Tannin Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

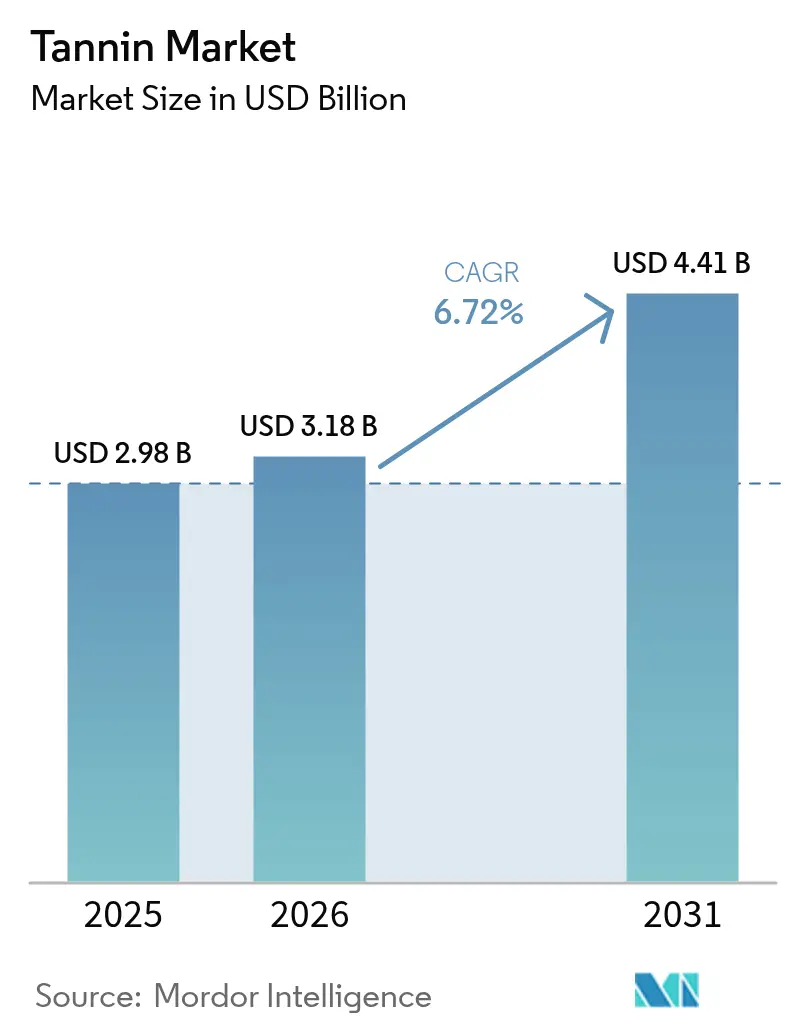

| Market Size (2026) | USD 3.18 Billion |

| Market Size (2031) | USD 4.41 Billion |

| Growth Rate (2026 - 2031) | 6.72% CAGR |

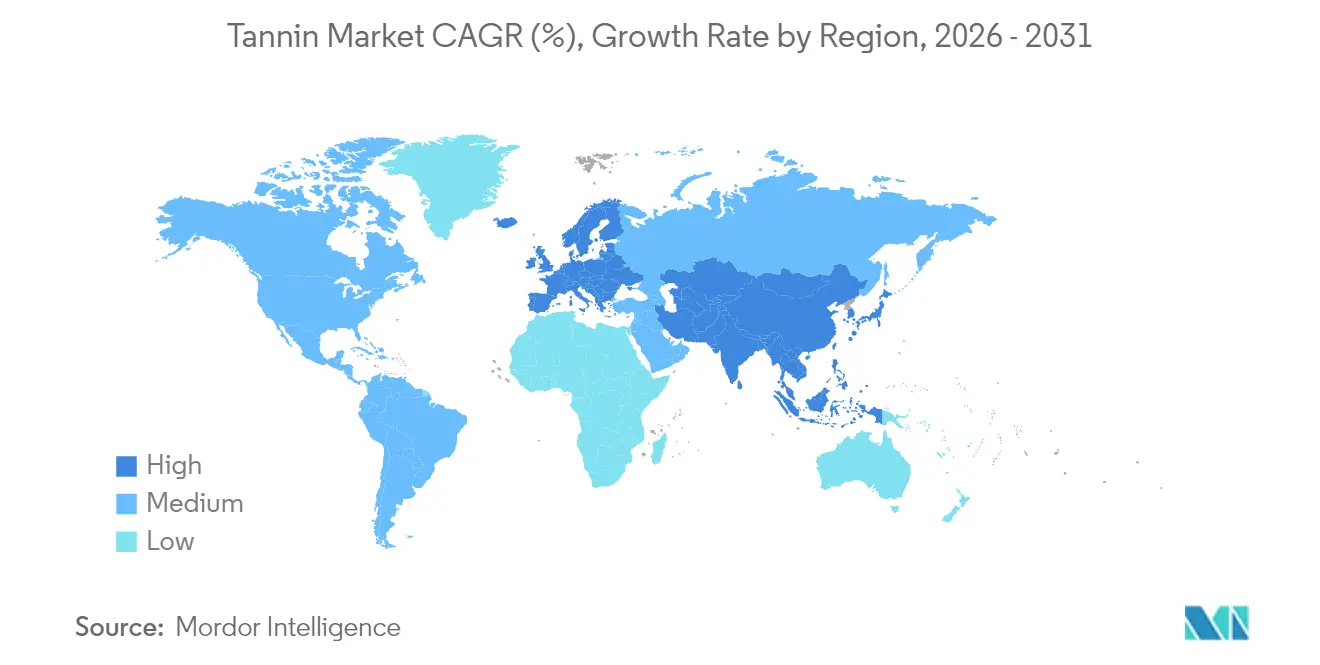

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Tannin Market Analysis by Mordor Intelligence

The tannin market size was valued at USD 2.98 billion in 2025 and estimated to grow from USD 3.18 billion in 2026 to reach USD 4.41 billion by 2031, at a CAGR of 6.72% during the forecast period (2026-2031). This upswing is largely fueled by a rising inclination towards natural inputs in sectors like leather, wine, wood composites, and specialty nutrition. As regulations tighten and consumers increasingly demand sustainable, eco-friendly products, there's a pronounced shift away from synthetic additives. Innovations in sourcing, especially with agro-waste, bark, and seaweed, bolster supply chain resilience and resonate with circular economy goals. Such strides not only lessen reliance on conventional raw materials but also champion environmental sustainability. Furthermore, the swift embrace of chrome-free leather, organic wine standards, and formaldehyde-free wood adhesives underscores the burgeoning appetite for bio-based polyphenols in both industrial and consumer realms. While market competition remains moderate, firms excelling in extraction technology and pursuing vertical integration are carving out a distinct advantage. These pioneers are not only enhancing operational efficiencies but also clinching premium contracts and solidifying their market stance. This trajectory paints a bullish long-term outlook for the tannin market, propelled by innovation, sustainability, and shifting consumer tastes.

Key Report Takeaways

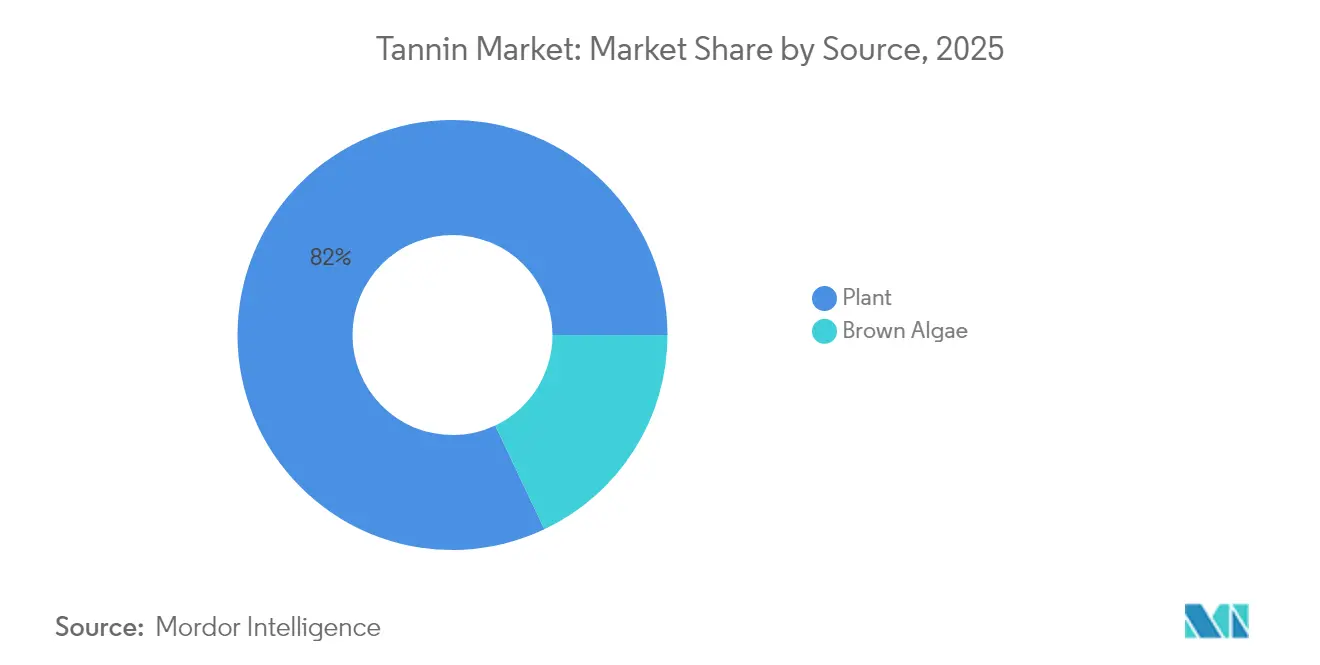

- By source, plant-derived tannins held 82.03% of tannin market share in 2025, while brown algae sources are forecast to advance at an 7.92% CAGR through 2031.

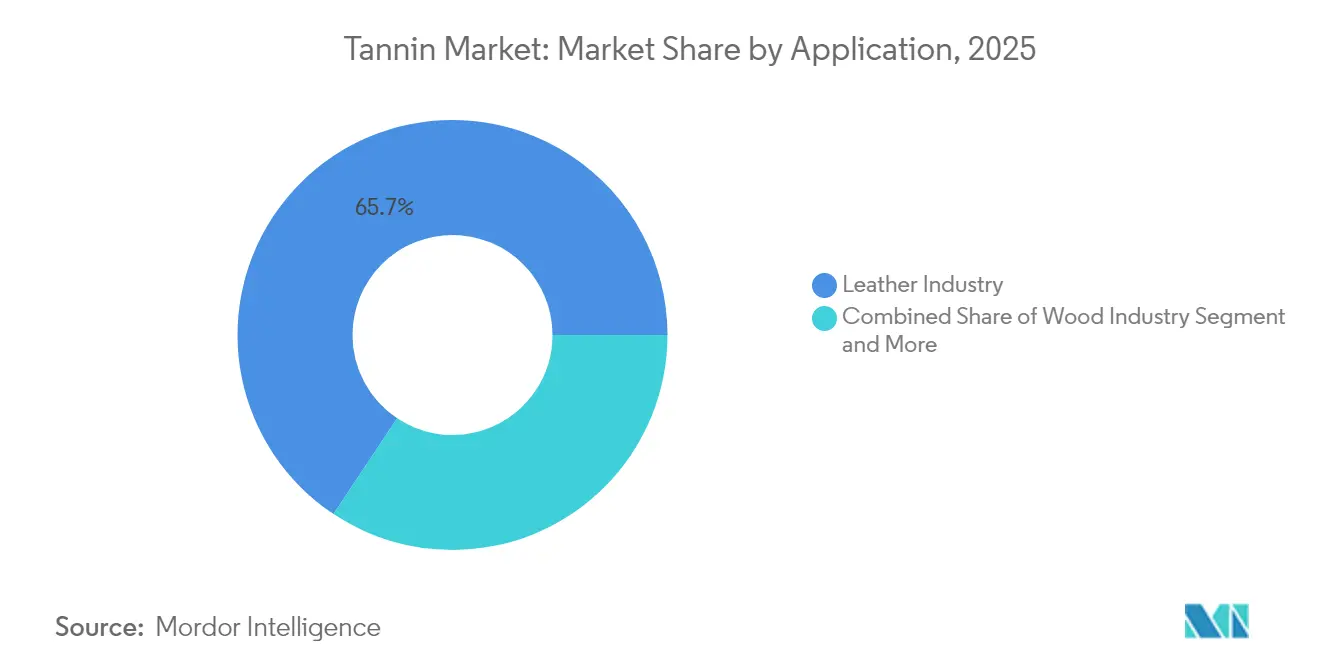

- By application, leather commanded 65.67% of tannin market size in 2025; wood composites are projected to grow the fastest at 7.24% CAGR to 2031.

- By geography, Europe led with 33.61% revenue share in 2025, whereas Asia-Pacific is poised to expand at 7.62% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tannin Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High demand for natural and eco-friendly tanning agents in leather industry | +1.8% | Global, with concentration in Europe and Asia-Pacific | Medium term (2-4 years) |

| Increasing use of tannins in wine and beverage production | +1.2% | Europe, North America, emerging wine regions | Short term (≤ 2 years) |

| Preferance of sustainable, and natural ingredients in food industry | +0.9% | Asia-Pacific, North America | Medium term (2-4 years) |

| Growth in the wood adhesive and particleboard industry | +1.1% | Global, with focus on North America and Europe | Long term (≥ 4 years) |

| Sustainable sourcing from agro-waste and bark extracts | +0.7% | Global | Long term (≥ 4 years) |

| Tannin's antioxidant and other properties drives its use in nutraceuticals | +0.6% | Europe, North America, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High demand for natural and eco-friendly tanning agents in leather industry

As the leather industry pivots towards sustainable tanning, there's a notable surge in demand for vegetable tannins, seen as eco-friendly alternatives to traditional chromium-based chemicals. Stricter limitations on hazardous chemicals in leather processing, driven by the European Union's REACH regulation, are pushing manufacturers towards natural substitutes. In North America, the U.S. Environmental Protection Agency's designation of certain chromium compounds as carcinogenic has hastened the shift to plant-based tanning agents. Reports highlight that vegetable-tanned leather not only fetches a premium in luxury markets but also resonates with the sustainability ethos of leading fashion brands. These brands are now prioritizing chrome-free materials in their sourcing policies, aligning with both consumer preferences and regulatory demands. Moreover, the advent of advanced bio-finishing systems is transforming leather processing, offering biodegradable solutions that boost durability and aesthetic appeal while meeting sustainability benchmarks. This industry-wide shift underscores a response to heightened consumer demand for eco-friendly products and regulatory pushes to curtail industrial chemical use. Key sectors championing this change include automotive upholstery, luxury leather goods, and footwear, all witnessing a rising appetite for sustainable, high-quality materials. Furthermore, a growing emphasis on circular economy principles is steering the leather industry towards waste minimization and resource efficiency, bolstering the move to sustainable tanning.

Increasing use of tannins in wine and beverage production

The demand for oenological tannins is witnessing significant growth as winemakers aim to improve color stability, enhance mouthfeel, and optimize aging characteristics, all while adhering to evolving regulatory requirements. In the United States, the Alcohol and Tobacco Tax and Trade Bureau (TTB) has established precise usage limits, allowing up to 24 pounds of tannins per 1000 gallons in red wine and 6.4 GAE per 1000 gallons in white wine. These standardized guidelines are driving consistent adoption across the industry[1]Source: Code of Federal Regulations, "Materials authorized for the treatment of wine and juice", ecfr.gov. In Europe, the European Food Safety Authority has approved tannic acid for use in animal feed at concentrations up to 15 mg/kg, thereby expanding its applications beyond traditional wine production. Globally, the International Organisation of Vine and Wine (OIV) has legitimized the use of oenological tannins by defining quality standards for botanical sources such as nutgalls, chestnut, oak, and grape seeds[2]Source: International Organisation of Vine and Wine (OIV), "International Oenological CODEX ", oiv.int. Additionally, the FDA's GRAS (Generally Recognized As Safe) designation for specific tannin compounds has facilitated their integration into broader food and beverage applications. Organic certification programs further contribute to market segmentation by creating premium opportunities for naturally sourced tannins.

Tannin's antioxidant and other properties drives its use in nutraceuticals

Growing clinical and regulatory recognition of tannins as potent antioxidants, anti-inflammatory agents, and modulators of gut microbiota is prompting nutraceutical formulators to integrate standardized bark, grape-seed, and seaweed extracts into capsules, powders, and functional gummies. The World Health Organization cites polyphenols such as tannins for their role in reducing oxidative stress markers associated with chronic diseases, giving brand owners a science-backed storyline for immunity and heart-health claims. In parallel, the U.S. Food and Drug Administration’s GRAS status for several tannin fractions lowers regulatory barriers, enabling rapid line extensions across sports-nutrition and healthy-aging portfolios. Refinement advances—like membrane filtration and spray-drying—now yield high-purity concentrates with consistent proanthocyanidin content, which simplifies dose labeling and stability testing for global distribution. Demand for clean-label antioxidants continues to rise, allowing suppliers to command premium pricing while deepening penetration in the USD-centric nutraceutical aisles of North America, Europe, and increasingly Asia-Pacific.

Growth in the wood adhesive and particleboard industry

As the wood products industry shifts towards formaldehyde-free adhesives, there's a notable surge in demand for tannin-based binding agents, especially in the production of particleboard and oriented strand board. The U.S. Environmental Protection Agency's stringent formaldehyde emission standards for composite wood products are pushing manufacturers to seek alternative adhesive systems. Tannin-based formulations emerge as compliant solutions. Meanwhile, the European Union's Construction Products Regulation sets emission limits, leaning towards natural adhesive alternatives and away from synthetic formaldehyde-based systems. The Forest Stewardship Council champions sustainable wood processing methods, endorsing bio-based adhesives from renewable sources, such as bark tannins. Research from the Technical Research Centre of Finland reveals that softwood bark can produce 130 kg of crude tannin powder per ton of dry bark, presenting a cost-effective alternative to fossil-based phenols. The International Organization for Standardization has recognized tannin adhesives as credible substitutes to traditional systems in their testing methods for wood-based panels. These advancements not only cater to the rising industrial demand but also elevate the value of bark materials, traditionally relegated to energy generation, thereby bolstering the principles of a circular economy in forest product manufacturing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex Extraction Processes Limit Commercial Scaling | -1.4% | Global, particularly affecting emerging markets | Short term (≤ 2 years) |

| Variability in Extraction Yields Across Geography | -0.8% | Global, with higher impact in developing regions | Medium term (2-4 years) |

| Stringent FDA and EU regulation increase complaince costs | -0.6% | Global, particularly affecting pharmaceutical applications | Short term (≤ 2 years) |

| Competition from Synthetic Alternatives | -0.5% | Asia-Pacific, Africa, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Complex extraction processes limit commercial scaling

Market expansion faces hurdles due to the technical intricacies and capital demands of tannin extraction processes, with smaller producers and newcomers feeling the pinch. Over 200 patents on tannin extraction methods, recorded by the U.S. Patent and Trademark Office, underscore the technological finesse needed for efficient production. The International Organization for Standardization has set stringent quality benchmarks for tannin products, necessitating meticulous control over extraction parameters. This poses challenges for firms without cutting-edge equipment. Meanwhile, the European Medicines Agency's Good Manufacturing Practice mandates for pharmaceutical-grade tannins call for advanced quality control and validated extraction methods. Similarly, the FDA's Current Good Manufacturing Practice guidelines for dietary supplements stipulate detailed botanical extraction requirements, driving up compliance costs and adding to technical challenges. Such regulatory and technical hurdles not only decelerate market entry but also inflate production expenses. This could hinder the competitiveness of tannin-based products, especially against synthetic counterparts, in price-sensitive sectors and emerging markets.

Variability in extraction yiels across geography

Geographic disparities in raw material quality, climate conditions, and processing infrastructure result in inconsistent tannin yields, posing challenges for supply chain management and pricing strategies. The World Meteorological Organization has reported increasing climate variability, which significantly impacts plant phenolic content and the seasonal availability of raw materials. Additionally, the Food and Agriculture Organization highlights notable regional differences in agricultural productivity, directly affecting the quality and quantity of tannin-rich feedstocks. Seasonal shifts in plant phenolic content further complicate extraction efficiency, necessitating advanced inventory management systems and precise processing schedules to maintain consistent product quality throughout the year. However, successful implementation requires extensive coordination among agricultural producers, processing facilities, and end-users. Variations in soil conditions, rainfall patterns, and harvesting practices influence the final tannin composition and its bioactivity levels, creating inconsistencies that manufacturers must address. To ensure reliable product specifications, manufacturers are compelled to implement robust quality control systems and maintain relationships with multiple suppliers. While these measures help mitigate variability, they also increase operational complexity and drive up costs, underscoring the need for innovative solutions to streamline supply chains and enhance efficiency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Plant Dominance Through Established Infrastructure

In 2025, plant-based tannins dominate the market with an 82.03% share, a testament to decades of refined extraction methods and dependable supply chains. These tannins are sourced from traditional favorites like quebracho, acacia, chestnut, and oak. This market leadership is bolstered by robust agricultural practices and processing facilities, ensuring top-notch quality and dependable supply. The U.S. Department of Agriculture's Forest Service has conducted in-depth studies on extracting bark tannins from the nation's forests, paving the way for a solid supply chain. Meanwhile, the European Forest Institute has rolled out sustainable bark harvesting guidelines, balancing forest vitality with the demand for tannin raw materials. These traditional sources enjoy broad regulatory acceptance, with the FDA deeming specific plant-derived tannins safe for food use. Furthermore, the International Union of Forest Research Organizations champions sustainable sourcing practices, ensuring a steady supply of tannins without compromising environmental standards.

Brown algae is emerging as the fastest-growing source, boasting an 7.92% CAGR projected through 2031. This surge is attributed to the algae's superior phlorotannin bioactivity and its burgeoning role in pharmaceuticals. The National Oceanic and Atmospheric Administration vouches for brown algae cultivation, deeming it a sustainable marine resource that can be harvested without harming the environment. Backing this, the European Maritime and Fisheries Fund is funding research into marine biotechnologies, spotlighting phlorotannin extraction for both pharmaceutical and nutraceutical applications. In Japan, the Agency for Marine-Earth Science and Technology has pioneered advanced cultivation methods, ensuring brown algae consistently yield phlorotannins year-round. The International Seaweed Association has set quality benchmarks for these marine-derived tannins, facilitating their integration into premium applications. Such advancements not only elevate brown algae as a sought-after source for niche applications but also address the sustainability challenges tied to harvesting terrestrial plants.

By Application: Leather Industry Leadership Through Regulatory Support

In 2025, the leather industry commands a robust 65.67% market share, buoyed by a global pivot towards sustainable tanning and mounting regulatory pressures to phase out chromium-based chemicals. Responding to these shifts, the European Chemicals Agency has curtailed the use of chromium compounds, thereby amplifying the demand for vegetable tanning. Similarly, the U.S. Environmental Protection Agency, through its Toxic Substances Control Act, champions natural tanning agents, sidelining synthetic counterparts. Workplace safety is also in focus, with the International Labour Organization setting standards that curtail exposure to hazardous tanning and leather chemicals, further endorsing plant-based alternatives. The Leather Working Group, a prominent industry association, has rolled out environmental stewardship protocols, with a clear emphasis on promoting vegetable tanning. In a significant industry move, major automotive manufacturers now mandate chrome-free leather for their interiors, bolstering the demand for natural tannins in high-volume applications.

Meanwhile, the wood industry is on an upswing, projected to grow at a 7.24% CAGR through 2031. This growth is largely attributed to stringent formaldehyde emission regulations and a rising appetite for sustainable building materials. The U.S. Environmental Protection Agency's standards on formaldehyde emissions for composite wood products are steering the industry towards tannin-based adhesive systems. Across the Atlantic, the European Union's Construction Products Regulation is setting performance benchmarks that lean towards bio-based adhesives, giving them an edge over synthetic counterparts. Recognizing the shift, the Forest Stewardship Council has rolled out certification standards that endorse tannin-based adhesives as eco-friendly substitutes to traditional formaldehyde systems. The International Organization for Standardization is also in the fray, laying down testing protocols for wood-based panels to validate the efficacy of tannin adhesives in structural roles. Adding to the momentum, the Green Building Council's LEED certification program is incentivizing the use of bio-based materials, including tannin-bonded wood products, by awarding them valuable points in sustainable construction projects.

Geography Analysis

In 2025, Europe commands a dominant 33.61% market share, bolstered by stringent environmental regulations and a robust industrial framework that champions natural tannin applications. The European Food Safety Authority has set forth definitive safety protocols for tannins in food, feed, and industrial uses, fostering a climate of regulatory certainty that attracts investments. Meanwhile, the European Medicines Agency has greenlit specific tannin compounds for pharmaceutical use, carving out lucrative market niches. The EU's REACH regulation curbs hazardous chemicals in industries, mandating a shift towards safer, natural alternatives like tannins. Further underscoring the region's commitment, the European Commission's Circular Economy Action Plan champions the transformation of agricultural and forestry waste into bio-based chemicals. On the financial front, the European Investment Bank is backing sustainable tech ventures, including tannin extraction and processing, bolstering the region's infrastructure.

Asia-Pacific is on a rapid ascent, projected to grow at a 7.62% CAGR through 2031, fueled by swift industrialization and evolving regulations that endorse natural product uses. China's strategic development plans, spearheaded by the National Development and Reform Commission, now spotlight bio-based chemicals, paving the way for tannin production. In India, the Ministry of Chemicals and Fertilizers rolls out production-linked incentives, bolstering the manufacturing of natural products, notably tannin extraction from agricultural byproducts. Japan's Ministry of Health, Labour and Welfare broadens the horizon for functional foods, now embracing tannin-based ingredients in varied formats. The Association of Southeast Asian Nations sets the stage with regional standards for natural products, streamlining trade for tannin materials. Down under, Australia's Department of Agriculture launches organic certification programs, paving the way for a premium market for naturally sourced tannins, thus diversifying the regional market landscape.

North America charts a steady growth trajectory, driven by regulatory measures that champion natural substitutes over synthetic ones. The U.S. Food and Drug Administration's GRAS determinations for tannin compounds pave their way into the food and beverage sector. The U.S. Environmental Protection Agency's standards on formaldehyde emissions bolster the case for tannin-based adhesives in wood manufacturing. Meanwhile, the Alcohol and Tobacco Tax and Trade Bureau refines regulations on wine treating materials, setting clear guidelines and limits for tannin use, balancing innovation with safety. South America, with its rich tapestry of raw material sources, sees Brazil spearheading investments in sustainable forestry, fortifying tannin supply chains. In the Middle East and Africa, there's a burgeoning interest, spurred by international programs advocating agricultural waste valorization and a rising consciousness of circular economy tenets.

Regulatory Landscape

Regulation for tannins differs by end use (food processing aids and additives, feed, nutraceuticals, and industrial applications), which creates a compliance-driven need for grade segregation and documentation across the supply chain. In the United States, tannic acid is affirmed as GRAS under 21 CFR 184.1097 with specific maximum use levels by food category, and oenological use is further shaped by the Alcohol and Tobacco Tax and Trade Bureau (TTB) limits for treatment of wine and juice. Internationally, FAO/WHO JECFA lists tannic acid (INS 181) with an ADI “not specified” when used as a processing aid (filtering agent) provided it is removed from food after use, while China regulates edible tannin under the National Food Safety Standard GB 1886.303-2021 (effective August 22, 2021).

Value Chain Analysis

The value chain starts with biomass sourcing (bark, wood, pods, and other tannin-rich botanicals such as quebracho, acacia, chestnut, oak, and tara), followed by primary processing (extraction, concentration, and drying or standardization). Quality control and regulatory documentation for food, feed, or technical grade come next, then distribution through ingredient traders and direct supply to end users in leather, food and beverage (including oenology), wood composites, and nutraceuticals. Manufacturing competitiveness is closely tied to extraction know-how, the ability to standardize polyphenol profiles, and adherence to downstream requirements, including FDA GRAS conditions for food uses and quality-system expectations in regulated segments.

Key constraints include geographic concentration for some feedstocks (for example, quebracho-linked supply dependence), seasonality and climate-driven yield variability, and logistics in producing regions, which can raise losses and working-capital needs. To reduce volatility and meet sustainability requirements from downstream buyers, producers increasingly contract directly with growers and forestry suppliers and pursue programs such as Forest Stewardship Council (FSC) certification, while vertical integration in extraction and finishing helps stabilize specifications and margins for high-volume leather and panel-adhesive customers.

Competitive Landscape

The tannin market remains moderate, with a handful of dominant regional and domestic players scattered across various countries. Leading companies are increasingly focusing on mergers, expansions, acquisitions, partnerships, and new product developments to enhance their brand visibility. Notable players in the market include Sodra Skogsagarna, Ajinomoto Co., Inc., Silvateam Group, Laffort Holding, and TANAC.

This moderate concentration in the industry paves the way for further consolidation, especially as firms aim to broaden their geographic footprint and deepen their application expertise through strategic buyouts. Success in this landscape hinges on adept regulatory compliance, as firms grapple with intricate approval processes across diverse jurisdictions, all while upholding stringent product quality and safety benchmarks. Moreover, technology adoption, especially in extraction efficiency and product standardization, is becoming a pivotal competitive edge. Companies are also prioritizing sustainable sourcing and circular economy initiatives, not just to stand out but to align with shifting regulatory landscapes.

The industry's moderate concentration creates opportunities for consolidation, particularly as companies seek to expand geographic reach and application expertise through strategic acquisitions. Regulatory compliance capabilities increasingly determine competitive success, as companies must navigate complex approval processes across multiple jurisdictions while maintaining product quality and safety standards.

Tannin Industry Leaders

-

Sodra Skogsagarna

-

Ajinomoto Co., Inc

-

Silvateam Group

-

Laffort Holding

-

TANAC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Application whitespace is emerging where regulations and buyer standards favor bio-based chemistry over synthetics, particularly in chrome-free leather systems, formaldehyde-constrained wood composites, and clean-label food and beverage formulations. In the U.S., the framework for tannic acid in foods (21 CFR 184.1097) provides defined, category-specific use limits that support standardized commercialization for formulators, while wine processing continues under TTB treatment limits and OIV quality definitions for botanical sources. These anchors create supplier opportunities in product standardization, including consistent sensory impact, color stability, and antioxidant performance, as well as in documentation packages that streamline multinational approvals and audits.

Feedstock and process innovation also supports expansion of supply options beyond legacy botanicals. In March 2026, a published integrated techno-economic assessment and life cycle assessment for industrial-scale spruce bark tannin extraction added process-design evidence for forestry byproduct valorization, aligning with circular economy sourcing that the market already references (bark, agro-waste, and marine biomass). Commercial opportunities therefore cluster around producers that turn regionally available byproducts into consistent food- or technical-grade extracts, and around downstream users in nutraceutical and functional food formats that adopt engineered delivery systems (for example, hydrogels or polymeric carriers) to improve stability and dosing consistency.

Recent Industry Developments

- March 2026: A peer-reviewed study published an integrated techno-economic assessment and life cycle assessment for industrial-scale extraction of tannins from spruce bark. The work strengthens the business case for valorizing forestry byproducts into standardized tannin intermediates and supports procurement strategies tied to circular-economy feedstocks.

- April 2025: Sodra announced plans to invest in a new production line at its Varo facility in Sweden to industrially extract tannin from tree bark for use as a vegetable tanning agent, with commissioning scheduled in 2026. The project expands access to bark-based inputs and reinforces vertical integration as a route to supply security for large-scale leather applications.

- February 2024: Silvateam S.p.A. acquired wet-green GmbH, the developer of patented wet-green technology for Olivenleder, to advance plant-based tanning solutions. The deal combines Silvateam's tannin extraction capabilities with a bio-based tanning agent platform, broadening sustainable leather-processing options tied to agricultural byproducts.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the tannin market covers revenues earned from tannin extracts and blends (natural and synthetic) that are sold into commercial applications such as food and beverage, leather processing, pharmaceuticals, and other industrial uses across major regions.

Scope exclusions: This sizing excludes captive, on-site extraction that is not sold as a product, and it also excludes downstream finished goods where tannins are only a minor additive cost.

Segmentation Overview

-

By Source

- Plant

- Brown Algae

-

By Application

- Food and Beverage

- Pharmaceutical and Nutraceutical

- Leather Industry

- Wood Industry

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

To build the base context, we started with public references that help validate demand signals and supply-side capacity, such as customs trade statistics for extracts and related materials, agriculture and forestry statistics on bark and wood resources, and food and beverage production releases from official statistical agencies. We also referenced technical publications and peer-reviewed journals that cover polyphenols, extraction yields, and typical use rates in wine, beverages, and industrial formulations.

Next, company annual reports, investor presentations, and press releases were used to understand product focus, regional footprint, and major end-use exposure. We also used paid subscriptions for company financials and intelligence, and for shipment-level import and export checks where trade flows were a helpful proxy for cross-border demand. These desk sources are illustrative, and many other public documents and datasets were also reviewed for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary discussions were run with tannin manufacturers, distributors, and downstream users in leather and food and beverage, so the model assumptions could be pressure-tested in real buying terms. We also spoke with technical experts involved in extraction and formulation to validate typical yields, grade differences, and how substitution with other polyphenols or additives shows up in procurement.

Coverage was balanced across APAC, EMEA, and the Americas, and we re-contacted sources when pricing, supply availability, or regulation-linked demand shifts created a visible break from the desk-research trendline.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 17% | APAC: 40% |

| Mid tier: 52% | Functional/Unit leaders: 30% | EMEA: 33% |

| Smaller Players: 17% | Managers: 53% | Americas: 27% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where production, trade movement, and end-use activity indicators were converted into a realistic demand pool for tannin extracts, and then translated into value using region-appropriate price bands. The totals were then corroborated through selective bottom-up approximations, such as rolling up sampled supplier revenues in key regions and applying volume-by-application checks using typical dosage ranges.

Key inputs that shaped the model included leather output and tanning activity levels, wine and RTD beverage production trends, pharmaceutical excipient and botanical extract usage indicators, and observed import and export directionality for extract categories. Pricing assumptions were not held flat, and they were updated using interview-led guidance on contract structures, grade mix shifts (for example, higher-purity extracts), and raw material tightness.

For forecasting, scenario analysis was used to reflect different adoption paths for natural ingredients and sustainability-driven formulation changes, which are meaningful demand levers in this market. Where bottom-up visibility was limited for smaller countries, the gap was handled by applying proxy ratios from similar end-use structures, and then validating the implied per-capita or per-output consumption against expert feedback.

Data Validation & Update Cycle

Outputs were checked against independent signals, including regional trade balances, production direction in leather and beverage end uses, and price movement logic, and then outliers were reviewed before sign-off. If a large variance appeared, the assumptions were revisited and sources were re-contacted, especially around grade split, application mix, and short-term supply disruptions.

A multi-step internal review is followed so calculation links, unit conversions, and currency timing stay consistent. Reports are refreshed annually, and interim updates are made when material events occur, such as regulatory changes, major capacity additions, or sharp raw material swings. Before delivery, a fresh update pass is completed so clients receive the most current view available.

Mordor Intelligence's Tannin Market Size Measured Against Other Published Estimates

Published numbers for tannins often do not match because each publisher draws the market boundary differently, and then uses different pricing logic and base-year choices. Differences also show up when one estimate leans more on supply-side output and another leans more on end-use consumption, which can move totals in opposite directions.

Trade-flow directionality and leather and beverage activity checks are the evidence points that keep Mordor Intelligence aligned to a defined demand pool for sold tannin extracts, rather than broader polyphenol ingredients. The remaining spread usually comes from whether synthetic tannins are fully included, how fast ASPs are assumed to rise, and how frequently assumptions are refreshed when raw material availability or regulation shifts.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.18 B (2026) | |

| Global Consultancy A | USD 3.10 B (2025) | Uses a different base year and a longer forecast window, and the scope appears to blend source categories more broadly, which can pull adjacent polyphenol ingredients into the revenue pool. |

| Trade Publisher B | USD 2.67 B (2024) | Anchors on an earlier base year and applies a price progression that is less sensitive to grade mix changes, which can understate value when higher-purity extracts take share. |

Across the three figures, the biggest drivers are timing, what is counted as a tannin extract sale, and how pricing is updated as the product mix shifts. By tying assumptions to observable demand signals and then confirming them through targeted supplier and buyer checks, our estimate stays traceable to clear steps that can be repeated and audited.

Key Questions Answered in the Report

What is the current size of the tannin market?

The tannin market stands at USD 3.18 billion in 2026 and is projected to grow to USD 4.41 billion by 2031.

Which segment leads the tannin market by application?

Leather dominates, accounting for 65.67% of 2025 revenue due to global shifts toward chrome-free processing.

Which region is growing fastest in the tannin market?

Asia-Pacific shows the highest CAGR at 7.62% through 2031, supported by bio-based chemical incentives in China and India.

What is the main driver behind tannin demand in wood composites?

Formaldehyde emission limits in North America and Europe are steering panel makers toward tannin-based adhesives.

Page last updated on: