Thiamine Hydrochloride Injection Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

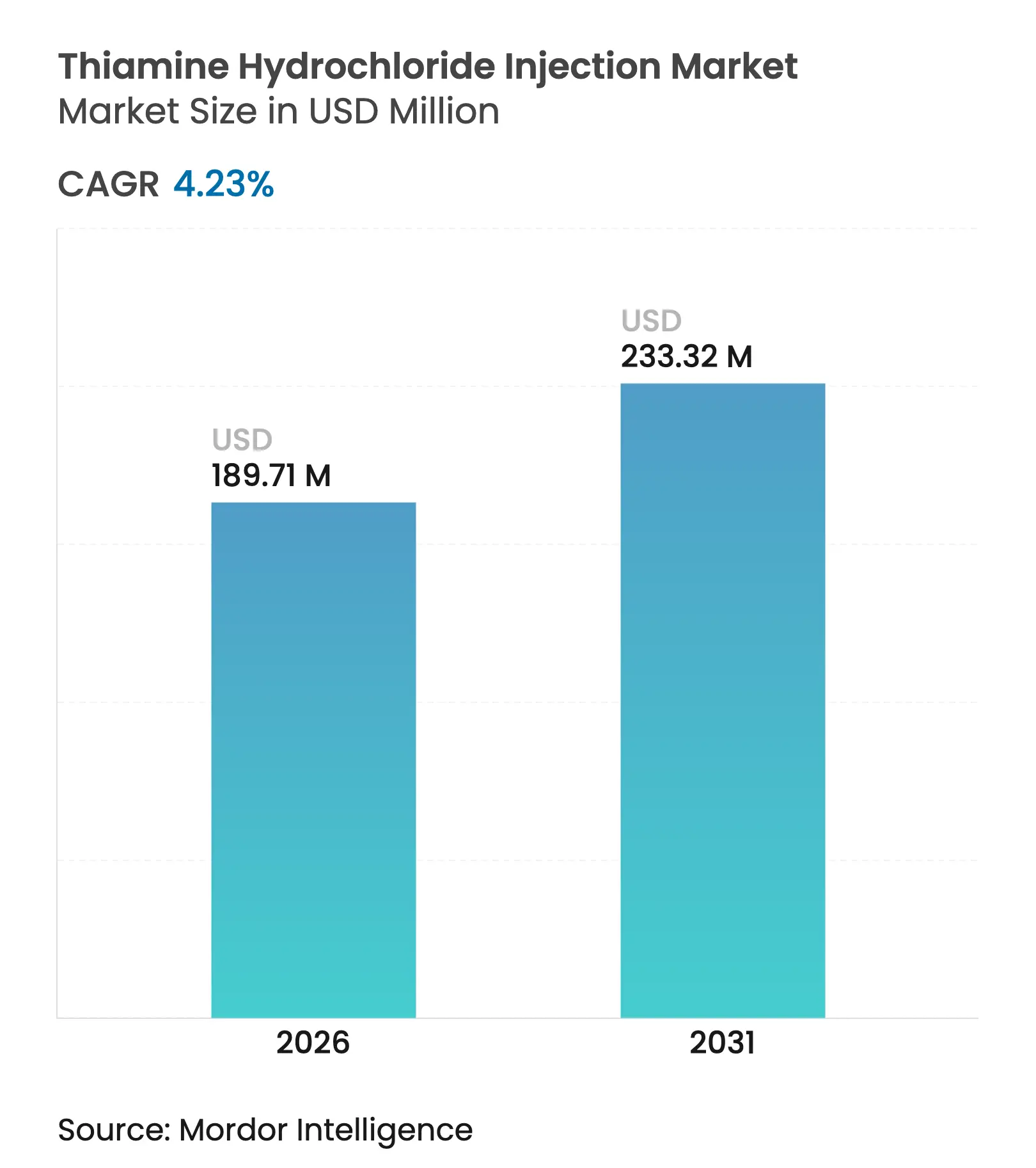

| Market Size (2026) | USD 189.71 Million |

| Market Size (2031) | USD 233.32 Million |

| Growth Rate (2026 - 2031) | 4.23 % CAGR |

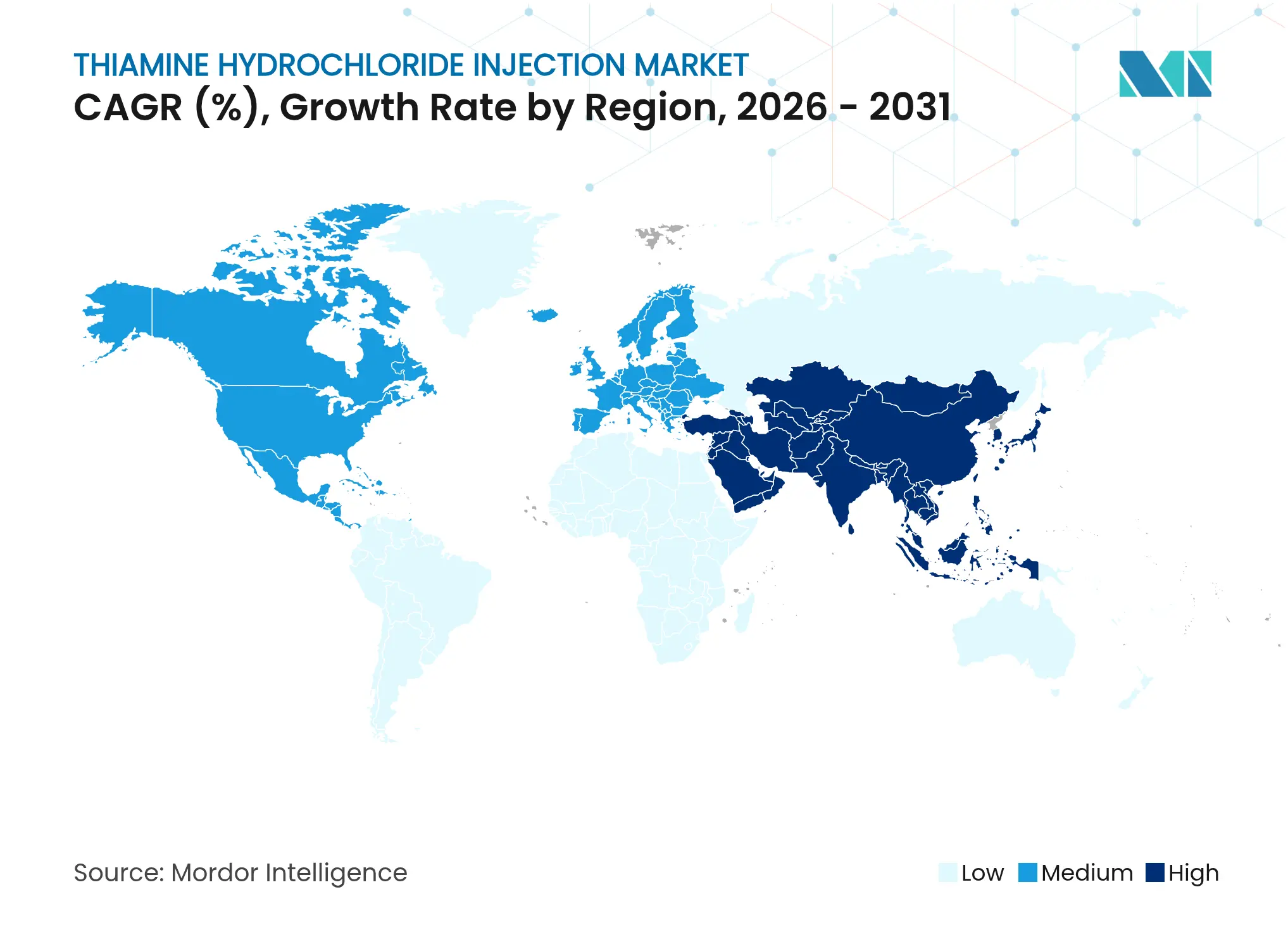

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Thiamine Hydrochloride Injection Market Analysis by Mordor Intelligence

thiamine hydrochloride injection market size in 2026 is estimated at USD 189.71 million, growing from 2025 value of USD 182.01 million with 2031 projections showing USD 233.32 million, growing at 4.23% CAGR over 2026-2031. Growth momentum reflects the compound effect of updated sepsis bundles that recommend parenteral thiamine, inventory hedging in response to prolonged drug shortages, and expanding outpatient infusion infrastructure. Hospitals continue to favor higher-potency 100 mg/mL vials to minimize storage footprints, yet demand for 50 mg/mL strengths is accelerating in ambulatory and home-infusion settings where dose flexibility and safety margins drive purchasing decisions. Ready-to-use (RTU) prefilled syringes are gaining traction as compounding standards tighten, while pre-pandemic supply chain vulnerabilities persist because aseptic lines require specialized regulatory oversight. Regionally, North America leads consumption, but Asia-Pacific offers the fastest growth on the back of healthcare capacity expansion and regulatory harmonization.

Key Report Takeaways

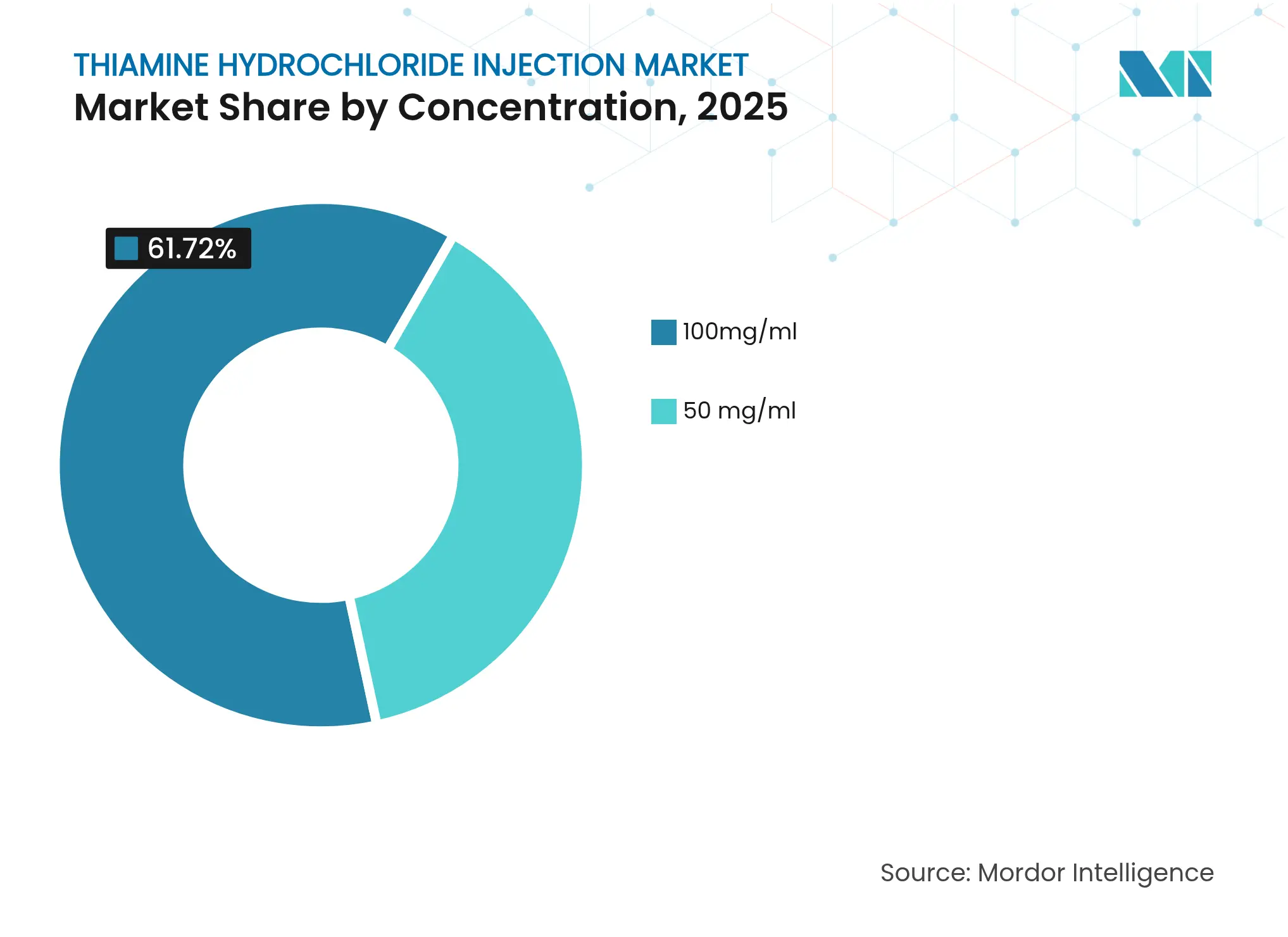

- By concentration, 100 mg/mL led with 61.72% of thiamine hydrochloride injection market share in 2025, 50 mg/mL is projected to advance at a 4.73% CAGR through 2031.

- By packaging type, glass ampoules held 47.85% share of the thiamine hydrochloride injection market size in 2025, RTU prefilled syringes are forecast to expand at a 5.05% CAGR to 2031.

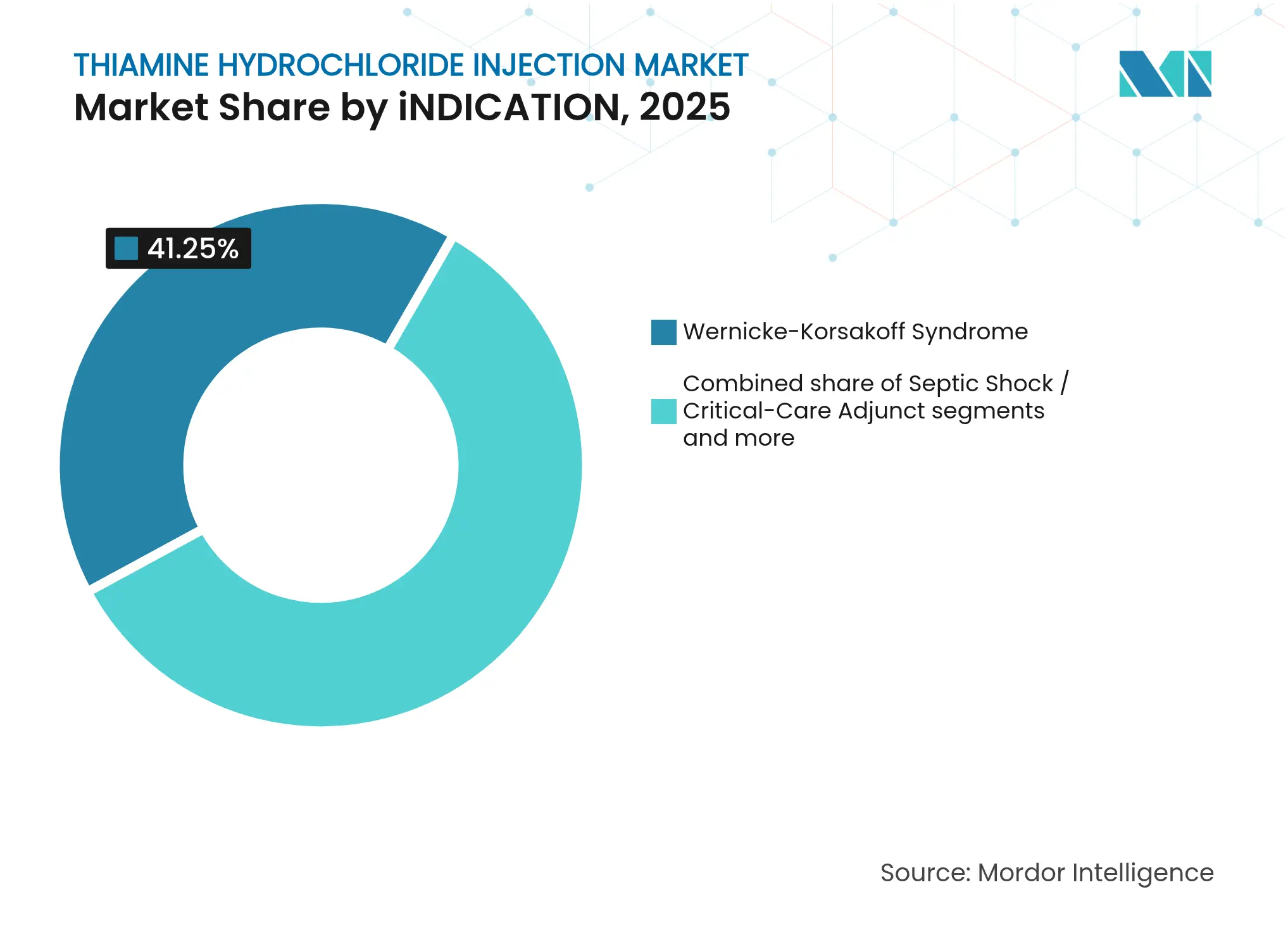

- By indication, Wernicke-Korsakoff syndrome captured 41.25% share of the thiamine hydrochloride injection market size in 2025, septic shock adjunct therapy is registering the highest projected CAGR at 5.29% through 2031.

- By end user, hospitals commanded 68.35% revenue share in 2025, while home-infusion services are rising at a 5.57% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Thiamine Hydrochloride Injection Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growing adoption of IV-thiamine in updated sepsis & septic-shock bundles Growing adoption of IV-thiamine in updated sepsis & septic-shock bundles | +0.8% | North America & Europe | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+0.8% | Geographic Relevance:North America & Europe | Impact Timeline:Medium term (2-4 years) |

Rise in alcohol-related Wernicke-Korsakoff syndrome hospitalizations Rise in alcohol-related Wernicke-Korsakoff syndrome hospitalizations | +0.6% | Global, concentrated in developed markets | Long term (≥ 4 years) | |||

Expanding emergency-medicine protocols for hypoglycemia adjunct therapy Expanding emergency-medicine protocols for hypoglycemia adjunct therapy | +0.4% | North America & APAC | Short term (≤ 2 years) | |||

Chronic shortages of injectable B-vitamins triggering inventory hedging Chronic shortages of injectable B-vitamins triggering inventory hedging | +0.5% | Global | Medium term (2-4 years) | |||

Shift toward ready-to-use (RTU) thiamine syringes in outpatient infusion Shift toward ready-to-use (RTU) thiamine syringes in outpatient infusion | +0.3% | North America & Europe | Long term (≥ 4 years) | |||

Emerging use in mitochondrial disease & metabolic ICU research trials Emerging use in mitochondrial disease & metabolic ICU research trials | +0.2% | Global, research-focused markets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Growing Adoption of IV Thiamine in Updated Sepsis & Septic-Shock Bundles

Updated critical-care guidelines in the United States, Japan, and parts of Europe now embed intravenous thiamine within metabolic resuscitation bundles, elevating routine usage beyond deficiency replacement. Clinical audits show that as many as 70% of ICU patients present with sub-clinical thiamine depletion, prompting protocolized supplementation to optimize lactate clearance and organ perfusion. While meta-analyses report mixed mortality signals, hospital formularies continue stocking thiamine to pre-empt litigation risk and align with quality-improvement metrics. Demand is therefore decoupled from final outcome certainty and instead linked to precautionary practice adoption across tertiary centers.

Rise in Alcohol-Related Wernicke-Korsakoff Syndrome Hospitalizations

Emergency departments in North America and Western Europe record rising admissions for alcohol-induced encephalopathy, with high-dose parenteral thiamine restoring neurologic function in 73% of cases according to multicenter audits. Shortages of Pabrinex in the United Kingdom until late-2025 underscore the fragility of single-supplier pipelines and have shifted procurement toward alternative high-potency generics. Aging demographics with elevated alcohol use disorder prevalence create structural demand tailwinds for thiamine hydrochloride injection market growth.

Expanding Emergency-Medicine Protocols for Hypoglycemia Adjunct Therapy

Several U.S. states revised prehospital guidelines after retrospective evidence showed no significant neurologic outcome difference in hypoglycemic patients receiving thiamine before dextrose. The new stance favors targeted administration for malnourished or chronic alcohol-use patients, curbing unnecessary doses yet reinforcing the need for portable RTU syringes that paramedics can deploy within minutes. Protocol heterogeneity among jurisdictions prolongs parallel stocking of both high-dose and low-dose SKUs, enlarging overall thiamine hydrochloride injection market demand.

Chronic Shortages of Injectable B-Vitamins Triggering Inventory Hedging

The U.S. Department of Health and Human Services reports median shortage durations of 4.6 years for sterile injectables, prompting hospital buyers to stockpile thiamine above daily utilization benchmarks. Safety-stock expansion inflates base-year volumes and rewards manufacturers with uninterrupted fill-finish capacity. The strategy, however, amplifies bull-whip effects when production lapses occur, encouraging vertically integrated firms to invest in redundant aseptic lines near demand centers.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

GMP compliance costs for low-volume aseptic lines GMP compliance costs for low-volume aseptic lines | -0.4% | Global, particularly emerging markets | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-0.4% | Geographic Relevance:Global, particularly emerging markets | Impact Timeline:Medium term (2-4 years) |

Stringent USP <797>/<800> compounding standards raising pharmacy costs Stringent USP <797>/<800> compounding standards raising pharmacy costs | -0.3% | North America | Short term (≤ 2 years) | |||

Frequent API supply disruptions from single-source producers Frequent API supply disruptions from single-source producers | -0.5% | Global | Medium term (2-4 years) | |||

Stability loss in high-pH diluents limiting premix shelf life Stability loss in high-pH diluents limiting premix shelf life | -0.2% | Global | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

GMP Compliance Costs for Low-Volume Aseptic Lines

The U.S. FDA issued a February 2025 warning to Aspen Pharmacare after inspectors cited inadequate laboratory controls and airflow segregation in its injection plant, forcing a production halt for North American shipments[1]Source: U.S. Food & Drug Administration, “Warning Letter: Aspen Pharmacare Holdings,” fda.gov . Comparable findings across smaller Asian contract sites underscore the steep fixed-cost burden of sterile compliance, which scales poorly for low-volume SKUs like thiamine hydrochloride injection. Capital outlays for isolator upgrades and environmental monitoring tilt competitive advantage toward large incumbents with diversified injectable platforms, reinforcing moderate concentration in the thiamine hydrochloride injection market.

Stringent Compounding Standards Raising Pharmacy Costs

Revised U.S. Pharmacopeia chapters mandate engineering controls such as segregated cleanrooms, continuous particle monitoring, and double-check verification for compounded sterile preparations. Many rural hospitals lack the capital to retrofit facilities and thus outsource or switch to branded RTU vials, transferring volume from in-house compounders to commercial manufacturers[2]Source: United States Pharmacopeia, “USP <797>/<800> Compounding Standards,” usp.org . While improving safety, the standards reduce compounding flexibility, potentially tightening localized supply during regional shortages.

Segment Analysis

By Concentration: Diverging Potency Preferences Shape Utilization

The thiamine hydrochloride injection market size associated with 100 mg/mL presentations equal to 61.72% share, owing to hospital protocols that administer 200–500 mg loading doses during acute neurologic crises. Conversely, 50 mg/mL fills registered smaller revenue but posted a robust 4.73% CAGR and are expected to close the gap by 2031 as home-infusion services expand. Hospitals prioritize single-vial efficiency to minimize dose preparation time, yet outpatient clinicians value lower risk of infiltration or dosing error in chronically ill patients. The thiamine hydrochloride injection industry is therefore balancing two potency tiers, forcing manufacturers to maintain dual filling campaigns that complicate batch scheduling.

Further bifurcation emerges at the indication level. Neurologists treating Wernicke’s encephalopathy administer 500 mg IV every 8 hours for 3 days, effectively dictating bulk utilization of the higher concentration. In contrast, metabolic resuscitation in sepsis frequently uses 200 mg doses that can employ either strength, enabling formularies to switch based on available inventory. Emerging solid-state salt forms developed at Purdue University show improved oxidative stability, opening pathways for intermediate concentrations that could simplify inventory management.

Note: Segment shares of all individual segments available upon report purchase

By Packaging Type: RTU Platforms Outpace Legacy Glass

Glass ampoules captured 47.85% revenue in 2025 because of entrenched tender contracts and lower unit costs suitable for high-volume public hospitals. However, RTU prefilled syringes are forecast to outpace at a 5.05% CAGR to 2031, reflecting clinician preference for error mitigation and compliance with time-pressed emergency workflows. Single-dose vials occupy a transitional role; they provide flexibility to draw partial doses while preserving sterility, positioning them well for smaller ambulatory centers seeking incremental modernization. Dual-chamber lyophilized syringe prototypes announced in 2024 promise room-temperature stability of six months, a leap that could enable low-resource settings to adopt RTU technology without cold-chain constraints.

Pricing differentials remain the largest headwind to RTU adoption. A 2 mL 100 mg RTU syringe sells for a 35% premium over the equivalent ampoule in U.S. hospital purchasing organization catalogs. Large systems offset this cost through reduced compounding labor and lower medication error liability, whereas smaller centers rely on distributor rebates to narrow the gap. Thus, while RTU uptake accelerates, the thiamine hydrochloride injection market will maintain a hybrid packaging landscape over the forecast horizon.

By Indication: Clinical Diversification Broadens Addressable Volume

Wernicke-Korsakoff syndrome contribute to 41.25% share of thiamine hydrochloride injection market size, cementing its role as the historical anchor. Septic shock adjunct therapy, is projected to deliver a 5.29% CAGR as metabolic bundles reach guideline saturation in tertiary ICUs across the United States, Germany, Japan, and Australia. General deficiency treatment in bariatric and oncology populations provides a stable stream that buffers volatility in acute-care segments. Hypoglycemia rescue indications remain niche yet clinically compelling, driven by paramedic protocols that prefer compact RTU syringes for field deployment.

Pipeline research is expanding therapeutic frontiers. The NIH-funded BENFOTEAM multicenter trial is probing high-dose benfotiamine in early Alzheimer’s, potentially unlocking neurodegenerative use cases that dwarf current revenue pools. Cardiac surgery trials combining thiamine with ascorbic acid to mitigate ischemia-reperfusion injury showed reductions in troponin I release, signaling cardiothoracic growth potential. Should these trials reach positive endpoints, demand heterogeneity will increase, necessitating broader SKU libraries and pharmacoeconomic analyses.

Note: Segment shares of all individual segments available upon report purchase

By End User: Home-Infusion Takes Growth Spotlight

Hospitals procured 68.35% of 2025 thiamine hydrochloride injection volumes, anchored by emergency departments and ICUs with 24/7 infusion capabilities. Home-infusion companies, however, logged a 5.57% CAGR outlook, aided by payer incentives that favor outpatient administration for chronic alcohol-use disorders and long-term parenteral nutrition. Ambulatory surgery centers leverage perioperative bundles that include thiamine for select gastric bypass and colorectal procedures, enhancing the channel’s mid-single-digit growth.

RTU packaging aligns with decentralized infusion, as evidenced by Australia’s January 2025 endorsement of Thiamine Sterop 100 mg/2 mL as the preferred IV brand across public facilities, emphasizing low-complexity deployment outside hospital pharmacies. As private insurers extend reimbursement to nurse-supervised home injections, volume share is set to migrate gradually from inpatient wards to community care, reinforcing dual-channel strategies for thiamine hydrochloride injection market participants.

Geography Analysis

North America generated 46.10% of global revenue in 2025 on the back of mature critical-care infrastructure and stringent USP standards that favor GMP-validated commercial injectables. U.S. hospitals maintain thiamine safety stocks equivalent to 90 days of use, double pre-COVID norms, inflating baseline demand while clinical utilization rises as sepsis bundles become standard of care. Canada experiences similar protocol adoption, and cross-border supply chains benefit from mutual recognition of manufacturing inspections, enabling efficient distribution from U.S. fill-finish plants.

Europe presents a fragmented yet sizable opportunity. Germany, France, and Italy collectively account for more than half of regional consumption, driven by universal health coverage that reimburses parenteral vitamin therapy for neurologic and critical-care indications. EU Annex 1 revisions have compelled smaller contract manufacturers to exit, consolidating orders with large multinational injectables firms. In the United Kingdom, the prolonged Pabrinex shortage focused parliamentary attention on single-source risk, prompting the National Health Service to broaden its supplier list, a move that opened the door for continental generics companies.

Asia-Pacific represents the fastest-growing geography at a 5.88% CAGR to 2031, propelled by China’s multi-year plan to upgrade ICU bed capacity and India’s rollout of national sepsis guidelines that include metabolic support. Japan’s bioequivalence requirement for imported injectables incentivizes local fill-finish partnerships, while South Korea’s reimbursement code revisions for parenteral vitamins support broader inpatient use. Rising alcohol consumption in Southeast Asia, particularly in Vietnam and Thailand, heightens Wernicke-Korsakoff incidence, drawing attention from regional neurologists who now lobby for standardized thiamine protocols. Australia’s centralized procurement of Thiamine Sterop illustrates how regulatory endorsements accelerate uptake of RTU formats across dispersed outpatient networks.

Competitive Landscape

Market Concentration

Market concentration is moderate: the top five companies command an estimated half of the revenue, with Baxter International, Pfizer, Fresenius Kabi, and B. Braun leveraging global GMP networks to secure large tenders. Their competitive edge centers on redundant aseptic capacity, advanced container technology, and regulatory liaison teams that expedite post-approval manufacturing changes. Mid-tier firms such as Hikma and Amneal address regional tenders and niche concentrations, while specialty players target research-grade formulations for mitochondrial studies.

Strategic moves over 2024–2025 include Baxter’s ten new injectable launches using proprietary SIGMA FLEX containers, increasing shelf life and reducing particulate contamination; Fresenius Kabi’s investment in an Illinois lyophilization suite; and Pfizer’s dual-sourcing of thiamine API from European and Asian partners to mitigate geopolitical risk. Technology acquisition also shapes rivalry: several firms are piloting bacterial nanocellulose microcapsules that stabilize thiamine against oxidation, a platform that could enable room-temperature RTU syringes with two-year dating.

Smaller entrants carve out therapeutic niches—such as high-concentration preservative-free thiamine for mitochondrial crisis research—benefiting from academic grants that bypass traditional formulary hurdles. Contract development and manufacturing organizations (CDMOs) with high-potency isolators align with these innovators to accelerate bench-to-clinic transitions. Overall, the competitive narrative is defined by supply resilience, packaging innovation, and regulatory agility rather than pricing races, protecting margins despite generic molecule status.

Thiamine Hydrochloride Injection Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Exela Pharma Sciences initiated a voluntary nationwide recall affecting select injectable SKUs, underscoring supply chain sensitivity

- June 2024: NSW Health designated Thiamine Sterop 100 mg/2 mL solution as preferred IV brand across Australian facilities

Table of Contents for Thiamine Hydrochloride Injection Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Growing adoption of IV-thiamine in updated sepsis & septic-shock bundles

- 4.2.2Rise in alcohol-related Wernicke–Korsakoff syndrome hospitalizations

- 4.2.3Expanding emergency-medicine protocols for hypoglycemia adjunct therapy

- 4.2.4Chronic shortages of injectable B-vitamins triggering inventory hedging

- 4.2.5Shift toward ready-to-use (RTU) thiamine syringes in outpatient infusion

- 4.2.6Emerging use in mitochondrial disease & metabolic ICU research trials

- 4.3Market Restraints

- 4.3.1GMP compliance costs for low-volume aseptic lines

- 4.3.2Stringent USP <797>/<800> compounding standards raising pharmacy costs

- 4.3.3Frequent API supply disruptions from single-source producers

- 4.3.4Stability loss in high-pH diluents limiting premix shelf life

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook (RTU, lyophilized, dual-chamber bags)

- 4.7Porter’s Five Forces

- 4.7.1Intensity of Rivalry

- 4.7.2Bargaining Power of Suppliers

- 4.7.3Bargaining Power of Buyers

- 4.7.4Threat of New Entrants

- 4.7.5Threat of Substitutes (Oral/PARENTERAL B1 complexes)

5. Market Size & Growth Forecasts

- 5.1By Concentration (mg/ml)

- 5.1.150 mg/ml

- 5.1.2100 mg/ml

- 5.2By Packaging Type

- 5.2.1Glass Ampoules

- 5.2.2Single-dose Vials

- 5.2.3Prefilled Syringes (RTU)

- 5.2.4IV Bags / Infusion Solutions

- 5.3By Indication

- 5.3.1Wernicke–Korsakoff Syndrome

- 5.3.2Septic Shock / Critical-Care Adjunct

- 5.3.3Thiamine Deficiency (General)

- 5.3.4Hypoglycemia Rescue Co-therapy

- 5.3.5Others (Metabolic disorders, Bariatric surgery)

- 5.4By End-User

- 5.4.1Hospitals

- 5.4.2Ambulatory Surgical Centers & Clinics

- 5.4.3Home-Infusion & Long-Term Care

- 5.5By Geography (Value)

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2India

- 5.5.3.3Japan

- 5.5.3.4South Korea

- 5.5.3.5Australia

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4South America

- 5.5.4.1Brazil

- 5.5.4.2Argentina

- 5.5.4.3Rest of South America

- 5.5.5Middle East and Africa

- 5.5.5.1GCC

- 5.5.5.2South Africa

- 5.5.5.3Rest of Middle East and Africa

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Hikma Pharmaceuticals (West-Ward)

- 6.3.2Fresenius Kabi

- 6.3.3Pfizer (Hospira)

- 6.3.4American Regent (Luitpold)

- 6.3.5Exela Pharma Sciences

- 6.3.6B. Braun Melsungen

- 6.3.7Mylan (Viatris)

- 6.3.8Baxter International

- 6.3.9Aurobindo Pharma

- 6.3.10Amneal Pharmaceuticals

- 6.3.11Akorn Pharmaceuticals

- 6.3.12Cipla Ltd.

- 6.3.13Shanghai Harvest Pharmaceutical

- 6.3.14Glanbia Nutritionals

- 6.3.15Shandong Tianli Pharmaceutical

- 6.3.16Thermo Fisher Scientific (Acros)

- 6.3.17SERVA Electrophoresis GmbH

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessmen

Global Thiamine Hydrochloride Injection Market Report Scope

Thiamine hydrochloride injection consists of a sterile solution of thiamine hydrochloride. It is designed for intramuscular (IM) or slow intravenous (IV) administration. Thiamine hydrochloride, or vitamin B1, presents as white crystals or crystalline powder, typically with a faint odor. It is highly soluble in water, soluble in glycerin, slightly soluble in alcohol, and remains insoluble in ether and benzene.

The thiamine hydrochloride injection market is segmented by indication, end-user, and geography. By indication, the market is segmented into Wernicke's disease, dietary supplements, pregnancy, and other indications. By end-user, the market is segmented into hospitals/clinics, home care settings, and other end-users. By geography, the market is segmented into North America, Europe, Asia Pacific, the Middle East and Africa, and South America. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).