Proteases Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.23 Billion |

| Market Size (2031) | USD 3.61 Billion |

| Growth Rate (2026 - 2031) | 10.05% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

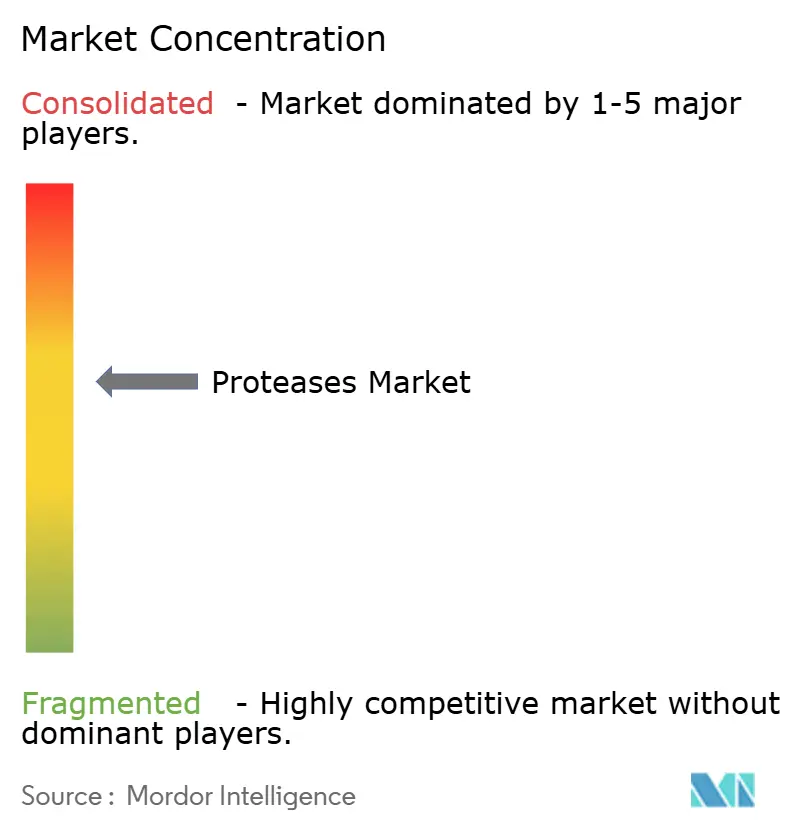

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Proteases Market Analysis by Mordor Intelligence

The protease enzymes market size was valued at USD 2.03 billion in 2025 and estimated to grow from USD 2.23 billion in 2026 to reach USD 3.61 billion by 2031, at a CAGR of 10.05% during the forecast period (2026-2031). This growth is driven by increased enzyme adoption across food, pharmaceutical, feed, and industrial applications. The market expansion is supported by sustainability requirements, advances in precision fermentation, and artificial intelligence applications in enzyme engineering that reduce development time. Research and development collaborations in North America, Europe, and Asia-Pacific are creating specialized market segments, including protein hydrolysates for sports nutrition and cell-culture enzymes for biologics production. Despite high regulatory compliance costs, the implementation of continuous processing platforms and cell-free expression systems is reducing production costs.

Key Report Takeaways

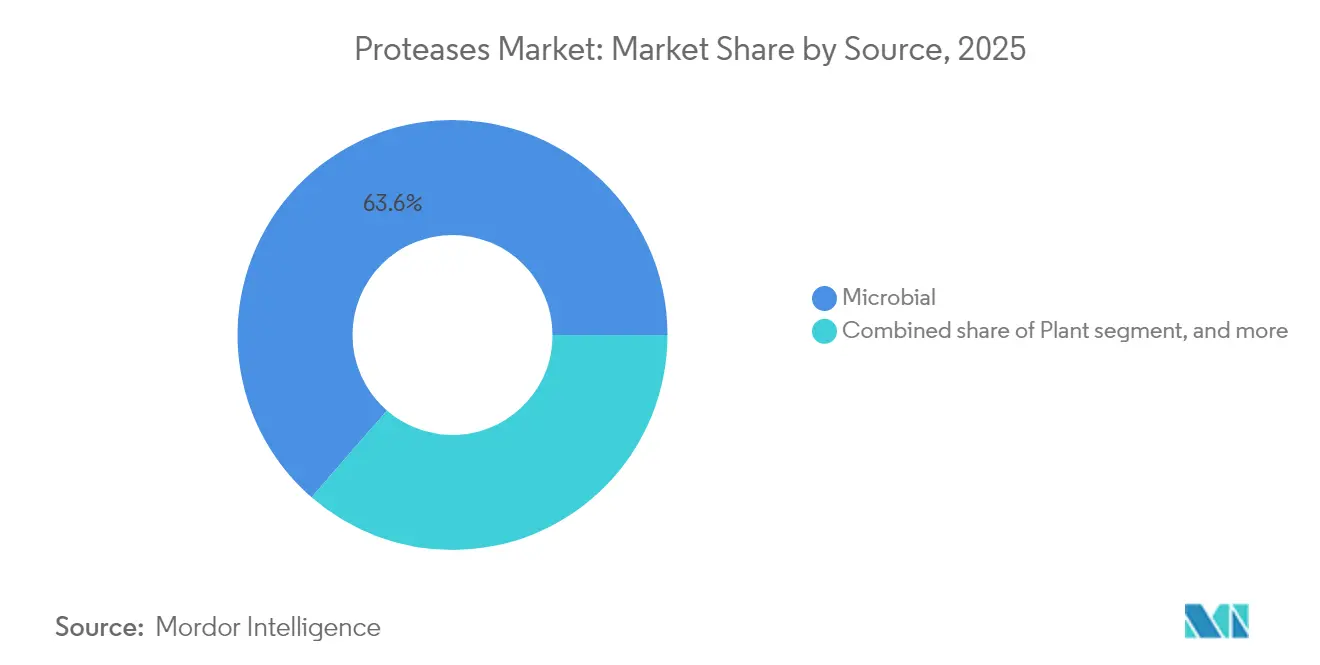

- By source, microbial proteases held 63.62% of the protease market share in 2025, while plant sources are set to expand at a 10.42% CAGR through 2031.

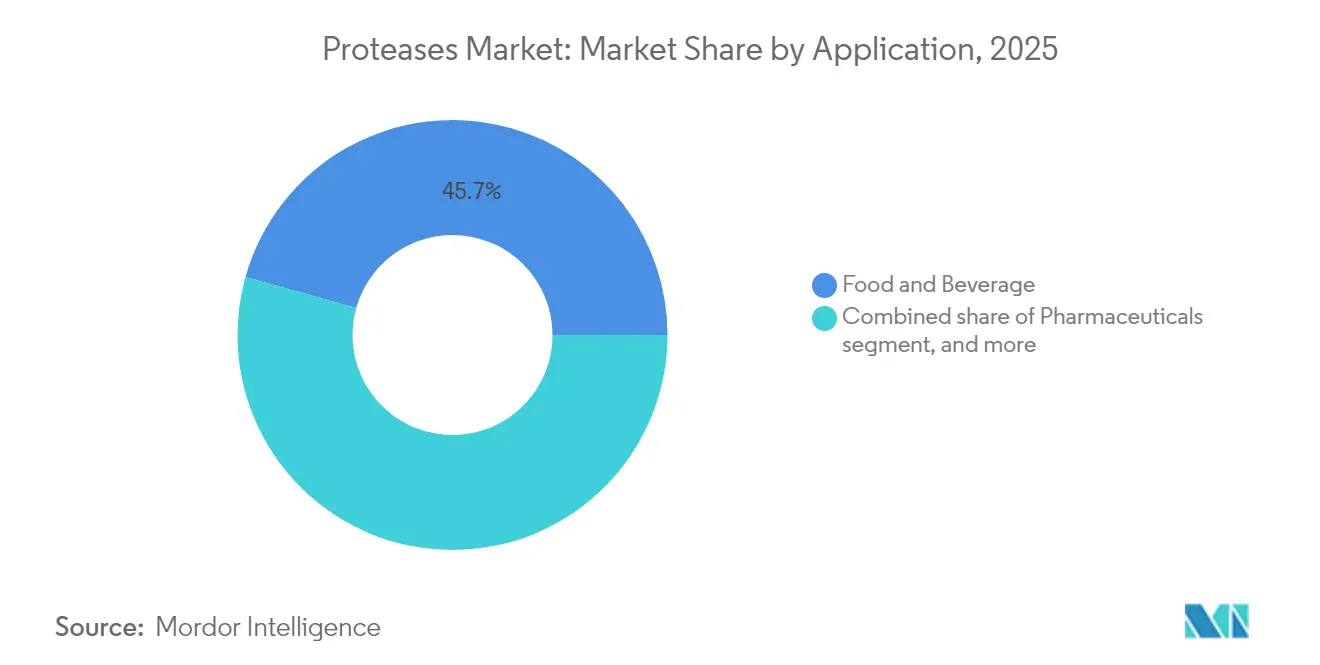

- By application, food and beverage accounted for 45.65% of the protease enzymes market size in 2025, while pharmaceuticals exhibited the highest 11.05% CAGR through 2031.

- By geography, North America dominated with 33.10% revenue share in 2025; Asia-Pacific is advancing at a 10.74% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Proteases Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of protein-hydrolysate demand in functional foods and beverages | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Growing inclination toward specialty and sustainable ingredients | +1.5% | Global, led by Europe regulatory frameworks | Long term (≥ 4 years) |

| Strategic investments by market players | +1.2% | North America and Asia-Pacific core markets | Short term (≤ 2 years) |

| Technological advancements in enzyme engineering and bioprocessing | +2.1% | Global, with research and development hubs in the United States, Europe, and China | Long term (≥ 4 years) |

| Increasing use in animal feed | +1.4% | Asia-Pacific and South America focus | Medium term (2-4 years) |

| Growing sports nutrition market driving protease adoption | +1.0% | North America and Europe, expanding toAsia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Protein-Hydrolysate Demand in Functional Foods and Beverages

The growing demand for protein hydrolysates in functional foods and beverages drives the protease market growth, as these enzymes break down proteins into bioactive peptides that improve digestibility, solubility, and nutritional value. Consumer preferences significantly influence this trend, with 72% of consumers choosing functional beverages with health benefits and 44% selecting products with natural ingredients in 2023, as per the Glanbia Nutritionals report[1]Source: Glanbia Nutritionals, "European Functional Beverage Market Insights for 2023," glanbianutritionals.com. In response, manufacturers have incorporated natural and clean-label protease solutions. The increasing popularity of protein-enriched drinks for muscle recovery, weight management, and wellness, along with enzyme technology improvements that minimize bitterness and enhance amino acid profiles, continues to drive demand. The combination of heightened health consciousness and expanding functional beverage consumption increases protease requirements in the food and beverage industry.

Growing Inclination Toward Specialty and Sustainable Ingredients

Consumer preference for sustainable and specialty ingredients is reshaping enzyme procurement strategies across food and beverage manufacturers, with plant-based and microbially-derived proteases gaining market share over animal-derived alternatives. Proteases sourced from these sustainable origins support clean-label, natural, and environmentally friendly formulations, aligning with the growing demand for specialty ingredients that promote health, wellness, and ethical considerations. According to the International Food Information Council 2024 Report, 36% of U.S. consumers stated that products labeled as natural or organic enhance their confidence in safety, further highlighting the importance of transparency and sustainability in food production[2]Source: "2024 IFIC Food & Health SURVEY,"International Food Information Council," ific.org. Additionally, regulatory frameworks such as the European Commission's biotechnology strategy, which emphasizes bio-based product development through lifecycle assessment frameworks and potential bio-content requirements, are creating favorable conditions for enzymatic processing solutions[3]Source: EUROPEAN COMMISSION, "COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT, THE COUNCIL, THE EUROPEAN ECONOMIC AND SOCIAL COMMITTEE AND THE COMMITTEE OF THE REGIONS," europa.eu. Collectively, these consumer trends and regulatory tailwinds are driving increased adoption of proteases in the food and beverage industry.

Strategic Investments by Market Players

The protease enzymes market is experiencing significant consolidation through mergers and capacity expansions. The USD 11.3 billion merger between Novozymes and Chr. Hansen formed Novonesis, a EUR 3.7 billion biosolutions company with expanded research and development capabilities and global presence. Companies are investing in precision fermentation infrastructure and AI-powered enzyme discovery platforms to address the limitations of traditional enzyme development timeframes. Major capital investments demonstrate industry confidence in the biologics sector, which drives enzyme demand. The market is characterized by strategic partnerships between enzyme producers and end-user industries, creating integrated value chains that ensure supply security and facilitate the development of application-specific enzyme solutions. Investment decisions are subject to increased scrutiny regarding sustainability impact and regulatory compliance, particularly in regions with strict environmental regulations.

Technological Advancements in Enzyme Engineering and Bioprocessing

Technological advancements in enzyme engineering and bioprocessing drive growth in the protease market through the development of efficient, stable, and specialized enzymes for diverse applications. Protein engineering, directed evolution, and immobilization techniques enhance protease specificity, thermal and pH stability, while reducing off-flavors in food and beverage applications. Improved bioprocessing technologies, including optimized fermentation and scalable production methods, increase yield and decrease production costs, making proteases more accessible to manufacturers. These technological developments enable product innovation, support clean-label and functional formulations, and expand protease applications across food, beverage, pharmaceutical, and industrial segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex regulatory compliance requirements | -1.5% | Global, most stringent in Europe and North America | Long term (≥ 4 years) |

| Allergenic-safety perception among food processors | -0.8% | Europe and North America primarily | Medium term (2-4 years) |

| High production costs impede market growth | -1.2% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Limited enzyme stability and shelf life | -0.9% | Global, critical in tropical regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complex Regulatory Compliance Requirements

Regulatory frameworks for enzyme applications differ across regions, creating compliance challenges that affect smaller enzyme producers and delay market entry for new protease variants. The FDA's GRAS approval process for food enzymes requires extensive safety documentation and extends development timelines by 12-18 months. The European Food Safety Authority implements stricter evaluation criteria, requiring additional toxicological studies. China's evolving regulatory system for novel food ingredients creates further complexity for companies seeking global market access, with recent amendments to food standards codes mandating comprehensive safety assessments for genetically modified enzyme preparations. Pharmaceutical applications face more rigorous requirements, as enzyme-based therapeutics must undergo clinical trials and comply with Good Manufacturing Practices standards. Companies must demonstrate enzyme purity, absence of microbial contaminants, and consistent activity levels across production batches. To address these requirements, companies are investing in regulatory affairs expertise and implementing dedicated quality systems. Compliance costs typically account for 15-20% of total development expenses for new enzyme products.

High Production Costs Impede Market Growth

Enzyme production costs remain high due to complex fermentation processes, downstream purification requirements, and quality control measures for food and pharmaceutical applications. Raw material costs, specifically specialized growth media and purification reagents, account for 40-60% of total production expenses, with price fluctuations affecting profit margins and pricing strategies. Energy-intensive fermentation and purification processes significantly impact operational costs, especially as sustainability requirements increase the adoption of renewable energy sources. The scale-up from laboratory to commercial production requires substantial capital investments in specialized bioreactor systems and downstream processing equipment, with payback periods exceeding 5 years in many cases. Competition from chemical alternatives in certain applications constrains pricing flexibility, requiring enzyme producers to demonstrate clear value propositions beyond environmental benefits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Microbial Dominance Drives Scalability

Microbial sources hold a 63.62% market share in 2025, as fermentation-based protease production offers better scalability and consistency compared to plant and animal extraction methods. Fungal and bacterial platforms allow precise control of enzyme properties through genetic modification, while utilizing existing bioprocessing infrastructure and regulatory pathways to maintain cost efficiency. Plant-derived proteases show the highest growth rate at 10.42% CAGR through 2031, supported by clean-label trends and increased consumer demand for natural food ingredients. Bromelain from pineapple and papain from papaya maintain commercial importance, despite supply chain uncertainties and seasonal availability limitations.

Animal-derived proteases experience reduced demand due to religious dietary restrictions, sustainability issues, and regulations concerning bovine spongiform encephalopathy prevention. This segment's market share decreases as microbial fermentation through synthetic biology produces animal-equivalent enzymes with identical functionality but reduced supply chain risks. New microbial platforms using extremophile organisms generate interest for their thermostable proteases suited to high-temperature industrial processes, though high production costs and lengthy regulatory approvals limit commercial implementation.

By Application: Food Processing Leads Pharmaceutical Growth

Food and beverage applications hold a dominant 45.65% market share in 2025, encompassing dairy processing, baking, meat tenderization, and protein hydrolysate production for functional foods. The pharmaceutical segment demonstrates the highest growth rate at 11.05% CAGR, driven by enzyme-based manufacturing processes and therapeutic applications. Biopharmaceutical manufacturing utilizes proteases for cell culture harvest, protein purification, and analytical quality control, while single-use bioprocessing systems increase demand for specialized enzyme formulations. Animal feed applications show significant growth in Asia-Pacific markets, where proteases enhance protein digestibility and minimize anti-nutritional factors in plant-based feed formulations.

Industrial applications in detergents, leather processing, and waste treatment represent established market segments, with growth constrained by synthetic alternatives and environmental regulations. The cosmetics and personal care segment demonstrates growth opportunities, particularly in exfoliation products and hair care formulations, though market entry faces barriers due to consumer safety testing requirements. Research investment focuses on emerging applications in plastic recycling and bioremediation, where engineered proteases show capability in degrading synthetic polymers and environmental contaminants.

Geography Analysis

North America holds 33.10% market share in 2025, driven by advanced biotechnology infrastructure, strict food safety regulations supporting enzymatic processing, and established pharmaceutical manufacturing capabilities. The region's strong intellectual property protection and substantial research and development investment in enzyme engineering reinforce its market position. Asia-Pacific exhibits the highest growth rate at 10.74% CAGR, attributed to expanding biopharmaceutical manufacturing capacity, government biotechnology initiatives, and increased enzymatic processing adoption in food production.

China's regulatory framework continues to adapt to accommodate enzyme applications in novel food ingredients, while India's pharmaceutical sector implements enzymatic processes for efficient production of generic drugs and biosimilars. Europe maintains consistent growth in its mature markets, with environmental regulations promoting bio-based processing solutions and circular economy practices. The European Commission's biotechnology strategy supports protease enzyme development, though strict regulatory requirements affect the timeline for new product launches.

South America, the Middle East, and Africa present growth opportunities in animal feed and food processing applications. These regions show potential for protease applications in livestock nutrition, aquaculture feed formulation, and food manufacturing processes. However, the market expansion faces constraints due to insufficient biotechnology infrastructure, including limited research facilities and production capabilities, as well as underdeveloped regulatory frameworks that slow down product approvals and market entry in these regions.

Competitive Landscape

The protease market shows moderate consolidation, with competition balanced between established biotechnology companies and specialized enzyme producers focusing on niche applications. This market structure reflects the diverse nature of enzyme applications across industries and the specialized expertise required for different market segments. The competitive landscape encompasses both global players with broad portfolios and regional companies targeting specific applications or geographical markets.

The industry's consolidation stems from requirements for economies of scale in research and development investment, regulatory compliance, and global market access, while smaller companies concentrate on specialized applications and new enzyme variants through biotechnology platforms. This consolidation trend indicates the increasing importance of scale and resource optimization in maintaining competitive advantages. The formation of larger entities through mergers and acquisitions enables companies to pool resources, share technological expertise, and enhance their market presence while maintaining operational efficiency.

Companies are adopting technology-driven differentiation as their main competitive strategy, investing in artificial intelligence, machine learning, and synthetic biology platforms to expedite enzyme development and reduce time-to-market for customized solutions. New opportunities are emerging in applications like plastic recycling, where engineered proteases show promise in synthetic polymer degradation, and in precision fermentation systems for alternative protein production in food applications. This technological advancement, coupled with stringent regulatory requirements, creates barriers to entry while encouraging established players to maintain their competitive edge through continuous innovation and quality improvements.

Proteases Industry Leaders

-

International Flavors & Fragrances, Inc.

-

BASF SE

-

DSM-Firmenich AG

-

Novonesis Group

-

Associated British Foods PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2024: Novozymes and Chr. Hansen has completed their merger, resulting in the formation of Novonesis, a global biosolutions company with 10,000 employees, a network of research and development and application centers, and operations across 30 industries. The company's portfolio is divided between promoting healthier lifestyles and improved food products, and minimizing chemical use while supporting climate-neutral practices, combining Novozymes' enzyme and microbial expertise with Chr. Hansen's ingredient systems for food, nutrition, pharmaceutical, and agricultural sectors.

- October 2023: Azelis expanded its partnership with DSM-Firmenich, making Azelis India the exclusive distributor of DSM-Firmenich's food enzymes and cultures portfolio in India. The distribution rights cover dairy cultures, dairy enzymes, dairy test kits, and bakery enzymes.

- March 2023: Kemin Indonesia launched Kemzyme Protease, a multi-protease enzyme solution for animal feed optimization. The product addresses the issue of undigested feed protein, which accounts for approximately 20% of feed protein and results in inefficient nutrient utilization and increased nitrogen excretion. Kemzyme Protease combines acid, neutral, and alkaline proteases to ensure compatibility with various feed ingredients. Its patented enteric coating maintains stability during feed processing and enables targeted release in the gastrointestinal tract, improving protein utilization and reducing environmental impact.

Global Proteases Market Report Scope

Protease is an enzyme that catalyzes the hydrolysis of peptide bonds present in proteins and has many functions, including industrial and medical purposes, like extracting gums, processing food, and treating inflammation. The protease market is segmented by source, application, and geography. By source, the market is segmented into animal (which is further segmented into trypsin, pepsin, renin, and other animal sources), plant (which is further segmented into papain, bromelain, and other plant sources), and microbial, which is further segmented into alkaline protease, acid protease, and neutral protease. By application, the market is segmented into food and beverage (which is further segmented into dairy, bakery, beverages, meat and poultry, and infant formula), pharmaceuticals, animal feed, and other applications. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The market sizing has been done in value terms (USD) for all the abovementioned segments.

| Animal |

| Plant |

| Microbial |

| Food and Beverage | Dairy |

| Bakery | |

| Beverages | |

| Meat and Poultry | |

| Others | |

| Pharmaceuticals | |

| Animal Feed | |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Spain |

| United Kingdom | |

| France | |

| Germany | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Singapore | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| United Arab Emirates | |

| Saudi Arabia | |

| Rest of Middle East and Africa |

| Source | Animal | |

| Plant | ||

| Microbial | ||

| Application | Food and Beverage | Dairy |

| Bakery | ||

| Beverages | ||

| Meat and Poultry | ||

| Others | ||

| Pharmaceuticals | ||

| Animal Feed | ||

| Other Applications | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Spain | |

| United Kingdom | ||

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Singapore | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| United Arab Emirates | ||

| Saudi Arabia | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current valuation of the protease enzymes market and its expected growth?

The market is valued at USD 2.23 billion in 2026 and is projected to reach USD 3.61 billion by 2031 at a 10.05% CAGR.

Which source category leads global protease demand?

Microbial sources dominate with 63.62% share in 2025, benefiting from fermentation scalability and regulatory precedence.

Which application segment is expanding fastest through 2031?

Pharmaceutical uses are advancing at an 11.05% CAGR as biologics production and enzyme-based therapeutics gain ground.

Which region is growing most rapidly for protease enzymes?

Asia-Pacific shows the highest 10.74% CAGR thanks to expanding biopharma capacity and supportive government policies.

Page last updated on: