Egg Replacers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

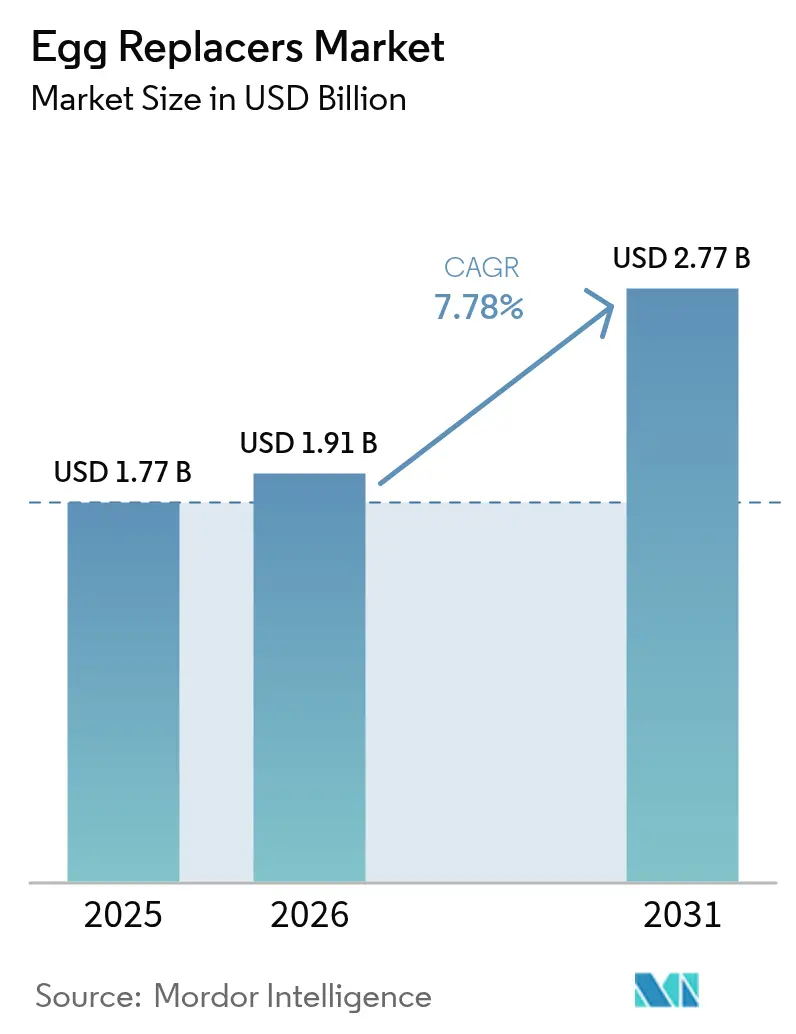

| Market Size (2026) | USD 1.91 Billion |

| Market Size (2031) | USD 2.77 Billion |

| Growth Rate (2026 - 2031) | 7.78% CAGR |

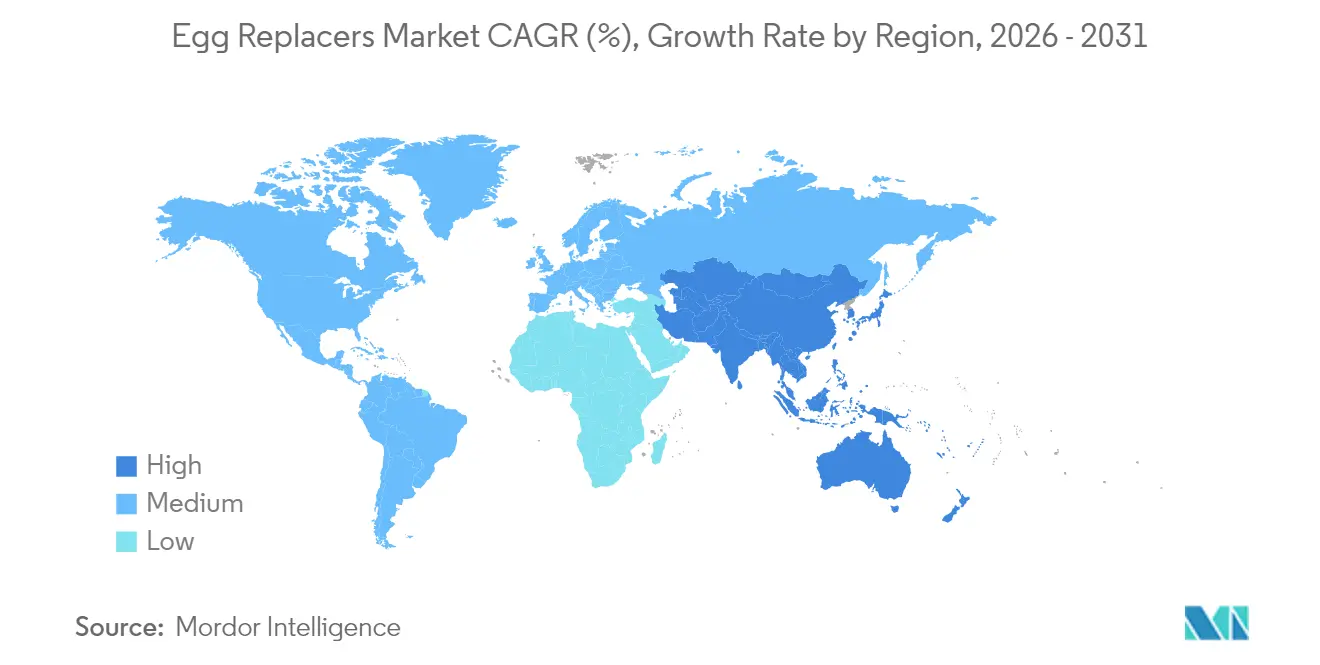

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

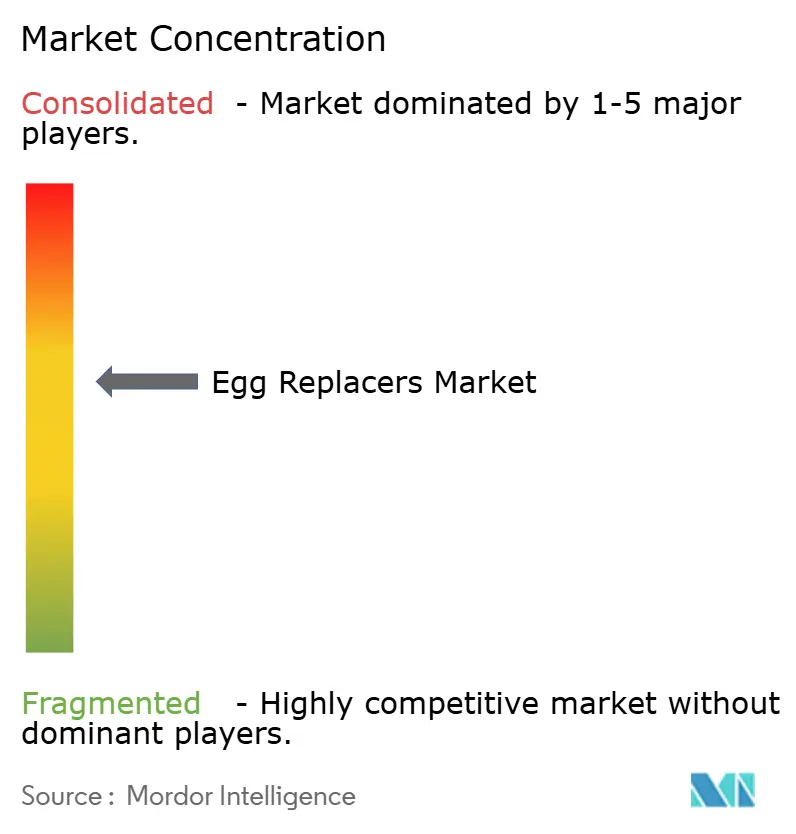

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Egg Replacers Market Analysis by Mordor Intelligence

Egg replacers market size in 2026 is estimated at USD 1.91 billion, growing from 2025 value of USD 1.77 billion with 2031 projections showing USD 2.77 billion, growing at 7.78% CAGR over 2026-2031. This upward trend is driven by several key factors, including rising conventional egg prices, stricter food-safety regulations, and increasing consumer preference for plant-based diets. Ingredient suppliers are proactively addressing supply chain vulnerabilities, while food manufacturers are focusing on developing formulations that maintain the desired taste and texture of products. Additionally, substantial investments in precision-fermentation platforms are accelerating innovation in the market. Large-scale buyers are securing multi-year contracts to ensure a reliable supply of high-functionality egg substitutes. Although achieving cost parity with shell eggs remains a challenge in 2025, the market benefits from heightened biosecurity measures, which are driving up baseline egg prices and narrowing the cost gap, further supporting the growth of the egg replacers market.

Key Report Takeaways

- By ingredient, dairy proteins led with 37.78% egg replacers market share in 2025; algal flour posts the fastest CAGR at 9.68% through 2031.

- By form, dry formats captured 75.05% of the egg replacers market size in 2025; liquid formats expand at an 10.95% CAGR to 2031.

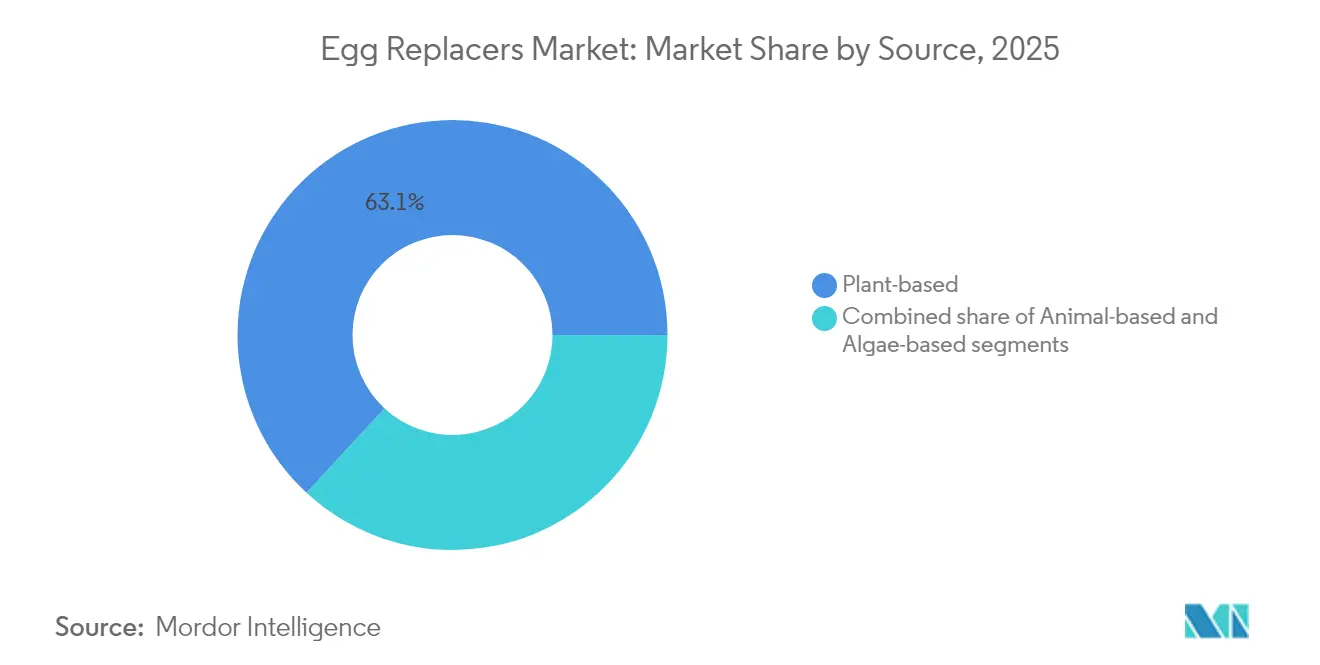

- By source, plant-based inputs accounted for 63.12% of the egg replacers market share in 2025, while algae-based sources are set to grow at 9.91% CAGR.

- By application, bakery and confectionery generated 40.12% of the egg replacers market size in 2025; sauces and dressings are set to advance at a 9.33% CAGR.

- By geography, North America dominated with 35.41% revenue share in 2025; Asia-Pacific records the quickest regional CAGR at 10.21% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Egg Replacers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing egg allergies and dietary restrictions among consumers | +1.2% | Global, with higher prevalence in North America and Europe | Medium term (2-4 years) |

| Rising adoption of vegan and plant-based diets globally | +1.8% | Global, led by North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Growing demand for clean-label and natural food ingredients | +1.5% | North America and Europe primarily, spreading to Asia-Pacific | Medium term (2-4 years) |

| Expansion of the bakery and confectionery industry | +1.3% | Global, with strongest growth in Asia-Pacific and Latin America | Long term (≥ 4 years) |

| Surge in individuals following vegetarian diets | +1.0% | Global, with concentrated growth in India, Europe, and North America | Long term (≥ 4 years) |

| Inconsistent egg pricing and bird flu-related supply problems | +2.2% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing egg allergies and dietary restrictions among consumers

Millions of individuals in the U.S. face food allergies, with eggs being one of the top 9 allergens requiring federal labeling. The Asthma and Allergy Foundation of America identified Wichita, Kansas, as the U.S. city most affected by seasonal allergies in 2025, reflecting broader trends [1]Source: Asthma and Allergy Foundation of America, "U.S. cities suffering most from seasonal allergies in 2025", aafa.org. Over 20 million Americans struggle with food allergies, highlighting the growing demand for effective alternatives, especially during critical developmental stages. Health Canada has mandated clear labeling for 11 priority allergens, including eggs, emphasizing the need for transparent egg replacement solutions. Similarly, the FDA has reinforced the importance of stringent allergen labeling to ensure consumer safety, particularly as some egg substitutes may contain other allergens. Adults with hen's egg white allergies face challenges such as limited dietary options and reduced social interactions, underscoring the need for innovative, safe, and functional food products. As food allergies become a pressing public health concern, the market is shifting toward allergen-free alternatives that prioritize safety, transparency, and inclusivity without compromising quality.

Rising adoption of vegan and plant-based diets globally

In January 2024, research by The Vegan Society revealed that about 3% of Great Britain's population, roughly 2 million people, identify as vegan or adhere to plant-based diets. Additionally, 10% of the population is reducing or eliminating animal products, indicating a significant shift toward plant-based consumption. London, the North East, and the South West lead regionally, with 4% of their populations adopting these diets. Younger individuals aged 16-44 and women (3.60% adoption rate compared to 1.98% for men) show higher adoption rates, highlighting key demographic trends and preferences[2]Source: The Vegan Society, "Nationwide trends highlight growing shift toward plant-based diets", vegansociety.com. This shift is driven by growing awareness of health benefits, environmental sustainability, and animal welfare, which are increasingly influencing consumer choices. The demand for innovative and functional plant-based alternatives continues to rise as these factors gain prominence. Government dietary guidelines are also progressively supporting diverse protein sources, including plant-based options, providing a robust regulatory framework that validates and encourages the adoption of these diets. This evolving landscape offers significant opportunities for stakeholders to develop and market products that cater to the surging demand for plant-based solutions.

Growing demand for clean-label and natural food ingredients

In December 2024, the FDA rolled out a final rule redefining "healthy" nutrient content claims. This move introduces updated parameters, reflecting evolving consumer preferences and regulatory trends. The newly established rule sets limits on added sugars, saturated fats, and sodium. It also underscores the importance of food groups like vegetables, fruits, grains, dairy, and proteins. This strategy responds to the surging demand for clean-label products, which emphasize easily recognizable and natural ingredients. Drawing from the Dietary Guidelines 2020-2025, the rule delineates clear food group equivalents. This guidance nudges manufacturers towards crafting products that uphold nutritional standards while maintaining ingredient transparency. Under this revamped framework, single-ingredient foods—think fruits, vegetables, whole grains, and lean proteins—automatically earn the "healthy" label. This endorsement bolsters the clean-label movement, championing formulations devoid of artificial additives and intricate chemical names. With a growing consumer appetite for transparent ingredient lists, manufacturers are actively reformulating their products. The regulatory landscape supports this shift and champions the adoption of natural ingredients. Take plant-based egg replacers, for instance: they align with clean-label standards and deliver on functional performance in various food applications. This evolving landscape meets consumer demands and sparks innovation, pushing the food industry towards healthier and more transparent offerings.

Expansion of the bakery and confectionery industry

In 2023, global egg production reached approximately 91 million metric tons, with China maintaining its position as the largest producer[3]Source: Food and Agriculture Organization, "Global egg production from 1990 to 2023", fao.org. This dominance highlights the critical role of eggs in food manufacturing and emphasizes the growing need for replacement technologies to address sustainability, cost, and supply chain challenges. The adoption of advanced detection methodologies, such as electronic noses and spectral analysis, demonstrates the industry's commitment to innovation in assessing egg freshness and ensuring product quality. These technologies not only enhance quality control but also align with the increasing demand for efficient and scalable egg replacers. Moreover, the integration of machine learning and multi-sensor data fusion is revolutionizing quality assessment processes, enabling more precise and reliable evaluations that benefit both traditional egg processing and the development of alternative ingredients. The economic significance of eggs, combined with safety and supply chain concerns, is driving manufacturers to adopt diversified ingredient sourcing strategies, with functional replacers emerging as a key solution. In bakery applications, egg replacers must effectively replicate essential properties—such as binding, leavening, and moisture retention—while maintaining product quality and consistency. This ensures consumer satisfaction and supports manufacturing efficiency, thereby accelerating the adoption and growth of egg replacers in the market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher production costs compared to conventional eggs | -1.5% | Global, most pronounced in developing markets | Medium term (2-4 years) |

| Taste and texture differences compared to traditional eggs | -1.2% | Global, varying by application and consumer segment | Long term (≥ 4 years) |

| Price volatility of key ingredients used in egg replacers | -0.8% | Global, with regional variations based on agricultural conditions | Short term (≤ 2 years) |

| Storage and shelf-life limitations of certain egg replacers | -0.5% | Global, particularly in regions with limited cold chain infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher production costs compared to conventional eggs

Manufacturing egg replacers involves more complex processes, specialized equipment, and higher-value raw materials compared to conventional egg production. These factors create cost disadvantages, limiting their adoption in price-sensitive markets. However, the USDA's projection of a 41.1% increase in egg prices by 2025 temporarily narrows this cost gap. Achieving long-term competitiveness will require scaling production and implementing technological advancements to improve efficiency. Precision fermentation technologies present a promising avenue for cost reduction. For instance, companies like Onego Bio are scaling the production of bioidentical egg white proteins, addressing supply constraints while maintaining competitive pricing strategies. The economic impact of highly pathogenic avian influenza, which is projected to cost American consumers USD 14.5 billion in 2024-25, has created short-term opportunities for egg replacers despite their higher baseline production costs. Additionally, drought conditions and rising grain prices are driving up feed expenses, further influencing the cost structure of both traditional and alternative protein sources. Supply chain disruptions have also contributed to temporary opportunities for egg replacers, as price volatility in conventional eggs reduces the cost disparity during periods of crisis. These factors collectively highlight the evolving dynamics of the egg replacer market and the potential for growth despite existing challenges.

Taste and texture differences compared to traditional eggs

Consumer acceptance of egg replacers struggles due to sensory discrepancies with conventional eggs. This is especially evident in dishes where egg flavor and texture are paramount, such as scrambled eggs, baked goods, and custards. Research indicates that plant-based alternatives often carry off-flavors linked to plant proteins. This challenge prompts the need for advanced masking techniques and flavor enhancement strategies to align with consumer expectations. In response, food scientists are turning to sustainable protein sources like mung beans, lupin beans, and chickpeas. They're also harnessing precision fermentation technologies to craft proteins that mimic the cooking properties of egg proteins, such as coagulation and emulsification. Noteworthy technological strides include the emergence of 3D-printed plant-based alternatives. These innovations, featuring microalgae and mung bean proteins, boast an impressive 19% protein content. Additionally, Taiwan's Industrial Technology Research Institute has unveiled groundbreaking plant-based egg substitutes. By integrating patented fungal strains with seaweed and soy proteins, they've crafted products that authentically replicate the textures of both egg whites and yolks. These advancements aim to provide sensory experiences that resonate with traditional egg enthusiasts, tackling a significant market adoption hurdle. With continuous progress in ingredient sourcing, processing technologies, and product formulation, the plant-based egg market is poised for growth in the coming years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient: Dairy Proteins Leverage Established Functionality

In 2025, dairy proteins, with their well-recognized functional properties, command a 37.78% market share. Established regulatory frameworks bolster their application in food processes, particularly for binding, emulsification, and foaming. The FDA's stringent food labeling regulations, as outlined in 21 CFR Part 101, ensure consistent quality standards for dairy protein ingredients. This transparency not only informs consumers but also strengthens market confidence. Backed by decades of research, dairy proteins excel in intricate food systems, harmonizing their multifaceted properties. Such extensive research and application development reduce formulation risks for food producers. Moreover, the robust supply chain infrastructure for dairy proteins provides cost benefits and quality assurances, a challenge for smaller ingredient categories. Clear regulations on dairy protein labeling and safety promote predictable compliance, fueling ongoing investment and innovation in the sector.

Algal flour is poised to be the fastest-growing ingredient segment, projected to expand at a 9.68% CAGR through 2031. This growth is driven by biotechnological advancements that enhance its nutritional and functional profile compared to traditional alternatives. The European Food Safety Authority has approved microalgae as safe for dietary supplements. In parallel, the U.S. FDA has classified several microalgae species as "Generally Recognized as Safe" for consumption, establishing a robust regulatory foundation for market expansion. Microalgae cultivation is notable for its minimal land and resource demands, yet it offers a complete amino acid profile and high protein content, addressing urgent sustainability challenges. Furthermore, government support for biotechnology and sustainable protein sources facilitates the commercialization and scaling of algal flour.

By Form: Dry Formats Dominate Through Processing Advantages

In 2025, the dry form leads the market with a 75.05% share, driven by benefits like extended shelf-life, lower shipping costs, and easier storage, aligning with food manufacturers' supply chain goals. Emerging preservation technologies further enhance its appeal. Research shows bionanocomposite coatings from egg components can preserve fresh eggs for up to three weeks at room temperature without refrigeration, reducing weight loss by 37% and improving quality metrics like the Haugh Unit and Yolk Index. These innovations suggest similar preservation techniques could enhance the stability and usability of dry egg replacer formulations. The concentrated nature of dry formats allows manufacturers to achieve desired functionalities with smaller quantities, ensuring consistent performance across varying conditions. Additionally, FDA regulations under 21 CFR Part 160 provide a clear framework for dried egg products, supporting the development and commercialization of dry egg replacers.

Liquid formats are growing rapidly, with a projected CAGR of 10.95% through 2031, driven by the convenience of ready-to-use formulations that eliminate reconstitution in commercial food production. The Korean Journal of Food Preservation highlights ovalbumin, which constitutes 54% of egg white proteins and plays a key role in gelation, foaming, and emulsification, emphasizing the complexity liquid replacers must replicate. Advances in separation techniques have improved ovalbumin extraction, enabling the production of bioactive peptides with antioxidant and antimicrobial benefits. Liquid alternatives offer immediate functionality and integrate seamlessly into production processes, making them valuable for high-volume applications requiring precise dosing and mixing. Innovations in protein extraction and preservation technologies have enhanced the functional characteristics and shelf-life of liquid egg replacers, positioning them as a versatile solution for modern food manufacturing.

By Source: Plant-Based Leadership Faces Algae-Based Disruption

In 2025, established agricultural supply chains, supportive regulatory frameworks, and growing consumer acceptance bolster plant-based sources, commanding a 63.12% market share. These factors facilitate easier market entry and scaling for ingredient manufacturers. The European Union, through policy initiatives and research funding, advocates for a heightened domestic supply of plant-based proteins, fostering a favorable environment for their development and commercialization. Germany has earmarked EUR 38 million to aid the shift towards sustainable proteins, also endorsing public research in plant-based foods. Additionally, a 2024 regulatory review of the protein policy seeks to tackle supply security and price stability concerns, promoting diversified protein sourcing strategies. Diverse protein sources, from soy and pea to faba bean and potato, offer distinct functional traits, aligning with specific food applications and consumer tastes.

Algae-based alternatives are rapidly gaining traction, with projections indicating a 9.91% CAGR growth through 2031. This momentum is driven by biotech advancements in precision fermentation and cultivation, enhancing nutritional profiles and bolstering environmental sustainability. The precision fermentation sector for food ingredients has witnessed explosive growth, with 62 companies marking a 4.4-fold surge since 2018, drawing nearly USD 2 billion in investments from 2013 to 2022. Emerging industry bodies, such as the Precision Fermentation Alliance and Food Fermentation Europe, advocate for regulatory frameworks and market expansion of biotech-based ingredients. The U.S., buoyed by favorable regulations, is set to lead market development, while Europe, propelled by sustainability concerns and supportive policies, is making significant headway. Collaborations between R&D firms and food companies are crucial, focusing on elevating the quality of plant-based alternatives and pioneering novel ingredient solutions.

By Application: Bakery Applications Leverage Functional Complexity

In 2025, bakery and confectionery applications hold a 40.12% market share, highlighting the critical role of egg replacers in binding, leavening, moisture retention, and structure formation. These functions are essential for maintaining product quality and meeting consumer expectations. The diverse demands of baking require egg replacers to perform multiple roles, posing technical challenges. Ingredients with proven performance records are better equipped to address these challenges. Under 21 CFR Part 102, government food safety regulations mandate transparency in labeling for bakery products using egg replacers. These regulations require the use of common names for nonstandardized foods and the disclosure of characterizing ingredients' percentages when they significantly influence consumer perception or pricing, directly impacting marketing strategies. Advanced processing technologies have enabled egg replacers to replicate essential baking properties like gas retention, protein coagulation, and moisture management, driving their adoption in this sector.

Sauces and dressings are projected to experience the fastest market growth, with a CAGR of 9.33% through 2031. This growth is driven by clean-label reformulations and advancements in emulsification technologies, catering to consumer demand for natural ingredients without compromising texture or stability. The FDA's draft guidance on labeling plant-based alternatives emphasizes clear product descriptions and ingredient transparency, aiding manufacturers in communicating the benefits of egg replacers. Specifically addressing plant-based egg alternatives, the guidance advocates for truthful and clear information to enhance consumer understanding. Egg replacers are integral to sauces and dressings, leveraging their emulsification properties to maintain stability while meeting clean-label requirements. The regulatory framework supports innovation by providing clear guidelines for labeling and consumer communication, fostering greater acceptance of alternative ingredients and driving growth in this category.

Geography Analysis

In 2025, North America commands a dominant 35.41% market share, buoyed by its robust infrastructure for plant-based foods, well-defined regulatory frameworks, and an increasing consumer embrace of alternative proteins. These elements pave the way for smoother market entry and expansion for manufacturers of egg replacers. The region's sophisticated supply chains, cutting-edge processing technologies, and hefty venture capital investments work in tandem to spur innovation and commercialization. In Canada, post-public consultations, regulatory bodies have underscored the importance of transparent labeling for plant-based egg substitutes. This move not only aims to clear up potential consumer confusion but also seeks to bolster market growth through assured regulatory clarity. Moreover, the FDA's recent guidance rolls out standardized labeling protocols for plant-based alternatives, streamlining compliance hurdles and enhancing consumer comprehension of product features and nutritional content.

Asia-Pacific is set to lead the growth charge, boasting a projected 10.21% CAGR through 2031. This surge is attributed to the region's burgeoning middle class, evolving dietary choices, and heightened health awareness, all of which amplify the demand for functional food ingredients. Coupled with the region's vast food manufacturing prowess and rich agricultural resources, these factors yield cost benefits in ingredient production and processing. As urbanization progresses, there's a noticeable tilt towards premium processed food categories. A testament to the region's innovative spirit is Taiwan's Industrial Technology Research Institute, which has pioneered plant-based egg alternatives harnessing patented fungal strains and seaweed proteins, underscoring the region's biotechnological strides and its potential leadership in alternative protein innovations.

Europe continues to play a pivotal role in the market, bolstered by sustainability drives, a preference for clean labels, and regulatory frameworks that champion the use of plant-based ingredients across diverse food categories. The EU's initiative to bolster domestic plant-based protein production not only addresses food security but also curtails import dependencies. Germany's 2023 commitment of EUR 38 million towards a sustainable protein transition underscores the region's dedication to nurturing innovation in this domain. Additionally, the European Food Safety Authority's revamped guidance for novel food applications, set to take effect in February 2025, seeks to clarify regulations for avant-garde ingredients while upholding rigorous safety standards for consumer protection. Meanwhile, South America and the Middle East and Africa stand at the cusp of burgeoning opportunities, thanks to their rich agricultural assets and expanding food processing sectors. Yet, hurdles like infrastructural constraints and regulatory ambiguities could temper their growth in the near term when juxtaposed with more mature markets.

Competitive Landscape

The global egg replacers market is moderately consolidated, with a few dominant players coexisting alongside several regional and niche companies. Prominent firms such as Cargill, Incorporated, Archer-Daniels-Midland Company, Ingredion Incorporated, Tate & Lyle PLC, and Kerry Group plc hold substantial market shares, driven by their robust product portfolios and extensive global distribution networks. These leading companies actively invest in product innovation, sustainable sourcing practices, and strategic collaborations to maintain their competitive edge. Meanwhile, smaller firms focus on developing specialized formulations that align with growing consumer preferences for vegan, allergen-free, and clean-label products.

Emerging disruptors are reshaping the market landscape by leveraging precision fermentation and biotechnology to deliver advanced functional properties and improved sustainability compared to traditional alternatives. Companies like Onego Bio and The EVERY Company are at the forefront of this innovation, creating bioidentical proteins through fermentation processes that replicate the functionality of egg proteins. These advancements address critical supply chain vulnerabilities and ethical concerns, positioning these disruptors as key players in the evolving market. Additionally, as regulatory frameworks mature, competitive intensity is expected to rise. For example, the FDA's draft guidance on plant-based alternative labeling introduces standardization opportunities, favoring companies with strong compliance capabilities and well-established quality systems.

Specialized applications, often requiring unique functional properties, present significant white-space opportunities for businesses aiming to differentiate their offerings. Furthermore, underdeveloped regional markets, constrained by limited distribution networks, provide untapped potential for companies willing to invest in infrastructure and market penetration strategies. Emerging ingredient categories, such as algae-based proteins, are also gaining traction due to their innovative nature. These ingredients not only deliver substantial nutritional benefits but also align with growing consumer demand for environmentally sustainable solutions. Together, these factors create a promising landscape for market expansion and long-term growth opportunities.

Egg Replacers Industry Leaders

-

Cargill, Incorporated

-

Archer-Daniels-Midland Company

-

Ingredion Incorporated

-

Tate & Lyle PLC

-

Kerry Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Corbion has launched Vantage 11E and Vantage 12E egg replacers to help bakeries tackle egg supply and pricing challenges, with Vantage 11E providing complete egg replacement in bread and buns and Vantage 12E enabling up to 40% egg reduction in cakes and sweet goods, according to the brand.

- April 2025: Innophos expanded its Levair portfolio with the addition of Levair Egg Replace. Levair Egg Replace is an egg replacement solution for commercial bakeries. According to the brand, the new egg replacement was designed for full or partial egg replacement of egg yolks and dried whole eggs. The applications the product may be used in include cakes, donuts, muffins, and sponge cakes.

- August 2024: Nandi Proteins has secured over GBP 500,000 from Nesta and Scottish Enterprise to advance its egg white replacer, which uses vegetable proteins to substitute egg whites in products like gluten-free bread and muffins. According to the brand, this innovation enables vegetarian meat alternatives to be marketed as vegan and supports the removal of undesirable ingredients such as methylcellulose and chemical emulsifiers, aligning with industry trends toward cleaner labels and healthier formulations.

- June 2024: Revyve, a Dutch food tech company, has unveiled a minimally processed, clean-label egg replacement for burgers, made from upcycled brewer’s yeast and free from stealth starches, emulsifiers, and E-numbers. According to the brand, this yeast-based ingredient mimics the binding and gelling properties of egg whites, delivering a firm, springy texture and sensory appeal in plant-based burgers while also being non-GMO, vegan, and cost-effective for manufacturers.

Global Egg Replacers Market Report Scope

The Global Egg Replacers market has been segmented by form into dry and liquid egg replacements.By source, the market of egg replacers is segmented as plant-based and animal-based. Based on theapplication, the global egg replacers can be broadly classified according to the use in bakery & confectionery,dressings & spreads, savories, sauces, and others. Also, referring to the basic ingredient presence, the egg replacers are segregated intodairy proteins, soy-based products, starch, algal flour, and others. At last, the global egg replacers marketis differentiated on the basis ofGeography.

| Dairy Proteins |

| Starch |

| Soy-based Products |

| Hydrocolloids |

| Algal Flour |

| Others |

| Dry |

| Liquid |

| Plant-based |

| Animal-based |

| Algae-based |

| Bakery and Confectionery |

| Snacks and Savories Products |

| Sauces and Dressings |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Ingredient | Dairy Proteins | |

| Starch | ||

| Soy-based Products | ||

| Hydrocolloids | ||

| Algal Flour | ||

| Others | ||

| By Form | Dry | |

| Liquid | ||

| By Source | Plant-based | |

| Animal-based | ||

| Algae-based | ||

| By Application | Bakery and Confectionery | |

| Snacks and Savories Products | ||

| Sauces and Dressings | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the egg replacers market?

The egg replacers market reached USD 1.91 billion in 2026 and is projected to hit USD 2.77 billion by 2031.

Which ingredient segment leads the egg replacers industry?

Dairy proteins currently hold the top position with 37.78% market share because of their proven functional performance.

Which region is growing fastest for egg substitutes?

Asia-Pacific posts the quickest regional CAGR at 10.21% through 2031 due to dietary diversification and government-supported protein innovation.

What role does regulation play in adoption?

Clear labeling rules from the FDA, EFSA, and Health Canada reduce compliance uncertainty, helping new egg replacers reach shelves more quickly while protecting consumers.

Page last updated on: