Health Ingredients Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

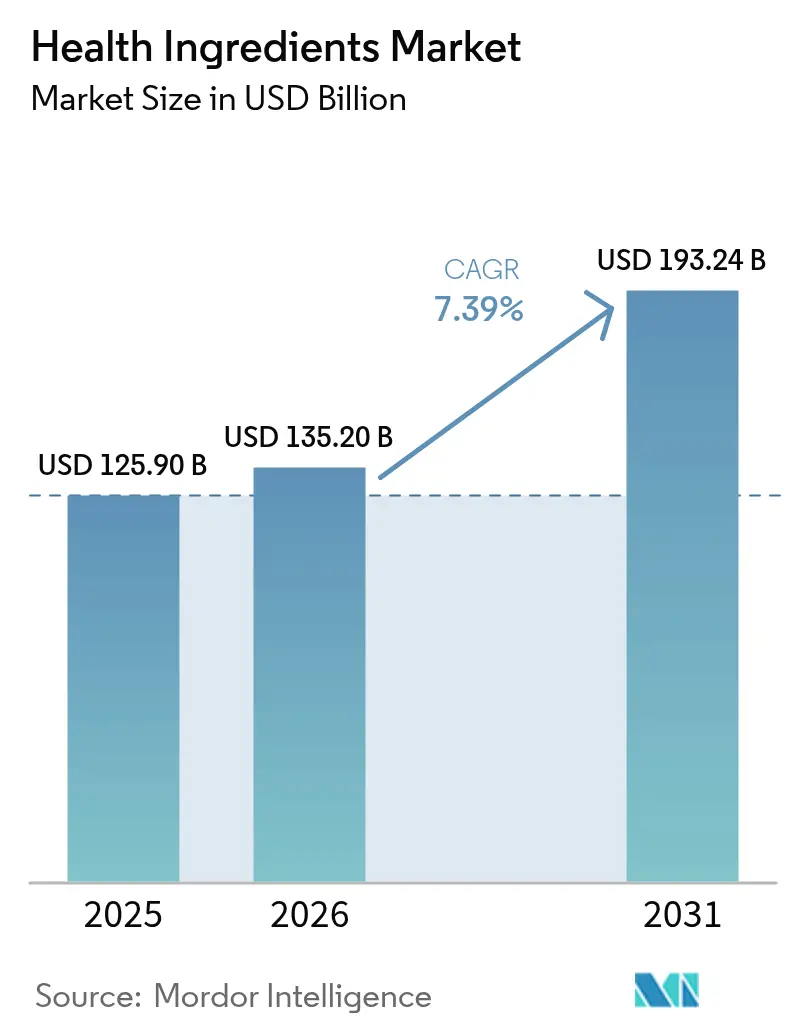

| Market Size (2026) | USD 135.2 Billion |

| Market Size (2031) | USD 193.24 Billion |

| Growth Rate (2026 - 2031) | 7.39% CAGR |

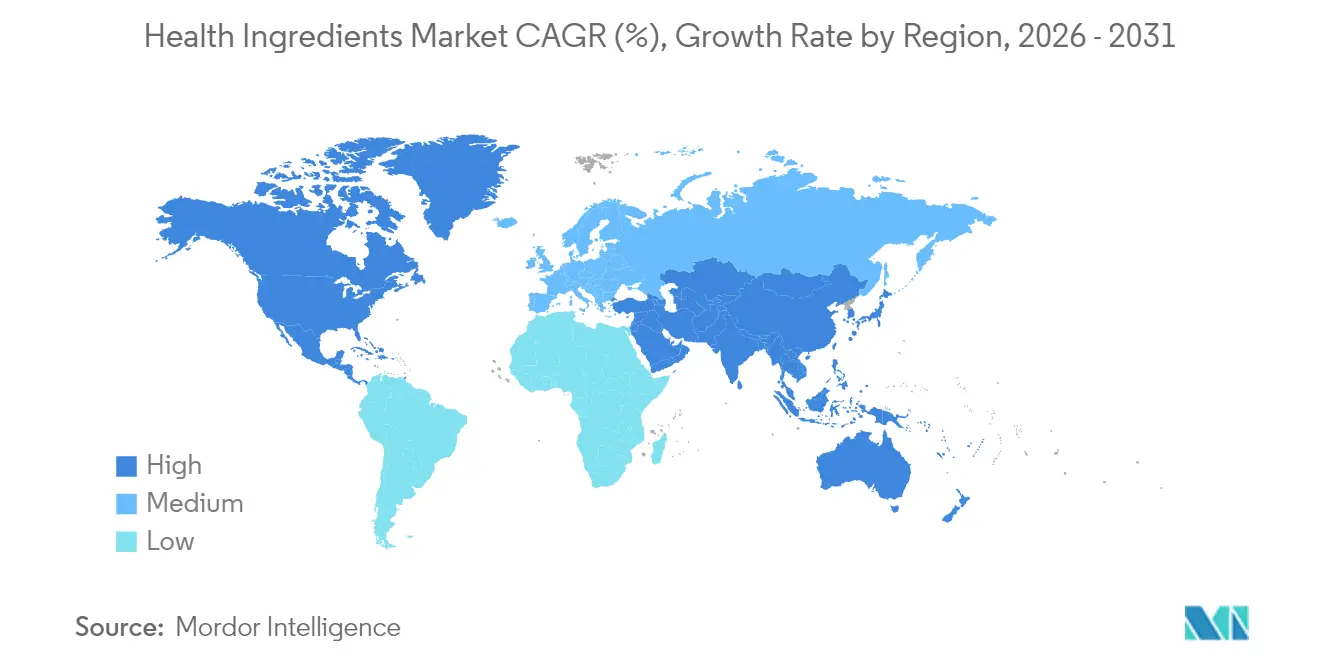

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Health Ingredients Market Analysis by Mordor Intelligence

The health ingredients market size in 2026 is estimated at USD 135.2 billion, growing from 2025 value of USD 125.90 billion with 2031 projections showing USD 193.24 billion, growing at 7.39% CAGR over 2026-2031. The market's robust expansion is largely attributed to the escalating prevalence of lifestyle-related diseases, surging healthcare costs, and a marked pivot towards preventive care and nutritional wellness. A pivotal moment looms in February 2025, when the FDA's updated definition of "healthy" foods comes into play, opening new avenues for ingredient suppliers who resonate with these elevated nutritional and formulation benchmarks. Within product segmentation, proteins dominate, highlighting their widespread acceptance in wellness and functional offerings. Vitamins, meanwhile, are poised for a notable upswing, driven by a growing awareness of micronutrient deficiencies. The market's sourcing landscape is led by plant-based ingredients, echoing a consumer preference for sustainable and vegan options. Dry formats continue to be favored across diverse applications, yet liquid forms are making a pronounced entrance, praised for their adaptability and superior bioavailability. In terms of application, the food and beverage sector takes the lead, propelled by the rising trend of fortified and functional products. Notably, the pharmaceutical industry is outpacing its counterparts, underscoring a growing inclination to integrate health ingredients into both therapeutic and preventive strategies. Geographically, North America emerges as the dominant player, supported by a discerning, health-focused consumer base and transparent regulatory frameworks. Meanwhile, the Asia-Pacific region is swiftly ascending, driven by increasing incomes, a heightened health consciousness, and rapid urbanization.

Key Report Takeaways

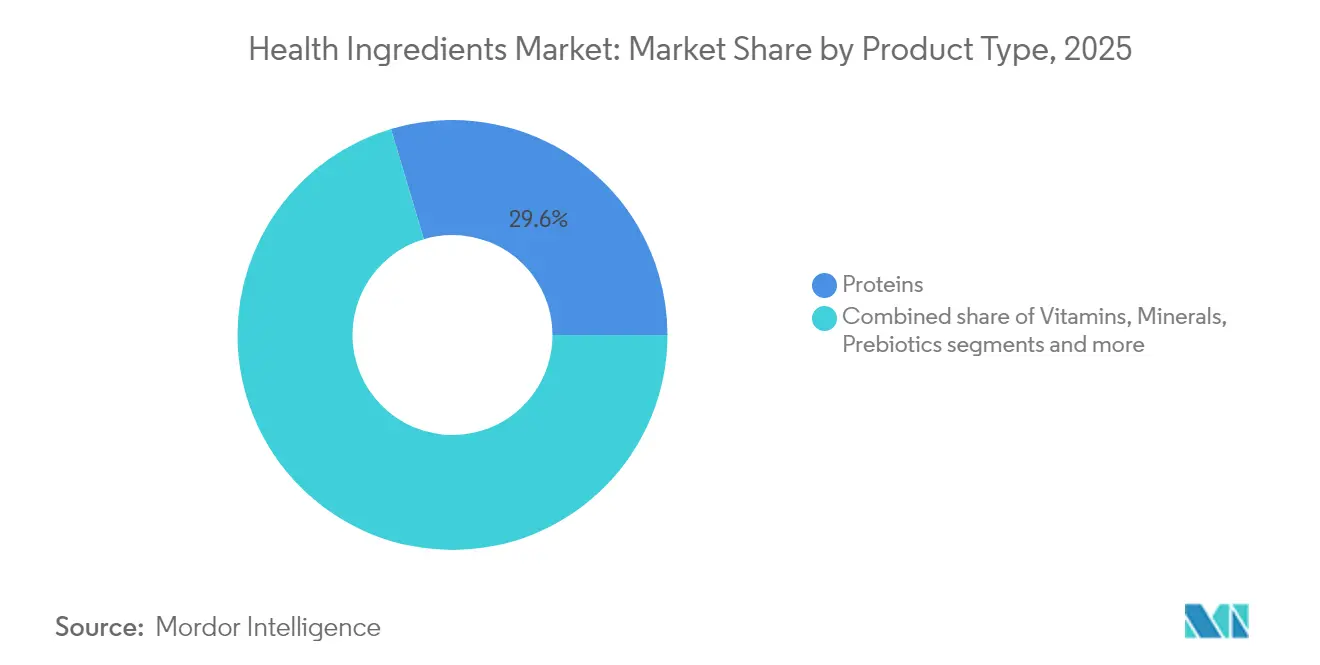

- By product type, proteins held 29.62% of the health ingredients market share in 2025, while vitamins are projected to post the fastest 8.82% CAGR through 2031.

- By source, plant-based ingredients led with 62.12% of the health ingredients market size in 2025, whereas microbial-based inputs top growth at 8.98% CAGR.

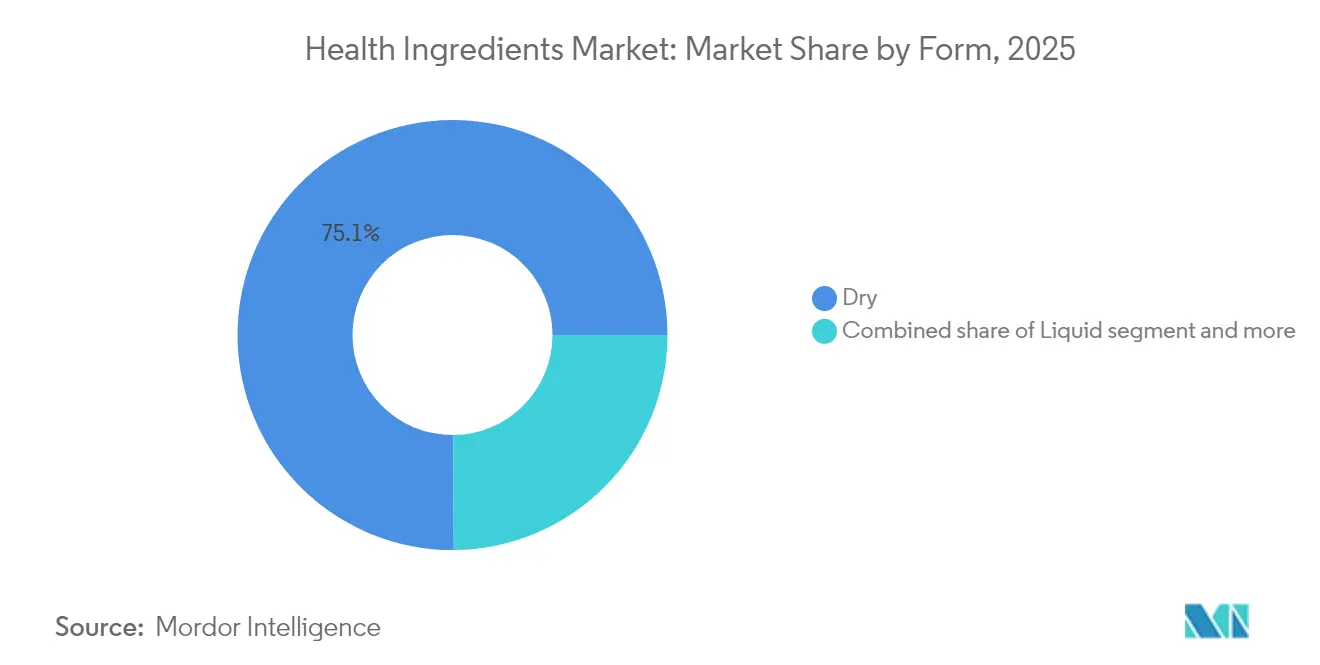

- By form, dry formats commanded 75.10% of the health ingredients market size in 2025; liquid formats recorded the highest 10.39% CAGR toward 2031.

- By application, food and beverages contributed 39.84% of the health ingredients market size in 2025, while pharmaceutical demand rises at an 11.78% CAGR.

- By geography, North America captured 35.22% of the health ingredients market share in 2025; Asia-Pacific expands the quickest at 10.32% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Health Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer focus on wellness and disease prevention through nutrition | +1.2% | Global, with higher intensity in North America and Europe | Medium term (2-4 years) |

| Increasing prevalence of chronic diseases and lifestyle disorders | +1.8% | Global, particularly acute in Asia-Pacific urban centers | Long term (≥ 4 years) |

| Growing demand for natural and clean-label ingredients | +1.5% | North America and the European Union are leading, expanding into the Asia-Pacific | Medium term (2-4 years) |

| Aging global population seeking functional foods | +1.1% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Heightened demand for fortified food products | +0.9% | Asia-Pacific core, spill-over to Middle East amd Africa and Latin America | Short term (≤ 2 years) |

| Increasing adoption of plant-based ingredients | +1.3% | Global, with early gains in North America, Europe, and urban Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Focus on Wellness and Disease Prevention Through Nutrition

According to the American Heart Association’s 2024 report, 29.3 million adults globally have been diagnosed with diabetes, 9.7 million remain undiagnosed, and 115.9 million are estimated to have pre-diabetes [1]Source: American Heart Association, "2024 Heart Disease and Stroke Statistics: A Report of US and Global Data From the American Heart Association," researchgate.net. This revelation is driving the growth of the global health ingredients market. As consumers become more proactive about their health, they're gravitating towards preventive, nutrition-centric solutions. This trend has heightened the demand for ingredients that boast clinically validated health benefits, transcending mere nutrition. For example, Kerry Group's Wellmune is known for bolstering immune health, while Nestlé Health Science's LactoSpore is recognized for its digestive benefits. With healthcare costs on the rise globally, many consumers are opting for dietary preventive measures instead of turning to costly treatments. In response to this trend, DSM-Firmenich has unveiled its Healthy Longevity platform, focusing on brain, digestive, and immune health. At the same time, wearable health technologies, such as Fitbit and Apple Watch, are enabling users to monitor their vitals and adjust their diets in real-time. This blend of health-centric lifestyles, scientifically backed formulations, and personalized monitoring is not just fueling market growth but also indicating a significant shift towards proactive health management through functional nutrition.

Increasing Prevalence of Chronic Diseases and Lifestyle Disorders

The increasing prevalence of chronic diseases is driving growth in the global health ingredients market. Factors such as sedentary lifestyles, poor dietary habits, and stress have increased the demand for preventive health solutions, including functional foods and dietary supplements containing bioactive ingredients. Consumers are taking a more active role in managing their health through nutrition, resulting in higher consumption of vitamins, minerals, and omega-3 fatty acids. These ingredients support immune function, reduce inflammation, and maintain cardiovascular, metabolic, and cognitive health. The transition from reactive to preventive healthcare approaches has expanded beyond consumer preferences to become a medical necessity. The rising number of chronic disease diagnoses has prompted individuals to seek natural and functional solutions for symptom management and disease prevention, sustaining the demand for health ingredients in food, beverage, and supplement products. According to the Italian National Institute of Statistics (ISTAT), in 2023, over 23.6 million individuals in Italy were living with at least one chronic disease, highlighting the need for dietary and lifestyle interventions [2]Source: Italian National Institute of Statistics, "Number of people affected by at least one chronic disease in Italy," istat.it.

Growing Demand for Natural and Clean-Label Ingredients

The Food and Drug Administration (FDA) is tightening its grip on Generally Recognized as Safe (GRAS) regulations, pushing for more stringent safety documentation and potentially sidelining self-affirmed safety claims. This shift in the regulatory landscape is a boon for companies like Givaudan and Naturex, which boast comprehensive safety dossiers and a portfolio of natural ingredients. In contrast, suppliers of synthetic ingredients are finding themselves under heightened scrutiny. As consumers increasingly gravitate towards clean-label and organic products, premium pricing has become the norm. This trend has particularly favored compliant companies like Ingredion, known for its plant-based, non-GMO offerings. Moreover, the clean-label movement is reshaping production methods. For instance, solvent-free technologies, such as hydrodynamic cavitation, are now being employed to extract valuable bioactives like curcumin and polyphenols. To align with consumer demands, companies such as IFF and FrieslandCampina are integrating blockchain traceability, ensuring both ingredient integrity and ethical sourcing. Natural health ingredients are finding their way into dietary supplements, herbal medicines, and functional foods, resonating with consumer preferences. Highlighting the market's potential, a 2023 report from the Center for the Promotion of Imports revealed that 52% of European consumers turned to supplements for preventive health, emphasizing the demand for safe, traceable, and naturally sourced ingredients.

Aging Global Population Seeking Functional Foods

As the global population ages, the demand for health ingredients surges, driven by seniors' quest for vitality, management of age-related conditions, and an enhanced quality of life. With older adults facing increased risks like osteoporosis, cardiovascular issues, and cognitive decline, there's a noticeable pivot towards functional foods and supplements. Products such as Nestlé Health Science’s Meritene and Swisse’s Ultivite are now in the spotlight, designed to bolster joint health, memory, heart function, and digestion. This wellness-centric approach among seniors is amplifying the demand for nutrient-dense, bioavailable, and easily digestible formulations. In response, manufacturers are rolling out age-specific innovations, including collagen peptides, omega-3s, and plant-based proteins. These innovations aim to address the specific nutritional needs of seniors, ensuring they receive targeted support for their health challenges and improving their overall quality of life. This trend is particularly evident in aging regions; for instance, the U.S. Census Bureau highlighted in 2025 that 59% of U.S. metro areas boasted a median age of 40 or older [3]Source: U.S. Census Bureau, “An Aging Nation: U.S. Median Age Surpassed 39 in 2024 – Census.gov," census.gov . Such demographic shifts spotlight a burgeoning market opportunity for health ingredients tailored to longevity and senior wellness, resonating across diverse global populations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited availability of raw materials | -0.8% | Global, with acute impact in regions dependent on specific botanical sources | Short term (≤ 2 years) |

| Price volatility of natural and organic ingredients | -1.1% | Global, particularly affecting premium ingredient segments | Short term (≤ 2 years) |

| Technical challenges in maintaining ingredient stability and shelf life | -0.6% | Global, with higher impact on liquid formulations and sensitive compounds | Medium term (2-4 years) |

| Complex regulatory requirements and approval processes across different regions | -0.9% | Global, with varying intensity based on regulatory maturity | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Availability of Raw Materials

As climate change disrupts traditional botanical cultivation zones and intensifies cross-industry demand, supply chain constraints significantly restrain the Global Health Ingredients Market. The geographic concentration of specialty ingredients, such as ashwagandha from India and ginseng from Korea, renders the supply chain vulnerable to extreme weather, geopolitical instability, and trade barriers. This vulnerability drives volatility in both the availability and pricing of these ingredients. In response, companies like ADM and Evonik are diversifying their sourcing and adopting alternative production methods, such as cellular agriculture and synthetic biology, to lessen their dependence on conventional farming. Yet, the industry's pivot towards sustainable sourcing, evidenced by certifications like Rainforest Alliance and FairWild, temporarily tightens supply as producers adapt to these environmental and social benchmarks. To bolster long-term stability, industry leaders are forging grower partnerships and investing in regional production hubs. A prime example is DSM-Firmenich's foray into localized fermentation facilities. Such strategies are pivotal for ensuring ingredient continuity and fostering global market growth, even in the face of escalating supply chain challenges.

Price Volatility of Natural and Organic Ingredients

Weather variability, seasonal harvest cycles, and shifting supply-demand dynamics drive significant price volatility for natural ingredients in the Global Health Ingredients Market. This unpredictability poses challenges for food and supplement manufacturers trying to forecast costs. The U.S. Department of Agriculture (USDA) reports that food prices have closely followed these global commodity market fluctuations, exacerbating pricing instability. The costs of organic-certified ingredients rise due to limited certifier availability, inspection fees, and varying regional regulatory standards, which add complexity to the certification process. Moreover, currency fluctuations in international trade heighten price unpredictability for imported ingredients like maca, turmeric, and spirulina, making cost management more difficult. To navigate these challenges, larger companies utilize forward contracts and financial hedging, backed by sophisticated procurement systems. In contrast, smaller firms often find themselves without such tools, making them more vulnerable to market shocks. This disparity has led to increased industry consolidation, with larger, financially robust players gaining a competitive edge through enhanced cost resilience and tighter supply chain control.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Proteins Lead Market Share Despite Vitamin Growth Surge

In 2025, proteins commanded a dominant 29.62% share of the Global Health Ingredients Market, buoyed by a consistent consumer shift towards alternative protein sources. These proteins play pivotal roles in muscle health, weight management, and sports nutrition. The protein segment encompasses a diverse range: from plant-based options like pea and soy, to animal-derived choices such as whey and collagen, and even microbial sources like mycoprotein. Industry leaders, including DSM-Firmenich and Roquette, are pioneering specialized protein formulations tailored for various life stages and health conditions, notably targeting sarcopenia prevention in aging adults. Additionally, a rising demand for clean-label and allergen-free protein options is propelling segment growth in both developed and emerging markets.

Vitamins are on a rapid ascent, projected to grow at a CAGR of 8.82% through 2031. This surge is largely attributed to heightened awareness of micronutrient deficiencies and proactive fortification efforts, especially in Southeast Asia and Sub-Saharan Africa. While minerals enjoy steady traction in fortified foods and supplements, prebiotics and probiotics are witnessing a notable boom. This surge is driven by an intensified focus on gut health, immunity, and mental well-being, with brands like FrieslandCampina's Biotis and Chr. Hansen’s probiotic strains are leading the charge. Nutritional lipids, with a spotlight on algal omega-3s, are emerging as the go-to sustainable alternative to traditional fish oil. Meanwhile, niche segments like functional carbohydrates and enzymes are finding their footing, catering specifically to sports and digestive health. The “Others” category, which includes postbiotics and human milk oligosaccharides (HMOs), is also carving out a niche, showcasing promising growth despite its limited market share.

By Source: Plant-Based Dominance Challenged by Microbial Innovation

In 2025, plant-based ingredients commanded a leading share of 62.12%, fueled by a surging demand for natural, sustainable, and allergen-free substitutes to animal-derived components. This upward trajectory is bolstered by technological strides in extraction and purification, amplifying ingredient potency while upholding a clean-label image. Widely embraced in supplements and functional foods, ingredients like turmeric extract, pea protein, and green tea polyphenols are at the forefront. Industry giants, Kerry Group and Ingredion, have broadened their portfolios with plant-based offerings, aligning with both health and environmental standards, further cementing the segment's dominance.

Microbial-based ingredients are the fastest-growing segment, boasting a robust 8.98% CAGR (2026-2031). This surge is propelled by innovations in precision fermentation and synthetic biology, which either replicate or enhance compounds once exclusively sourced from plants or animals. Cargill's strategic forays into life sciences VC funds highlight a pronounced commitment to microbiome health and fermentation-derived actives. While animal-based ingredients still hold sway in niches requiring distinct bioactive profiles, they grapple with intensifying scrutiny over sustainability and ethical considerations. Meanwhile, the "Others" category, encompassing synthetic and hybrid formats, is making strides. Leveraging microencapsulation techniques like spray drying and coacervation, these formats safeguard bioactives and facilitate controlled release. The melding of biotechnology with traditional production methods unveils fresh avenues for nimble companies navigating a diverse ingredient landscape.

By Form: Dry Formulations Dominate While Liquid Processing Advances

In 2025, dry formulations dominated the market, capturing a substantial 75.10% share. Their logistical efficiency, extended shelf life, and compatibility with popular delivery forms like powders, capsules, and tablets underscore their appeal. Manufacturers favor these formats for their storage convenience, reduced transportation costs, and the widespread availability of production infrastructure. Consumers, particularly in the dietary supplements realm, readily embrace these dry formats. Furthermore, dry ingredients ensure enhanced stability for sensitive compounds, including vitamins, minerals, and botanical extracts, making them ideal for functional foods, nutraceuticals, and pharmaceuticals.

On the other hand, liquid formulations are on a rapid ascent, boasting a CAGR of 10.39% projected through 2031, with the functional beverage segment leading the charge. Innovations such as nanoemulsion technology are pivotal, boosting the solubility and bioavailability of oil-based ingredients like omega-3s and curcumin in water-based beverages. Companies are harnessing techniques like hydrodynamic cavitation and advanced homogenization to optimize the extraction and delivery of bioactives, ensuring better absorption and stability. Meanwhile, gels and pastes, though niche, cater to foodservice and institutional markets with their concentrated, ready-to-use formulations.

By Application: Food and Beverages Lead While Pharmaceuticals Accelerate

In 2025, the food and beverages segment dominated the market, seizing a 39.84% share. This segment's broad applications span bakery, confectionery, snacks, dairy, and, notably, functional beverages. Strong distribution networks and a rising consumer appetite for health-enhancing foods have bolstered this dominance. Functional beverages, in particular, are witnessing rapid growth as consumers gravitate towards convenient formats infused with ingredients like electrolytes, collagen, and antioxidants. In response to shifting wellness trends, manufacturers are rolling out innovative clean-label and plant-based options, catering to global market demands.

Meanwhile, the pharmaceutical segment is emerging as the fastest-growing, with projections estimating a CAGR of 11.78% through 2031. This surge is attributed to the increasing adoption of nutraceuticals as complementary therapies, coupled with innovations in drug delivery systems and excipients. A testament to this trend was Roquette’s strategic acquisition of IFF’s Pharma Solutions division in March 2024, a deal valued at up to USD 2.85 billion, highlighting the industry's pivot towards pharmaceutical-grade health ingredients. Dietary supplements are gaining traction, fueled by a heightened awareness of preventive health. Concurrently, feed applications are expanding, driven by a renewed emphasis on livestock health and productivity. Additionally, the “Others” category, encompassing personal care and cosmetics, is leveraging bioactives like hyaluronic acid and biotin, seamlessly merging nutrition with beauty and wellness.

Geography Analysis

In 2025, North America commanded the market, clinching a 35.22% share. This dominance is bolstered by robust regulatory frameworks, heightened consumer awareness of functional nutrition, and well-established distribution channels spanning the food, supplement, and pharmaceutical sectors. The region's vibrant research and development ecosystem, coupled with substantial venture capital influx, empowers biotechnology firms to spearhead innovations in ingredient synthesis and delivery technologies. These factors collectively position North America as a leader in driving advancements and meeting consumer demands in the health ingredients market.

On the other hand, the Asia-Pacific region is on a rapid ascent, boasting a projected CAGR of 10.32% through 2031. This surge is driven by urbanization, increasing disposable incomes, and a burgeoning middle class gravitating towards health-centric diets. While Japan stands out with its sophisticated functional food regulations, other emerging markets navigate through more streamlined approval processes. The region's dynamic growth is further supported by increasing investments in infrastructure and the rising influence of local manufacturers in the global market. Europe, with its stringent regulatory landscape, showcases a robust appetite for natural and organic products, underscoring a regional commitment to sustainability and ethical sourcing. European consumers are increasingly inclined to invest in ingredients that boast clinically validated benefits and transparent sourcing.

South America, the Middle East, and Africa are emerging as hotspots, spurred by urban expansion and a growing affinity for Western dietary trends. Yet, these regions grapple with regulatory hurdles and pricing dilemmas. Nonetheless, as their economies burgeon, so does the demand for health ingredients. These regions are also witnessing increased collaborations with global players, which are helping to address supply chain inefficiencies and improve market accessibility. Given the global interconnectivity of ingredient supply chains, the Asia-Pacific's upward trajectory is poised to sway global pricing and material accessibility, thereby redefining sourcing and distribution strategies worldwide.

Regulatory Landscape

Regulation for health ingredients is shaped by food additive rules, supplement and food ingredient safety substantiation, and tighter post-market scrutiny. In the United States, FDA actions in 2026 reinforced oversight around additives and colorants, including approving gardenia (genipin) blue for use as a color additive while encouraging faster industry phase-out of FD&C Red No. 3 ahead of the January 15, 2027 deadline. FDA also signaled a stronger post-market posture in 2026 through its Human Foods Program deliverables and chemical review framework, which raises the value of robust safety dossiers for widely used ingredients.

In Europe, the framework under Regulation (EC) No 1333/2008 continued to evolve through targeted updates. Commission Regulation (EU) 2025/2058 updated Annexes II and III to realign additive categories, and Commission Regulations (EU) 2026/189 and 2026/196 introduced stricter purity specifications, including heavy metal limits and microbiological criteria, for several common hydrocolloids and stabilizers (for example, E 407, E 410, E 412, E 414, E 415, E 440, and E 1450), alongside updates relevant to foods for special medical purposes. These changes increase testing, supplier qualification, and specification management requirements for ingredient manufacturers supplying food and medical nutrition applications.

Value Chain Analysis

The value chain spans upstream agricultural and microbial inputs, extraction and fermentation, refining and formulation into standardized ingredient systems, and downstream incorporation into food and beverages, dietary supplements, feed, and pharmaceuticals. Large integrated processors and ingredient specialists (for example, ADM, Cargill, DSM-Firmenich, Kerry Group, and Ingredion) source plant materials, dairy streams, and microbial feedstocks, then apply processes such as advanced extraction, spray drying, microencapsulation, and precision fermentation to deliver proteins, vitamins, probiotics, nutritional lipids, and botanical actives in dry and liquid formats.

Key pinch points sit at (i) raw material availability and price volatility for botanicals and protein crops, and (ii) compliance and quality requirements that vary by end use, especially pharmaceutical-grade and special medical nutrition. Regulatory approval and evidence generation timelines for novel foods and GRAS-type pathways can extend 12 to 24 months, which can shape portfolio planning and capacity utilization. In 2026, fertilizer- and energy-linked disruptions reinforced upstream sensitivity, with nitrogen fertilizer economics tied to natural gas costs and periodic shocks to urea and ammonia supply transmitting into crop yields and input pricing, driving dual-sourcing, regionalization, and traceability investments across the chain.

Competitive Landscape

The health ingredients market demonstrates moderate consolidation, with established multinational companies maintaining competitive positions through vertical integration, Research and Development capabilities, and global distribution networks. Market leaders, including Archer-Daniels-Midland Company, Cargill, Incorporated, BASF SE, and DSM-Firmenich AG, maintain strong positions through diversified portfolios across multiple ingredient categories and end-use applications. This diversification provides resilience against segment-specific volatility. The market sees increased competition from specialized biotechnology firms developing new production methods and smaller companies targeting niche applications with high-margin potential.

Technology adoption serves as a key differentiator, as companies invest in precision fermentation, microencapsulation, and advanced extraction methods to enhance ingredient functionality while reducing production costs. The global increase in patent filings for functional food innovation indicates higher Research and Development investment and strategic positioning around proprietary technologies.

New opportunities exist in personalized nutrition, where companies can use consumer health data to develop targeted ingredient formulations. Sustainable production methods that address environmental concerns while maintaining cost competitiveness present additional growth potential. Market disruption comes from cellular agriculture companies developing animal-free proteins and biotechnology firms using synthetic biology to produce complex molecules traditionally sourced naturally, potentially transforming conventional supply chains and value propositions.

Health Ingredients Industry Leaders

-

Archer-Daniels-Midland Company

-

Cargill, Incorporated

-

BASF SE

-

Kerry Group

-

DSM-Firmenich AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Capacity additions in functional proteins and specialty lipids are creating room for suppliers that can deliver consistent sensory performance, clean labels, and application support across foods, beverages, and specialized nutrition. In May 2026, Bunge opened a USD 550 million integrated soy protein concentrate and textured soy protein concentrate facility in Morristown, Indiana, and FrieslandCampina Ingredients completed a Borculo (Netherlands) expansion in March 2026 that doubled capacity for whey protein isolate and milk fat globule membrane, improving supply availability for high-protein beverages, clinical nutrition, and active lifestyle formulations. Cargill also announced an expansion of its Port Klang, Malaysia, edible oil facility in March 2026 with a new specialty fats line and integrated lipid R&D, aligning with demand for functional fats used in bakery, confectionery, and nutrition applications.

Regulatory actions are also shifting opportunity toward reformulation-ready, well-documented ingredient systems and alternatives to legacy additives. FDA initiated a new post-market safety review approach in 2026 starting with BHT and azodicarbonamide, and EFSA updated guidance in 2026 on data requirements for food additive risk assessment, increasing the premium on suppliers with stronger toxicology packages, impurity controls, and traceability. Ingredient makers that pair compliant specifications, including heavy metal and microbiological criteria where relevant, with faster customer-facing development support, such as ready-to-use premixes, heat-stable proteins for RTD formats, and fermentation-derived actives, are positioned to win programs linked to clean-label renovation and functional performance upgrades.

Recent Industry Developments

- July 2026: Archer-Daniels-Midland (ADM) partnered with The EVERY Company to enable US-based commercial-scale production of OvoPro egg white protein made via precision fermentation at ADM's Clinton, Iowa, facility. The partnership links alternative protein scale-up to established ingredient manufacturing infrastructure and supports broader adoption in food and beverage formulations that need functional egg protein performance without animal sourcing.

- May 2026: Bunge opened a USD 550 million fully integrated soy protein concentrate and textured soy protein concentrate facility in Morristown, Indiana, designed to process 4.5 million bushels of soybeans annually. The site adds large-scale North American capacity for plant proteins used in health-positioned foods, beverages, and meat alternative applications, improving supply security and shortening customer lead times for customized formats.

- March 2024: Roquette completed the acquisition of IFF's Pharma Solutions business for up to USD 2.85 billion. This transaction strengthened Roquette's position in pharmaceutical-grade excipients and specialty ingredients, reflecting deeper integration of health ingredients into drug delivery and medical nutrition value chains.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers health-focused ingredients (such as proteins, vitamins, minerals, probiotics, prebiotics, nutritional lipids, functional carbohydrates, enzymes, and plant or fruit extracts) that are sold as inputs to manufacturers of foods, beverages, supplements, feed, and pharmaceuticals.

Scope exclusions: Excluded from this sizing are colors, high-intensity sweeteners, and purely synthetic preservatives.

Segmentation Overview

-

By Product Type

- Proteins

- Vitamins

- Minerals

- Prebiotics

- Nutritional Lipids

- Probiotics

- Functional Carbohydrates

- Enzymes

- Others

-

By Source

- Plant-based

- Animal -based

- Microbial-based

- Others

-

By Form

- Dry

- Liquid

- Others

-

By Application

-

Foods and Beverages

- Bakery and Confectionary

- Snacks

- Dairy Products

- Beverages

- Others

- Dietary Supplements

- Feed

- Pharmaceuticals

- Others

-

Foods and Beverages

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to pin down the demand pool and pricing logic for common ingredient groups, before assumptions are tested with industry conversations. We usually start with public sources such as the US FDA (including GRAS notices and related guidance), the European Commission and EFSA publications, and FAO and OECD agriculture and food statistics that signal output and consumption shifts linked to nutrition.

To connect ingredients with end markets, we also refer to sources such as UN Comtrade trade statistics, national statistical agencies (for food manufacturing and pharma output series), and peer-reviewed journals that discuss adoption of probiotics, plant extracts, and similar ingredient classes. Company annual reports, investor presentations, association websites, and reputable press are used to track product mix changes and capacity moves, while paid subscriptions for company financials and shipment-level import or export views are used selectively to sanity-check major flows. These examples are not exhaustive, and we reviewed many other sources for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work is used to validate what is actually counted as a health ingredient in contracts, and how pricing and volumes move by form and application. We spoke with ingredient suppliers, distributors, and downstream product manufacturers, and the inputs were checked across APAC, EMEA, and the Americas so regional demand drivers and regulatory timing differences could be reflected in the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 14% | APAC: 41% |

| Mid tier: 60% | Functional/Unit leaders: 34% | EMEA: 32% |

| Smaller Players: 14% | Managers: 52% | Americas: 27% |

Market-Sizing & Forecasting

Our sizing starts with a top-down build where ingredient demand is reconstructed from end-use output and trade signals, then refined using penetration assumptions for key health claims and formulations. To keep totals realistic, the results are cross-checked with selective bottom-up approximations, such as sampled price-per-kilogram ranges multiplied by estimated volumes for major ingredient groups, and then confirmed through distributor channel checks.

Inputs that typically matter here include functional food and supplement consumption trends, trade balances for key ingredient categories, shifts in plant-based sourcing, the share of dry versus liquid formats, and the pace of reformulation activity in food and beverage and in pharmaceuticals. Where bottom-up visibility is weak for niche extracts or enzymes, gaps are handled through conservative proxy mapping to adjacent ingredient baskets and then corrected during primary validation.

For forecasting, scenario analysis is used so adoption speed, regulatory changes, and pricing progression can be adjusted transparently by region and application. The forward view is anchored to expert consensus on which ingredient types are gaining share, and it is checked against macro indicators that influence discretionary health spending and packaged food output.

Data Validation & Update Cycle

Validation is done by comparing model outputs with independent signals, then reviewing variance drivers until they make sense in plain business terms. Checks include year-over-year growth versus end-use output, trade consistency versus regional demand, and price movement logic versus commonly quoted ingredient ranges.

Before sign-off, anomalies are flagged for a second analyst review, and follow-up calls are triggered when a data point would move totals beyond a reasonable range. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is completed so clients receive the latest updated view.

Mordor Intelligence's Health Ingredients Market Size Compared Against Other Published Estimates

Published market sizes for health ingredients often differ even when the topic name looks the same, because each publisher chooses its own inclusion rules, revenue point in the chain, and year labeling for the size and forecast.

The main gap comes from whether factory-gate revenues and excluded adjacent categories are blended into one total. Mordor Intelligence counts health ingredients sold as inputs (like probiotics, proteins, and functional carbohydrates) while keeping colors, high-intensity sweeteners, and purely synthetic preservatives outside the number.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 135.20 B (2026) | |

| Industry Research Publisher A | USD 128.42 B (2025) | Uses a different base year and may apply a wider function-led grouping across applications, which can shift what gets counted as a health ingredient and how regional rollups are timed. |

| Global Market Report B | USD 133.54 B (2026) | Often reports at factory-gate values with a supply-chain revenue lens and a shorter-step CAGR window, which can change pricing progression and the treatment of resales and bundled services. |

The spread in the table is largely explained by scope edges, base-year choices, and whether the value is tied to ingredient inputs versus broader revenue definitions. By keeping the variables and exclusions explicit, and then re-checking them with supplier and buyer conversations, we arrive at a practical number that can be repeated and stress-tested when assumptions change.

Key Questions Answered in the Report

What is the current size of the health ingredients market in 2026?

The health ingredients market size is USD 135.2 billion in 2026.

Which region is growing the fastest in the health ingredients market?

Asia-Pacific posts the strongest 10.32% CAGR toward 2031, driven by urbanization and rising disposable income.

Which product category leads the health ingredients market share?

Proteins lead with 29.62% of market share in 2025, reflecting sustained demand for alternative and functional proteins.

Why are microbial-based ingredients gaining momentum?

Microbial ingredients grow at 8.98% CAGR because precision fermentation offers consistent quality, reduced land use, and scalable output.

Page last updated on: