase of Ampliphae’s encryption-visibility technology augments its quantum-safe portfolio. NetSfere launched the first enterprise-ready ML-KEM 1024 communication platform, targeting regulated industries with immediate PQC compatibility. Vendors now compete on platform integration—unified key orchestration across SaaS, IaaS, and on-premise assets—rather than isolated point solutions. Industry-specific templates for HIPAA, PCI-DSS, and CJIS bolster value propositions, especially among SMEs seeking turnkey compliance. Artificial-intelligence-driven policy automation further differentiates offerings by cutting operational overhead and addressing the high TCO restraint shadowing the encryption software market.

Consolidation is expected as cash-rich incumbents acquire algorithm innovators to fast-track PQC portfolios. Meanwhile, open-source communities pressure pricing on commoditized components, encouraging premium vendors to double down on managed services and regulatory expertise. Success hinges on the ability to deliver end-to-end encryption lifecycle management—from discovery and inventory through migration and continuous audit—across heterogeneous customer estates.

Encryption Software Industry Leaders

IBM

Microsoft

Broadcom Inc.

Sophos Ltd.

Thales

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Arqit Quantum Inc. acquired Ampliphae’s technology IP to integrate encryption-visibility tools into its quantum-safe platform

- April 2025: Arqit Quantum Inc. launched a confidential-computing-enhanced quantum-safe encryption service built on Intel Trust Domain Extensions, adding rapid key rotation and data-sovereignty controls

- March 2025: NetSfere debuted an enterprise-ready quantum-proof communication platform using ML-KEM 1024 encryption

- March 2025: The Government of Canada allocated CAD 360 million (USD 267 million) to quantum-communication and PQC initiatives under the National Quantum Strategy

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the encryption software market as the total license, subscription, and embedded cloud-service revenues earned from products that apply symmetric, asymmetric, or emerging post-quantum ciphers to secure data at rest, in transit, and in use across endpoints, servers, networks, and public clouds. According to Mordor Intelligence, coverage spans packaged software, native SaaS tools, and key-management add-ons sold to commercial and public-sector end users worldwide.

Scope Exclusion: Stand-alone hardware modules, consultancy-only engagements, and managed security service fees sit outside this boundary.

Segmentation Overview

- By Component

- Software

- Service

- By Deployment Model

- On-premise

- Cloud

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By Function

- Disk Encryption

- Communication Encryption

- File/Folder Encryption

- Cloud Encryption

- Database Encryption

- By Industry Vertical

- IT and Telecommunication

- BFSI

- Healthcare

- Government

- Retail

- Education

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interview cybersecurity architects at banks, cloud providers, healthcare systems, and technology OEMs across North America, Europe, and Asia-Pacific. Short surveys with CIOs and procurement heads validate penetration rates, post-quantum upgrade timelines, and typical subscription price bands, giving us live feedback to refine desk-derived assumptions.

Desk Research

We begin with structured reviews of publicly available datasets such as US NIST FIPS-140 validation lists, Eurostat ICT security surveys, and UN Comtrade exports of cryptographic software, which anchor supply, trade, and adoption trends. Regulations compiled by ENISA, the PCI Security Standards Council, and HIPAA portals help size compliance-driven demand, while annual filings and investor decks reveal vendor revenue splits. D&B Hoovers and Dow Jones Factiva provide additional firm-level context. These illustrations are indicative; many further sources inform our desk work.

A second sweep captures patent momentum via Questel, breach statistics from Verizon DBIR, and regional pricing snapshots pulled from procurement portals, ensuring the desk foundation reflects both innovation and commercial reality.

Market-Sizing & Forecasting

A top-down construct converts country-level IT spend and data-center capacity into an addressable encryption pool, which is then filtered by observed penetration and unit ASPs. Results are cross-checked through selective bottom-up roll-ups of leading vendor revenues and sampled contract values. Key variables include encrypted workload share, cloud migration intensity, regulated record volumes, enterprise key-management deployments, and average price erosion. Forecasts employ multivariate regression blended with scenario analysis that flexes regulation timing and quantum-safe adoption curves, and gap areas in bottom-up inputs are bridged using region-specific price-volume proxies.

Data Validation & Update Cycle

Analysts run variance checks against independent breach incident counts and vendor filings, escalate anomalies for peer review, and adjust before sign-off. The model refreshes annually, with mid-cycle updates triggered by material regulatory or technology inflections, ensuring clients always receive the latest vetted view.

Why Mordor's Encryption Software Baseline Commands Reliability

Published estimates often diverge because firms start from dissimilar scopes, pricing logic, and refresh rhythms. Our disciplined selection of variables, live respondent feedback, and yearly recalibration minimizes those gaps.

Key gap drivers include whether services are counted, how post-quantum spending is treated, and the currency year applied for historic conversions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 19.40 bn (2025) | Mordor Intelligence | - |

| USD 13.50 bn (2024) | Global Consultancy A | Focuses on core data-center software only; omits post-quantum upgrades |

| USD 15.57 bn (2023) | Industry Research B | Excludes service revenue and uses older currency baselines |

The comparison shows that, by aligning scope with real purchase behaviors and validating every assumption with end users, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can rely on with confidence.

Key Questions Answered in the Report

What is the encryption software market worth today and how fast is it growing?

The market stands at USD 22.81 billion in 2026 and is forecast to reach USD 51.32 billion by 2031, posting a 17.6% CAGR.

Which deployment model is expanding most quickly?

Cloud-based encryption leads with a 24.07% CAGR through 2031 as organizations migrate workloads to hybrid and multi-cloud environments.

Why is healthcare showing the highest vertical growth?

Updated HIPAA rules, rapid digitization, and the need to secure telehealth data are propelling healthcare encryption at a 20.55% CAGR.

How do U.S. federal mandates influence adoption rates?

Executive Orders 14028 and 14144, plus a 2035 deadline for post-quantum cryptography, require end-to-end encryption across federal systems and their supplier networks, accelerating market demand.

Which region will grow fastest over the next five years?

Asia-Pacific is projected to expand at a 19.78% CAGR, driven by rapid digital transformation and tightening data-protection regulations across major economies.

Page last updated on: