US Herbal Medicine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 60.39 Billion |

| Market Size (2026) | USD 64.65 Billion |

| Market Size (2031) | USD 98.49 Billion |

| Growth Rate (2026 - 2031) | 8.79% CAGR |

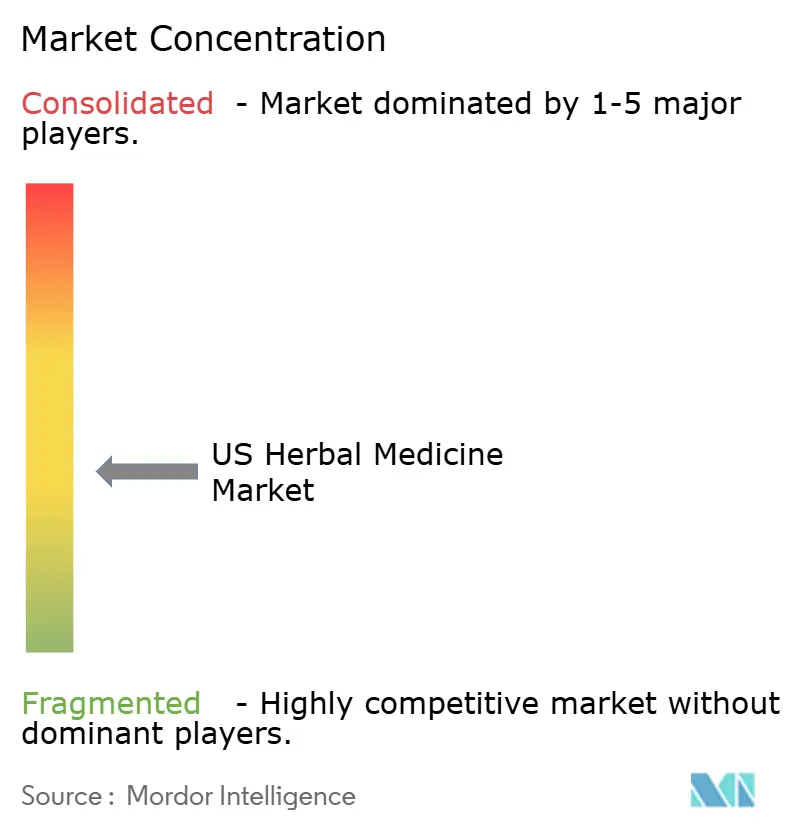

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Herbal Medicine Market Analysis by Mordor Intelligence

The US Herbal Medicine Market size was valued at USD 60.39 billion in 2025 and is estimated to grow from USD 64.65 billion in 2026 to reach USD 98.49 billion by 2031, at a CAGR of 8.79% during the forecast period (2026-2031).

In 2024, retail sales of herbal supplements reached USD 13.23 billion, reflecting a 5.4% year-over-year growth. This increase signals a return to steady growth following a decline in 2022. The direct-to-consumer channel led the market with USD 7.503 billion, surpassing the mass market channel at USD 2.607 billion and the natural, health-food, and specialty channel at USD 3.121 billion.[1]American Botanical Council, “U.S. Sales of Herbal Supplements Exceed $13 Billion at Retail,” Nutraceuticals World, nutraceuticalsworld.com This highlights the growing influence of digital commerce in shaping consumer purchasing behavior in the US herbal medicine market. The market is further driven by older consumers managing chronic conditions with supplements and by new routines focused on digestive and metabolic support, particularly among GLP-1 users. Additionally, clinical substantiation, tariff exposure, and compliance with DSHEA and 21 CFR Part 111 are becoming critical differentiators. Leading brands are increasingly adopting standardized formulations, verified sourcing, and scaled digital distribution to maintain a competitive edge.

Key Report Takeaways

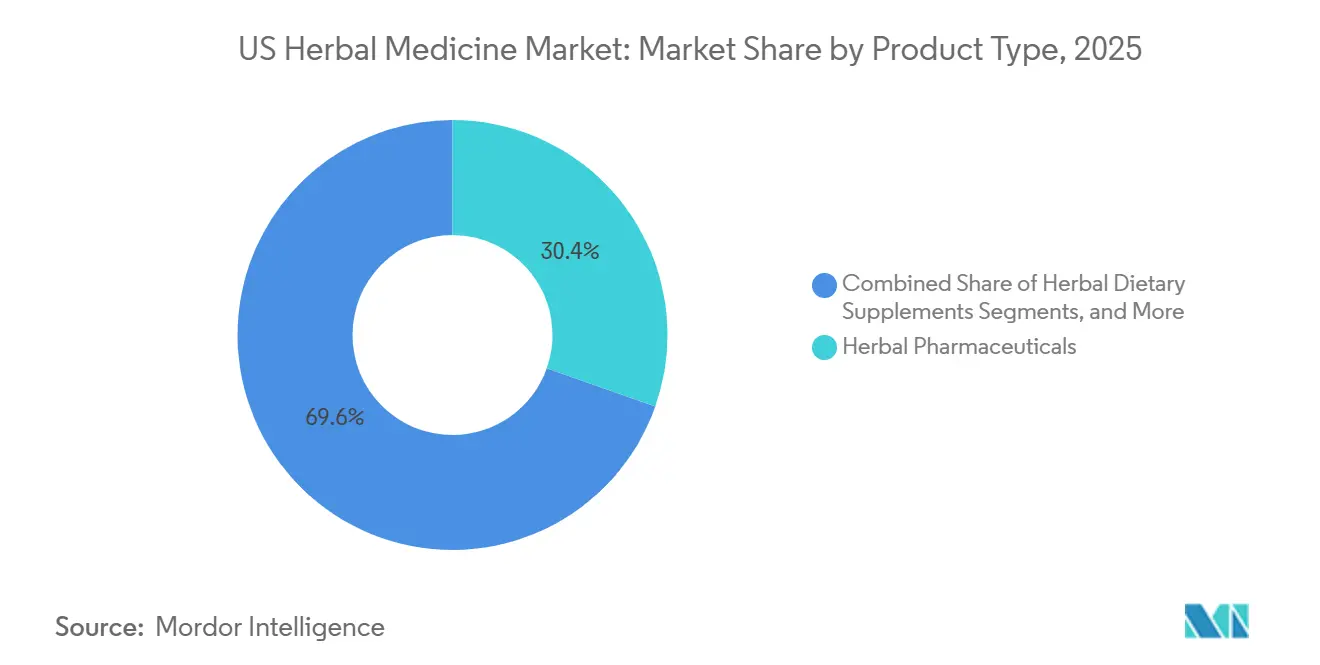

- By product type, herbal pharmaceuticals held 30.44% share in 2025, while Herbal dietary supplements are projected to expand at a 9.42% CAGR through 2031.

- By source, roots & rhizomes held 42.79% share in 2025 and are also projected to grow at a 9.05% CAGR through 2031.

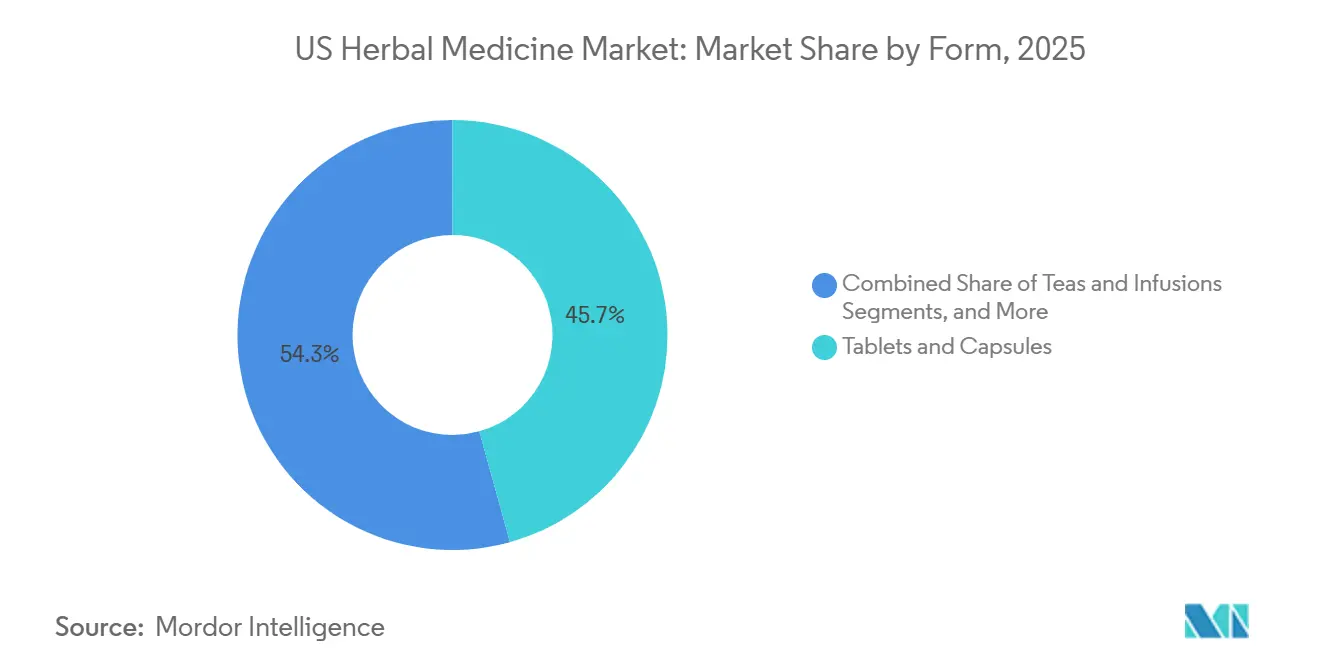

- By form, tablets & capsules led with 45.73% share in 2025, while teas & infusions are projected to advance at a 10.99% CAGR through 2031.

- By distribution channel, hospitals & retail pharmacies accounted for 38.61% share in 2025, while online & e-commerce are expected to record the fastest CAGR at 9.97% through 2031.

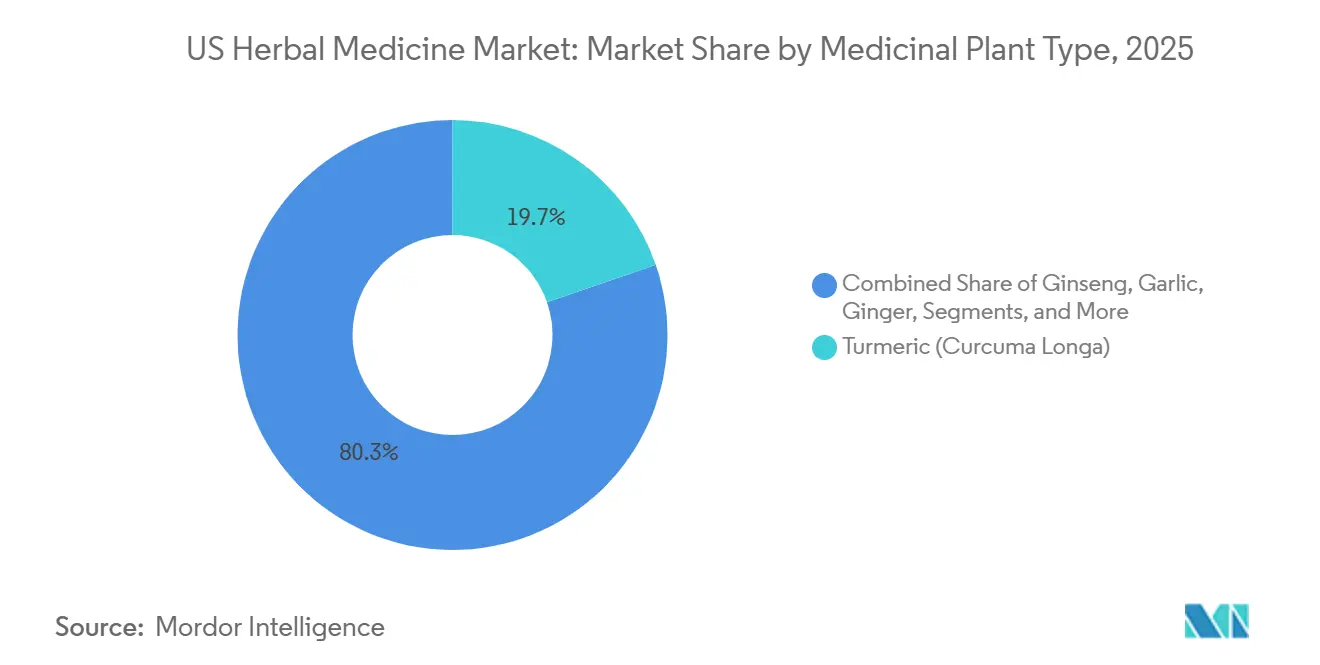

- By medicinal plant type, turmeric held 19.68% share in 2025, while ginseng is projected to grow at a 10.26% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

US Herbal Medicine Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Preventive self-care and natural-remedy preference | +2.4% | National, strongest in coastal metropolitan areas including California, New York, and Massachusetts | Long term (≥ 4 years) |

| Clean-label and plant-based premiumization | +1.3% | National, with stronger concentration in the West and Northeast | Medium term (2-4 years) |

| E-commerce and DTC discovery expansion | +1.6% | National, with rising adoption across the Midwest and South | Medium term (2-4 years) |

| Aging population and chronic-condition self-management | +1.9% | National, strongest in Florida, Texas, Arizona, and the Mid-Atlantic | Long term (≥ 4 years) |

| GLP-1 support routines for digestive and metabolic botanicals | +1.2% | National, with stronger activity in large urban prescription markets | Short term (≤ 2 years) |

| Integrative wellness adoption among Millennials and Gen Z | +0.9% | National, strongest in urban and suburban health-conscious populations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Preventive Self-Care and Natural-Remedy Preference

Preventive health behavior is driving the US herbal medicine market, shifting focus from occasional illness responses to daily wellness routines. Older adults remain key contributors, maintaining supplement spending despite financial constraints, which highlights consistent demand. Consumers increasingly prefer products aligned with long-term wellness goals, as seen in 2024 retail trends where ashwagandha sales rose while elderberry declined. This shift favors premium, evidence-backed products over value offerings, strengthening revenue stability through regimen use rather than one-time purchases.

Aging Population and Chronic-Condition Self-Management

The aging population, projected to reach 73 million by 2030, significantly influences the US herbal medicine market.[2]Frontiers in Nutrition, “Factors Associated with the Use of Combined Nutritional Complementary and Alternative Medicine among Southern US Older Adults, Results from the Study of Aging II,” Frontiers in Nutrition, frontiersin.org Older adults frequently use turmeric and Boswellia for inflammation, ginkgo biloba and ginseng for cognition, and berberine and cinnamon for blood sugar support. Many purchases are driven by consumer research rather than physician recommendations, creating opportunities for education-driven digital sales models. Transparency in herb-drug interactions is critical, as older consumers often manage multiple therapies simultaneously.

GLP-1 Support Routines Lifting Digestive and Metabolic Herbs

GLP-1 adoption is expanding the US herbal medicine market by boosting demand for digestive and metabolic wellness products. Ingredients like ginger, berberine, and ashwagandha are gaining traction for their roles in nausea relief, glucose metabolism, and appetite balance. This trend is broadening the use of botanical ingredients and supporting multi-ingredient formulations that combine symptom relief with long-term wellness benefits.

E-Commerce and DTC Discovery Expansion

Online purchasing is transforming the US herbal medicine market, driving discovery and retention. iHerb reported USD 2.9 billion in net sales for fiscal 2025, with a significant rise in subscription-based models like AutoShip & Save.[3]AARP Public Policy Institute, “Insights on Integrative Medicine and Older Adults,” AARP, aarp.org Direct-to-consumer channels now dominate, offering brands better insights into customer behavior and enabling faster responses compared to traditional retail. This shift underscores the importance of digital capabilities as a core competitive advantage.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Limited clinical substantiation for many herbal products | -1.8% | National, strongest in healthcare-integrated markets in the Northeast and West | Long term (≥ 4 years) |

| Ingredient quality variability and adulteration | -1.4% | National, with elevated risk in online and specialty channels | Short term (≤ 2 years) |

| Import dependence and tariff volatility for non-native botanicals | -1.2% | National, strongest for brands sourcing from India and China | Short term (≤ 2 years) |

| Contamination and recall exposure in fast-growing categories | -0.7% | National, strongest in moringa, tejocote root, and exotic adaptogen categories | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Import Dependence and Tariff Volatility for Non-Native Botanicals

In 2026, the US herbal medicine market faces significant challenges due to its reliance on imports. Approximately 40% of U.S. dietary supplement herb imports come from India, while 80% of raw supplement ingredient volume is sourced from China, exposing brands to price volatility and supply disruptions. Tariff actions have further increased costs, with Chinese botanicals facing a 145% tariff burden and Indian botanicals like turmeric, ashwagandha, and Boswellia encountering a 50% to 55% burden. India produces 78% of the world’s turmeric and is the sole cultivator of Boswellia serrata, making quick substitutions difficult. Smaller companies must navigate between reduced margins and higher retail prices, emphasizing the need for strategic inventory planning and supplier diversification.

Limited Clinical Substantiation for Many Herbal Products

Limited clinical substantiation remains a challenge for the US herbal medicine market, particularly in pharmacy-linked and institutional channels requiring stringent evidence. Under DSHEA, manufacturers must ensure product safety and labeling accuracy but are not obligated to prove efficacy through randomized trials, leading to uneven evidence depth. Recent FDA discretion allows the DSHEA disclaimer to appear once per label, simplifying labeling but not addressing the evidence gap. Products lacking credible evidence or a clear user experience struggle to secure repeat purchases, leaving premium pricing concentrated among brands with high-quality formulations and robust substantiation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pharmaceutical-Grade Standards Anchor Premium Positioning

In 2025, Herbal Pharmaceuticals held 30.44% of the US herbal medicine market. Herbal Dietary Supplements are projected to grow at a 9.42% CAGR through 2031, driven by the strong institutional presence of standardized botanical formulations in pharmacy and hospital channels. These products benefit from a focus on consistency, documentation, and third-party verification, giving pharmaceutical-grade offerings an edge in compliance-driven settings.

Herbal Dietary Supplements are expanding rapidly due to their alignment with consumer self-education, adaptogen use, and direct-to-consumer distribution. The projected growth reflects increasing consumer interest in managing stress, sleep, metabolic health, and daily wellness outside traditional prescriptions. Additionally, Herbal Functional Food and Beverages are gaining traction as mainstream food companies seek plant-based positioning and easier integration into daily routines.

By Source: Roots & Rhizomes Lead and Accelerate

Roots & Rhizomes held a 42.79% share in 2025 and are the fastest-growing source segment, with a projected 9.05% CAGR through 2031. This growth is driven by the commercial and clinical importance of root-derived actives like ginseng saponins, turmeric curcuminoids, and ashwagandha withanolides. These ingredients are widely recognized by consumers and formulators and are adaptable across various delivery formats.

The segment is expected to maintain its leadership as advancements in formulation enhance the performance of these actives in commercial products. Improved absorption and targeted biological effects support higher-value positioning while retaining familiar ingredient names. Traceable domestic cultivation for select botanicals strengthens provenance narratives, although many high-demand inputs still rely on overseas sources.

By Form: Established Formats Hold Share While Sensory Formats Grow Fastest

Tablets & Capsules accounted for 45.73% of 2025 sales, while Teas & Infusions are projected to grow at a 10.99% CAGR through 2031. Tablets and capsules remain popular in pharmacies and structured supplement routines due to their convenience, portability, and precise dosing.

Teas and infusions are growing faster as they align with lifestyle-driven wellness and sensory self-care, particularly among younger consumers. Powders and granules are also gaining importance in superfood and greens blends, although confidence in moringa products was impacted by a 2025 Salmonella recall.

By Distribution Channel: Digital Commerce Compresses the Pharmacy Lead

Hospitals & Retail Pharmacies held a 38.61% share in 2025, while Online & E-commerce is projected to grow at a 9.97% CAGR through 2031. Pharmacy-linked channels benefit from consumer trust in regulated retail environments and third-party quality markers, which address concerns about quality and ingredient variability.

Online and e-commerce channels are growing rapidly due to their ability to streamline product discovery and provide brands with greater control over education, subscriptions, and consumer data. The acquisition of Vitacost by iHerb in January 2026 further strengthened this channel by consolidating two major online health retail platforms.

By Medicinal Plant Type: Turmeric Anchored, Ginseng Ascending

In 2025, Turmeric held a 19.68% market share, supported by strong consumer familiarity with curcumin and its anti-inflammatory benefits across supplements, beverages, and personal care. Turmeric’s leadership in specialized retail channels underscores its dominance in the US herbal medicine market.

Ginseng is projected to grow at a 10.26% CAGR through 2031, driven by expanding use cases in cognition, metabolic support, gut-brain modulation, and GLP-1 companion routines. Echinacea and garlic remain key for immune and cardiovascular support, while aloe vera holds a strong position in topical applications. St. John’s Wort and Milk Thistle have also seen notable growth, reflecting sustained interest in botanicals for brain and liver health.

Geography Analysis

California, Texas, New York, and Florida dominate the U.S. herbal medicine market, showcasing the largest state-level revenue concentrations. The West, led by California and the Pacific Northwest, serves as a key innovation hub where premium natural retailers and direct-to-consumer wellness brands test new botanical ingredients before broader launches. This aligns with the market's premiumization trend, as consumers in these regions are more receptive to specialty formats, plant-based products, and emerging herbal claims.

The Northeast, particularly New York and Massachusetts, has a strong presence of integrative health practitioners and academic medical institutions that prioritize evidence-based botanical applications. This drives demand for standardized products with robust documentation, making the region significant for premium, pharmaceutical-grade, and clinically positioned herbal formulations. Additionally, New York City's multicultural environment boosts demand for Traditional Chinese Medicine botanicals and Ayurvedic herbs, often distributed through ethnic specialty retail channels.

The Midwest remains commercially vital, supporting manufacturing, fulfillment, and value-driven distribution across the central U.S. Established supplement production in the region caters to mass retail and pharmacy networks, ensuring channel coverage and compliance reliability. While FDA cGMP regulations under 21 CFR Part 111 apply nationwide, enforcement is particularly critical in areas with concentrated supplement production and packaging activities.

Competitive Landscape

In 2025, the top five companies in the US herbal medicine market are projected to hold a combined 20% share, indicating a moderately fragmented landscape. This scenario paves the way for a diverse array of competitors, including regional brands, private-label manufacturers, practitioner-led firms, and direct-to-consumer specialists. These players compete through sourcing strategies, formulation focuses, and brand trust. While scale is significant, it is not the sole determinant of leadership, as consumers often prioritize products tailored to specific health objectives or those with a strong ingredient reputation.

Consolidation is becoming increasingly evident. Herbalife announced its acquisition of select assets from Bioniq for USD 55 million, with potential contingent payments reaching USD 95 million, signaling a stronger focus on biomarker-driven personalization in supplement delivery. Similarly, iHerb’s acquisition of Vitacost demonstrated how platform players are strengthening their control over digital retail channels in the US herbal medicine market.

Opportunities exist in clinical-grade herbal pharmaceuticals for pharmacies and institutions, precision adaptogen formulations for older adults managing multiple therapies, and GLP-1 companion products with clearer substantiation. Emerging companies are targeting these niches with focused formulations addressing specific conditions like perimenopause, cognitive longevity, or metabolic microbiome support. This approach aligns with evolving consumer preferences, as buyers increasingly seek issue-specific herbal products.

US Herbal Medicine Industry Leaders

Amway Corp.

Himalaya Wellness Company

Nature's Sunshine Products, Inc.

NOW Health Group, Inc.

Herbalife Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Herbalife Ltd. acquired select assets of UK-based Bioniq for USD 55 million, with up to USD 95 million in performance-based payments. The transaction was expected to close by Q2 2026.

- February 2026: iHerb Holdings, LLC finalized the acquisition of Vitacost.com from The Kroger Co. This move consolidated two major U.S. online health retail platforms.

- October 2025: Gaia Herbs launched Berberine & Milk Thistle, targeting metabolic and liver support using organic botanicals for the U.S. market.

- May 2025: Garden of Life, a Nestlé Health Science brand, introduced Dr. Formulated Hair Growth for Men. It was available in capsule and gummy formats priced at USD 44.99 and USD 29.99, respectively.

US Herbal Medicine Market Report Scope

As per the scope of the report, herbal medicine, also known as phytomedicine or herbalism, is the study and use of the medicinal properties of plants for therapeutic purposes, health enhancement, and disease prevention. It relies on extracts from roots, leaves, bark, seeds, and flowers.

The US herbal medicine market is segmented by product type, source (plant part), form, distribution channel, and medicinal plant type. By product type, the market includes herbal pharmaceuticals, herbal dietary supplements, herbal functional foods & beverages, and herbal cosmetics & personal care. By source (plant part), the market is segmented into leaves, roots & rhizomes, whole plant, fruits & seeds, and flowers & bark. By form, the market is categorized into tablets & capsules, powder & granules, liquid extracts & syrups, teas & infusions, and others (e.g., soft gels and gummies). By distribution channel, the market is segmented into hospitals & retail pharmacies, online/e-commerce, specialty stores, and hypermarkets & supermarkets. By medicinal plant type, the market includes aloe vera, echinacea, turmeric (Curcuma longa), ginseng, ginger, garlic, ginkgo biloba, and others (e.g., ashwagandha and cinnamon). The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Herbal Pharmaceuticals |

| Herbal Dietary Supplements |

| Herbal Functional Food & Beverages |

| Herbal Cosmetics & Personal Care |

| Leaves |

| Roots & Rhizomes |

| Whole Plant |

| Fruits & Seeds |

| Flowers & Bark |

| Tablets & Capsules |

| Powder & Granules |

| Liquid Extracts & Syrups |

| Teas & Infusions |

| Others (Soft gel and Gummies, among others) |

| Hospitals & Retail Pharmacies |

| Online/ E-Commerce |

| Specialty Stores |

| Hypermarkets & Supermarkets |

| Aloe Vera |

| Echinacea |

| Turmeric (Curcuma Longa) |

| Ginseng |

| Ginger |

| Garlic |

| Ginkgo Biloba |

| Others (Ashwagandha and Cinnamon, among others) |

| By Product Type | Herbal Pharmaceuticals |

| Herbal Dietary Supplements | |

| Herbal Functional Food & Beverages | |

| Herbal Cosmetics & Personal Care | |

| By Source (Plant Part) | Leaves |

| Roots & Rhizomes | |

| Whole Plant | |

| Fruits & Seeds | |

| Flowers & Bark | |

| By Form | Tablets & Capsules |

| Powder & Granules | |

| Liquid Extracts & Syrups | |

| Teas & Infusions | |

| Others (Soft gel and Gummies, among others) | |

| By Distribution Channel | Hospitals & Retail Pharmacies |

| Online/ E-Commerce | |

| Specialty Stores | |

| Hypermarkets & Supermarkets | |

| By Medicinal Plant Type | Aloe Vera |

| Echinacea | |

| Turmeric (Curcuma Longa) | |

| Ginseng | |

| Ginger | |

| Garlic | |

| Ginkgo Biloba | |

| Others (Ashwagandha and Cinnamon, among others) |

Key Questions Answered in the Report

What is the projected value of the US herbal medicine market by 2031?

The US herbal medicine market is projected to reach USD 98.49 billion by 2031 from USD 64.65 billion in 2026, growing at a CAGR of 8.79% over the forecast period.

Which product type leads sales in the U.S. herbal medicine space?

Herbal Pharmaceuticals led product type sales with a 30.44% share in 2025, supported by stronger institutional acceptance and standardized formulations.

Which form is growing fastest for herbal products in the United States?

Teas & Infusions are projected to grow the fastest at a 10.99% CAGR through 2031, even though Tablets & Capsules remained the largest form with 45.73% share in 2025.

Why are online channels gaining share so quickly?

Online and e-commerce channels are forecast to grow at a 9.97% CAGR because they combine convenience, wide assortment, subscription models, and stronger first-party consumer data.

Which medicinal plant currently leads sales and which one is growing fastest?

Turmeric led with 19.68% share in 2025, while Ginseng is expected to grow fastest at a 10.26% CAGR through 2031.

What are the biggest risks affecting herbal medicine suppliers in the U.S.?

The main risks are limited clinical substantiation, tariff exposure on imported botanicals, ingredient quality variability, and contamination or recall events in fast-growing categories.

Page last updated on: