Modular Furniture Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 91.60 Billion |

| Market Size (2031) | USD 127.88 Billion |

| Growth Rate (2026 - 2031) | 6.90% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Modular Furniture Market Analysis by Mordor Intelligence

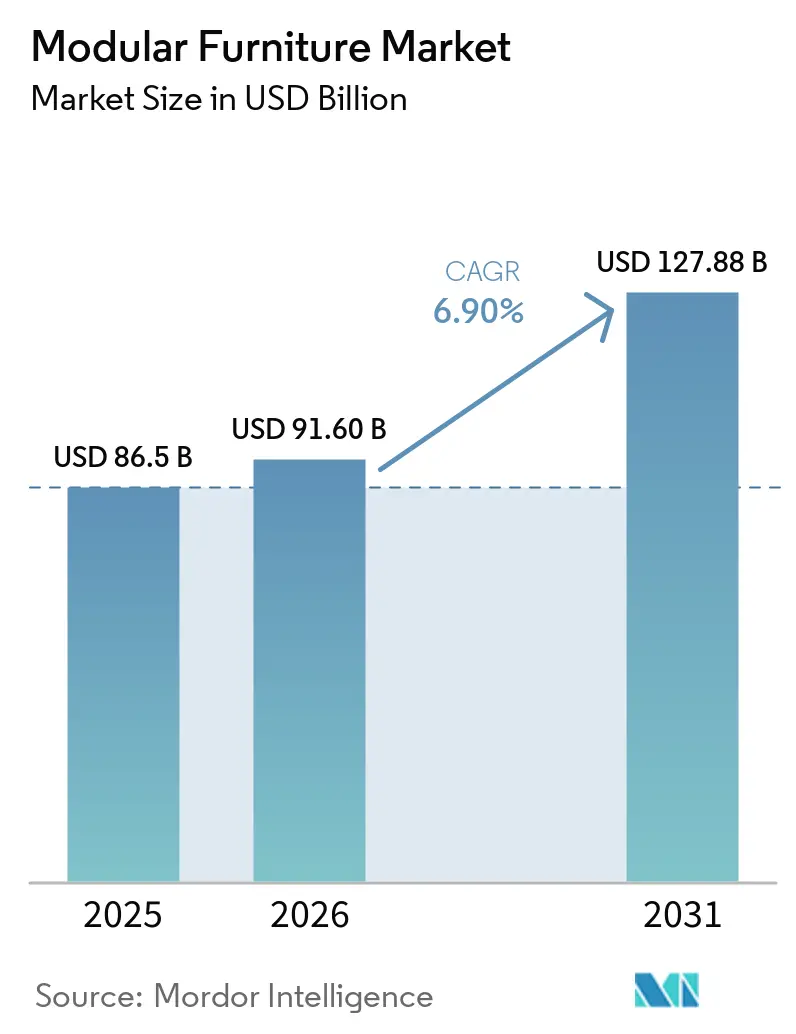

The modular furniture market size is projected to expand from USD 86.5 billion in 2025 and USD 91.6 billion in 2026 to USD 127.9 billion by 2031, registering a CAGR of 6.9% between 2026 and 2031. This pace is above the 5.9% growth recorded from 2020 to 2025. It shows that the modular furniture market is entering a faster phase as housing patterns, office use, and sustainability rules change together. Hybrid work continues to support demand, with JLL reporting that employees attending the office 3 to 4 days per week rose 19 percentage points year over year to 55% in 2026, which is pushing employers toward layouts that can be adjusted without major fit-out waste. Smaller urban homes are reinforcing the same shift, with NAIOP noting in October 2025 that apartments built in the last decade were 30 square feet smaller than those from the prior decade, which supports compact and multi-use designs across the modular furniture market[1]"NAIOP, “Shrinking Apartments and Surging Storage: America’s Construction Boom Redefining Urban Space,” NAIOP, blog.naiop.org. Europe held the largest regional share at 37.8% in 2025, while Asia-Pacific is set to post the fastest growth at 8.3% through 2031, showing that the modular furniture market is balancing a mature regulatory core with faster expansion in high-urbanization economies. Competition remains moderate, with large commercial platforms expanding scale through transactions such as HNI’s December 2025 close of Steelcase, even as manufacturers face added wood traceability costs under the European Union Deforestation Regulation and labor shortages in fitted projects.

Key Report Takeaways

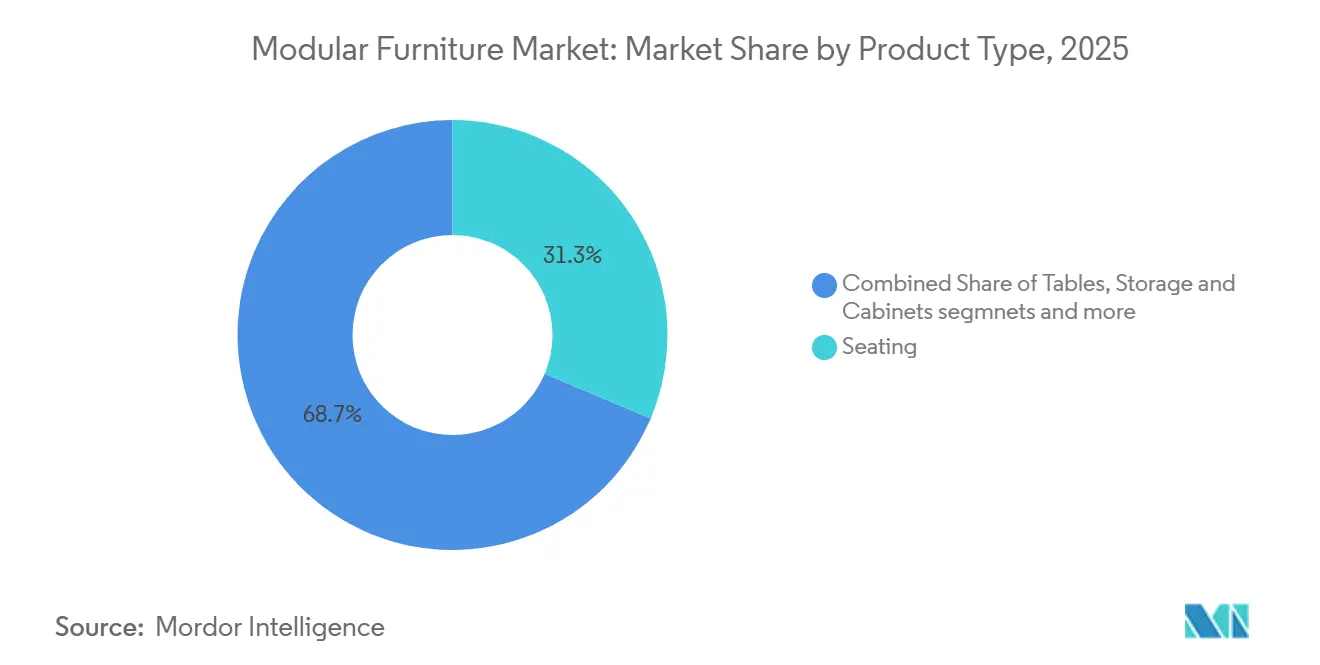

- By product type, seating accounted for 31.3% of the modular furniture market's revenue share in 2025, while Office Furniture Systems is projected to expand at a 7.8% CAGR through 2031.

- By material type, wood accounted for 43.5% in 2025, while Plastic & Polymer is forecast to grow at an 8.1% CAGR through 2031.

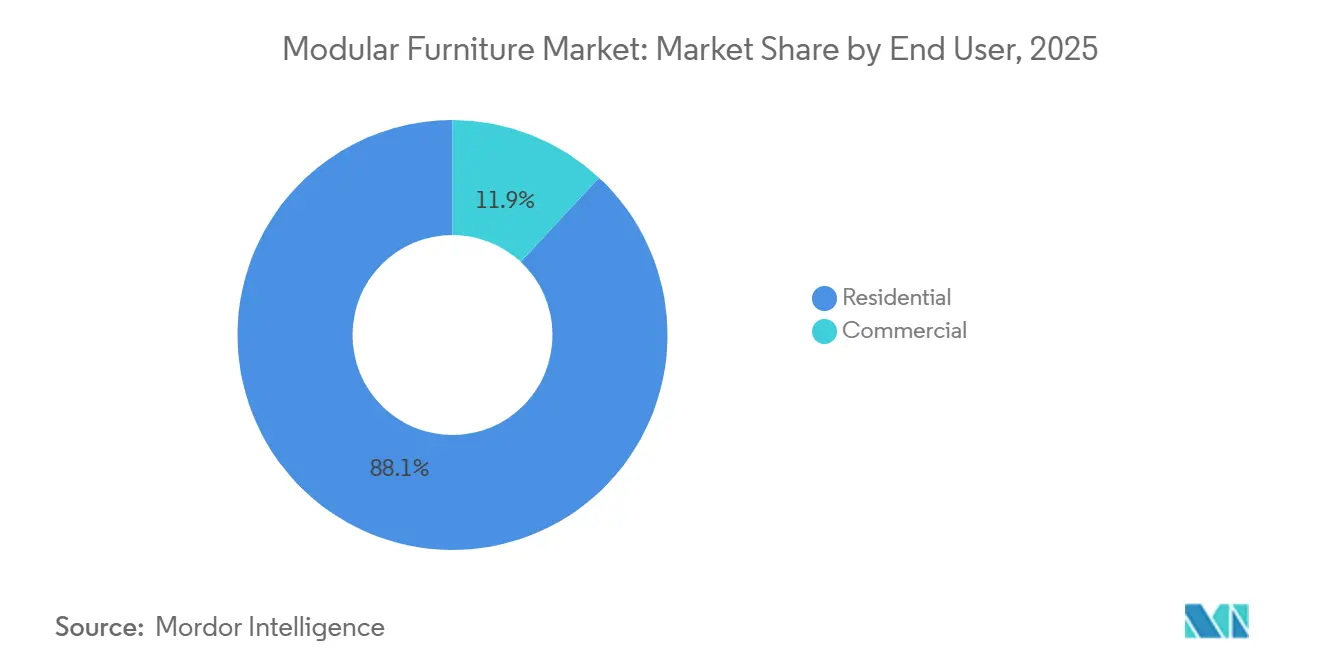

- By end user, residential accounted for 58.6% of the modular furniture market's revenue share in 2025, while Commercial is expected to advance at a 7.9% CAGR through 2031.

- By distribution channel, B2C/Retail accounted for 71.6% of the modular furniture market's revenue in 2025, while B2B/Project is projected to grow at an 8.1% CAGR through 2031.

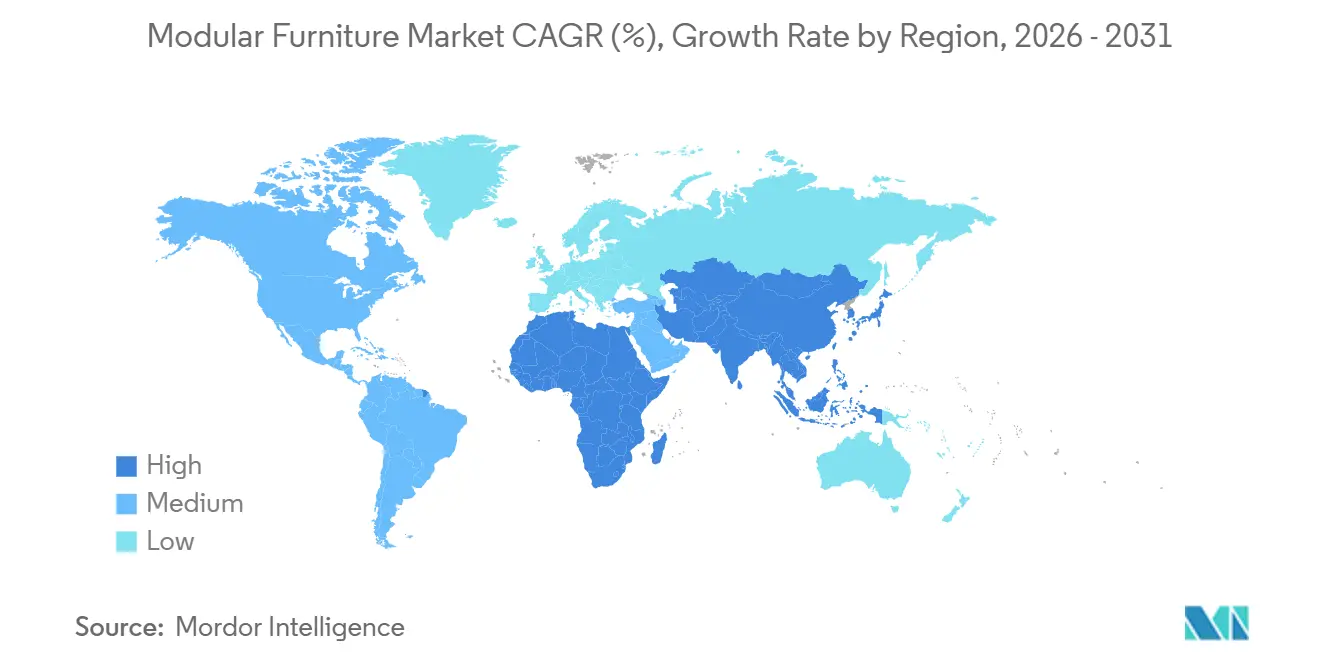

- By geography, Europe accounted for 37.8% in 2025, while Asia-Pacific is projected to record the highest CAGR of 8.3% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Modular Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Space-saving demand from smaller urban homes | +1.5% | Global, with concentration in Asia-Pacific megacities and North American urban metros | Short term (≤ 2 years) |

| Hybrid work and office reconfiguration | +1.3% | Global, strongest in North America, Western Europe, and Asia-Pacific commercial hubs | Short term (≤ 2 years) to Medium term (2-4 years) |

| E-commerce and digital configurators expand customization | +1.0% | Global, with North America, Europe, and Asia-Pacific leading adoption | Medium term (2-4 years) |

| Circular and sustainable furniture preferences | +0.8% | Europe primary, with spillover into Asia-Pacific and North America | Long term (≥ 4 years) |

| Office-to-residential conversions need pre-engineered fit-outs | +0.7% | North America and Europe | Short term (≤ 2 years) to Medium term (2-4 years) |

| Repairability and product-passport rules favor modular design | +0.5% | Europe-led, with progressive adoption across developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Space-saving Demand from Smaller Urban Homes

The modular furniture market continues to benefit from smaller city homes because each lost square foot increases the value of storage, foldability, and room-to-room flexibility. NAIOP reported in October 2025 that apartments built in the last 10 years were 30 square feet smaller than those delivered in the prior decade, indicating that space efficiency is now a structural design issue rather than a temporary preference. That shift supports systems that combine seating, storage, and sleeping functions in a single layout, especially in compact apartments where fixed furniture reduces usable space. The same pressure is visible across dense cities in the Asia-Pacific region, where smaller floor plans raise the value of products that can move between living, working, and storage use across the day. Global brands are responding with direct product changes, and IKEA introduced its PS 2026 line with more than 40 modular and multipurpose products designed for small-space living[2]"IKEA, “First Look, Upcoming IKEA PS 2026 Collection,” IKEA Newsroom, ikea.com. Manufacturers that build visible upgrade paths into these systems can also turn an initial sale into repeat demand for add-on modules, replacement parts, and room extensions over time.

Hybrid Work and Office Reconfiguration

Hybrid work has become a stable operating model, keeping the modular furniture market closely tied to office redesign cycles. JLL reported that the share of employees attending the office 3 to 4 days per week rose to 55% in 2026, confirming that structured hybrid work is not fading but is becoming the standard pattern in many occupier portfolios. CBRE also found that average building utilization reached 53% in 2025, while the occupancy ratio rose to 111% in 2026, indicating many employers are planning for more people than the number of fixed seats on a given day. That pressure is changing layout choices, with more firms adding phone booths, focus rooms, and smaller meeting rooms that rely on movable and reconfigurable furniture systems rather than built-in construction. CBRE also noted that design density tightened to 190 square feet per seat from 196, which increases the value of desking and storage systems that can be reallocated quickly as teams change size. As a result, the modular furniture market is benefiting not only from office returns but also from the need to keep reshaping space without the full demolition and rebuild costs.

E-commerce and Digital Configurators Expand Customization

Digital tools are changing the buying path in the modular furniture market by reducing purchase uncertainty and making customization easier to understand. The 3D Cloud Furniture Shopping Trends Study 2026 found that 80% of users who engaged with a 3D product configurator rated it very helpful, and 40% of users who used the tool spent more than their original budget, compared with 17% of non-users. That result matters because it shows that online furniture demand is moving away from a discount-led model and toward a higher-value model built around configuration, visualization, and confidence. Raymour & Flanigan expanded its 3D Cloud partnership in November 2024 to deploy a sectional configurator across its online and store network, which shows that these tools are now becoming mainstream in furniture retail rather than experimental add-ons. The same logic is spreading into project channels, where virtual configuration helps commercial buyers test complex modular layouts before committing to orders. This shortens the route from design to approval and reduces costly site revisions after specification.

Circular and Sustainable Furniture Preferences

Sustainability preferences are supporting the modular furniture market because products that can be repaired, disassembled, and upgraded fit more easily into circular buying models. Modular construction has an inherent advantage here because damaged components can be replaced at the component level rather than forcing a full product discard. European policy is moving in the same direction, with the Directive on Repair of Goods aimed at improving access to repair and extending product life across consumer categories. At the same time, traceability and material scrutiny are becoming stricter for wood-based goods entering Europe, which raises the value of systems that use materials efficiently and remain serviceable for longer. Procurement teams are therefore placing greater weight on products that can demonstrate clear material origins, replaceable parts, and lower end-of-life waste. This shift not only supports premium brands but also supports manufacturers that can document maintenance, reuse, and take-back processes practically.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher upfront cost versus conventional furniture | -1.2% | Global, most acute in price-sensitive emerging markets across South and Southeast Asia and Africa | Short term (≤ 2 years) to Medium term (2-4 years) |

| Assembly complexity and durability concerns | -0.8% | Global, amplified in markets with lower modular adoption and limited after-sales infrastructure | Short term (≤ 2 years) |

| Wood traceability compliance raises sourcing costs | -0.6% | Europe is primary, with Asia-Pacific supply-chain spillover | Medium term (2-4 years) to Long term (≥ 4 years) |

| Installer shortages delay fitted modular projects | -0.6% | North America and Western Europe, with an emerging effect in the Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher Upfront Cost versus Conventional Furniture

Higher sticker prices remain one of the clearest barriers in the modular furniture market, especially for first-time residential buyers who prioritize the visible purchase cost over lifetime value. Precision joinery, interchangeable parts, and stronger component specifications often lift pricing above comparable conventional pieces. This issue is more pronounced in emerging markets, where furniture purchases are commonly funded with cash or informal credit rather than structured financing. Even when lifecycle economics are favorable, that longer-term value can be hard to communicate at the point of purchase if the price gap is immediate and clear. Commercial buyers face a more balanced trade-off because reconfiguration can reduce replacement cost later, but mid-market budgets still make upfront approvals harder. Brands that narrow this gap through design-for-cost engineering and clearer ownership economics are better placed to widen adoption without weakening product quality.

Assembly Complexity and Durability Concerns

Assembly concerns still slow the modular furniture market because many buyers link modular formats with difficult setup or weak long-term performance. The problem is not uniform across the category, but lower-quality products have shaped perception more broadly than their share alone would suggest. When instructions are unclear or connector hardware is weak, buyers are more likely to leave negative reviews that affect the whole segment, not just one brand. Online channels can amplify this issue because customers cannot easily judge material weight, joint quality, or fit before ordering. The problem becomes more serious in markets with limited after-sales support, where a single missing part or failed connector can turn a repairable issue into a full replacement. Manufacturers that offer stronger testing, clearer assembly tools, and dependable access to spare parts are more likely to separate themselves from lower-tier competitors on this point.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Office Systems Outpacing a Seating-Dominant Market

Seating held 31.3% of the modular furniture market share in 2025, making it the largest product group. Its lead came from broad use across living rooms, lounges, lobbies, and outdoor settings, where sectional formats allow buyers to extend, split, or rotate layouts without replacing the full system. That flexibility supports repeat purchases because households and businesses can add units as room needs or headcount changes over time. Seating also benefits from design visibility, since it is often the first modular purchase in both homes and shared commercial spaces. This keeps the category central to volume growth even when buyers delay spending in other furniture areas.

Office Furniture Systems is projected to grow at 7.8% through 2031, driven by tighter office density and a greater need for layouts that can be quickly reconfigured. Firms are using modular desks, storage units, divider units, and benching systems to support hybrid attendance patterns and shared-occupancy models. These systems reduce the need for repeated fit-out work when teams expand, contract, or move across floors. The category also fits procurement priorities because standardized parts can be installed, replaced, or moved more easily than fixed joinery. This keeps office systems as the strongest growth engine in the modular furniture market's product mix.

By Material Type: Wood Dominates, Polymers Gain Speed

Wood accounted for 43.5% of demand in 2025, making it the largest material in the modular furniture market. Its strength comes from design familiarity, visual appeal across price tiers, and engineered wood's ability to support standardized production at consistent dimensions. Medium-density fiberboard, particleboard, and plywood remain especially useful because they combine predictable shaping with cost efficiency at scale. Wood is also deeply embedded in buyer expectations for residential furniture, which keeps it relevant across both entry-level and premium ranges. As a result, wood remains the base material for many wardrobes, cabinets, shelving systems, and bedroom products.

Plastic & Polymer is expected to expand at 8.1% through 2031, making it the fastest-growing material segment. The growth reflects rising use in outdoor modular furniture, lightweight storage, and residential products designed for small apartments where portability matters. These materials also perform well where moisture resistance, hygiene, and low maintenance are important, including hospitality, education, and some healthcare settings. Their lower weight can also simplify delivery and installation compared with heavier wood-based products. That mix of durability and ease of handling is helping polymers gain share in use cases where function matters more than traditional material preference.

By End-User: Residential Scale, Commercial Momentum

Residential accounted for 58.6% of the modular furniture market in 2025, which kept households as the main volume base for the category. This lead is structural because every new housing unit creates immediate demand for storage, seating, sleeping, and dining solutions. The need is especially strong in urban apartments, where buyers prefer products that fit small layouts and can be adjusted when family needs change. Residential demand also spans a wide price range, from ready-to-assemble storage to more premium bedroom and living systems selected as part of interior planning. That breadth keeps home demand central to the modular furniture market even when project channels become more active.

Commercial is forecast to grow at 7.9% through 2031, making it the fastest-growing end-user segment in the modular furniture market. Office reconfiguration remains the largest driver, but hotel renovations and mixed-use projects are also helping demand for factory-planned systems. The United States office-to-residential pipeline stood at 90,300 units at the start of 2026, which supports demand for pre-engineered storage, kitchen, and sleeping solutions in converted apartments. These projects value repeatable layouts because they help compress planning and installation time across large unit counts. That makes modular systems attractive even when project buyers remain cost-sensitive.

By Distribution Channel: B2C Scale Meets B2B Growth

B2C/Retail accounted for 71.6% of the value in 2025, keeping consumer channels at the center of the modular furniture market. Home centers, specialty furniture stores, online platforms, and local workshops all play a role in this channel mix. Digital channels are gaining popularity faster because they help buyers visualize room fit, compare finishes, and understand configuration options before purchase. That reduces hesitation in categories where size, color, and layout compatibility matter greatly. It also helps sellers present more upsell choices without relying only on showroom space.

B2B/Project accounted for 28.4% in 2025 and is projected to grow at 8.1% through 2031, giving it the fastest pace among channels. Its main advantage lies in larger order sizes tied to office fit-outs, hospitality upgrades, healthcare facilities, and residential development projects. Buyers in this channel usually value delivery reliability, installation support, specification compliance, and product breadth more than headline price alone. This creates a favorable position for suppliers that can cover multiple furniture categories within a single project. It also means winning one contract can produce demand over a long delivery window rather than in a single retail transaction.

Geography Analysis

Europe accounted for 37.8% of the modular furniture market in 2025, maintaining its position as the largest regional market. Its lead comes from dense urban demand, renovation activity, and earlier movement on circular procurement and material traceability. The European Union Deforestation Regulation, which applies to relevant wood products from December 30, 2026, is already shaping sourcing and compliance planning across the region. This environment favors suppliers that can reduce material use, prove wood origin, and support part replacement over time. Western Europe still anchors premium residential and contract demand, while Central and Eastern Europe remain important production bases for cost-competitive supply into the broader region.

Asia-Pacific is set to grow at 8.3% through 2031, making it the fastest-growing regional market in modular furniture. India is one of the main demand engines, driven by urbanization, rising income levels, and expanding office investment, which are driving both household and commercial furniture demand. China remains central to regional production, but domestic demand is shifting toward more value-led, flexible product formats as the housing cycle evolves. KOKUYO and Lamex highlighted this direction in March 2026 with the ingCloud SAIBI-LX launch at CIFF Guangzhou, aimed at flexible, long-lasting workplace use[3]"KOKUYO and Lamex, “KOKUYO Furniture Unveils Immersive Exploration Future Workplace at CIFF Guangzhou,” Lamex, lamex.com. Japan, South Korea, and Southeast Asia also support regional demand through office upgrades, hospitality projects, and residential renovation cycles.

North America remains the second-largest regional block, supported by a large office base, mature online furniture buying, and a growing adaptive reuse pipeline. The United States office-to-residential pipeline reached 90,300 units at the start of 2026, creating demand for factory-built systems that fit compact converted apartments. Mexico is also gaining relevance as industrial investment and supply-chain diversification raise demand for commercial interiors and local production capacity. South America is smaller, with Brazil anchoring regional demand, though growth is still affected by economic volatility and higher landed costs for imported systems. The Middle East and Africa remain earlier-stage markets, but hospitality and premium residential projects in the Gulf are helping build visibility for modular formats. Across regions, the modular furniture market performs best where urban density, formal project channels, and renovation activity develop simultaneously.

Competitive Landscape

The modular furniture market is moderately fragmented in residential and mid-market categories, where many regional suppliers compete on price, design, and delivery time. The commercial and premium tiers are more concentrated because scale, dealer coverage, and project execution matter much more in those parts of the business. A major structural change occurred on December 10, 2025, when HNI completed its acquisition of Steelcase, creating a combined company with pro forma annual revenue of USD 5.8 billion. That combination raised the scale threshold for commercial furniture and strengthened bargaining power in large-account discussions. It also showed that leading companies in the modular furniture market are using consolidation to expand their portfolios and dealer reach, rather than relying solely on organic expansion.

Haworth followed a similar path in February 2026 by adding Tayco and Heller, which expanded its casegoods, office, indoor, outdoor, and recyclable polymer capabilities[4]“Haworth Makes Strategic Investment in Canada with Acquisition of Tayco,” Haworth Media Room, haworth.com. These moves matter because product breadth helps suppliers serve whole projects rather than isolated categories, which is increasingly important in workplace and hospitality contracts. Product development is also shifting toward adaptable systems, and IKEA’s PS 2026 launch showed how mass-market brands are aligning new ranges with small-space living and multi-use demand. The competitive field in the modular furniture market, therefore, rewards both scale and product relevance across changing use cases.

Premium brands continue to defend their position through proprietary system design and long product life rather than relying solely on price competition. USM’s continued promotion of the Haller system shows how connector architecture can serve as a moat when customers want a system they can reconfigure over many years. KOKUYO and Lamex are also pushing flexible workplace formats in China, which reflects the race to capture evolving office demand across Asia-Pacific. Smaller regional companies still have room to win where local customization, delivery speed, or sustainability documentation matter more than global scale. For the modular furniture market as a whole, the balance of power still sits between a few large contract players and a wide base of specialized regional brands. That mix supports ongoing consolidation at the top without removing the strong role of regional firms in residential and mid-market demand.

Modular Furniture Industry Leaders

-

IKEA

-

MillerKnoll, Inc.

-

Steelcase Inc.

-

HNI Corporation

-

Haworth Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Haworth acquired a majority shareholding in Tayco, a Toronto-based manufacturer of office furniture and case goods, expanding its North American manufacturing capacity and product portfolio. The acquisition followed Haworth reporting record global sales of USD 2.7 billion in 2025, an 8% year-over-year increase.

- February 2026: Haworth announced that Heller Furniture of Westport, Connecticut, had joined the Haworth group. Heller’s indoor and outdoor furniture range, known for its fully recyclable polymer construction, strengthens Haworth’s sustainability and outdoor modular offerings.

- March 2026: KOKUYO and Lamex debuted the ingCloud next-generation modular table and sofa system, SAIBI-LX, in Mainland China at the 57th China International Furniture Fair in Guangzhou, alongside a China Office Environment White Paper developed in collaboration with Matrix Design studio.

- August 2026: HNI Corporation and Steelcase Inc. announced a definitive merger agreement with total consideration to Steelcase shareholders of approximately USD 2.2 billion, the largest consolidation transaction in the commercial office furniture category in recent years

Global Modular Furniture Market Report Scope

| Seating | Sofas & Sectionals |

| Lounge Seating | |

| Ottomans & Benches | |

| Tables | Coffee & Side Tables |

| Dining Tables | |

| Work Tables | |

| Storage & Cabinets | Wardrobes & Closets |

| Shelving & Bookcases | |

| TV & Media Units | |

| Kitchen Cabinets | |

| Beds & Bedroom Systems | Beds & Bed Frames |

| Nightstands & Dressers | |

| Office Furniture Systems | Desking Systems |

| Workstations & Cubicles | |

| Mobile Storage | |

| Outdoor Modular Furniture | Outdoor Seating |

| Outdoor Tables | |

| Other Product Types |

| Wood |

| Plastic & Polymer |

| Metal |

| Other Materials |

| Residential |

| Commercial |

| B2B/Project | |

| B2C/Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Local Workshops | |

| Other Distribution Channels |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and the Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of the Middle East and Africa |

| By Product Type | Seating | Sofas & Sectionals |

| Lounge Seating | ||

| Ottomans & Benches | ||

| Tables | Coffee & Side Tables | |

| Dining Tables | ||

| Work Tables | ||

| Storage & Cabinets | Wardrobes & Closets | |

| Shelving & Bookcases | ||

| TV & Media Units | ||

| Kitchen Cabinets | ||

| Beds & Bedroom Systems | Beds & Bed Frames | |

| Nightstands & Dressers | ||

| Office Furniture Systems | Desking Systems | |

| Workstations & Cubicles | ||

| Mobile Storage | ||

| Outdoor Modular Furniture | Outdoor Seating | |

| Outdoor Tables | ||

| Other Product Types | ||

| By Material Type | Wood | |

| Plastic & Polymer | ||

| Metal | ||

| Other Materials | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2B/Project | |

| B2C/Retail | Home Centers | |

| Specialty Furniture Stores | ||

| Online | ||

| Local Workshops | ||

| Other Distribution Channels | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and the Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of the Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected value of the modular furniture space by 2031?

The modular furniture market is projected to reach USD 127.9 billion by 2031, rising from USD 91.6 billion in 2026 at a 6.9% CAGR.

Which region leads demand and which region is growing the fastest?

Europe led with 37.8% in 2025, while Asia-Pacific is forecast to record the fastest growth at an 8.3% CAGR through 2031.

Which product category holds the largest share and which one is expanding the fastest?

Seating was the largest product category with 31.3% in 2025, while Office Furniture Systems is expected to grow the fastest at a 7.8% CAGR.

Why is hybrid work still important for furniture demand?

Hybrid work is keeping offices in redesign mode, with higher attendance and tighter seating ratios pushing employers toward layouts that can be reconfigured quickly.

What are the main risks facing suppliers and manufacturers?

The main risks are higher upfront pricing versus conventional furniture, installation labor shortages, assembly concerns, and rising wood traceability costs under European rules.

Page last updated on: