Molded Fiber Egg Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.98 Billion |

| Market Size (2031) | USD 2.77 Billion |

| Growth Rate (2026 - 2031) | 6.97% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Molded Fiber Egg Carton Market Analysis by Mordor Intelligence

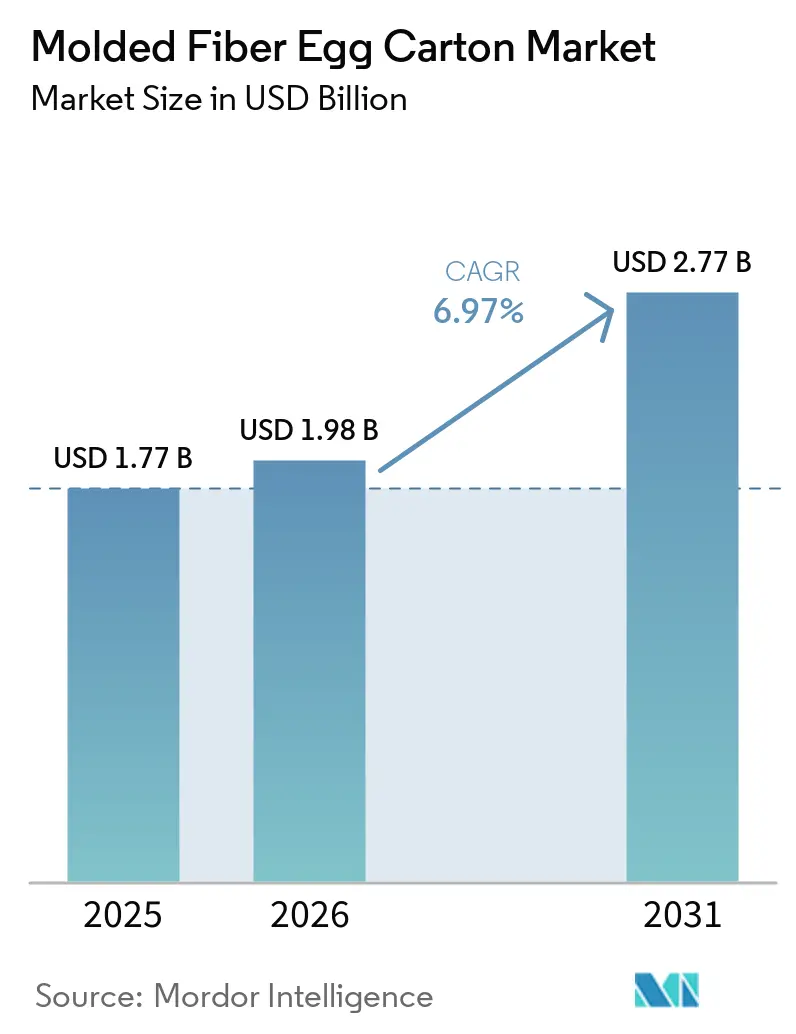

The molded fiber egg carton market size is projected to expand from USD 1.77 billion in 2025 and USD 1.98 billion in 2026 to USD 2.77 billion by 2031, registering a CAGR of 6.97% between 2026 to 2031. The molded fiber egg carton market is being lifted by tighter plastic phaseout rules in North America and Europe, where retailers and converters are moving away from foam and other difficult-to-recycle formats. The molded fiber egg carton market is also supported by a larger global egg consumption base, as poultry output rises and more eggs move through organized retail and mechanized packing systems. At the same time, cage-free housing mandates and stronger shelf-ready presentation needs are changing carton specifications toward better printability, tighter dimensional control, and more reliable closure performance. Producers that already offer PFAS-free formats are in a stronger position in the molded fiber egg carton market because they face lower reformulation pressure than plastic and coated paperboard alternatives. Raw material and freight volatility still weigh on margins, but the molded fiber egg carton market continues to benefit from retail conversion and industrial packing investment.

Key Report Takeaways

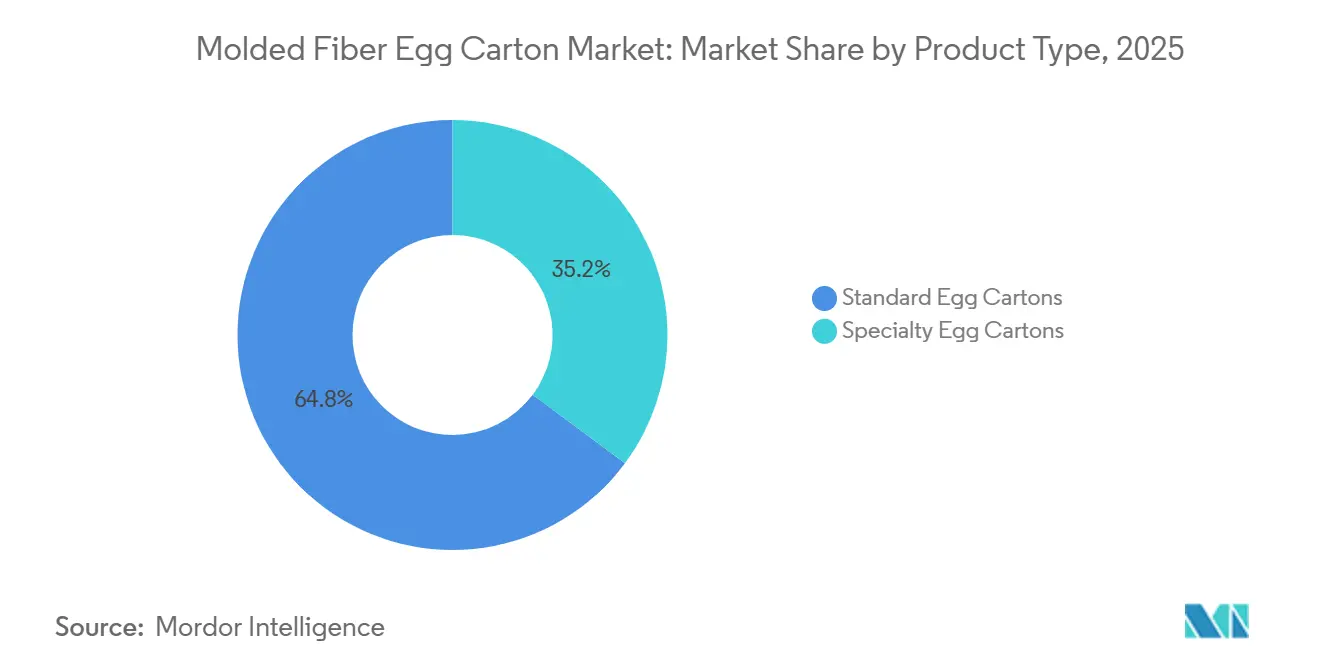

- By product type, Standard Egg Cartons held 64.83% of the molded fiber egg carton market in 2025.

- By capacity, the molded fiber egg carton market for the 19 to 30 eggs segment is projected to grow at 8.12% CAGR through 2031.

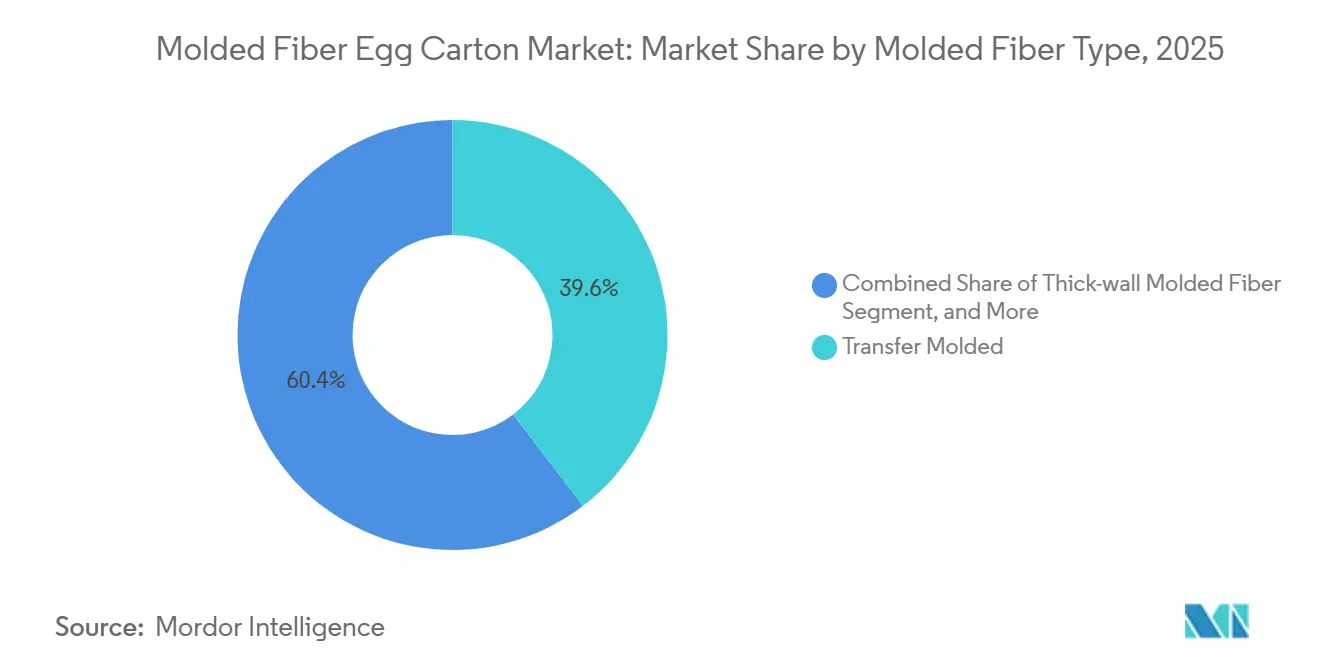

- By molded fiber type, Transfer Molded formats accounted for 39.61% of the molded fiber egg carton market in 2025.

- By application, the molded fiber egg carton market for industrial is projected to grow at a 8.27% CAGR through 2031.

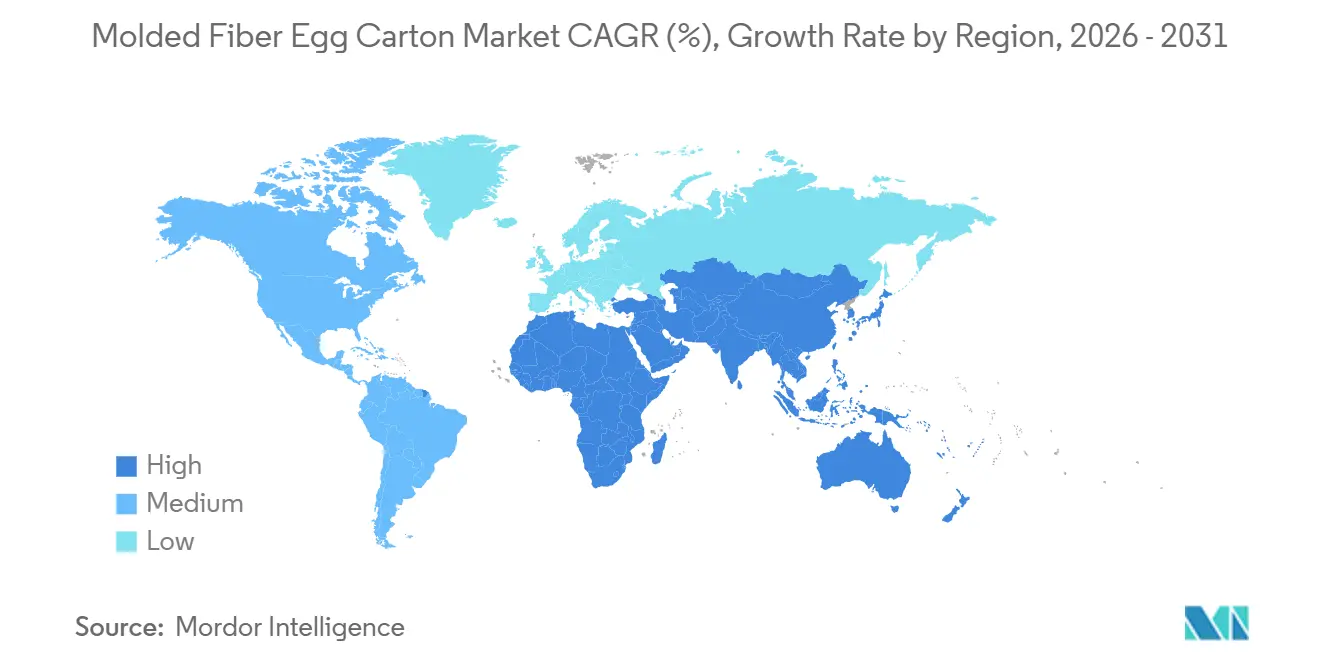

- By geography, North America held 34.91% of the molded fiber egg carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Molded Fiber Egg Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Plastic Phaseout and Circular Packaging Mandates | +2.1% | Global, concentrated in the EU and North America | Medium term (2-4 years) |

| Growing Egg Consumption and Poultry Output | +1.8% | Asia-Pacific, Africa, South America | Long term (≥ 4 years) |

| Premiumization of Organic, Free-Range, And Cage-Free Eggs | +1.2% | North America, the EU, Australia, and New Zealand | Medium term (2-4 years) |

| Retail Preference for Recyclable and Compostable Shelf-Ready Packs | +0.9% | Global, North America, and the EU are leading | Short term (≤ 2 years) |

| Auto-Packer Compatibility Becomes a Procurement Criterion | +0.5% | North America and the EU, early adoption in the Asia-Pacific | Medium term (2-4 years) |

| Forever-Chemical-Free Food-Contact Compliance Favors Qualified Fiber Formats | +0.3% | EU primary, North America, and select US states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Plastic Phaseout and Circular Packaging Mandates

Regulation (EU) 2025/40 enters into full force on August 12, 2026, and establishes binding recyclability and PFAS rules for food-contact packaging across the EU.[1]European Parliament and Council of the European Union, “Regulation (EU) 2025/40 of the European Parliament and of the Council of 19 December 2024 on Packaging and Packaging Waste,” Official Journal of the European Union, eur-lex.europa.eu The same regulation states that packaging with a recyclability grade below C cannot be placed on the EU market from January 1, 2030. That deadline is changing conversion decisions now because producers cannot afford to keep investing in formats that may lose market access within a normal equipment cycle. The direction of regulation in North America has also moved toward tighter limits on foam and other low-recyclability materials, which shortens the practical runway for those formats in egg packaging. In the molded fiber egg carton market, the advantage is not only environmental positioning; fiber formats usually require less reformulation than plastic or coated paperboard when PFAS-related rules tighten. This is making compliance readiness a direct purchasing factor in the molded fiber egg carton market, especially for suppliers serving retailers and brand owners that cannot risk packaging changes close to enforcement dates.

Growing Egg Consumption and Poultry Output

The molded fiber egg carton market continues to benefit from rising egg output in major producing countries where commercial packing systems are expanding. India’s egg production is forecast to grow 5% in marketing year 2026, while Brazil is projected to add 3% output in the same period. Global poultry meat production is forecast to reach 110.7 million metric tons in 2026, up 3% from 2025, reflecting broader poultry capacity expansion in countries such as China and Brazil. As poultry operations scale, informal reuse packaging becomes less workable in supermarket and export supply chains that need standardized stacking, handling, and pack integrity. That shift raises baseline demand in the molded fiber egg carton market, especially in South Asia and South America, where integrated egg operations are adding throughput. In the molded fiber egg carton market, poultry expansion supports carton demand not only by increasing egg production but also by advancing formal packing standards.

Premiumization of Organic, Free-Range, and Cage-Free Eggs

The molded fiber egg carton market is also being reshaped by the move toward cage-free, free-range, and organic eggs. In the United States, 40% of the laying flock was operating in cage-free systems as of 2025. In the EU, cage-free and barn-system hens together accounted for 55.2% of total housing by 2024, and Germany added 634,000 free-range places that year. Those production changes influence packaging needs because specialty eggs are sold with stronger claims around origin, welfare, and freshness, which increases the value of print quality and shelf presentation. Specialty cartons also need better fit and more reliable closure performance when egg size and shell appearance become less uniform across premium flocks. This keeps the molded fiber egg carton market oriented toward higher-specification cartons that can support branding and protection.

Retail Preference for Recyclable and Compostable Shelf-Ready Packs

Retailers are increasingly treating recyclability, compostability, and documentation as standard procurement requirements instead of optional extras. Hartmann’s premium molded fiber cartons for Burnbrae Farms’ Island Gold brand were nominated for 2 PAC Global Awards in March 2026, showing that retailers now expect egg packs to communicate sustainability and product positioning at the shelf. MyPak Packaging states that 100% machinability on customer packing lines is a core product target for the Australia and New Zealand supply, indicating that line performance is being judged alongside environmental claims. Shelf-ready packs that run smoothly through denesting, filling, and closure systems help retailers reduce handling losses and improve presentation. That favors suppliers that can combine verified sustainable positioning with reliable auto-packer performance. In the molded fiber egg carton market, retail requirements are therefore concentrating demand around converters that can prove both sustainability and execution quality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Recovered Fiber and Drying Energy Costs | -1.2% | Global, North America, and the EU most acute | Short term (≤ 2 years) |

| Competition from Low-Cost Plastic, Foam, and Corrugated Alternatives | -0.9% | Asia-Pacific, South America, Africa | Long term (≥ 4 years) |

| Recycled-Fiber Chemical Migration and Traceability Burden | -0.5% | EU primary, North America secondary | Short term (≤ 2 years) |

| Avian Influenza-Led Layer Flock Volatility Distorts Carton Demand Planning | -0.3% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Recovered Fiber and Drying Energy Costs

The molded fiber egg carton market remains exposed to swings in recovered fiber availability and drying energy costs. Traditional wet-process production depends on steady pulp input and heat-intensive drying, so short-term margins can move more sharply than end demand. PulPac’s commercial rollout with Nippon Molding was positioned on materially lower energy use than conventional wet forming, underscoring how important energy intensity remains across the current production base. Producers without long-term recycled fiber coverage are more vulnerable when raw material markets tighten or freight costs rise. These pressures are hardest to overcome in high-volume contracts, where egg producers focus on carton cost per unit. As a result, the molded fiber egg carton market can face margin compression even when regulatory and retail conditions continue to support volume growth.

Competition from Low-Cost Plastic, foam, and Corrugated Alternatives

The molded fiber carton market still faces price competition from foam, plastic, and corrugated alternatives in cost-sensitive regions. EPS trays and corrugated packs can remain attractive where poultry operators prioritize upfront packaging cost over environmental credentials. This is especially relevant in industrial channels, where stacking strength and freight efficiency often matter more than shelf appearance or brand communication. Solenis reported that its PFAS-free barrier solution for molded fiber met FDA food-contact requirements at a cost premium of less than 10% compared with conventional PFAS-treated articles, indicating the compliance gap is narrowing but not fully closed. Conversion, therefore, moves faster in countries with binding recyclability or chemical restrictions and slower in those with limited enforcement. That leaves part of the molded fiber egg carton market exposed to substitution risk in emerging markets, even as premium channels continue to convert to fiber.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Standard Cartons Sustain Volume, Specialty Formats Lift Margins

Standard Egg Cartons held 64.83% of the molded fiber egg carton market share in 2025, reflecting their strong position in commodity egg channels where cost per unit and compatibility with legacy packing lines matter most. Their fit with both transfer-molded and thermoformed production, along with familiar recycled-fiber sourcing, keeps volumes steady across organized retail. Specialty Egg Cartons for cage-free, organic, free-range, and pasture-raised eggs are projected to grow at a 7.73% CAGR through 2026-2031, indicating where mix improvement is developing.

Hartmann’s premium work on Burnbrae Farms’ Island Gold packaging illustrates how specialty molded fiber cartons are increasingly being used as brand assets rather than simple commodity inputs.[2]Hartmann North America, “Burnbrae Farms Nominated for Two PAC Global Awards,” Hartmann Packaging, hartmann-packaging.com The cage-free transition is also pushing higher baseline carton requirements, not only more units. Eggs from these systems can show greater variation in size and shell appearance, underscoring the need for better nest tolerance and more secure closure performance. That gap favors higher-specification fiber formats that can protect the product while carrying stronger on-pack communication.

By Capacity: Single-Serve Anchors Retail, Bulk Formats Power Industrial Growth

The 19 to 30 Eggs segment is projected to grow at 8.12% CAGR through 2026-2031, making it the fastest-rising capacity band in the molded fiber egg carton market. The segment is supported by industrial packing expansion in Asia-Pacific and South America, where integrated poultry operators are running higher-throughput lines. Big Herdsman markets intelligent tray packers capable of 36,000 to 72,000 eggs per hour, which shows the scale at which large-format packing systems are now being deployed. Shipped a 5,000-units-per-hour automated egg tray production line to India in January 2026, reinforcing the pace of packaging infrastructure investment in South Asia.

The Up to 6 Eggs segment held 56.75% of the 2025 market value, supported by single-serve and small-household purchasing patterns in North America and Europe. The 7 to 12 Eggs format remains the mainstream retail and foodservice pack, while 13 to 18 Eggs serves larger households and club retail needs. Larger pack sizes also offer better fiber cost efficiency per egg, which aligns converter economics with rising industrial demand. That combination keeps the molded fiber egg carton market tilted toward bulk formats, where scale, automation, and freight efficiency increasingly shape purchasing decisions.

By Molded Fiber Type: Transfer Molded Leads on Scale, Thermoformed Fiber Advances on Performance

Transfer Molded formats held 39.61% of the 2025 market value, giving them the leading position in the molded fiber egg carton market because they remain cost-efficient at high-volume run rates. Their established manufacturing base across major regions and their suitability for standard trays support broad adoption in value-focused supply contracts. Thermoformed Fiber is projected to grow at 7.94% CAGR through 2026-2031, supported by smoother surfaces, better dimensional control, and stronger print performance in premium retail formats. Those attributes also matter on auto-packer lines that need consistent denesting and closure behavior.

Nippon Molding completed Japan’s first commercial Dry Molded Fiber installation using PulPac Modula technology in April 2025, signaling that dry-forming is moving from pilot work into real production. The company positioned the process on materially lower energy use than conventional wet pressing and tunnel drying, which could improve mid-market production economics as adoption expands. PFAS-free compliance, better finish quality, and precision forming are increasingly converging within a single product family, giving advanced fiber formats a broader commercial role. In the molded fiber egg carton industry, this segment is where compliance needs and premium positioning are overlapping most clearly.

By Application: Retail Leads Value Share, Industrial Commands Faster Growth

Retail held 37.93% of the 2025 market value, while Industrial is projected to expand at 8.27% CAGR from 2026 to 2031, making the application mix one of the clearest growth differentiators in the molded fiber egg carton market. Retail demand stays supported by branded shelf presentation, cage-free messaging, and the need for packs that can move cleanly through organized retail distribution. Industrial demand is rising faster as bulk packing stations, export-oriented processors, and hatchery operations invest in higher-throughput equipment and standardized formats. Global poultry meat production is forecast to reach 110.7 million metric tons in 2026, up 3% from 2025, reflecting the broader poultry investment cycle that feeds industrial packaging needs.

Commercial channels such as bakeries, foodservice, and food processing remain steady buyers as cage-free sourcing commitments widen. These buyers value supply reliability and stack performance more than premium shelf appearance, which keeps format requirements distinct from retail. As poultry operations scale in emerging markets, demand is shifting toward cartons that fit automated packers and bulk-handling systems. That makes industrial expansion additive to retail premiumization rather than a replacement for it in the molded fiber egg carton market.

Geography Analysis

North America held 34.91% of the 2025 market value, giving it the largest share of the molded fiber egg carton market that year. Hartmann said its cumulative North American investments exceeded USD 100 million across Rolla, Missouri, and Brantford, Ontario, from 2024 through 2027, with Phase 1 completed and Phase 2 underway in early 2026. Huhtamäki strengthened its southeastern US position through the April 2025 acquisition of Zellwin Farms Company for USD 18 million, adding a business with annual net sales of around USD 20 million.[3]Huhtamäki Oyj, “Huhtamaki Acquires Zellwin Farms Company,” Huhtamäki, huhtamaki.com HPAI-related flock losses created planning volatility through 2025, while Target maintained a 57-61% cage-free unit egg sales goal for end-2026, and Mexico’s egg production is forecast to reach 66 billion units in marketing year 2026, which keeps regional carton demand supported.

Europe combines large-volume egg consumption with the most demanding compliance environment for carton converters. Germany consumed 20.8 billion eggs in 2024, and free-range housing expanded by 5.4% that year, adding 634,000 new places. Regulation (EU) 2025/40 takes full effect on August 12, 2026, and its recyclability and PFAS provisions are creating barriers to non-compliant packaging across the region. In South America, Brazil’s egg production is projected to grow 3% in marketing year 2026, which supports local demand for molded pulp cartons tied to expanding poultry output.

Asia-Pacific is the fastest-growing region, with a projected CAGR of 7.66% from 2026 to 2031 in the molded fiber egg carton market. China’s egg production is forecast at 682 billion units in marketing year 2026, while India is forecast at 156 billion units with 5% growth, making the region the main volume base for future carton demand. Nippon Molding’s DMF rollout in Japan points to rising demand for more resource-efficient fiber packaging in advanced Asian markets. MyPak supplies PFAS-free and BRC-certified molded fiber packs across Australia and New Zealand, which shows how premium and compliance-led demand is also deepening in Oceania. Middle East and Africa remain earlier-stage opportunities where poultry formalization, urban retail growth, and upgraded cold-chain systems are steadily improving the case for standardized molded fiber cartons.

Competitive Landscape

The molded fiber egg carton market remains fragmented, with Hartmann Packaging and Huhtamäki operating as the clearest tier-1 suppliers across North America and Europe, while many regional converters remain smaller and more localized. Hartmann reported 2024 revenue of DKK 3,810 million (USD 554 million), up from DKK 3,494 million (USD 508 million) in 2023, and ROIC improved to 27.9% from 16.9%. Huhtamäki’s Fiber Packaging segment posted EUR 50.4 million (USD 54 million) in adjusted EBIT for 2025, up 16% from 2024, driven by comparable net sales growth of 8%. Those results suggest that scale, operational discipline, and quality credentials still matter more than simple volume in the molded fiber egg carton market.

Hartmann used 2025 and 2026 to deepen capacity, announcing a new production line and warehouse at Tønder in March 2026 and continuing North American expansion after completing Phase 1 and starting Phase 2. Huhtamäki took a bolt-on route with its April 2025 acquisition of Zellwin Farms Company, which widened its access to southeastern US egg producers. These moves show that leading suppliers are trying to secure regional proximity, customer relationships, and machine-ready capacity before growth markets tighten. The molded fiber egg carton market is therefore seeing competition play out through capacity placement and execution quality rather than headline price alone.

Technology is becoming another dividing line between leaders and followers. Nippon Molding’s commercial adoption of PulPac dry molded fiber technology indicates that lower-water and lower-energy processes are moving into commercial use for trays and related food packaging.[4]PulPac, “Nippon Molding Accelerates Dry Molded Fiber Rollout in Japan with Successful Machine Installation,” PulPac, pulpac.com That matters because producers that improve energy efficiency and forming precision can compete more effectively in both premium retail and compliance-driven formats. Regional specialists still have room to grow in South Asia, Africa, and parts of South America where local carton supply trails poultry expansion. At the same time, some large poultry operators are moving toward internal packaging capability, which creates a displacement risk for regional converters that lack long-term contracts or a differentiated product offer.

Molded Fiber Egg Carton Industry Leaders

Hartmann Packaging A/S

Huhtamäki Oyj

CKF Inc.

Omni-Pac Ekco GmbH

Dispak Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Hartmann Packaging's Denmark factory announced investment in a new production line and warehouse to increase capacity, marking continued infrastructure expansion at a 60-year-old flagship site.

- February 2026: Hartmann North America announced completion of Phase 1 expansion and initiation of Phase 2 at IPPE 2026 in Atlanta, with cumulative North American investments exceeding USD 100 million across Rolla, Missouri and Brantford, Ontario from 2024 through 2027.

- January 2026: AGICO shipped a 5,000-units-per-hour automated egg tray production line to a customer in India, signaling accelerating capital deployment in South Asian molded fiber egg packaging infrastructure and growing demand from the region's industrializing poultry sector.

- April 2025: Huhtamäki Oyj acquired Zellwin Farms Company, a Zellwood, Florida-based molded fiber egg carton and egg flat producer serving Southeastern US egg producers, for an enterprise value of USD 18 million, adding approximately USD 20 million in annual net sales and expanding Huhtamäki's North American manufacturing footprint.

Global Molded Fiber Egg Carton Market Report Scope

The scope of the report includes an in-depth analysis of the molded fiber egg carton market, covering production, distribution, and consumption. Molded fiber egg cartons are biodegradable and eco-friendly packaging solutions designed to protect eggs during transportation and storage. The study examines market trends, growth drivers, challenges, and opportunities, providing insights into the competitive landscape and key market players.

The Molded Fiber Egg Carton Market Report is Segmented by Product Type (Standard Egg Cartons, and Specialty Egg Cartons), Capacity (Up to 6 Eggs, 7 to 12 Eggs, 13 to 18 Eggs, and 19 to 30 Eggs), Molded Fiber Type (Transfer Molded, Thermoformed Fiber, and Thick-wall Molded Fiber), Application (Retail, Commercial, and Industrial), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Standard Egg Cartons |

| Specialty Egg Cartons |

| Up to 6 Eggs |

| 7 to 12 Eggs |

| 13 to 18 Eggs |

| 19 to 30 Eggs |

| Transfer Molded |

| Thermoformed Fiber |

| Thick-wall Molded Fiber |

| Retail |

| Commercial |

| Industrial |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Standard Egg Cartons | ||

| Specialty Egg Cartons | |||

| By Capacity | Up to 6 Eggs | ||

| 7 to 12 Eggs | |||

| 13 to 18 Eggs | |||

| 19 to 30 Eggs | |||

| By Molded Fiber Type | Transfer Molded | ||

| Thermoformed Fiber | |||

| Thick-wall Molded Fiber | |||

| By Application | Retail | ||

| Commercial | |||

| Industrial | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size and forecast for the molded fiber egg carton market?

The molded fiber egg carton market was valued at USD 1.77 billion in 2025 and stood at USD 1.98 billion in 2026. It is projected to reach USD 2.77 billion by 2031 at a 6.97% CAGR.

Which product category leads carton demand for eggs?

Standard Egg Cartons led demand with 64.83% of 2025 value because they remain the default format in commodity egg channels and organized retail.

Which application is growing the fastest through 2031?

Industrial applications are projected to grow at 8.27% CAGR through 2031 as bulk packing stations and integrated poultry processors invest in automated lines and standardized formats.

Why are retailers moving toward molded fiber packs?

Retailers are asking for recyclable, compostable, shelf-ready packs that also run reliably on filling lines. That favors fiber formats with better sustainability documentation and machinability.

Which region is expanding the fastest in terms of egg carton demand?

Asia-Pacific is the fastest-growing region with a projected 7.66% CAGR through 2031, supported by very large egg production bases in China and India and rising packaging investment.

What are the main challenges facing suppliers of molded fiber egg cartons?

The main pressures come from volatile recovered fiber and drying energy costs, along with low-cost competition from foam, plastic, and corrugated alternatives in price-sensitive markets.

Page last updated on: