Secure Multi-Party Computation Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

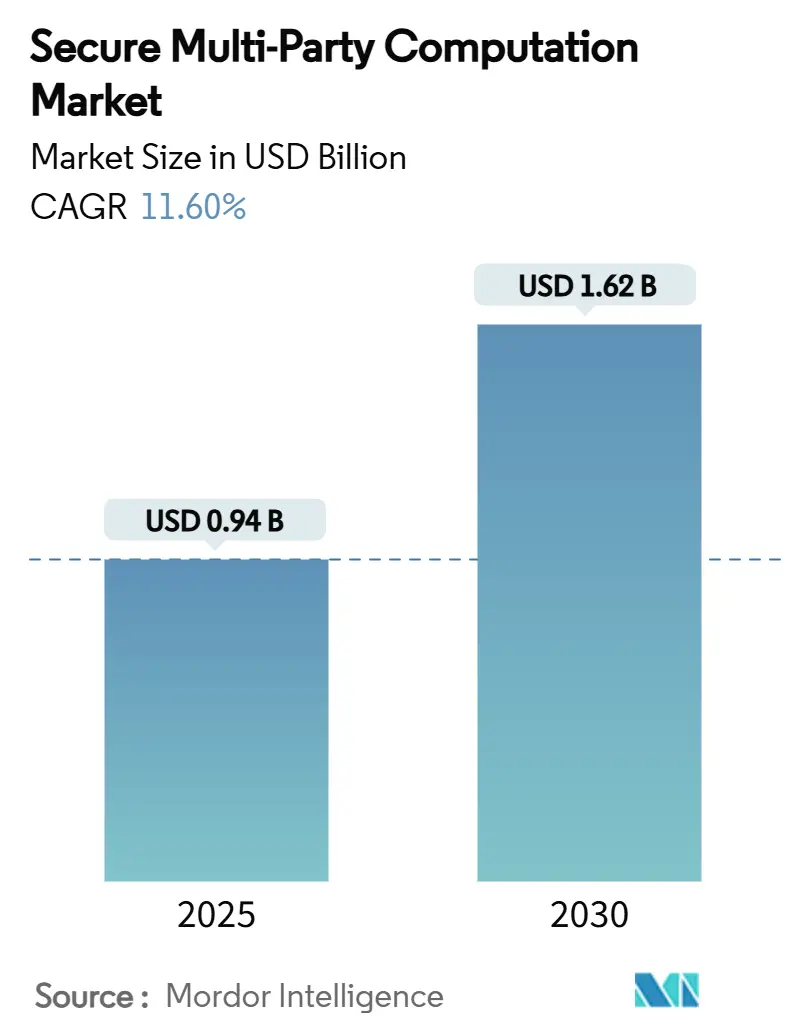

| Market Size (2025) | USD 0.94 Billion |

| Market Size (2030) | USD 1.62 Billion |

| Growth Rate (2025 - 2030) | 11.60% CAGR |

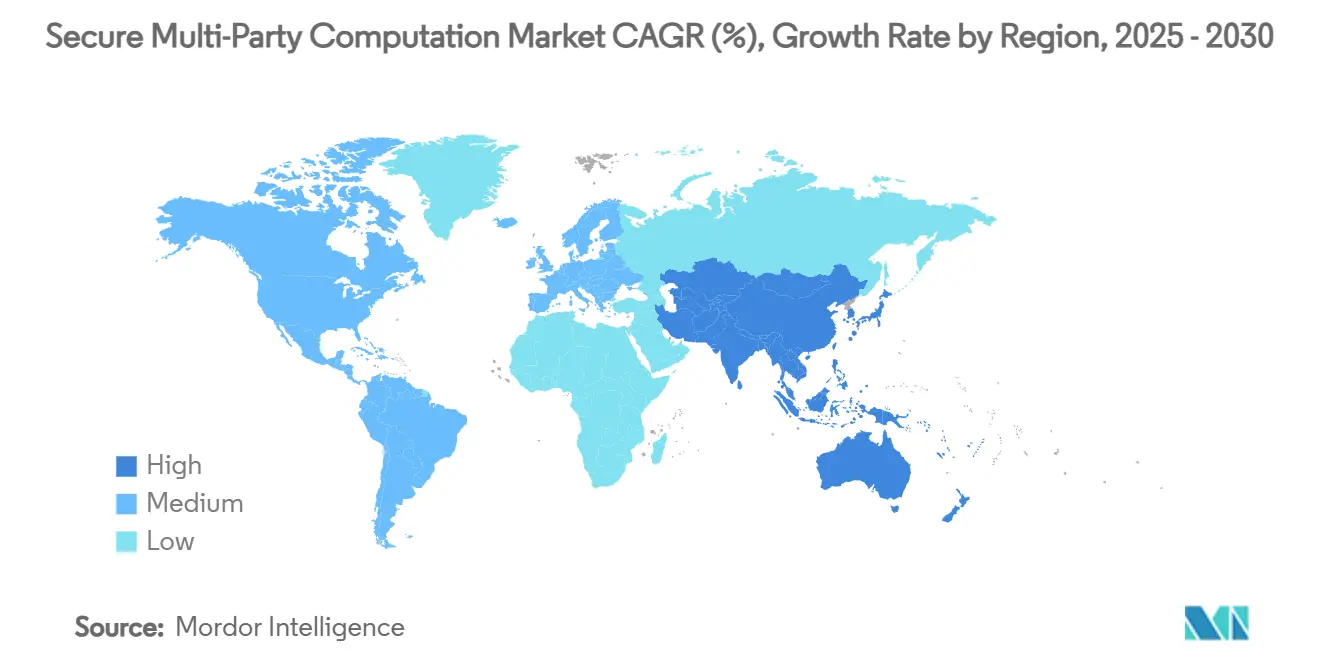

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Secure Multi-Party Computation Market Analysis by Mordor Intelligence

The secure multi-party computation market size reached USD 0.94 billion in 2025 and is forecast to climb to USD 1.62 billion by 2030, reflecting an 11.6% CAGR. Enterprises regard the technology as the missing layer that lets them collaborate on sensitive data while staying compliant with fast-tightening privacy laws. Converging forces—regulatory demands, cloud-native adoption, institutional crypto expansion, and performance gains from hardware accelerators—keep the secure multi-party computation market on a steady growth path. Vendors differentiate through protocol efficiency, sector-specific tooling, and managed services that mask cryptographic complexity from end-users. Asia-Pacific’s policy push around privacy computing and digital finance adds a powerful geographic tailwind, while North America’s mature financial sector keeps near-term demand resilient. Competition centers on talent acquisition, protocol standardization, and low-latency execution environments.

Key Report Takeaways

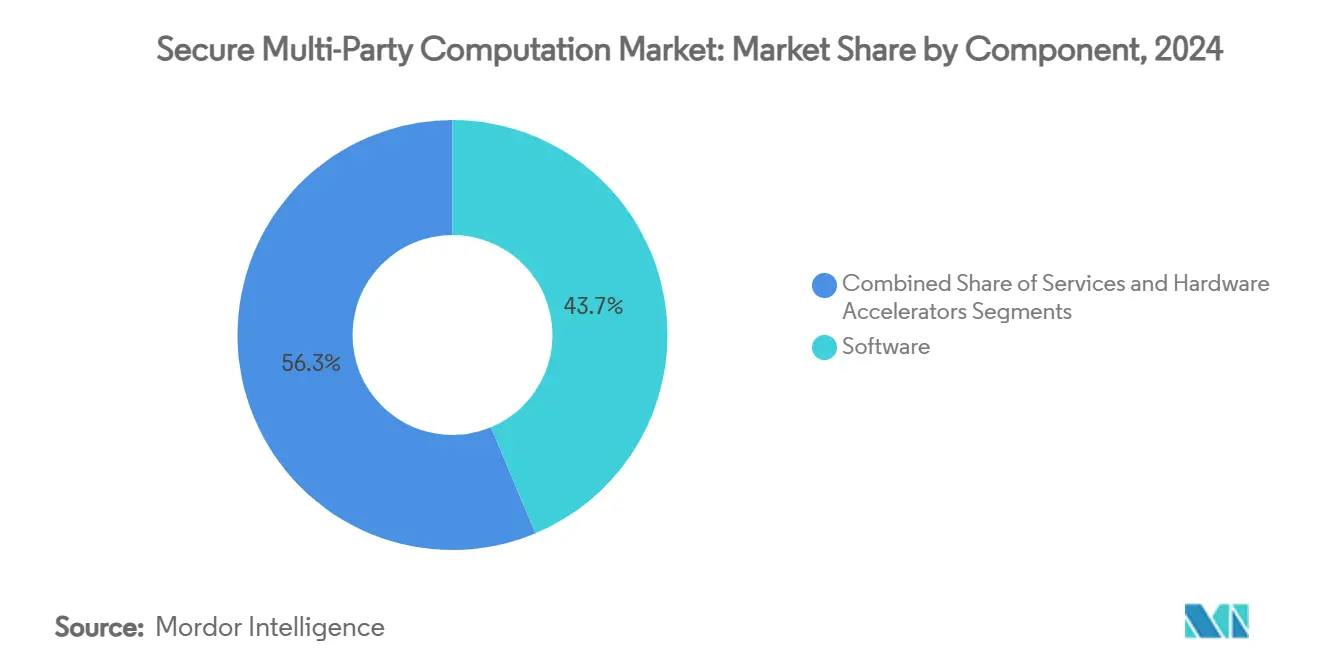

- By component, software held 43.7% of the secure multi-party computation market share in 2024, while hardware accelerators are projected to expand at a 13.2% CAGR through 2030.

- By deployment mode, cloud deployments captured 50.3% of the secure multi-party computation market size in 2024; hybrid deployments are forecast to grow at a 13.1% CAGR to 2030.

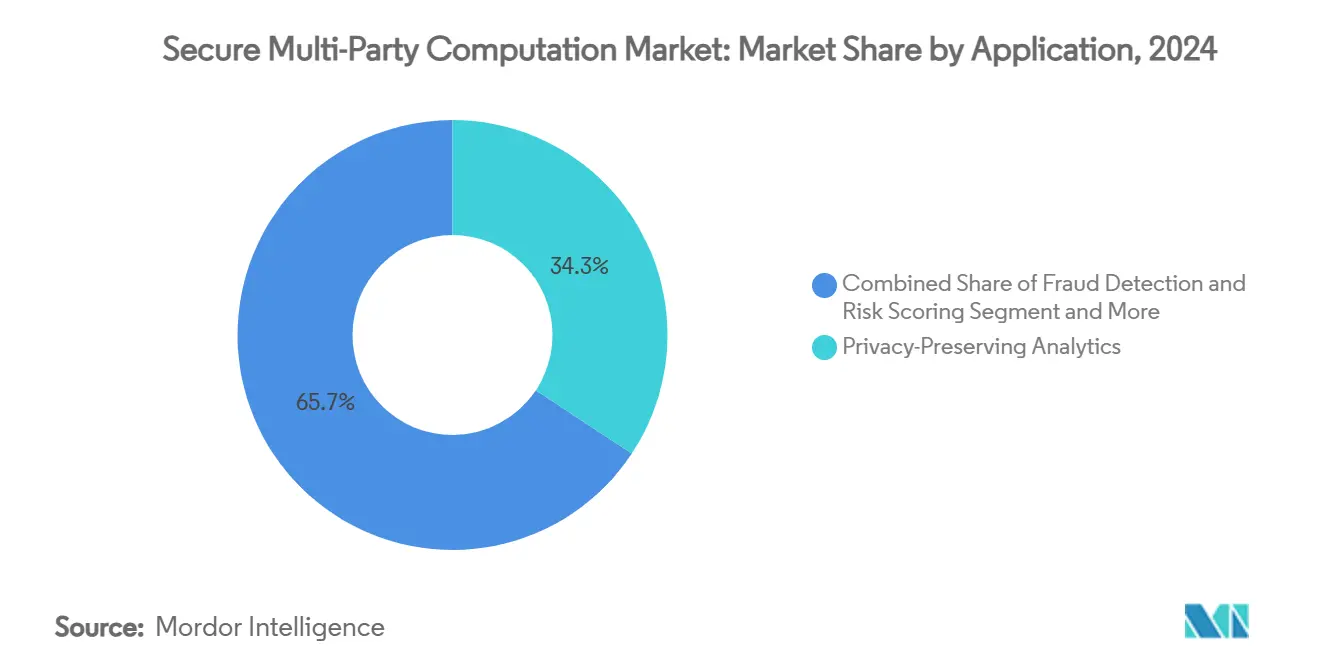

- By application, privacy-preserving analytics led with 34.3% of secure multi-party computation market share in 2024; digital-asset custody and key management are advancing at a 12.6% CAGR through 2030.

- By industry vertical, BFSI commanded 29.1% of the secure multi-party computation market share in 2024, whereas IT and telecom record the highest projected CAGR at 12.8% through 2030.

- By geography, North America dominated with 38.5% revenue share in 2024; Asia-Pacific is on track for a 13% CAGR between 2025-2030.

Global Secure Multi-Party Computation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing privacy-first regulations (GDPR, CCPA, etc.) | +2.1% | Global, with strongest impact in EU and North America | Medium term (2-4 years) |

| Surge in data-sharing collaborations in BFSI and healthcare | +1.8% | North America and EU, expanding to APAC | Short term (≤ 2 years) |

| Cloud-native PET stacks adopted by hyperscalers | +1.5% | Global, led by North America and Europe | Medium term (2-4 years) |

| Rising crypto-custody and digital-asset key-management needs | +1.2% | Global, with concentration in crypto-friendly jurisdictions | Short term (≤ 2 years) |

| Post-quantum threat mitigation via threshold cryptography | +0.9% | Global, with early adoption in defense and finance sectors | Long term (≥ 4 years) |

| Edge-AI and IoT demand for lightweight MPC protocols | +0.7% | APAC core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Privacy-First Regulations Drive Enterprise Adoption

GDPR Article 25, California’s CCPA, and related statutes now require privacy-by-design architectures, positioning secure multi-party computation as a compliance enabler. [1]European Data Protection Board, “EDPB Guidance on Privacy-Enhancing Technologies,” edpb.europa.eu The European Data Protection Board’s 2024 guidance and NIST’s 2025 differential-privacy evaluation guide give enterprises clear validation paths. Multinationals use the technology to keep data resident yet still derive aggregate insight, reducing cross-border legal risk. Boards view deployment as a defensive investment that also unlocks new collaborative revenue streams. Subsequent local reforms in the United Kingdom and Japan echo similar language, broadening regulatory momentum.

Surge in Data-Sharing Collaborations Across Critical Sectors

Banks and hospitals recognize that pooled analytics surpass siloed models, accelerating the adoption of secure multi-party computation market solutions for fraud detection and medical research. [2]Swift, “AI-Powered Fraud Detection Collaboration,” swift.com Swift’s Google Cloud pilot improved anomaly detection accuracy by sharing blinded transaction patterns. ARPA-H’s DeCaPH framework demonstrated cross-hospital cancer research without exposing patient data. As more institutions join, network effects compound, turning privacy barriers into collaborative advantages. Sector leaders report shorter research cycles and improved fraud-loss ratios, reinforcing a virtuous adoption loop.

Cloud-Native PET Stacks Transform Enterprise Infrastructure

Hyperscalers embed privacy-enhancing technologies directly into managed services, letting companies add secure multi-party computation routines through familiar APIs. Google Cloud’s template jobs and Azure’s Duality integration lower the talent hurdle. Auto-scaling and pay-as-you-go pricing shrink the total cost of ownership, while confidential-computing enclaves address sovereignty concerns. Mid-market firms now pilot projects that would previously require dedicated cryptographers. Hardware options such as photonic accelerators appear as service tiers, compressing compute latency further.

Rising Crypto-Custody Demands Accelerate Key-Management Innovation

Institutional crypto growth turns threshold signatures and distributed key custody into mandatory infrastructure. Taurus rolled out privacy-preserving stablecoin contracts on the Aztec Network, pairing compliance with on-chain confidentiality. Large banks adopt secure multi-party computation to decentralize private-key control, eliminating single points of failure. As stablecoin circulation moves toward USD 1-2 trillion by decade-end, demand for resilient, regulator-friendly custody architectures expands, pushing the secure multi-party computation market into mainstream fintech stacks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High latency and compute overhead of current protocols | -1.4% | Global, with stronger impact in latency-sensitive applications | Short term (≤ 2 years) |

| Shortage of SMPC-skilled cryptographers and engineers | -0.8% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| Interoperability gaps among open-source MPC frameworks | -0.6% | Global, affecting enterprise adoption rates | Medium term (2-4 years) |

| Unclear cross-border liability for multi-party data misuse | -0.5% | Global, with regional variations in legal frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Latency and Compute Overhead Limit Real-Time Applications

Benchmarking shows secure multi-party computation workloads can be 100-1000 times slower than plaintext processing, restricting use in high-frequency trading or autonomous control systems. Mixed-protocol research trims communication rounds, but hardware acceleration remains vital. FPGA and photonic prototypes from Optalysys cut homomorphic-encryption runtimes sharply, yet are still rare in production. Enterprises, therefore, adopt hybrid architectures, reserving secure multi-party computation only for the data elements that must remain private.

Critical Shortage of SMPC-Skilled Personnel Constrains Market Growth

Commercial deployment calls for expertise spanning cryptography, distributed systems, and domain knowledge—skills concentrated in a small pool of practitioners. Vendors compete aggressively for talent, lifting salary benchmarks and elongating project timelines. Academic curricula trail enterprise demand; most engineers learn through research fellowships or consultancy engagements. The NSF’s USD 23 million PDaSP program funds practical tools and coursework, but workforce effects will lag near-term market needs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Acceleration Raises Performance Ceiling

Software continues to lead value capture, accounting for 43.7% revenue in 2024. Hardware accelerators, however, post the fastest 13.2% CAGR as companies chase lower latency. Notably, Optalysys photonic processors promise order-of-magnitude speed gains for homomorphic operations. [3]Optalysys, “Photonic Accelerators for Homomorphic Encryption,” optalysys.com Services fill expertise gaps through managed deployments and cryptographic audits.

The secure multi-party computation market increasingly bundles hardware with software licenses, mirroring GPU adoption in AI. ASIC-based threshold-signature modules attract crypto-custody firms that demand deterministic latency. As accelerator prices fall, mid-tier banks and healthcare networks are expected to broaden uptake.

By Deployment Mode: Hybrid Models Offer Control and Scale

Cloud accounted for 50.3% revenue in 2024 as enterprises favored ease of integration. The hybrid segment is projected to expand at a 13.1% CAGR, balancing performance with data-sovereignty mandates. On-premise remains significant in defense and critical infrastructure sectors.

Hybrid deployments partition workloads so that sensitive joins execute inside local enclaves while compute-heavy analytics run in the cloud. Confidential computing hardware, such as Intel SGX, secures boundary points. The secure multi-party computation market size attached to hybrid models will likely surpass on-premise totals by the late 2020s as policy frameworks mature.

By Application: Digital-Asset Custody Becomes Star Performer

Privacy-preserving analytics held the largest 34.3% revenue slice in 2024. Digital-asset custody and key management are accelerating at a 12.6% CAGR amid institutional crypto expansion. Fraud-detection engines, secure AI/ML training, and blockchain middleware follow closely.

Threshold-signature services give banks confidence to hold multi-billion-dollar token positions without exposing single points of compromise. Secure multi-party computation solutions underpin private settlement layers, enabling parties to reconcile on-chain assets securely. The secure multi-party computation market size for custody platforms is forecast to reach mid-nine-figure dollar values by 2030, supported by regulatory endorsements.

By Industry Vertical: IT and Telecom Lead Growth Curve

BFSI captured 29.1% of revenue in 2024 through fraud detection, risk modeling, and compliant crypto services. IT and telecom are the fastest climbers at 12.8% CAGR, as carriers use privacy tech to optimize shared network analytics without leaking competitive data.

Healthcare turns to secure multi-party computation to merge genomic and clinical datasets, while government agencies trial secure census tabulation. Retail pilots focus on joint demand forecasting across suppliers. Collectively, vertical diversification shields the secure multi-party computation industry from over-reliance on any single sector.

Geography Analysis

North America wielded 38.5% revenue share in 2024, powered by mature capital markets, early cloud adoption and DARPA-backed privacy R&D. [4]NITRD, “FY 2025 Budget Supplement,” nitrd.gov A dense ecosystem of cryptography startups and venture investors sustains rapid feature innovation. Local regulators explicitly reference privacy-enhancing technologies, giving enterprises legal certainty.

Asia-Pacific is projected to grow at a 13% CAGR as governments champion privacy computing and digital payments. Japan’s Personal Information Protection Commission guidance, Singapore’s fintech sandboxes, and China’s data-sovereignty rules collectively lift regional demand. The secure multi-party computation market sees manufacturing use cases emerge around supply-chain tracing, complementing strong fintech momentum.

Europe benefits from GDPR’s privacy-by-design mandate and a long academic lineage in cryptography. The European Data Protection Board’s 2024 endorsement of PETs unblocked hesitations among mid-sized firms. Switzerland’s crypto-valley ecosystem creates outsized custody demand, while Germany’s Industry 4.0 initiatives spur industrial data-sharing pilots. Together, these trends anchor steady, regulation-driven adoption across the continent.

Competitive Landscape

The secure multi-party computation market remains moderately fragmented. Niche cryptography houses—Sepior, Partisia, Duality—spearhead protocol breakthroughs, whereas broad-reach vendors like Fireblocks integrate SMPC into turnkey custody stacks. Arcium’s 2024 acquisition of Inpher signaled accelerating consolidation as buyers seek full-stack capability.

Competition pivots on performance metrics and vertical specialization. Vendors pursue hardware acceleration partnerships to differentiate on latency and throughput. Talent scarcity yields high acquisition costs, favoring firms able to bundle managed services that mask cryptographic complexity. Open-source frameworks gain traction, but enterprises still pay for enterprise-grade audits, SLA assurances, and compliance mapping. Patent applications cluster around threshold-signature optimizations and low-round MPC protocols, indicators of a market shifting from research to execution.

Secure Multi-Party Computation Industry Leaders

Sepior ApS

Partisia A/S

Duality Technologies, Inc.

Inpher, Inc.

Enveil, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Taurus introduced a private stablecoin contract with zero-knowledge privacy on Aztec, combining confidentiality and compliance.

- April 2025: Taurus launched Taurus-NETWORK™, the first interbank digital-asset collaboration layer, with Arab Bank Switzerland and Capital Union Bank as founding members.

- March 2025: Taurus expanded to Turkey via BankPozitif, marking the first institutional-grade crypto custody solution by a Turkish bank.

- March 2025: NIST finalized its differential-privacy evaluation guidelines, providing a practical yardstick for PET deployments.

- January 2025: The Hashgraph Association partnered with Taurus to streamline HBAR custody, staking, and tokenization for financial institutions.

Global Secure Multi-Party Computation Market Report Scope

| Software |

| Services |

| Hardware Accelerators |

| On-Premise |

| Cloud-based |

| Hybrid |

| Privacy-Preserving Analytics |

| Fraud Detection and Risk Scoring |

| Secure AI/ML Training and Inference |

| Digital-Asset Custody and Key Management |

| Blockchain and Smart Contracts |

| Other Applications |

| BFSI |

| Healthcare and Life Sciences |

| Government and Defense |

| IT and Telecom |

| Retail and E-commerce |

| Other Industry Verticals |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| Hardware Accelerators | |||

| By Deployment Mode | On-Premise | ||

| Cloud-based | |||

| Hybrid | |||

| By Application | Privacy-Preserving Analytics | ||

| Fraud Detection and Risk Scoring | |||

| Secure AI/ML Training and Inference | |||

| Digital-Asset Custody and Key Management | |||

| Blockchain and Smart Contracts | |||

| Other Applications | |||

| By Industry Vertical | BFSI | ||

| Healthcare and Life Sciences | |||

| Government and Defense | |||

| IT and Telecom | |||

| Retail and E-commerce | |||

| Other Industry Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Malaysia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the secure multi-party computation market?

The secure multi-party computation market size stood at USD 0.94 billion in 2025 and is projected to reach USD 1.62 billion by 2030.

Which region leads the secure multi-party computation market?

North America commanded 38.5% revenue share in 2024, driven by early regulatory clarity and advanced financial services adoption.

Which component segment is growing fastest?

Hardware accelerators are projected to grow at a 13.2% CAGR through 2030 as organizations seek lower latency.

Why are hybrid deployments gaining traction?

Hybrid architectures offer the scale of cloud computing while meeting data-sovereignty rules, leading to a forecast 13.1% CAGR for the segment.

Which application will see the highest growth?

Digital-asset custody and key management is expected to expand at a 12.6% CAGR, fuelled by institutional cryptocurrency adoption.

What is the main restraint holding back wider SMPC adoption?

Protocol latency remains the largest technical hurdle, creating a 1.4% drag on forecast CAGR until hardware accelerators become mainstream.

Page last updated on: