United States Generic Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

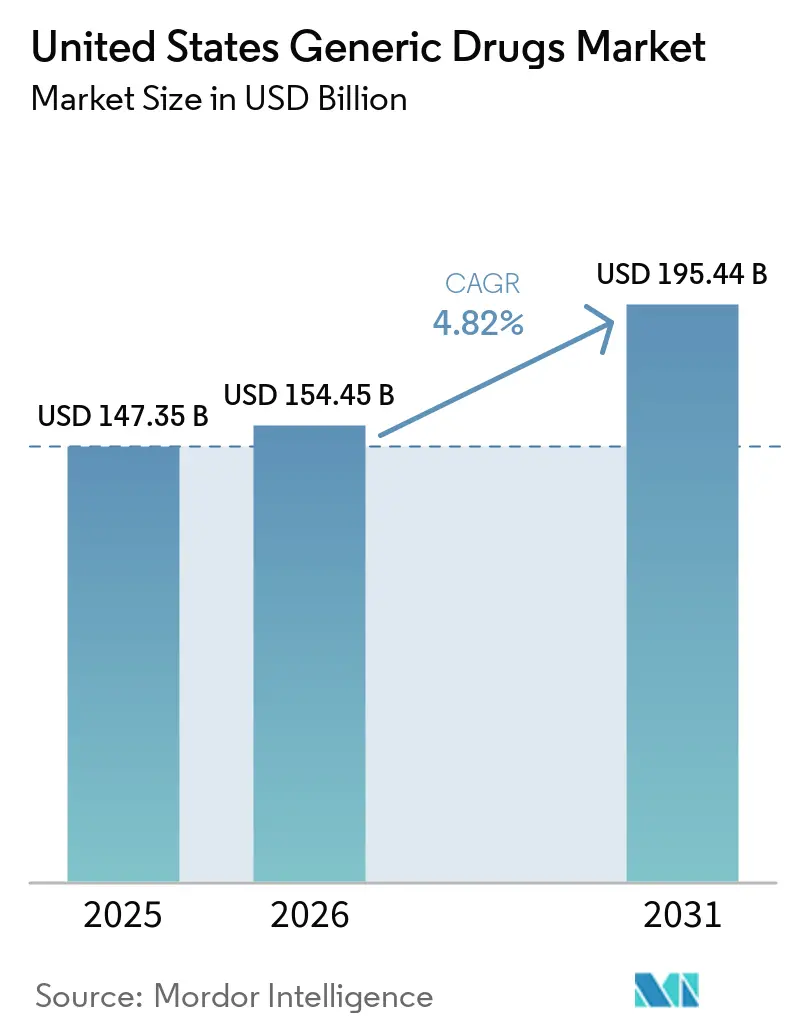

| Base Year Market Size (2025) | USD 147.35 Billion |

| Market Size (2026) | USD 154.45 Billion |

| Market Size (2031) | USD 195.44 Billion |

| Growth Rate (2026 - 2031) | 4.82% CAGR |

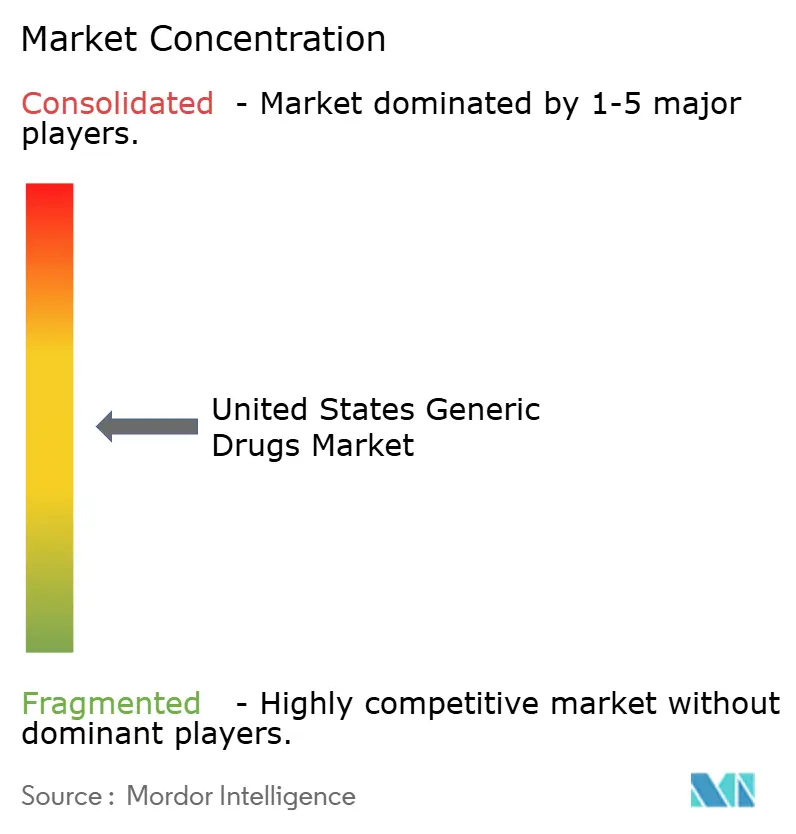

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Generic Drugs Market Analysis by Mordor Intelligence

The United States Generic Drugs Market size is projected to be USD 147.35 billion in 2025, USD 154.45 billion in 2026, and reach USD 195.44 billion by 2031, growing at a CAGR of 4.82% from 2026 to 2031.

The market is moving through a period in which new loss-of-exclusivity events in high-volume therapies are aligning with a broader biosimilar rollout, which is widening the addressable product base for manufacturers. As of March 2026, the FDA had cleared 92 biosimilars across 20 unique molecules, and 67 had already launched in the United States, which supports a second growth lane beyond traditional small-molecule generics. Competitive conditions remain moderate to high because scale, portfolio range, and manufacturing discipline matter more once multi-source entry pushes prices down across mature molecules. Corporate strategy is therefore shifting toward complex injectables, device-linked products, biosimilars, and selective acquisitions that shorten development time for higher-value launches. The policy backdrop is also changing the cost equation, as Executive Order 14293 and the later Strategic Active Pharmaceutical Ingredients Reserve order favor domestic manufacturing capacity and tighter oversight of foreign facilities.

Key Report Takeaways

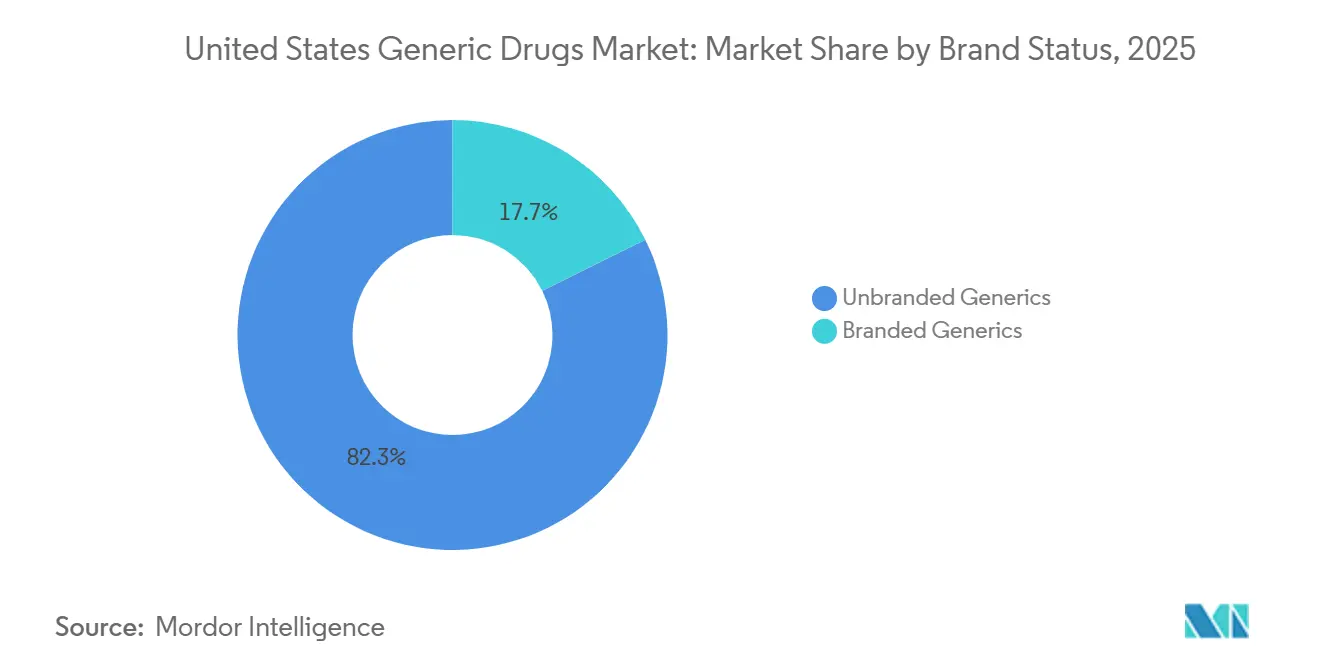

- By brand status, unbranded generics led with 82.31% share in 2025, while branded generics are projected to expand at 5.38% CAGR through 2031.

- By molecule type, small molecule generics held 85.24% share in 2025, while biosimilars are forecast to grow at 7.52% CAGR through 2031.

- By therapeutic area, cardiovascular generics accounted for 25.52% of the United States generic drugs market size in 2025, while oncology is advancing at 7.28% CAGR through 2031.

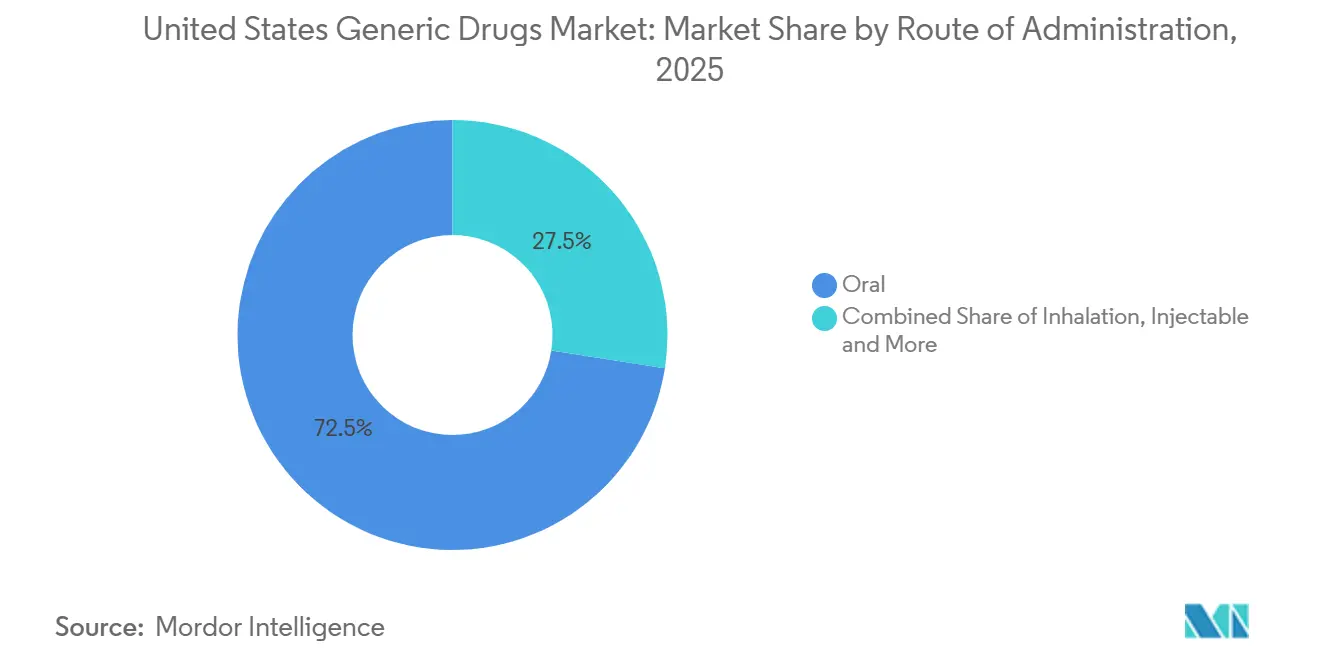

- By route of administration, oral generics represented 72.52% share in 2025, while inhalation generics are expected to grow at 5.28% CAGR through 2031.

- By distribution channel, retail pharmacies held 78.52% of the United States generic drugs market share in 2025, while online pharmacies are projected to expand at 7.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Generic Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patent-Loss Wave In Cardiometabolic And CNS Brands | +1.5% | Global, concentrated in US | Short term (≤ 2 years) |

| Payer Pressure For Low-Net-Cost Substitution | +1.0% | US primary, spill-over to employer-insured segments nationally | Short term (≤ 2 years) |

| Faster ANDA Review Under GDUFA III | +0.5% | US | Medium term (2-4 years) |

| Expansion Of Complex Injectables And Device-Linked Generics | +0.8% | US hospital and specialty channel | Long term (≥ 4 years) |

| Model-Integrated Evidence In Bioequivalence Packages | +0.3% | US, with regulatory precedent extending to EU | Medium term (2-4 years) |

| U.S.-Manufacturing Prioritization For Domestic Supply | +0.4% | US domestic, indirect impact on imports from APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Patent-Loss Wave in Cardiometabolic and CNS Brands: Blockbuster Volume Multiplies Rapidly

The near-term pipeline for the United States generic drugs market is being supported by a new cluster of patent-loss events in cardiometabolic and CNS therapies. These molecules sit inside large chronic treatment pools, so generic entry can shift very high prescription volumes in a short period once exclusivity ends. The effect is stronger when payer rules already favor rapid substitution and when prescribers are familiar with the underlying therapy class. This setup raises launch importance for companies that can file on time, secure manufacturing slots, and build early channel availability before markets become crowded. It also supports capacity utilization across oral solids and related supply networks, which makes this driver broader than a single product event. For the United States generic drugs market, this remains the clearest short-cycle volume trigger during the first half of the forecast period.

Payer Pressure for Low-Net-Cost Substitution: Mandates Intensify Beyond Voluntary Switching

Commercial insurers, pharmacy benefit managers, and public programs continue to push lower-net-cost substitution through prior authorization, formulary tiering, and step-edit rules. This matters because generic and biosimilar uptake now depends as much on reimbursement design as on product availability. In the United States, adalimumab biosimilars held 60% of the combined adalimumab market in March 2026, and ustekinumab biosimilars reached 27% share, showing how quickly uptake can move once payer alignment improves. The same reports also show that oncology, ophthalmology, and pegfilgrastim biosimilars have moved faster than immunology and insulin, which means payer economics are strongest where clinical substitution is already accepted. For the United States generic drugs market, this demand pull lowers the time between launch and meaningful volume capture. It also reinforces why commercial access teams matter almost as much as regulatory execution in the current cycle.

Faster ANDA Review under GDUFA III: First-Cycle Rates Signal a Persistent Gap

GDUFA III continues to support faster review pathways for applicants that submit complete dossiers and meet facility correspondence requirements. The FDA’s Generic Drugs Program Fiscal Year 2025 Activities Report stated that the Office of Generic Drugs approved 689 ANDAs in FY2025 and kept on-time review performance in the 97% to 100% range across standard and priority tracks. Faster decisions matter because they shorten the wait between filing and commercial planning, especially for products tied to narrow launch windows. The benefit is not evenly distributed, since companies with stronger regulatory teams and better manufacturing readiness are more likely to clear the first review cycle. That gives well-resourced manufacturers a throughput advantage even when industrywide submission volumes soften. In the United States generic drugs market, GDUFA III therefore favors execution quality rather than simply rewarding filing volume.

Expansion of Complex Injectables and Device-Linked Generics: Margin Recovery Vehicle for Generic Manufacturers

Manufacturers are directing more capital toward complex injectables, device-linked formats, and difficult-to-copy sterile products because plain oral solids offer less pricing protection after multi-source entry. This strategic shift is visible across the United States generic drugs market in both pipeline design and external deal activity. Viatris announced approval of the first generic iron sucrose injection in the United States in August 2025, while Apotex received FDA approval in April 2026 for generic Infuvite Adult and Pediatric Injections with 180-day Competitive Generic Therapy exclusivity[1]Viatris, “Viatris Announces Approval of First Generic Iron Sucrose Injection in the US,” Viatris Newsroom, newsroom.viatris.com. Hikma has also highlighted injectables, respiratory products, and semi-solids as key R&D priorities for high-value pipeline delivery. The main commercial attraction is that fewer firms can navigate the technical and regulatory demands of these products, which slows competitive crowding after launch. That makes complex dosage forms an important margin defense within the United States generic drugs market through 2031.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Multi-Source Price Erosion | -0.7% | Global, most acute in US oral solid generics | Long term (≥ 4 years) |

| Nitrosamine Testing And Reformulation Burden | -0.3% | Global, US compliance deadline creates near-term cost spike | Medium term (2-4 years) |

| PBM Specialty-Generic Markups Distorting Uptake | -0.4% | US, concentrated in specialty channel | Medium term (2-4 years) |

| Retail Pharmacy Closures Reducing Substitution Throughput | -0.3% | US national, disproportionate in rural and low-income areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Multi-Source Price Erosion: A Structural Margin Drain That Suppresses Investment Return

Price erosion remains the most persistent structural restraint in the United States generic drugs market because mature molecules lose pricing power quickly after several competitors enter. Once that happens, volume growth often fails to translate into revenue growth at the same rate, which weakens returns on filings that looked attractive at launch. The problem is most severe in commodity oral solids, where substitution is easy and commercial differentiation is limited. Sandoz reported USD 7.8 billion in net sales for 2025 with 2% constant-currency growth, which illustrates how large volumes can still produce modest top-line momentum when price pressure remains intense[2]Sandoz Group AG, “Sandoz Delivers Strong Full-Year Results, Guidance for 2026 Reflects an Expected Acceleration in Growth,” WebDisclosure, webdisclosure.com. This environment pushes companies toward complex generics and biosimilars, but not every firm has the capital or technical base to make that transition at speed. The result is a United States generic drugs market in which operating discipline matters as much as launch success.

PBM Specialty-Generic Markups Distorting Uptake: A Market Efficiency Failure with Policy Implications

The Federal Trade Commission reported in January 2025 that the three largest PBMs applied markups of 100% to 7,736% on specialty generic drugs dispensed through affiliated pharmacies, creating USD 7.3 billion in excess revenue relative to acquisition cost benchmarks. The same report stated that 63% of specialty generic prescriptions were reimbursed at more than 100% above acquisition cost, and 22% were marked up by more than 1,000%. This does not reduce the technical ability to launch a generic, but it does distort where volume flows and which dispensing channels benefit. Therapeutic areas such as oncology and other specialty categories are more exposed because reimbursement design can overpower normal substitution logic. Independent and unaffiliated pharmacies face a weaker economic position under this structure, which slows broader diffusion across channels. In the United States generic drugs market, the restraint is therefore tied to channel efficiency rather than product supply alone.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Brand Status: Unbranded Volume Dominates, but Branded Generics Capture Margin Growth

Unbranded generics held 82.31% of the United States generic drugs market share in 2025, which shows how firmly substitution rules are embedded across U.S. dispensing channels. This segment remains the basic operating core of the United States generic drugs market because payers, providers, and pharmacies are already organized around lower-cost substitution at scale. Commercial health plans and government programs have built decades of formulary behavior around these products, so demand is broad rather than concentrated in a few therapeutic classes. That gives unbranded portfolios a stabilizing role even when molecule-level pricing weakens after new competition arrives. It also explains why large manufacturers continue to treat broad portfolio coverage as a defensive asset rather than just a volume business.

The branded generic segment is smaller, but it is forecast to grow at 5.38% CAGR through 2031, which makes it the faster-moving opportunity in this split. Growth is being supported by authorized generic launches, reformulations, device-linked presentations, and other product variations that delay full commoditization. In practice, branded generics can create a short earnings window when a product enters the market with limited competition and stronger channel recognition. That window narrows once multiple producers enter and pricing resets, but it still matters for firms that can sequence launches around the loss-of-exclusivity calendar. The United States generic drugs industry is therefore treating branded generics less as a permanent share pool and more as a timed profitability event. Within the United States generic drugs market, this creates a two-speed structure in which volume sits with unbranded products while near-term margin opportunities often emerge in branded formats.

By Molecule Type: Small Molecules Form the Base, Biosimilars Drive the Growth Narrative

Small molecule generics accounted for 85.24% of the market in 2025, which reflects the long-standing dominance of tablets, capsules, and other familiar prescription formats. This share gives the United States generic drugs market a large and resilient volume base that is closely tied to chronic-disease prescribing patterns. Many near-term launches in cardiometabolic, CNS, endocrine, and anti-infective therapy still flow through this part of the market. The segment also benefits from established manufacturing systems, broad pharmacy stocking behavior, and a regulatory pathway that is well understood by experienced filers. Even so, the category faces its heaviest pressure in molecules that attract dense filing activity and rapid multi-source competition.

Biosimilars are projected to grow at 7.52% CAGR through 2031, making them the strongest growth engine by molecule type in the United States generic drugs market. The expanding biosimilar opportunity is already visible in the commercialization pace, with 92 FDA-cleared biosimilars across 20 molecules and 67 U.S. launches by March 2026. Samsung Bioepis also noted that the FDA’s draft and revised guidance in late 2025 and early 2026 signaled greater flexibility around comparative efficacy expectations and non-U.S. comparator use, which could shorten development timelines for future programs. That does not mean every biologic loss-of-exclusivity event will have an immediate biosimilar response, because development remains expensive and technically selective. The United States generic drugs industry still faces a meaningful execution threshold under the biosimilar user fee and launch planning framework. Even so, the United States generic drugs market is steadily shifting from a small-molecule story toward a mixed small-molecule and biologics substitution story.

By Therapeutic Area: Cardiovascular Scale Anchors Revenue, Oncology Defines the Growth Gradient

Cardiovascular therapies accounted for 25.52% of the United States generic drugs market size in 2025, giving this category the largest revenue base among therapeutic areas. The segment’s scale comes from long treatment duration, broad patient populations, and years of accumulated loss-of-exclusivity across statins, antihypertensives, anticoagulants, and related therapies. It remains central to the United States generic drugs market because prescription refill behavior is strong and payer substitution is already mature. These qualities make cardiovascular drugs a dependable base for both retail and institutional dispensing. They also mean that each new loss-of-exclusivity event in this area can add meaningful volume even when pricing is competitive.

Oncology is forecast to grow at 7.28% CAGR through 2031, which gives it the highest growth rate among therapeutic areas in the United States generic drugs market. The strongest proof point comes from biosimilar penetration, as trastuzumab reached 88% molecule-level market share and bevacizumab reached 92% in the third quarter of 2025. This section of the market is being shaped by successive biosimilar approvals and by payer acceptance that is stronger than in several other biologic categories. CNS, endocrine and metabolic, respiratory, and anti-infective therapies also remain active launch zones, which broadens the growth base beyond oncology alone. In anti-infectives, pricing pressure remains heavy in older commodities, but manufacturers can still protect value through sterile injectable formats and differentiated delivery. Hikma’s emphasis on high-value injectables supports that direction and shows how therapeutic focus is increasingly tied to formulation strategy. For the United States generic drugs market, oncology sets the pace for expansion, while cardiovascular medicines continue to anchor total revenue.

By Route of Administration: Oral Volume Is the Foundation, Inhalation Momentum Is Underappreciated

Oral generics represented 72.52% of the market in 2025, making them the largest route of administration across the United States generic drugs market. This dominance reflects the simple fact that many high-volume generic prescriptions in cardiometabolic and CNS care still default to tablets and capsules. Oral products also benefit from mature manufacturing lines and wide dispensing across retail pharmacies, mail-order services, and institutional buyers. The route remains the economic backbone of the market even when unit pricing is under pressure. That is why scale players continue to defend oral portfolios while they invest in more technically demanding platforms.

Inhalation generics are projected to grow at 5.28% CAGR through 2031, which gives the segment more strategic weight than its current size suggests. The core attraction is regulatory difficulty, because manufacturers must show both drug performance and device equivalence before launch. This tends to limit the field of viable entrants and protects pricing longer than in basic oral solids. Injectable formats are also gaining importance as the United States generic drugs market moves toward long-acting, sterile, and complex hospital products. These programs require more specialized development and manufacturing capabilities, which favors firms with broader technical depth. Topical and dermal products remain part of the mix, but their growth profile is steadier and their entry barriers are usually lower than in inhalation and injectables. The United States generic drugs market is therefore evolving from route-based volume concentration toward route-based margin differentiation. That shift matters because route complexity is becoming a practical filter for where future investment will earn acceptable returns.

By Distribution Channel: Retail Holds the Base, Online Pharmacies Reshape the Margin Stack

Retail pharmacies held 78.52% of the United States generic drugs market share in 2025, which keeps the channel at the center of prescription fulfillment. This lead reflects the role of neighborhood dispensing in chronic disease therapy, refill management, and immediate access for maintenance drugs. Retail also remains important because a large part of the United States generic drugs market still depends on broad physical distribution rather than highly specialized administration settings. Even so, the channel is under structural stress from store closures, staffing pressure, and weaker economics in several local markets. A 2024 Health Affairs study highlighted by the UC Berkeley School of Public Health found that nearly 1 in 3 retail pharmacies had closed since 2010, with rural areas and predominantly Black and Latino neighborhoods facing disproportionate losses.

Online pharmacies are forecast to grow at 7.54% CAGR through 2031, making them the fastest-growing channel in the United States generic drugs market. Amazon stated in February 2026 that Amazon Pharmacy would expand same-day medication delivery to 4,500 U.S. cities and towns by year-end, which strengthens convenience-led competition for standard prescriptions. This shift changes the margin stack because digital fulfillment can pair lower dispensing friction with subscription pricing models for common generics. Hospital pharmacies remain important for sterile injectables and acute-care use, while specialty pharmacies keep gaining relevance in oncology and biosimilar dispensing. That growth is not fully efficient, because PBM ownership structures can steer reimbursement and concentrate volume in captive specialty channels. The United States generic drugs industry is therefore moving toward a more mixed channel structure in which physical retail still leads, but online and specialty formats shape the next layer of growth. For the United States generic drugs market, distribution is no longer just a fulfillment issue, it is a major determinant of where value is captured.

Geography Analysis

The United States generic drugs market size stood at USD 154.45 billion in 2026, and this national scale reflects both broad prescription demand and the single-regulator structure under the FDA. The United States generic drugs market operates under one federal approval framework, but access and dispensing capacity vary widely across states and local communities. High-value growth is becoming more concentrated in complex generics and biosimilars, which places greater importance on manufacturing readiness, specialty distribution, and payer access. Imported supply still plays a major role in supporting U.S. availability, which means domestic policy changes can reshape sourcing even when end demand stays stable. This makes geography in the United States generic drugs market less about formal regional markets and more about where production, dispensing, and reimbursement conditions are strongest.

Dispensing infrastructure has become more uneven as retail pharmacy closures continue to accumulate across the country. The Health Affairs research highlighted by UC Berkeley found that closure rates have been especially severe in rural communities and in predominantly Black and Latino urban neighborhoods. When local pharmacy access weakens, patients shift toward mail-order and online channels, which can support digital growth but may slow direct substitution in certain chronic categories. The practical result is that the same United States generic drugs market can show different fulfillment patterns depending on local store density, insurer design, and patient access to digital pharmacy services.

Domestic production geography is also shifting under federal policy pressure. Executive Order 14293 in May 2025 directed agencies to streamline approval timelines for domestic manufacturing and increase foreign facility for-cause inspections, while the August 2025 order created the Strategic Active Pharmaceutical Ingredients Reserve[3]The White House, “Regulatory Relief to Promote Domestic Production of Critical Medicines,” The White House, whitehouse.gov. These measures improve the relative appeal of U.S.-based manufacturing investments for large generic producers that can support domestic scale. In practical terms, the United States generic drugs market is likely to direct more incremental investment toward states that already have pharmaceutical labor pools, manufacturing infrastructure, and permitting capacity.

Competitive Landscape

The United States generic drugs market remains moderately consolidated at the top, with Teva, Viatris, Sandoz, Amneal, Hikma, and large Indian-origin multinationals setting much of the commercial pace. These firms control a large share of filing activity, supply depth, and launch readiness, but the market still contains a long tail of mid-sized and niche competitors. That structure prevents a winner-take-all outcome because many product markets become intensely contested after approval. In the United States generic drugs market, competitive advantage therefore comes from breadth, technical depth, and low-cost execution rather than from brand power alone.

Strategic behavior across the leader group has become more consistent over the last year. One track is portfolio migration away from pure commodity oral solids and toward biosimilars, injectables, and other complex formats where the number of credible entrants is lower. A second track is capability buying through selective transactions, as shown by Amneal’s April 2026 agreement to acquire Kashiv BioSciences for USD 1.1 billion to strengthen vertical integration in biosimilar manufacturing. Teva also announced the USD 700 million acquisition of Emalex Biosciences in April 2026 to deepen its neuroscience portfolio beyond the core generics base. Viatris moved in a different direction by closing the USD 815 million divestiture of its Biocon Biologics stake in the first quarter of 2026, which signals a preference for a lighter integration model in biosimilars.

White-space opportunities still exist, but they are concentrated in narrower lanes than before. First-time generics with 180-day Competitive Generic Therapy exclusivity remain attractive because they provide a temporary pricing shelter that plain oral solids rarely offer. Peptide and GLP-1 pathways are also drawing interest, and Apotex stated in April 2026 that it had received the first U.S. FDA tentative approval for a generic version of semaglutide injection. Another layer of competition is forming around formulation and delivery intellectual property as companies try to extend value after reference biologics lose exclusivity. The United States generic drugs market therefore remains open to new entrants, but the easiest path is no longer simple scale, it is technical specialization, disciplined filing quality, and strong channel positioning.

United States Generic Drugs Industry Leaders

Teva Pharmaceutical Industries Ltd.

Sandoz Group AG

Hikma Pharmaceuticals PLC

Amneal Pharmaceuticals, Inc.

Viatris Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Apotex, in partnership with Orbicular Pharmaceutical Technologies and Gland Pharma, received FDA approval for generic Infuvite Adult and Pediatric Injections, both carrying 180-day CGT exclusivity, marking a significant expansion of Apotex's US sterile injectable portfolio.

- April 2026: Apotex received the first US FDA tentative approval for a generic version of Ozempic (semaglutide injection), in partnership with Orbicular, establishing regulatory proof of concept for the complex peptide generic pathway ahead of any patent-based commercial launch clearance.

United States Generic Drugs Market Report Scope

As per the scope of the report, generic drugs are medications that have the same active ingredients, strength, dosage form, and intended use as brand-name drugs. They are typically sold at a lower cost because they do not have the same development and marketing expenses as the original branded medications.

The segmentation of the United States generic drugs market is categorized by brand status, molecule type, therapeutic area, route of administration, and distribution channel. By brand status, the market is divided into unbranded generics and branded generics. By molecule type, it includes small molecule generics and biosimilars. By therapeutic area, the market covers cardiovascular, central nervous system, endocrine and metabolic, oncology, respiratory, anti-infectives, and other therapeutic areas. By route of administration, the segmentation includes oral, injectable, topical and dermal, inhalation, and other routes of administration. By distribution channel, the market is segmented into retail pharmacies, hospital pharmacies, online pharmacies, and specialty pharmacies. For each segment, the market size and forecast are provided in terms of value (USD).

| Unbranded Generics |

| Branded Generics |

| Small Molecule Generics |

| Biosimilars |

| Cardiovascular |

| Central Nervous System |

| Endocrine and Metabolic |

| Oncology |

| Respiratory |

| Anti-infectives |

| Other Therapeutic Areas |

| Oral |

| Injectable |

| Topical and Dermal |

| Inhalation |

| Other Routes of Administration |

| Retail Pharmacies |

| Hospital Pharmacies |

| Online Pharmacies |

| Specialty Pharmacies |

| By Brand Status | Unbranded Generics |

| Branded Generics | |

| By Molecule Type | Small Molecule Generics |

| Biosimilars | |

| By Therapeutic Area | Cardiovascular |

| Central Nervous System | |

| Endocrine and Metabolic | |

| Oncology | |

| Respiratory | |

| Anti-infectives | |

| Other Therapeutic Areas | |

| By Route of Administration | Oral |

| Injectable | |

| Topical and Dermal | |

| Inhalation | |

| Other Routes of Administration | |

| By Distribution Channel | Retail Pharmacies |

| Hospital Pharmacies | |

| Online Pharmacies | |

| Specialty Pharmacies |

Key Questions Answered in the Report

What is driving growth in the United States generic drugs market through 2031?

Growth is being supported by new loss-of-exclusivity events, expanding biosimilar launches, payer pressure for lower-net-cost substitution, and policy support for domestic manufacturing. The market is projected to rise from USD 154.45 billion in 2026 to USD 195.44 billion by 2031 at a 4.82% CAGR.

Which product type leads the United States generic drugs market today?

Small molecule generics lead by molecule type with 85.24% share in 2025, while unbranded generics lead by brand status with 82.31% share. These categories remain the volume base of the sector.

Why are biosimilars becoming more important in the United States?

Biosimilars are forecast to grow at 7.52% CAGR through 2031, which is faster than small molecules. By March 2026, the FDA had cleared 92 biosimilars across 20 molecules, with 67 already launched in the country.

Which therapeutic area offers the strongest near-term expansion?

Oncology is the fastest-growing therapeutic area at 7.28% CAGR through 2031. This is supported by strong biosimilar penetration, including 88% share for trastuzumab and 92% for bevacizumab in the third quarter of 2025.

How are online pharmacies changing prescription fulfillment in the United States?

Online pharmacies are projected to grow at 7.54% CAGR through 2031, faster than retail channels. Amazon Pharmacys expansion to 4,500 U.S. cities and towns by end 2026 shows how convenience, delivery speed, and subscription models are changing access patterns.

What is the biggest structural risk for generic drug manufacturers in the United States?

Persistent price erosion remains the main structural challenge, especially in mature oral solids after several competitors enter the same molecule. PBM markup practices in specialty generics also reduce channel efficiency and can slow broader adoption.

Page last updated on: