Second Hand Apparel Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

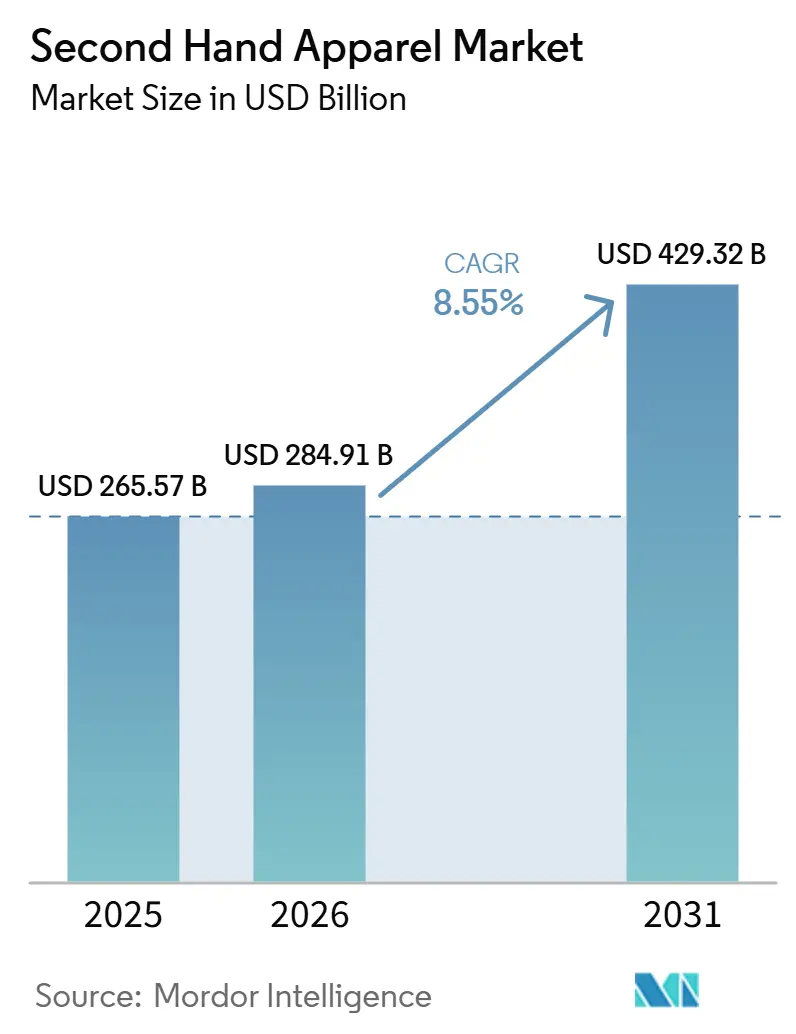

| Market Size (2026) | USD 284.91 Billion |

| Market Size (2031) | USD 429.32 Billion |

| Growth Rate (2026 - 2031) | 8.55% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

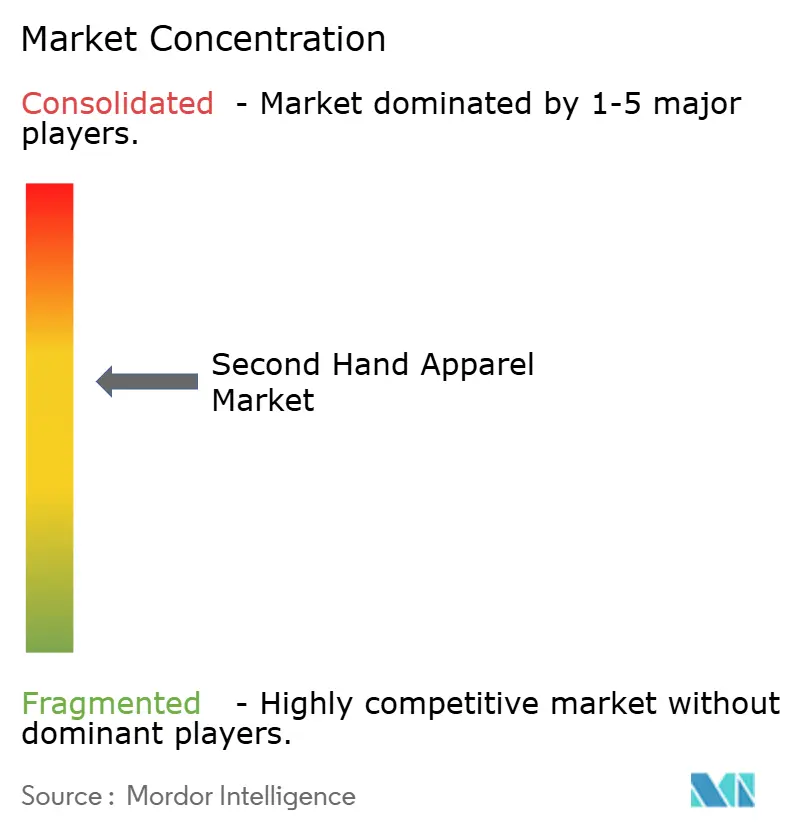

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Second Hand Apparel Market Analysis by Mordor Intelligence

The second hand apparel market size was valued at USD 265.57 billion in 2025 and will reach USD 429.32 billion by 2031, advancing at an 8.55% CAGR from 2026 to 2031. The second hand apparel market has moved into a mainstream retail position, with resale now representing 10% of total global apparel spending, which shows that used clothing is becoming a regular part of wardrobe buying rather than a niche purchase route. Growth is being supported by a stronger value focus, broader acceptance of circular shopping, and a faster shift toward digital discovery, where shoppers increasingly find secondhand items through social feeds and platform tools instead of store-led browsing. The second hand apparel market is also benefiting from brand participation, as more apparel companies use resale programs to keep customers inside their ecosystems and unlock repeat supply through trade-ins and branded resale channels. Trust remains a central challenge because counterfeit risk, inconsistent item condition, and high processing needs can reduce repeat buying and pressure platform margins when intake quality is poor. Competition remains fragmented, and the companies that stand to gain most are those that improve supply capture, verification quality, and the buying experience without raising fulfillment complexity.

Key Report Takeaways

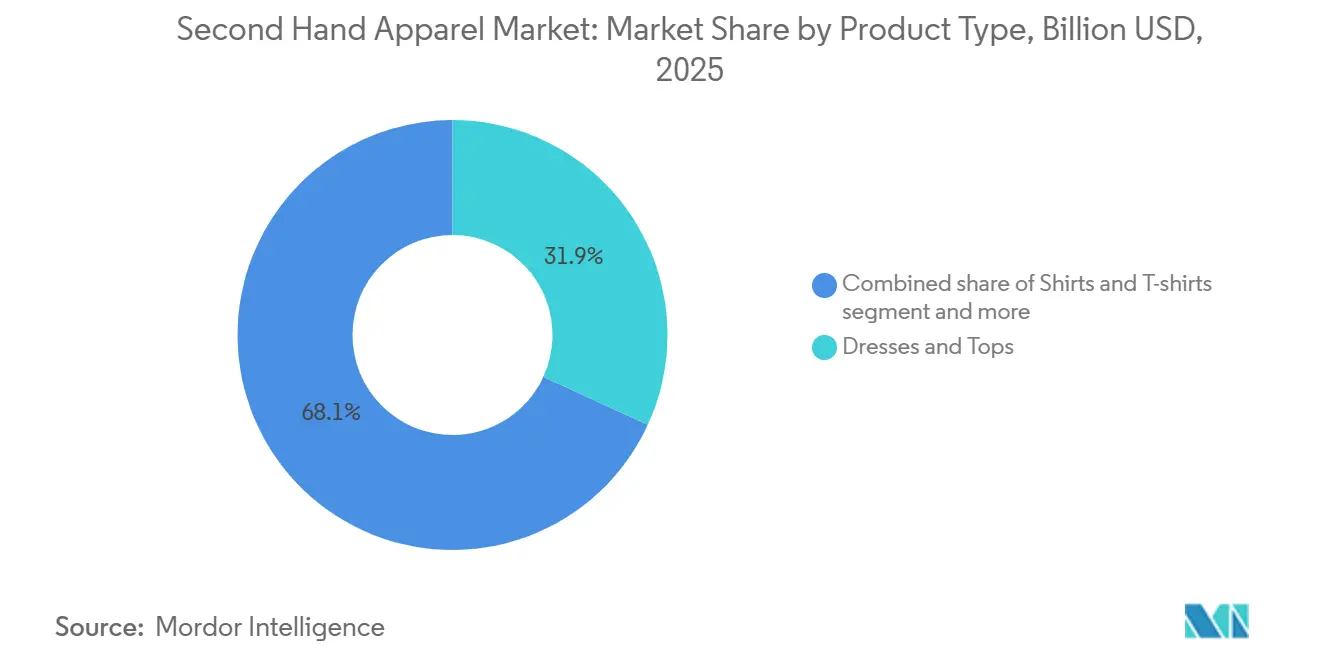

- By product type, Dresses and Tops led with 31.9% of the second hand apparel market size in 2025, while Shirts and T-shirts are forecast to expand at a 9.2% CAGR through 2031.

- By sector, Resale held 73.2% of the second hand apparel market share in 2025 and is also projected to record the fastest 9.4% CAGR through 2031.

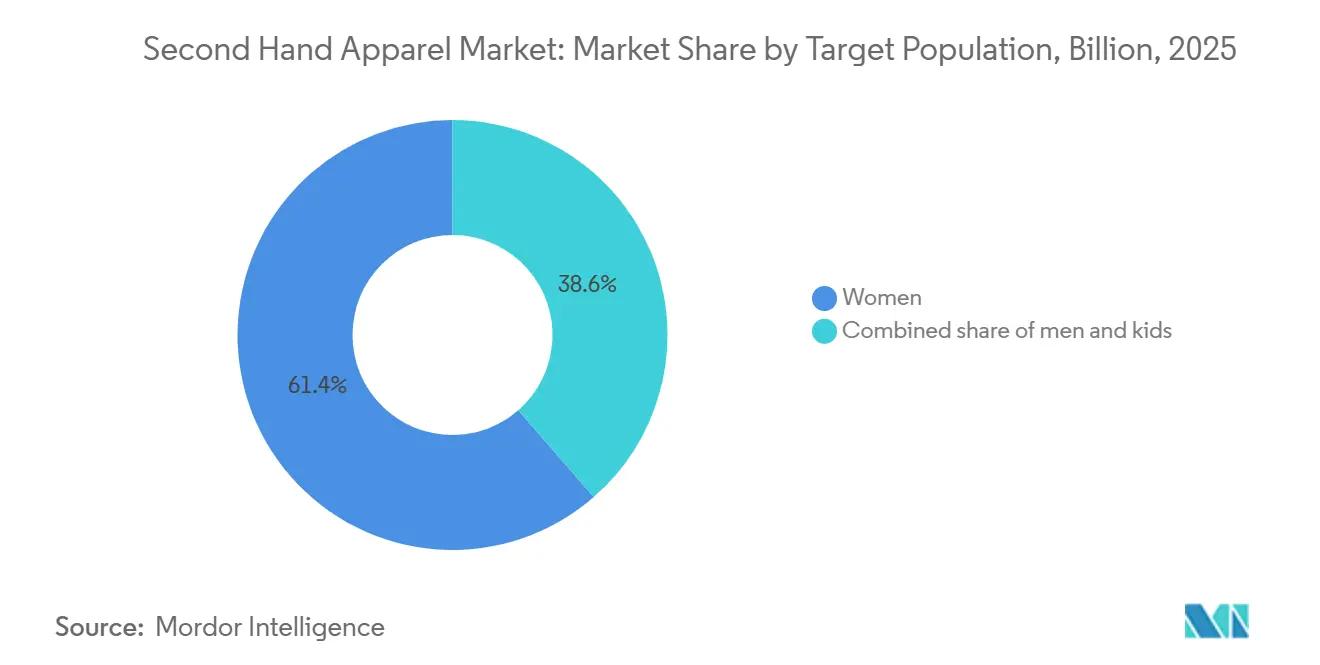

- By target population, Women accounted for 61.4% of the 2025 market, while Kids segment is expected to grow at the highest 9.3% CAGR through 2031.

- By distribution channel, Offline Retail Stores held 53.3% of the 2025 market, while Online Retail Stores are projected to advance at a 10.1% CAGR through 2031.

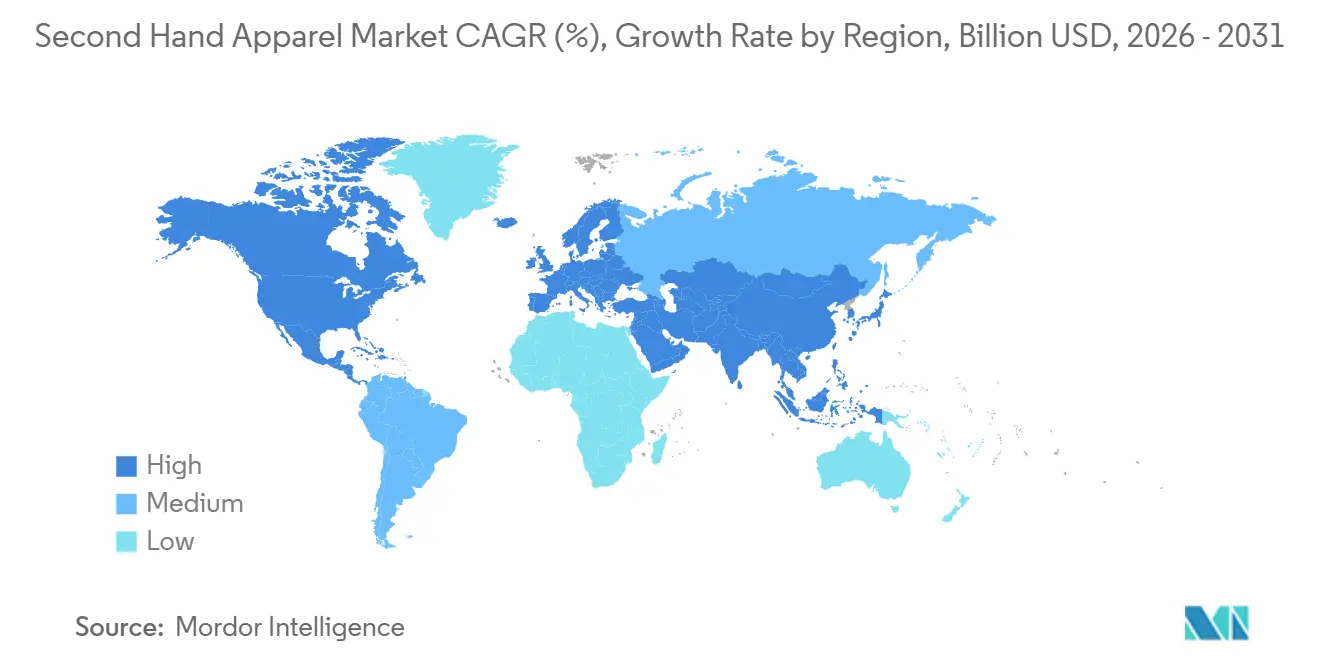

- By geography, North America commanded 37.9% of the global market in 2025, while Asia-Pacific is forecast to post the fastest 9.6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Second Hand Apparel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Consumer Shift Toward Circular Fashion | +2.5% | Global, led by North America, Western Europe, and East Asia | Long term (≥ 4 years) |

| E-Commerce and Social Commerce Expansion | +2.0% | Global, with outsized impact in Asia-Pacific and North America | Short to medium term (≤ 4 years) |

| Brand-Led Resale and Resale-as-a-Service Adoption | +1.3% | North America and Europe core, and spill over to the Asia-Pacific | Medium term (2-4 years) |

| AI-Enabled Discovery, Pricing, and Authentication | +1.0% | North America, Western Europe, East Asia | Medium to long term (2-5 years) |

| Price Sensitivity in Premium and Mass Apparel | +1.2% | Global, most acute in North America and South America | Short term (≤ 2 years) |

| Sustainability Reporting Pressure on Apparel Brands | +0.6% | EU core, growing in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising consumer shift toward circular fashion

Circular fashion is moving beyond lifestyle positioning and translating into measurable spending behavior. Secondhand clothing sales in the top 20 circular shopping economies are projected to rise 28% year over year in 2025, growing more than three times faster than conventional clothing retail in the same markets. Generational shifts are driving this trend. Bank of America card data indicates that Gen Z is expected to account for 41% of secondhand sellers in the first half of 2026, up from 37% in 2024. Gen Z is also expected to be the only generation to increase apparel spending growth across all income cohorts in March 2026. The current cycle differs from earlier resale momentum because resale is emerging as a discovery channel for aspirational brands. BCG survey data from April–May 2025 is expected to show that 66% of secondhand buyers were introduced to a new brand through resale, up from 59% in 2022. This trend suggests that the channel can actively generate firsthand demand rather than cannibalize it. The US Bureau of Labor Statistics is expected to formalize this shift in early 2025 by incorporating secondhand apparel into the Consumer Price Index, recognizing it as a core component of household consumption rather than a peripheral category[1]Source: U.S. Bureau of Labor Statistics, “Monthly Labor Review,” U.S. Bureau of Labor Statistics, bls.gov .

E-commerce and social commerce expansion

Social commerce is changing how consumers discover and purchase secondhand products in ways that legacy marketplace interfaces cannot replicate. ThredUp's 2026 Resale Report found that nearly 50% of shoppers discover secondhand items through social media, creator content, and influencer feeds rather than traditional search. This shift makes platform discoverability more dependent on content strategy than SEO. According to Bank of America, secondhand apparel transactions per US household rose 22% year over year in March 2026, while spending per transaction declined. This pattern indicates higher purchase frequency at lower average price points, which aligns with the typical profile of social-driven impulse discovery. The implication for platform strategy remains underappreciated: transaction frequency now matters more than basket size. As a result, platforms that do not build social-native interfaces risk losing younger buyer cohorts to content-embedded alternatives, including TikTok Shop and Instagram Checkout. Online resale in the United States grew 23% in 2024 and is projected to nearly double over the next five years, establishing digital platforms as the structural growth engine of the pre-owned fashion market.

Brand-led resale and resale-as-a-service adoption

Brand-owned and brand-partnered resale programs are expected to reach a commercial inflection point by 2025. In Q3 2025 alone, 17 fashion brands are expected to launch dedicated resale programs, reflecting a shift from pilot experimentation to operational integration within core commercial strategies. ThredUp’s Resale-as-a-Service (RaaS) platform is expected to support circularity initiatives for more than 60 global brands, including J.Crew, Tommy Hilfiger, and Madewell. This would represent a 37% increase in branded resale adoption since May 2025, when the company is expected to eliminate upfront fees for RaaS partners. BCG analysis identifies two dominant models: brand-owned platforms, such as Patagonia Worn Wear and Rolex Certified Pre-Owned, and resale-as-a-service partnerships with third-party platforms. Both models increasingly incorporate Digital Product Passports (DPPs) to enable one-click resale. In one documented case, Chloé x Vestiaire Collective reduced seller processing time by more than 60%. A counterintuitive dynamic is emerging: brand-led resale programs are functioning as customer acquisition tools for first-hand channels. In 2025, nearly 47% of consumers are expected to say they would be more likely to make a first-time purchase from a brand if it offered trade-in credit for used apparel.

AI-enabled discovery, pricing, and authentication

AI is reducing the operational cost structure of resale in ways that platform financial results do not yet fully reflect, but these efficiencies will prove decisive during the 2026–2031 forecast period. A FashionUnited analysis dated June 2026 notes that the EU’s Ecodesign for Sustainable Products Regulation (ESPR), approved under Regulation (EU) 2024/1781, will mandate Digital Product Passports for textiles beginning around 2028[2]Source: European Union, “Regulation (EU) 2024/1781,” EUR-Lex, eur-lex.europa.eu. These passports will create structured, machine-readable garment identities, enabling AI systems to authenticate, grade, and price items automatically at intake. ThredUp’s June 2026 Direct Listing launch integrated AI-powered tools for studio-quality image processing, auto-populated product details, and smart pricing recommendations, allowing sellers to list items within minutes. The launch generated nearly 18% of beta listings priced above USD 100, with an average selling price of USD 60, more than double the managed marketplace average. AI pricing tools also create a supply-side effect: more accurate value signals increase sellers’ willingness to list items. This is material, as ThredUp’s 2026 report estimated that USD 23.3 billion in additional US market value depends on reducing friction for prospective sellers. AI-powered visual authentication, which leads the fashion resale authentication services segment with a 45% share, is also reducing platform authentication costs and enabling real-time fraud detection at scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inventory Quality, Variability, and Condition Uncertainty | -1.3% | Global, most acute in peer-to-peer and emerging markets | Long term (≥ 4 years) |

| High Reverse Logistics and Processing Complexity | -1.0% | Global, with greater severity in markets with diffuse supply networks | Medium term (2-4 years) |

| Authentication, Fraud, and Counterfeit Risk | -0.9% | Global, most severe in the luxury apparel and accessories segments | Medium to long term (2-5 years) |

| Consumer Trust Gaps in Peer-to-Peer Resale | -0.5% | Global, with a concentration in less mature resale markets | Short to medium term (≤ 4 years) |

| Source: Mordor Intelligence | |||

Inventory quality variability and condition uncertainty

Quality inconsistency remains the most persistent structural drag on conversion rates in the secondhand channel, and the industry often underestimates the difficulty of addressing it. Unlike new goods, each secondhand item is effectively unique, with variations in condition, provenance, and wear patterns. These differences make automated quality grading technically challenging and make human inspection expensive at scale. Research slated for publication in the Journal of Fashion Marketing and Management in 2025 identifies the absence of standardized quality grading as a critical bottleneck in secondhand reverse logistics[3]Source: Journal of Fashion Marketing and Management, “Research on Secondhand Reverse Logistics and Quality Grading,” Emerald Publishing, emerald.com. Low-quality item rates further compound this challenge by weakening the economics of individual item processing. For managed platforms, the cost implications are significant: items that fail quality review still require processing, photography, and return or disposal, with no revenue recovery. Online fashion return rates already average 30% to 40% for conventional apparel, and heterogeneous secondhand inventory further increases sorting complexity within these reverse logistics networks. Platforms that gain a durable competitive advantage will likely be those that solve grading at intake, either through AI-assisted condition scoring at the seller stage or through physical inspection networks integrated into the supply origination point.

Authentication, fraud, and counterfeit risk

Counterfeit infiltration in the secondhand channel is intensifying as replica manufacturing becomes more sophisticated and platform volumes exceed human verification capacity. Entrupy, one of the leading authentication technology providers, processed more than USD 3.7 billion worth of products in 2025 and noted that apparel and accessories are now among the most counterfeited categories it has assessed. This marks a shift from prior years, when handbags dominated counterfeit activity. Research released by the UK Intellectual Property Office found that nearly 60% of consumers who unknowingly purchased counterfeit secondhand items experienced negative outcomes, including poor durability and refund disputes. In addition, 14% reported that the experience deterred them from secondhand shopping entirely, creating a churn effect that platform growth models rarely account for. Authentication accuracy of 98% to 99% appears high, but at the transaction volumes processed by leading platforms, that margin of error can result in thousands of misclassified items each year. The costs per incident include refunds, reputational damage, and potential regulatory exposure. Platforms are investing in AI-powered visual authentication and DPP-linked verification infrastructure. However, authentication costs, which range from 5% to 15% of product value for mid-market items, remain a margin constraint and limit how broadly platforms can deploy these systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dresses and Tops Anchor Volume, but Casualwear Accelerates Fastest

Dresses and Tops are expected to hold the largest share in 2025, at 31.86%. This position reflects the dominance of women’s fashion in global resale volumes and the relatively higher resale value retention of occasion and lifestyle wear compared to performance or workwear categories. Women’s clothing accounted for 42.8% of all secondhand apparel expenditures across multiple survey periods, a pattern supported by US BLS data on consumer secondhand spending (US BLS). Shirts and T-shirts are projected to be the fastest-growing product segment, with a CAGR of 9.22% from 2026 to 2031. Growth in this segment is driven by the democratization of resale through peer-to-peer apps, where casual basics support high-volume, low-friction transactions with rapid turnover.

Sweaters, Coats and Jackets, and Jeans and Pants show distinct performance trends. Structured outerwear commands premium resale values on curated platforms but records slower sales velocity, while denim has built a dedicated sub-community of collectors and sustainability-oriented buyers. Other Product Types, including vintage formal wear, activewear, and accessories-adjacent apparel, represent emerging growth pockets, particularly among Gen Z buyers who are highly active in niche category communities on social platforms. BCG’s April–May 2025 consumer survey found that Gen Z buyers are more likely than average to seek the “thrill of the hunt” and limited items in secondhand markets, sustaining premium pricing power for scarcer product types.

By Sector: Resale Dominance Widens as Technology Shifts Value Capture

The resale sector is projected to account for 73.24% of the market in 2025 and is expected to be the fastest-growing sector, registering a CAGR of 9.37% during 2026-2031. This trend indicates that market leadership in secondhand commerce is compounding rather than plateauing. Such dual dominance is uncommon in mature consumer categories and suggests that resale platforms are converting supply that would previously have gone to donation or disposal. The Traditional Thrift Stores and Donations segment continues to maintain a significant physical footprint, particularly in North America, where Goodwill and the Salvation Army operate thousands of stores. However, its share is expected to compress at a faster pace as resale platforms improve seller economics and reduce friction in supply origination.

A key structural insight often missed in consensus commentary is that Traditional Thrift and Resale do not simply compete for the same buyer. They serve different needs, with thrift retaining a price-floor role for items priced under USD 5 to USD 20, while resale moves toward mid-market branded goods. Mercari’s US business reported its first full-year profit in fiscal 2025, with US revenue increasing 11% year over year in the October-to-December quarter, marking its first double-digit growth rate in four years. This performance illustrates how managed platforms in the resale sector are converting scale into profitability. As resale platforms mature and improve their cost structures, the gap with donation-based thrift in seller experience and buyer trust is expected to widen further.

By Target Population: Women's Market Leads, Kids Segment Emerges as Strategic Opportunity

The women segment accounted for 61.42% of the 2025 market, supported by decades of fashion culture, higher average item values, and a greater willingness to buy and sell preloved clothing compared to the men’s and children’s segments. Men represented a smaller but growing cohort. BCG noted that male secondhand buyers in the United States are more likely to approach resale transactionally, including viewing selling as a partial or full-time income source, suggesting that the segment’s TAM remains underleveraged relative to engagement intent.

The kids segment is the fastest-growing target segment, registering a CAGR of 9.29% during 2026-2031. Growth is driven by lifecycle logic that adults apply to children’s clothing, including short wear cycles, rapid growth, and lower emotional attachment to used goods, making secondhand children’s apparel one of the clearest value propositions in the market. The Bank of America Institute found that lower-income Gen X households, which index high on children’s apparel spending relative to disposable income, are among the most active secondhand buyers, supporting the kids segment’s structural growth case. Platforms that bundle children’s resale with household management tools, trade-in credit for outgrown items, and automatic size-up notifications will capture this segment more effectively than generic resale interfaces.

By Distribution Channel: Offline Holds Scale, Online Captures Share

Offline retail stores are expected to retain the largest channel share, at 53.28% in 2025, supported by the physical footprint of donation-based thrift chains and the tactile buying experience that many secondhand shoppers, particularly older demographics, prefer when assessing product condition. The resilience of the physical channel also reflects supply-side dynamics. Donation-based thrift chains receive continuous inflows from consumer drop-offs without incurring the seller acquisition costs that digital platforms face.

Online retail stores are expected to be the fastest-growing channel, registering a CAGR of 10.14% during 2026-2031 and outpacing the market average by nearly 160 basis points. This growth is driven by the compounding effects of AI-powered discovery, social commerce integration, and the geographic reach advantages of digital platforms over brick-and-mortar stores. US online resale grew by 23% in 2024 and is projected to nearly double over the next five years, supported by accelerating buyer acquisition rates. The market is not shifting to a purely digital model. Physical thrift retains structural resilience, but the channel share shift is expected to continue as younger cohorts entering the market online are unlikely to transition to physical channels. ThredUp’s Q1 2026 results, with 1.71 million active buyers, up 25% year-over-year, and 1.64 million orders, up 19%, reflect the accelerating buyer base that online-first platforms are building.

Geography Analysis

North America is expected to account for 37.91% of the second-hand apparel market share in 2025, maintaining its position as the largest regional block due to its well-established resale infrastructure, consumer familiarity with digital platforms, and price-sensitive shopping behavior. ThredUp stated that the US secondhand market is expected to grow nearly four times faster than the broader retail clothing market in 2025. The region also benefits from a large installed base of branded apparel, which supports mass and premium resale activity across thrift, marketplace, and authenticated channels. Continued apparel price pressure has reinforced value-driven shopping behavior, helping resale sustain consumer interest even when discretionary budgets remain tight. North American brands with exposure to Europe also face pressure to develop stronger circular systems as the EU tightens textile product rules and resale traceability expectations.

Europe is expected to remain the second-largest regional block in the second-hand apparel market in 2025, supported by the alignment of regulation and consumer behavior. The region has strong platform adoption, and Vinted reported solid growth expectations for 2025 in both gross merchandise value and revenue, indicating that the peer-to-peer model has reached significant scale in European apparel resale. Core markets such as Germany, the United Kingdom, France, and the Netherlands continue to anchor demand, although purchase motivations vary between value-driven and sustainability-driven shoppers. Eastern Europe remains less developed in authenticated premium resale, creating opportunities for service providers that can introduce trust tools and verification without requiring heavy local inventory ownership. H&M Group’s continued positioning of Sellpy within its broader circularity agenda also shows that European apparel players are treating resale as an operational line of business rather than a limited brand initiative.

Asia-Pacific is projected to be the fastest-growing geography in the second-hand apparel market, with a 9.61% CAGR from 2026 to 2031, as mobile-first shopping, rising platform familiarity, and cross-border flows broaden access. Mercari is expected to launch a new US app in June 2026 and has stated plans to expand to at least 50 countries and regions by 2028, after extending its Global App into Taiwan and Hong Kong in late 2025. This highlights how Asia-based platforms are expanding outward from established domestic ecosystems. India is developing more organized, branded, and luxury resale activity through digitally active urban centers, while Southeast Asian markets continue to strengthen trust mechanisms in premium categories through verification and curated onboarding. South America, the Middle East, and Africa remain smaller in absolute size, but they remain important to long-term growth as recommerce activity rises and several African markets continue to serve as major destinations for used clothing inflows from Europe and North America.

Competitive Landscape

The secondhand apparel market remains highly fragmented, with no company holding more than a low double-digit share globally. The market includes managed marketplaces such as ThredUp and The RealReal, peer-to-peer platforms such as Vinted, Poshmark, and Depop, and brand-linked resale programs that operate alongside first-hand retail channels. These boundaries are becoming less rigid as larger operators add peer-to-peer tools, peer-to-peer platforms expand verification and curation, and brands build resale participation through partners rather than remaining outside the channel. The RealReal’s Q1 2026 results reported gross merchandise value growth of 24%, total revenue of USD 189.7 million, and a 10% increase in active buyers to 1.1 million, showing that authenticated luxury resale can continue to grow as competition expands. This performance supports the view that scale in premium resale depends less on catalog size alone and more on trust, service quality, and repeat buyer confidence.

Technology spending is becoming the clearest differentiator in the secondhand apparel market, as operators need better tools to process unique inventory with lower friction. Platforms now deploy AI across item recognition, condition assessment, pricing support, listing support, and buyer matching. As a result, leading platforms are working to improve cost efficiency and conversion simultaneously. ThredUp’s June 2026 Direct Listing beta provides a clear example, as the company combined 0% seller fees with AI-based listing tools and stated that nearly 18% of beta listings were priced above USD 100, while the average selling price reached USD 60. Mercari’s June 2026 launch of a new US app and its broader international expansion plan reflect a similar effort to expand cross-border reach and attract more digitally native resale activity. These developments matter because the next stage of competition will depend heavily on which operators can capture supply earlier, list it faster, and present it more clearly across mobile-led shopping environments.

Brand-linked ecosystems are adding another layer of competition in the secondhand apparel market by combining product familiarity, trade-in incentives, and direct customer relationships. ThredUp stated that its resale-as-a-service platform supports more than 60 global brands, including J.Crew, Tommy Hilfiger, and Madewell, giving these labels a practical way to participate in resale without building the full operating stack independently. H&M Group’s use of Sellpy indicates a similar direction, with resale becoming more closely tied to broader circular business priorities and ongoing customer engagement. Smaller regional players still have room to compete, as they often understand local supply patterns, brand preferences, and trust expectations better than large global platforms with standardized operating models.

Second Hand Apparel Industry Leaders

ThredUp Inc.

The RealReal, Inc.

Poshmark, Inc.

Vinted Group

Mercari, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: ThredUp launched the open beta of Direct Listing, a peer-to-peer selling tool integrated into its existing marketplace, offering 0% seller fees and AI-powered listing tools. During beta, nearly 18% of listings were priced above USD 100 with an average selling price of USD 60, more than double the managed marketplace average, demonstrating the unit economics uplift that P2P supply can provide at the top of the price range.

- June 2026: Vinted launched in Australia, its newest market outside Europe, by connecting Australian sellers with UK buyers through an international shipping corridor. This move further expanded its cross-border resale reach following its January 2026 US launch.

- January 2026: Vinted made its formal US market entry with a campaign targeting New York consumers, committing tens of millions of dollars in marketing investment over the following months to establish a foothold against incumbent platforms Poshmark, ThredUp, and Mercari.

Global Second Hand Apparel Market Report Scope

Second hand apparel (or used clothing) refers to any garment or accessory that has been previously owned and worn by another individual before being sold, donated, or passed on. The global second hand apparel market is segmented by product type, sector, target population, distribution channel, and geography. By product type, the market is segmented into dresses and tops, shirts and t-shirts, sweaters, coats and jackets, jeans and pants, and others. By sector, the market is segmented into resale and traditional thrift stores and donations. By target population, the market is segmented into women, men, and kids. By distribution channel, the market is segmented into offline retail stores and online retail stores. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Dresses and Tops |

| Shirts and T-shirts |

| Sweaters |

| Coats and Jackets |

| Jeans and Pants |

| Other Product Types |

| Resale |

| Traditional Thrift Stores and Donations |

| Women |

| Men |

| Kids |

| Offline Retail Stores |

| Online Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Kenya | |

| Egypt | |

| Rest of Middle East and Africa |

| Product Type | Dresses and Tops | |

| Shirts and T-shirts | ||

| Sweaters | ||

| Coats and Jackets | ||

| Jeans and Pants | ||

| Other Product Types | ||

| Sector | Resale | |

| Traditional Thrift Stores and Donations | ||

| Target Population | Women | |

| Men | ||

| Kids | ||

| By Distribution Channel | Offline Retail Stores | |

| Online Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Kenya | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the second hand apparel market?

The second hand apparel market was valued at USD 265.57 billion in 2025 and is projected to reach USD 429.32 billion by 2031, growing at an 8.55% CAGR from 2026 to 2031.

Which region leads global sales for used clothing resale?

North America held the largest share in 2025 at 37.91%, supported by mature resale platforms, strong consumer familiarity, and continued value-focused apparel buying.

Which region is expanding the fastest through 2031?

Asia-Pacific is forecast to record the fastest growth, with a 9.61% CAGR from 2026 to 2031, helped by mobile-first commerce and cross-border platform expansion.

Which product categories generate the most demand?

Dresses and Tops led the market in 2025 with a 31.86% share, while Shirts and T-shirts are set to grow the fastest through 2031 at a 9.22% CAGR.

Page last updated on: