North America Cannabidiol (CBD) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

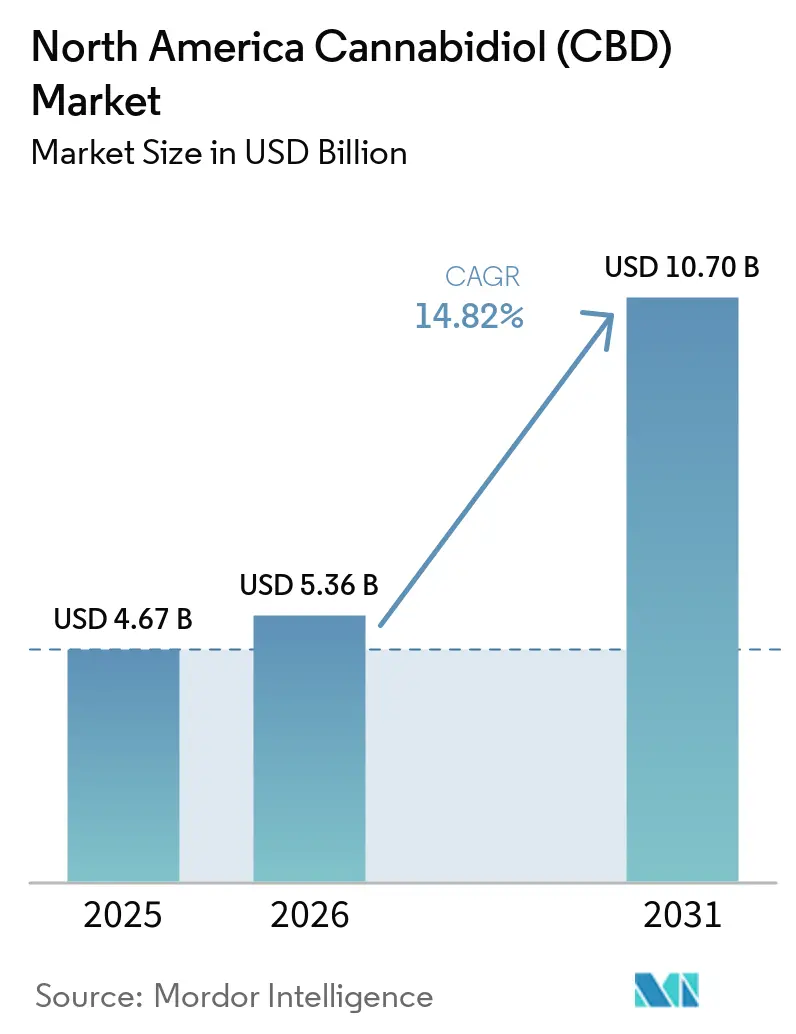

| Base Year Market Size (2025) | USD 4.67 Billion |

| Market Size (2026) | USD 5.36 Billion |

| Market Size (2031) | USD 10.70 Billion |

| Growth Rate (2026 - 2031) | 14.82% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Cannabidiol (CBD) Market Analysis by Mordor Intelligence

The North America Cannabidiol Market size is expected to increase from USD 4.67 billion in 2025 to USD 5.36 billion in 2026 and reach USD 10.70 billion by 2031, growing at a CAGR of 14.82% over 2026-2031.

The market is moving beyond a narrow wellness niche because physician-directed access is starting to connect compliant products with formal care pathways and healthcare spending flows. Eligible hemp-derived CBD products entered a federal physician-directed reimbursement pathway for participating Medicare care models in 2026, which widened the commercial ceiling for compliant suppliers and raised the value of clinical documentation. The category is also benefiting from stronger retail normalization, wider omnichannel placement, and faster digital conversion, which together favor brands that can support repeat purchases and channel consistency. Charlotte’s Web tied its 2025 growth to broader marketplace reach, while cbdMD continued to show the importance of direct digital revenue, which indicates that distribution quality now matters as much as brand awareness in the North America cannabidiol (CBD) market. Competition remains fragmented, yet recent acquisitions, balance sheet restructuring, and clinical platform building show that the next phase of expansion will favor brands with compliance depth, formulation credibility, and staying power.

Key Report Takeaways

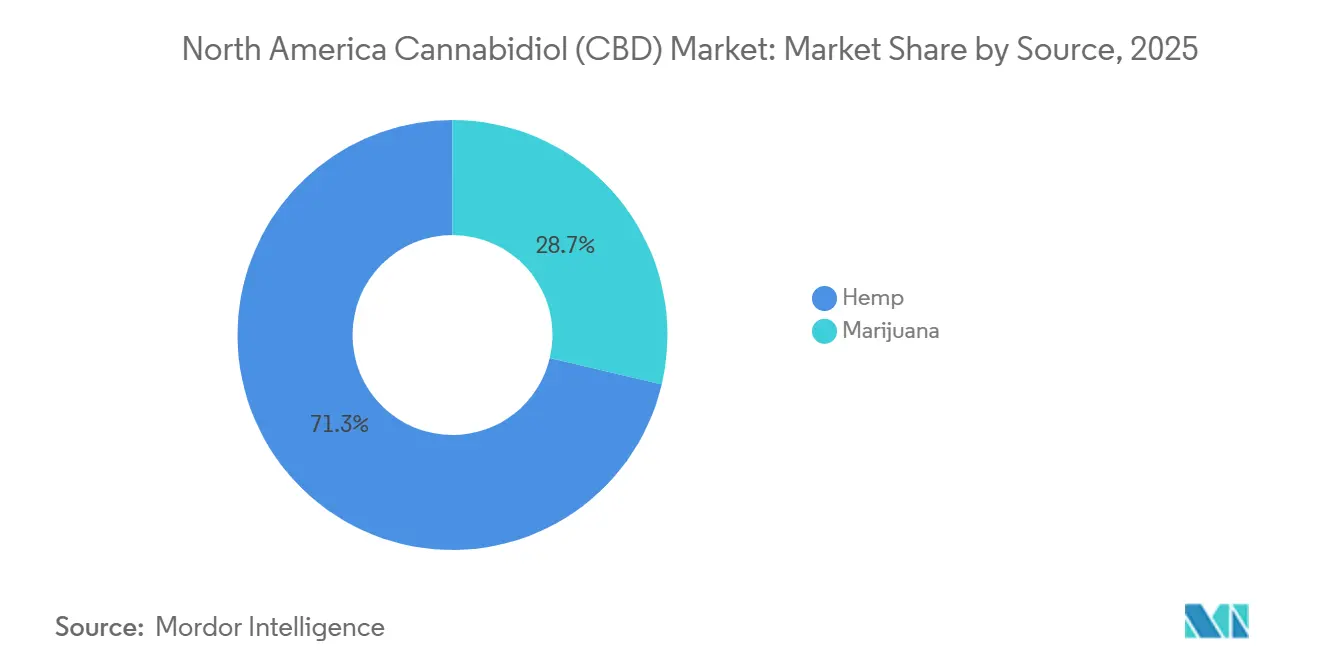

- By source, hemp led with a 71.31% share in 2025, while marijuana-derived CBD is forecast to expand at a 17.38% CAGR through 2031.

- By end use, wellness and personal use held a 32.24% share in 2025, while pet care is expected to have the highest CAGR at 16.52% through 2031.

- By product form, gummies and confectionery accounted for a 28.52% share in 2025, while topicals and skin care are expected to advance at a 16.25% CAGR through 2031.

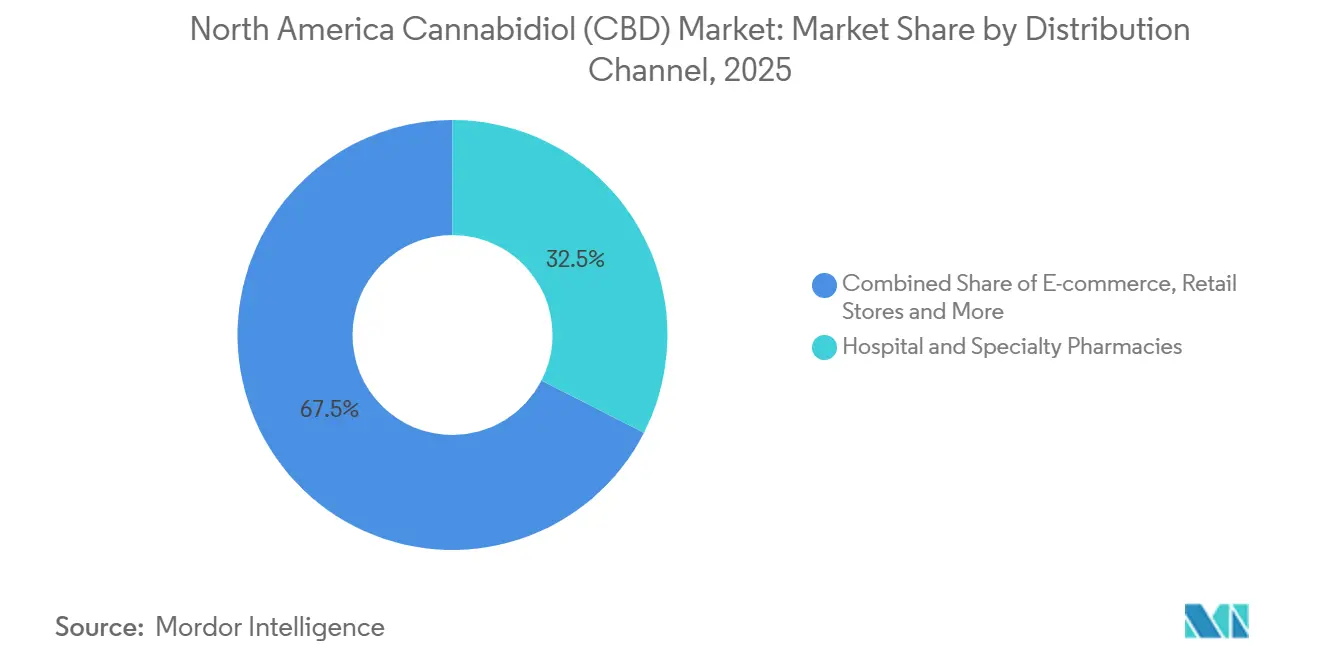

- By distribution channel, hospital and specialty pharmacies held a 32.52% share in 2025, while e-commerce is projected to grow at an 18.25% CAGR through 2031.

- By geography, the United States held a 40.22% share in 2025, while Mexico is projected to expand at a 16.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Cannabidiol (CBD) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Clinical Adoption in Pain and Anxiety Management | +2.1% | United States (primary), Canada | Medium term (2-4 years) |

| Retail Normalization of Hemp-Derived CBD Products | +2.8% | United States, Canada | Short term (≤ 2 years) |

| Strong Pull from Pet Wellness and Veterinary Adjacent Use Cases | +1.5% | North America (US-dominant) | Medium term (2-4 years) |

| Product Innovation in Gummies, Softgels, and Beverages | +2.0% | United States, Canada | Short term (≤ 2 years) |

| Rising Demand for Third-Party Tested, Traceable CBD Formulations | +1.3% | United States (primary) | Short term (≤ 2 years) and Medium term (2-4 years) |

| E-Commerce and Direct-to-Consumer Brand Scaling | +2.5% | United States, Canada, Mexico | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expanding Clinical Adoption In Pain And Anxiety Management

The North America cannabidiol (CBD) market is gaining support from a clearer clinical use case in anxiety, sleep disturbance, and related care settings. A 2024 multicenter randomized clinical trial reported that nanodispersible CBD reduced GAD-7 anxiety scores by 7.02 points versus placebo, while also improving sleep quality and depression measures. Clinical development is also continuing in academic settings, with the University of Florida trial on CBD for anxiety and sleep disturbance moving through Phase 2 and targeting primary completion by late 2026[1]ClinicalTrials.gov, “Use of CBD in the Treatment of Anxiety,” ClinicalTrials.gov, clinicaltrials.gov. Federal policy direction also turned more favorable in late 2025 when the White House instructed agencies to prioritize cannabidiol research and widen physician access pathways. This matters for the North America cannabidiol (CBD) market because brands with stronger evidence, cleaner documentation, and more disciplined manufacturing can move closer to physician recommendation instead of depending only on paid consumer outreach. It also changes brand positioning, since clinical readiness now affects reimbursement access, pharmacy acceptance, and the ability to compete in healthcare-linked channels.

Retail Normalization Of Hemp-Derived CBD Products

The North America cannabidiol (CBD) market is also benefiting from a broader shift toward normalized retail access across major digital and mainstream channels. As large retailers and marketplace operators bring CBD into regular assortment logic, shelf access becomes a quality filter instead of a simple distribution win. Charlotte’s Web said its 2025 growth was supported by expanded presence on Walmart.com, Amazon, and Faire, which showed that broad retail integration is now a basic requirement for scale. This shift does not make competition easier, because tighter assortment rules can push weaker products out of the category and give compliant brands more durable visibility. The North America cannabidiol (CBD) market therefore looks more tiered in 2026, with better-tested and better-documented products holding a clearer path to retention in normalized retail environments.

Strong Pull From Pet Wellness And Veterinary Adjacent Use Cases

The North America cannabidiol (CBD) market is seeing a durable demand push from pet care, which remains one of the clearest higher-growth use cases in the category. Pet care is already the fastest-growing end-use segment, and the appeal is tied to premium spending on companion animal health, behavior support, and pain management. Health Canada’s 2025 consultation showed strong veterinary interest, with 90 of 135 submissions focused on veterinary drugs containing CBD, which suggests that the professional channel wants a formal pathway rather than informal use. That shift matters because a formal veterinary route would move part of demand from casual consumer purchase toward clinician-guided product selection and stronger product standards. The North America cannabidiol (CBD) market could therefore see pet-focused brands gain pricing support, better repeat demand, and stronger channel credibility as veterinary use becomes more structured. The same trend also supports specialization, because pet formulas, dosing formats, and safety expectations differ from mainstream adult wellness products.

E-Commerce And Direct-To-Consumer Brand Scaling

The North America cannabidiol (CBD) market continues to gain momentum from e-commerce, which is the fastest-growing distribution channel through 2031. This growth is not only a volume story, because digital leaders also gain tighter control over pricing, product education, subscription retention, and first-party customer data. cbdMD reported direct-to-consumer net sales of USD 3.8 million in Q2 fiscal year 2026, equal to 67% of total revenue, which showed that direct digital sales still carry major weight inside the operating model. The North America cannabidiol (CBD) market also favors brands that can turn first purchases into subscription demand, because repeat-use products reward consistency, convenience, and trusted replenishment cycles. Established operators therefore gain a structural advantage when they combine digital storefronts, marketplace placement, and offline visibility instead of relying on a single sales path. This is especially important in a category where education, reassurance, and proof of quality often drive the second and third purchase more than the first one.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patchwork State and Federal Compliance Requirements | -1.8% | United States (primary), Canada | Long term (≥ 4 years) |

| Ongoing Banking, Payments, and Insurance Frictions for CBD Brands | -1.2% | United States (primary), Canada | Medium term (2-4 years) |

| Price Erosion from Hemp Biomass Oversupply and Private Labeling | -0.9% | United States, Canada | Short term (≤ 2 years) |

| Restrictive Labeling, Claims, and Advertising Enforcement | -0.7% | United States (primary) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Patchwork State And Federal Compliance Requirements

The North America cannabidiol (CBD) market still faces a serious drag from uneven compliance rules across jurisdictions and channels. Medterra said California Assembly Bill 8 will halt its THC-containing product sales in the state after July 1, 2026, which shows how state-level action can quickly disrupt existing product portfolios[2]Medterra, “California Regulatory Update,” Medterra, medterracbd.com. Canada is moving through a different process, with consultation and streamlining steps that point to a more defined product pathway, but that contrast also highlights how uneven the regional framework remains. Larger operators can absorb reformulation work, compliance review, and slower approval timing more easily than smaller brands can. This means the North America cannabidiol (CBD) market may continue to consolidate, not only because demand is rising, but because the cost of staying compliant keeps increasing.

Price Erosion From Hemp Biomass Oversupply And Private Labeling

The North America cannabidiol (CBD) market also remains exposed to price pressure from earlier oversupply and the steady growth of private-label activity. Even when consumer demand improves, upstream margin recovery can lag because too many suppliers still compete on low-price extract and simple me-too formulations. This matters most for businesses that lack strong formulation identity, clinical support, or brand trust, since those operators are easier to replace in both retail and online channels. The result is a weaker pricing floor for commodity-style products and a wider performance gap between premium brands and undifferentiated sellers. The North America cannabidiol (CBD) market therefore rewards companies that can defend value through certification, channel fit, product quality, and better use-case clarity rather than price-per-milligram alone.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Hemp Remains The Volume Base While Marijuana-Derived CBD Gains Faster Momentum

Hemp accounted for 71.31% of the North America cannabidiol (CBD) market share in 2025, which kept it firmly ahead of marijuana-derived CBD on a revenue basis. This lead reflects the scale advantage built around hemp cultivation, extraction capacity, established supply routes, and wider compatibility with mainstream wellness positioning across the region. In the North America cannabidiol (CBD) industry, hemp also fits more easily into broad retail and e-commerce models because it has already been normalized for a larger set of commercial use cases. That installed base gives hemp-derived products a strong presence across oils, gummies, capsules, topicals, and pharmacy-adjacent formats that need consistency and familiar sourcing. It also means the largest share of the North America cannabidiol (CBD) market still rests on suppliers that can manage agricultural inputs, extraction standards, and quality documentation at scale.

Marijuana-derived CBD is projected to grow at a 17.38% CAGR through 2031, which places it ahead of the overall market pace and shows that demand is broadening beyond the largest source category. Part of that growth comes from adult-use cannabis settings where consumers often prefer fuller cannabinoid profiles and perceive those formulations as more potent or more complete. The White House focus on expanding cannabinoid research also gives more visibility to clinically oriented development pathways, which may support higher-value formulations across both source groups over time[3]The White House, “Increasing Medical Marijuana and Cannabidiol Research,” The White House, whitehouse.gov. The North America cannabidiol (CBD) market therefore has a dual structure by source, with hemp preserving the larger commercial base and marijuana-derived CBD widening the premium growth lane. This balance matters because it keeps scale economics centered in hemp while allowing faster-growth demand pockets to emerge where clinical perception, channel rules, and consumer preference favor differentiated cannabinoid origin.

By End Use: Wellness Anchors Current Demand While Pet Care And Pharmaceuticals Lift Strategic Value

Wellness and personal use held 32.24% of the market in 2025, which made it the largest end-use category in the North America cannabidiol (CBD) market. This segment remains the volume anchor because it connects CBD with sleep support, stress management, exercise recovery, and familiar daily wellness routines. It is also the easiest category for brands to position across multiple formats, which helps explain why gummies, tinctures, capsules, and topical products all feed into this same demand pool. The broad reach of wellness and personal use gives companies a large consumer entry point, but it also creates more direct price competition and faster imitation. For that reason, brands in the North America cannabidiol (CBD) market often use formulation layering, ingredient pairing, and stronger quality signals to stand out within the largest end-use base.

Pet care is projected to grow at a 16.52% CAGR through 2031, which gives it the strongest growth outlook among end-use segments and shows how quickly the use case is becoming mainstream. Health Canada’s consultation process signaled material interest in veterinary CBD pathways, which supports the idea that pet demand is moving closer to formal professional oversight. Pharmaceuticals also carry strategic weight because physician-directed reimbursement pathways can convert part of CBD demand from discretionary spending into budgeted care spending. That shift matters for the North America cannabidiol (CBD) market because clinical channels place more value on documentation, standardization, and formulation discipline than consumer-led channels do. The end-use structure therefore mixes a large and steady wellness base with two value-accretive lanes, one in pet care and one in pharmaceuticals, that can improve pricing quality and channel defensibility.

By Product Form: Gummies Lead Adoption While Topicals Build A Stronger Clinical Case

Gummies and confectionery held a 28.52% share in 2025, which made them the leading product form in the North America cannabidiol (CBD) market. Their position is tied to precise dosing, discreet consumption, broad familiarity, and easier onboarding for consumers who do not want tinctures or inhaled formats. Gummies also support brand extension because companies can combine CBD with adjacent ingredients and create distinct use-case messages around sleep, calm, recovery, or daily balance. This keeps the format commercially attractive even as the field becomes more crowded, since format familiarity lowers the barrier to trial. In the North America cannabidiol (CBD) industry, gummies continue to function as both a customer acquisition format and a premiumization vehicle when brands add functional ingredients and sharper positioning.

Topicals and skin care are projected to grow at a 16.25% CAGR through 2031, which makes them the fastest-growing form and gives them a different role inside the portfolio mix. This growth reflects demand for localized use cases, stronger interest in anti-inflammatory and skincare applications, and better fit with pharmacy-style recommendations. The North America cannabidiol (CBD) market also benefits when topicals are paired with more evidence-backed delivery approaches, because clinically defensible differentiation matters more as healthcare-linked channels expand. Oils and tinctures still retain importance for experienced users who value dose control and flexible use, while capsules and softgels fit better with standardized routines and a more medical presentation. The product form structure therefore shows a clear split, with gummies holding the broadest consumer reach and topicals, capsules, and other format-specific products shaping the next stage of category depth.

By Distribution Channel: Pharmacy-Led Credibility Supports Share While E-Commerce Expands Reach

Hospital and specialty pharmacies accounted for 32.52% of the North America cannabidiol (CBD) market size in 2025, which made them the largest distribution channel in the regional mix. This leadership reflects the value of pharmacist review standards, product documentation, and tighter confidence around compliant, clearly labeled, and consistently manufactured items. The 2026 physician-directed reimbursement pathway strengthens this channel further because it gives more weight to products that meet formal healthcare expectations and can be integrated into supervised care models. In practice, that creates a self-reinforcing quality loop where better-documented brands gain better shelf access, and better shelf access improves trust, repeat use, and healthcare visibility. For the North America cannabidiol (CBD) market, pharmacy strength is therefore not only a channel share story, but also a signal that compliance and clinical credibility are becoming commercial assets.

E-commerce is forecast to grow at an 18.25% CAGR through 2031, which makes it the fastest-growing channel and one of the clearest engines of volume expansion. Digital channels work well for education-heavy products, because companies can explain dosage, use cases, ingredients, and testing detail in more depth than many physical shelves allow. cbdMD’s 2026 results showed how direct digital revenue remains central to operating performance, especially when brands use subscriptions and repeat-order systems to extend customer lifetime value. Retail stores still matter because they remain an important trial point for new buyers, while specialty outlets and practitioner channels serve more selective consumers who want curated products and stronger trust cues. The distribution picture in the North America cannabidiol (CBD) market is therefore not a simple shift from offline to online, but a layered system where pharmacies build trust, e-commerce builds scale, and physical retail supports discovery.

Geography Analysis

The United States accounted for 40.22% of regional revenue in 2025, which kept it at the center of the North America cannabidiol (CBD) market. Its lead is supported by a deeper wellness retail base, broader e-commerce activity, and stronger visibility of branded CBD products across multiple channels. The most important recent change is the opening of a physician-directed reimbursement route for eligible hemp-derived products within approved Medicare-linked care settings. That change matters because it gives compliant suppliers a path into healthcare decision flows instead of leaving the category tied only to consumer self-selection. It also raises the commercial value of evidence, quality assurance, and pharmacy acceptance in the North America cannabidiol (CBD) market.

Mexico is the fastest-growing country segment with a 16.15% CAGR through 2031, which shows that the regional story is no longer limited to the United States and Canada. Its smaller starting base creates more room for acceleration as formal product access improves and compliant cross-border supply options expand. Demand in Mexico is still earlier in its development, but the opportunity is increasingly visible for companies that can navigate import, registration, and product-quality expectations. This makes Mexico an important medium-term growth lever for the North America cannabidiol (CBD) market, especially for brands that already understand regulated product categories. The commercial appeal is stronger for suppliers with disciplined compliance systems, because faster growth alone does not remove the need for product standardization and trust.

Canada remains a structurally important part of the North America cannabidiol (CBD) market because the country combines high cannabis familiarity with an active policy discussion on non-prescription cannabidiol pathways. Health Canada gathered 135 submissions during its consultation process and later summarized broad stakeholder views on how CBD products might fit into a more accessible health product framework. The March 2025 streamlining amendments also showed that regulators are willing to reduce some process burden within the cannabis framework. If a clearer over-the-counter pathway is adopted, Canada could convert existing familiarity into faster uptake of standardized CBD formats sold through more conventional retail and health channels.

Competitive Landscape

The North America cannabidiol (CBD) market remained fragmented in 2026, but the shape of competition is becoming clearer and more disciplined. A top tier of science-backed and omnichannel brands is separating itself from a wider field of private-label and less differentiated sellers. This separation is being driven by compliance depth, clinical ambition, manufacturing quality, and access to stronger retail and pharmacy relationships. The North America cannabidiol (CBD) market therefore looks less like a broad race for awareness and more like a contest over documentation, distribution quality, and capital strength. That shift is visible in the kinds of strategic moves that leading companies are making across acquisition, restructuring, and healthcare channel development.

cbdMD strengthened its position in January 2026 through the acquisition of Bluebird Botanicals, which added GRAS-status full-spectrum formulation intellectual property and an established e-commerce customer base. Charlotte’s Web also reshaped its balance sheet through a March 2026 transaction with British American Tobacco, which included debenture conversion and a USD 10 million equity investment to strengthen financial flexibility. Those moves matter because they support product development, channel expansion, and the ability to absorb compliance costs that smaller brands may struggle to carry. Another example came in March 2026 when Splash Beverage Group signed a letter of intent for acquisition and merger with Medterra, which showed that outside categories also view CBD platforms as valuable commercial assets. The North America cannabidiol (CBD) market is therefore consolidating through transactions that are aimed less at simple scale and more at channel access, formulation assets, and strategic optionality.

The competitive white space in the North America cannabidiol (CBD) market is increasingly centered on products that can satisfy both consumer convenience and clinical scrutiny. Water-soluble formats, pharmacy-friendly presentations, and delivery systems with clearer performance logic are likely to command more attention than undifferentiated commodity products. Smaller brands can still win by owning a narrow position, such as transparency, organic credentials, price-value balance, or specialist use-case focus. Even so, the market is becoming harder for sellers that lack proof of quality, repeatable channel execution, or a clear reason to be chosen over a larger peer. The practical result is that the North America cannabidiol (CBD) market remains fragmented on paper, while real competitive power is concentrating among companies that can pair brand reach with evidence, compliance, and better capital support.

North America Cannabidiol (CBD) Industry Leaders

Canopy Growth Corporation

Charlotte’s Web Holdings, Inc.

Tilray Brands, Inc.

CV Sciences, Inc.

Medterra CBD

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: cbdMD launched a dedicated clinical healthcare channel to support the CMS Beneficiary Engagement Incentive (BEI) pathway, engaging accountable care organizations, oncology practices, and health systems. Eligible hemp-derived CBD products can be furnished to Medicare beneficiaries up to USD 500 annually under physician supervision.

- April 2026: The FDA took a significant step in its approach to CBD regulation by introducing an enforcement discretion policy. This policy allows orally administered, hemp-derived CBD products to be provided to Medicare patients, but only under the supervision of a treating physician. To comply, products must meet four key criteria, including following GMP manufacturing standards and ensuring they are not marketed to children.

North America Cannabidiol (CBD) Market Report Scope

As per the scope of the report, Cannabidiol (CBD) is a naturally occurring compound found in the cannabis plant. It is one of the many cannabinoids present in cannabis and is known for its potential therapeutic properties.

The segmentation for the North America Cannabidiol (CBD) market is categorized by source, end use, product form, distribution channel, and country. By source, the market is divided into hemp and marijuana. By end use, it includes pharmaceuticals, wellness and personal use, food and beverages, cosmetics and skin care, pet care, and other end uses. By product form, the segmentation covers oils and tinctures, capsules and softgels, gummies and confectionery, topicals and skin care, and other product forms. By distribution channel, the market is segmented into hospital and specialty pharmacies, retail stores, e-commerce, and other distribution channels. By country, the segmentation includes the United States, Canada, and Mexico. For each segment, the market size and forecast are provided in terms of value (USD).

| Hemp |

| Marijuana |

| Pharmaceuticals |

| Wellness and Personal Use |

| Food and Beverages |

| Cosmetics and Skin Care |

| Pet Care |

| Other End Use |

| Oils and Tinctures |

| Capsules and Softgels |

| Gummies and Confectionery |

| Topicals and Skin Care |

| Other Product Forms |

| Hospital and Specialty Pharmacies |

| Retail Stores |

| E-commerce |

| Other Distribution Channels |

| United States |

| Canada |

| Mexico |

| By Source | Hemp |

| Marijuana | |

| By End Use | Pharmaceuticals |

| Wellness and Personal Use | |

| Food and Beverages | |

| Cosmetics and Skin Care | |

| Pet Care | |

| Other End Use | |

| By Product Form | Oils and Tinctures |

| Capsules and Softgels | |

| Gummies and Confectionery | |

| Topicals and Skin Care | |

| Other Product Forms | |

| By Distribution Channel | Hospital and Specialty Pharmacies |

| Retail Stores | |

| E-commerce | |

| Other Distribution Channels | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the 2026 size of the North America cannabidiol (CBD) space?

The North America cannabidiol (CBD) market stood at USD 5.36 billion in 2026 and is projected to reach USD 10.70 billion by 2031 at a 14.82% CAGR, based on the figures provided in the draft.

Which source category leads revenue in North America cannabidiol (CBD)?

Hemp led the source mix with a 71.31% share in 2025, reflecting its larger cultivation, extraction, and commercial infrastructure across the region.

Which end-use category is growing the fastest for CBD in North America?

Pet care is projected to record the fastest end-use growth at a 16.52% CAGR through 2031, supported by rising premium pet health spending and stronger veterinary interest.

Why are hospital and specialty pharmacies important for CBD brands?

Hospital and specialty pharmacies held a 32.52% share in 2025 and matter because channel acceptance increasingly depends on product quality, documentation, and healthcare-facing credibility.

Which country offers the fastest growth outlook in the region?

Mexico is expected to post the fastest country-level expansion at a 16.15% CAGR through 2031, which points to meaningful medium-term upside from a smaller base.

What is changing competition among leading CBD companies in North America?

Competition is shifting toward clinical readiness, compliance depth, and channel strength, as seen in cbdMDs Bluebird Botanicals acquisition, Charlottes Webs BAT-backed restructuring, and the Splash Beverage LOI with Medterra.

Page last updated on: