Medicinal Mushroom Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.48 Billion |

| Market Size (2031) | USD 12.79 Billion |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medicinal Mushroom Market Analysis by Mordor Intelligence

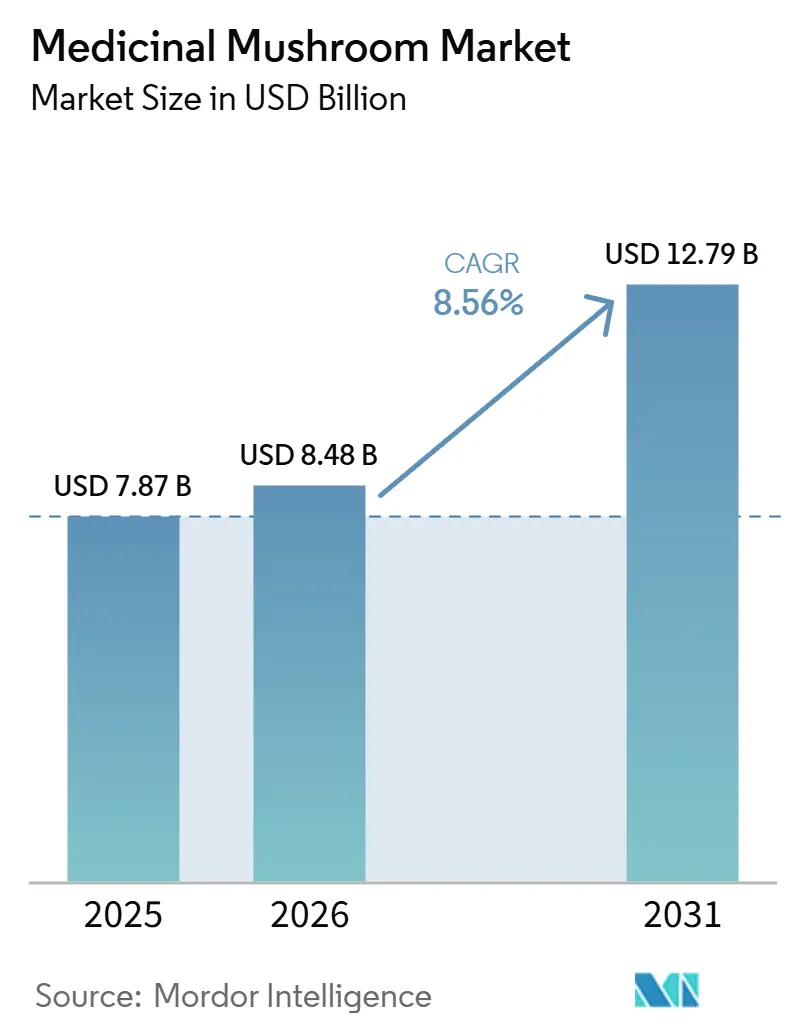

The Medicinal Mushroom Market size is projected to expand from USD 7.87 billion in 2025 and USD 8.48 billion in 2026 to USD 12.79 billion by 2031, registering a CAGR of 8.56% between 2026 to 2031.

Demand keeps rising as more consumers treat immune health, cognitive support, and stress management as part of routine preventive care rather than occasional treatment. The medicinal mushroom market is also benefiting from wider use of mushroom bioactives in beverages, snacks, powders, capsules, and other daily wellness formats that are easier for mainstream buyers to adopt. Product quality is becoming a stronger value driver because clinically studied extracts, fruiting-body-only formulations, and standardized beta-glucan content support premium pricing and stronger shelf credibility in the medicinal mushroom market. Competition remains active because a long tail of digital-first brands is pushing category access wider, while vertically integrated suppliers are using traceability and testing to stand apart, a pattern highlighted by Real Mushrooms’ 2026 acquisition of Mushroom Science. Even with that momentum, the medicinal mushroom market still faces uneven regulation and adulteration risk across sourcing and claims, yet ongoing clinical work, stronger testing methods, and steady supplement spending continue to support broad growth through 2031.

Key Report Takeaways

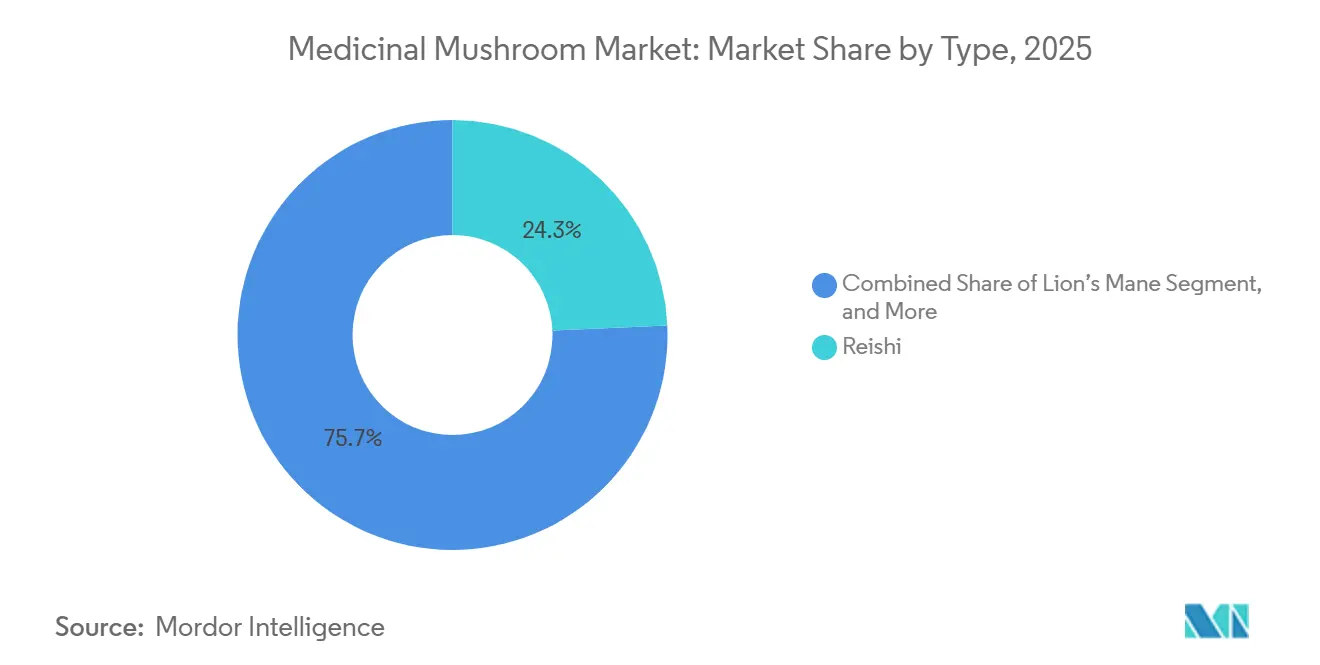

- By type, reishi held 24.32% of revenue in 2025, while Lion’s Mane recorded the highest projected CAGR at 9.39% through 2031.

- By form, extracts accounted for 38.23% of revenue in 2025, while Capsules and Tablets are forecast to expand at an 8.76% CAGR through 2031.

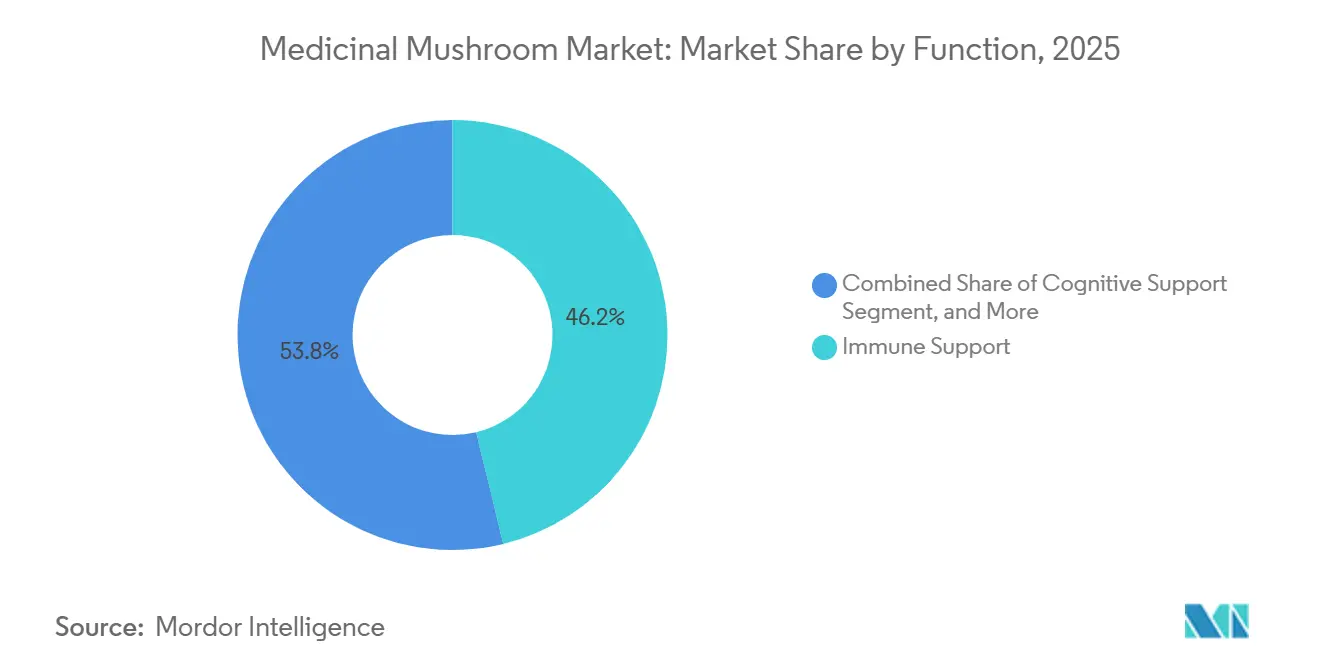

- By function, immune support led with 46.16% of revenue in 2025, while Cognitive Support is projected to advance at a 10.57% CAGR through 2031.

- By distribution channel, online retail held 41.63% of revenue in 2025 and also posted the fastest projected CAGR at 9.94% through 2031.

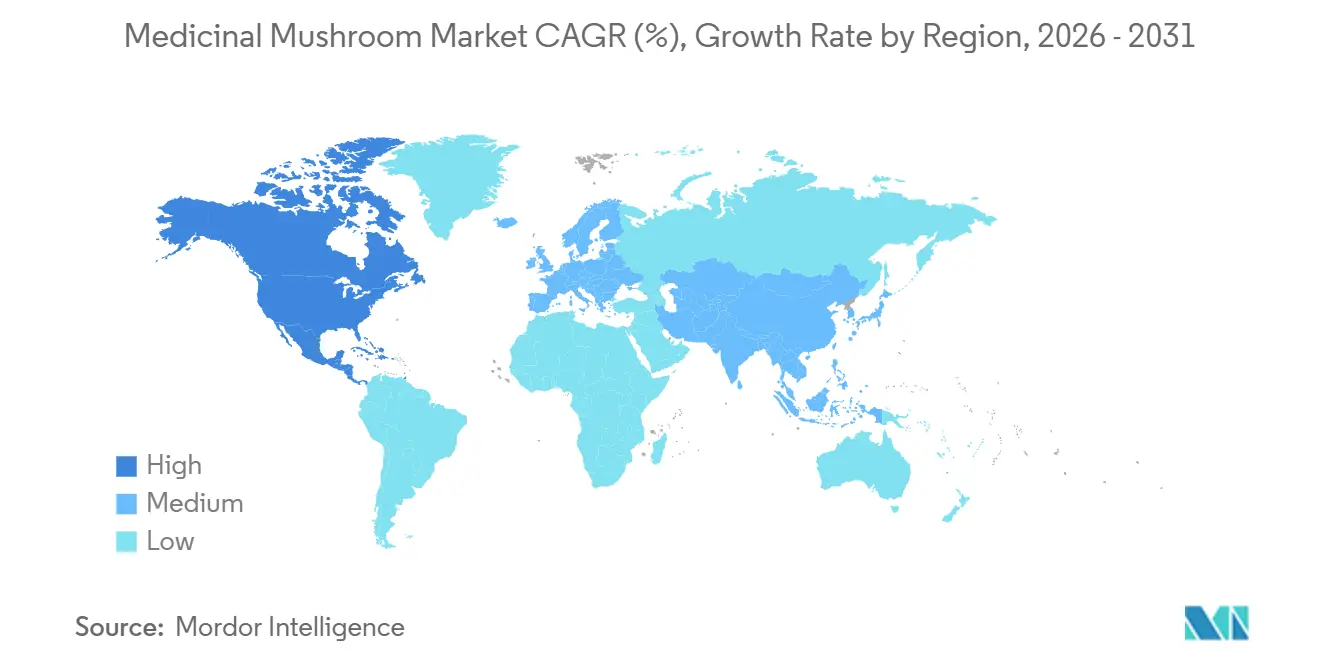

- By geography, Asia-Pacific captured 38.63% of global revenue in 2025, while North America is forecast to grow at the highest CAGR of 9.04% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medicinal Mushroom Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Consumer Demand for Natural Immune Resilience | +2.0% | Global | Short term (≤ 2 years) |

| Expansion of Nootropic and Cognitive Wellness Use | +1.6% | North America & Europe | Medium term (2-4 years) |

| Growth of Clean-Label Plant-Based Supplements and Functional Foods | +1.3% | North America, Europe, APAC | Medium term (2-4 years) |

| Clinical Validation and Standardized Extract Adoption | +1.1% | Global | Long term (≥ 4 years) |

| Premiumization Through Traceable Fruiting-Body and Beta-Glucan Positioning | +0.9% | North America & Europe | Medium term (2-4 years) |

| E-Commerce Education and Refill Economics for Specialized Wellness Products | +1.0% | North America, Europe, APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Demand for Natural Immune Resilience

Consumer demand for proactive immune support has remained well above pre-2020 levels, and that sustained behavior continues to anchor the medicinal mushroom market. Reishi and Turkey Tail stay central to this demand because both species are already tied to established immune positioning in supplements and wellness blends. A 2025 randomized, double-blind, placebo-controlled study tied to Fungi Perfecti and UC San Diego reported measurable immune-balancing effects from Lion’s Mane mushroom mycelium under stress conditions, which gave brands a stronger scientific base for targeted immune messaging. That shift is important because it moves product positioning away from broad wellness language and toward more specific, evidence-based communication that can justify higher prices and better placement. In the medicinal mushroom market, companies with stronger study files are in a better position to protect claims, support retailer discussions, and hold premium margins as buyers become more selective. This pattern also raises pressure on smaller brands that rely on generic immune narratives without clear product differentiation or documented active content.

Expansion of Nootropic and Cognitive Wellness Use

Cognitive wellness is becoming one of the strongest demand engines in the medicinal mushroom market, with Lion’s Mane at the center of that shift. A double-blind, randomized, placebo-controlled crossover study published in Frontiers in Nutrition in April 2025 found that a 3 g standardized Hericium erinaceus fruiting body extract improved psychomotor skill performance in healthy adults, even though the effects were not universal across all cognition tasks. That matters because it supports more precise positioning around reaction speed, dexterity, and stress-related performance rather than broad claims that every aspect of cognition will improve. The clinical base is also widening because additional randomized studies were registered in 2025 and early 2026 to compare Lion’s Mane extract formats and track cognitive, biomarker, and gut microbiota outcomes.[1]ClinicalTrials.gov, “The Impact of Supplementation With Hericium Erinaceus, Lion’s Mane, Extract on Cognitive Functioning,” ClinicalTrials.gov, clinicaltrials.gov As these trials progress, the medicinal mushroom market is likely to see a clearer separation between premium formulators that can support narrow function claims and brands that still sell on general nootropic appeal. This supports product segmentation by extract type, formulation method, and target use rather than by species name alone.

Growth of Clean-Label Plant-Based Supplements and Functional Foods

Clean-label expectations are reshaping purchase decisions in the medicinal mushroom market, especially for consumers who now look beyond the front label and study sourcing and extraction claims more closely. The fruiting-body-versus-mycelium debate has moved into mainstream consumer awareness, which has increased demand for products with verified species identity, visible sourcing standards, and disclosed beta-glucan content. Real Mushrooms’ acquisition of Mushroom Science in February 2026 reflects that shift because the combined business publicly emphasized pure extracted mushrooms, no fillers, and no mycelium-fermented grain as a core quality position. In practical terms, this means clean-label credibility is no longer a niche premium message and is becoming part of the baseline trust screen for many buyers. The medicinal mushroom market is therefore rewarding suppliers that can document provenance, extraction integrity, and compositional consistency across batches. That reward is likely to grow as more products move into mainstream retail channels where buyer scrutiny and shelf competition are both higher.

Clinical Validation and Standardized Extract Adoption

Clinical validation is turning into a commercial advantage in the medicinal mushroom market because buyers, retailers, and regulators all respond more favorably to products with measurable active content. ISO/TS 25006:2025 created quality parameters for sporoderm-broken Ganoderma lucidum spore powder, including limits and testing guidance for aflatoxins, heavy metals, pesticide residues, and marker compounds.[2]International Organization for Standardization, “ISO/TS 25006:2025, Traditional Chinese Medicine, Sporoderm-Broken Ganoderma lucidum Spore Powder,” International Organization for Standardization, standards.iteh.ai Research published in Scientific Reports in March 2025 also validated a Congo Red UV spectrophotometry method for beta-glucan detection across multiple Cordyceps species, with an average recovery rate of 100.9%, which strengthens the case for more standardized labeling. These developments matter because they give the medicinal mushroom market more reliable tools for comparing ingredients, verifying claims, and separating higher-quality extracts from weaker ones. Standardization also supports pricing discipline since products with documented beta-glucan levels are easier to defend in premium and pharmacist-adjacent channels. Over time, companies that invest early in testing systems and third-party verification are likely to capture both regulatory and commercial advantages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Inconsistency and Claims Substantiation Burden | -1.2% | Global, most acute in North America & EU | Short term (≤ 2 years) |

| Raw Material Contamination and Adulteration Risk | -0.9% | APAC source base, global impact | Medium term (2-4 years) |

| Supply Variability From Substrate Quality and Species-Specific Cultivation Limits | -0.7% | APAC & MEA | Medium term (2-4 years) |

| Batch-to-Batch Bioactive Variability and Limited Clinical Equivalence | -0.6% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Inconsistency and Claims Substantiation Burden

Regulatory complexity remains one of the clearest friction points in the medicinal mushroom market because product language, ingredient status, and launch timelines differ sharply across regions. In the United States, structure and function wording can be used under dietary supplement rules, but disease claims are not allowed, which creates a narrow path for consumer communication. The FDA reinforced that boundary when it issued a warning letter in September 2025 tied to adulterated Amanita muscaria products after its earlier determination that Amanita muscaria does not meet GRAS standards. In Europe, novel food authorization can slow launches for certain mushroom extracts and add material cost, which is especially difficult for smaller entrants with limited regulatory budgets. The medicinal mushroom market therefore operates through a patchwork of compliance expectations that raises formulation, legal, and packaging costs without creating a simple global playbook. That uncertainty often pushes brands toward safer but less differentiated claim language, which can weaken shelf impact and slow category development.

Raw Material Contamination and Adulteration Risk

Adulteration risk remains a structural weakness in the medicinal mushroom market because species substitution, filler use, and weak identity controls can occur well before finished products reach consumers. The Botanical Adulterants Prevention Program documented these issues in its October 2024 Cordyceps Adulteration Bulletin, which described lower-cost substitutions, undeclared grain-based fillers, and mycelium biomass sold as fruiting body material across several supply chains. A separate study on commercial Ganoderma dietary supplements found that only 26.3% of tested samples matched their labels, which points to a broader quality-control issue rather than a few isolated failures. When label accuracy is inconsistent, consumer trust becomes harder to build and harder to recover, especially in categories that already depend on technical claims and premium pricing. The medicinal mushroom market also faces greater pressure to verify imported raw material because long transit periods and mixed sourcing routes can complicate routine quality checks. Until authentication becomes more common across the full value chain, leading brands will continue to carry higher testing costs to protect quality and brand reputation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Reishi Anchors Revenue While Lion’s Mane Redefines the Growth Story

Reishi held 24.32% of type-segment revenue in 2025, while Lion’s Mane is forecast to expand at a 9.39% CAGR through 2031, showing that the medicinal mushroom market is balancing established demand with newer growth stories. Reishi’s lead reflects its long integration into traditional Chinese and Japanese use patterns and its broad positioning across immune, anti-fatigue, and stress-related applications. Lion’s Mane is building momentum because the evidence base around cognition, mood, and function-specific outcomes is widening, which gives brands more room to develop targeted products. A 2025 systematic review in Frontiers in Nutrition brought together 5 randomized controlled trials on Hericium erinaceus and found measurable benefits across mild cognitive impairment, depression, and menopause-related symptoms. In the medicinal mushroom market, that body of evidence is helping Lion’s Mane move from a single-product hero ingredient into a platform for differentiated cognitive and emotional wellness positioning.

Cordyceps and the other medicinal mushroom types retained smaller shares of the medicinal mushroom market, but they continue to build credible demand in narrower use cases. Turkey Tail benefits from its long-standing connection to oncology-adjacent wellness, while Shiitake gains from consumer familiarity as both a food ingredient and a wellness ingredient. Cordyceps militaris also has clinical support from a randomized controlled trial that examined immune response in healthy adults, which helps the segment maintain relevance outside endurance and energy narratives. Provenance is becoming more important across this segment because buyers increasingly distinguish between commodity-grade supply and traceable premium material with clearer cultivation documentation. This shift favors producers that can show origin, identity, and processing transparency, especially when the medicinal mushroom industry is trying to defend premium pricing against lower-cost, less-verified supply.

By Form: Extracts Dominate on Potency Positioning as Encapsulated Formats Scale

Extracts accounted for 38.23% of revenue in 2025, which shows that concentration, convenience, and perceived potency remain central buying criteria in the medicinal mushroom market size for form-level products. Their lead also reflects the fact that extracts fit both direct-consumer supplement formats and ingredient supply into powders, beverages, blends, and other functional food applications. Competitive differentiation inside extracts increasingly depends on whether brands can explain water, ethanol, or dual-extraction methods in a credible way and connect those methods to active content. Standardized beta-glucan messaging and third-party testing matter more here than in lower-processed forms because buyers expect extracts to offer measurable value beyond raw mushroom material. Dried mushrooms, fresh mushrooms, powders, teas, and tinctures still play an important role because they serve traditional-use consumers, culinary wellness formats, and shoppers who prefer less processed presentations.

Capsules and Tablets are projected to grow at an 8.76% CAGR through 2031, making them the fastest-growing form because they simplify dosing and fit everyday supplement routines. That growth also reflects wider acceptance among office workers and older adults who prefer familiar delivery forms with straightforward label directions. In March 2026, Host Defense launched a mushroom gummy line, which shows how format expansion is being used to draw in new consumers who care more about taste and consistency than extract strength per serving. Liquid extracts are also gaining attention in some European markets because fast-absorption positioning and traditional-use cues still resonate with specialist buyers. Across the medicinal mushroom market, form choice is now part of category strategy rather than simple packaging, since it shapes compliance, consumer entry, repeat use, and price realization.

By Function: Immune Support Leads as Cognitive Applications Build Critical Mass

Immune Support commanded 46.16% of functional revenue in 2025, while Cognitive Support is projected to advance at a 10.57% CAGR through 2031, showing how the medicinal mushroom market combines a stable core with a faster-moving growth edge. Immune support remains the largest function because it aligns with familiar consumer needs and because species such as Reishi and Turkey Tail already hold clear wellness associations. A randomized controlled trial published through PMC examined immune modulation by Reishi beta-1,3/1,6-D-glucan in healthy adults and showed that the mechanism can be observed in controlled conditions. Cognitive support is expanding more quickly because Lion’s Mane continues to gain scientific visibility, digital attention, and product development focus across powders, capsules, coffees, and blends. That split between a trusted immune category and an emerging cognitive category gives the medicinal mushroom market a broader demand base than single-benefit supplement categories usually achieve.

Anti-Cancer Support, Antioxidant Support, Skin Care Support, Stress and Sleep Support, and other applications accounted for the remaining medicinal mushroom market demand outside the 2 leading functions. Stress and Sleep products benefit from overlap with the broader adaptogen space, especially in teas, tinctures, and evening wellness blends that use Reishi and Chaga positioning. Skin Care Support is gaining ground in East Asia because mushroom-derived compounds are moving into hydration and anti-aging formulations, which extends supplier opportunities beyond oral supplements. Other functional uses such as gut health, energy, and exercise-related wellness remain smaller, but Cordyceps continues to attract interest because of its ATP-related performance narrative and its clinical visibility in immune response research. This wider mix of use cases matters because it helps the medicinal mushroom market reduce dependence on one therapeutic story and support more innovation across channels.

By Distribution Channel: Online Retail Holds Dual Dominance Across Share and Growth

Online Retail held 41.63% of distribution revenue in 2025 and is forecast to grow at a 9.94% CAGR through 2031, which means it leads both scale and momentum in the medicinal mushroom market share for channel performance. This dual lead reflects the category’s fit with digital education, direct product comparison, subscription ordering, and home delivery of repeat-use wellness products. Digital-first brands also benefit from being able to explain sourcing, extraction, and dosage more fully online than they can on a small label in physical retail. Subscription models are especially useful in the medicinal mushroom market because many products are positioned around routine use over several weeks instead of immediate one-time effects. As a result, online retail is not just a convenient outlet and has become the main environment where many consumers discover, evaluate, and stay with a brand.

Supermarkets and Hypermarkets remain important because they widen category visibility and support formats such as mushroom coffee, gummies, and multi-mushroom blends that are easier for mainstream buyers to trial. Pharmacies and Drugstores play a different role because they support products that rely on stronger quality documentation, clearer health framing, and professional recommendation. Specialty Stores still matter in the premium tier because staff guidance, curated ranges, and deeper product explanation help reduce confusion in a complex category. Across the medicinal mushroom market, the main strategic tension is between reach and control, since algorithm-driven discovery can widen access but also push brands into price competition unless they own strong product evidence or exclusive supply advantages. That is why more companies are working toward tighter sourcing relationships, better testing visibility, and stronger brand education rather than relying only on paid digital traffic.

Geography Analysis

Asia-Pacific held 38.63% of global revenue in 2025, which made it the largest regional block in the medicinal mushroom market and reflected its strong cultivation base, processing depth, and longstanding cultural familiarity with medicinal fungi. China remains central because it carries major cultivation and extraction capacity for several commercially important species. Japan also matters because Reishi and Lion’s Mane already fit into established wellness and traditional-use frameworks, which supports both specialist and mainstream product circulation. South Korea is building relevance through functional food and cosmetics applications that use mushroom bioactives in beverages, snacks, and skin-related products. Published Lion’s Mane trials have also included Japanese study populations, which reinforces the region’s influence on the evidence base behind cognition-focused products.

North America is projected to grow at a 9.04% CAGR through 2031, making it the fastest-growing geography in the medicinal mushroom market. The region’s strength comes from advanced e-commerce infrastructure, active direct-to-consumer brands, and a consumer base that is comfortable experimenting with new supplement formats. The United States remains the main engine because digital education, subscription programs, and product storytelling are especially effective in categories that require explanation around sourcing and active content. Canada adds support through a relatively developed natural health product environment, while Mexico represents an earlier-stage opportunity where modern supplement distribution is still building. Europe remains important but more complex because retail buyers often expect stronger product dossiers, clearer ingredient documentation, and more conservative health positioning than many North American brands are used to providing.

Middle East and Africa and South America are the smallest geographies in the medicinal mushroom market, and both regions still rely heavily on imported products because local cultivation and extraction depth remain limited for premium species. In the Gulf markets, especially the UAE and Saudi Arabia, interest is strongest among urban consumers who already spend on premium wellness and functional food products. South Africa remains a smaller but visible entry point because specialty retail and imported wellness categories are becoming easier to access. In South America, Brazil and Argentina are the primary markets, and cross-border e-commerce is the most immediate route for wider category penetration because it allows global brands to reach consumers even where local specialist distribution is still thin.

Competitive Landscape

The medicinal mushroom market remains moderately fragmented, with a long tail of direct-to-consumer brands alongside a smaller group of vertically integrated players that control cultivation, extraction, and branded finished products. No single company holds dominant global share, so competition is moving away from pure price pressure and toward ingredient integrity, scientific support, and supply-chain transparency. Real Mushrooms’ February 2026 acquisition of Mushroom Science is a clear example of this shift because the deal joined 2 brands that were both already positioned around fruiting-body sourcing and third-party beta-glucan verification. Fungi Perfecti is pursuing a related but broader strategy by pairing research visibility with new formats and more targeted product lines under the Host Defense brand. In this environment, companies that can show traceability, active-content testing, and a clear sourcing story are better placed to protect premium price points.

Competitive strategies are also widening because the medicinal mushroom market is no longer defined only by capsule supplements. In April 2026, Hypha Labs announced a partnership with Mycology Resources that combined Hypha Labs’ Mushroom Accelerator technology and MicroPearls delivery system with cultivation and distribution capabilities, showing how platform partnerships are entering the space. In April 2026, Host Defense expanded its MycoBenefits line with women’s wellness formulas, which shows how brands are using targeted demographic positioning to open new demand pockets. Pharmacy-led channels in Japan and South Korea also remain a meaningful white space because many Western brands have not yet built the product dossiers or professional education programs needed for stronger entry there.

The medicinal mushroom market is therefore moving toward a structure where quality proof, format innovation, and regulatory readiness matter as much as brand visibility. ISO testing frameworks and peer-reviewed analytical methods are helping stronger manufacturers turn quality control into a selling point rather than a back-end cost. Emerging ingredient biotechnology and more precise compound mapping may add another layer of competition over time, especially for companies trying to shorten the path from mushroom selection to clinically differentiated extracts. Until then, the most durable advantage in the medicinal mushroom market is likely to remain the ability to prove what is in the product, where it came from, and why it performs differently from the crowded field of lookalike offerings.

Medicinal Mushroom Industry Leaders

Aloha Medicinals, Inc.

Fungi Perfecti LLC

Host Defense Mushrooms

Nature’s Way Brands LLC

Swanson Health Products, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Host Defense (Fungi Perfecti LLC) launched MycoBenefits for Women, introducing 2 targeted mushroom mycelium formulas addressing menopause and hormonal support, one of the first category-specific women's health innovations in the medicinal mushroom supplement space, available at select US retailers and HostDefense.com.

- April 2026: Hypha Labs, Inc. announced a strategic partnership with Mycology Resources LLC, combining Hypha Labs' proprietary Mushroom Accelerator technology and MicroPearls delivery system with Mycology Resources' cultivation expertise and international distribution network for commercial-scale mushroom-based ingredient development.

- March 2026: Host Defense (Fungi Perfecti LLC) launched a mushroom gummy supplement line powered by mycelium grown in Washington state, targeting convenience-driven consumers and expanding the brand's product format range to address entry-level supplement buyers.

- February 2026: Real Mushrooms acquired Mushroom Science (JHS Natural Products), consolidating 2 of North America's leading pure-extract mushroom supplement brands to advance quality standards and third-party beta-glucan verification across the combined portfolio.

Global Medicinal Mushroom Market Report Scope

The Medicinal Mushroom Market comprises the global production, processing, distribution, and commercialization of mushrooms and mushroom-derived products used for their therapeutic, nutritional, and functional health benefits. Medicinal mushrooms contain bioactive compounds such as polysaccharides, beta-glucans, terpenoids, and antioxidants that are associated with immune modulation, cognitive support, antioxidant activity, stress management, and overall wellness.

The Medicinal Mushroom Market is segmented by type, form, function, distribution channel, and geography. Based on type, the market is categorized into Reishi, Chaga, Cordyceps, Lion’s Mane, Turkey Tail, Maitake, Shiitake, and other medicinal mushroom types. By form, the market is segmented into fresh mushrooms, dried mushrooms, extracts, powder, capsules and tablets, liquid extracts, and teas and tinctures. Based on function, the market comprises immune support, cognitive support, anti-cancer support, antioxidant support, skin care support, stress and sleep support, and other functional applications. By distribution channel, the market is divided into online retail, supermarkets and hypermarkets, pharmacies and drugstores, specialty stores, and other distribution channels. Geographically, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East & Africa, and South America.

| Reishi |

| Chaga |

| Cordyceps |

| Lion’s Mane |

| Turkey Tail |

| Maitake |

| Shiitake |

| Other Medicinal Mushroom Types |

| Fresh Mushrooms |

| Dried Mushrooms |

| Extracts |

| Powder |

| Capsules and Tablets |

| Liquid Extracts |

| Teas and Tinctures |

| Immune Support |

| Cognitive Support |

| Anti-Cancer Support |

| Antioxidant Support |

| Skin Care Support |

| Stress and Sleep Support |

| Other Functional Applications |

| Online Retail |

| Supermarkets and Hypermarkets |

| Pharmacies and Drugstores |

| Specialty Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Reishi | |

| Chaga | ||

| Cordyceps | ||

| Lion’s Mane | ||

| Turkey Tail | ||

| Maitake | ||

| Shiitake | ||

| Other Medicinal Mushroom Types | ||

| By Form | Fresh Mushrooms | |

| Dried Mushrooms | ||

| Extracts | ||

| Powder | ||

| Capsules and Tablets | ||

| Liquid Extracts | ||

| Teas and Tinctures | ||

| By Function | Immune Support | |

| Cognitive Support | ||

| Anti-Cancer Support | ||

| Antioxidant Support | ||

| Skin Care Support | ||

| Stress and Sleep Support | ||

| Other Functional Applications | ||

| By Distribution Channel | Online Retail | |

| Supermarkets and Hypermarkets | ||

| Pharmacies and Drugstores | ||

| Specialty Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the medicinal mushroom market?

The medicinal mushroom market stands at USD 8.48 billion in 2026 and is forecast to reach USD 12.79 billion by 2031, growing at an 8.56% CAGR.

Which product type leads demand in medicinal mushrooms?

Reishi led the type segment with 24.32% share in 2025 because it has broad consumer familiarity and strong positioning across immune, stress, and anti-fatigue uses.

Which function is growing the fastest in medicinal mushrooms?

Cognitive support is the fastest-growing function with a 10.57% CAGR through 2031, supported by rising interest in Lion’s Mane and a growing clinical base.

Why is online retail so important for this category?

Online retail held 41.63% of revenue in 2025 and is also the fastest-growing channel at a 9.94% CAGR because the category relies heavily on education, comparison, and repeat ordering.

Which region leads global revenue for medicinal mushrooms?

Asia-Pacific led with 38.63% of global revenue in 2025 due to strong cultivation capacity, established traditional use, and deeper processing infrastructure.

Page last updated on: