Golf Equipment and Apparel Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 20.87 Billion |

| Market Size (2031) | USD 26.71 Billion |

| Growth Rate (2026 - 2031) | 5.06% CAGR |

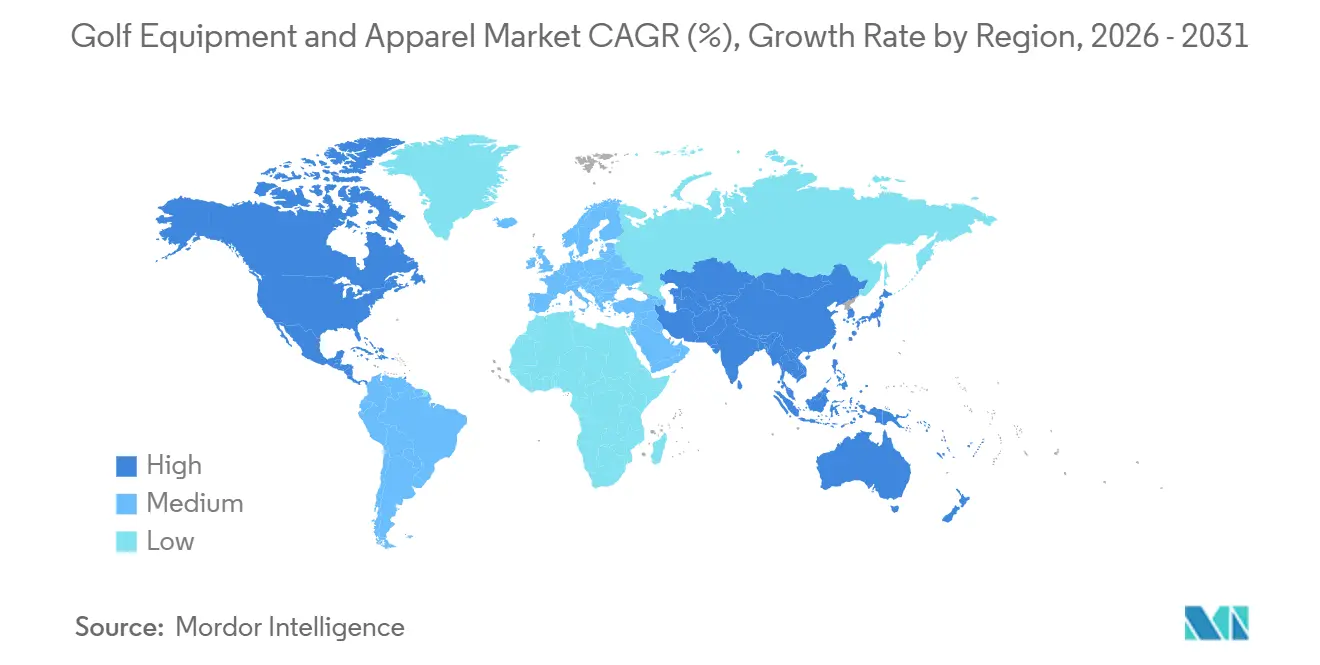

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Golf Equipment and Apparel Market Analysis by Mordor Intelligence

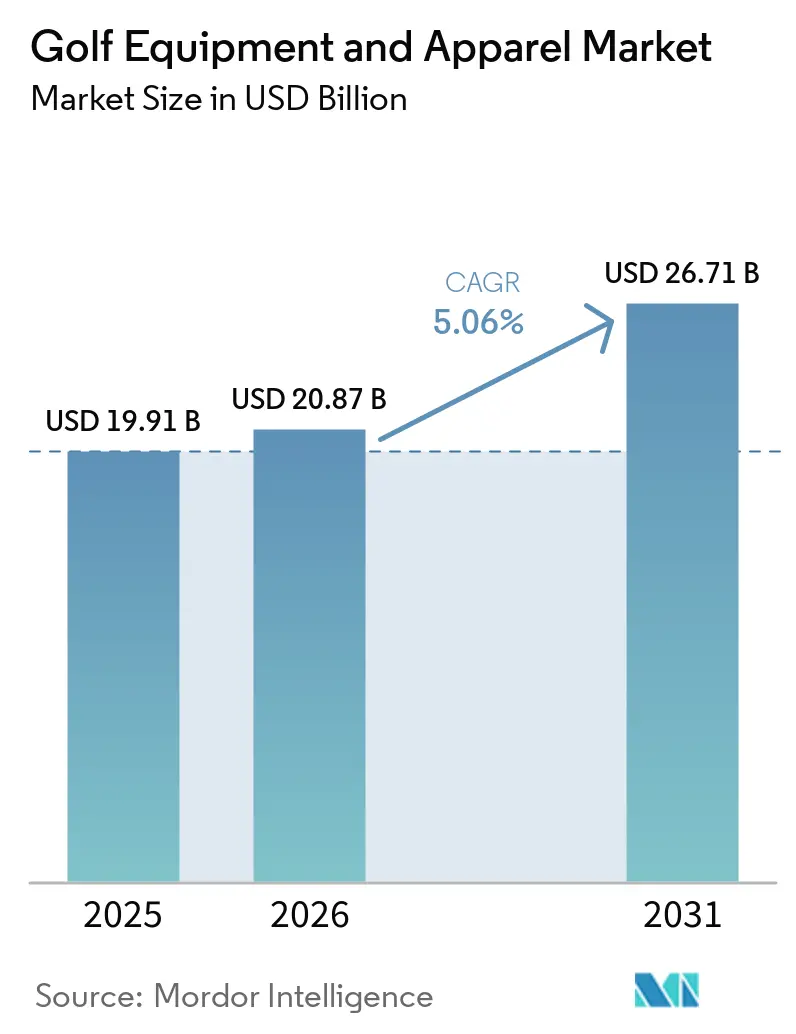

The golf equipment and apparel market size is expected to grow from USD 19.91 billion in 2025 to USD 20.87 billion in 2026 and is forecast to reach USD 26.71 billion by 2031 at 5.06% CAGR over 2026-2031. The growth is supported by increasing participation in golf across both traditional and emerging markets. Rising interest among younger players, women, and recreational golfers is expanding the consumer base for clubs, balls, footwear, and performance apparel. Manufacturers are continuously introducing technologically advanced equipment and premium apparel designed to enhance player performance and comfort. The growing popularity of golf tourism, driving ranges, and golf entertainment venues is further stimulating demand. Additionally, expanding e-commerce penetration and customization options are improving product accessibility and consumer engagement, contributing to sustained market growth over the forecast period.

Key Report Takeaways

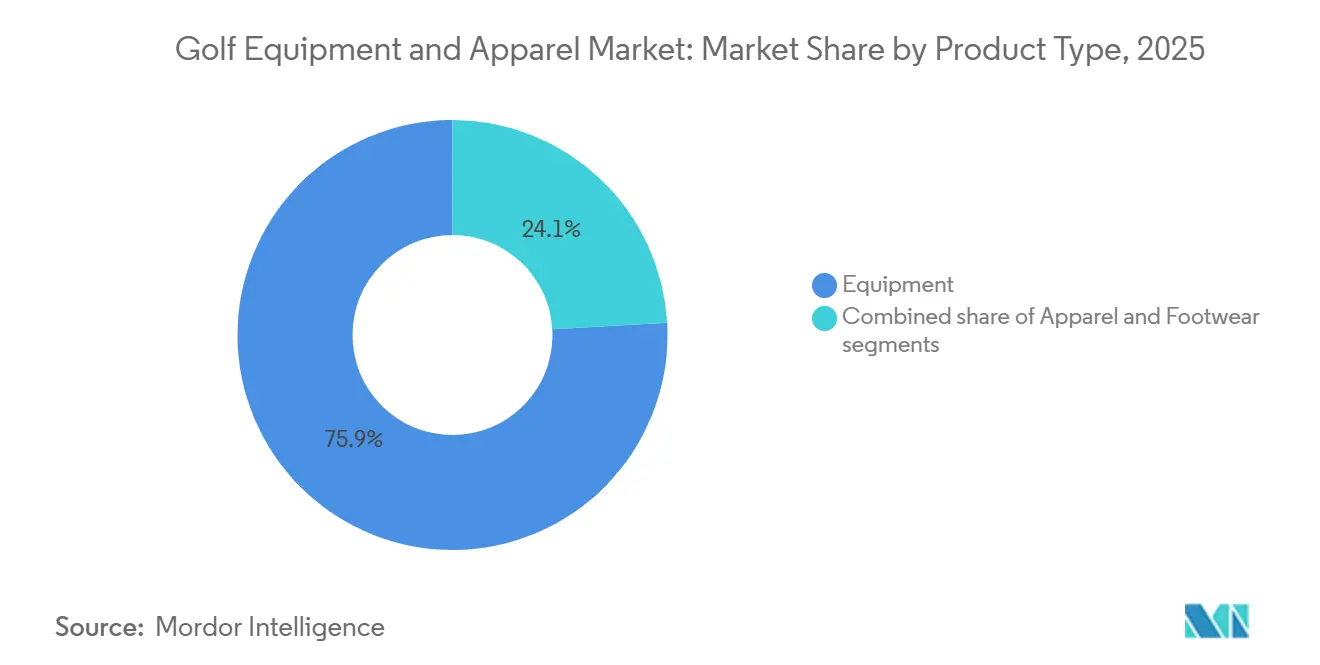

- By product type, equipment held 75.91% share in 2025, while apparel is projected to expand at a 5.74% CAGR through 2031.

- By category, mass held 66.75% share in 2025, while premium is projected to grow at a 5.46% CAGR through 2031.

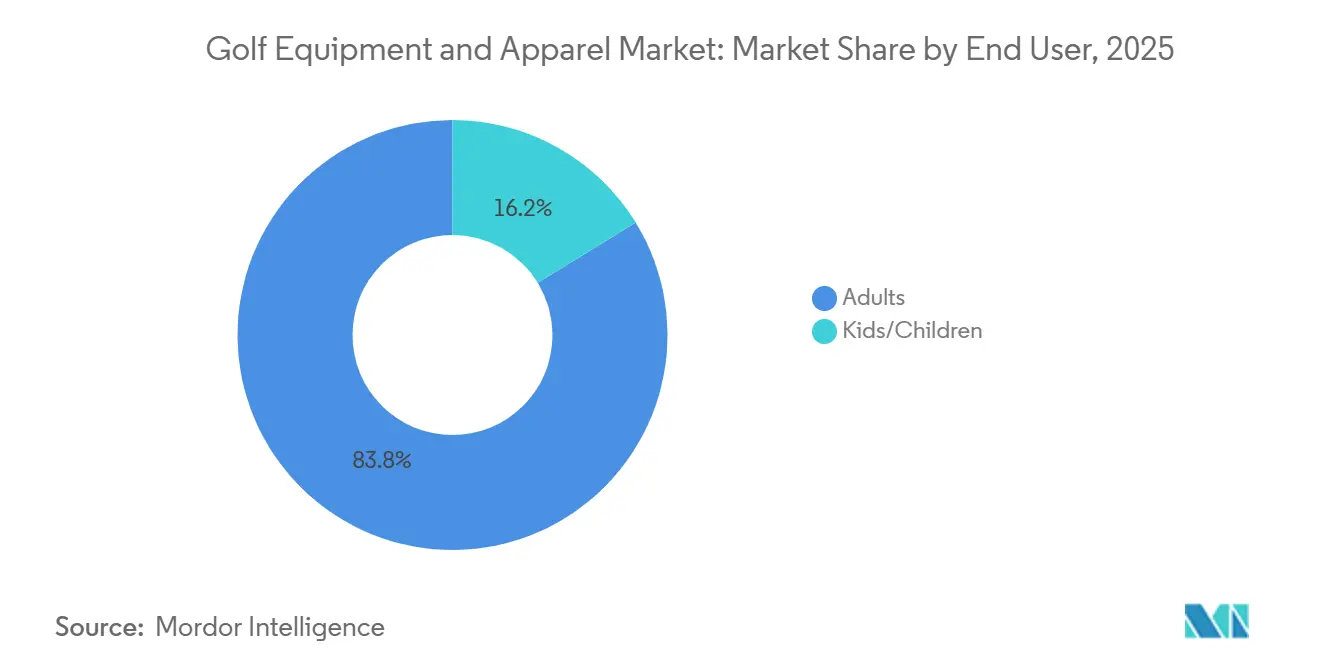

- By end user, adults held 83.76% share in 2025, while kids and children are forecast to grow at a 5.58% CAGR through 2031.

- By distribution channel, offline retail stores held 71.25% share in 2025, while online retail stores are projected to grow at a 6.21% CAGR through 2031.

- By geography, North America held 49.01% of the golf equipment and apparel market share in 2025, while Asia-Pacific is forecast to expand at a 5.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Golf Equipment and Apparel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing participation in golf among younger age groups and women | +0.8% | Global, with outsized gains in North America, Europe, and East Asia | Short term (≤ 2 years) |

| Expansion of public golf courses and golf entertainment venues | +0.7% | North America primary, Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Rising demand for premium and technologically advanced golf clubs | +0.9% | Global core markets, including the United States, United Kingdom, Japan, and South Korea | Short term (≤ 2 years) |

| Increasing popularity of golf tourism and destination golf travel | +0.6% | North America, Europe, and Southeast Asia resort hubs | Medium term (2-4 years) |

| Growth of professional golf tournaments and media coverage | +0.5% | Global, with peak impact in North America and Europe | Short term (≤ 2 years) |

| Adoption of performance-enhancing golf apparel with moisture-wicking features | +0.6% | Global, with Asia-Pacific and North America leading uptake | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing participation in golf among younger age groups and women

Increased participation in golf among younger age groups and women is creating sustained demand for golf equipment and apparel worldwide. According to the National Golf Foundation, the number of on-course female golfers in the United States increased by 45% between 2020 and 2025, representing a net gain of 2.5 million participants and reaching a record 8.1 million golfers[1]Source: National Golf Foundation, “The Record Rise of Female Golf”, ngf.org. This expanding player base is driving purchases of golf clubs, balls, footwear, apparel, and accessories tailored to diverse consumer segments. At the same time, younger golfers are increasingly entering the sport through golf entertainment venues, academies, and beginner programs, supporting long-term market growth. According to the United States Golf Association, the U.S. handicap base reached 3.68 million golfers in 2025, with a record 82 million scores posted, indicating deeper engagement among active players[2]Source: United States Golf Association, “Golf Participation Boomed in 2025; More Than 82 Million Rounds Posted Domestically”, usga.org. Higher participation and increased playing frequency encourage golfers to upgrade equipment regularly and invest in performance-oriented apparel, contributing to continued market expansion.

Expansion of public golf courses and golf entertainment venues

The expansion of public golf courses and golf entertainment venues is increasing accessibility to the sport and supporting demand for golf equipment and apparel. Off-course golf formats are attracting new participants by providing a more casual and approachable introduction to the game. In the United States, off-course golf participation reached 37.9 million players in 2025, creating a substantial pool of consumers familiar with golf who represent potential future buyers of clubs, balls, footwear, and apparel. These venues encourage regular engagement through practice sessions, social events, and beginner-friendly experiences, helping convert casual participants into active golfers. Investments in golf infrastructure are also accelerating globally; for example, in March 2026, AKCEL Holding and XRange Golf Entertainment announced an AED 1 billion (USD 272 million) investment to develop new golf entertainment venues across the UAE. Such facilities simplify product trials, club fitting experiences, and equipment demonstrations, making first-time purchases more accessible and contributing to growth in the golf equipment and apparel market.

Rising demand for premium and technologically advanced golf clubs

Rising demand for premium and technologically advanced golf clubs is contributing significantly to growth in the golf equipment and apparel market. Golfers are increasingly seeking equipment that offers measurable improvements in distance, accuracy, forgiveness, and overall performance, encouraging manufacturers to invest heavily in innovation. Advanced club designs incorporating lightweight materials, aerodynamic structures, and data-driven fitting technologies are attracting both professional and recreational players. The growing willingness of consumers to spend on high-performance products is also supporting the premiumization trend across the market. Reflecting this shift, TaylorMade introduced the Qi4D driver family in January 2026, featuring Finite Element Analysis face engineering, a new shaft system, and Launch Monitor-enabled fitting markers designed to optimize fitting outcomes. Such innovations strengthen consumer confidence in performance claims and encourage equipment upgrades.

Increasing popularity of golf tourism and destination golf travel

The increasing popularity of golf tourism and destination golf travel is creating additional demand for golf equipment and apparel worldwide. Golf travelers typically participate in multiple rounds during trips, increasing the need for high-quality clubs, apparel, footwear, and accessories. The trend is also encouraging golfers to invest in premium products that enhance performance and comfort across different playing conditions. Between 2022 and 2025, more than 12 million Americans traveled for golf annually, representing a 49% increase compared with comparable pre-pandemic levels. These trips generated over USD 30 billion in tourism-related spending, highlighting the growing economic significance of golf travel[3]Source: National Golf Foundation, “Travel’s Expanding Golf Economy Impact”, ngf.org. As golfers visit renowned courses and resort destinations, they are more likely to purchase new equipment and branded apparel before and during their trips. The continued expansion of golf tourism is therefore supporting equipment upgrades, apparel purchases, and overall market growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of golf equipment, apparel, and course memberships | -0.5% | Global, most severe in South Asia, Africa, and South America | Long term (≥ 4 years) |

| Limited accessibility of golf facilities in developing regions | -0.4% | Africa, South and Southeast Asia, and South America | Long term (≥ 4 years) |

| Competition from alternative sports and fitness activities | -0.4% | Global, particularly among 18-34-year-old urban demographics | Medium term (2-4 years) |

| Seasonal dependence affecting golf participation and equipment sales | -0.3% | North America, Northern Europe, and Northern Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High cost of golf equipment, apparel, and course memberships

The high cost of golf equipment, apparel, and course memberships continues to limit broader participation in the sport and poses a challenge to market expansion. Premium golf clubs, specialized balls, performance apparel, and footwear often require substantial upfront spending, making the sport less accessible to price-sensitive consumers. In addition to equipment expenses, golfers frequently incur costs related to club memberships, green fees, coaching, and practice facilities. These financial requirements can discourage new entrants from taking up the sport and may reduce the frequency of participation among existing players. The impact is particularly evident in emerging markets, where disposable incomes are comparatively lower and golf is often perceived as a premium leisure activity. Although manufacturers offer products across various price ranges, affordability remains a key consideration for many consumers.

Limited accessibility of golf facilities in developing regions

Limited accessibility of golf facilities in developing regions remains a significant challenge for the golf equipment and apparel market. Many emerging economies have a relatively small number of golf courses, driving ranges, and training centers compared to established golfing markets. The high capital investment required for course development, maintenance, and land acquisition often restricts infrastructure expansion. As a result, potential participants may have limited opportunities to learn and regularly engage with the sport. The lack of accessible facilities also reduces demand for golf clubs, balls, apparel, footwear, and related accessories, as fewer consumers actively participate in golf. In addition, long travel distances to available courses can discourage recreational play and limit player retention. Consequently, inadequate golf infrastructure in developing regions continues to constrain the pace of market growth and broader adoption of the sport.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Technology Inflection Drives Equipment, Apparel Captures Fastest Growth

The equipment segment accounted for the largest share of the golf equipment and apparel market, representing 75.91% of total revenue in 2025. Its dominance is primarily attributed to the high value and replacement demand associated with golf clubs, balls, bags, rangefinders, and other performance-oriented accessories. Golfers frequently invest in technologically advanced equipment designed to improve accuracy, distance, and overall gameplay, supporting consistent sales across both professional and recreational segments. Continuous innovation in club materials, fitting technologies, and ball construction has further strengthened consumer interest in premium equipment. The presence of established brands with extensive product portfolios and strong distribution networks also contributes to the segment’s leadership position.

The apparel segment is projected to register the fastest growth, expanding at a CAGR of 5.74% through 2031. Growth is being driven by increasing consumer preference for performance-focused golf clothing that combines comfort, functionality, and style. Manufacturers are introducing advanced fabrics featuring moisture-wicking, stretchability, UV protection, and temperature regulation to enhance on-course performance. The growing participation of younger players and women in golf is also creating new opportunities for apparel brands to diversify product offerings. Additionally, the influence of athleisure trends is encouraging consumers to purchase golf apparel for both sporting and casual wear applications.

By Category: Mass Foundations Sustain Volume, Premium Tier Outpaces The Market

The mass category dominated the golf equipment and apparel market, accounting for 66.75% of total revenue in 2025. Its leadership is largely attributed to the broad consumer base of recreational and amateur golfers who prioritize affordability and accessibility when purchasing golf products. Mass-market equipment, apparel, and accessories are widely available through sporting goods retailers, specialty golf stores, and online platforms, enabling extensive market penetration. Manufacturers continue to strengthen this segment by offering quality products at competitive price points while maintaining performance standards suitable for everyday golfers. The category also benefits from growing participation in golf across emerging markets, where price-sensitive consumers represent a significant share of demand.

The premium category is projected to witness the fastest growth, registering a CAGR of 5.46% through 2031. Rising consumer interest in high-performance golf equipment, technologically advanced products, and luxury golf apparel is driving demand across this segment. Professional and avid golfers are increasingly willing to invest in premium clubs, balls, footwear, and apparel that offer enhanced performance, durability, and customization features. The influence of professional tournaments, celebrity endorsements, and premium golf lifestyles is also encouraging greater spending on high-end products. Manufacturers are responding by introducing innovative materials, custom-fitting services, and exclusive product collections tailored to affluent consumers.

By End User: Adult Core Anchors Revenue, Youth Segment Reshapes Long-Term Strategy

The adults segment dominated the golf equipment and apparel market, accounting for 83.76% of total revenue in 2025. This substantial share is primarily driven by the high participation of adults in recreational, amateur, and professional golf activities worldwide. Adult consumers represent the largest purchasing group for golf clubs, balls, bags, footwear, apparel, and accessories, contributing significantly to overall market demand. Higher disposable incomes and a greater willingness to invest in premium and technologically advanced golf products further support the segment’s leadership. Corporate golf events, club memberships, golf tourism, and regular participation in tournaments also encourage consistent spending among adult golfers.

The kids and children segment is projected to record the fastest growth, expanding at a CAGR of 5.58% through 2031. Increasing efforts by golf associations, schools, and training academies to promote youth participation are creating favorable conditions for market expansion. Many golf clubs and organizations are introducing junior development programs aimed at encouraging early engagement with the sport. Manufacturers are responding by launching age-specific equipment, apparel, and footwear designed to meet the performance and comfort requirements of young players.

By Distribution Channel: Physical Stores Hold Share, Digital Commerce Redefines Conversion

The offline retail stores segment accounted for the largest share of the golf equipment and apparel market, representing 71.25% of total revenue in 2025. Its dominance is supported by consumers' preference for physically evaluating golf clubs, apparel, footwear, and accessories before making a purchase. Many golfers rely on in-store product demonstrations, professional fitting services, and expert guidance to select equipment that matches their skill level and playing style. Specialty golf stores, pro shops, and sporting goods retailers continue to serve as important distribution channels, particularly for premium and customized products. The ability to access immediate product availability and personalized customer service further strengthens the appeal of offline retail outlets.

The online retail stores segment is projected to witness the fastest growth, registering a CAGR of 6.21% through 2031. Increasing internet penetration and the growing adoption of e-commerce platforms are making golf products more accessible to consumers across diverse regions. Online channels offer a broad selection of equipment, apparel, and footwear, enabling customers to compare products, prices, and reviews conveniently. Manufacturers and retailers are increasingly investing in direct-to-consumer platforms, digital marketing strategies, and personalized online shopping experiences to expand their reach.

Geography Analysis

North America dominated the golf equipment and apparel market with a 49.01% revenue share in 2025, supported by the region’s well-established golf culture, extensive course infrastructure, and high consumer spending on premium golf products. The United States remains the largest contributor, driven by strong participation rates across professional, amateur, and recreational golfers. The presence of leading manufacturers, advanced retail networks, and a thriving golf tourism industry further strengthens regional demand. Consumers in the region show a strong preference for technologically advanced clubs, performance golf balls, and premium apparel. Additionally, increasing adoption of custom-fitted equipment and direct-to-consumer sales channels continues to support market expansion across North America.

Asia-Pacific is projected to register the fastest CAGR of 5.92% through 2031, driven by rising golf participation and growing disposable incomes across several countries. Markets such as Japan, South Korea, China, and Australia are witnessing increasing interest in golf among younger consumers and corporate professionals. Expanding golf course development, golf academies, and driving range facilities are contributing to greater equipment and apparel sales. International tournaments and promotional activities are also improving awareness and participation levels. Furthermore, the growing popularity of premium sportswear and technologically enhanced golf equipment is expected to accelerate market growth throughout the forecast period.

Europe maintains a significant position in the golf equipment and apparel market, supported by established golfing communities in the United Kingdom, Germany, France, Spain, and the Nordic countries. Demand in the region is driven by golf tourism, club memberships, and increasing interest in performance-focused apparel. South America represents a smaller but steadily expanding market, with Brazil and Argentina contributing to regional growth through rising participation and infrastructure development. Meanwhile, the Middle East and Africa are experiencing gradual market expansion due to increasing investments in premium golf resorts, tourism projects, and international golf events. Growing interest in luxury sports and leisure activities is expected to create additional opportunities across these regions.

Competitive Landscape

The golf equipment and apparel market exhibits a moderately consolidated competitive structure, led by established manufacturers with strong brand equity, extensive product portfolios, and global distribution networks. Companies such as Acushnet Holdings Corp. (Titleist and FootJoy), Topgolf Callaway Brands Corp., TaylorMade Golf Company, Inc., and PING, Inc. maintain significant market positions through continuous innovation in golf clubs, balls, footwear, and apparel. Their long-standing relationships with professional golfers, golf courses, and specialty retailers strengthen customer loyalty and reinforce their market presence across major golfing regions.

Competition is driven by ongoing investments in product development, performance-enhancing technologies, and premium product offerings. Leading equipment manufacturers focus on advancements in club design, ball aerodynamics, fitting technologies, and lightweight materials to improve player performance. In the apparel segment, companies emphasize moisture management, stretch fabrics, UV protection, and comfort-oriented designs to cater to both professional and recreational golfers. Strategic sponsorships of professional tours, tournaments, and athletes further enhance brand visibility and influence purchasing decisions among consumers.

Despite the dominance of major players, the market remains competitive due to the presence of numerous specialized and lifestyle-focused brands. Companies such as PXG, Peter Millar, TravisMathew, G/FORE, and J.Lindeberg have established strong positions in premium equipment and golf apparel niches by targeting specific consumer preferences and lifestyle trends. The growing popularity of e-commerce, direct-to-consumer sales channels, and customized golf products has lowered barriers to market entry, enabling emerging brands to expand their reach and compete effectively alongside larger industry participants.

Golf Equipment and Apparel Industry Leaders

Acushnet Holdings Corp. (Titleist & FootJoy)

TaylorMade Golf Company, Inc.

PING, Inc.

Mizuno Corporation

The Callaway Golf Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Topgolf opened its 102nd US venue in Parsippany, New Jersey, introducing a new venue prototype featuring arcade games, reimagined driving range targets, and a personalized "My Bay, My Way" experience, marking the brand's continued venue rollout under new majority ownership by Leonard Green & Partners.

- May 2026: Callaway Golf introduced its Quantum driver lineup, which featured Tri-Force Face technology. This innovative design combined titanium, poly mesh, and carbon fiber, and included an AI-optimized face crafted from actual impact data, all aimed at enhancing distance and spin performance for competitive players.

- March 2026: McLaren entered the golf equipment arena with the debut of McLaren Golf. Leveraging its rich heritage in Formula 1 and high-performance automotive engineering, McLaren Golf developed premium golf equipment, emphasizing precision, innovation, and performance enhancement.

Global Golf Equipment and Apparel Market Report Scope

The Golf Equipment and Apparel Market comprises the production, distribution, and sale of products specifically designed for playing and participating in golf. The golf equipment and apparel market is segmented by product type, category, end user, distribution channel, and geography. Based on the product type, the market is segmented into apparel, footwear and equipment. Based on category, the market is segmented into mass and premium. Based on end user, the market is segmented into kids/children and adults. The market is segmented by distribution channel into offline and online retail stores. The market also covers the global-level analysis of major regions, such as North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts were made based on value (USD million).

| Apparel | |

| Footwear | |

| Equipment | Golf Clubs |

| Golf Balls | |

| Golf Bags and Accessories |

| Mass |

| Premium |

| Adults |

| Kids/Children |

| Offline Retail Stores |

| Online Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| France | |

| Italy | |

| Sweden | |

| Ireland | |

| Austria | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| New Zealand | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Apparel | |

| Footwear | ||

| Equipment | Golf Clubs | |

| Golf Balls | ||

| Golf Bags and Accessories | ||

| By Category | Mass | |

| Premium | ||

| By End User | Adults | |

| Kids/Children | ||

| By Distribution Channel | Offline Retail Stores | |

| Online Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| France | ||

| Italy | ||

| Sweden | ||

| Ireland | ||

| Austria | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| New Zealand | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2031 outlook for golf equipment and apparel market?

The golf equipment and apparel market is forecast to reach USD 26.71 billion by 2031 from USD 20.87 billion in 2026, at a 5.06% CAGR.

Which product area contributes the most revenue today?

Equipment leads the revenue mix with 75.91% share in 2025, which shows that clubs, balls, and related hardware still form the core spending base.

Which sales channel is growing the fastest?

Online retail stores are growing the fastest at a 6.21% CAGR through 2031, even though offline stores still held 71.25% share in 2025.

Which region is expanding the quickest?

Asia-Pacific is forecast to grow at a 5.92% CAGR through 2031, supported by South Korea, Japan, China, Australia, and New Zealand.

Why are premium golf products gaining traction?

Premium products are benefiting from AI-led fitting, visible technology upgrades, and stronger aspirational demand tied to tournaments and media exposure.

Page last updated on: