Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

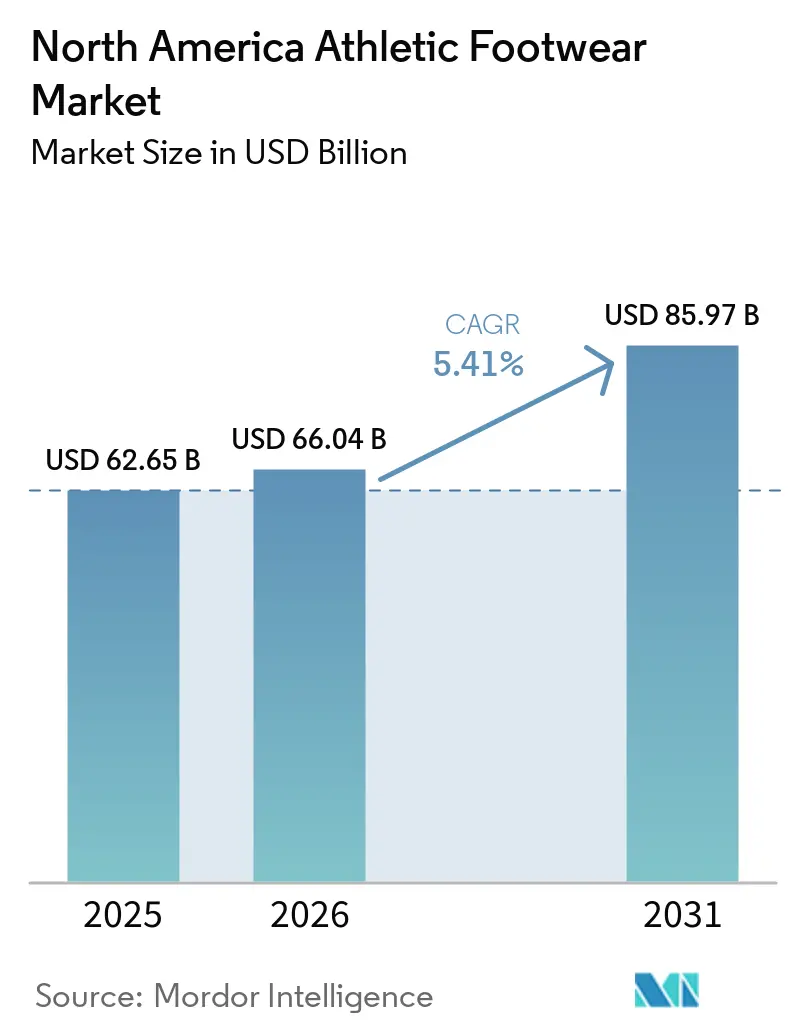

| Base Year Market Size (2025) | USD 62.65 Billion |

| Market Size (2026) | USD 66.04 Billion |

| Market Size (2031) | USD 85.97 Billion |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

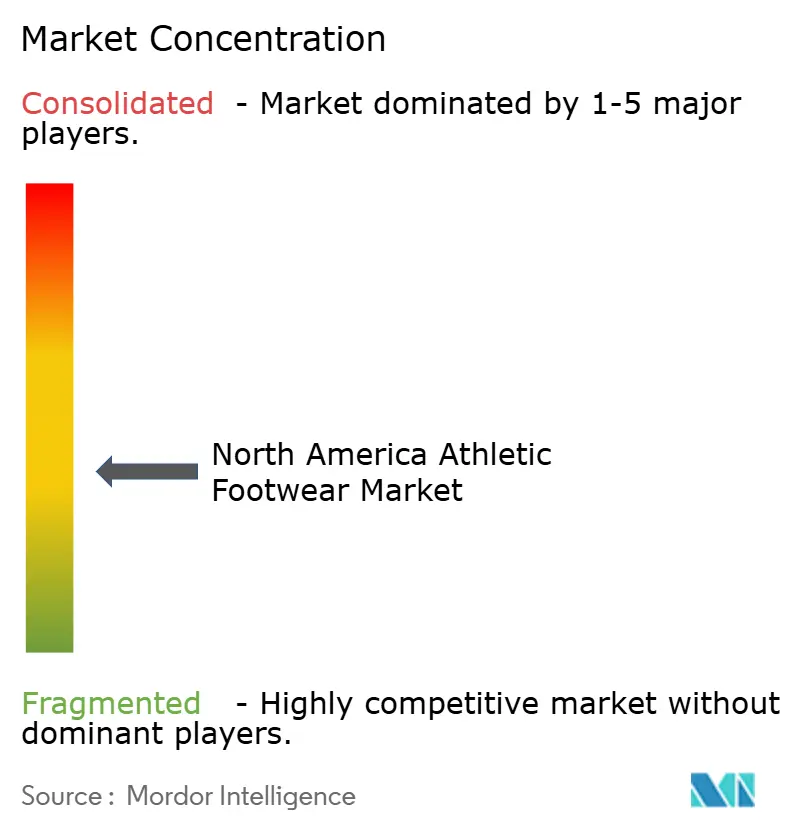

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Athletic Footwear Market Analysis by Mordor Intelligence

North America athletic footwear market size in 2026 is estimated at USD 66.04 billion, growing from 2025 value of USD 62.65 billion with 2031 projections showing USD 85.97 billion, growing at 5.41% CAGR over 2026-2031. This growth is driven by a combination of established consumer preferences and emerging trends, such as the popularity of athleisure, the use of eco-friendly materials, and innovative designs that seamlessly blend sports functionality with lifestyle appeal. Increasing female participation in both organized and recreational sports, the expansion of youth fitness programs, and the introduction of products that combine performance with fashion are significantly broadening the market's consumer base. The United States remains the dominant market in the region, while Mexico is emerging as a key area for growth. Sports shoes continue to lead in popularity, with running shoes gaining traction as a fast-growing segment. Although men represent the largest consumer group, there is a noticeable rise in demand among children, indicating a generational shift in preferences.

Key Report Takeaways

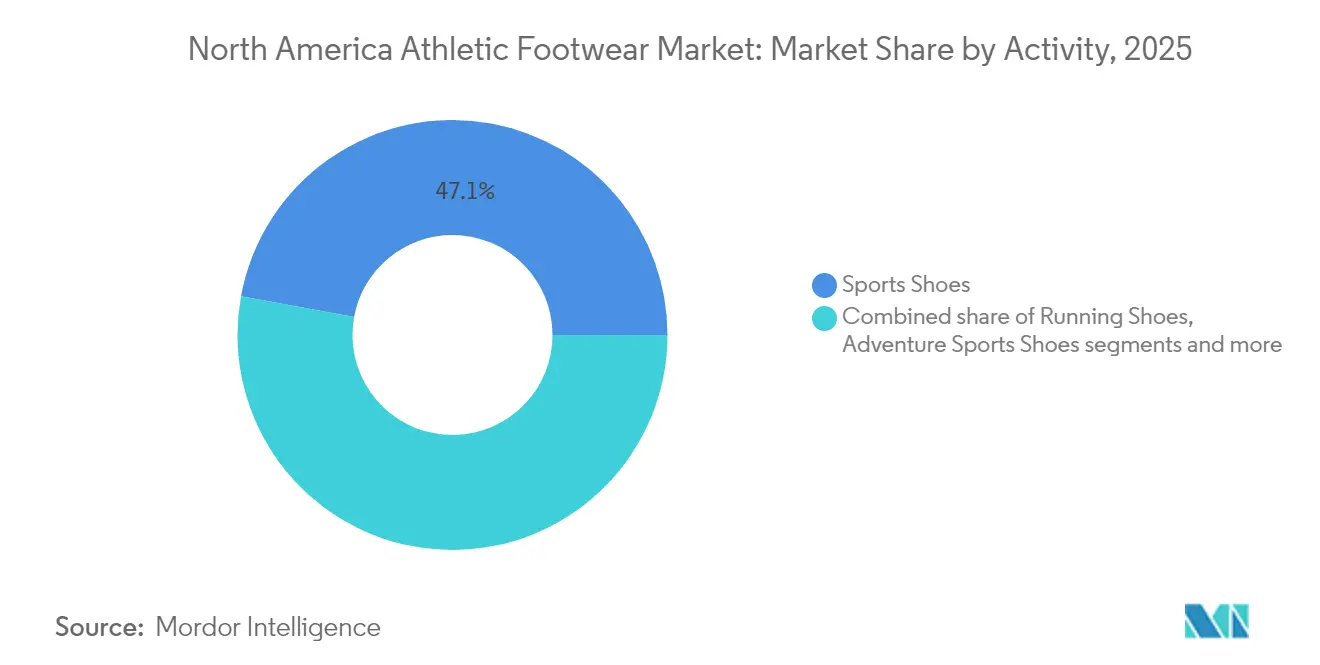

- By activity, sports shoes held 47.12% of the North America athletic footwear market share in 2025, while running shoes are forecast to grow at a 6.05% CAGR to 2031.

- By product type, shoes dominated with an 85.10% revenue share in 2025; boots are projected to expand at a 5.78% CAGR through 2031.

- By end user, men accounted for 63.65% of demand in 2025, whereas the kids/children segment is set to record a 6.18% CAGR up to 2031.

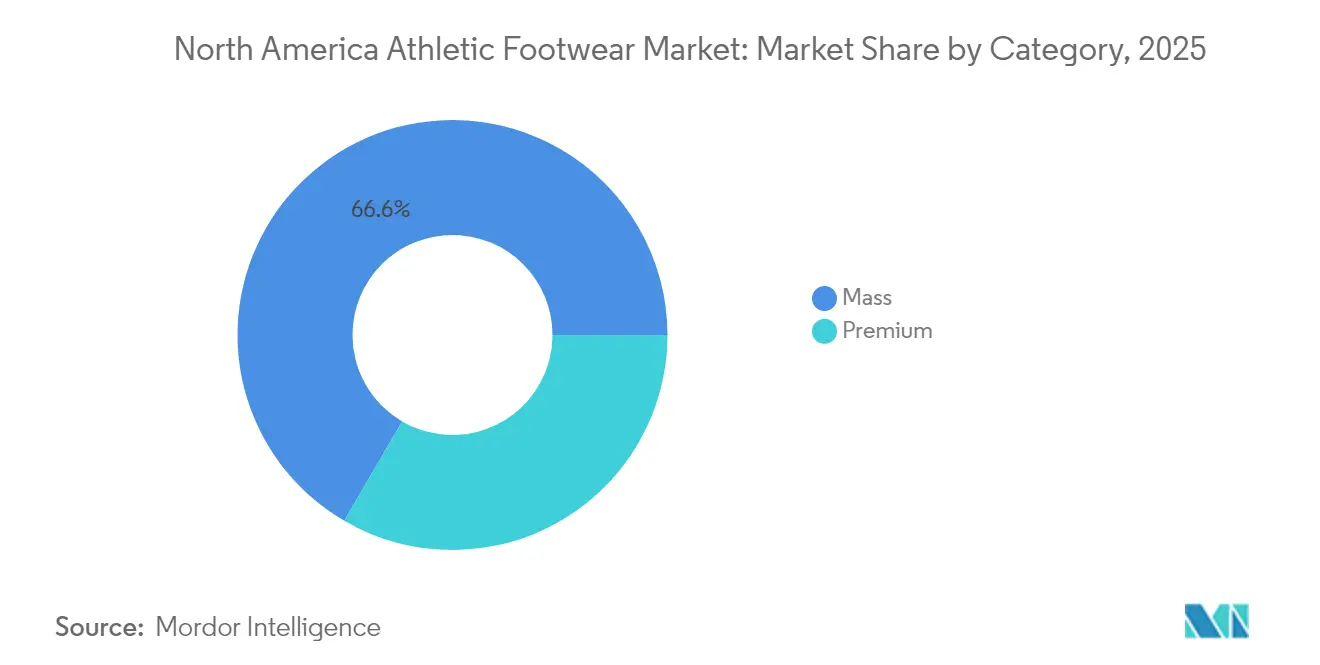

- By category, mass market represented 66.60% of sales in 2025; the premium tier is poised for a 6.52% CAGR to 2031.

- By distribution channel, sports and athletic goods stores led with 45.70% of revenue in 2025, while online retail stores are tracking a 6.72% CAGR through 2031.

- By geography, the United States captured 82.30% of 2025 revenue, while Mexico is on track for the fastest 7.09% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Athletic Footwear Market Trends and Insights

Drivers Impact Table*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Significant growth in women sports participation rate | +0.8% | United States and Canada, with spillover to Mexico | Medium term (2-4 years) |

| Aggressive marketing by reputed brands | +1.2% | North America-wide, concentrated in urban centers | Short term (≤ 2 years) |

| Influence of social media platforms and celebrity endorsements | +0.9% | North American expanding to Canada | Short term (≤ 2 years) |

| Favourable government initiatives to boost sports culture | +0.7% | United States primarily, expanding to Canada | Long term (≥ 4 years) |

| Increasing athleisure trend | +1.1% | North America expanding to Mexico | Medium term (2-4 years) |

| Sustainability and ethical consumption | +0.6% | North America expanding to Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Significant growth in women sports participation rate

The increasing participation of women in sports is playing a significant role in driving the North American athletic footwear market. As of 2024, nearly half of all females, around 49%, are actively involved in sports, according to Project Play [1]Source: Project Play, "Participation Trends," projectplay.org. Legislative efforts, such as discussions around the Protection of Women and Girls in Sports Act, have brought female athletics into the spotlight, encouraging brands to focus on creating women-specific products. For instance, Under Armour has expanded its women’s product range with launches like the UA Flow Synchronicity, designed specifically to cater to the anatomy of the female foot. The Women's Sports Foundation in 2024 reported that 67% of women credit sports participation for their leadership development, which is expected to drive higher women's participation in sports in the future [2]Source: Women's Sports Foundation, "The Generational Impact of Sports on Women’s Leadership," womenssportsfoundation.org. The government conducts various initiatives to encourage more women to get more active, more often, by promoting participation in physical activities. For example, the Government of Canada is committed to building and maintaining an inclusive Canadian sport system and providing opportunities for women and girls in all aspects of the sport, including coaching.

Aggressive marketing by reputed brands

Leading brands in North America are driving the growth of the athletic footwear market through impactful and relatable marketing strategies. Nike, for instance, has gained significant attention with campaigns like “You Can’t Stop Us” and “Dream Crazier,” which feature prominent American athletes such as Serena Williams and Colin Kaepernick. These campaigns not only promote products but also inspire consumers by delivering powerful messages of empowerment and perseverance. Similarly, Under Armour focuses on connecting with U.S. audiences through initiatives like its partnership with Stephen Curry and the launch of the Curry Flow 10. By combining athlete-driven storytelling with limited-edition releases, the brand creates excitement and exclusivity around its products. Adidas also engages North American consumers through collaborations, such as its partnership with Bad Bunny and basketball-themed product launches. These efforts are further amplified by significant investments in digital marketing and exclusive access platforms like Nike’s SNKRS app and Adidas’ Confirmed app. This comprehensive approach makes it challenging for smaller brands to compete with the extensive reach, visibility, and cultural influence of these major players.

Favourable government initiatives to boost sports culture

Government investments in sports infrastructure and participation programs are establishing sustainable demand for athletic footwear across North America, particularly in underserved communities and youth markets. The U.S. Department of Health and Human Services' National Youth Sports Strategy of 2025 aims to reduce barriers like costs and access limitations. The strategy recognizes youth sports as a billion-dollar industry driven by parental spending on sports programs. Sports participation rates have increased due to enhanced physical education in schools and government-sponsored after-school programs, creating opportunities for athletic footwear manufacturers in the educational sector. The Canadian government allocated USD 24.2 million to Indigenous sport programs supporting First Nations, Inuit, and Métis communities, as reported in February 2025 [3]Source: Canada CA, "Government of Canada investing USD 24.2 million in Indigenous sport programs to empower First Nations, Inuit and Métis communities, " canada.ca. The funding supports 119 Indigenous-led projects aimed at increasing access to sport and physical activities across communities nationwide. Such government initiatives in the region are expected to drive the demand for athletic footwear in the North American market.

Influence of social media platforms and celebrity endorsements

Social media and celebrity endorsements are playing a major role in driving growth in the North American athletic footwear market. Platforms like Instagram, TikTok, and X (formerly Twitter) have become powerful tools for brands to connect with consumers and create buzz around their products. For example, the Nike-Tiger Woods collaboration has gained immense popularity, generating over 36,500 average monthly searches in the United States, as reported by Licensing International in September 2024. This highlights how celebrity partnerships can significantly boost brand visibility and consumer interest. In addition to traditional celebrity endorsements, brands are increasingly leveraging social media strategies to engage with their audience. Micro-influencers and user-generated content are becoming key components of marketing campaigns, allowing brands to reach niche audiences in a more authentic and relatable way. Through combining high-profile collaborations with digital engagement strategies, athletic footwear companies are not only enhancing their market presence but also building stronger connections with consumers.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Counterfeit products affecting brand reputation | -0.4% | North America-wide, concentrated in border regions | Short term (≤ 2 years) |

| High price points of premium footwear | -0.3% | United States and Canada, limited Mexico impact | Medium term (2-4 years) |

| Regulatory and import barriers | -0.5% | United States primarily, Canada secondary | Medium term (2-4 years) |

| Slow pace of penetration in rural and low-income areas | -0.2% | Rural United States, Mexico, select Canadian regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Counterfeit products affecting brand reputation

The rise of counterfeit athletic footwear is becoming a serious issue for brands and consumers in North America. Fake sneakers are flooding the market, with the U.S. being a major target. For instance, U.S. Customs reported seizing nearly USD 100 million worth of counterfeit shoes in just one year, according to the Michelson Institute for Intellectual Property [4]Source: Michelson Institute for Intellectual Property, "Sneakerheads and the Law: Tackling Counterfeit Sneakers Through IP," michelsonip.com. This growing problem not only impacts legitimate sales but also confuses consumers who may unknowingly purchase fake products. To combat this, leading brands are stepping up their efforts by introducing advanced authentication technologies, such as QR codes and blockchain-based tracking systems, to verify product authenticity. They are also intensifying legal actions against counterfeiters and launching awareness campaigns to educate consumers on how to identify genuine products. Despite these measures, counterfeit footwear remains a persistent issue, especially with knockoffs being sold on third-party e-commerce platforms. This ongoing challenge continues to harm brand reputation and creates difficulties for both consumers and legitimate businesses in the market.

High price points of premium footwear

The high cost of premium athletic footwear poses a significant barrier to wider adoption in the North American market. For example, products like the Adidas Adizero Adios Pro Evo 2, priced at USD 500, showcase advanced features and cutting-edge technology but remain unaffordable for many consumers. Economic pressures, including rising inflation and stagnant wages, particularly impact rural and lower-income communities, further limiting access to these high-end products. While the premium segment continues to thrive among affluent urban buyers and professional athletes, the average consumer often finds these price points prohibitive. This affordability gap not only restricts market growth but also opens the door for counterfeit products to gain traction. At the same time, the gap opens up opportunities for mid-tier and challenger brands such as Skechers, Brooks, or Under Armour’s mid-range lines to capture price-sensitive consumers with performance-oriented yet more affordable alternatives. These brands often sacrifice some cutting-edge technology in favor of broader accessibility, positioning themselves as value-for-money options.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Activity: Running Shoes Sustain Technology Race

In 2025, sports shoes led the North America athletic footwear market, accounting for 47.12% of the total revenue. Their popularity is driven by their versatility, making them suitable for activities like team sports, gym workouts, and casual wear. Running shoes, while holding a smaller market share, have gained significant attention due to their association with marathon culture and advancements in performance-enhancing technologies. Niche categories such as Adventure Sports Shoes and hybrid lifestyle designs have found their place in the market, catering to consumers with specific needs and preferences, thereby contributing to the market's diversity.

Running shoes are projected to grow at the fastest pace, with a compound annual growth rate (CAGR) of 6.05% expected through 2031. This growth is attributed to continuous innovations, including lighter foams, carbon plates, and 3D-printed uppers, which improve performance and attract both professional athletes and fitness enthusiasts. Meanwhile, sports shoes are anticipated to maintain steady growth, supported by the ongoing athleisure trend that combines athletic functionality with casual style. Adventure Sports Shoes are also expected to see moderate growth as outdoor recreational activities continue to rise in popularity, appealing to consumers seeking active and adventurous lifestyles.

By Product Type: Shoes Remain Core, Boots Gain Traction

In 2025, traditional shoes dominated the market, accounting for 85.10% of total sales. Their widespread appeal lies in their reliability and versatility, making them a preferred choice for everyday activities such as school routines, casual outings, and sports like basketball or tennis. These shoes have become a staple for consumers who prioritize comfort and functionality. Although boots represented a smaller segment, they gained popularity in specific categories like winter wear and hiking, catering to consumers seeking durable and weather-resistant options. Meanwhile, sandals and other open footwear types, though holding a smaller market share, have established a loyal customer base, particularly for post-sport recovery and use in warmer climates where breathability and ease of wear are crucial.

Boots are projected to experience the fastest growth, with a compound annual growth rate (CAGR) of 5.78% expected through 2031. This growth is driven by the rising demand for multifunctional hiking footwear, innovative recovery-focused designs such as Nike’s collaboration with Hyperice, and the use of climate-resilient materials that address changing weather conditions. At the same time, Traditional Shoes are anticipated to grow steadily as brands continue to focus on enhancing comfort, durability, and affordability. These improvements ensure that Traditional Shoes remain a popular choice for a wide range of consumers, offering a balance of performance, practicality, and everyday usability.

By End User: Youth Demand Accelerates

In 2025, men accounted for 63.65% of the demand for athletic footwear, driven by strong discretionary spending and their deep connection to mainstream sports leagues. This segment continues to dominate as men frequently purchase footwear for both performance and casual use, supported by a wide range of options tailored to their needs. Women followed with a growing market share, fueled by an increasing variety of designs, color options, and improved fits that cater specifically to their preferences. Meanwhile, the Kids/Children segment, though smaller, remains significant due to the frequent need for replacements as children outgrow their shoes quickly, making it a dynamic and fast-moving category.

Looking ahead, the kids/children segment is expected to lead market growth, with a projected annual growth rate of 6.18%. This expansion is supported by initiatives like youth sports campaigns, such as Project Play 63×30, which encourage active lifestyles among children. The women’s segment is also set to grow at a high-single-digit rate, driven by advancements in gender-specific technologies and inclusive marketing strategies that resonate with a broader audience. Meanwhile, the men’s segment is anticipated to maintain steady mid-single-digit growth, supported by regular replacement cycles and the adoption of new technologies that enhance performance and comfort.

By Category: Premium Tier Moves Up-Market

Mass-market-priced footwear dominated the market in 2025, contributing 66.60% of the total revenue. This segment's success stems from its affordability, making it accessible to a wide range of consumers across different income levels. These products cater to everyday needs, offering functional and budget-friendly options for casual wear, sports, and other activities. On the other hand, premium footwear, while representing a smaller share, has gained traction among performance-driven and fashion-conscious consumers. These products often feature advanced technologies, sustainable materials, and exclusive designs, appealing to those willing to invest in quality and innovation.

Looking ahead, the premium footwear segment is expected to grow at a compound annual growth rate (CAGR) of 6.52% through 2031. This growth is driven by the increasing demand for high-performance features, such as energy-efficient midsoles and eco-friendly designs, which justify their higher price points. Meanwhile, the mass-market segment is projected to grow at a more moderate pace as consumers balance economic challenges with a growing focus on health and fitness. Despite slower growth, the mass-market segment will continue to play a crucial role in meeting the needs of price-sensitive buyers while maintaining its position as a key revenue driver in the market.

By Distribution Channel: Digital Share Rises

Sports and athletic goods stores dominated the market in 2025, contributing 45.70% of the total revenue. These stores attract customers by offering personalized services such as gait analysis and expert advice, which help shoppers find the right products for their needs. The immediate availability of products and the ability to physically try them on make these stores a preferred choice for many consumers. Their wide product range also ensures they cater to various customer preferences, solidifying their position as a key distribution channel. However, the growing popularity of online shopping is gradually challenging their dominance as consumers increasingly prioritize convenience and competitive pricing.

Online retail stores are projected to grow at a strong 6.72% CAGR through 2031, driven by advancements in technology like AI-powered fit prediction tools and hassle-free return policies. The direct-to-consumer strategies adopted by brands have further accelerated the growth of this channel, allowing them to connect directly with their customers. While online platforms continue to gain momentum, traditional brick-and-mortar stores are adapting by offering omnichannel services, such as in-store pickups and online order assistance, to stay competitive. Supermarkets and hypermarkets also play a role in the market by catering to convenience-focused shoppers, bundling footwear with other sporting goods to maintain steady growth in this segment.

Geography Analysis

The United States contributes a significant 82.30% of the regional revenue in 2025, driven by its strong sports culture, national leagues, and an extensive retail network. Government initiatives, such as updated physical activity guidelines and infrastructure grants, further boost the demand for athletic footwear. However, economic uncertainties and rising competition from emerging brands push established players to innovate faster and adopt more competitive pricing strategies to maintain their market position.

Canada shares many similarities with the U.S. in terms of consumer demand, but also has unique seasonal requirements that drive interest in insulated and all-weather footwear. The country’s customs regulations for sports footwear influence import duties and product classifications, which directly impact pricing strategies. Outdoor recreation and winter sports play a significant role in sustaining demand for trail and snow-ready footwear, ensuring a balanced product mix that caters to the diverse needs of Canadian consumers in the North America athletic footwear market.

Mexico, projected to grow at a 7.09% CAGR, benefits from a young and urbanizing population with increasing disposable income. While price sensitivity and limited rural infrastructure pose challenges, brands are successfully reaching the expanding middle class through affordable entry-level product lines and targeted social media campaigns. This approach helps companies tap into Mexico’s growing market potential, making it an important contributor to the overall regional growth.

Competitive Landscape

The competitive landscape in the North American athletic footwear market is moderately fragmented. The market is divided between large-scale players and agile disruptors. Recent mergers and acquisitions reflect a shift in retailer strategies. For instance, Dick’s Sporting Goods announced its acquisition of Foot Locker for USD 2.4 billion, aiming to enhance its presence in sneaker culture and expand internationally. Similarly, the US-based sneaker company Sketchers accepted a USD 9.4 billion buyout offer from 3G Capital, indicating private equity's confidence in the long-term growth potential of the market. These developments highlight how both retailers and brands are realigning to stay competitive in a dynamic market.

Innovation in product design and technology continues to be a key driver in the market. Adidas recently launched a 3D-printed Climacool sneaker, setting new standards for manufacturing flexibility and breathability. Nike collaborated with Hyperice to introduce heated, air-compression recovery boots, blending advanced performance technology with user comfort. On has gained traction with its spray-on uppers and robust sales growth, showcasing how emerging brands are leveraging unique materials and designs to capture consumer attention. These advancements underline the importance of staying ahead in product innovation to maintain market relevance.

Sustainability is no longer just a marketing strategy but a critical factor for competitiveness. PUMA has committed to achieving 90% recycled or certified materials by 2024, while ASICS has introduced circular-design models like the recyclable Nimbus Mirai. These initiatives reflect the growing consumer demand for environmentally friendly products. Brands that can scale such eco-friendly innovations without significantly increasing costs are likely to secure a loyal customer base among environmentally conscious buyers. The focus on sustainability is reshaping the market, pushing companies to adopt greener practices while maintaining affordability and quality.

North America Athletic Footwear Industry Leaders

-

Adidas AG

-

Nike, Inc.

-

Puma SE

-

Under Armour, Inc.

-

VF Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The United States-based sneaker company Sketchers has agreed to be taken private by the investment firm 3G Capital in a deal worth 9.42 billion US dollars.

- May 2025: Dick’s announced its USD 2.4 billion acquisition of Foot Locker (including Kids Foot Locker, Champs Sports, WSS, and atmos)

- April 2024: Nike launched a lineup of athletic footwear and apparel. This includes the debut of a new Air Zoom unit in the Pegasus Premium running shoe, offering enhanced energy return for runners.

- December 2024: Under Armour launched two new shoes at Sneaker Con through Stephen Curry, the Golden State Warriors star. Stephen Curry presented De'Aaron Fox's debut signature shoe. The launch event marked De'Aaron Fox's first collaboration with Under Armour.

North America Athletic Footwear Market Report Scope

Athletic footwear is primarily designed to be worn during sports or other forms of physical exercise to provide proper comfort and grip to the end-user. The North America athletic footwear market (henceforth referred to as the market studied) is segmented by activity, product type, end user, category, distribution channel, and geography. By activity, the market is segmented into running shoes, sports shoes, adventure sports shoes and other product types. By product type, the market is segmented into shoes and boots. By end user, the market is segmented into men, women and kids/children. By category, into premium and mass. By distribution channel, the market is segmented into sports and athletic goods stores, supermarkets/hypermarkets, online retail stores and other distribution channels. It provides an analysis of emerging and established economies across North America, comprising the United States, Canada, Mexico, and the Rest of North America For each segment, the market sizing and forecasts have been done on the basis of value (USD million).

By Activity

| Running Shoes |

| Sports Shoes |

| Adventure Sports Shoes |

| OtherProduct Types |

By Product Type

| Shoes |

| Boots |

By End User

| Men |

| Women |

| Kids/Children |

By Category

| Premium |

| Mass |

By Distribution Channel

| Sports and Athletic Goods Stores |

| Supermarkets/Hypermarkets |

| Online Retaile Stores |

| Other Distribution Channels |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Activity | Running Shoes |

| Sports Shoes | |

| Adventure Sports Shoes | |

| OtherProduct Types | |

| By Product Type | Shoes |

| Boots | |

| By End User | Men |

| Women | |

| Kids/Children | |

| By Category | Premium |

| Mass | |

| By Distribution Channel | Sports and Athletic Goods Stores |

| Supermarkets/Hypermarkets | |

| Online Retaile Stores | |

| Other Distribution Channels | |

| By Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

What is the current value of the North America athletic footwear market?

The market is valued at USD 66.04 billion in 2026 and is projected to reach USD 85.97 billion by 2031 at a 5.41% CAGR.

Which activity segment is expanding the fastest?

Running shoes show the strongest momentum, advancing at a 6.05% CAGR through 2031.

How significant is online retail for athletic footwear sales?

Online channels are the fastest-growing distribution avenue, rising at a 6.72% CAGR as brands boost direct-to-consumer platforms.

Which demographic offers the highest growth potential?

Kids/Children’s footwear demand is set to climb at a 6.18% CAGR, supported by youth sports programs and frequent replacement cycles.

Page last updated on: