Cannabidiol (CBD) Oil Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.95 Billion |

| Market Size (2031) | USD 5.20 Billion |

| Growth Rate (2026 - 2031) | 12.03% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

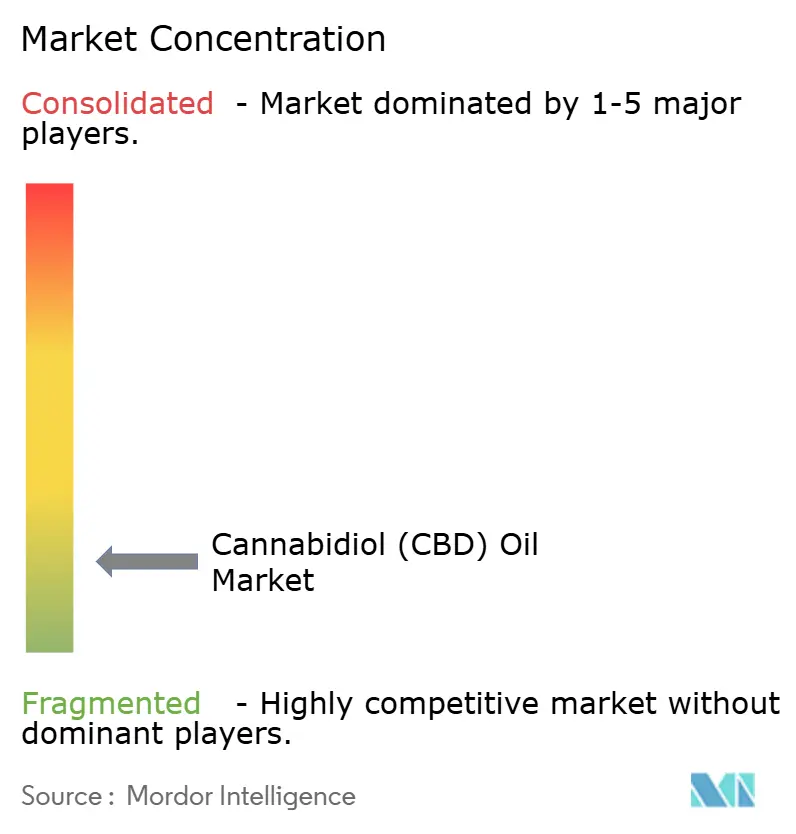

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cannabidiol (CBD) Oil Market Analysis by Mordor Intelligence

Cannabidiol (CBD) Oil market size in 2026 is estimated at USD 2.95 billion, growing from 2025 value of USD 2.63 billion with 2031 projections showing USD 5.2 billion, growing at 12.03% CAGR over 2026-2031.

Regulatory harmonization, rising clinical validation, and sustained consumer interest in plant-based wellness products are pushing the Cannabidiol (CBD) Oil market beyond niche status toward mainstream therapeutic adoption. Companies are ramping capital spending on extraction lines that meet pharmaceutical Good Manufacturing Practice (GMP) requirements, signaling confidence that both prescription and over-the-counter channels will expand. Clinical‐trial disclosures show consistent focus on chronic pain and refractory epilepsy, while beverage formulators invest in water-soluble nano-emulsions that widen usage occasions. In parallel, the cost base is falling as high-yield hemp cultivars and large-volume supercritical CO₂ systems improve output per acre and lower unit costs.

Key Report Takeaways

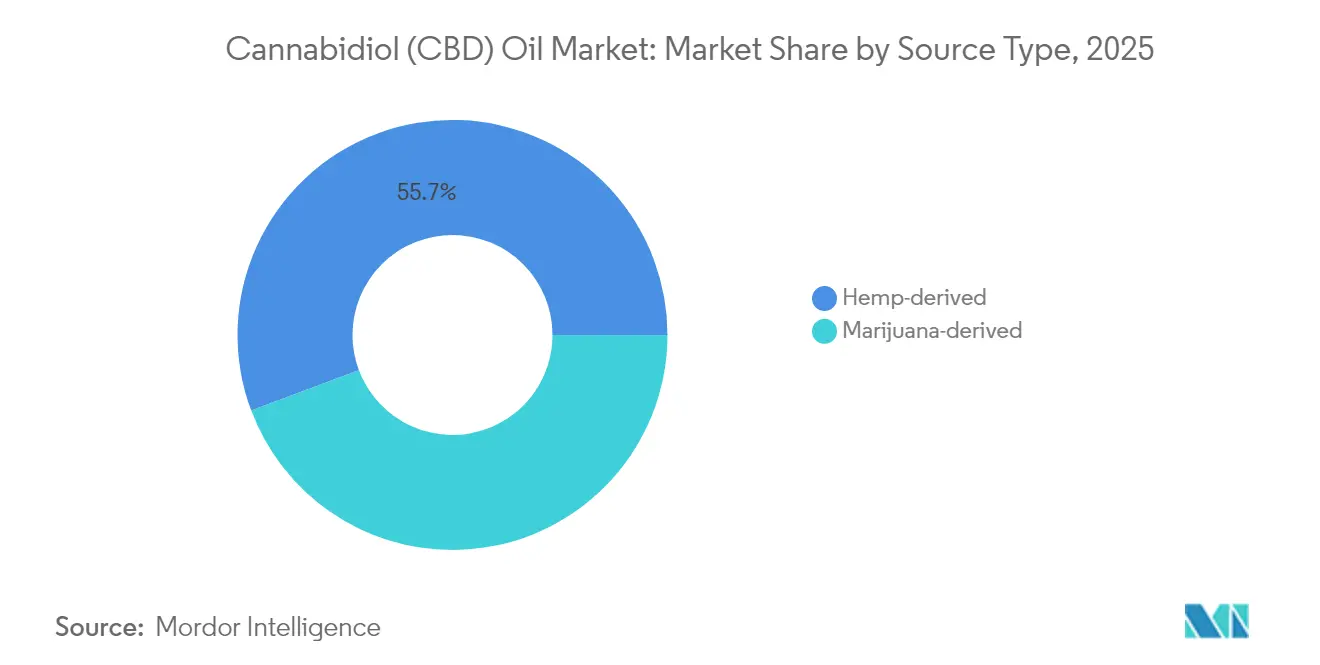

- By source type, hemp-derived oils held 55.72 % of the Cannabidiol (CBD) Oil market share in 2025, while marijuana-derived oils are projected to advance at a 13.12 % CAGR through 2031.

- By product form, oils captured 42.63 % of 2025 revenue; edibles and gummies are on track to register the fastest 13.84 % CAGR through 2031.

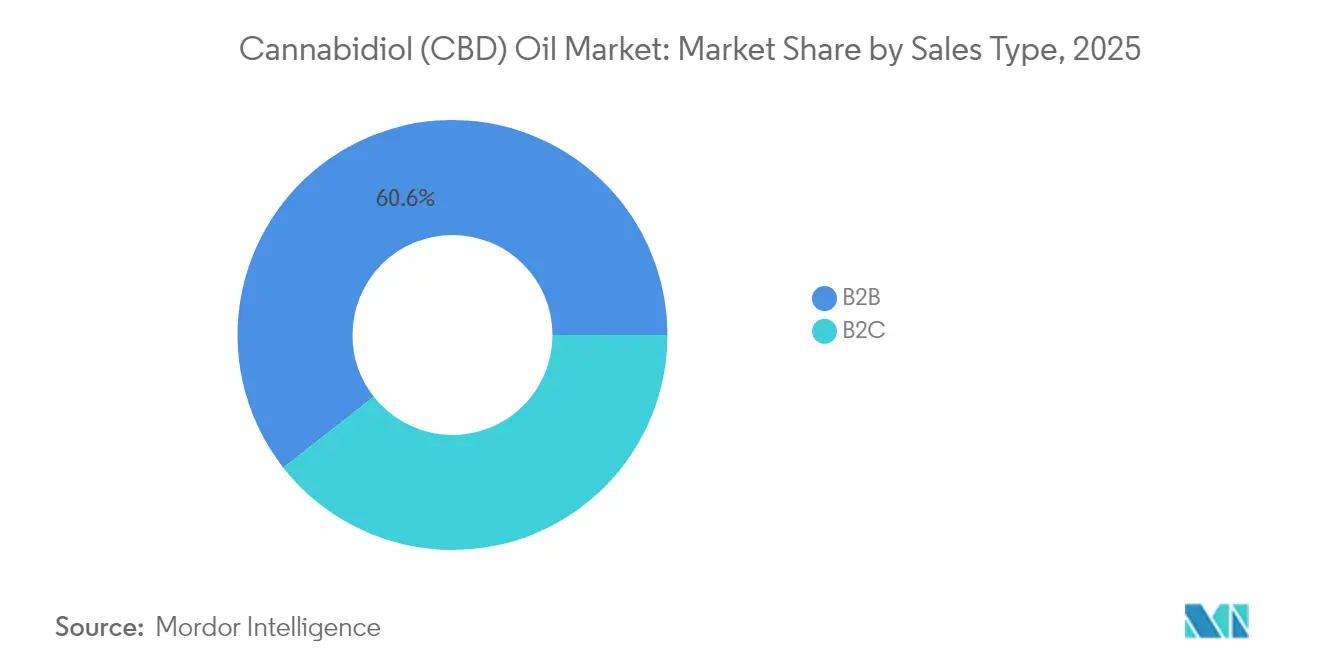

- By sales type, the B2B channel accounted for 60.58 % of 2025 value; the B2C route is forecast to compound at 13.56 % through 2031.

- By end-use sector, medical and pharmaceuticals commanded 47.31 % of 2025 revenue, whereas veterinary and pet products are poised for a 14.65 % CAGR over 2026-2031.

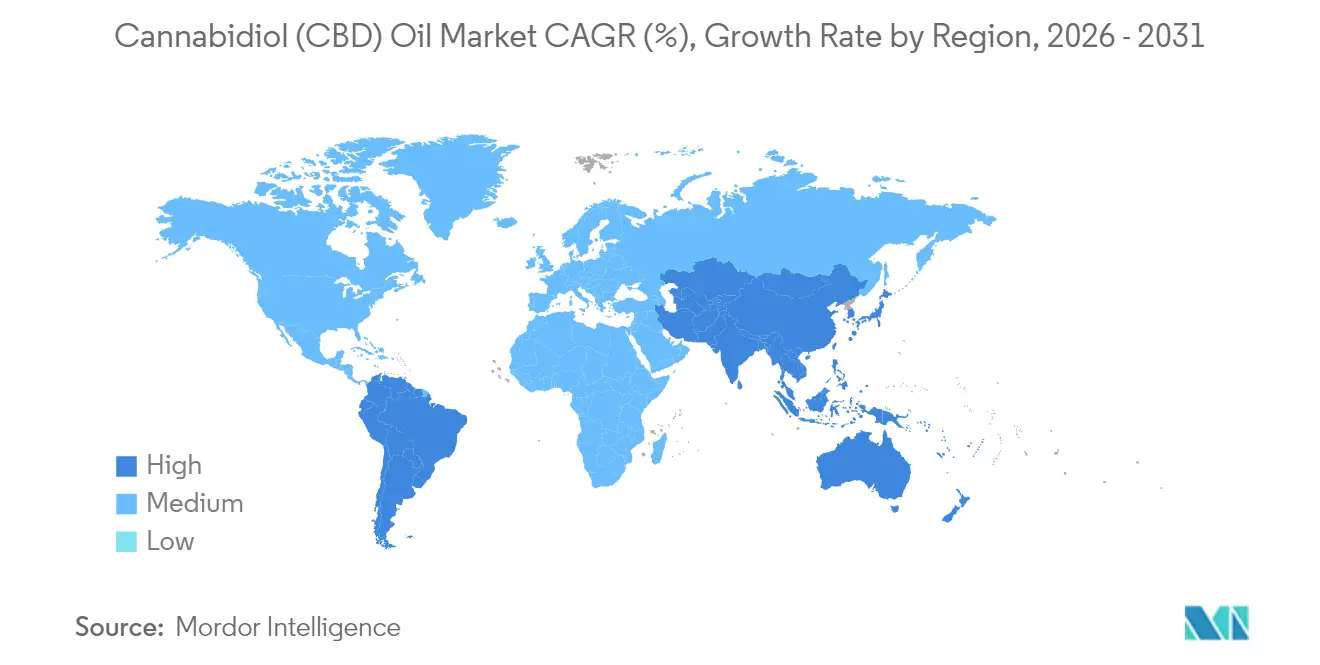

- By geography, North America dominated with 46.92 % revenue in 2025; Asia-Pacific is expected to log the fastest 15.42 % CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cannabidiol (CBD) Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Harmonization of hemp-friendly legislation accelerating adoption | + 3.8 % | North America & Europe, spillover to Asia-Pacific | Medium term (2-4 years) |

| Expanding clinical evidence validating CBD for chronic pain & epilepsy | + 3.2 % | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Consumer migration toward plant-based, non-opioid therapeutics | + 2.1 % | Global, early adoption in North America | Medium term (2-4 years) |

| Omnichannel distribution boom boosting accessibility | + 1.8 % | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Cost declines from large-scale hemp cultivation & extraction technology | + 1.4 % | Global, initial impact in North America | Medium term (2-4 years) |

| Widespread integration of CBD into functional beverages and RTDs | + 1.2 % | North America & Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Harmonization of Hemp-friendly Legislation Accelerating Adoption

Policymakers on both sides of the Atlantic are aligning hemp statutes, lowering the compliance burden and giving national health agencies leeway to approve Cannabidiol (CBD) Oil market formulations that meet quality norms. The proposed U.S. re-schedule to Schedule III could neutralize Internal Revenue Code Section 280E expenses, which currently absorb up to 70 % of gross profit for vertically integrated firms. Comparable momentum in Germany has already lifted unit sales of GMP-certified tinctures, a data point firms cite when forecasting European rollouts. Country-level law changes shorten product-registration timelines, letting brands launch standardized SKUs across multiple markets rather than tailoring labels for every jurisdiction. This convergence[1]Ian A. Stewart, “Proposed Cannabis Reschedule Sidesteps State Law Effects,” Wilson Elser, wilsonelser.com prompts batch-size increases that drive production economies of scale, thereby dampening prices and boosting consumption.

Expanding Clinical Evidence Validating CBD for Chronic Pain & Epilepsy

A systematic review covering 40 studies confirmed that THC-free cannabidiol activates TRPV-1 and 5HT-1A pathways, substantiating its analgesic impact on osteoarthritis and neuropathic pain. U.S. oncologists now reference cannabidiol adjunct therapy in 2024 supportive-care guidelines, especially for intractable chemotherapy-induced nausea. This growing dossier enables drug developers to justify randomized controlled trials that may secure insurance reimbursement. The Cannabidiol (CBD) Oil market therefore benefits from dual credibility—familiar consumer perception and hard clinical data[2]Cásedas et al., “Cannabidiol Systematic Review on Pain Treatment,” mdpi.com—creating cross-over demand from both wellness shoppers and prescribers.

Consumer Migration Toward Plant-based, Non-opioid Therapeutics

Roughly 13 % of Canadians self-report cannabis use for medical reasons, an indicator that pain sufferers are looking for non-addictive solutions. In the United States, pharmacy chains test end-caps featuring hemp-derived oils next to vitamin-C drops, reinforcing the notion that cannabidiol is a mainstream supplement rather than an alternative fringe substance. This behavioral shift[3]Canadian Centre on Substance Use and Addiction, “Clearing the Smoke on Cannabis: Medical Use of Cannabis and Cannabinoids,” ccsa.ca draws risk-averse demographic segments—such as seniors—into the Cannabidiol (CBD) Oil market, improving repeat-purchase probabilities due to perceived safety.

Omnichannel Distribution Boom Boosting Accessibility

Mobile shopping handles 51.8 % of digital CBD transactions, pushing brands to optimize page load times and one-click checkout for handheld devices. At the same time, physical stores supply discovery channels where pharmacists or nutritionists can explain dose titration, complementing the self-guided e-commerce journey. Brands that synchronize online inventory with in-store allocations report 20 % fewer stock-outs, safeguarding shelf visibility while smoothing cash flow.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory ambiguity on THC limits and labeling standards | – 2.4 % | Global, significant in emerging markets | Medium term (2-4 years) |

| Supply-chain bottlenecks in organic-certified hemp seeds | – 1.6 % | North America & Europe | Short term (≤ 2 years) |

| Quality inconsistency owing to lack of unified global GMP protocols | – 1.3 % | Developing markets | Long term (≥ 4 years) |

| Inconsistent customs enforcement across borders | – 0.8 % | Trade corridors worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Ambiguity on THC Limits and Labeling Standards

A peer-reviewed assessment of 53 hemp items found labeling inaccuracies in 66 % of samples, exposing buyers to unintentional psychotropic intake. Such findings erode trust and force responsible producers to shoulder higher quality-assurance costs[4]Johnson et al., “Potency and Safety Analysis of Hemp Delta-9 Products,” j-cannabis-research.biomedcentral.com , which in turn compress margins. Retailers now demand certificates of analysis with QR codes, adding friction to listings and eliminating low-budget newcomers from key platforms.

Supply-chain Bottlenecks in Organic-certified Hemp Seeds

Demand for USDA-organic status surpasses seed availability, leading to a 12-month backlog in high-CBD genetics. Farmers who cannot secure certified seed often miss premium contract opportunities. The Cannabidiol (CBD) Oil market, therefore, experiences input-price volatility, which discourages long-term planning for smaller cultivators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Hemp Dominance Faces Marijuana Challenge

Hemp-derived oils make up the majority of Cannabidiol (CBD) Oil market revenue because 0.3 % THC compliance eases interstate commerce, financial-service access, and mainstream-retailer placements. National pharmacy groups prefer hemp SKUs for risk mitigation, documenting a 30 % reorder increase within six months of initial shelf launches. Margin architecture benefits from scale: a single extraction batch often supplies cosmetic, nutraceutical, and tincture fill lines, spreading overhead across multiple revenue streams. Despite hemp leadership today, marijuana-sourced oils are gaining favor among experienced users who equate trace cannabinoid diversity with stronger symptom relief. Licensed dispensaries report that full-spectrum oils command 35-50 % price premiums yet maintain high turn rates, suggesting value-perception rather than price alone guides purchase decisions. Vertical integrators weigh these dynamics by operating dual lines, isolating hemp flows for big-box retail and full-spectrum lines for medical dispensaries, thereby hedging regulatory risk while meeting diverse demand.

Marijuana-derived oils notch a 13.12 % CAGR forecast, powered by dispensary expansion in U.S. adult-use states and Germany’s personal-use law. Patients with chronic pain often pivot from isolates to full-spectrum blends after experiencing what they describe as enhanced efficacy, a switch that raises average monthly spend by 22 %. Compliance, however, involves potency caps and tamper-proof packaging, boosting cost-of-goods. Operators that integrate in-house testing and date-coded serialization mitigate these burdens and secure listing priority in regulated markets. On the supply side, indoor cultivators increasingly use LED spectra fine-tuning to boost minor cannabinoid ratios, aligning crop profiles with formulation demand in the Cannabidiol (CBD) Oil market.

By Product Form: Oils Maintain Leadership

Oils remain the backbone of the Cannabidiol (CBD) Oil market thanks to dose flexibility, sublingual onset of 15-45 minutes, and easy pairing with flavors like peppermint to mask hemp’s terpene bitterness. Clinicians favor calibrated droppers when titrating seizure-control regimens, and pharmacists often lock oils behind counters alongside prescription items, reinforcing their medical-grade perception. Conversion analytics reveal cross-selling dynamics: 28 % of oil buyers add topical rollers in the same basket, inflating unit economics without extra acquisition cost. Bottlers embrace lightweight recyclable glass, trimming freight weight by 7 %, a logistics gain that flows directly to gross margin.

Edibles and gummies are on a growth tear, advancing faster than any other form factor as they offer single-serve convenience and longer systemic windows of 4-8 hours. Vegan pectin versions attract flexitarians, while sugar-free SKUs serve diabetic customers, expanding addressable pools. The Cannabidiol (CBD) Oil market benefits because edible-first users often graduate to oils once familiarity sets in, increasing lifetime value. Skin-contact products such as balms and transdermal patches harness cannabidiol’s anti-inflammatory traits for localized support, appealing to athletes and mature adults. Though these segments remain smaller by volume, innovation pipelines suggest higher SKU diversity ahead.

By Sales Type: B2B Infrastructure Supports B2C Growth

Wholesale contracts anchor revenue stability in the Cannabidiol (CBD) Oil market, accounting for a 60.58 % share and furnishing predictable off-take that underwrites capital-equipment repayments. Ingredient suppliers sell winterized crude to beverage companies, distillates to vape formulators, and isolates to cosmetic labs, creating a matrix of revenue streams buffered against single-category downturns. Payment-term extensions of 60-90 days free up working capital for both parties and deepen relationships that can evolve into joint-R&D projects.

Direct-to-consumer sales are catching up, forecast to grow at 13.56 % per year as brands exploit e-commerce to build data-rich feedback loops. Subscription programs ship 30-milliliter droppers monthly, supported by dashboards that prompt dose adjustments based on user-reported outcomes, which reduces churn by 18 %. Offline drugstores gain traction among first-time users who seek face-to-face dosage guidance. Kiosks within grocery aisles also emerge, bundling cannabidiol tinctures with collagen peptides or magnesium, illustrating category blending in wellness-oriented baskets. Firms that unify B2B and B2C channels tend to post higher gross-to-net retention, a metric closely watched by private-equity investors.

By End-use Sector: Medical Leadership, Veterinary Acceleration

Physician-led use dominates, with the medical segment commanding 47.31 % of 2025 revenue in the Cannabidiol (CBD) Oil market. Insurance carriers in Germany, Israel, and selected U.S. states reimburse cannabidiol for Lennox-Gastaut syndrome when mainstream treatments fail, lowering out-of-pocket barriers. Brands thus invest in randomized controlled trials to expand labeled indications, expecting premium ex-factory pricing to offset research expense. Hospitals demand serialized tracking from seed lot through final bottle, and suppliers deploying blockchain audits meet these criteria, winning multi-year tenders.

Vet-specific formulations are surging, powered by pet-owner interest in non-steroidal options for anxiety and arthritis. Bacon-flavored drops and chew squares account for 70 % of unit volume in pet channels because palatability drives compliance. The Wisconsin Veterinary Examining Board now allows practitioners to discuss cannabidiol options openly, a policy shift that sets precedent for other U.S. states. Grooming salons increasingly stock mini dropper packs, encouraging trial among dog owners. The Cannabidiol (CBD) Oil market thus enjoys an ancillary revenue stream with relatively light regulatory hurdles yet high price elasticity.

Nutraceutical producers incorporate cannabidiol into multivitamin softgels, while functional beverage brands release low-dose sparkling waters aimed at calm-focus positioning during workdays. Cosmetic giants develop anti-aging serums leveraging antioxidative properties, pushing cannabidiol into premium beauty counters. Each addition broadens category exposure and invites cross-promotion.

Geography Analysis

North America contributes nearly half of global revenue in the Cannabidiol (CBD) Oil market and features mature retail networks, cross-border cultivation clusters, and advanced clinical research centers. U.S. operators anticipate that a Schedule III re-classification will allow standard tax deductions, potentially improving net margins by 10-15 % [FDA.GOV]. Canadian issuers supply pharmaceutical-grade isolate to Europe and Australia, illustrating how a clear national framework unlocks export capital. Mexico’s draft bill outlines a federal registry for CBD producers, hinting at new North-South supply corridors that could leverage low-cost labor while serving 130 million residents once final rules publish.

Asia-Pacific is expanding the Cannabidiol (CBD) Oil market fastest, gaining traction in Australia’s Special Access Scheme, Japan’s zero-THC cosmetic aisle, and South Korea’s monitored prescription program. Chinese hemp acreage covers more than half the planet’s total, and processors run GMP plants dedicated to export because domestic rules limit ingestible use. Start-ups in Singapore pursue blockchain compliance engines to serve as regional quality hubs, anticipating wider liberalization. Investors see an upside in blending local cultivation with Australian-style clinical rigor to serve rising middle-class consumers.

Europe advances under Germany’s April 2024 personal-use law, which has already lifted vaporizer sales and medical-prescription renewals. The United Kingdom’s Food Standards Agency weighs novel-food applications and signals dosage caps that most exporters can meet with minor label edits. Italy debates expansion of its medical program, Spain explores pilot cultivation licenses, and France tracks a gradual shift from resin toward herbal formats—a movement that nudges policymakers toward modernizing rules. Harmonization remains slow, yet pharmaceutical distributors hold pan-EU contracts that accelerate cross-border shipments once clearances emerge.

Middle East & Africa post mid-teen growth as Israel’s clinical-trial ecosystem draws global pharmaceutical partnerships, while South Africa prototypes a regulated supply chain after its decriminalization milestone. South America rides competitive agronomy and favorable sunlight. Brazil allows personal imports of 0.2 % THC oils via prescription, and domestic labs are honing good-manufacturing standards in anticipation of broader reforms. Colombia’s licensed bank covers both cultivation and manufacturing, supporting EU-GMP certification that draws European buyers. Argentina’s new medical regulations include local cultivation incentives aiming to reduce reliance on imports. The Cannabidiol (CBD) Oil market thus benefits from low-cost biomass but confronts currency volatility that complicates multi-year pricing agreements.

Competitive Landscape

The Cannabidiol (CBD) Oil market is fragmented, with top five brands well below the 40 % revenue threshold that would indicate oligopoly. Cannabis specialists, pharma upstarts, and consumer-goods conglomerates coexist, using different playbooks. Vertical integration gains momentum as operators seek margin insulation by controlling genetics, extraction, fill-finish, and direct sales. For instance, a Canadian player shed non-core beverage assets to focus on GMP oil lines, a move that improved asset turnover and freed cash for R&D.

Large-cap consumer companies enter through minority stakes or joint ventures. A tobacco major’s medical-cannabis alliance aims to leverage inhalation-device expertise to develop metered-dose cannabinoid therapies. These alignments pool regulatory know-how, clinical-trial funding, and mass-distribution clout, posing competitive pressure on pure-play independents. Start-ups counter by focusing on underserved micro-niches—women’s hormonal health, athlete recovery, or neuro-support—and by publishing peer-reviewed data that establish scientific authority.

Technology drives differentiation. Closed-loop CO₂ extraction paired with terpene preservation protocols yields cleaner flavor and minor-cannabinoid retention. Cloud platforms trace plant batches from greenhouse to bottle, enabling QR-scan verification on retail shelves. Vial-level serialization reassures pharmacists and veterinarians. Firms slow to adopt such systems risk delistings from pharmacies that now audit suppliers.

Pricing wars are limited because high-quality inputs and testing expenses set a floor. Instead, brands compete on formulation innovation: liposomal delivery for improved bioavailability, flavor masking for geriatric palatability, or pairing cannabidiol with melatonin for sleep blends. The Cannabidiol (CBD) Oil industry therefore favors companies with both laboratory depth and consumer-experience design.

Cannabidiol (CBD) Oil Industry Leaders

Aurora Cannabis Inc.

Canopy Growth Corporation

Charlotte’s Web Holdings Inc.

Jazz Pharmaceuticals plc

Tilray Brands Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Xebra Brands announced intent to buy BSK Holdings, a U.S.–Mexican e-commerce specialist that generated USD 50 million revenue since 2021, increasing digital reach and cross-border logistics capacity.

- January 2025: Philip Morris International, via Vectura, partnered with Avicanna to co-develop cannabinoid therapies, signaling diversification beyond nicotine portfolios.

- December 2024: The UK Food Standards Agency entered risk-management phase on cannabidiol novel-food filings following eight-week public consultation.

- August 2024: Canopy Growth completed its shift to asset-light cannabis operations and reported a 10 % uptick in Canadian medical revenue, affirming focus on core strengths.

Global Cannabidiol (CBD) Oil Market Report Scope

As per the scope of the report, CBD is one of the many cannabinoids found in cannabis plants. This has been a traditional remedy for many years. CBD oil is obtained from the plants by crushing the seeds or plants. The cannabidiol (CBD) oil market is segmented by product (marijuana-based and hemp-based), application (multiple sclerosis, depression and sleep disorders, neurological pain, and other applications), and geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (in USD million) for the above segments.

| Hemp-derived |

| Marijuana-derived |

| Capsules & Softgels |

| Edibles & Gummies |

| Oils |

| Topicals & Creams |

| Other Forms |

| Business-to-Business (B2B) | |

| Business-to-Consumer (B2C) | Offline Retail Pharmacies |

| Online / E-commerce | |

| Others |

| Cosmetics & Beauty |

| Medical & Pharmaceuticals |

| Nutraceuticals & Functional Foods |

| Veterinary Products |

| Wellness & Personal Care |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Netherlands | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Israel |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Source Type | Hemp-derived | |

| Marijuana-derived | ||

| By Product Form | Capsules & Softgels | |

| Edibles & Gummies | ||

| Oils | ||

| Topicals & Creams | ||

| Other Forms | ||

| By Sales Type | Business-to-Business (B2B) | |

| Business-to-Consumer (B2C) | Offline Retail Pharmacies | |

| Online / E-commerce | ||

| Others | ||

| By End-Use Sector | Cosmetics & Beauty | |

| Medical & Pharmaceuticals | ||

| Nutraceuticals & Functional Foods | ||

| Veterinary Products | ||

| Wellness & Personal Care | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Netherlands | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Israel | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the Cannabidiol (CBD) Oil Market?

The Cannabidiol (CBD) Oil Market is valued at USD 2.95 Billion in 2026.

How is consumer demand evolving in terms of preferred CBD oil delivery formats?

Shoppers are migrating from tinctures toward gummies, beverages, and topical rollers, seeking convenience, flavor variety, and application-specific solutions.

Why are vertically integrated CBD oil companies gaining an advantage over single-stage operators?

Controlling cultivation, extraction, formulation, and direct sales helps these firms manage quality end-to-end, comply with shifting regulations faster, and capture margin at multiple points in the value chain.

What trend is shaping product development for the veterinary CBD segment?

Formulators are prioritizing pet-friendly flavors and weight-based dosing guides as veterinarians become more willing to recommend cannabidiol for anxiety and joint support in animals.

How are quality-assurance requirements influencing competitive dynamics?

Retailers and pharmacists increasingly demand QR-linked certificates of analysis, favoring brands with in-house or certified third-party labs while squeezing out producers that lack rigorous testing protocols.

What role do functional beverages play in CBD oil market expansion?

Water-soluble nano-emulsion technology has allowed brands to infuse cannabidiol into ready-to-drink teas and sparkling waters, opening grocery and convenience-store channels that reach new, mainstream consumers.

Page last updated on: