Hyaluronic Acid Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.16 Billion |

| Market Size (2031) | USD 2.84 Billion |

| Growth Rate (2026 - 2031) | 5.63% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

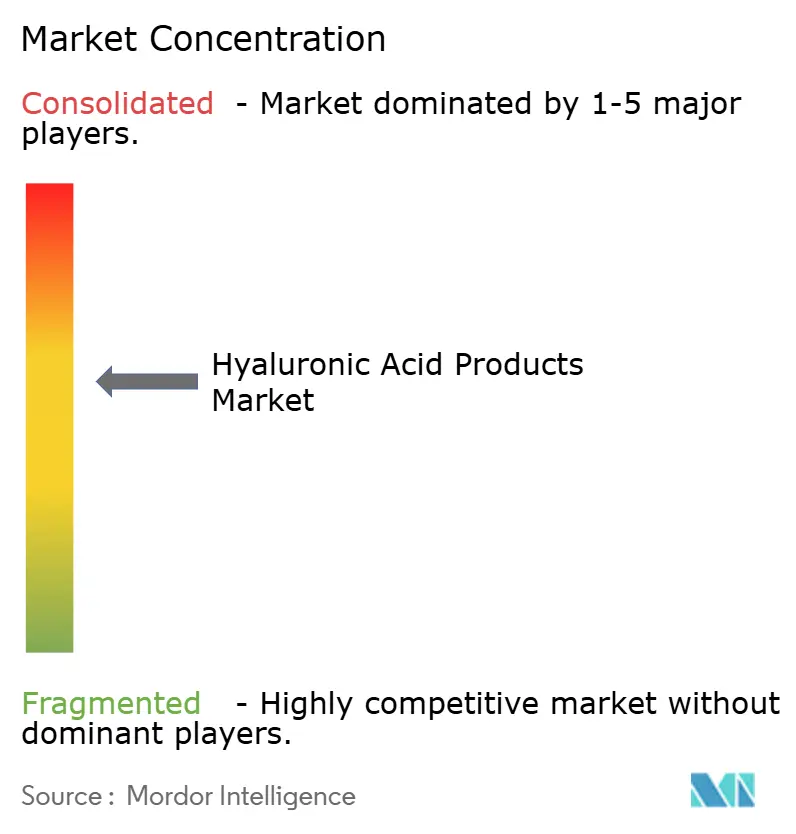

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Hyaluronic Acid Products Market Analysis by Mordor Intelligence

The Hyaluronic Acid Products market size is projected to expand from USD 2.04 billion in 2025 and USD 2.16 billion in 2026 to USD 2.84 billion by 2031, registering a 5.63% CAGR between 2026 and 2031. This growth is driven by the rising demand for products that offer gentle and effective hydration, supported by increasing clinical evidence of their benefits and clearer regulatory guidelines under the Modernization of Cosmetics Regulation Act. While facial care continues to lead in sales, there is a growing focus on hair care products, such as scalp serums and hyaluronic acid-infused shampoos, as part of the "skinification" trend, which applies skincare principles to hair care. Premium brands are differentiating themselves by developing advanced formulations with multi-molecular-weight hyaluronic acid. E-commerce is playing a significant role in market expansion, with subscription-based models and AI-driven tools helping consumers select personalized skincare solutions. The market remains moderately consolidated.

Key Report Takeaways

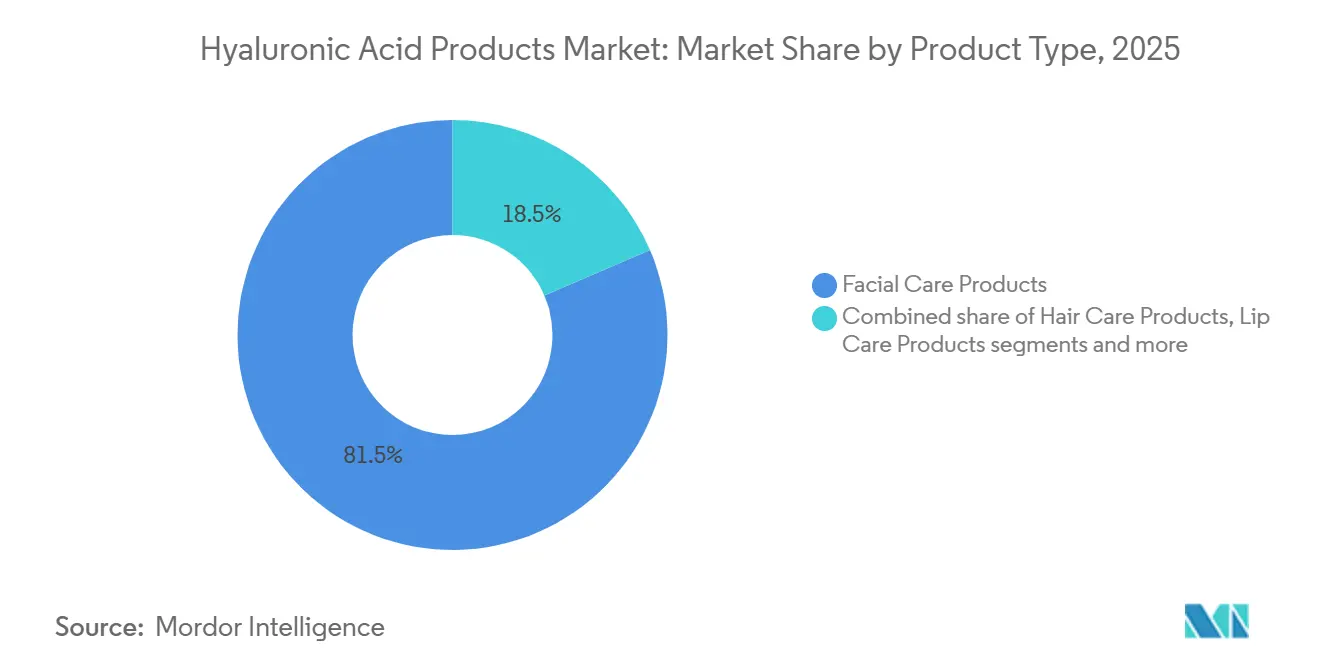

- By product type, facial care products accounted for 81.47% of the hyaluronic acid products market share in 2025, whereas hair care products are forecast to grow at a 6.14% CAGR through 2031.

- By price range, the mass segment accounted for 74.31% of the hyaluronic acid products market size in 2025, while premium products are poised to expand at a 6.57% CAGR to 2031.

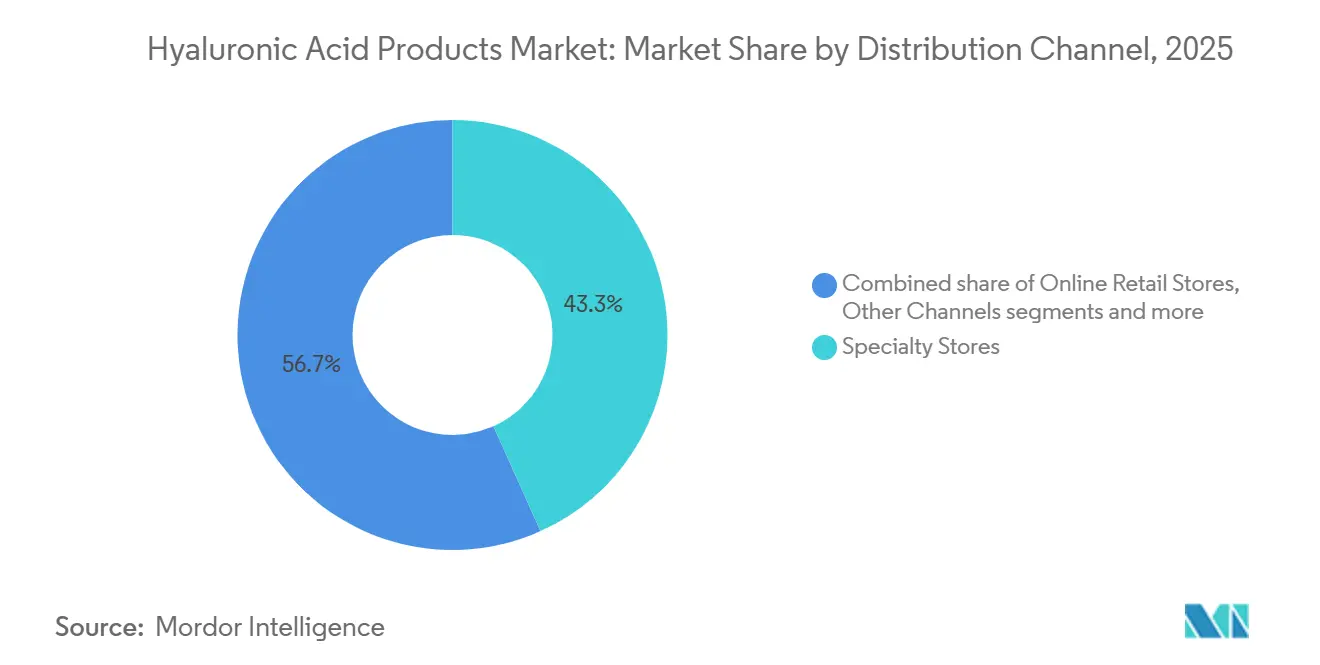

- By distribution channel, specialty stores led with 43.28% revenue share in 2025; online retail stores are projected to grow at a 7.48% CAGR, overtaking other offline formats by 2031.

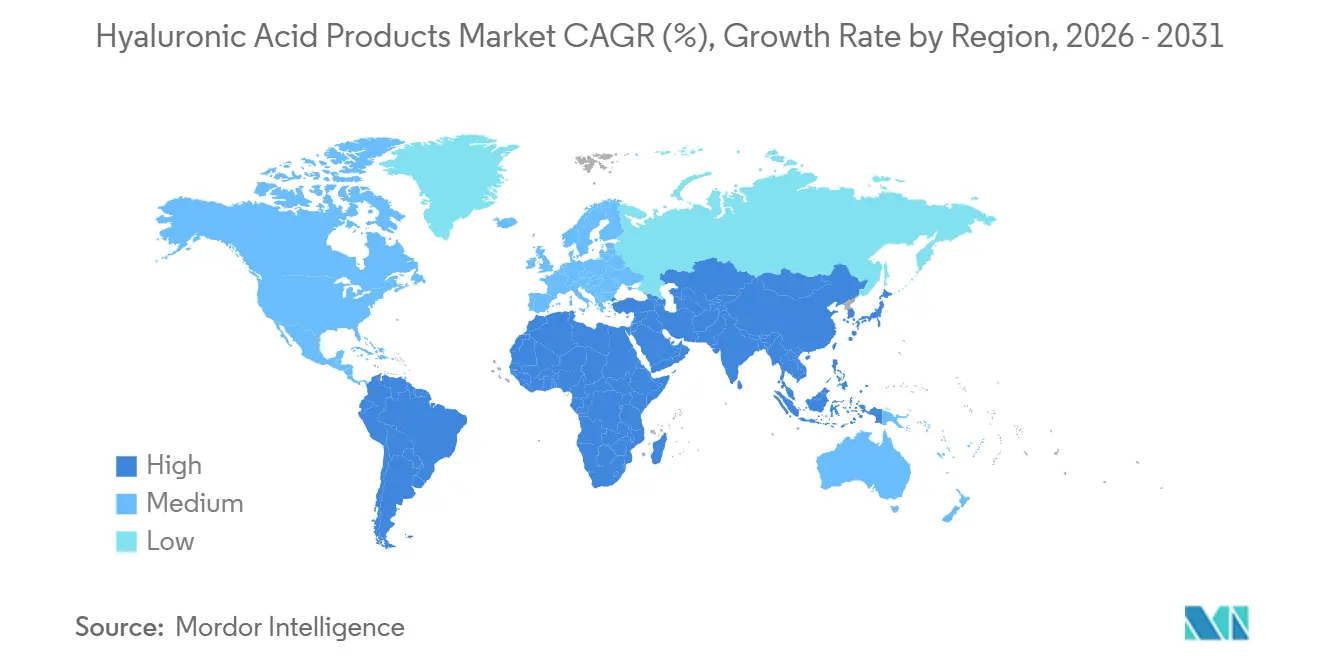

- By geography, North America contributed 41.25% of the hyaluronic acid products market share in 2025, whereas Asia-Pacific is projected to record a 6.53% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hyaluronic Acid Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of sensitive skin and dryness-related concerns | +0.9% | Global, with elevated incidence in North America and Europe | Medium term (2-4 years) |

| Awareness of anti-aging, plumping, and smoothing benefits across skin, lips, and hair | +1.2% | Global, particularly North America, Europe, and Asia-Pacific urban centers | Long term (≥ 4 years) |

| Growing exposure to harsh environmental conditions | +0.7% | Asia-Pacific urban areas, Middle East and Africa | Short term (≤ 2 years) |

| Preference for ingredient-led and science-backed beauty formulations | +0.8% | North America, Europe, and Asia-Pacific affluent segments | Medium term (2-4 years) |

| Expansion of premium, dermatologist-recommended, and salon-inspired product lines | +0.9% | North America, Europe, and Asia-Pacific tier-1 cities | Long term (≥ 4 years) |

| Growth of men's grooming and unisex beauty categories | +0.6% | Global, with accelerated adoption in Asia-Pacific and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of sensitive skin and dryness-related concerns

The rising prevalence of sensitive, dry skin is driving global demand for hyaluronic acid-based products. A 2024 study in Southeast Asia found that 86.9% of Thai consumers reported having sensitive skin, with 57.5% describing it as moderate to severe, according to a study published in PubMed Central[1]Source: PubMed Central, "Sensitive Skin in Thais: Prevalence, Clinical Characteristics, and Diagnostic Cutoff Scores",pmc.ncbi.nlm.nih.gov. This sensitivity is often caused by damage to the skin barrier from frequent use of strong active ingredients, leading to a need for gentle, hydrating solutions. Hyaluronic acid, known for holding up to 1,000 times its weight in water and being non-irritating, has become a key ingredient in daily skincare and post-procedure products. Its increasing use in facial serums and barrier repair products across both affordable and premium brands shows its growing importance and supports the steady growth of the global hyaluronic acid products market across different regions and income levels.

Awareness of anti-aging, plumping, and smoothing benefits across skin, lips, and hair

Awareness of hyaluronic acid's anti-aging, plumping, and smoothing benefits is growing, especially given the high prevalence of acne-related skin issues. In 2024, the International Journal of Pharmaceutical and Clinical Research reported that 68.5% of males and 59.6% of females experience acne, which can lead to barrier damage, inflammation, and dehydration[2]Source: International Journal of Pharmaceutical and Clinical Research, "Clinical Trends of Acne Vulgaris Patients in a Western India Tertiary Care Hospital: Descriptive Study", impactfactor.org. This has increased the demand for hyaluronic acid, which hydrates and smooths the skin without clogging pores or worsening breakouts. Its proven effectiveness in injectable treatments has raised expectations for topical products. The growing use of hyaluronic acid in acne-friendly serums, lip care products, and scalp treatments underscores its versatility. As consumers recognize its benefits beyond wrinkle reduction, such as skin recovery and texture improvement, hyaluronic acid is becoming a key ingredient in both mass and premium beauty products.

Preference for ingredient-led and science-backed beauty formulations

Consumers are increasingly choosing beauty products with simple, science-backed ingredients, and demand for natural options is growing. In 2024, 74% of consumers said organic ingredients are important in personal care products, according to NSF Organization[3]Source: NSF Organization, "74% of Consumers Consider Organic Ingredients Important in Personal Care Products", nsf.org. This trend shows that people, especially Millennials and Gen Z, are paying closer attention to ingredient lists and linking safety and effectiveness to clean, well-documented ingredients. Hyaluronic acid is a popular choice because it is scientifically proven, widely considered safe, and fits well with organic and clean-label trends. As a result, brands are focusing on creating clinically tested products to build trust, support higher prices, and meet consumer expectations for transparency and quality. This focus on transparency and science-backed claims is helping brands cater to the evolving preferences of informed and health-conscious consumers.

Growth of men’s grooming and unisex beauty categories

The popularity of men’s grooming and unisex beauty products is significantly driving the demand for hyaluronic acid products worldwide. Male consumers are increasingly looking for simple, all-in-one solutions, and hyaluronic acid serums are meeting this need by providing hydration, controlling oil, and soothing the skin after shaving in a single product. Unisex brands are also contributing to this trend by removing gender-specific features, such as fragrances, and promoting hyaluronic acid as a high-performance, versatile ingredient suitable for everyone. This shift is particularly evident in South Korea and Japan, where products like BB creams and scalp tonics have made daily skincare routines for men more common and socially accepted. In North America and Europe, the market is steadily growing, supported by increased shelf space in retail stores and targeted online marketing campaigns that appeal to a broader audience.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher formulation and testing costs associated with premium or multi-molecular-weight hyaluronic acid variants | -0.5% | Global, particularly North America and Europe with stringent regulatory requirements | Medium term (2-4 years) |

| Consumer skepticism around exaggerated or unclear efficacy claims | -0.4% | North America and Europe, with emerging scrutiny in Asia-Pacific | Short term (≤ 2 years) |

| Price sensitivity in mass and emerging markets | -0.6% | Asia-Pacific emerging economies, Latin America, Middle East and Africa | Long term (≥ 4 years) |

| Availability of alternative hydrating ingredients such as glycerin, ceramides, and panthenol | -0.3% | Global, with higher substitution in Mass segment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher formulation and testing costs associated with premium or multi-molecular-weight hyaluronic acid variants

Complex formulation processes and stringent regulatory testing requirements are slowing the growth of the global hyaluronic acid products market, particularly for premium and multi-molecular-weight variants. To meet the International Organization for Standardization (ISO) 22716 Good Manufacturing Practice standards, manufacturers must invest in advanced purification techniques, molecular weight profiling, and endotoxin control. These processes significantly increase development time and costs. Cross-linked and high-performance variants require thorough safety and performance validation, often involving third-party clinical testing, which adds further financial and operational burdens. These challenges create significant barriers for new entrants, making it difficult for smaller players to compete. While larger companies may benefit from economies of scale and outsourcing in the long term, the short-term impact on profitability remains a concern for the industry.

Consumer skepticism around exaggerated or unclear efficacy claims

Consumer skepticism about exaggerated or unclear product claims is becoming a significant challenge in the global hyaluronic acid products market. Many consumers are now more cautious due to increased regulatory actions by the Federal Trade Commission against misleading anti-aging claims. The lack of mandatory pre-market cosmetic approval under MoCRA, overseen by the United States Food and Drug Administration, allows vague or unsupported marketing claims to continue. As a result, consumers are paying closer attention to specific product details, such as molecular weight, formulation transparency, and how well the product suits their needs, rather than relying on broad promises like hydration or anti-aging benefits. Brands that fail to provide clear, evidence-backed information risk losing consumer trust and facing backlash on social media.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Facial Care Dominance Meets Hair Care Momentum

Facial care products led the hyaluronic acid products market in 2025, capturing 81.47% of the total market share. This dominance is due to the widespread use of hyaluronic acid in products like serums, moisturizers, masks, and cleansers, which address key concerns such as hydration, anti-aging, and skin barrier repair. The high frequency of daily use, strong recommendations from dermatologists, and ongoing advancements in multi-molecular weight formulations have solidified facial care as the most significant segment. Both mass-market and premium brands continue to innovate in this space to meet consumer demands.

Hair care products are the fastest-growing segment in the hyaluronic acid products market, with a projected CAGR of 6.14% through 2031. This growth is fueled by rising consumer interest in scalp health, moisture retention, and frizz management, particularly through products such as shampoos, conditioners, scalp serums, and leave-in treatments. The trend of incorporating skincare principles into hair care, along with the expansion of premium scalp care offerings, is driving adoption. Additionally, the relatively lower market penetration of hair care products compared to facial care suggests significant growth opportunities in the coming years.

By Price Range: Mass Accessibility Versus Premium Innovation

The mass segment is expected to maintain its dominance in the hyaluronic acid products market, accounting for 74.31% of the total market share in 2025. This segment's strong position is attributed to its affordability, widespread availability, and accessibility through mass retail outlets, drugstores, and online platforms. Consumers widely use hyaluronic acid-based products for skincare, haircare, and personal care in their daily routines, which further strengthens this segment's leadership. Additionally, continuous product innovation at competitive price points supports steady growth driven by high sales volumes.

On the other hand, the premium segment is anticipated to grow faster, with a projected CAGR of 6.57% from 2026 to 2031. This growth is fueled by increasing consumer preference for products with higher concentrations, advanced formulations, and proven clinical benefits. Premium brands are gaining traction due to their focus on anti-aging properties, dermatological advantages, and luxury appeal, especially among urban and high-income consumers. The influence of dermatologists and beauty influencers, along with the convenience of e-commerce platforms, further boosts the adoption of premium hyaluronic acid products.

By Distribution Channel: Specialty Expertise Meets Online Convenience

Specialty stores are the leading distribution channel in the hyaluronic acid products market, accounting for 43.28% of the total market share in 2025. These stores attract consumers by offering a carefully selected range of products, including dermo-cosmetic and premium brands. The availability of in-store experts who provide guidance and build trust further strengthens their position. Specialty stores are particularly popular for skincare and treatment-focused hyaluronic acid products, as customers value brand credibility and expert recommendations when making purchasing decisions.

On the other hand, online retail stores are expected to grow significantly, with a projected CAGR of 7.48% through 2031. This growth is fueled by increasing digital adoption, the convenience of shopping from home, and the availability of a wide range of products. Online platforms also allow brands to launch exclusive products, provide detailed information, and offer competitive pricing, making them appealing to both mass and premium product consumers. Additionally, the ease of doorstep delivery and the influence of digital marketing are driving more customers to shop for hyaluronic acid products online.

Geography Analysis

North America continues to lead the hyaluronic acid products market, holding 41.25% of the market share in 2025. This dominance is driven by high consumer awareness of skincare and aesthetic solutions, as well as significant spending on personal care products. The region benefits from a well-established network of clinics and advanced direct-to-consumer channels, which support the adoption of premium products. Additionally, mass-market offerings remain widely accessible through organized retail stores and online platforms, ensuring a broad consumer reach.

Asia-Pacific is expected to be the fastest-growing region, with a projected CAGR of 6.53% through 2031. The region's growth is fueled by rapid advancements in beauty and personal care formulations, as well as the increasing use of hyaluronic acid in cosmetics and wellness products. Key manufacturing hubs in the region also drive strong export activity. Furthermore, rising disposable incomes and the growing popularity of digital commerce in major economies like China and India are boosting demand for both mass-market and premium products.

Other regions, including Europe, South America, and the Middle East and Africa, contribute to steady market growth. Europe’s market is shaped by strict regulatory requirements, which influence product development and launch timelines. In South America, there is a strong demand for affordable cosmetic applications, while the Middle East and Africa see growing interest in skincare products due to climate-related needs and expanding urban retail networks. These regions collectively offer growth opportunities for both global and regional players in the market.

Regulatory Landscape

Regulatory requirements for hyaluronic acid products span cosmetics oversight and ingredient-level rules for ingestible uses, creating a fragmented compliance environment for global brands. In the United States, hyaluronic acid used in foods and supplements is commonly positioned through the FDA GRAS framework under the Federal Food, Drug, and Cosmetic Act, with FDA maintaining a GRAS notice inventory; one notable filing, GRAS Notice GRN 000976 for sodium hyaluronate, was later ceased at the notifier’s request, reinforcing that manufacturers retain responsibility for safety and substantiation even when FDA does not complete an evaluation.

In the European Union, uses that fall under food applications intersect with Novel Food Regulation (EU) 2015/2283, where ingredients not consumed significantly prior to May 1997 require authorization and inclusion in the Union list, supported by EFSA scientific assessment. In Asia, positive-list style frameworks provide clearer route-to-market for some applications: Japan lists hyaluronic acid as an Existing Food Additive (managed via the Japan Food Chemical Research Foundation), and China expanded permission by authorizing hyaluronic acid as a new food material in 2021, widening allowed uses beyond earlier health-food positioning. Across markets, tightening scrutiny of claims (including US FTC actions on misleading marketing) increases the need for evidence-backed labeling and performance substantiation for hyaluronic acid-containing finished products.

Competitive Landscape

The hyaluronic acid products market is moderately consolidated, with key players dominating both the supply and value chains. Suppliers specializing in fermentation processes play a crucial role in ensuring product quality, consistency, and molecular customization. These suppliers significantly influence the cosmetic and dermatology industries. Large companies, particularly those backed by beauty and pharmaceutical brands, benefit from their scale, strong branding, and established distribution networks. This creates high barriers for new entrants, although innovation-driven companies still find opportunities to compete.

Companies in this market are focusing on strategies such as vertical integration, proprietary technologies, and intellectual property protection to stay competitive. Many are developing advanced formulations, such as cross-linked hyaluronic acid structures and improved delivery systems, to enhance product performance and extend their lifecycle. Partnerships between ingredient manufacturers and product brands are becoming common, as they help speed up product development and ensure a steady supply of raw materials. Additionally, clinical validation and science-backed claims are now essential for maintaining credibility and securing a premium market position.

Meanwhile, smaller direct-to-consumer brands are changing the competitive landscape by emphasizing transparency and digital engagement. These brands use online platforms, third-party testing, and clear communication about ingredients to build trust with consumers, often without the high costs associated with traditional players. Tools like personalized recommendations, data-driven insights, and virtual product experiences are helping these brands strengthen customer relationships. Overall, success in the global hyaluronic acid products market depends on innovation, scientific rigor, and effective omnichannel strategies.

Hyaluronic Acid Products Industry Leaders

-

Kenvue Inc.

-

L'Oréal S.A.

-

Procter & Gamble Company

-

The Estée Lauder Companies

-

Beiersdorf AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace for hyaluronic acid products is the crossover between topical beauty routines and ingestible formats, supported by expanding regulatory permission for hyaluronic acid in functional food and beverage formulations in multiple jurisdictions. The EU’s Novel Food framework and EFSA assessments have established defined pathways for certain hyaluronic acid uses, while China’s 2021 authorization of hyaluronic acid as a new food material has helped normalize broader general-food applications under specific conditions, creating additional formulation and branding room for beauty-from-within concepts beyond traditional capsules.

On the supply side, opportunities concentrate around fermentation-based, standardized food-grade sodium hyaluronate with robust documentation packages that simplify multi-market commercialization. Established ingredient suppliers such as Kewpie (Fine Chemical) and Kikkoman Biochemifa publicly position food-grade sodium hyaluronate portfolios with specifications and regulatory support, which can accelerate B2B adoption by functional food brands and private-label programs. In finished goods, the market is also opening further in adjacent routine-led categories (for example, scalp serums and hyaluronic acid-infused shampoos under the skinification trend) and in online-first commercialization, where subscription models and AI-driven product selection tools create lower-friction trial and replenishment for mass and premium hyaluronic acid products.

Recent Industry Developments

- July 2026: L'Oreal updated its Revitalift Filler Hyaluronic Acid serum for the European market, positioning the formula around three types of hyaluronic acid alongside PDRN. The reformulation highlights continued competition around multi-weight hyaluronic acid systems and premium claim architecture in mass-premium facial care, the largest product segment by value.

- June 2025: WNP launched an All-in-One Hyaluronic Acid Skincare Set via its website, bundling a multi-step regimen into a single system built around technologies such as 4D hyaluronic acid and microencapsulation. The launch illustrates how direct-to-consumer brands use regimen packaging and differentiated delivery claims to raise basket size and improve repeat purchase in online channels.

- September 2024: SkinCeuticals (L'Oreal) introduced HA Intensifier Multi-Glycan, a hyaluronic acid serum positioned to improve hydration and plumpness while addressing fine lines. The product reinforces premiumization through clinically oriented positioning and supports category expansion beyond basic hydration toward multi-benefit anti-aging propositions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers finished consumer products that use hyaluronic acid as a key functional ingredient, and the value reflects sales of those products across major retail and online channels, as well as country-level demand patterns.

Scope exclusions: It does not count hyaluronic acid raw material sales, contract manufacturing fees, or professional-only injectable and ophthalmic uses that sit outside consumer product retailing.

Segmentation Overview

-

By Product Type

-

Facial Care Products

- Face Serums

- Cleansers

- Others

- Eye Care Products

- Lip Care Products

-

Hair Care Products

- Shampoo

- Conditioner

- Others

- Other Product Types

-

Facial Care Products

-

By Price Range

- Mass

- Premium

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Specialty Stores

- Online Retail Stores

- Other Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- United Kingdom

- Germany

- Spain

- France

- Italy

- Netherlands

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the initial demand and pricing logic, and then stress-tested it against public signals that move with skincare consumption. We mainly relied on public sources such as the US FDA cosmetics guidance pages, the EU Cosmetics Regulation resources, UN Comtrade trade statistics, World Bank macro series, and trade association publications related to personal care and dermatology products.

Alongside those, we reviewed company annual reports, investor presentations, earnings-call notes, and product launch coverage in reputed press to map how hyaluronic acid is positioned across mass and premium ranges. To tighten model inputs, we also referenced paid subscriptions used for company financials and intelligence, patent databases, and shipment-level import/export views where available. The sources listed here are illustrative, and many other public documents were read to fill gaps, validate assumptions, and clarify definitions.

Primary Interviews and Surveys

Primary work focused on cross-checking what desk sources cannot fully show, especially price ladders by channel, mix shifts between mass and premium, and the pace of online-led growth. We spoke with a balanced set of stakeholders, including brand-side commercial teams, distributors and retail channel specialists, and formulation and regulatory experts across APAC, EMEA, and the Americas, and then used their inputs to confirm the final scope and assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 12% | APAC: 45% |

| Mid tier: 42% | Functional/Unit leaders: 42% | EMEA: 30% |

| Smaller Players: 22% | Managers: 46% | Americas: 25% |

Market-Sizing & Forecasting

Market sizing starts with a top-down build where category demand is reconstructed from consumer product spend pools and channel splits, and then refined using hyaluronic-acid penetration cues inside facial, eye, lip, and hair care items. As the model is formed, selective bottom-up checks are used, such as sampled SKU price points by channel and a limited roll-up of visible brand revenues, which helps correct for mix and coverage gaps.

The inputs that mattered most included the share of facial care within total hyaluronic-acid product sales, online retail growth versus store-based channels, mass versus premium mix, regional adoption differences, and observed pricing progression for key formats like serums and creams. Where data is thin in smaller countries, the gaps are handled through proxy indicators like beauty and personal care spend trends and import intensity, and those ratios are re-tested with interview feedback. For forecasting, scenario analysis is used around channel growth and price mix, and the final path is kept consistent with expert views on promotional intensity and premiumization over the forecast window.

Data Validation & Update Cycle

Validation is done by comparing the modeled totals with independent signals such as category growth rates, trade flows for relevant finished goods, and observed shifts in online share, and then checking whether the implied per-capita consumption looks reasonable by region. When a variance shows up, we revisit the drivers step by step, which often means re-checking price ladders, channel shares, or regional mix and then recalculating the totals.

Before sign-off, the work goes through multiple analyst reviews so calculation logic, unit consistency, and assumptions are aligned to the written scope. Reports are refreshed annually, and interim updates are triggered when there are material events like major regulatory changes, sharp currency moves, or unusually large pricing resets in key channels. Right before delivery, a final pass is done so the numbers reflect the latest available public signals.

Mordor Intelligence's Hyaluronic Acid Products Market Size Versus Other Published Estimates

Published market sizes for hyaluronic acid products can vary a lot, even when the topic sounds similar, because each publisher draws the boundary in a different place and updates inputs on its own schedule. Differences usually come from what is counted as a product, how prices are averaged across channels, and the timing used for currency conversion.

In refresh-led reviews, the spread is often explained by how frequently average selling prices are re-checked, whether online discounting is captured, and if the latest FX rates are applied consistently across regions. By using a tight consumer-product scope, updating channel mix and ASP steps during the annual refresh, and re-contacting experts when a price or share shift looks unusual, the sizing stays anchored to what is actually sold in retail, which is the main reason the 2026 value reported by Mordor Intelligence sits far below broader figures that fold in injections and ophthalmic uses.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.16 B (2026) | |

| Industry Publisher A | USD 9.50 B (2024) | Uses a wider definition that includes medical and clinical categories like injections and eye drops, and it also extends into other HA uses beyond consumer personal care, which lifts the total addressable value. |

| Global Publisher B | USD 11.00 B (2024) | Focuses largely on injection-cycle products and clinical applications (such as osteoarthritis and dermal fillers), so the number reflects a therapy-led market rather than only finished consumer skincare and hair care products. |

The table shows that scope boundaries are the biggest driver, and pricing and currency timing decisions tend to widen the gap further. When the same product set is kept consistent and channel-weighted prices are updated in a repeatable way, the resulting market size becomes easier to trace back to clear inputs and to validate year over year.

Key Questions Answered in the Report

What is the projected value of the Global Hyaluronic Acid Products market by 2031?

It is forecast to reach USD 2.84 billion by 2031, growing at a 5.63% CAGR between 2026 and 2031.

Which product category currently generates the highest revenue?

Facial Care Products lead with 81.47% of market share in 2025.

Which region is expected to post the fastest growth through 2031?

Asia-Pacific is projected to expand at a 6.53% CAGR, driven by regulatory approvals and K-beauty exports.

How quickly is the online channel growing?

Online Retail Stores are advancing at a 7.48% CAGR, fueled by subscriptions and AI-based diagnostics.

Page last updated on: