Network Encryption Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

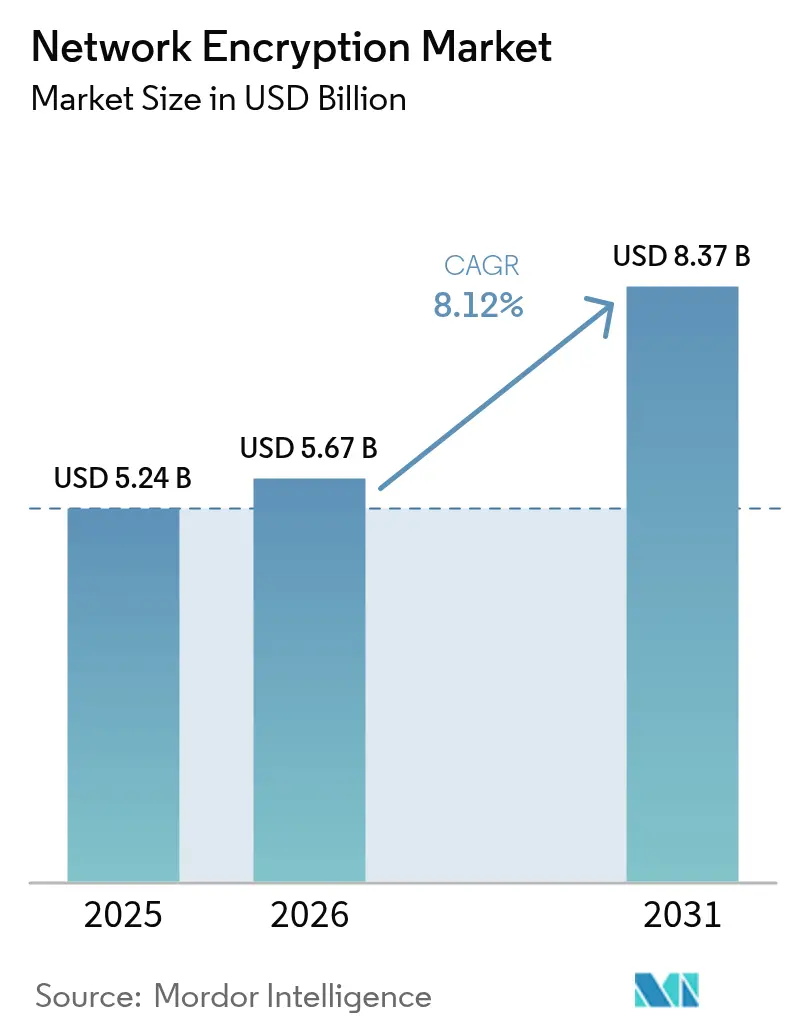

| Market Size (2026) | USD 5.67 Billion |

| Market Size (2031) | USD 8.37 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Network Encryption Market Analysis by Mordor Intelligence

The network encryption market size is expected to grow from USD 5.24 billion in 2025 to USD 5.67 billion in 2026 and is forecast to reach USD 8.37 billion by 2031 at 8.12% CAGR over 2026-2031. Escalating quantum computing threats, the migration to zero-trust architectures, and tightening regulatory mandates converge to sustain a robust demand trajectory for advanced cryptographic controls. Enterprises race to deploy quantum-resistant algorithms ahead of commercially viable quantum computers, while 5G rollouts and cloud adoption create large volumes of traffic that must be encrypted at line rate. Hardware-accelerated solutions remain critical for ultra-low-latency use cases; however, the rapid rise of software-defined and managed encryption platforms signals a long-term shift toward flexible consumption models. Vendor differentiation increasingly hinges on seamless integration with identity platforms, automated key management, and support for the first wave of post-quantum standards.

Key Report Takeaways

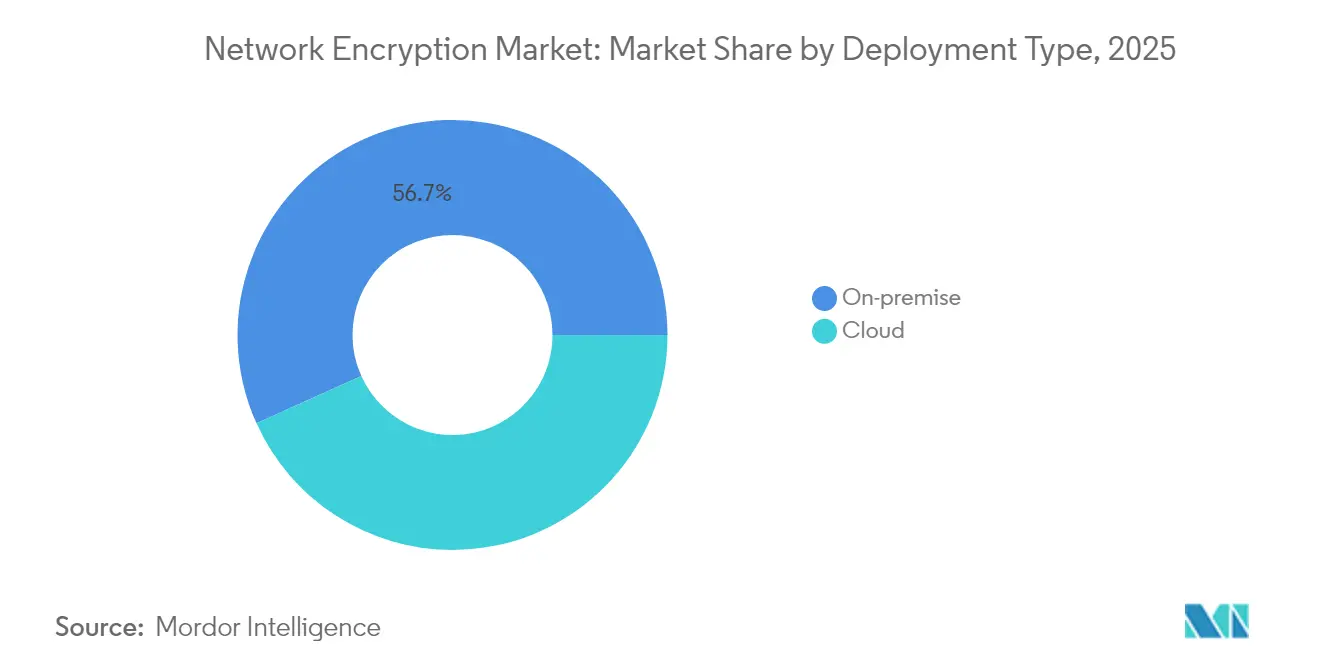

- By deployment type, on-premise solutions held 56.74% of the network encryption market share in 2025, whereas cloud implementations are expected to expand at a 9.87% CAGR through 2031.

- By component, hardware accounted for 49.01% of the network encryption market size in 2025, while solutions and services registered the fastest growth, at a 10.05% CAGR, from 2026 to 2031.

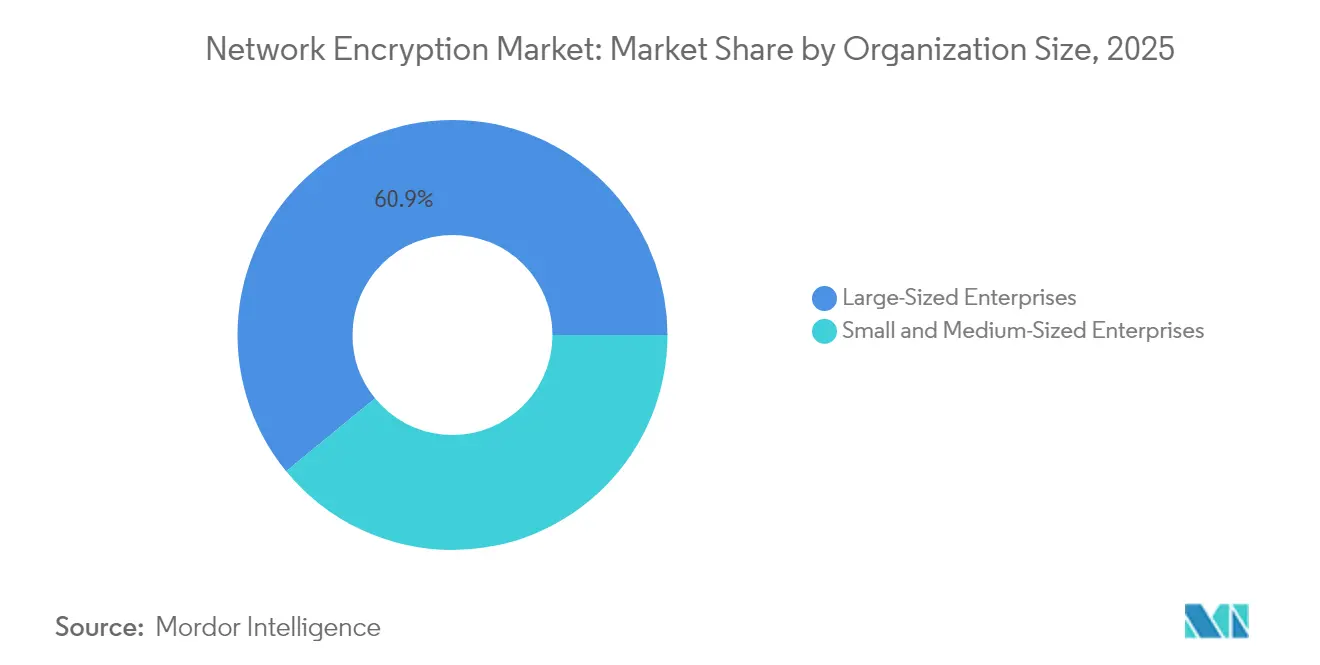

- By organization size, large enterprises commanded a 60.92% revenue share in 2025; however, the SME segment is forecasted to advance at a 9.94% CAGR.

- By end-user industry, BFSI led with a 27.35% share in 2025, while healthcare is projected to grow at an 8.49% CAGR through 2031.

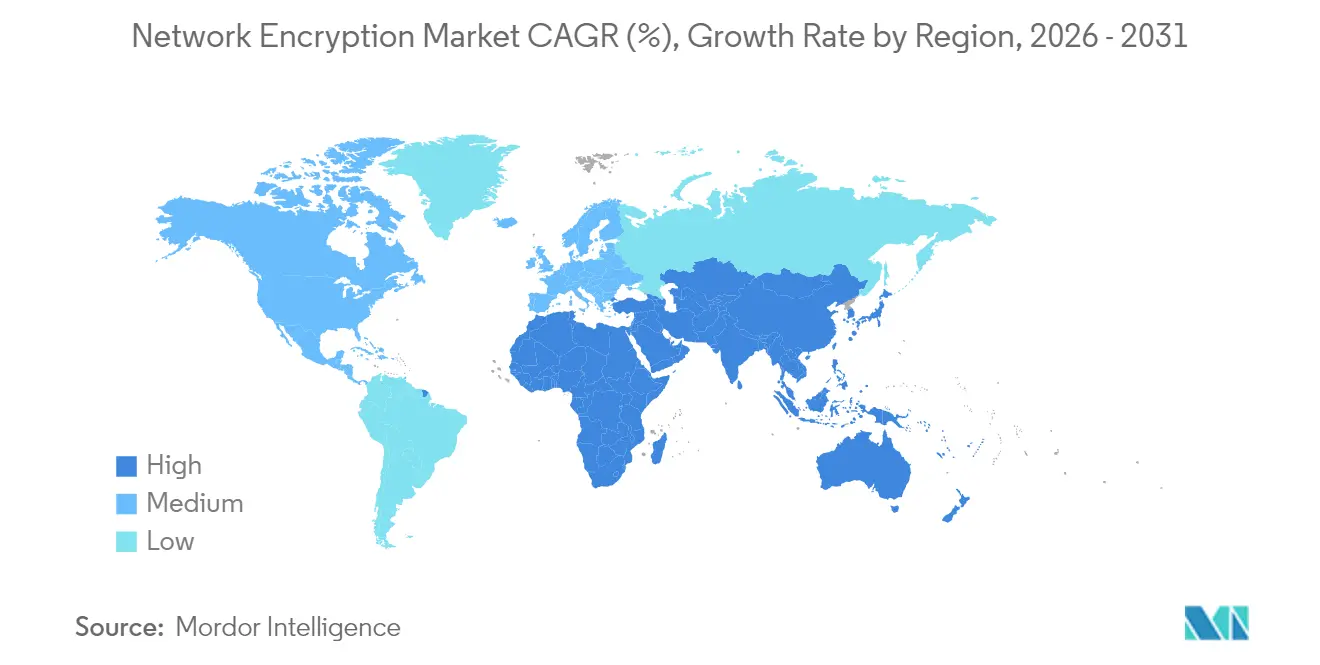

- By geography, North America retained a 33.45% share in 2025, whereas the Asia Pacific is projected to post the highest regional CAGR at 8.86% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Network Encryption Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing number of network security breaches | +2.1% | Global with heightened focus in North America and Europe | Short term (≤ 2 years) |

| Accelerating adoption of cloud-based workloads | +1.8% | Global led by North America and Asia Pacific | Medium term (2-4 years) |

| Surge in 5G rollouts requiring high-speed inline encryption | +1.5% | Asia Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Compliance mandates such as GDPR and HIPAA | +1.2% | Europe and North America primarily, expanding to Asia Pacific | Long term (≥ 4 years) |

| Growing concern over quantum computing threats | +0.9% | Global with early adoption in North America and Europe | Long term (≥ 4 years) |

| Rising adoption of zero trust architectures | +0.8% | North America and Europe, expanding to Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Number of Network Security Breaches

Ransomware campaigns and state-sponsored intrusions grew in frequency and sophistication during 2024, driving boards to accelerate encryption investments across data-in-motion channels. Breach disclosure laws in the United States, Europe, and several Asia-Pacific jurisdictions impose heavy penalties for unprotected data exposure, prompting enterprises to encrypt internal east-west traffic alongside external communications. Insurance underwriters have tightened policy terms, granting premium discounts only when policyholders can prove ubiquitous encryption coverage. As a result, procurement teams now treat network-level encryption as a baseline control, rather than an optional safeguard, which propels continuous spending even when broader IT budgets are tightened. Vendors able to deliver easy-to-deploy appliances and automated policy engines gain rapid traction.

Accelerating Adoption of Cloud-Based Workloads

Cloud migration places new emphasis on encryption agility, because workloads spin up and down within seconds across multi-cloud footprints. Native cloud networking services now incorporate advanced encryption, enabling security teams to centralize key governance while application owners maintain DevOps velocity.[1]Amazon Web Services, “New Amazon VPC Lattice: Simplify Service-to-Service Connectivity, Security, and Monitoring,” amazon.com Service mesh frameworks integrate transparent TLS termination, removing the need for developers to code encryption calls. Consumption-based pricing lowers entry barriers for SMEs, enabling them to match the security posture of larger peers without capital purchases. Consequently, cloud-centric encryption platforms experience double-digit growth, driving demand for complementary key management-as-a-service offerings.

Surge in 5G Rollouts Requiring High-Speed Inline Encryption

Release 17 of the 3GPP standard mandates end-to-end encryption for network slicing, prompting operators to deploy line-rate cryptography at speeds of 100 Gbps and above.[2]3rd Generation Partnership Project, “Release 17 Specifications,” 3gpp.org Equipment vendors embed dedicated cryptographic processors in base stations and core routers, thereby avoiding the need for separate appliances that introduce latency. Industrial 5G use cases, ranging from autonomous robotics to remote surgery, cannot tolerate more than sub-millisecond delays; therefore, carriers favor hardware that pairs switching silicon with encryption engines on a single chipset. Capital outlays for encryption-ready 5G infrastructure, therefore, form a multi-year demand funnel, especially in the Asia Pacific, where greenfield deployments are more prevalent.

Compliance Mandates Such as GDPR and HIPAA

Regulators increasingly specify encryption at rest and in transit as explicit requirements rather than best-practice recommendations. Under GDPR, supervisory authorities throughout the European Union issue multimillion-euro fines when organizations fail to secure personal data during network transfer. In the United States, the 2025 update to the HIPAA Privacy Rule broadens the definition of protected health information, compelling covered entities to encrypt all telehealth traffic. Similar provisions appear in India’s Digital Personal Data Protection Act and Brazil’s LGPD, creating a harmonizing effect that raises the global floor for encryption adoption. Compliance teams now view certificate life-cycle automation and centralized audit logging as essential capabilities, benefiting platform vendors that integrate policy, key management, and reporting within a single console.[3]European Commission, “Cyber Resilience Act,” europa.eu

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High implementation cost of network encryption solutions | -1.4% | Global, with sharper pressure on SMEs in emerging markets | Short term (≤ 2 years) |

| Performance overhead and latency concerns in high-speed networks | -1.1% | Global, acutely felt in high-frequency trading and industrial control settings | Medium term (2-4 years) |

| Interoperability complexities across multi-vendor environments | -0.9% | Global, especially in large enterprises running heterogeneous infrastructure | Medium term (2-4 years) |

| Shortage of skilled cryptography professionals | -0.7% | Global, most pronounced in Asia Pacific and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Implementation Cost of Network Encryption Solutions

Comprehensive deployments often require specialized appliances, consulting services, and staff training, driving project outlays from USD 500,000 to well above USD 5 million for mid-sized enterprises. Budget pressure is more acute in emerging economies where local currency fluctuations inflate imported hardware prices. Additionally, legacy switches and routers may lack built-in crypto acceleration, forcing expensive infrastructure refreshes. Managed services do offset capital burdens, but small businesses still struggle with recurring subscription fees. As a result, price-sensitive buyers defer or narrow project scope, limiting near-term penetration in segments outside regulated verticals.

Performance Overhead and Latency Concerns in High-Speed Networks

Encrypting high-frequency trading feeds or manufacturing control loops adds 50-200 microseconds per hop, an unacceptable delay for applications that measure success in single-digit microseconds. Even when hardware acceleration is present, CPU cycles consumed by cryptographic operations can reduce overall throughput by 10-30%. Operators sometimes adopt selective encryption, leaving less-critical traffic unprotected to preserve performance, which limits total addressable spend. Vendors therefore face pressure to innovate lightweight ciphers, pipeline architectures, and FPGA-based offloads that close the latency gap without spiking power consumption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Cloud Migration Accelerates Despite Security Concerns

Cloud implementations are projected to register the fastest 9.87% CAGR through 2031, yet on-premise deployments still represented 56.74% of the network encryption market share in 2025. The large installed base of legacy applications and stringent data sovereignty rules in BFSI and government sectors anchor on-premise demand, while new digital services default to cloud-native encryption offerings. Major providers bundle key lifecycle management and automated certificate rotation, lowering the operational burden for security teams.

Hybrid patterns emerge as organizations retain mission-critical workloads on-site but route development, analytics, and customer-facing services through cloud backbones. This two-speed architecture allows buyers to experiment with consumption-based encryption without abandoning their existing investments. Vendors that supply unified policy engines capable of extending across on-premises gear and virtual appliances in public clouds gain account stickiness. As post-quantum algorithms become mainstream, cloud platforms offer faster upgrade cycles, potentially tilting long-term volume toward hosted encryption models.

By Component: Software-Defined Solutions Reshape Market Dynamics

Hardware retained 49.01% of the network encryption market share in 2025, as ultrafast links still rely on ASICs and FPGAs to maintain line-rate performance. Yet the solutions and services segment posts a 10.05% CAGR, illustrating the pivot toward flexible, software-controlled security. Enterprises value API-driven orchestration that integrates with infrastructure-as-code workflows, enabling the dynamic creation of tunnels and policy changes within seconds.

Managed security service providers integrate encryption into bundled offerings that combine threat detection, certificate automation, and zero-trust segmentation. Artificial intelligence assists by analyzing key usage patterns and predicting certificate expirations, reducing unplanned outages. Modular licensing also allows customers to scale bandwidth or algorithm suites without forklift upgrades. Over the forecast period, chip-level crypto blocks will become commoditized, while differentiation will shift to software analytics, compliance reporting, and broader integration capabilities.

By Organization Size: SME Adoption Accelerates Through Cloud Accessibility

Large enterprises contributed 60.92% of 2025 revenue, reflecting complex global networks and deep security budgets. Nonetheless, SMEs demonstrate a 9.94% CAGR thanks to pay-as-you-go models that remove large upfront costs. Cloud marketplaces now offer encryption-as-a-service bundles that can be deployed with just a few clicks, eliminating the need for specialized cryptography staff.

Vendor marketing emphasizes regulatory alignment, providing templated policies that map to HIPAA, PCI-DSS, and GDPR controls. Automated dashboards surface compliance gaps, supporting audit readiness for firms with limited personnel. As cyber insurers tighten coverage terms, SMEs perceive encryption as a prerequisite for affordable premiums, further stimulating demand. The democratization of advanced cryptography, therefore, widens the addressable base beyond traditional high-security verticals.

By End-User Industry: Healthcare Emerges as Growth Leader

BFSI remained the single largest contributor with a 27.35% share in 2025, derived from sustained investment in encryption for payments, core banking, and trading infrastructure. Healthcare’s 8.49% CAGR outpaces all other industries as telehealth platforms and electronic health records generate sensitive data flows that traverse public networks. Hospitals upgrade to TLS 1.3 and quantum-safe algorithms to protect patient confidentiality amid a rise in ransomware events.

Telecommunications operators also appear prominently as they embed encryption into 5G and edge computing nodes. Government and defense agencies uphold consistent demand, often specifying domestic key generation and multi-factor authentication within procurement tenders. Media and entertainment companies encrypt high-value content across CDNs to combat piracy, while manufacturers secure industrial IoT traffic between plants and cloud analytics engines. Cross-industry reliance on distributed workflows ensures that the network encryption market maintains a diverse revenue mix.

Geography Analysis

North America accounted for 33.45% of the revenue in 2025, underpinned by early zero-trust adoption, rich cyber budgets, and proximity to most leading encryption vendors. Federal mandates requiring quantum-resistant migration by 2026 further accelerate domestic upgrades. U.S. carriers likewise bundle inline encryption into nationwide 5G programs, stimulating equipment refresh cycles.

The Asia Pacific is projected to deliver the fastest 8.86% CAGR through 2031, driven by significant cloud investments in China, India, and Southeast Asia. Regional regulators tighten data residency rules, prompting enterprises to deploy locally managed key stores. Governments channel stimulus funds toward quantum research and 5G infrastructure, indirectly subsidizing encryption-capable hardware. Japanese financial institutions are piloting dual-algorithm schemes that combine classical and lattice-based ciphers, signaling an upcoming wave of post-quantum transitions.

Europe remains a pivotal market, as GDPR fines motivate ongoing spending on encryption. The forthcoming Cyber Resilience Act extends mandatory security controls to connected products, indirectly broadening the scope of encrypted channels. Telecom operators in Germany and France are integrating traffic-layer encryption into their Open RAN rollouts, while Scandinavian countries are leading early trials of quantum key distribution backbones. The Middle East and Africa, as well as South America, show rising adoption, although skills shortages and budget constraints push customers toward managed services and cloud deployment models.

Competitive Landscape

The network encryption market is moderately fragmented. Established infrastructure vendors, such as Cisco Systems, Juniper Networks, and Huawei Technologies, leverage in-house silicon to sustain their high-performance leadership. Simultaneously, specialized software vendors focus on quantum-safe algorithms and zero-trust orchestration layers, eroding market share from incumbents in greenfield cloud projects. Vendor selection criteria now weigh integration depth with identity providers and policy engines above raw throughput figures.

Intellectual property filings highlight fierce competition around FPGA-based cryptographic accelerators and distributed key escrow mechanisms. Mergers target complementary strengths: Thales absorbing Imperva reflects hardware players seeking database-level encryption intellectual property, while service providers align with hyperscale clouds to embed security natively. Early movers in post-quantum readiness command premium pricing as risk-averse industries lock in long-term confidentiality.

Channel ecosystems also matter. Vendors cultivate partnerships with system integrators that package encryption with zero trust assessments, cloud migration projects, and 5G deployments. Open-source libraries, such as OpenSSL 3.2, gain corporate backing to accelerate the rollout of hybrid classical-quantum cipher suites. As buyers favor consolidated platforms, suppliers able to bundle certificate automation, analytics, and threat detection alongside transport-layer encryption stand to capture upsell opportunities.

Network Encryption Industry Leaders

Thales Trusted Cyber Technologies

Juniper Networks Inc.

Atos SE

Certes Networks Inc.

Senetas Corporation Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: The Financial Services Information Sharing and Analysis Center published the white paper “The Timeline for Post Quantum Cryptographic Migration.” Developed with experts from financial institutions that collectively manage USD 100 trillion in assets across 75 countries, the paper calls for a synchronized global roadmap and clear milestones to steer regulators, banks, and vendors toward quantum-resistant encryption.

- September 2025: Akamai Technologies enabled post-quantum cryptography on its edge computing platform, letting customers activate TLS 1.3 hybrid key group X25519MLKEM768 at no additional cost. The rollout allows current browsers to open quantum-safe sessions while preserving backward compatibility, and Akamai plans to extend full PQC coverage across its network by early 2026.

- September 2025: OpenSSL Corporation adopted Entrust nShield 5c network-attached Hardware Security Modules for its production code-signing environment. The FIPS 140-3 certified hardware supplies a tamper-resistant root of trust and introduces NIST-standardized algorithms ML-KEM, SLH-DSA, and ML-DSA, bringing quantum-safe digital signatures to future OpenSSL releases.

- September 2025: Cisco Systems introduced the N9300 Series Smart Switches for data centers, combining up to 800 Gbps throughput with built-in Layer 4 segmentation. The switches integrate Hypershield for distributed policy enforcement and Live Protect eBPF functions that can deploy instant compensating controls against new vulnerabilities without taking systems offline.

Global Network Encryption Market Report Scope

Network encryption is encoding sensitive data such as passwords, credentials, and files, among others, which are transmitted or communicated through a computer network. The study also tracks key market parameters, underlying growth influencers, and major vendors operating in the industry, which is expected to support market estimations and growth rates over the forecast period.

The Network Encryption Market Report is Segmented by Deployment Type (Cloud, On-Premise), Component (Hardware, Solutions and Services), Organization Size (Small and Medium-Sized Enterprises, Large-Sized Enterprises), End-User Industry (Telecom and IT, BFSI, Government, Media and Entertainment, Healthcare, Defence and Aerospace, Other End-User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Cloud |

| On-premise |

| Hardware |

| Solutions and Services |

| Small and Medium-Sized Enterprises |

| Large-Sized Enterprises |

| Telecom and IT |

| BFSI |

| Government |

| Media and Entertainment |

| Healthcare |

| Defence and Aerospace |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Deployment Type | Cloud | ||

| On-premise | |||

| By Component | Hardware | ||

| Solutions and Services | |||

| By Organization Size | Small and Medium-Sized Enterprises | ||

| Large-Sized Enterprises | |||

| By End-User Industry | Telecom and IT | ||

| BFSI | |||

| Government | |||

| Media and Entertainment | |||

| Healthcare | |||

| Defence and Aerospace | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of the network encryption space by 2031?

The sector is forecast to reach USD 8.37 billion by 2031.

Which deployment model is growing fastest for network encryption solutions?

Cloud-based deployments are expanding at a 9.87% CAGR through 2031.

Why is Asia Pacific considered the most dynamic region for network-level encryption?

Rapid 5G expansion, digital transformation programs, and evolving data protection laws are propelling a 8.86% regional CAGR.

Which end-user vertical shows the highest forward growth?

Healthcare leads with an 8.49% CAGR, driven by telehealth and electronic health record protection demands.

How are quantum computing advancements influencing encryption strategies?

Organizations are migrating to post-quantum algorithms and dual-cipher approaches in anticipation of cryptographically relevant quantum computers.

What inhibits broader SME adoption of advanced network encryption?

High implementation and recurring costs, along with limited in-house expertise, remain the main barriers despite growing cloud-based options.

Page last updated on: