Botanical And Plant Derived Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 54.71 Billion |

| Market Size (2031) | USD 79.74 Billion |

| Growth Rate (2026 - 2031) | 7.82% CAGR |

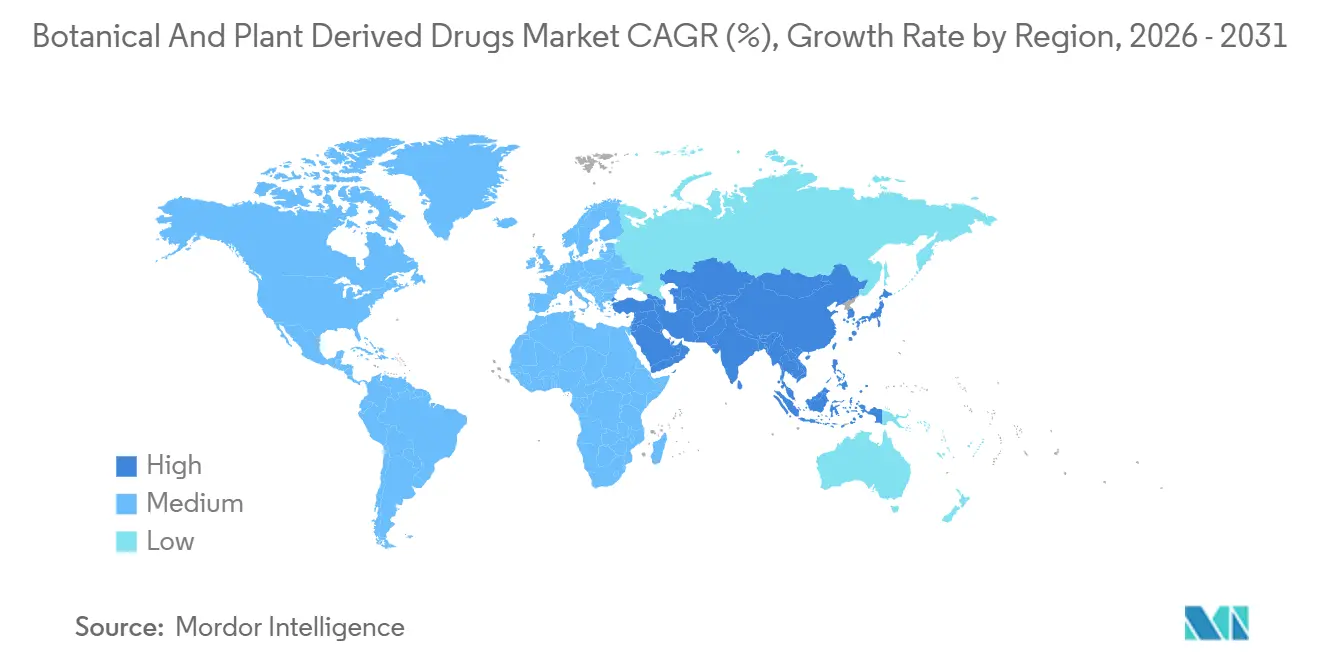

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

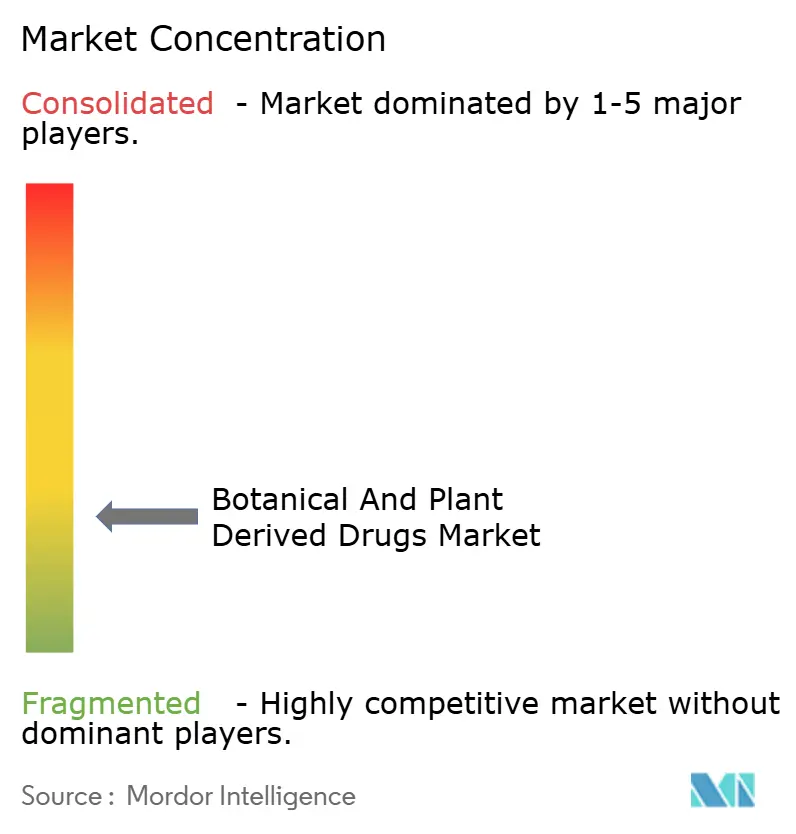

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Botanical And Plant Derived Drugs Market Analysis by Mordor Intelligence

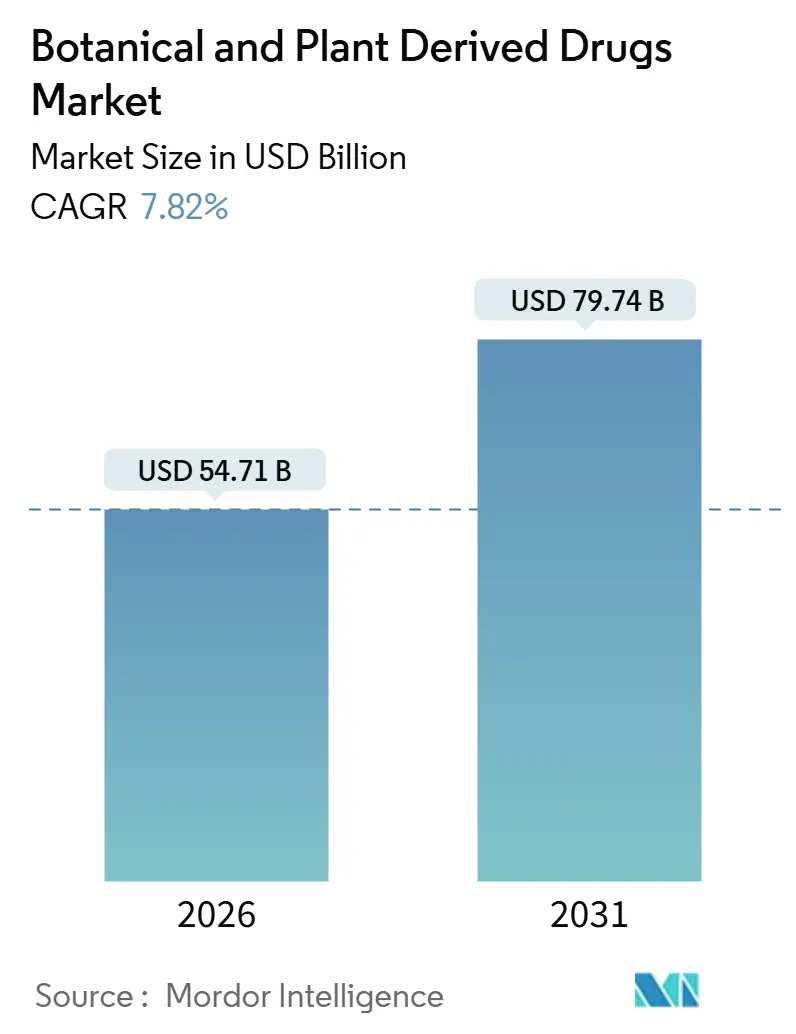

The Botanical And Plant Derived Drugs Market size is estimated at USD 54.71 billion in 2026, and is expected to reach USD 79.74 billion by 2031, at a CAGR of 7.82% during the forecast period (2026-2031).

Regulatory agencies are refining approval pathways for complex extracts, supercritical-fluid platforms are achieving commercial yields, and insurers are piloting coverage models that reward phytomedicines able to curb hospitalization costs. The FDA’s updated botanical drug guidance has shortened investigational timelines by clarifying chemistry-manufacturing-and-controls (CMC) expectations, while the European Medicines Agency’s herbal monograph program supplies a unified quality benchmark across 30 nations.[1]U.S. Food and Drug Administration, "Botanical Drug Development Guidance for Industry," FDA, fda.govCapital is flowing toward plant-cell bioreactors that bypass climate-sensitive cultivation, and toward AI-enabled dosing engines that personalize polyherbal regimens. Competitive intensity is rising as generics manufacturers enter expiring niches, contract development and manufacturing organizations (CDMOs) add phytochemical suites, and digital therapeutics startups bundle botanical products with remote monitoring, squeezing margins on undifferentiated offerings.

Key Report Takeaways

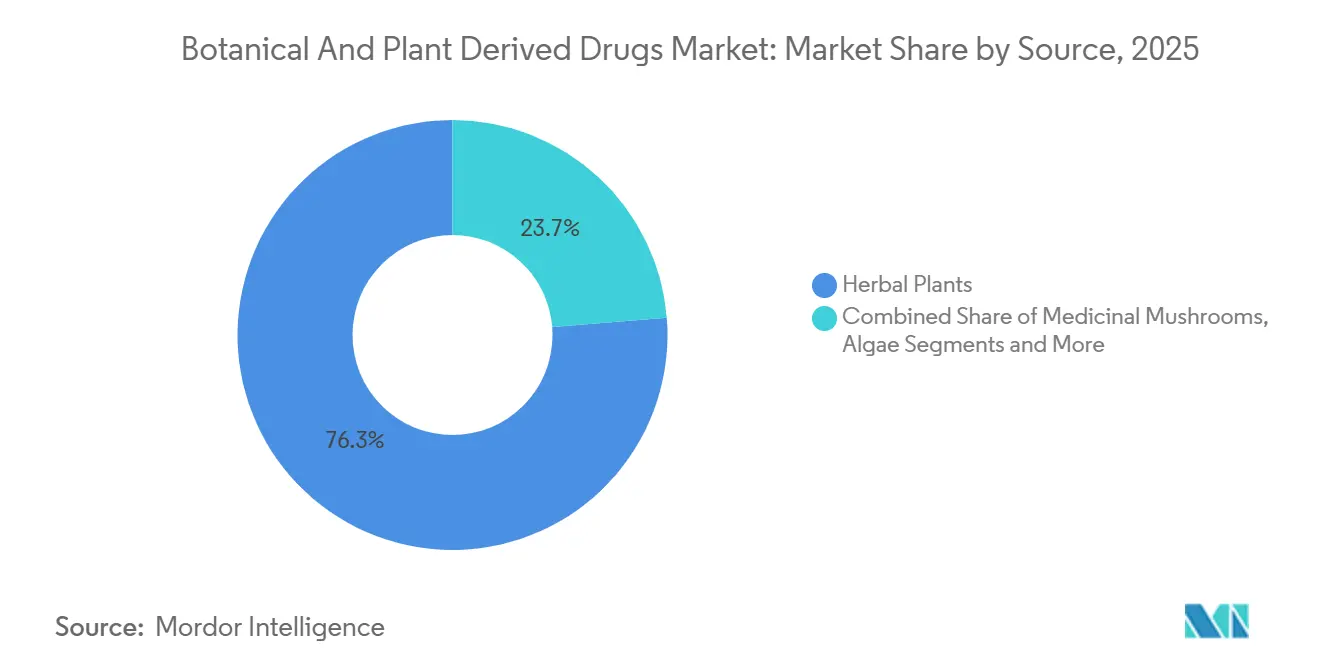

- By source, herbal plants held 76.27% revenue share in 2025, while medicinal mushrooms are set to expand at a 10.42% CAGR through 2031.

- By product type, prescription drugs accounted for 62.45% share of the botanical and plant-derived drugs market size in 2025; OTC products are forecast to grow at 9.13% CAGR to 2031.

- By dosage form, tablets led with 41.46% revenue share in 2025, whereas injectable formulations are advancing at a 9.54% CAGR to 2031.

- By therapeutic area, cardiovascular applications captured 30.24% of botanical and plant-derived drugs market share in 2025; oncology is projected to expand at a 10.32% CAGR between 2026 and 2031.

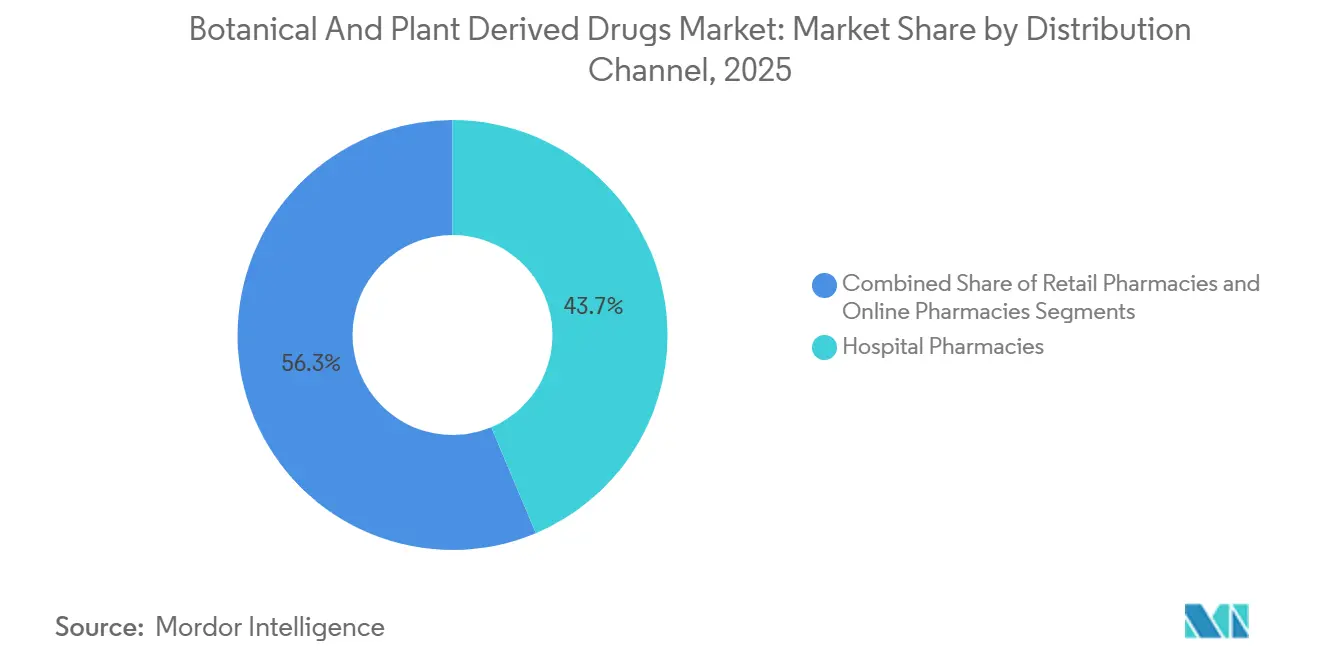

- By distribution channel, hospital pharmacies controlled 43.66% of 2025 revenue; online pharmacies will expand at an 11.77% CAGR to 2031.

- By geography, North America generated 34.74% of global revenue in 2025, while Asia-Pacific is on track for a 9.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Botanical And Plant Derived Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Preference for Natural Remedies | 1.5% | Global, with pronounced uptake in North America & Europe | Medium term (2-4 years) |

| Growing Chronic-Disease Burden Driving Complementary Therapies | 1.3% | Global, acute in aging OECD markets and urbanizing Asia-Pacific | Long term (≥ 4 years) |

| Advances in Extraction & Formulation Technologies | 1.2% | North America & EU innovation hubs, manufacturing scale in Asia-Pacific | Medium term (2-4 years) |

| Regulatory Support for Traditional Medicines | 1.0% | Asia-Pacific core, spill-over to Middle East & Africa | Long term (≥ 4 years) |

| Biomanufacturing Breakthroughs (Plant-Cell Bioreactors) | 0.9% | North America & EU pilot facilities, Asia-Pacific commercial scale | Long term (≥ 4 years) |

| AI-Enabled Personalized Botanical Dosing | 0.7% | North America early adoption, Europe & Asia-Pacific follow | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Preference for Natural Remedies

Consumers are gravitating toward plant-based therapeutics after pandemic-era experiences underscored the importance of immune resilience. An NIH survey documented that 38% of U.S. adults used botanical supplements during 2025, making them the most prevalent complementary modality.[2]National Institutes of Health, "Complementary Health Approaches Among Adults: United States, 2025," NIH, nih.govMillennials and Gen Z cohorts cite perceived safety and sustainability as key drivers, prompting payers to reassess formularies that historically favored synthetics. Cannabidiol solutions for epilepsy and turmeric extracts for arthritis now enjoy mainstream clinical endorsements, while hybrid products that marry botanical actives with conventional excipients blur categorical lines. The FDA’s streamlined botanical pathway reduces development risk, enabling mid-cap innovators to compete against incumbents on speed to market.

Growing Chronic-Disease Burden Driving Complementary Therapies

Non-communicable diseases cause 74% of global mortality, incentivizing health systems to adopt adjunct therapies that improve adherence and defer costly interventions. Hawthorn extract cut heart-failure hospitalization by 12% in a meta-analysis published by the Journal of the American College of Cardiology, validating the botanical and plant-derived drugs market as a source of maintenance therapies.[3]Suzanna M. Zick, "Hawthorn Extract in Heart Failure: A Meta-Analysis," Journal of the American College of Cardiology, acc.org Oncology departments prescribe cannabis-based medicines for chemotherapy-induced nausea and neuropathic pain, while endocrinologists explore cinnamon and fenugreek for glycemic control. Value-based care models amplify this trend because providers assume financial risk for total cost of care, making low-cost botanical adjuncts economically attractive.

Advances in Extraction & Formulation Technologies

Supercritical carbon dioxide extraction delivers pharmaceutical-grade purity without residual solvents, addressing batch variability that once hindered botanical adoption. The FDA's 2024 guidance explicitly recognizes supercritical methods as validated techniques for isolating active constituents. Nanoemulsion platforms boost bioavailability by 3 to 5 times, as demonstrated in a Nature Nanotechnology study showing curcumin-loaded nanoparticles achieved therapeutic plasma levels at one-third the oral dose of standard extracts. Contract manufacturers now offer turnkey extraction and encapsulation, lowering capital barriers for smaller developers. These technologies also enable precision dosing, a prerequisite for prescription-grade products that must meet pharmacokinetic benchmarks comparable to synthetic drugs.

Regulatory Support for Traditional Medicines

China's National Medical Products Administration created a parallel review track in 2024 that accepts historical-use data for formulations documented in classical texts, cutting approval timelines from 36 months to 18 months. India's Central Drugs Standard Control Organisation launched a similar fast-track pathway for Ayurvedic formulations with established safety profiles. The Association of Southeast Asian Nations is negotiating mutual recognition agreements for traditional-medicine registrations, creating a de facto regional standard. Japan's Pharmaceuticals and Medical Devices Agency continues to refine Kampo drug standards, mandating active-marker validation and good agricultural practices. These frameworks converge toward a global baseline that permits multinational companies to leverage a single dossier across jurisdictions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented & Stringent Regulatory Pathways | -0.8% | Global, acute in markets requiring full new-drug applications | Medium term (2-4 years) |

| Raw-Material Quality Variability | -0.6% | Global supply chains, critical for Asia-sourced botanicals | Short term (≤ 2 years) |

| Climate-Change-Induced Supply Shocks | -0.5% | High-altitude & tropical regions, cascading to global supply | Long term (≥ 4 years) |

| IP / Bioprospecting Disputes | -0.4% | Biodiversity-rich regions (Latin America, Africa, Southeast Asia) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented & Stringent Regulatory Pathways

Divergent standards across jurisdictions create duplicative development costs and delay market entry. The United States requires botanical products to follow the investigational new drug pathway with full CMC documentation, while the EU's herbal medicine directive permits traditional-use registration based on 30 years of documented use, including 15 years within the EU. This fragmentation forces companies to maintain parallel programs, effectively doubling clinical and regulatory expenditures for global launches. Smaller innovators struggle to navigate these complexities, often limiting commercialization to a single region and forgoing broader opportunities. The lack of harmonization also creates arbitrage where products approved as dietary supplements in one jurisdiction are marketed as prescription drugs in another, undermining consumer confidence and complicating pharmacovigilance. Efforts toward convergence, such as the International Council for Harmonisation's botanical working group, have made limited progress due to fundamental disagreements over whether mixtures should be regulated as single entities or as combinations of individual constituents.

Raw-Material Quality Variability

Botanical manufacturing faces inherent challenges in standardizing active constituents due to genetic diversity, soil conditions, harvest timing, and post-harvest handling. A Journal of Pharmaceutical Sciences study found that ginseng samples from different suppliers varied by up to 300% in ginsenoside content, even when sourced from the same geographic region. This variability complicates dose-response relationships and can lead to therapeutic failures or adverse events when patients switch suppliers. Regulatory agencies are responding with stricter requirements for raw-material characterization, including DNA barcoding to verify species identity and high-performance liquid chromatography to quantify marker compounds. However, these controls add cost and complexity, particularly for multi-herb formulations where each ingredient requires independent validation. Climate variability exacerbates the challenge, as drought or temperature extremes can alter secondary-metabolite profiles even within a single growing season. Vertical integration is emerging as a risk-mitigation strategy, with pharmaceutical companies acquiring botanical farms and implementing good agricultural and collection practices to ensure traceability from field to finished product.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Medicinal Mushrooms Outpace Traditional Herbs

Herbal plants held 76.27% of source-based revenue in 2025, reflecting their entrenched position in prescription formulations, over-the-counter remedies, and traditional medicine systems. Medicinal mushrooms are forecast to grow at a 10.42% CAGR from 2026 to 2031, driven by psilocybin's breakthrough-therapy designations for treatment-resistant depression and functional mushrooms such as lion's mane and reishi entering mainstream supplement channels. The FDA granted breakthrough status to psilocybin-assisted therapy in 2024, accelerating Phase 3 trials and positioning mushroom-derived compounds as potential blockbusters in psychiatry. Algae represent a smaller but strategically important segment, with spirulina and chlorella gaining traction in nutraceutical formulations and omega-3 production shifting from fish oil to algal sources due to sustainability concerns.

The mushroom surge reflects a broader shift toward psychoactive botanicals for mental health, an area where synthetic drugs face efficacy plateaus and patent cliffs. Clinical data are compelling as a Lancet Psychiatry study reported that psilocybin therapy achieved remission in 37% of treatment-resistant depression patients, compared to 17% for conventional antidepressants. Functional mushrooms are capitalizing on nootropic trends, with brands marketing cognitive-enhancement and immune-support claims backed by preclinical research. Herbal plants remain dominant due to their established supply chains, extensive pharmacopeial monographs, and regulatory acceptance, but innovation is slowing as major botanicals face generic competition and limited opportunities for intellectual property protection. Other botanicals, including resins, gums, and essential oils, serve niche applications in topical and aromatherapy products.

By Product Type: OTC Gains as Self-Care Expands

Prescription drugs accounted for 62.45% of product-type revenue in 2025, anchored by high-value oncology and cardiovascular formulations that require physician oversight. Over-the-counter products are projected to grow at a 9.13% CAGR from 2026 to 2031, fueled by regulatory reclassifications, direct-to-consumer marketing, and digital health platforms that lower barriers to self-medication. The FDA's 2024 decision to grant OTC status to low-dose cannabidiol for sleep disorders exemplifies this trend, expanding access while maintaining safety guardrails through dosage limits and labeling requirements. E-commerce is amplifying OTC growth, as online pharmacies and subscription services bundle botanical supplements with telehealth consultations, creating integrated care pathways that bypass traditional retail.

Prescription botanical drugs retain their premium positioning through intellectual property on extraction methods, delivery systems, and combination formulations. GW Pharmaceuticals' Epidiolex, a cannabidiol oral solution for epilepsy, generated USD 888 million in sales in 2024, demonstrating that botanical drugs can achieve blockbuster status when supported by rigorous clinical evidence and regulatory approval. The OTC segment is fragmenting into premium and value tiers, with premium brands emphasizing organic certification, third-party testing, and transparent supply chains to justify price premiums, while value brands compete on cost and convenience. Regulatory scrutiny is intensifying as adverse-event reports rise, prompting calls for mandatory good manufacturing practices and post-market surveillance for OTC botanicals. The botanical and plant-derived drugs industry is witnessing a shift as consumers increasingly self-direct their care through digital platforms that offer personalized recommendations based on symptom profiles and health goals.

By Dosage Form: Injectables Emerge for Oncology Applications

Tablets captured 41.46% of dosage-form revenue in 2025, benefiting from patient familiarity, manufacturing scale, and compatibility with existing pharmacy infrastructure. Injectables are forecast to grow at a 9.54% CAGR from 2026 to 2031, driven by oncology's adoption of plant-derived cytotoxics such as paclitaxel, vincristine, and etoposide, which require parenteral administration to achieve therapeutic concentrations. Capsules and pills serve similar markets as tablets but offer advantages for moisture-sensitive botanicals and time-release formulations. Liquids and suspensions cater to pediatric and geriatric populations, while topical formulations address dermatological and musculoskeletal indications. Powders and granules remain niche, primarily used in traditional medicine systems where practitioners customize dosing.

The injectable surge reflects oncology's reliance on plant-derived chemotherapeutics, which account for approximately 60% of approved anticancer drugs according to a Nature Reviews Drug Discovery review. Paclitaxel, sourced from Pacific yew bark or produced via plant-cell culture, remains a first-line treatment for ovarian, breast, and lung cancers, with global sales exceeding USD 1.2 billion in 2024. Manufacturers are developing next-generation formulations such as albumin-bound paclitaxel and liposomal vincristine to improve pharmacokinetics and reduce toxicity. Tablets maintain dominance in chronic-disease management, where daily oral dosing aligns with patient preferences and adherence strategies. Regulatory frameworks favor tablets for OTC botanicals, as they enable precise dosing and tamper-evident packaging, addressing safety concerns that have historically limited botanical drug adoption. The botanical and plant-derived drugs market size for injectable formulations is projected to expand as oncology departments integrate plant-derived cytotoxics into combination protocols that pair them with immunotherapies and targeted agents.

By Therapeutic Area: Oncology Accelerates on Cannabinoid Adjuncts

Cardiovascular indications represented 30.24% of therapeutic-area revenue in 2025, reflecting widespread use of botanicals such as hawthorn, garlic, and omega-3 fatty acids in hypertension and heart-failure management. Oncology is projected to grow at a 10.32% CAGR from 2026 to 2031, propelled by cannabinoid adjuncts for chemotherapy side effects, plant-derived cytotoxics, and immune-modulating botanicals in integrative oncology protocols. Respiratory applications include herbal expectorants and anti-inflammatory agents, while gastrointestinal products address irritable bowel syndrome and inflammatory bowel disease. Neurological indications are expanding rapidly, with cannabidiol for epilepsy and psilocybin for depression leading the category. Dermatology relies on topical botanicals for wound healing and anti-aging, infectious diseases deploy antimicrobial plant extracts, and other categories encompass metabolic, musculoskeletal, and urological applications.

Oncology's ascent is tied to the integration of botanical drugs into supportive care pathways, where they manage symptoms without interfering with primary chemotherapy. A Journal of Clinical Oncology systematic review found that cannabis-based medicines reduced chemotherapy-induced nausea by 35% compared to placebo, with efficacy comparable to synthetic antiemetic. Plant-derived cytotoxics remain foundational, with taxanes and vinca alkaloids representing USD 3.8 billion in global sales in 2024. Cardiovascular dominance persists due to the chronic nature of heart disease and the preventive focus of botanical interventions, which align with value-based care incentives to reduce hospitalizations. Regulatory pathways favor cardiovascular and gastrointestinal botanicals, which can leverage traditional-use data and surrogate endpoints, whereas oncology applications require rigorous clinical trials demonstrating survival benefits or quality-of-life improvements. The botanical and plant-derived drugs market is witnessing increased investment in oncology as pharmaceutical companies recognize the unmet need for adjunct therapies that improve patient tolerance of aggressive chemotherapy regimens.

By Distribution Channel: E-Pharmacies Disrupt Traditional Retail

Hospital pharmacies commanded 43.66% of distribution-channel revenue in 2025, serving as the primary outlet for prescription botanical drugs and injectable formulations used in inpatient and outpatient oncology settings. Online pharmacies are forecast to grow at an 11.77% CAGR from 2026 to 2031, capitalizing on e-prescribing integrations, subscription models, and direct-to-consumer brands that bypass traditional retail markups. Retail pharmacies and drug stores remain significant for OTC botanicals, offering immediate availability and pharmacist consultations, but face margin pressure from online competitors. The channel mix is shifting as payers negotiate preferred pharmacy networks and manufacturers launch direct-to-patient programs that bundle medications with adherence support and outcomes tracking.

The e-pharmacy surge is reshaping botanical drug economics, as online platforms aggregate demand and negotiate bulk pricing with manufacturers, passing savings to consumers while capturing data on purchasing patterns and therapeutic outcomes. A National Association of Boards of Pharmacy report noted that online sales of herbal supplements grew by 42% in 2024, outpacing brick-and-mortar growth by a factor of 6. Regulatory oversight is tightening, with the FDA issuing warning letters to online retailers selling unapproved botanical drugs and the Drug Enforcement Administration monitoring e-pharmacies dispensing controlled botanical substances such as cannabis. Hospital pharmacies retain their stronghold in high-acuity settings, where clinical pharmacists play a critical role in dosing, drug-interaction screening, and formulary management for complex botanical regimens. The botanical and plant-derived drugs market share held by online pharmacies is expected to climb as younger patient cohorts prefer digital-first purchasing experiences and as telehealth consultations become reimbursable by a broader range of insurers.

Geography Analysis

North America held 34.74% of geographic revenue in 2025, driven by the United States' large pharmaceutical market, advanced clinical research infrastructure, and regulatory frameworks that support botanical drug development. Asia-Pacific is forecast to grow at a 9.23% CAGR from 2026 to 2031, fueled by China's traditional Chinese medicine modernization initiatives, India's Ayurveda pharmaceutical exports, and Japan's Kampo clinical-validation programs. Europe benefits from the European Medicines Agency's herbal monograph system, which provides a streamlined approval pathway for botanicals with established traditional use. The Middle East and Africa represent emerging markets, with South Africa's indigenous plant biodiversity attracting bioprospecting investments and Gulf Cooperation Council countries importing herbal medicines for expatriate populations. South America, led by Brazil and Argentina, is developing its botanical drug sector around Amazonian biodiversity, though regulatory frameworks remain underdeveloped compared to other regions.

Asia-Pacific's acceleration reflects government policies that integrate traditional medicine into national healthcare systems, reducing out-of-pocket costs and expanding insurance coverage for botanical treatments. China's National Medical Products Administration approved 47 new traditional Chinese medicine products in 2024, a 30% increase over 2023, signaling regulatory commitment to the sector. India's Ayurveda pharmaceutical exports reached USD 1.8 billion in 2024, with major markets in North America and Europe where diaspora communities and wellness trends drive demand. Japan's Tsumura & Co., the leading Kampo manufacturer, reported revenue of JPY 148 billion (USD 1.1 billion) in fiscal 2024, reflecting stable domestic demand and growing international interest in Japanese herbal formulations. The botanical and plant-derived drugs market size for Asia-Pacific is projected to expand as governments invest in clinical validation programs that generate evidence acceptable to Western regulators, enabling cross-border commercialization.

North America's leadership persists due to high per-capita healthcare spending, robust intellectual property protections, and a mature market for dietary supplements that serves as a testing ground for botanical drug candidates. Europe's herbal medicine market is consolidating as multinational pharmaceutical companies acquire regional botanical brands to access established distribution networks and leverage regulatory expertise. The botanical and plant-derived drugs market share commanded by North America is expected to remain substantial through 2031, although Asia-Pacific's faster growth rate will narrow the gap as traditional medicine systems gain global acceptance and as Asian manufacturers scale production to meet international quality standards.

Competitive Landscape

The botanical and plant-derived drugs market exhibits moderate fragmentation, while hundreds of regional manufacturers and contract development organizations serve niche segments and traditional medicine markets. Competitive strategies bifurcate along two axes. Western pharmaceutical companies pursue intellectual property on single-molecule extracts, novel delivery systems, and indication-specific formulations, exemplifying this through Jazz Pharmaceuticals' acquisition of GW Pharmaceuticals for USD 7.2 billion in 2021, securing exclusive rights to cannabidiol epilepsy treatments and a pipeline of cannabinoid therapies. Asian conglomerates such as Yunnan Baiyao and China Traditional Chinese Medicine Holdings vertically integrate from cultivation through distribution, leveraging scale economies and government support to dominate domestic markets while expanding internationally through acquisitions and joint ventures. White-space opportunities are emerging in personalized botanical medicine, where AI-driven dosing platforms and pharmacogenomic testing enable tailored regimens, and in biomanufactured botanicals, where plant-cell culture eliminates agricultural dependencies and enables year-round production at pharmaceutical-grade consistency.

Technology adoption is accelerating as companies deploy supercritical fluid extraction to improve yield and purity, implement blockchain for supply-chain traceability, and partner with digital therapeutics platforms to bundle botanical products with remote monitoring and behavioral interventions. Smaller innovators are carving niches in rare botanicals, where limited competition and high barriers to entry support premium pricing, and in condition-specific formulations that target underserved populations such as pediatric epilepsy or geriatric cognitive decline. Patent filings are concentrated in extraction methods, combination formulations, and indication expansions, with the United States Patent and Trademark Office issuing 342 botanical drug patents in 2024, a 15% increase over 2023. Regulatory compliance is becoming a competitive differentiator, as companies with in-house expertise in FDA botanical guidance and EMA herbal monographs can accelerate development timelines and reduce regulatory risk, attracting partnership interest from larger pharmaceutical companies seeking to diversify portfolios beyond synthetic molecules. The botanical and plant-derived drugs market is witnessing increased merger and acquisition activity as incumbents seek to acquire clinical-stage assets and as private equity firms recognize the sector's defensive characteristics during economic downturns.

Botanical And Plant Derived Drugs Industry Leaders

-

China Traditional Chinese Medicine Holdings

-

Tsumura & Co.

-

Tasly Holding Group

-

Dr. Willmar Schwabe GmbH & Co. KG

-

Yunnan Baiyao Group Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Jazz Pharmaceuticals announced that its cannabidiol product Epidiolex achieved USD 950 million in global sales for fiscal year 2025, representing 18% growth over 2024, driven by label expansions into additional seizure disorders and geographic launches in Asia-Pacific markets. The company is advancing Phase 3 trials for cannabidiol in autism spectrum disorder, with top-line results expected in late 2026.

- December 2025: Nick Jones, a former member of the 82nd Airborne Division, is participating in a first-of-its-kind FDA-approved clinical trial overseen by Dr. Sue Sisley at the Scottsdale Research Institute, which will test whole psilocybin mushrooms in group therapy settings for police, fire personnel and military veterans.

- June 2025: Medsafe has given a New Zealand psychiatrist approval to prescribe medicinal psilocybin for treating treatment-resistant depression. This is the first time psilocybin will be prescribed outside of a research setting in New Zealand, and will give people with this severe condition more options. The approval is specific to this psychiatrist, so only they will be able to prescribe psilocybin. The psychiatrist can prescribe, supply and administer medicinal psilocybin to any patient they have assessed and diagnosed with treatment-resistant depression.

- January 2025: Coloradans will soon be able to take psychedelic mushrooms in a regulated environment as the state's natural medicine program finishes taking shape this year. The voter-approved program will allow licensed facilitators to conduct therapeutic sessions using psilocybin, the active ingredient found in magic mushrooms, starting in 2025.

Global Botanical And Plant Derived Drugs Market Report Scope

Botanical and plant-derived drugs are regulatory bodies approved medicines made from plant materials, algae, or macroscopic fungi, tested for safety and efficacy to treat, diagnose, or prevent diseases.

The Botanical and Plant-Dreived Drugs Market Report is segmented by Source, Product Type, Dosage Form, Therapeutic Area, Distribution Channel and Geography. By Source, the market is segmented into Herbal Plants, Medicinal Mushrooms, Algae, and Other Botanicals. By Product Type, the market is segmented into Prescription Drugs and OTC. By Dosage Form, the market is segmented into Tablets, Capsules, Pills, Injections, Liquids & Suspensions, Topical Formulations, and Others. By Therapeutic Area, the market is segmented into Cardiovascular, Oncology, Respiratory, GI, Neurological, Dermatology, Infectious Diseases, and Others. By Distribution Channel, the market is segmented into Hospital, Retail, and Online. By Geography, the market is segmented into North America, Europe, Asia-Pacific, MEA, and South America. The market report also covers the estimated market sizes and trends across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Herbal Plants |

| Medicinal Mushrooms |

| Algae |

| Other Botanicals |

| Prescription Drugs |

| Over-the-Counter (OTC) |

| Tablets |

| Capsules |

| Pills |

| Injections |

| Liquids & Suspensions |

| Topical Formulations |

| Others (Powders & Granules) |

| Cardiovascular |

| Oncology |

| Respiratory System |

| Gastro-intestinal |

| Neurological |

| Dermatology |

| Infectious Diseases |

| Others |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Source | Herbal Plants | |

| Medicinal Mushrooms | ||

| Algae | ||

| Other Botanicals | ||

| By Product Type | Prescription Drugs | |

| Over-the-Counter (OTC) | ||

| By Dosage Form | Tablets | |

| Capsules | ||

| Pills | ||

| Injections | ||

| Liquids & Suspensions | ||

| Topical Formulations | ||

| Others (Powders & Granules) | ||

| By Therapeutic Area | Cardiovascular | |

| Oncology | ||

| Respiratory System | ||

| Gastro-intestinal | ||

| Neurological | ||

| Dermatology | ||

| Infectious Diseases | ||

| Others | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the botanical and plant-derived drugs space today, and what value does it reach by 2031?

The segment is valued at USD 54.71 billion in 2026 and is projected to climb to USD 79.74 billion by 2031, reflecting a 7.82% CAGR.

Which product or therapeutic focus delivers the highest growth momentum through 2031?

Oncology applications advance the fastest at a 10.32% CAGR, propelled by cannabinoid adjuncts for chemotherapy side effects and plant-derived cytotoxics integrated into combination regimens.

Which recent regulatory actions most significantly accelerate commercialization?

The FDA’s updated botanical guidance streamlines chemistry-manufacturing-and-controls submissions, and China’s NMPA review track now accepts historical-use data, together shortening approval cycles and lowering evidence thresholds for well-characterized extracts.

What primary supply-chain risk does climate change pose, and how are manufacturers responding?

Drought and shifting climates threaten yields of high-altitude and tropical botanicals, pushing raw-material prices up; producers are mitigating risk through vertical farming, seed-bank conservation, and plant-cell bioreactors that bypass field cultivation.

Which distribution channel is expanding the quickest, and why?

Online pharmacies are set to grow at an 11.77% CAGR through 2031 thanks to e-prescribing integrations, subscription models, and direct-to-consumer brands that reduce retail mark-ups and provide doorstep fulfillment.

How does artificial intelligence enhance patient outcomes in this field?

AI-enabled platforms combine pharmacogenomic data, biomarker tracking, and patient-reported outcomes to fine-tune dosing; a 2025 clinical pilot cut opioid co-prescribing by 28% when paired with cannabis-based pain regimens.

Page last updated on: