Cannabidiol (CBD) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

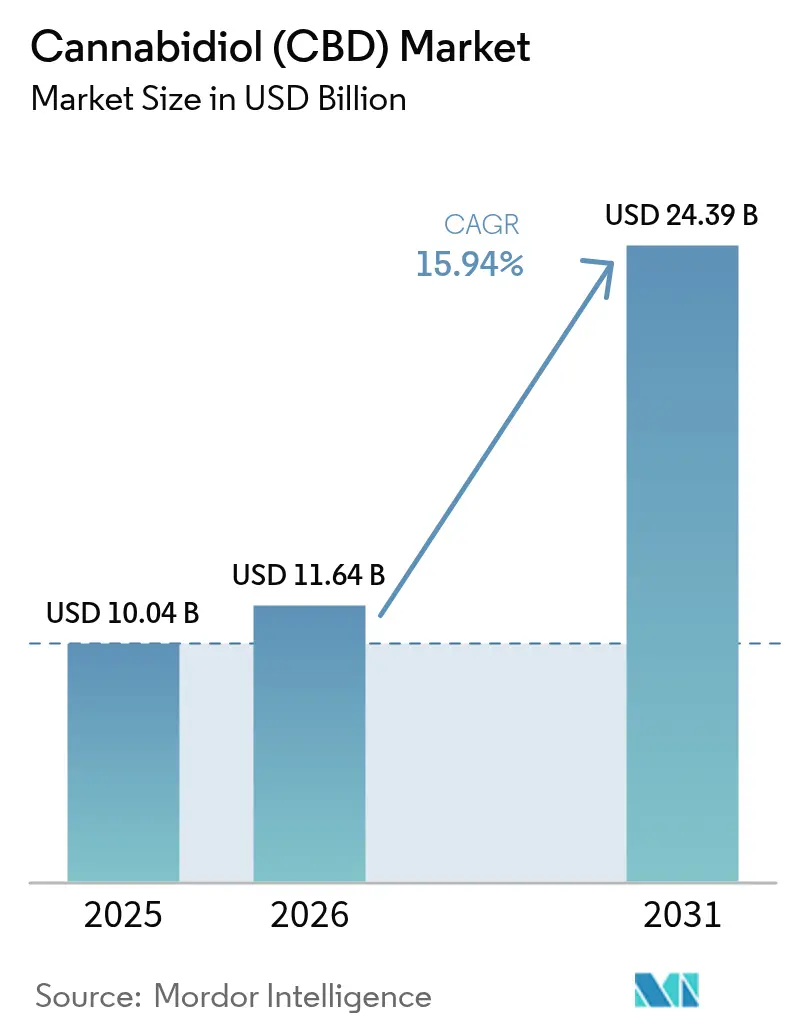

| Market Size (2026) | USD 11.64 Billion |

| Market Size (2031) | USD 24.39 Billion |

| Growth Rate (2026 - 2031) | 15.94% CAGR |

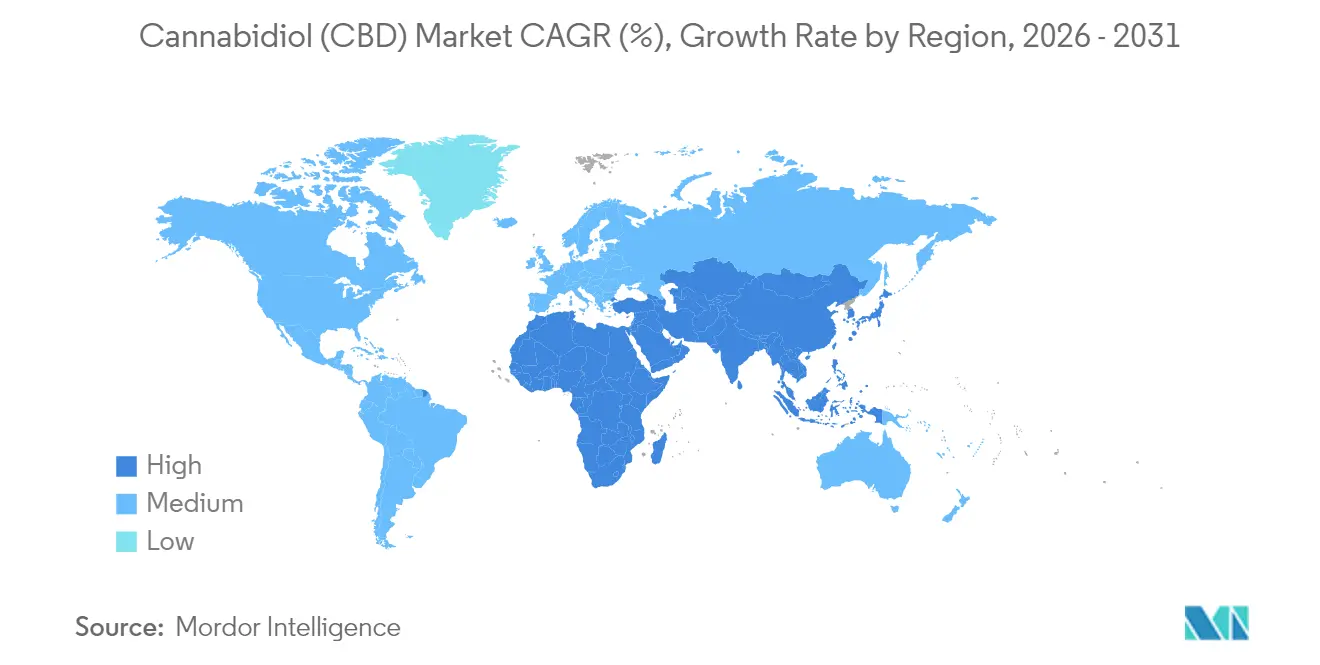

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cannabidiol (CBD) Market Analysis by Mordor Intelligence

The Cannabidiol Market size was valued at USD 10.04 billion in 2025 and estimated to grow from USD 11.64 billion in 2026 to reach USD 24.39 billion by 2031, at a CAGR of 15.94% during the forecast period (2026-2031).

Rapid pharmaceutical-grade innovation is driving the CBD market from niche wellness to mainstream therapeutic and consumer applications. The imminent United States rescheduling of cannabis to Schedule III could unlock FDA-approved cannabinoid drugs for pharmacies, while nanoemulsion and other fast-acting delivery technologies widen the addressable base for ingestibles and topicals. Additionally, Canopy Growth’s acquisition of Wana and Jetty signals that brand portfolios and proprietary IP will dictate competitive advantage in the CBD market.

Key Report Takeaways

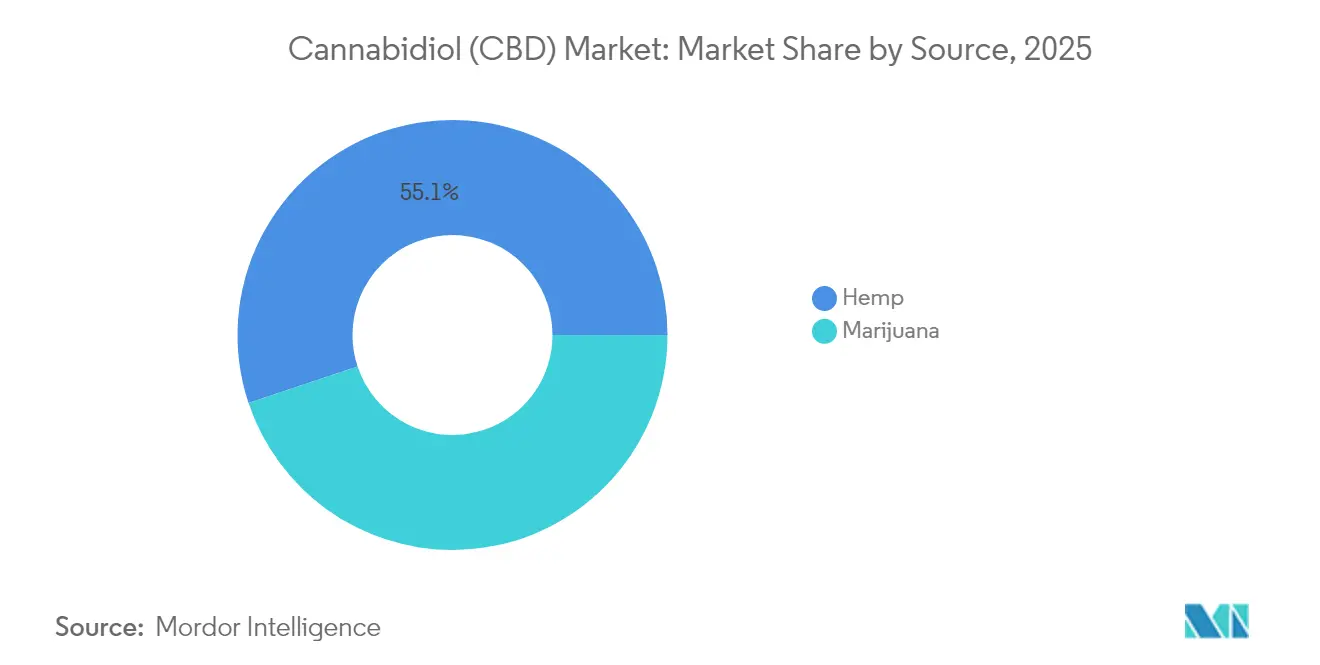

- By source, hemp accounted for a 55.12% share of the CBD market in 2025, while marijuana-derived CBD is set to grow at an 18.35% CAGR between 2026 and 2031.

- By end use, the pharmaceutical segment captured 40.91% of CBD market share in 2025; pet care is projected to expand at a 31.28% CAGR through 2031.

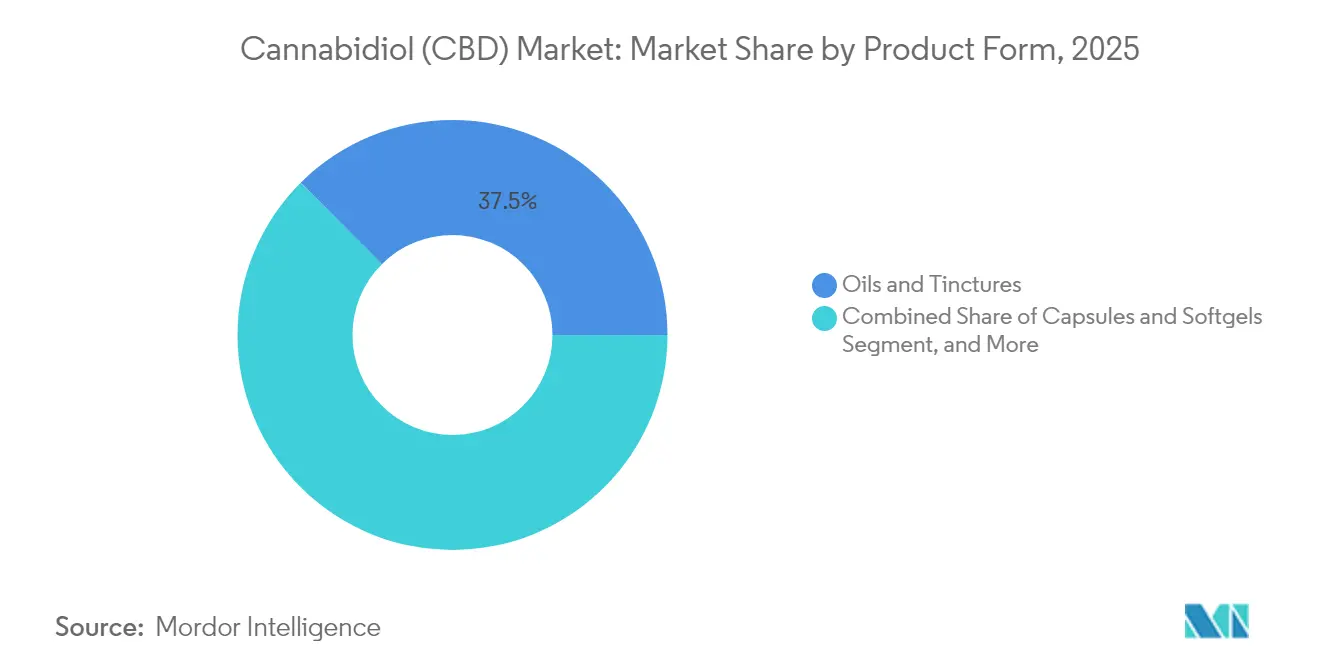

- By product form, oils & tinctures held 37.48% of CBD market share in 2025; gummies & confectionery are forecast to post a 29.35% CAGR to 2031.

- By distribution channel, retail stores led with a 46.02% revenue share in 2025; E-commerce is advancing at a 21.86% CAGR.

- By geography, North America accounted for 46.55% of 2025 revenue, whereas the Asia-Pacific region is estimated to chart a 19.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cannabidiol (CBD) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic pain management driving prescription CBD uptake | +1.2% | North America; Europe | Medium term (2-4 years) |

| Regulatory pathways opening OTC CBD in pharmacy chains | +0.9% | North America; Japan | Short term (≤2 years) |

| Adoption of CBD-infused functional foods among aged population | +0.7% | Europe; North America | Medium term (2-4 years) |

| Increasing consumer health awareness | +0.5% | Global | Short term (≤2 years) |

| Rising integration of CBD in cosmetic and skincare formulations | +0.4% | Asia-Pacific; Europe | Medium term (2-4 years) |

| Expansion of online retail platforms and e-commerce penetration | +0.3% | Global | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Chronic Pain Management Driving Prescription CBD Uptake

Prescription adoption is climbing as CBD proves effective for refractory neurological disorders. Jazz Pharmaceuticals reported 46-87% median seizure reductions in multiple epilepsy types, and 89% of caregivers intend to continue Epidiolex therapy. Nurses documented seizure declines in 85% of treated cases, and behavioral improvements were observed in patients with tuberous sclerosis complex. These outcomes necessitate broader clinical trials for chronic pain, prompting pharmaceutical investment in cannabinoid research and development. United States rescheduling to Schedule III would facilitate FDA approval and pharmacy distribution, thereby expanding reimbursable access in the cannabidiol market.

Regulatory Pathways Opening for Over-the-Counter CBD in Pharmacy Chains

Japan’s December 2024 Cannabis Control Law revision permits medical cannabis products and introduces a tiered cultivation license, ending a decades-long “drug lag”.[1]GR Japan, “Cannabis Law Reform Summary,” grjapan.comIn the United States, the FDA acknowledges that present supplement rules cannot govern CBD, prompting legislative proposals while states enact divergent measures, such as California’s emergency ban on hemp foods with detectable THC.[2]FDA, “Cannabidiol Product Safety Update,” fda.govMainstream pharmacy groups are therefore preparing OTC shelves for compliant SKUs once federal clarity emerges, expanding the cannabidiol market.

Adoption of CBD-Infused Functional Foods Among Aged Population

Older consumers seek non-pharmaceutical relief for sleep, joint, and inflammatory issues, accelerating demand for functional foods fortified with cannabidiol. Le Herbe’s water-dissolvable powder leverages nanoemulsion to reduce onset to 15–30 minutes and triple shelf life. 3-D-printed tablets allow bespoke dosages, albeit at printer costs above USD 4,000 that limit near-term scaling. Enhanced bioavailability positions CBD beverages and snacks as routine dietary aids with further growth opportunities for the cannabidiol market.

Increasing Awareness among Consumers Regarding Health

Convenience-store surveys show that the majority of shoppers recognize the benefits of CBD, even though trial rates lag. Education campaigns stress correct dosage and COA verification, a strategy reinforced by Tilray’s hemp-derived delta-9 THC beverage roll-out as an alcohol alternative across large developed markets. National beverage chains stocking THC seltzers underscore the normalization of cannabinoid consumption within the expanding cannabidiol market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict regulation on cannabidiol products | −1.4% | Japan; United States | Short term (≤2 years) |

| Price compression from oversupply of hemp biomass | −0.8% | North America | Short term (≤2 years) |

| Banking & insurance restrictions on CBD start-ups in developing countries | −0.5% | Latin America; Africa | Medium term (2-4 years) |

| Lack of uniform global regulatory frameworks and labeling standards | −0.4% | Global | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Strict Regulation on Cannabidiol Products

Japan enforces the world’s lowest THC threshold, demanding zero-detectable levels in imported CBD and limiting raw material to mature stalk and seed, thereby tightening supply channels.[3]USDA FAS, “Japan Hemp Market Report,” usda.govIn the United States, FDA’s stance that current supplement rules are “inadequate” sustains a federal vacuum, while California bans retail hemp foods with detectable THC. Unaligned rules raise compliance costs and delay nationwide rollouts.

Price Compression from Oversupply of Hemp Biomass

Hemp acreage planted boom still feeds inventories, forcing isolate prices downward and cutting brand counts from 4,000 to roughly 2,000. Charlotte’s Web responded by debuting CBN-led “Stay Asleep” gummies to capture premium sleep-aid demand. Ultrasonic and pressurized-liquid extraction allow purity gains that justify higher margins, yet processors without IP or scale exit the CBD market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Hemp Commands Volume While Marijuana Gains Value Momentum

Hemp-derived products captured 55.12% of 2025 revenue as favorable legislation and established farming supply chains ensured consistent input quality. The CBD market size for hemp formats is projected to expand at a mid-teens CAGR as ingestibles and cosmetics widen consumer reach. Demand for marijuana-derived extracts, however, is forecast to climb 18.35% annually between 2026 and 2031 as the entourage effect gains clinical backing and potential U.S. Schedule III status relaxes research barriers. The CBD market welcomes hybrid extraction methods such as Smokenol that capture smoke-borne terpenes, blurring traditional source distinctions and enabling tailored cannabinoid ratios for formulators.

Hemp’s legal clarity supports multinational retailers that require THC-free inventory, especially in Europe and parts of Asia. Marijuana-sourced CBD appeals to prescription channels where trace THC content is permissible under pharmacopoeia standards. As pharmaceutical trials broaden beyond epilepsy to pain and anxiety, vertically integrated cultivators with both hemp and marijuana licenses are best positioned to supply diversified APIs at scale.

By End Use: Pharmaceuticals Lead Revenue; Pet Care Races Ahead

Pharmaceutical applications generated 40.91% of 2025 sales, buoyed by Epidiolex’s USD 198.7 million Q1 2024 revenue and continued expansion into tuberous sclerosis and Lennox-Gastaut syndrome indications. This dominance translates into the highest CBD market share across end uses, with payers increasingly reimbursing cannabinoid prescriptions. The CBD market size for pet care, however, is forecast to advance at 31.28% CAGR as owners adopt functional chews and oils for arthritis, anxiety, and postoperative recovery in companion animals. Veterinary practitioners cite growing peer-reviewed evidence for canine osteoarthritis pain reduction, underpinning demand for GMP-grade tinctures.

Wellness and personal-use SKUs continue evolving toward targeted benefits. “Stay Asleep” CBN plus CBD gummies address the 67% of adults reporting sleep issues, illustrating how broadened cannabinoid profiles capture additional consumer need states. Such functional diversification boosts category resiliency against raw-material oversupply shocks.

By Product Form: Oils & Tinctures Retain Pole Position While Gummies Surge

Consumers gravitate toward oils and tinctures for dosage flexibility, granting the format 37.48% revenue in 2025. Precise droppers and minimal excipients appeal to medically supervised regimens, sustaining trust among health-care providers. Gummies and confectionery, projected to grow 29.35% annually to 2031, attract first-time users who prefer familiar snack formats and tastemasked profiles. Alcohol-replacement trends further energize the CBD market size for gummies; Australian consumers cite cannabis gummies’ hangover-free benefit when choosing them over beer.

Advanced nanoemulsion shortens edible onset to under 30 minutes and boosts bioavailability, eroding oils’ speed advantage and expanding gummies’ evening-winding-down occasions. Topicals are likewise adopting water-soluble nano-drops to lift dermal absorption, underpinning the premiumization of cosmetic SKUs.

By Distribution Channel: Brick-and-Mortar Still Commands Trust; E-Commerce Accelerates

Retail stores accounted for 46.02% of 2025 revenue, as shoppers value live staff guidance and instant product access. Pharmacies, wellness chains, and grocery banners broaden shelf space following clearer local statutes. Nonetheless, E-commerce is on a 21.86% CAGR trajectory. In the CBD market, patients dealing with chronic conditions often prefer one-click reordering and discreet delivery options to avoid stigma and maintain privacy.

Convenience retailers like Circle K expand pilot kiosks stocked with broad-spectrum gummies and seltzers, while Yesway’s Feel Good Shop+ curates impulse-purchase SKUs adjacent to energy drinks. Potential U.S. Schedule III rescheduling would channel FDA-approved cannabinoid drugs into hospital and specialty pharmacies, cementing medical supply chains that align with payer reimbursement and physician prescribing workflows.

Geography Analysis

North America remained the epicenter of the CBD market with 46.55% revenue in 2025. Imminent federal rescheduling is expected to shrink illicit channels, reduce possession arrests, and catalyze double-digit investment in clinical trials. Consolidation is also reshaping the landscape; Cresco Labs’ USD 2 billion acquisition of Columbia Care exemplifies scale pursuit under tightening capital markets. Canada remains the hub for GMP-grade cannabinoid research, while Mexico’s pending secondary regulations could open Latin America’s most populous market.

Asia-Pacific is projected to post a 19.74% CAGR through 2031, propelled by Japan’s landmark reforms that legalize medical cannabinoid products. China’s beauty sector leads CBD adoption via cross-border e-commerce, with luxury serums commanding premium pricing. Australia’s Special Access Scheme facilitates prescription CBD for anxiety and insomnia, building physician familiarity and patient loyalty.

Europe presents sizable upside as Germany moves to decriminalize adult-use cannabis, lifting investor sentiment and reviving Canopy Growth’s European restructuring. The European Monitoring Centre for Drugs and Drug Addiction is drafting a harmonized CBD safety framework, addressing current patchworks that hamper trade. The UK emphasizes novel-food authorizations, fostering white-label supply chains. France and Italy accelerate medical-cannabis trials, stimulating pharmaceutical demand for GMP isolate and distillate.

Competitive Landscape

The CBD market exhibits fragmentation; top multinationals are pursuing vertical integration to control genetics, extraction, and branded distribution. Canopy Growth’s 2024 purchase of Wana and Jetty refocuses its United States strategy on high-margin edibles and solventless concentrates. CV Sciences’ USD 1.4 million acquisition of Extract Labs brings in-house manufacturing and CBD-isolate supply, improving gross margin resilience.

Pharma players anchor the prescription segment: Jazz Pharmaceuticals leverages GW’s IP estate to defend Epidiolex exclusivity while exploring cannabidiol combinations with standard anti-epileptics. Patents for novel delivery, including Real Isolates’ Smokenol, signal a rising R&D intensity and potential litigation barriers for late entrants. Meanwhile, Radicle Science and Open Book Extracts co-develop rigorously tested consumer products, responding to calls from retailers and consumers for transparency.

Startups capitalize on white spaces in the pet wellness, beauty, and sleep aid niches. Capital inflows favor firms with differentiated technology or proprietary genetics, leaving commodity tincture sellers vulnerable amid raw-material price compression. As branding dictates shelf impact, marketing spend shifts toward clinical substantiation and QR-code traceability to reassure cautious shoppers.

Cannabidiol (CBD) Industry Leaders

Cannoid LLC

Medical Marijuana, Inc

Nuleaf Naturals LLC

Elixinol Wellness Ltd.

Aurora Cannabis Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Tilray Brands reported a 9% year-over-year increase in net revenue for Q2 2025, reaching USD 211 million, with a gross profit increase of 29% to USD 61 million.

- January 2025: Canopy Growth reported a 54% reduction in Adjusted EBITDA loss to USD 6 million and improved free cash flow by 16%, despite a 9% year-over-year decline in net revenue to USD 63.0 million.

- December 2024: Charlotte's Web provided an update on DeFloria's Phase 1 clinical trial results for AJA001, a multi-compound hemp extract developed for treating autism spectrum disorder, demonstrating safety and tolerability.

- December 2024: Vireo Growth Inc. announced a USD 397 million merger with Proper Brands and three other cannabis companies, expanding its operations across several states, including Missouri, Nevada, and Utah.

Global Cannabidiol (CBD) Market Report Scope

As per the scope of this report, Cannabidiol (CBD) is a chemical compound obtained from marijuana and hemp plants and is commonly used for medical purposes. The Cannabidiol (CBD) Market is segmented by Source (Hemp and Marijuana ), Application (Anxiety/ Stress, Neurological Conditions, Skin Care, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market report also covers the estimated market sizes and trends of 17 countries across major regions globally. The report offers values (in USD million) for the above segments.

| Hemp |

| Marijuana |

| Pharmaceuticals |

| Wellness & Personal Use |

| Food & Beverages |

| Cosmetics & Skin Care |

| Pet Care |

| Nutraceuticals & Supplements |

| Oils & Tinctures |

| Capsules & Softgels |

| Gummies & Confectionery |

| Topicals / Skin Care |

| Vape Products |

| Others |

| Hospital & Specialty Pharmacies |

| Retail Stores |

| E-commerce |

| Medical Dispensaries |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Source | Hemp | |

| Marijuana | ||

| By End Use | Pharmaceuticals | |

| Wellness & Personal Use | ||

| Food & Beverages | ||

| Cosmetics & Skin Care | ||

| Pet Care | ||

| Nutraceuticals & Supplements | ||

| By Product Form | Oils & Tinctures | |

| Capsules & Softgels | ||

| Gummies & Confectionery | ||

| Topicals / Skin Care | ||

| Vape Products | ||

| Others | ||

| By Distribution Channel | Hospital & Specialty Pharmacies | |

| Retail Stores | ||

| E-commerce | ||

| Medical Dispensaries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current global CBD market size?

The CBD market size stands at USD 11.64 billion in 2026.

What is the forecast compound annual growth rate (CAGR) for the CBD market to 2031?

The market is projected to expand at a 15.94% CAGR and reach USD 24.39 billion by 2031.

Which application segment holds the largest CBD market share?

The pharmaceutical segment led with 40.91% revenue share in 2025.

Which geographic region is expected to grow fastest through 2031?

Asia-Pacific is forecast to post a 19.74% CAGR, the highest among all regions.

What technology is improving CBD product bioavailability and onset time?

Nanoemulsion technology shortens onset to 15–30 minutes and boosts absorption.

How could U.S. Schedule III rescheduling affect CBD pharmaceuticals?

Rescheduling would allow FDA approval of cannabinoid drugs for pharmacies, expanding prescription access and accelerating R&D investment.

Page last updated on: