Sports Shoes Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

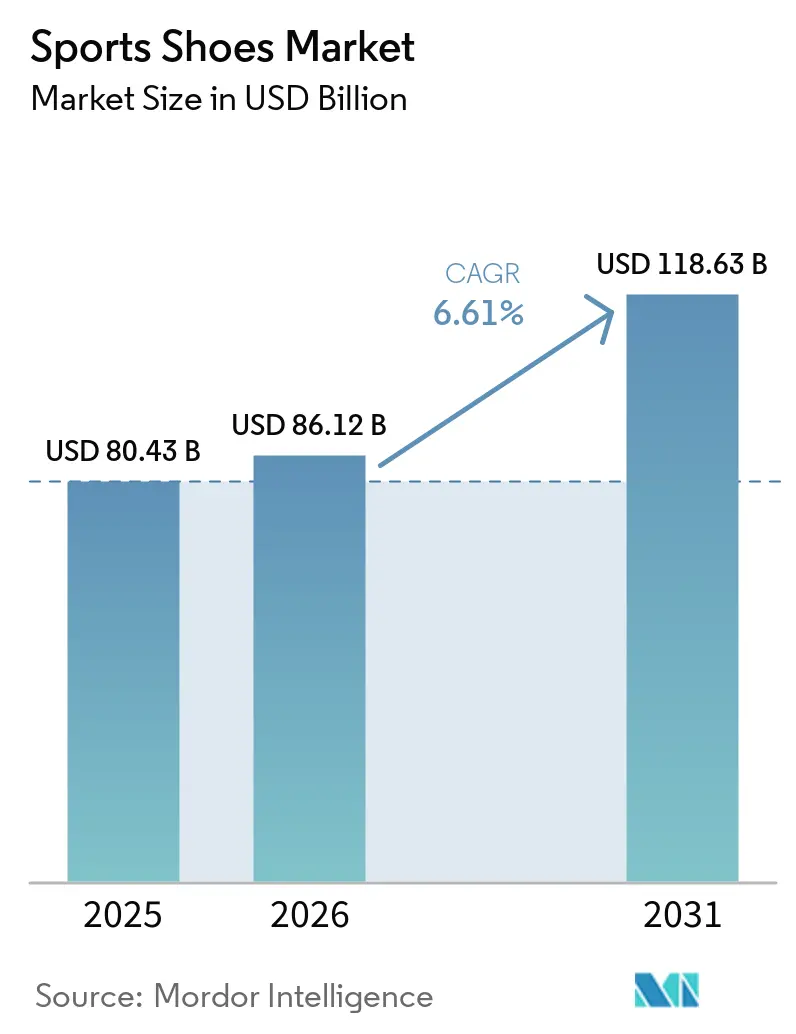

| Market Size (2026) | USD 86.12 Billion |

| Market Size (2031) | USD 118.63 Billion |

| Growth Rate (2026 - 2031) | 6.61% CAGR |

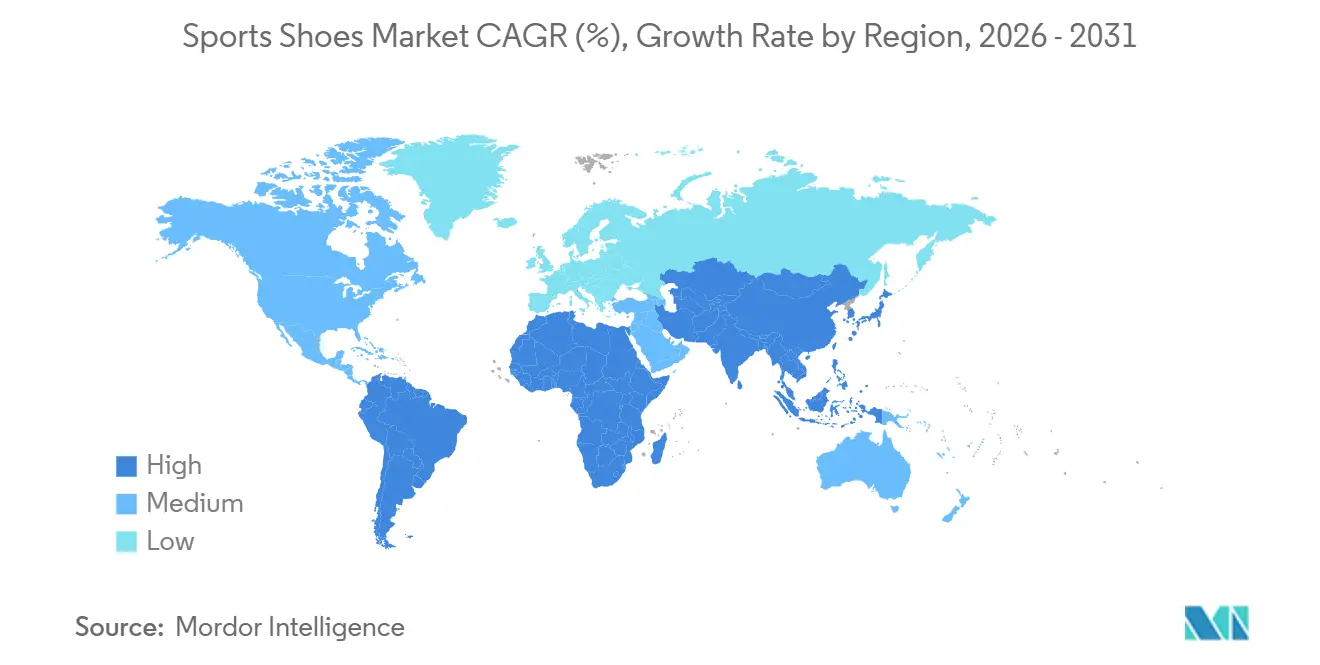

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

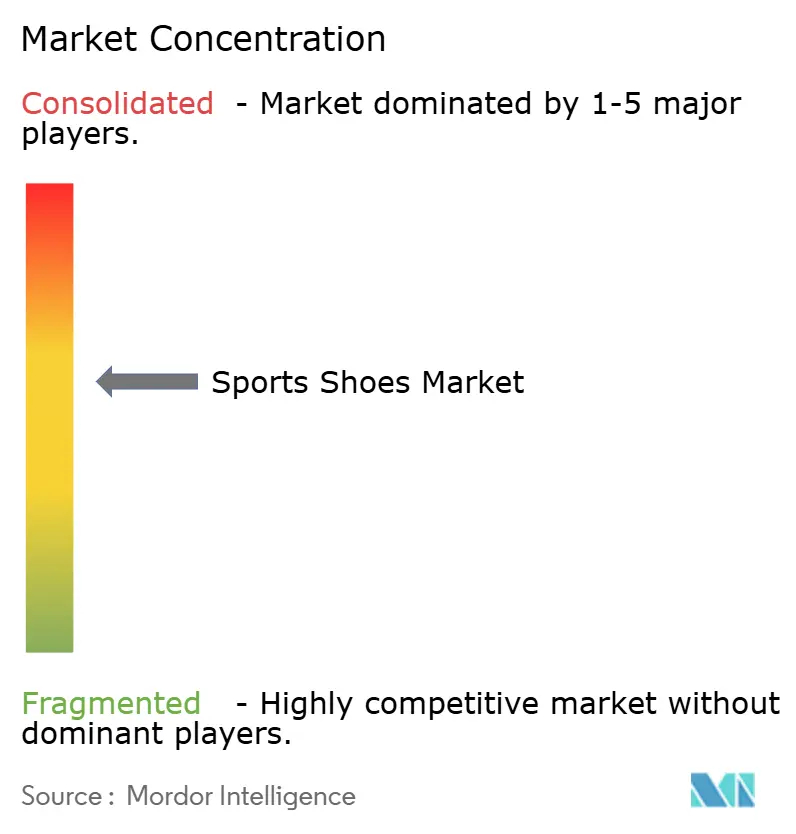

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sports Shoes Market Analysis by Mordor Intelligence

The sports shoes market size was valued at USD 80.43 billion in 2025 and is estimated to grow from USD 86.12 billion in 2026 to reach USD 118.63 billion by 2031, at a CAGR of 6.61% during the forecast period (2026-2031). Sustained expansion in the sports shoes market stems from higher global participation in running, wider use of AI-enabled virtual-fit tools that trim online return rates, and the mass adoption of carbon-plated “super-shoes” that deliver verifiable performance gains. Health agencies and corporate wellness programs are normalizing mileage-based fitness routines, while the convergence of athletic and lifestyle fashion keeps technical sneakers in everyday rotations. Challenger brands thrive by capitalizing on direct-to-consumer (DTC) models and agile product drops, even as incumbents accelerate research and development around lightweight foams, bio-based midsoles, and circular design. Regionally, the sports shoes market is pivoting toward Asia-Pacific, where rising disposable incomes and digital retail penetration underpin premium uptake.

Key Report Takeaways

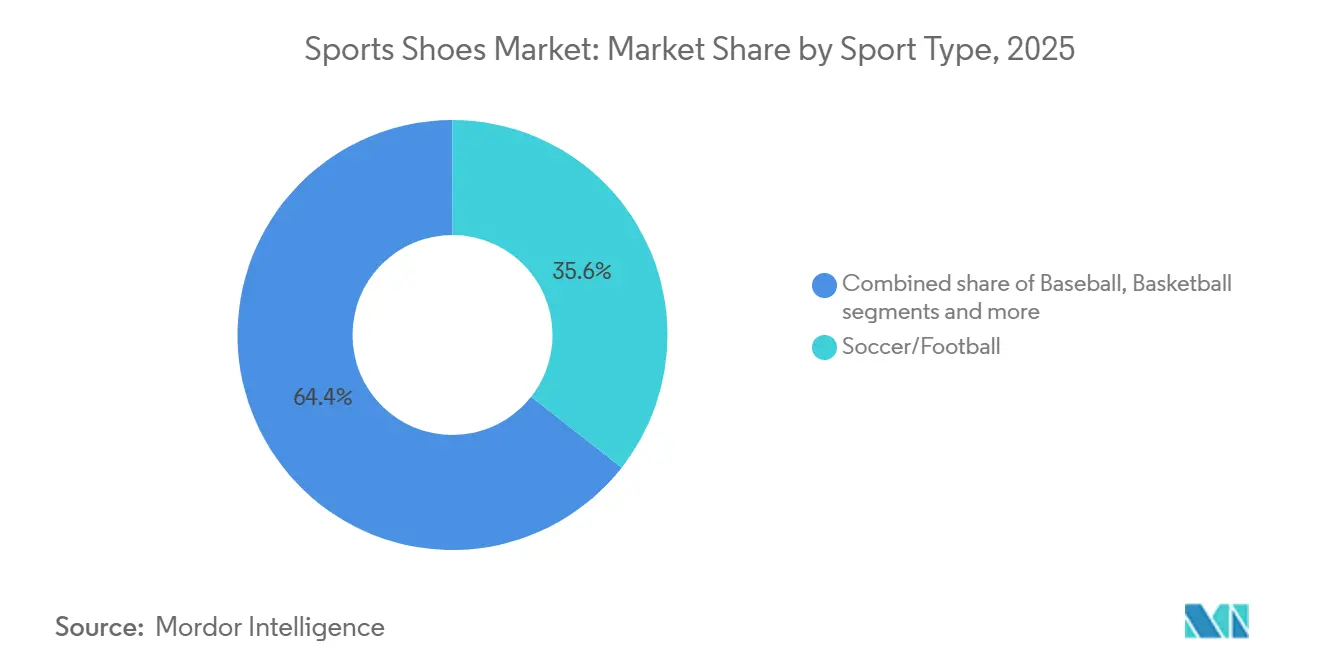

- By sport type, Soccer/Football footwear led with 35.59% of the sports shoes market share in 2025, whereas basketball shoes are forecasted to grow at a 7.08% CAGR through 2031.

- By end user, Men accounted for 61.69% of the sports shoes market share in 2025, while the kids segment is expected to expand at a 6.97% CAGR through 2031.

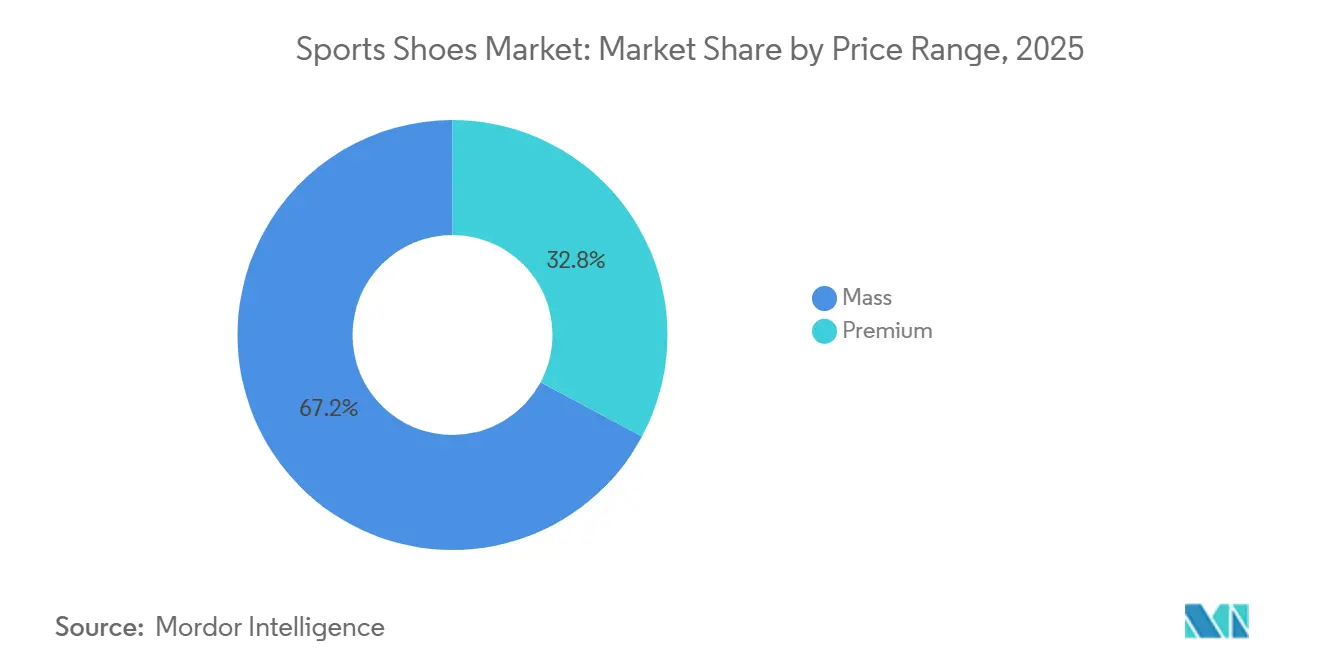

- By price range, Mass-market shoes captured 67.18% of 2025 revenue, but the premium tier is projected to grow at a 7.17% CAGR through 2031 on the back of carbon-fiber race models.

- By distribution, Sports and Athletic Goods Stores held a 35.72% share in 2025, yet online retail stores are anticipated to advance at the highest 7.81% CAGR through 2031 as brands deepen omnichannel investments.

- Geographically, North America controlled 40.40% of 2025 turnover, while Asia-Pacific is predicted to outstrip all regions with a 7.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sports Shoes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health and fitness awareness | +1.2% | Global, with pronounced gains in Asia-Pacific urban centers and North America's suburbs | Medium term (2-4 years) |

| E-commerce and DTC channel expansion | +1.5% | Global, led by North America and Europe; accelerating in Asia-Pacific tier-2 cities | Short term (≤ 2 years) |

| Athleisure blurring performance and lifestyle | +0.9% | North America, Europe, and the Asia-Pacific metropolitan areas | Medium term (2-4 years) |

| Carbon-plated super-shoes reach mass runners | +0.7% | North America and Europe core; spillover to the Asia-Pacific affluent segments | Short term (≤ 2 years) |

| AI-driven virtual-fit tools are lifting online conversions | +0.6% | Global e-commerce channels are strongest in North America and Europe | Short term (≤ 2 years) |

| City-level run clubs triggering premium drop cycles | +0.5% | Urban centers in North America, Europe, and select Asia-Pacific cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Health and Fitness Awareness

Post-pandemic, running has solidified its status as a primary fitness activity. This shift has led to a surge in gym memberships among women, spurring innovations in female-specific footwear that seamlessly marry technical performance with style. With governments and health organizations championing active lifestyles, there's a consistent demand for both entry-level and high-performance running shoes. This trend is especially evident in the Asia-Pacific region. Here, urbanization and increasing disposable incomes are broadening the market. ASICS, for instance, anticipates a 35% annual growth in India and is setting its sights on dominating running-shoe sales by 2029, eyeing a market projected to hit USD 4.8 billion by 2033. In response, brands are unveiling models tailored to the region, striking a balance between affordability and advanced features. This ensures that health-conscious consumers, regardless of their income bracket, can access high-performance footwear. Such democratization of technology is not only shortening product cycles but also heightening competition in the mass-market arena.

E-commerce and DTC Channel Expansion

Major brands are increasingly turning to direct-to-consumer (DTC) strategies as their main growth engine. In 2025, Adidas highlighted a 14-16% growth in its DTC segment and is now emphasizing omnichannel integration to boost its profit margins[1]Source: Adidas AG, “Direct-to-Consumer Strategy Update 2026,” adidas-group.com . Projections indicate that online retail stores will grow at a 7.81% CAGR through 2031, surpassing traditional retail channels. This growth is driven by brands pouring investments into their own e-commerce platforms, offering perks like exclusive colorways, early product releases, and subscription services. The economic rationale behind this shift is clear: DTC channels sidestep wholesale markdowns, grant access to direct consumer data, and allow for flexible pricing. Yet, the journey isn't smooth for everyone. In 2025, Nike grappled with DTC hurdles while adjusting its wholesale partnerships, underscoring that strong brand equity doesn't always smooth out distribution challenges. Meanwhile, smaller brands and regional players are seizing the moment. They're collaborating with third-party platforms and harnessing social commerce to connect with consumers under 35. This demographic, which constitutes two-thirds of the adult running shoe market growth, heavily relies on social media for brand discovery.

Athleisure Blurring Performance and Lifestyle

Running shoes, once purely functional, have evolved into essential lifestyle items. As athleisure apparel gained momentum in 2025, it naturally pulled footwear along. Seizing this opportunity, Adidas, in 2026, branded its running shoes as both performance-driven and fashion-forward, allowing users to fluidly transition from track to street. This blend is particularly evident in the premium and mid-tier markets. Here, brands craft shoes featuring technical midsoles paired with versatile uppers, catering to consumers who appreciate both functionality and aesthetics. While this trend broadens the market by drawing in non-athletes who prioritize comfort and style, it also poses a risk: potential brand dilution if technical credibility wanes. To navigate this landscape, successful brands are adopting a dual approach: maintaining separate product lines for serious runners and lifestyle enthusiasts, ensuring they cater to diverse consumer segments without compromising their brand essence.

Carbon-Plated Super-Shoes Reach Mass Runners

Once the domain of elite marathoners, carbon-fiber plates have now entered the mainstream. At the 2025 Chicago and New York City marathons, participants donned "super-shoes" boasting 4-6% enhancements in running economy. Brands have made this cutting-edge technology accessible, introducing models priced between USD 200-300, a significant drop from the USD 500 tag of exclusive releases like the Adidas Adios Pro Evo 2. Studies validate the performance boost, highlighting a 2-4% efficiency uptick, which has ignited a fresh upgrade cycle among recreational runners chasing these incremental benefits. Yet, with the technology's lifespan capped at 150-250 miles, the frequent need for replacements not only favors brands but also tightens consumer wallets. In a nod to the industry's future, Puma has teamed up with Chinese materials expert Shincell, hinting that the forthcoming innovations will prioritize durability and sustainability, in addition to performance, on its NITRO foam platform[2]Source: Puma SE, “Puma and Shincell Announce NITRO Lab Partnership,” puma.com .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and grey-market proliferation | -0.8% | Global, with acute challenges in the Asia-Pacific and emerging markets | Long term (≥ 4 years) |

| Raw-material cost volatility (EVA, rubber) | -0.6% | Global, with the highest exposure in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Microplastic midsole scrutiny and regulation risk | -0.4% | Europe (REACH), North America (California DTSC), and emerging in the Asia-Pacific | Medium term (2-4 years) |

| The booming resale segment is cannibalizing new-shoe sales | -0.7% | North America and Europe core; expanding to Asia-Pacific urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Counterfeit and Grey-Market Proliferation

Counterfeit sports shoes not only undermine brand equity but also diminish pricing power. Seizures, such as the Philippines' USD 2.69 million haul in 2025, represent just a fraction of the broader illicit trade, as highlighted by the Philippines Counterfeit[3]Source: Bureau of Customs “Counterfeit sports shoes seizures”, customs.gov.ph. Grey-market channels further complicate brand positioning by selling authentic, yet diverted, inventory below authorized prices, thereby eroding margins. This challenge is especially pronounced in the Asia-Pacific region, where fragmented distribution networks and e-commerce marketplaces often shield unauthorized sellers. In response, brands are adopting measures like blockchain-based authentication, serialized product codes, and collaborations with platforms such as StockX, which verify authenticity prior to resale. Despite these efforts, enforcement remains sporadic. With premium shoes retailing between USD 250-500, the economic allure for counterfeiters is undeniable, underscoring the need for coordinated regulatory action to combat the issue effectively.

Raw-Material Cost Volatility (EVA, Rubber)

In 2024-2026, prices for ethylene vinyl acetate (EVA) and rubber, which make up over 65% of athletic footwear midsoles and outsoles, saw notable fluctuations. EVA prices swung between USD 1,500 and 2,100 per ton, with regional spreads ranging from USD 1.39 to 2.23 per kilogram, as reported by EVA Pricing. These price shifts, largely driven by feedstock changes linked to crude oil and natural gas, have tightened margins for brands. Many of these brands find it challenging to transfer these costs to consumers without jeopardizing their sales volume. The most affected are mass-market segments, where consumers are more price-sensitive, and smaller brands that don't have the luxury of hedging. To counteract these challenges, brands are diversifying their suppliers, exploring alternative materials such as bio-based foams, and entering into long-term contracts. However, these strategies often demand significant capital and scale, giving larger, established brands an edge over newer entrants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sport Type: Basketball Surges on Signature-Line Momentum

In 2025, soccer/football footwear commanded a 35.59% market share, with Firm Ground cleats leading the segment at 38%. These cleats reaped rewards from global participation rates and sponsorships in professional leagues. Meanwhile, basketball shoes are set to outpace the competition, projected to grow at a 7.08% CAGR through 2031. This surge is fueled by a blend of performance and lifestyle, allowing signature athlete lines, most notably Nike's Kobe series, which accounted for 37% of signature shoe sales in 2025, to evolve from mere court essentials to coveted streetwear. The segment's growth is bolstered by brands' strategic investments in athlete endorsements, cutting-edge technology platforms like Nike's Zoom Air and Adidas' Boost, and timely colorway releases that spark social media conversations and spur impulse buys.

Tennis footwear carves out a steady niche, with advancements in lateral stability and durability resonating with both recreational and competitive players. Baseball cleats, on the other hand, cater to a focused North American audience, offering metal and molded studs tailored for varying playing surfaces. The "Other Sports Type" category, which includes training, walking, and cross-training shoes, is riding the wave of the athleisure trend. Consumers are increasingly drawn to versatile footwear that seamlessly transitions between activities. Furthermore, the carbon-plated technology, which has already made waves in running, is now being explored in basketball and training. Brands are experimenting with plate geometries aimed at boosting vertical leaps and lateral agility, hinting at a potential new performance benchmark that could command premium pricing across all sports.

By End User: Kids Segment Accelerates on Youth Participation

In 2025, men's sports shoes dominate the market with a commanding 61.69% share. This stronghold is buoyed by rising average selling prices and a trend of frequent replacements, driven by both athletic pursuits and lifestyle choices. The kids' segment is on a robust trajectory, growing at a 6.97% CAGR. This growth is fueled by parents' dedication to youth sports and a heightened awareness of the significance of quality footwear in child development and injury prevention. Meanwhile, women's sports shoes are emerging as a lucrative frontier. Brands are now tailoring gender-specific technologies and designs to cater to distinct biomechanical needs and aesthetic preferences.

The rapid expansion of the kids' segment is further amplified by the surge in organized youth sports. Parents are increasingly willing to invest in premium sports shoes for their aspiring young athletes. This trend is underscored by New Balance's strategic long-term partnership with the WNBA, highlighting brands' intensified focus on women's sports. Their aim is clear: to capitalize on the rising female participation and viewership. Moreover, the fusion of performance and fashion in women's sports shoes has given rise to new product categories. These cater to both athletic pursuits and lifestyle choices, significantly expanding market opportunities.

By Price Range: Premium Gains Share on Technology Differentiation

In 2025, mass market shoes command a dominant 67.18% share of the market. This segment thrives on consumers' focus on accessibility, functionality, and competitive pricing. Catering to a diverse group of value-conscious buyers, mass market footwear provides reliable athletic options for everyday use. Brands emphasize durability and essential performance features, all while maintaining affordability. This approach cements mass-market shoes as the global consumer favorite.

On the other hand, the premium shoes segment, though smaller in volume, is charting a robust growth path, projected to expand at a 7.17% CAGR through 2030. This growth is driven by material innovations, the adoption of smart technologies, and exclusive product launches. Such developments appeal to consumers who value enhanced performance and sustainability. In developed markets, premium buyers prioritize quality craftsmanship, brand prestige, and eco-friendly practices. They're also more willing to invest in footwear that aligns with their lifestyle values. As a result, premium brands are expanding their allure by blending cutting-edge features with aspirational branding. In a strategic move, mass market players are rolling out selective premium offerings, targeting consumers with rising purchasing power and heightened expectations.

By Distribution Channel: Online Retail Captures Omnichannel Shift

In 2025, Sports and Athletic Goods Stores held onto a 35.72% distribution share, leveraging in-person fitting services, product trials, and expert staff guidance, elements deemed essential by performance-driven consumers. Meanwhile, Online Retail Stores are projected to experience a surge, boasting a 7.81% CAGR through 2031. This growth is fueled by brand investments in direct-to-consumer (DTC) platforms, AI-enhanced virtual fitting tools, and exclusive online product launches. Adidas, in 2025, highlighted a 14-16% growth in its DTC segment, emphasizing an omnichannel strategy that empowers consumers to research online, try products in-store, and purchase through their chosen medium. This economic shift towards DTC channels is enticing; they sidestep wholesale markdowns, offer direct insights into consumer behavior, and allow for dynamic pricing. However, this transition demands hefty investments in technology, logistics, and customer service, an endeavor that poses challenges for smaller brands.

Supermarkets and hypermarkets target the mass market with value-driven offerings and impulse buys. In contrast, other distribution avenues, like specialty boutiques and brand flagship stores, cater to premium consumers, emphasizing curated selections and experiential shopping. While the COVID-19 pandemic acted as a catalyst for e-commerce adoption, subsequent data indicate that these behavioral changes are here to stay. Brands that adeptly navigate the economics of omnichannel, harmonizing online ease with in-store experiences, stand poised to reap significant rewards as the distribution landscape becomes increasingly fragmented.

Geography Analysis

In 2025, North America commands a dominant 40.40% market share, buoyed by its rich sports culture, affluent consumers, and a penchant for premium sports shoes. The region's established market sees frequent product updates, unwavering brand loyalty, and a retail landscape that adeptly melds traditional and online shopping. Yet, as saturation tightens its grip and economic uncertainties make consumers more price-sensitive, growth has begun to decelerate. In response, brands are honing in on premiumization, innovative footwear technologies, and eco-friendly materials to maintain their edge and pricing authority.

Asia-Pacific is on the fast track, eyeing a robust CAGR of 7.82% up to 2031. This surge is powered by rising incomes, a burgeoning middle class, and an uptick in sports participation, especially in China and India. Bolstered by government initiatives championing sports and infrastructure, the region is laying a solid groundwork for sustained demand. With health consciousness on the rise and digital platforms like social media amplifying the message, the Asia-Pacific region is cementing its status as a pivotal growth hub in the global sports shoes arena.

Europe, while mature, enjoys steady growth, owing to its ingrained sports culture, a heightened focus on sustainability, and a penchant for premium brands. Initiatives like UEFA’s Women’s Football Development Program are not only broadening participation but also birthing new consumer segments. With a keen eye on sustainability, Europe is pushing boundaries in eco-friendly materials and circular economy practices. Companies like ASICS are at the forefront, unveiling fully recyclable footwear to align with shifting consumer desires and regulatory standards. Meanwhile, South America and the Middle East and Africa, with their burgeoning middle classes, urbanization trends, and a rising sports enthusiasm, are emerging as promising markets. As these regions bolster their retail frameworks and adopt localized brand strategies, they're poised for significant growth in the global sports shoes landscape.

Competitive Landscape

The sports shoes market is moderately consolidated, with well-known brands like Nike, Adidas, and Puma holding strong positions due to their trusted brand image, innovation, and widespread global distribution networks. However, the competitive landscape is changing quickly as newer brands like On and Hoka, along with direct-to-consumer startups, gain popularity by offering specialized products and advanced technologies. Even the biggest players are facing challenges as consumer preferences shift, demand grows for niche and performance-specific products, and competition increases from more agile newcomers. This trend toward specialized performance brands catering to specific sports and consumer groups is opening doors for smaller, focused competitors to challenge the established leaders.

Key industry trends include a growing focus on direct-to-consumer channels, with Puma reporting a 12% increase in DTC sales in Q1 2025. This strategy helps brands improve profit margins and build stronger connections with customers. Additionally, technology is becoming a major factor, with companies using AI-driven design, 3D printing, and smart footwear innovations to enhance product development and performance. These advancements are helping brands stay relevant in a fast-changing market.

The industry is also seeing significant consolidation, with major deals like 3G Capital’s USD 9.4 billion acquisition of Skechers. These acquisitions are part of strategic efforts to expand operations and strengthen market positions. Sustainability is becoming increasingly important for staying competitive, with companies like Dow introducing low-carbon materials and BASF creating fully recyclable synthetic leather solutions. These efforts align with growing consumer and regulatory demands for environmentally friendly products.

Sports Shoes Industry Leaders

Nike Inc.

Adidas AG

Puma SE

New Balance Athletics Inc.

Skechers USA, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Puma announced a strategic partnership with Chinese materials specialist Shincell to establish a dedicated R&D laboratory in Suzhou, China, focused on evolving the NITRO running foam platform through physical foaming processes that create micro- and nano-bubbles, targeting lighter and more responsive midsoles for upcoming footwear seasons.

- May 2025: 3G Capital has acquired Skechers, the world’s third-largest footwear brand, signifying a significant milestone for the comfort-focused company. With annual sales of USD 9 billion, Skechers is set to enhance its global presence by investing in direct-to-consumer channels, innovation, and infrastructure. Both organizations regard this partnership as a strategic alignment aimed at achieving long-term growth.

- May 2025: In a strategic move, Dick's Sporting Goods has purchased Foot Locker for a hefty USD 2.4 billion. This acquisition not only bolsters Dick's presence in the global sneakers arena but also paves the way for its inaugural foray into international markets. With this expansion into new U.S. locales and a global footprint, the unified entity is poised for sustained growth, riding the wave of robust industry momentum.

Global Sports Shoes Market Report Scope

| Baseball |

| Basketball |

| Soccer/Football |

| Tennis |

| Other Sports Type |

| Men |

| Women |

| Kids |

| Mass |

| Premium |

| Supermarkets/Hypermarkets |

| Sports and Athletic Good Stores |

| Online Retail Stores |

| Other Distribution channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Sport Type | Baseball | |

| Basketball | ||

| Soccer/Football | ||

| Tennis | ||

| Other Sports Type | ||

| End User | Men | |

| Women | ||

| Kids | ||

| Price Range | Mass | |

| Premium | ||

| Distribution Channels | Supermarkets/Hypermarkets | |

| Sports and Athletic Good Stores | ||

| Online Retail Stores | ||

| Other Distribution channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the sports shoes market?

The sports shoes market size was valued at USD 80.43 billion in 2025 and is estimated to grow from USD 86.12 billion in 2026 to reach USD 118.63 billion by 2031, at a CAGR of 6.61% during the forecast period.

Which region leads the sports shoes market and which is growing fastest?

Geographically, North America controlled 40.40% of 2025 turnover; Asia-Pacific will outstrip all regions with a 7.82% CAGR.

How is e-commerce influencing category performance?

Online channels are expanding at 7.81% CAGR and now facilitate the majority of global footwear purchases, driven by virtual fitting tools and direct-to-consumer strategies.

How are brands addressing sustainability expectations?

Companies are introducing recyclable materials, bio-based foams and circular design processes while setting time-bound targets for reduced carbon footprints.

Page last updated on: