Gym Apparel Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 115.93 Billion |

| Market Size (2031) | USD 163.61 Billion |

| Growth Rate (2026 - 2031) | 7.13% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gym Apparel Market Analysis by Mordor Intelligence

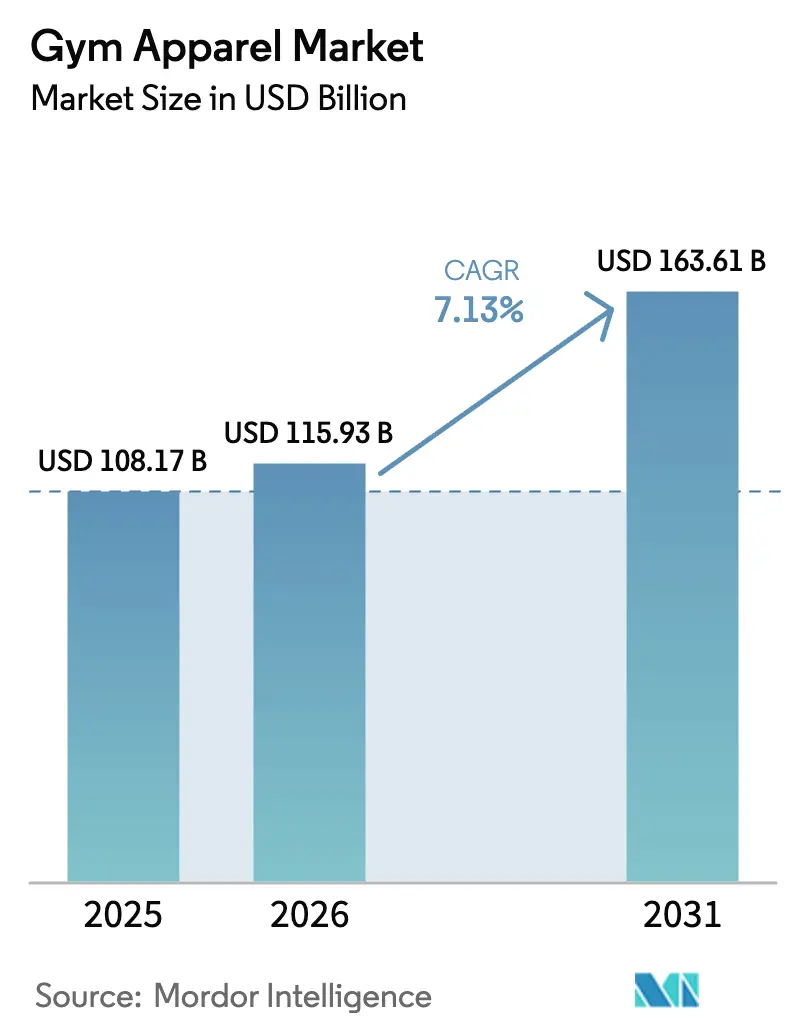

The global gym apparel market size is expected to grow from USD 108.17 billion in 2025 to USD 115.93 billion in 2026 and is forecast to reach USD 163.61 billion by 2031 at a 7.13% CAGR over 2026-2031. This growth trajectory underscores the fusion of rising athleisure trends, a surge in wellness-focused consumer spending, and innovations in technical fabrics. Together, these elements are reshaping gym apparel into a blend of performance gear and a lifestyle statement. The market's momentum is largely driven by younger demographics prioritizing fitness. For instance, in 2025, 73% of United Kingdom Gen Z respondents reported exercising at least twice weekly, marking an 11 percentage point increase from the previous year. Additionally, their monthly fitness expenditure rose to GBP 48.81 (USD 61), reflecting a 17% uptick[1]Source: The Gym Group, “Gen z fitness pulse report 2025: key findings,” thegymgroup.com.

Key Report Takeaways

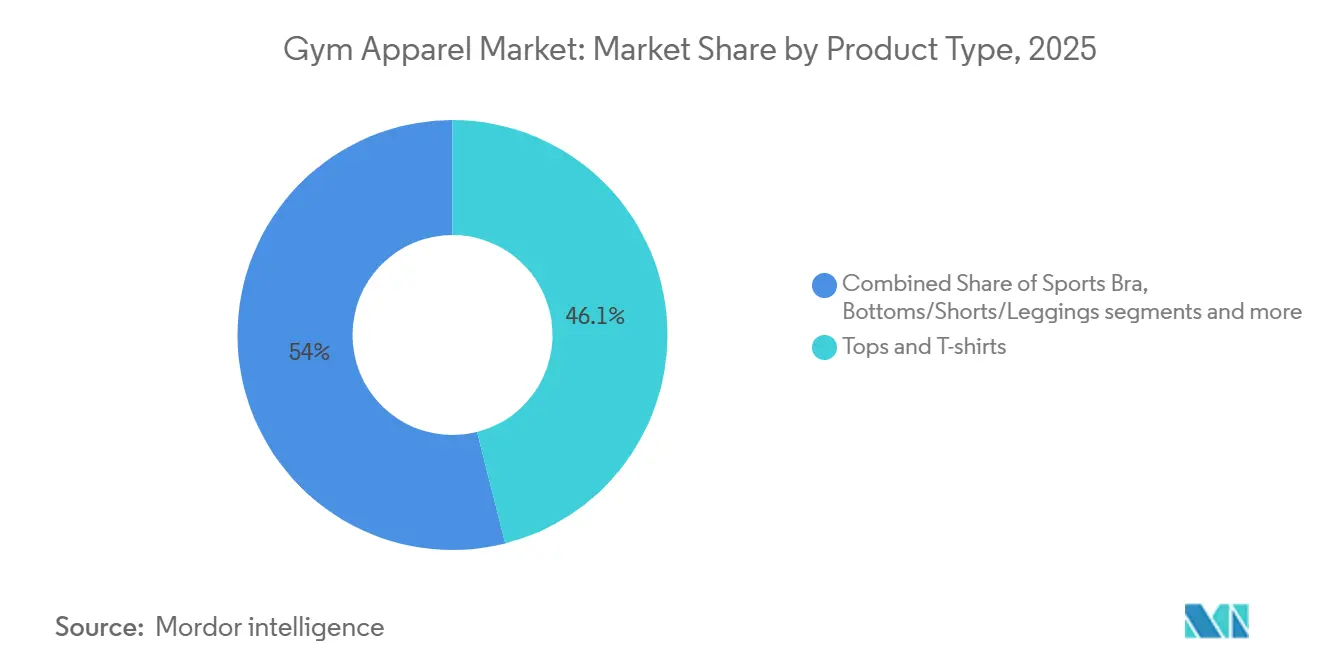

- By product type, tops and t-shirts captured 46.05% of the gym apparel market share in 2025, while sports bras are forecast to advance at an 8.33% CAGR through 2031.

- By end user, male consumers held 63.55% of the 2025 base, yet the female segment is projected to expand at a 7.31% CAGR between 2026-2031.

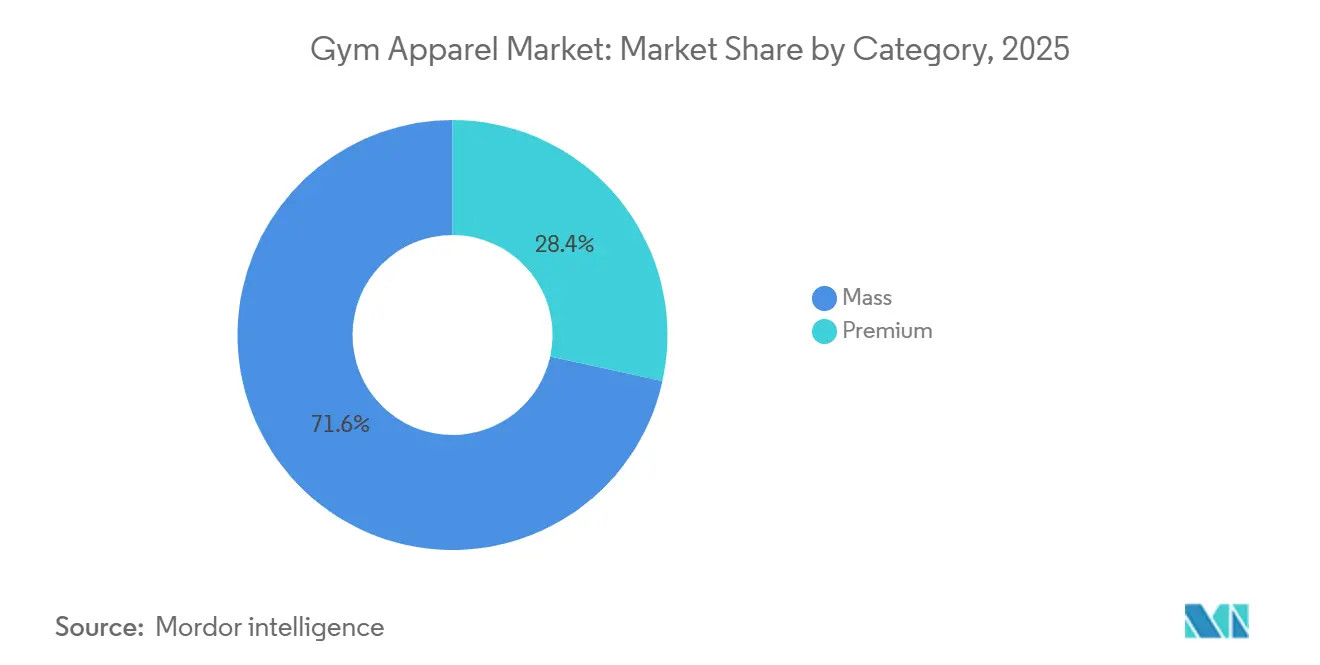

- By category, mass lines dominated with 71.56% of 2025 revenue, whereas the premium tier is anticipated to record a 7.72% CAGR over the same forecast window.

- By distribution channel, specialty stores led with 34.16% share in 2025; online retail is set to grow fastest at an 8.25% CAGR through 2031.

- By geography, North America accounted for 32.48% in 2025, but Asia-Pacific is expected to post the strongest regional growth at a 7.93% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Gym Apparel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of athleisure and lifestyle-wear trends | +1.2% | Global, with strongest adoption in North America, Western Europe, and urban China | Medium term (2-4 years) |

| Rising health and wellness awareness | +1.5% | Global, particularly Asia-Pacific (India, China) and South America | Long term (≥ 4 years) |

| Technological innovation in performance fabrics | +0.9% | Global, led by North America and Europe; rapid adoption in premium segments across Asia-Pacific | Medium term (2-4 years) |

| Growing youth participation in fitness activities | +1.3% | Global, with pronounced impact in Asia-Pacific, North America, and Middle East | Long term (≥ 4 years) |

| Inclusivity and body-positive positioning | +0.8% | North America, Western Europe, Australia; emerging in urban Asia-Pacific markets | Medium term (2-4 years) |

| Brand-centric marketing and collaborations | +0.7% | Global, with highest ROI in digitally mature markets (North America, Europe, East Asia) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growth of athleisure and lifestyle‑wear trends

Athleisure's transition from a niche segment to a mainstream category has transformed consumer purchase drivers, with a growing preference for versatile apparel suitable for workouts, remote work, and social settings. The convergence of performance and fashion in athleisure has enabled brands to justify premium pricing by combining technical fabrics with trend-focused designs. Purchases by Gen Z and millennials are heavily influenced by social media recommendations, highlighting the importance of digital discovery and influencer-driven trends in promoting athleisure adoption. Active consumers increasingly wear activewear for non-exercise occasions, such as staying at home, running errands, shopping, and socializing. This shift demonstrates that gym apparel has evolved into everyday wardrobe essentials rather than being limited to performance-specific use. This lifestyle-oriented positioning allows brands to achieve higher unit sales per customer and expand their addressable market to include casual exercisers and wellness-focused consumers in addition to dedicated athletes.

Rising health and wellness awareness

Increasing awareness of the risks associated with chronic diseases and the mental health benefits of physical activity is driving sedentary populations to adopt more active lifestyles, thereby expanding the market for gym apparel. This shift is largely influenced by the growing recognition of exercise as a key factor in preventing chronic illnesses such as obesity, diabetes, and cardiovascular diseases. Additionally, the emphasis on mental well-being has positioned physical activity as a critical tool for stress management and improving overall mental health. According to The Gym Group's 2025 United Kingdom survey, 87% of Gen Z respondents stated that working out improves or significantly improves mental health, while 65% identified regular exercise as the most effective method for enhancing mental well-being, surpassing healthy eating and digital wellness content[2]Source: The Gym Group, “Gen z fitness pulse report 2025: key findings,” thegymgroup.com. Government initiatives are further supporting this trend; for instance, China's August 2025 policy aims to grow the sports industry to over RMB 7 trillion by 2030[3]China Government Website, “Opinions of the General Office of the State Council on Unleashing the Potential of Sports Consumption and Further Promoting the High-Quality Development of the Sports Industry,” gov.cn. This growing focus on wellness is generating sustained demand for functional gym apparel designed to support a variety of activities, including strength training, yoga, running, and group fitness classes, each of which requires specialized fabrics and fits.

Technological innovation in performance fabrics

Fabric innovation plays a key role in differentiating premium products and supporting higher price points. Brands are incorporating features such as moisture-wicking, anti-microbial, sweat-concealing, and sustainable properties into gym apparel. In March 2026, Lululemon introduced ShowZero technology, designed to alter how light interacts with fabric, making sweat nearly invisible while maintaining breathability and a lightweight feel. This technology was developed through extensive laboratory and on-court testing in collaboration with professional tennis player Frances Tiafoe. Similarly, Teijin Frontier launched a multi-functional textile for the Spring/Summer 2027 season. This textile combines water-repellent and water-absorbent yarns on the skin-facing layer, along with UV protection, heat shielding, and reduced transparency. It targets the sportswear and outdoor markets, with sales targets of 150,000 meters in fiscal 2027 and 400,000 meters by fiscal 2029. These technical advancements allow brands to justify premium pricing while addressing consumer preferences for performance and environmental sustainability. Active consumers increasingly prioritize moisture management and odor resistance when purchasing activewear.

Growing youth participation in fitness activities

Youth participation in fitness activities is a key driver of the global gym apparel market, as younger consumers increasingly focus on health, aesthetics, and active lifestyles. Greater awareness of physical well-being, influenced by social media, fitness influencers, and digital workout platforms, has motivated individuals aged 18–35 to engage in gym workouts, sports, and outdoor activities. This trend is further supported by the growth of fitness centers, boutique studios, and community-based wellness programs, which have made exercise more accessible and socially engaging. Consequently, demand for stylish, functional, and performance-oriented gym apparel has increased, with younger consumers prioritizing comfort, durability, and fashion. Furthermore, the rising popularity of athleisure, where fitness wear is used for both exercise and casual settings, has boosted purchase frequency, contributing to sustained market growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of counterfeit and grey-market products | -0.6% | Global, with highest incidence in Asia-Pacific, South America, and online marketplaces | Short term (≤ 2 years) |

| Fast-changing fashion cycles and trend fatigue | -0.5% | North America, Western Europe, and urban Asia-Pacific; less pronounced in emerging markets | Medium term (2-4 years) |

| Fit and sizing inconsistency across brands | -0.3% | Global, with greater impact in e-commerce-heavy markets (North America, Europe, China) | Medium term (2-4 years) |

| Environmental impact of synthetic materials | -0.4% | Europe (regulatory pressure), North America, and Australia; emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of counterfeit and grey‑market products

The presence of counterfeit and grey-market products significantly restrains the global gym apparel market by compromising brand integrity and diminishing consumer trust. These unauthorized products, often sold at much lower prices through informal channels and online platforms, appeal to price-sensitive consumers but generally lack the quality, performance, and durability of authentic items. This situation adversely affects the revenue and profitability of established brands while posing challenges in maintaining consistent brand positioning and customer loyalty. Additionally, the widespread availability of counterfeit goods complicates supply chain oversight and increases the costs associated with enforcement and anti-counterfeiting measures for manufacturers. Consequently, legitimate market players face heightened competitive pressures and potential reputational harm, which collectively hinder overall market growth.

Fast‑changing fashion cycles and trend fatigue

Rapidly changing fashion cycles and increasing trend fatigue are restraining factors in the global gym apparel market, as they contribute to volatility in consumer demand and pressure brands to continuously innovate. Frequent shifts in styles, colors, and designs may lead consumers to delay purchases or show reduced interest in new collections, resulting in shorter product lifecycles and unpredictable sales patterns. This dynamic compels companies to expedite design and production processes, often leading to higher operational costs, surplus inventory, and markdown risks. Furthermore, constant exposure to evolving trends through digital platforms can overwhelm consumers, diminishing brand loyalty and making it challenging for companies to maintain long-term engagement. As a result, the need to adapt to rapidly changing trends can impact profitability and impede stable market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sports Bras Drive Technical Innovation

Tops and t-shirts accounted for 46.05% of the market share in 2025, driven by increasing demand for versatile, performance-oriented clothing suitable for both workouts and everyday use. The rise in fitness activity participation, particularly among urban consumers, has fueled the need for breathable, moisture-wicking, and stretchable tops such as t-shirts, tank tops, and hoodies. The growing popularity of athleisure has extended the use of topwear beyond gyms into casual and work-from-home wardrobes, leading to increased purchase frequency. Additionally, ongoing product innovations, including anti-odor fabrics, temperature regulation, and sustainable materials, have enhanced consumer appeal. Brand influence, celebrity endorsements, and social media trends also play a significant role in shaping consumer preferences, encouraging investments in stylish yet functional topwear.

Sports bras are projected to grow at a CAGR of 8.33% from 2026 to 2031, driven by increasing participation of women in fitness, sports, and wellness activities, alongside a broader focus on female empowerment and health awareness. As more women engage in activities such as running, yoga, and high-intensity training, the demand for supportive, comfortable, and well-fitted sports bras has risen significantly. Advances in fabric technology, including moisture management, seamless construction, and varying support levels tailored to different activities, have further boosted product adoption. Moreover, the growing acceptance of sports bras as standalone athleisure wear, particularly among younger consumers, has expanded their usage beyond workouts. Inclusive sizing, body positivity movements, and targeted marketing campaigns have also contributed to higher adoption, positioning sports bras as a rapidly growing segment within the global gym apparel market.

By End User: Female Segment Accelerates

Male consumers accounted for 63.55% of the gym apparel market in 2025, driven by increasing awareness of physical fitness, muscle building, and performance-oriented training. A growing number of men are participating in gym workouts, strength training, and sports activities, resulting in higher demand for durable, functional, and comfortable apparel. The influence of fitness culture, including bodybuilding trends, sports personalities, and digital fitness content, has further motivated men to invest in specialized gym wear. Additionally, rising disposable incomes and the shift toward athleisure have expanded the use of gym apparel beyond workouts into casual and everyday wear. Product innovations such as sweat-wicking fabrics, compression wear, and ergonomic designs enhance performance, supporting continued growth in this segment.

The female segment is projected to grow at a 7.31% CAGR from 2026 to 2031, driven by increasing health consciousness, greater participation in fitness activities, and the influence of wellness-focused lifestyles. More women are engaging in activities such as yoga, running, gym training, and group fitness classes, leading to higher demand for comfortable, stylish, and supportive apparel. The expansion of women-centric fitness programs, along with social media influence and body positivity movements, has encouraged greater adoption of gym wear. Furthermore, the popularity of athleisure has significantly contributed to growth, as women increasingly prefer versatile apparel that combines fashion and functionality for both active and casual use. Continuous innovation in fit, fabric, and inclusive sizing, along with targeted marketing by brands, further strengthens demand in the female segment.

By Category: Premium Segment Commands Margin

The mass category accounted for 71.56% of the market share in 2025, driven by factors such as affordability, wide accessibility, and increased fitness participation among middle- and lower-income consumer groups. As global health awareness rises, a significant number of consumers are joining gyms, engaging in home workouts, or adopting active lifestyles, leading to strong demand for cost-effective gym apparel. Value-oriented brands, private labels, and e-commerce platforms have enhanced accessibility through competitive pricing, frequent discounts, and extensive product availability. Additionally, fast fashion brands are entering the activewear market, offering trendy designs at lower price points, which appeal to price-sensitive consumers. The growing popularity of athleisure as everyday wear further drives repeat purchases in this segment, supporting volume-driven growth.

The premium segment is projected to grow at a CAGR of 7.72% from 2026 to 2031, fueled by rising disposable incomes, increasing brand consciousness, and growing demand for high-performance and aesthetically appealing gym apparel. Consumers in this segment prioritize quality, advanced fabric technologies, and superior fit, often seeking features such as moisture management, durability, and ergonomic design. Global fitness trends, celebrity endorsements, and aspirational branding further encourage customers to invest in premium products that reflect their lifestyle and status. Additionally, innovations in sustainable materials, smart textiles, and limited-edition collections enhance product differentiation and perceived value. The expansion of boutique fitness studios and personalized wellness experiences also supports premium apparel consumption, reinforcing growth in this segment.

By Distribution Channel: Online Retail Surges

Specialty stores accounted for 34.16% of the distribution share in 2025, driven by the demand for personalized shopping experiences and expert guidance. These stores are preferred by consumers for their curated product selections, trained staff, and the opportunity to evaluate fit, comfort, and fabric quality before purchasing, particularly for performance-oriented apparel. Specialty retailers enhance brand credibility by offering authentic products, exclusive collections, and access to the latest innovations. Additionally, in-store experiences such as product trials, fitness consultations, and community engagement activities foster customer loyalty and encourage repeat purchases. These attributes make specialty stores especially attractive to fitness enthusiasts who prioritize quality and informed purchasing decisions.

Online retail is projected to grow at a CAGR of 8.25% from 2026 to 2031, driven by convenience, broader product availability, and competitive pricing. Consumers increasingly favor digital platforms for their ability to browse multiple brands, compare prices, and read customer reviews before making a purchase. The growth of mobile commerce, fast delivery options, and hassle-free return policies has further accelerated online adoption. Moreover, targeted digital marketing, influencer collaborations, and personalized recommendations enhance consumer engagement and encourage impulse purchases. The expansion of direct-to-consumer strategies by brands, along with frequent online discounts and exclusive product launches, also supports robust growth in this channel, positioning it as a significant driver of overall market expansion.

Geography Analysis

North America accounted for 32.48% of the global gym apparel market in 2025, driven by a well-established fitness culture, high consumer spending power, and widespread adoption of athleisure. A significant portion of the population actively engages in gym workouts, sports, and wellness programs, supported by extensive access to fitness centers and digital training platforms. Consumers in the region prioritize performance, comfort, and brand value, fueling demand for technologically advanced fabrics and premium products. Additionally, the strong presence of leading global brands, frequent product innovations, and the influence of fitness influencers and celebrity endorsements continue to shape purchasing behavior and sustain market growth.

The Asia-Pacific region is projected to grow at a CAGR of 7.93% from 2026 to 2031, driven by rapid urbanization, rising disposable incomes, and increasing health awareness among a large and youthful population. Greater exposure to global fitness trends through social media and digital platforms has encouraged more individuals to adopt active lifestyles, particularly in countries such as China, India, and Southeast Asian nations. The expansion of affordable gyms, fitness apps, and organized sports activities has further boosted participation. While price sensitivity in several markets supports the growth of mass and mid-range segments, the emerging middle class is driving demand for branded and premium gym apparel, creating a balanced growth environment.

In Europe, South America, and the Middle East and Africa, the gym apparel market is supported by lifestyle changes, increasing fitness awareness, and the gradual expansion of organized retail and fitness infrastructure. Europe benefits from mature markets with high participation in sports and outdoor activities, along with a preference for sustainable and high-quality apparel. South America is experiencing growth due to rising urban populations and growing interest in fitness and body wellness, despite economic fluctuations. In the Middle East and Africa, steady adoption is driven by improving health consciousness, government initiatives promoting active lifestyles, and the growing presence of international and regional brands. Across these regions, the rising influence of athleisure and digital retail channels further contributes to market expansion.

Competitive Landscape

The global gym apparel market is moderately concentrated, with Nike and Adidas maintaining leading positions while facing growing competition from emerging and specialized players. This competitive environment is shaped by newer entrants capturing consumer attention through targeted offerings and distinct brand identities. Established brands benefit from extensive distribution networks, strong brand recognition, and diverse product portfolios, while niche players gain momentum by aligning with shifting consumer preferences, particularly in performance, style, and lifestyle integration.

Competitive strategies within the market reveal distinct approaches. Established companies leverage scale-driven models, utilizing wholesale distribution, large-format retail presence, and strategic partnerships to sustain visibility and sales volume. Conversely, emerging brands focus on direct consumer engagement through digital-first channels, community-driven marketing, and immersive retail experiences. Product innovation remains a critical area of competition, with investments in advanced materials, functional designs, and performance-focused features aimed at supporting premium positioning and fostering customer loyalty.

Growth opportunities are evident in underpenetrated segments such as inclusive sizing, specialized support apparel, modest activewear, and products designed for older consumers. Brands addressing these gaps through technical innovation and thoughtful design are better positioned to achieve higher margins and stand out in the market. Additionally, the adoption of technologies like supply chain tracking, authentication tools, and data-driven personalization is enhancing transparency and combating counterfeit products. Increased involvement from financial stakeholders is also shaping strategic priorities, driving a stronger emphasis on profitability, operational efficiency, and long-term value creation in this evolving market landscape.

Gym Apparel Industry Leaders

Nike Inc.

Adidas AG

Lululemon Athletica Inc.

Puma SE

Under Armour Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Lululemon introduced ShowZero sweat-concealing technology, designed to modify how light interacts with fabric, making sweat nearly invisible while preserving breathability and a lightweight feel. This innovation was developed through comprehensive laboratory and on-court testing in collaboration with professional tennis player Frances Tiafoe and was showcased in his custom kit at the BNP Paribas Open.

- June 2025: Gym Shark made its debut with the "Onyx" collection in Australia. This launch marked the company's effort to expand its product portfolio and strengthen its presence in the Australian activewear market.

- February 2025: Nike teamed up with Skims to unveil a fresh line of gym apparel under the collaborative brand name, NikeSKIMS. This partnership aims to deliver a diverse range of activewear, primarily targeting the U.S. market and beyond, with a focus on combining functionality and style to cater to a wide audience.

- February 2025: Lululemon introduced its "Glow Up" collection, featuring women's activewear staples like leggings, a tank top, and a onesie. This collection highlights the brand's commitment to innovation and meeting the evolving preferences of its female customer base.

- February 2025: Adidas rolled out its premium activewear line, dubbed "A-Type," showcasing a selection of tracksuits, tops, and bottoms. The A-Type collection reflects Adidas' strategy to target the premium segment of the activewear market by offering high-quality and stylish products.

Global Gym Apparel Market Report Scope

| Tops and T-shirts |

| Bottoms/ShortsLeggings |

| Sports Bra |

| Others |

| Male |

| Female |

| Mass |

| Premium |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| United Arab Emirates | |

| Nigeria | |

| Morocco | |

| Egypt | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Tops and T-shirts | |

| Bottoms/ShortsLeggings | ||

| Sports Bra | ||

| Others | ||

| By End User | Male | |

| Female | ||

| By Category | Mass | |

| Premium | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| United Arab Emirates | ||

| Nigeria | ||

| Morocco | ||

| Egypt | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected value of the gym apparel market by 2031?

The gym apparel market is projected to reach USD 163.61 billion by 2031, advancing at a 7.13% CAGR from 2026-2031.

Which product segment will expand fastest through 2031?

Sports bras lead with an 8.33% forecast CAGR, driven by inclusive sizing and high-impact support innovations.

Which region shows the strongest growth potential?

Asia-Pacific is set to post the quickest regional rise at a 7.93% CAGR.

How large is the premium share within gym apparel?

Premium lines accounted for 28.44% of 2025 revenue and are forecast to grow at 7.72% CAGR, outpacing the mass tier.

Page last updated on: