Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 65.30 Billion |

| Market Size (2031) | USD 78.43 Billion |

| Growth Rate (2026 - 2031) | 3.73% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Dairy Ingredients Market Analysis by Mordor Intelligence

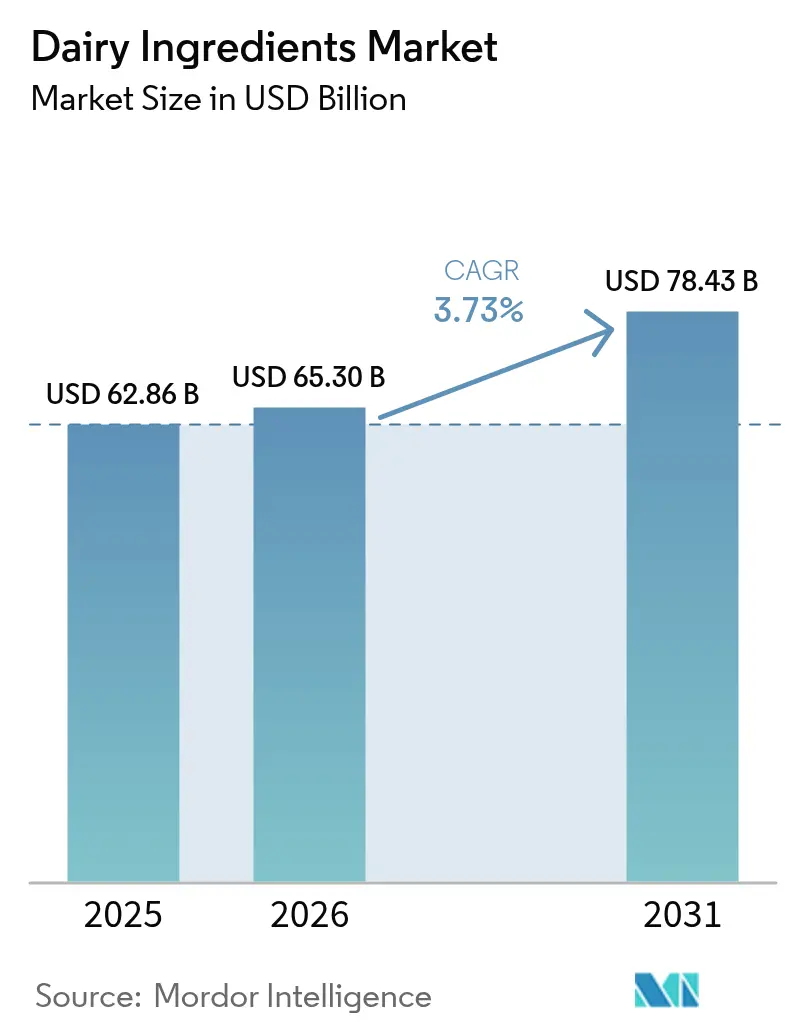

The dairy ingredients market size reached USD 62.86 billion in 2025, stood at USD 65.30 billion in 2026, and is forecast to reach USD 78.43 billion by 2031, expanding at a CAGR of 3.73% during 2026-2031. The market growth continues due to increased consumer preference for protein-rich products, established processing technologies, and higher utilization of specialty powders in food security programs. Europe remains the largest regional market, supported by regulatory quality requirements and developed milk collection networks. The Asia-Pacific region demonstrates the highest growth rate, driven by higher income levels, urban population growth, and favorable government policies that increase milk production and ingredient demand. Market applications expand through sports nutrition products, infant formula, and functional foods, while advancements in fermentation processes and automated plant operations improve production efficiency and reduce environmental impact across the dairy ingredients market.

Key Report Takeaways

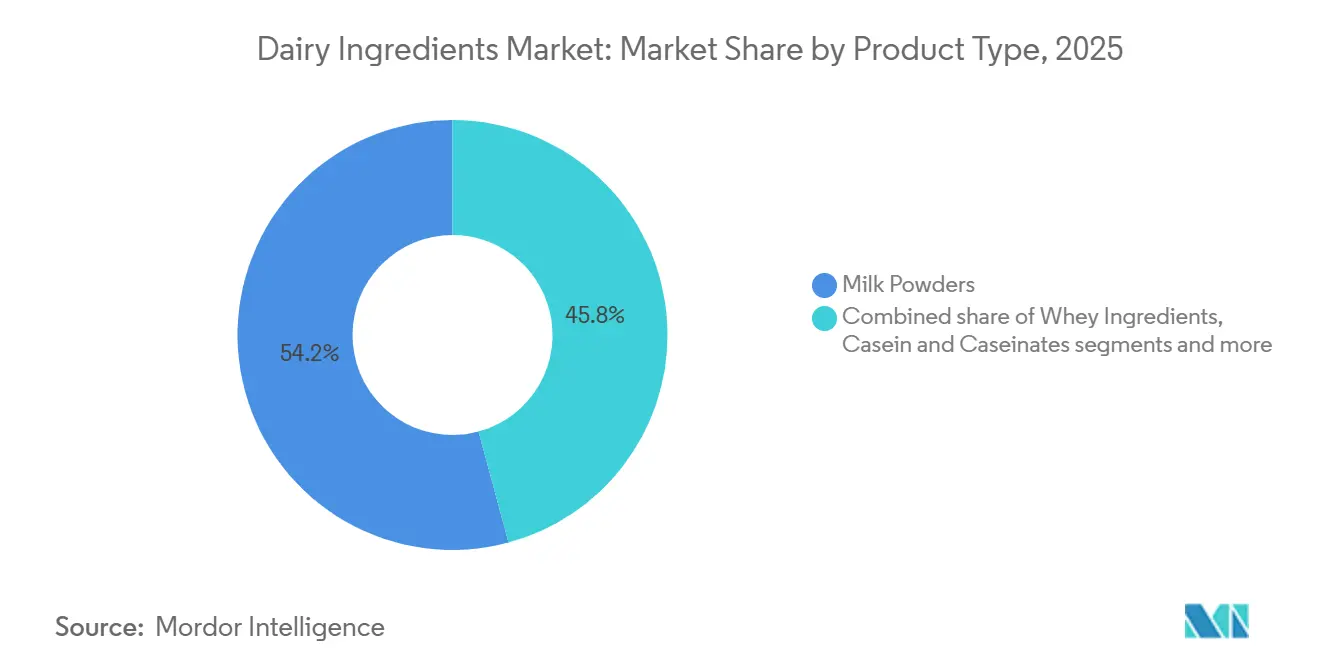

- By product type, milk powders led with 59.62% of 2025 revenue and are projected to expand at a 4.01% CAGR through 2031.

- By nature, conventional ingredients dominated with 89.74% share in 2025, while organic lines are set for a 4.91% CAGR during 2026-2031.

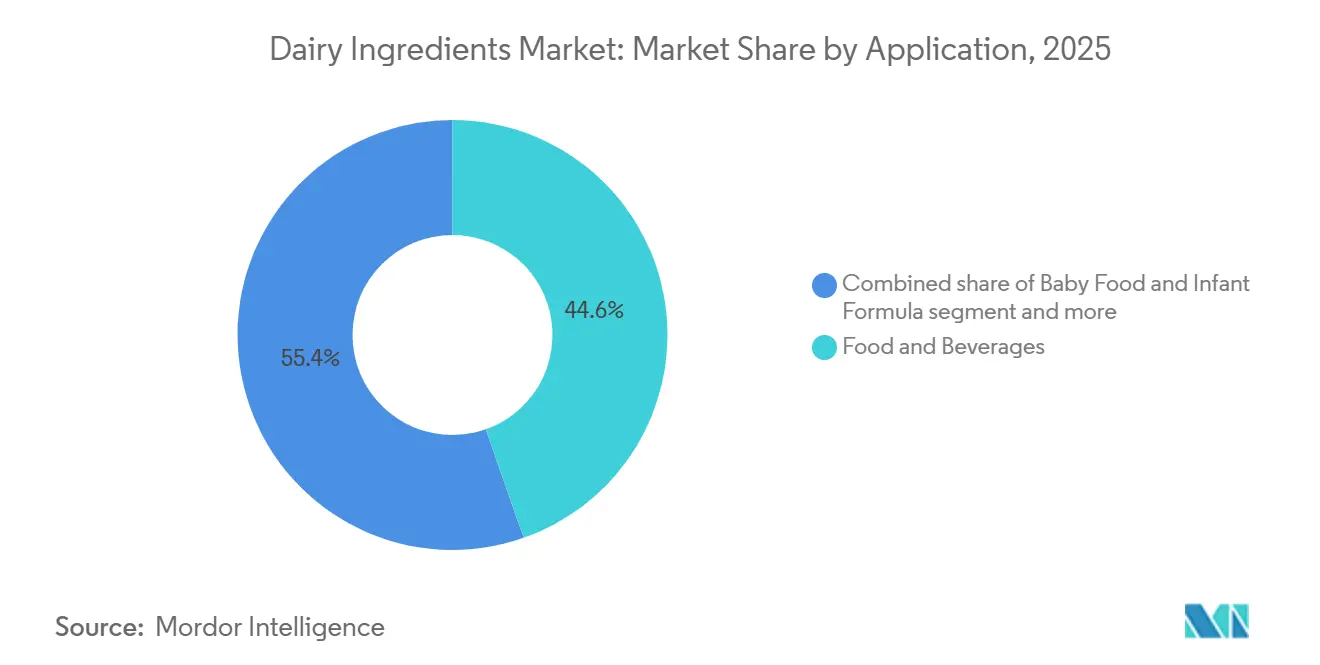

- By application, food and beverages held a 44.62% share in 2025, whereas baby food and infant formula are poised for a 4.46% CAGR to 2031.

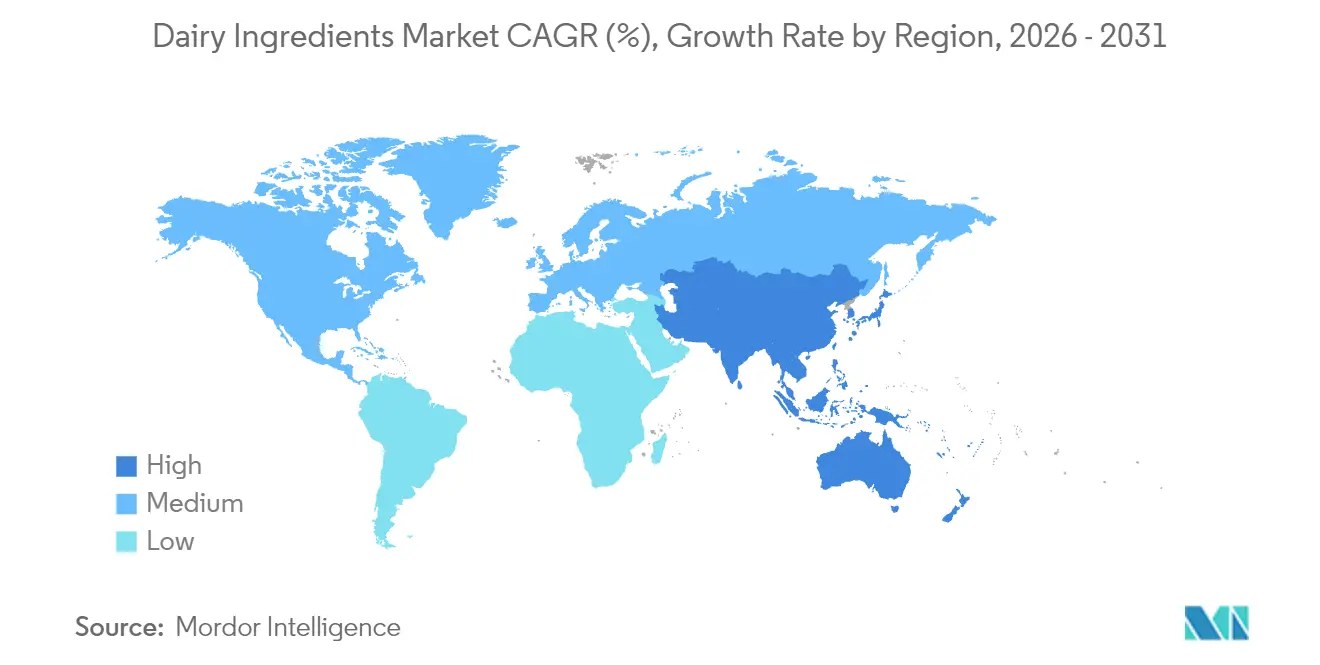

- By geography, Europe retained a 32.43% share in 2025, yet Asia-Pacific is forecast to grow at a 4.52% CAGR over the period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dairy Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for protein-rich foods | +0.8% | Global, with strongest impact in North America and Asia-Pacific | Medium term (2-4 years) |

| Increasing adoption in sports nutrition products | +0.6% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Expansion of the infant formula market | +0.5% | Asia-Pacific core, with spillover to emerging markets | Long term (≥ 4 years) |

| Growing adoption in functional food and beverage sector | +0.4% | Global, led by developed markets | Medium term (2-4 years) |

| Surging usage in bakery and confectionery industry | +0.3% | Europe and North America, expanding globally | Short term (≤ 2 years) |

| Rising consumption in emerging markets | +0.7% | Asia-Pacific, Latin America, and Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for protein-rich foods

The protein market expansion is transforming the food industry, extending dairy ingredient applications beyond sports nutrition into mainstream food and beverage categories. Market demand indicates consumers require functional benefits, including muscle support, satiety, and sustained energy from standard products such as breakfast cereals and baked goods. Dairy Management Inc.'s research and technological investments facilitate the manufacturing of high-protein, shelf-stable beverages and convenient formats that maintain quality while preserving nutritional value. Market growth is evident in ready-to-drink shakes, protein bars, and functional dairy snacks, with whey and casein proteins delivering complete amino acid profiles that surpass many plant-based alternatives. Market analysis shows that Millennials and Gen Z consumers demonstrate significant demand, analyzing product specifications and evaluating protein content as a primary purchase factor. Companies integrating dairy proteins demonstrate strong market positioning in the expanding functional nutrition segment of the dairy ingredients market.

Increasing adoption in sports nutrition products

In 2024, Arla Foods Ingredients' strategic acquisition of Volac's whey nutrition business underscores the sector's growth potential, with the company anticipating significant sales growth in whey protein isolate over the next five years. The market expansion reflects broader lifestyle changes where fitness and wellness have become integral to consumer identity, creating demand for convenient, high-quality protein sources within the dairy ingredients market. Innovation in sports nutrition is driving product diversification beyond traditional protein powders into ready-to-drink beverages, protein bars, and functional snacks that incorporate advanced dairy ingredients. The sector benefits from increasing female participation in fitness activities and the growing popularity of plant-forward diets that still include high-quality animal proteins for performance optimization. Precision fermentation technologies are beginning to complement traditional dairy sourcing in the dairy ingredients market, with companies like Helaina developing human lactoferrin equivalents that offer superior bioavailability for athletic performance applications.

Expansion of the infant formula market

Infant formula represents a critical growth vector for the dairy ingredients market, with whey protein hydrolysates becoming increasingly sophisticated to address cow milk protein allergies while maintaining nutritional efficacy. The sector's evolution reflects advancing understanding of infant nutrition, where manufacturers seek to replicate human milk's beneficial components through innovative dairy ingredient combinations. Regulatory frameworks are becoming more stringent, with the FDA establishing new standards for infant formula grade whey protein phospholipid concentrates, ensuring quality consistency across manufacturers. Asian markets are driving significant expansion in the dairy ingredients market, particularly in China, where demographic shifts toward quality-focused parenting are increasing demand for premium infant nutrition products. The market is witnessing technological advancements in enzyme selection and hydrolysis conditions to produce optimal whey protein hydrolysates that retain essential amino acids while minimizing allergenicity. Innovation extends to specialized formulations addressing specific health conditions, where dairy ingredients provide functional benefits beyond basic nutrition, creating premium market segments with higher value propositions.

Growing adoption in functional food and beverage sector

Functional foods incorporating dairy ingredients are experiencing unprecedented growth as consumers seek products that deliver health benefits beyond basic nutrition. This expansion reflects a fundamental shift in consumer behavior where food choices are increasingly driven by health optimization rather than mere sustenance. Probiotics and fermented dairy ingredients are leading this transformation in the dairy ingredients market, with manufacturers developing sophisticated delivery systems that ensure bacterial viability while enhancing product palatability. The sector benefits from growing scientific evidence supporting dairy bioactives' role in immune function, digestive health, and cognitive performance, creating opportunities for premium positioning. Clean label trends are driving reformulation toward natural dairy ingredients that provide functional benefits without artificial additives, aligning with consumer preferences for transparency and authenticity in food production.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lactose intolerance and dairy allergies | -0.4% | Global, with highest impact in Asia-Pacific and parts of Africa | Long term (≥ 4 years) |

| Growing popularity of plant-based alternatives | -0.6% | North America and Europe, expanding to urban centers globally | Medium term (2-4 years) |

| Volatility in raw milk prices | -0.3% | Global, with acute impact in price-sensitive emerging markets | Short term (≤ 2 years) |

| Health-related dietary concerns | -0.2% | Developed markets, particularly North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lactose intolerance and dairy allergies

According to the World Population Review data from 2025, 44% of Australians are lactose intolerant [1]Source: World Population Review, "Lactose Intolerance by Country 2025", worldpopulationreview.com. The challenge is particularly acute in Asian markets where lactase persistence is less common, yet these regions represent the fastest-growing dairy consumption markets, creating a complex dynamic for industry players. Manufacturers are responding with advanced lactase enzyme technologies, including DSM-Firmenich's Maxilact Next, a fast-acting enzyme that enables efficient lactose-free dairy production while maintaining product quality and nutritional integrity. Prebiotic strategies using galactooligosaccharides are emerging as complementary solutions, potentially shifting gut microbiomes to improve lactose digestion without complete lactose removal. The constraint is driving innovation in alternative dairy proteins through precision fermentation for the dairy ingredients market, where companies can produce dairy-identical proteins without lactose content. Consumer education about lactose-reduced products and their health benefits is becoming crucial for market expansion, particularly in regions where dairy consumption has traditionally been limited by genetic factors affecting lactose metabolism.

Growing popularity of plant-based alternatives

The FDA's recent guidance on plant-based dairy alternative labeling reflects the regulatory system's attempt to balance innovation with consumer clarity, potentially impacting how these products compete with traditional dairy ingredients [2]Source: U.S. Food and Drug Administration (FDA), “Draft Guidance on Plant-Based Milk Labeling”, fda.gov. The competitive pressure is driving dairy ingredient innovation toward cleaner labels, enhanced nutritional profiles, and sustainability improvements that address consumer concerns, driving alternative adoption. Precision fermentation technologies are creating hybrid opportunities where dairy proteins can be produced without traditional livestock, potentially bridging the gap between conventional and alternative dairy products. The challenge is spurring collaboration between traditional dairy companies and alternative protein developers, creating new market categories that combine the functional benefits of dairy with the sustainability appeal of plant-based production.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Milk Powders Lead Innovation

Milk powders command 59.62% of the dairy ingredients market share in 2025 while simultaneously achieving the fastest growth rate of 4.01% CAGR among product types, reflecting their versatility across applications and critical role in global food security initiatives. This dual leadership position stems from technological advances in spray drying and roller drying methods that have enhanced product quality and functional properties, making milk powders increasingly attractive for manufacturers seeking cost-effective protein fortification solutions. Skimmed milk powder and whole milk powder represent the largest subsegments, with growing demand from emerging markets where shelf stability and nutritional density are paramount considerations for food security programs.

Whey ingredients constitute the second-largest category, with whey protein concentrates and isolates experiencing robust demand from sports nutrition and functional food applications. The segment benefits from increasing consumer awareness of whey protein's superior amino acid profile and bioavailability compared to plant-based alternatives. Milk protein concentrates and isolates are gaining traction across the dairy ingredients market. Manufacturers seek ingredients that provide both functional and nutritional benefits in clean-label formulations. Lactose and derivatives, while representing a smaller market share, are experiencing renewed interest through innovative applications like lactulose production for prebiotic benefits.

By Nature: Organic Segment Accelerates

Conventional dairy ingredients maintain an 89.74% market share in 2025, reflecting their established supply chains and cost advantages, while organic ingredients achieve the highest growth rate at 4.91% CAGR through 2031, driven by consumer willingness to pay premium prices for perceived health and environmental benefits. The USDA reported a 15.5% increase in organic whole milk sales in September 2024 compared to the previous year, with total organic fluid milk sales reaching 249 million pounds, demonstrating robust consumer demand despite higher price points. Organic milk exports increased by 36.2% year-to-date, signaling premium momentum in the dairy ingredients market. Compared to the previous year, this indicates strong international demand for premium dairy ingredients.

The organic segment's growth is supported by expanding retail distribution and increasing availability of organic feed ingredients, which historically constrained production capacity. Conventional ingredients continue to dominate due to their reliability, consistent quality, and established processing infrastructure that supports large-scale manufacturing operations. The price differential between organic and conventional ingredients is narrowing in some regions as organic production scales increase and conventional prices face upward pressure from sustainability requirements. Regulatory frameworks are evolving to support organic certification processes while maintaining stringent quality standards that ensure consumer confidence in premium positioning.

By Application: Food and Beverages Drives Growth

The food and beverages segment holds a 44.62% market share in 2025, while baby food and infant formula achieve the highest growth rate at 4.46% CAGR through 2031. The dominance of the food and beverage sector in the global dairy ingredients market is due to the high-volume use of functional proteins and fats in products like bakery, dairy-based drinks, and convenience foods. According to the International Dairy Federation (IDF), dairy ingredients are valued for their "techno-functional" properties, such as emulsification and foaming, essential for industrial food production.

The Infant Formula and Baby Food segment is growing faster due to a global shift toward "medicalized" nutrition and rising demand for high-value specialty components. This trend is influenced by WHO standards for nutrient density, pushing manufacturers toward complex formulations. For example, in 2024, Arla Foods Ingredients launched Lacprodan Alpha-10, a whey protein enriched with alpha-lactalbumin to meet specific amino acid requirements with lower protein content. In 2025, Nestlé integrated biotechnologically produced HMOs (Human Milk Oligosaccharides) into its premium lines to boost infant gut health, following EFSA’s expanded safety approvals. By 2026, FrieslandCampina Ingredients released a precision-fermented lactoferrin substitute, addressing the global shortage of high-purity bovine lactoferrin and meeting demand for immunity-boosting infant nutrition. While general food and beverages provide the market's volume base, the infant segment captures the highest value growth through rapid, science-led innovations.

Geography Analysis

Europe holds the largest regional market share at 32.43% in 2025, supported by its advanced processing infrastructure, strict quality standards, and robust consumer demand for premium dairy products. The region's increasing milk production directly contributes to higher dairy ingredient output. The well-established dairy processing facilities, combined with technological advancements in production methods, enable efficient conversion of raw milk into various dairy ingredients. The United Kingdom recorded total milk production of 14,890 million liters in 2024, according to DEFRA data. This substantial production volume underscores the region's capacity to meet both domestic and international demand in the dairy ingredients market.

The Asia-Pacific dairy ingredients market demonstrates the highest growth rate at 4.52% CAGR through 2031, fueled by increasing disposable incomes, population expansion, and growing health consciousness. The region's dairy ingredient market benefits from modernizing production facilities, improving supply chain infrastructure, and rising adoption of Western dietary habits. According to the United States Department of Agriculture, India's milk production is expected to reach 216.5 million metric tons in 2025, bolstered by government support and favorable weather conditions. The country's domestic fluid milk consumption is projected to reach 91 million metric tons. This growth trajectory reflects the region's expanding dairy processing capabilities and increasing consumer preference for dairy-based products.

North America benefits from advanced processing technology in the dairy ingredients market and strong domestic demand for protein-rich products, while facing increased competition from plant-based alternatives in urban markets. The region's strength lies in innovation capabilities and established supply chains that support large-scale ingredient production for both domestic and export markets. South America and the Middle East, and Africa represent emerging opportunities where rising disposable incomes and urbanization are driving increased dairy consumption, though infrastructure limitations and price sensitivity create challenges for premium ingredient penetration.

Competitive Landscape

The dairy ingredients market shows moderate consolidation, with established multinational corporations operating alongside regional players and technology-focused companies. Market dynamics reflect a balanced competitive environment where traditional manufacturers maintain strong positions while adapting to emerging trends. Recent market changes include Arla Foods Ingredients' acquisition of Volac's whey nutrition business in 2025, strengthening its whey protein isolate production capabilities. Companies are increasingly focusing on research and development to maintain their competitive positions in the evolving market landscape.

Companies are differentiating themselves through technological advancements, including precision fermentation, AI-driven processes, and sustainable production methods to serve premium market segments. The integration of advanced technologies has become a key factor in maintaining market competitiveness and meeting evolving consumer demands. Investment in sustainable production methods has emerged as a critical strategy across the dairy ingredients market for companies seeking to capture environmentally conscious market segments. These technological innovations are reshaping traditional production processes and creating new opportunities for market growth.

New market opportunities are emerging in precision fermentation, as companies develop alternative protein production methods. Companies like DairyX are pioneering the production of casein proteins without livestock for traditional cheese production, offering sustainable alternatives to conventional supply chains. Companies like NewMoo and Future Cow are leveraging biotechnology and molecular farming to create dairy-identical proteins from plant sources. These innovations are introducing new competitive elements to the ingredient supply chain and challenging established production methods while addressing growing sustainability concerns.

Dairy Ingredients Industry Leaders

-

Arla Foods amba

-

Fonterra Co-Operative Group Limited

-

Saputo Inc.

-

Groupe Lactalis

-

Royal Friesland Campina N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: New York-based food biotechnology company Pureture commenced commercial production of its alternative casein protein. The protein provided natural emulsification without requiring gums, thickeners, or stabilizers. The product met multiple dietary requirements, being dairy-free, lactose-free, allergen-free, additive-free, and non-GMO.

- March 2025: Dutch ingredient company Vivici launched Vivitein BLG, a dairy protein manufactured through precision fermentation. The protein was suitable for vegans and could be incorporated into protein powders, nutritional beverages, and various food applications.

- February 2025: Expana launched two milk concentrates and two whey permeates. The products, manufactured using ultrafiltration and diafiltration processes, were suitable for functional food products and other applications.

Global Dairy Ingredients Market Report Scope

Dairy ingredients, such as milk powder, milk protein concentrate, whey protein, and casein, are rich sources of essential nutrients, including proteins, amino acids, carbohydrates, minerals, and probiotics. Each of these ingredients has wide applications in the food and beverage industries, including bakery products, confectionery, sports nutrition, and infant formulas.

The dairy ingredients market is segmented by product type, nature, application, and geography. Based on product type, the market is segmented into milk powders, milk protein concentrates and milk protein isolates, whey ingredients, lactose and derivatives, casein and caseinates, and other types. The whey ingredients segment is further segmented into skimmed milk powder, whole milk powder, and others. Similarly, the whey ingredients segment is further segmented into whey protein concentrate, whey protein isolate, and hydrolyzed whey protein. By nature, the market is segmented into conventional and organic. By application, the market is segmented into food and beverages, dietary supplements, sport/performance nutrition, baby food and infant formula, elderly nutrition and medical nutrition, animal feed, pharmaceutical, and personal care and cosmetics. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East, and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

Product Type

| Milk Powders | Skimmed Milk Powder |

| Whole Milk Powder | |

| Others | |

| Milk Protein Concentrates and Isolates | |

| Whey Ingredients | Whey Protein Concentrate |

| Whey Protein Isolate | |

| Hydrolyzed Whey Protein | |

| Lactose and Derivatives | |

| Casein and Caseinates | |

| Others |

Nature

| Conventional |

| Organic |

Application

| Food and Beverages | Bakery Products |

| Snack Food | |

| Beverages | |

| Dairy and Dairy Alternative Products | |

| Others | |

| Dietary Supplements | |

| Sport/Performance Nutrition | |

| Baby Food and Infant Formula | |

| Elderly Nutrition and Medical Nutrition | |

| Animal Feed | |

| Pharmaceutical | |

| Personal Care and Cosmetics |

Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Turkey | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Rest of Middle East and Africa |

| Product Type | Milk Powders | Skimmed Milk Powder |

| Whole Milk Powder | ||

| Others | ||

| Milk Protein Concentrates and Isolates | ||

| Whey Ingredients | Whey Protein Concentrate | |

| Whey Protein Isolate | ||

| Hydrolyzed Whey Protein | ||

| Lactose and Derivatives | ||

| Casein and Caseinates | ||

| Others | ||

| Nature | Conventional | |

| Organic | ||

| Application | Food and Beverages | Bakery Products |

| Snack Food | ||

| Beverages | ||

| Dairy and Dairy Alternative Products | ||

| Others | ||

| Dietary Supplements | ||

| Sport/Performance Nutrition | ||

| Baby Food and Infant Formula | ||

| Elderly Nutrition and Medical Nutrition | ||

| Animal Feed | ||

| Pharmaceutical | ||

| Personal Care and Cosmetics | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Qatar | ||

| Turkey | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the dairy ingredients market?

The dairy ingredients market reached USD 62.86 billion in 2025, stood at USD 65.30 billion in 2026, and is forecast to reach USD 78.43 billion by 2031, expanding at a CAGR of 3.73% during 2026-2031.

Which product type holds the largest share?

Milk powders lead with 59.62% of 2025 share and remain the fastest-growing category at a 4.01% CAGR through 2031.

Which region is growing the fastest?

Asia-Pacific shows the strongest trajectory with a forecast 4.52% CAGR, supported by rising income levels and government investment in milk infrastructure.

Why are organic dairy ingredients gaining attention?

Organic dairy ingredients are expected to grow at 4.91% CAGR. Consumers prioritize health benefits, clean labels, and sustainable farming practices.

Page last updated on: