Wood Furniture Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

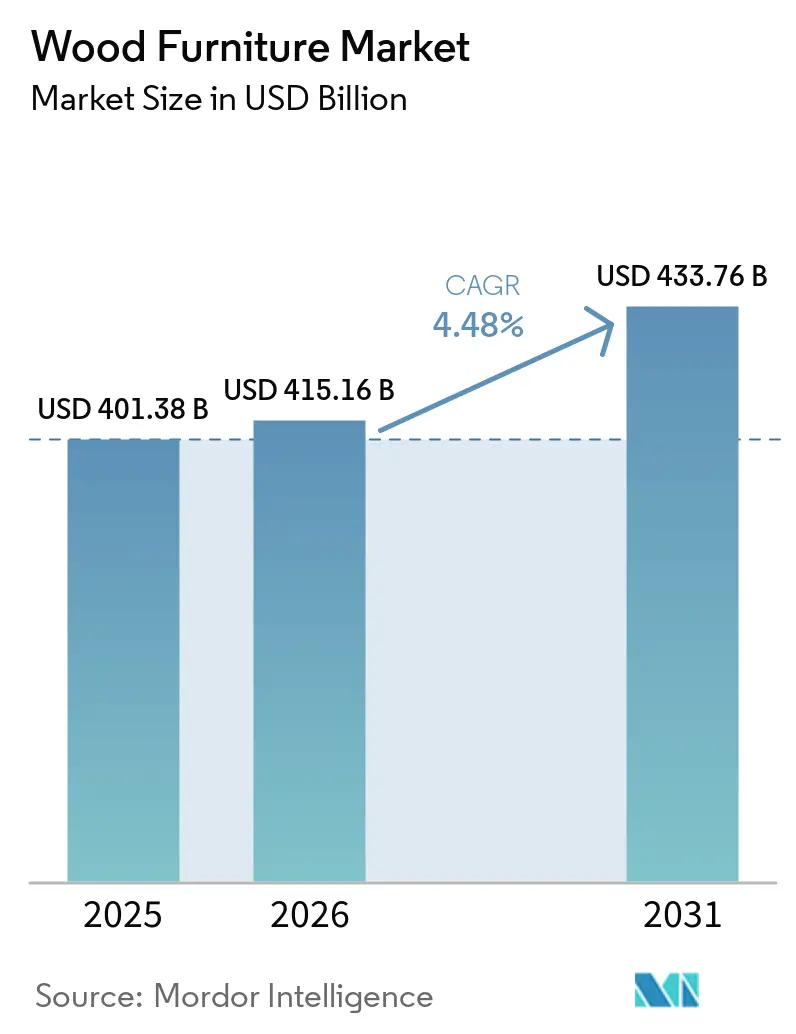

| Market Size (2026) | USD 415.16 Billion |

| Market Size (2031) | USD 433.76 Billion |

| Growth Rate (2026 - 2031) | 4.48% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

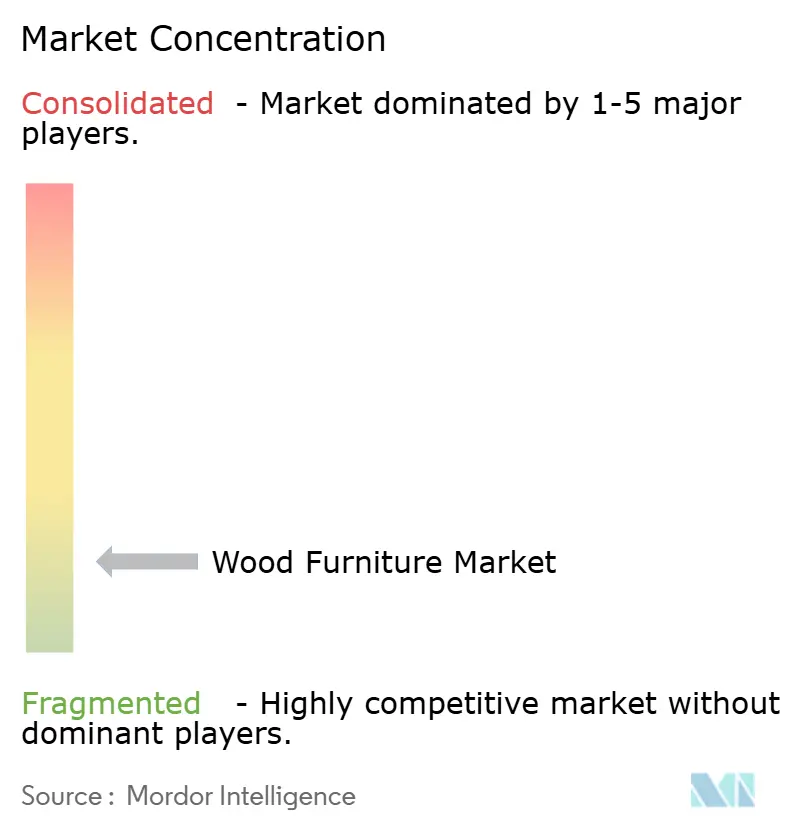

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wood Furniture Market Analysis by Mordor Intelligence

The global wood furniture market size stood at USD 415.16 billion in 2026, up from USD 401.38 billion in 2025, and is projected to reach USD 433.76 billion by 2031 at an 4.48% CAGR. The growth path in 2026 reflects normalization after the pandemic, with capital spending tilting from impulse home upgrades to planned commercial fit-outs and long-cycle residential projects that favor higher-value cabinetry and contract-grade furniture[1]JCHS.HARVARD.EDU https://www.jchs.harvard.edu/press-releases/modest-gains-2025-outlook-home-remodeling. Asia-Pacific leads both scale and momentum on the back of strong engineered panels capacity, continued export competitiveness in Vietnam, and gradually strengthening household demand in India, which adds resilience to the demand base in 2026. Certification and traceability requirements are now structural market shapers, as composite wood products are subject to third-party certification under the United States TSCA Title VI. In contrast, European market access hinges on end-to-end due diligence and geolocation traceability under deforestation-free rules. Process automation and digital mass customization are compressing lead times and reducing material waste, sustaining the competitiveness of engineered wood panels in price-sensitive and project-driven segments as 2026 procurement rounds open.

Key Report Takeaways

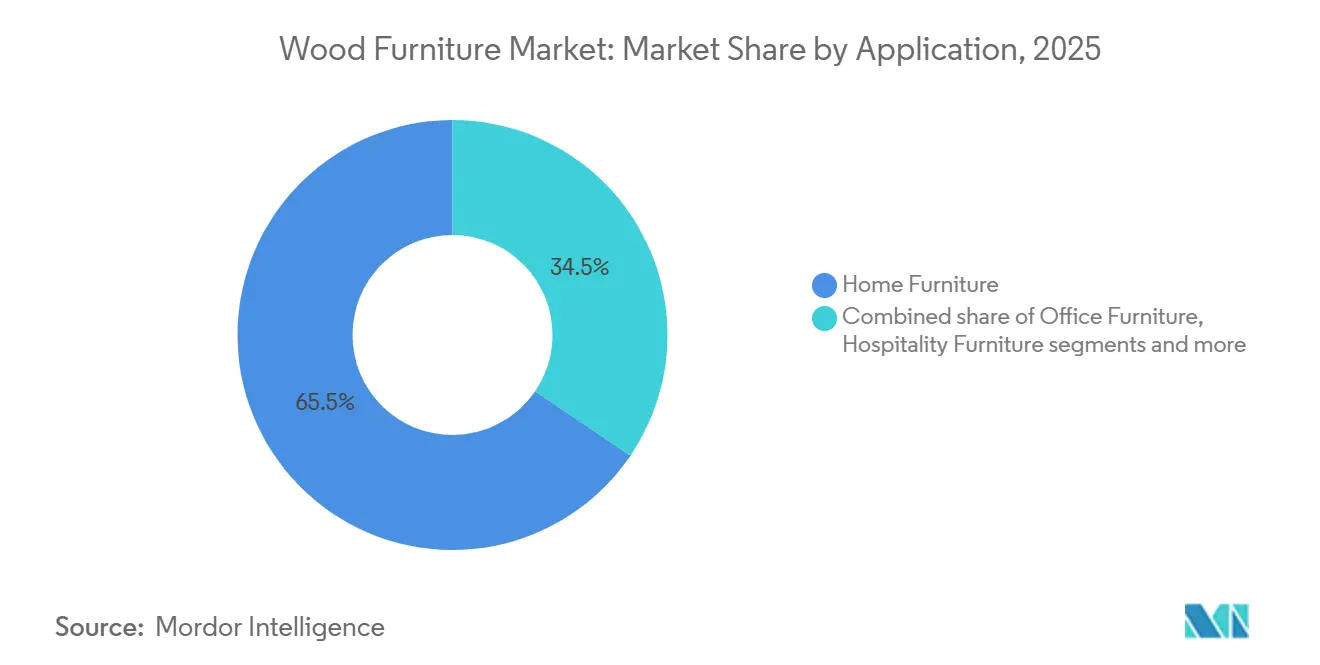

- By application, home furniture led with 65.51% of the global wood furniture market share in 2025, while hospitality is projected to post the fastest 5.98% CAGR through 2031, reflecting the release of deferred renovation budgets and the growing use of modular contract systems; these outcomes align with the broader trajectory of the global wood furniture market.

- By wood type, solid hardwoods accounted for 42.15% of the global wood furniture market share in 2025. They engineered wood panels are set to grow the fastest at a 5.78% CAGR, as digital nesting and factory automation improve material utilization and shorten custom-order lead times in the global wood furniture market.

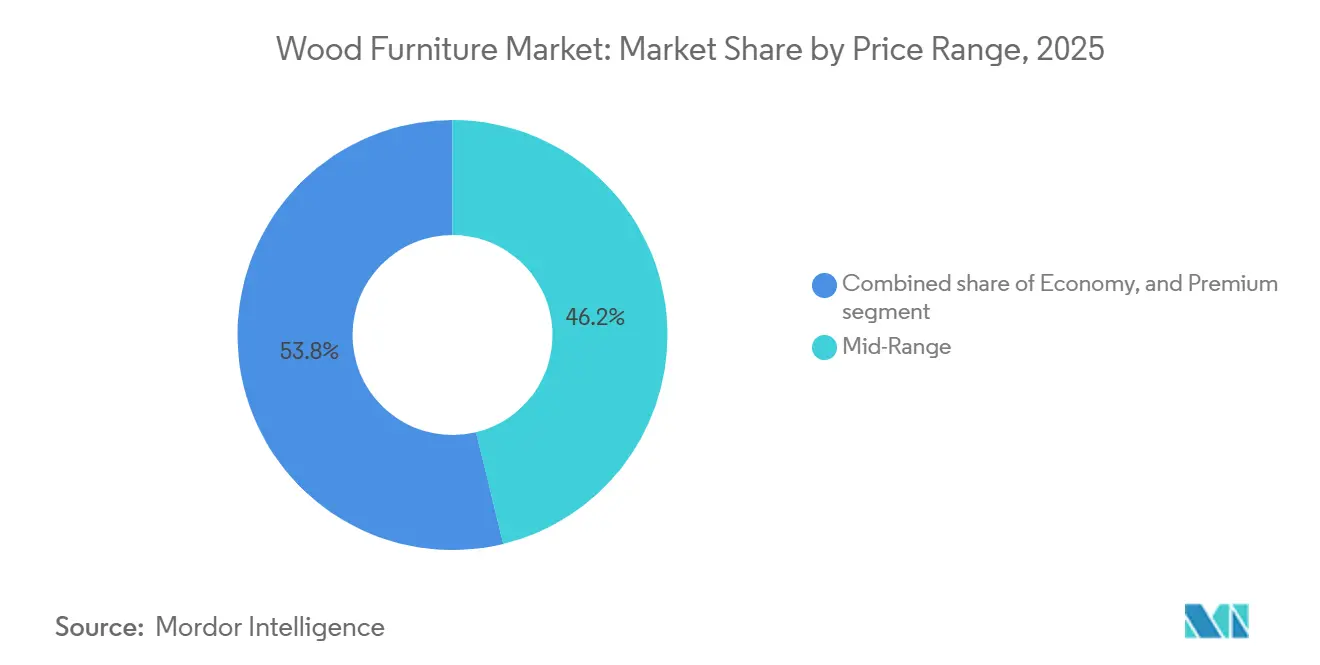

- By price range, the mid-range accounted for 46.21% of the global wood furniture market share in 2025, while the premium segment is forecast to grow at a 6.02% CAGR, driven by a willingness to pay for FSC or PEFC credentials and rapid configurability tools.

- By distribution channel, B2C retail captured 74.35% of the global wood furniture market share in 2025, and B2B or project-based channels are expected to grow at a 5.51% CAGR as hospitality and institutional fit-outs accelerate.

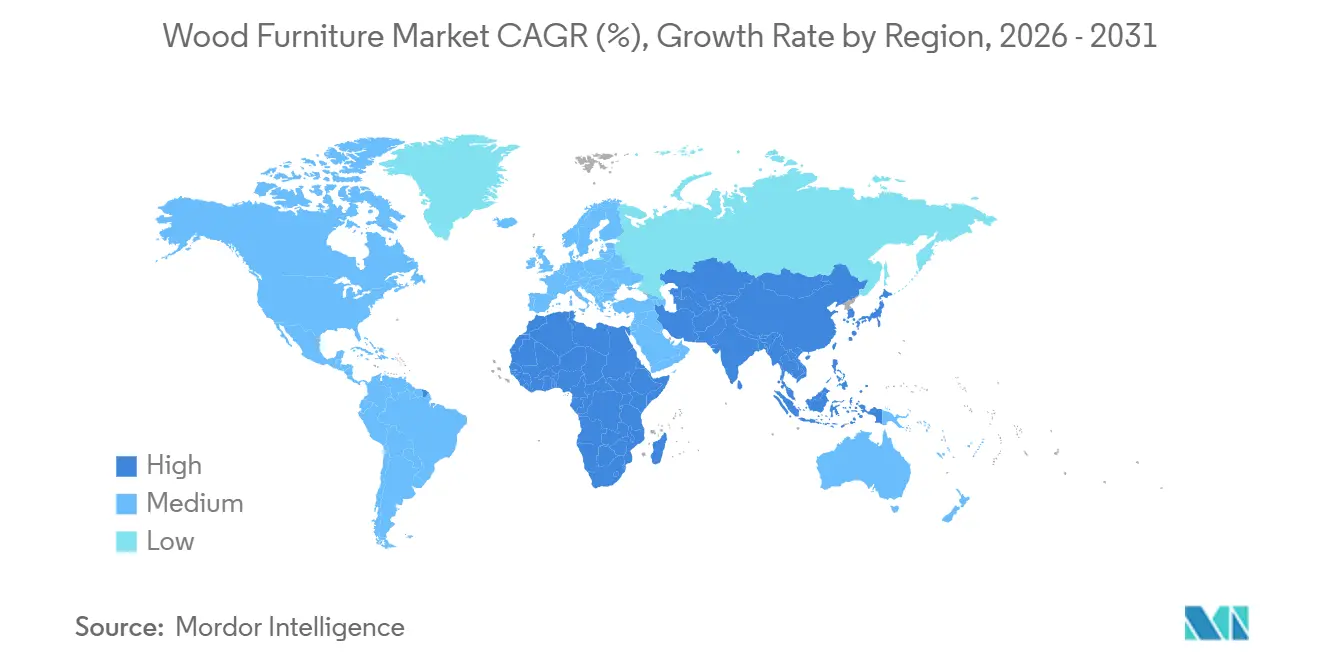

- By geography, Asia-Pacific commanded 38.11% of the global wood furniture market share in 2025 and is also the fastest-growing region at a 6.23% CAGR to 2031, supported by export capabilities and steady downstream demand.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Wood Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce adoption accelerates direct-to-consumer wood furniture | +0.9% | Global, early gains in North America and Asia-Pacific | Medium term (2-4 years) |

| Sustainability and certifications (FSC/PEFC) shape purchasing criteria | +0.7% | North America and the EU, with certified forest leadership in Canada | Long term (≥ 4 years) |

| Residential renovation and home improvement demand | +0.6% | North America core, spillover to EU suburban markets | Short term (≤ 2 years) |

| Hospitality and commercial fit-outs rebound (contract wood furniture) | +1.2% | Global, strongest in Asia-Pacific and North America urban corridors | Medium term (2-4 years) |

| Mass customization with CNC and automation, enabling solid wood at scale | +0.7% | Asia-Pacific and EU manufacturing hubs, and adoption in North America | Medium term (2-4 years) |

| Preference for low-embodied-carbon interiors favors wood over substitutes | +0.5% | EU and North America as primary adopters, with uptake in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Adoption Accelerates Direct-to-Consumer Wood Furniture

Digital commerce is expanding its role in how households and small businesses discover, configure, and purchase wood furniture, with leading omnichannel retailers showing a higher online mix in 2025 and early 2026. IKEA United States reported USD 5.3 billion in FY25 sales with meaningful contributions from online channels, underpinned by new omnichannel formats and localized fulfillment that reinforce a direct-to-consumer model for bulky goods[2]IKEA.COM ikea.com/us/en/newsroom/corporate-news/ikea-u-s-releases-fy25-annual-summary-and-announces-four-new-stores-planned-for-2026-pubf0e047b0. New configuration experiences and front-end design tools are reshaping shopper journeys, as real-time 3D customization platforms reduce quote-to-order time and help buyers visualize fit and finish before checkout. Integrated engineering-to-production workflows are improving margins by linking design outputs directly to nested cutting programs and production schedules, which helps small and medium shops meet short lead times for made-to-order pieces. The format change favors brands that unite digital storefronts with regional pickup, home delivery, and post-purchase services, a mix that has become essential as consumers expect easier last-mile solutions for heavier products. As 2026 progresses, the global wood furniture market benefits from these channel investments, which help protect conversion rates for complex, customizable furniture sets that were once a poor fit for online journeys.

Sustainability and Certifications (FSC/PEFC) Shape Purchasing Criteria

Certification of wood sourcing has become a core purchasing factor in North America and Europe, where consumers and institutional buyers often specify FSC or PEFC labels for both finished furniture and upstream components. Canada accounts for 160 million hectares of certified forests, equal to 41% of the world’s certified forest area, which anchors cross-Atlantic supply into certified product lines and supports premium willingness to pay in affluent retail and project channels[3]CANADIANWOODBC.COM https://canadianwoodbc.com/why-u-s-furniture-brands-care-about-forest-certification. PEFC expanded the traceable sources by developing standards for non-traditional timber contexts, and sector guidance for furniture and joinery clarifies how chain-of-custody and sustainable forest management claims should be substantiated in tender processes and retailer compliance programs. Industry associations also documented momentum in urban sourcing within certification systems during 2025, which adds another supply route that aligns with circularity and procurement rules promoting reuse and verified origin[4]AUSTRALIANFURNITURE.ORG.AU https://australianfurniture.org.au/imported-timber-furniture-fails-the-test-as-pefc-certifies-first-urban-trees. The certification trend lifts the premium tier by reinforcing provenance, chain of custody, and responsible forestry narratives that customers can verify. As 2026 demand consolidates, these dynamics enable brands with robust documentation to hold price and volume better than competitors lacking traceability capabilities, shaping mix across the global wood furniture market.

Residential Renovation and Home Improvement Demand

Remodeling and home improvement remain a stabilizer for the category in 2026, with remodeling spend in the United States at USD 509 billion in 2025, up 1.2% year over year. This is relevant for kitchen and bath cabinetry, storage, and built-in wood solutions. The category benefits from design-led upgrades, as homeowners continue to invest in functional and aesthetic improvements that prioritize durable wood surfaces and coordinated storage systems in heavy-use rooms. Large cabinet manufacturers are consolidating to expand brand portfolios and production footprints that cover stock, semi-custom, and luxury tiers in response to nationwide retail and builder programs. Such scale moves strengthen vendor reliability for big-box and pro channels while supporting investments in automation and product development that raise service levels for project customers. These factors help the global wood furniture market maintain a steady floor of demand through project-driven purchases, even when discretionary household spending is mixed.

Hospitality and Commercial Fit-Outs Rebound

Contract-grade demand is returning to a healthier trajectory in 2026, led by hospitality refresh cycles and workplace reconfigurations that specify modular wood casegoods and seating with visible craftsmanship and replaceable components. New workplace systems launched in 2025 and 2026 show a stronger tilt toward material variety, privacy, and multi-use zones, broadening the specification set for veneers and solid elements in open-plan and hybrid offices. Healthcare furniture launches emphasize intuitive mechanisms, durable materials, and occupant comfort, a feature set that commands premium pricing and favors wood-based designs that meet cleanliness and safety requirements. These product families support the return of multi-year procurement cycles in institutional verticals and expand contract manufacturers' opportunities to differentiate through finish options and integrated storage. As travel and workplace usage find a new equilibrium in 2026, the shift toward higher-performance contract products reinforces price integrity and extends order visibility across the global wood furniture market. This segment also complements sustainability objectives in corporate and hospitality settings, where material transparency and durability are embedded in procurement criteria that increasingly value certified wood.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Timber and panel price volatility and supply risks | -1.1% | Global, acute in the EU (post-Russia/Belarus sanctions removing 10% supply), North America (log costs pressuring sawmills) | Short term (≤ 2 years) |

| Compliance costs: formaldehyde/VOC rules and EUDR traceability | -0.9% | Global, most severe in the EU (EUR 1.8B Germany costs), North America (CARB/TSCA requirements), and export-dependent Asia-Pacific | Medium term (2-4 years) |

| Competition from non-wood materials and low-cost laminates | -0.6% | North America & EU (metal/plastic office furniture), Asia-Pacific (low-cost laminate substitution in economy segment) | Medium term (2-4 years) |

| Trade barriers, anti-dumping actions, and logistics disruptions | -0.8% | Global, concentrated impact on China exporters (216.01% anti-dumping margin), Vietnam/Malaysia (Section 232 tariffs), Cambodia (58% United States market reliance) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Timber and Panel Price Volatility and Supply Risks

Price indices for structural softwood in the United Kingdom fluctuated significantly through 2024 and 2025, reflecting supply adjustments and demand variability that affected mill operating patterns and shipments into downstream segments. Industry reviews noted that some sawmills idled less efficient capacity, and forest owners curtailed logging in response to unfavorable margins, which accentuated near-term swings in availability and spot prices as construction demand shifted. Panel producers also faced pressure on resin and energy costs over the period, which led to surcharges and scheduling constraints for furniture manufacturers using particleboard and MDF in high volumes. These conditions favored vertically integrated producers or firms with long-term supply agreements. At the same time, smaller fabricators faced tighter allocation and thinner margins on fixed-price orders, particularly in fast-moving consumer channels. As 2026 unfolds, procurement teams in the global wood furniture market continue to emphasize supply resilience, diversified sourcing, and materials optimization to buffer volatility.

Compliance Costs: Formaldehyde and VOC Rules Plus Deforestation-Free Traceability

The United States EPA finalized its TSCA risk evaluation for formaldehyde on January 2, 2025, and opened updates to composite wood emission standards and test methods in February 2026, reinforcing third-party certification and quality control regimes that composite wood importers and domestic manufacturers must meet. California’s CARB Phase 2 limits, carried into the federal TSCA framework, define stringent emission thresholds for hardwood plywood, MDF, and particleboard that require ongoing testing and recordkeeping for high-volume producers. On the EU side, deforestation-free rules require due diligence statements, legal harvest documentation, and geolocation data for EU-bound shipments of wood and derived products, setting a documentation baseline that suppliers must be ready to meet through digital traceability or equivalent systems. The intersection of these regimes raises compliance workloads across certification, testing, and data verification. However, firms with established supplier networks and robust chains of custody systems are better positioned to handle the changes in 2026.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Fleets and Institutions Propel Segmentation

Home furniture captured 65.51% of value in 2025 in the global wood furniture market, while hospitality is projected to be the fastest-growing application at a 5.98% CAGR through 2031 as postponed renovations return to plan and modular contract platforms scale across hotel and mixed-use projects. The home category covers chairs, tables, beds, wardrobes, sofas, dining sets, and kitchen cabinets, and it benefits in 2026 from continued remodeling activity that sustains cabinetry and storage demand even as discretionary purchases vary by income tier. Hospitality programs emphasize modularity and serviceability, which support visible joinery, replaceable upholstery, and surface refresh options within commercial lifecycles that prefer durable wood assemblies. Office furniture remains in reconfiguration mode as workplace systems adapt to hybrid work, with new lines launched in 2026 that expand finish and veneer selections while creating more private collaboration zones for open-plan layouts. Healthcare furniture continues to require high function and comfort for extended stays, with specialized seating products released in mid 2025 that align with clinical workflows and operational needs.

The application mix contributes to stable throughput in 2026 as institutional and commercial orders fill shop capacity, while residential demand provides a steady base in kitchens, baths, and living areas across the global wood furniture market. Within hospitality, operators seek flexible carpentry and finishes that refresh properties without full tear-outs, which has raised interest in modular wood components and replaceable parts to extend lifecycle value. Office programs are shifting toward adaptable systems that combine solid and veneered surfaces to manage privacy, noise, and collaboration, a direction seen in 2026 workplace systems that present expanded palettes and lounge modules. Healthcare demand remains specialized, with recliners, sleep chairs, and sofas engineered for caregivers and patients, and product introductions in 2025 indicate this niche will continue to carry premium price points where performance justifies spend. As 2026 proceeds, the alignment of specification, durability, and modularity strengthens the case for wood in project cycles, reinforcing demand patterns in the global wood furniture market.

By Wood Type: Panels Gain on Hardwoods via Automation

Solid hardwoods held 42.15% of value in 2025 across the global wood furniture market, yet engineered wood panels are forecast to post the fastest 5.78% CAGR as factories capture higher material utilization through intelligent nesting and streamline custom orders with integrated software and automation. Panels such as plywood, MDF, HDF, and particleboard support consistent quality at scale and enable surface treatments that meet aesthetic expectations in price-sensitive categories. As digital fabrication spreads, shops can maintain short lead times for complex projects while controlling yield and rework, which helps panels penetrate new use cases that formerly favored solid wood for cost or complexity reasons. Softwoods remain important in the economy and mid-range lines, though price volatility in upstream structural grades through 2025 affected cost predictability for some producers that rely on Northern and Central European feedstock. Reclaimed wood is gaining recognition as a premium option for projects where sustainability narratives and distinctive material character lift value, and investor activity in 2026 signals more structured capacity for reclaimed beams, flooring, and custom pieces.

Compliance dynamics also shape substrate choices in 2026, as composite wood imports and production must align with TSCA Title VI and CARB rules governing formaldehyde emissions from hardwood plywood, MDF, and particleboard. This underscores the importance of third-party certification and a documented chain of custody, especially for EU-bound lines that also prepare for deforestation-free due diligence. Factory investments in automation are widening access to mass customization by connecting design output to shop-floor execution, with CNC packages that reduce the labor required for complex joinery and panel processing. These capabilities allow both panels and solid wood to compete more effectively on lead time and finish variety, which supports engineered panels’ forecast growth within the global wood furniture market.

By Price Range: Premium Segment Captures Sustainability Premium

Mid-range pricing accounted for 46.21% of value in 2025 in the global wood furniture market, while the premium tier is set to grow at a 6.02% CAGR as affluent buyers and institutional customers pay for durability, customization, and verified sourcing credentials. Brands that display FSC or PEFC labels and robust chain-of-custody documentation find receptive audiences among projects and high-income households that value both aesthetics and provenance. The premium tier also benefits from new product development cycles that emphasize engineered mechanisms, improved ergonomics, and material variety, along with digital configuration that simplifies specifying and ordering. At the value end, importers managing composite wood lines must balance price sensitivity with compliance costs for emissions testing and certification, and competitive dynamics tighten where budget buyers are less able to absorb pass-through charges tied to regulation. Trade actions in select product categories can further pressure price bands in thin-margin markets, as illustrated by anti-dumping enforcement outcomes on wooden bedroom furniture from China that raise effective import costs for named entities.

In 2026, the premium tier’s momentum closely aligns with faster configuration, certified sourcing, and service models that maintain quality after delivery, which together support willingness to pay. Digital mass customization helps compress order-to-delivery timelines for premium buyers who want specific dimensions and finishes without extended lead times, and factory automation helps sustain quality at scale. Certification and traceability also create defensible positioning as procurement teams in hospitality and office projects embed these requirements into tender specifications. The mid-range remains the anchor for household replacement cycles, while the economy tier competes on value in channels where compliance overhead must be carefully managed to protect price points. Across tiers, these dynamics concentrate advantage in brands that align materials, documentation, and digital capabilities, thereby supporting mix quality in the global wood furniture market in 2026.

By Distribution Channel: B2C Dominates, B2B Accelerates

B2C or retail captured 74.35% of value in 2025 across the global wood furniture market, spanning home centers, specialty stores, online platforms, and local workshops, while B2B or project channels are forecast to grow at 5.51% CAGR as hospitality, office, and institutional projects advance. Omnichannel execution is now central to B2C performance, and United States operations at leading retailers are seeing rising online contributions, supported by localized formats and pickup points that facilitate the fulfillment of bulky goods. Home centers continue to win project spend from remodeling contractors and homeowners, with stable activity in the United States renovation outlays, adding a floor to the demand for cabinets and storage. Specialty stores differentiate through design services and curated assortments that emphasize wood finishes, veneers, and mixed-material pieces, which justify premium pricing and white-glove delivery models. Local workshops serve customized and restoration niches and increasingly rely on digital tools to compress design-to-fabrication steps and manage promise windows.

B2B or project channels show renewed energy in 2026 as hospitality renovations scale, and offices refresh to support hybrid work, which raises demand for modular systems and coordinating casegoods that require consistent finishes at volume. Healthcare furniture orders continue to move on clinical functionality and durability, supported by families of products introduced in mid 2025 that address caregiver and patient needs. The distribution picture highlights how channel capabilities, documentation, and automation reinforce performance as the global wood furniture market normalizes after the home improvement surge. Retailers and project suppliers that combine traceable sourcing, digital configuration, and reliable service hold stronger positions in 2026 compared with peers that have not upgraded their systems. As the year develops, these channel advantages help maintain order flow and pricing discipline, particularly in project segments where specification compliance is central.

Geography Analysis

Asia-Pacific held 38.11% of the global wood furniture market value in 2025 and is also forecast to grow the fastest at a 6.23% CAGR through 2031, as capacity in engineered wood, export-oriented production, and rising regional demand combine to sustain volume. Regional expansion by established retailers underscores the opportunity, with new Southeast Asia stores and supply relationships adding to assortments and logistics assets through 2025 and 2026. As 2026 progresses, upstream developments in certified forestry and panel production reinforce Asia-Pacific’s downstream exports, with manufacturers supporting buyer requirements for emissions and chain-of-custody documentation for destination markets. Localized demand growth in large markets provides a domestic buffer to export cycles, helping smooth capacity utilization and material procurement. The region’s mix of scale production and growing mid-income consumer bases keeps its central role intact in the global wood furniture market over the forecast period.

North America heads into 2026 with stable renovation activity across cabinetry, storage, and built-in categories, providing resilience to the overall demand picture for wood furniture. Retailers continue to test omnichannel formats and store footprints to balance online growth and local service, a strategy evident in United States expansion plans at leading players that aim to improve coverage and delivery density. Compliance regimes for composite wood and consumer exposure to formaldehyde remain a focal point for importers and domestic producers, and firms continue to invest in third-party certification and quality control to keep pace with regulatory expectations. Brand strategies that couple design differentiation with reliable delivery and service help steady category results despite mixed macro signals. As the year advances, these anchors maintain a constructive outlook for the region’s contribution to the global wood furniture market.

Europe’s market is adapting to timber supply and compliance dynamics that shape sourcing, pricing, and documentation for furniture producers and importers. Industry associations in the United Kingdom recorded significant timber price swings through 2025 as supply and mill operations adjusted, a context that continued to affect furniture supply chains into 2026. Enterprises serving EU markets are preparing for strict due diligence on deforestation-free sourcing and the geolocation of harvest sites, reinforcing the value of digital traceability and long-term supplier relationships for market access. Certification bodies and sector associations support the adoption of sustainable forest management and chain-of-custody practices, which add a layer of competitive differentiation for brands that sell into public tenders and corporate projects. European producers continue to invest in automation and product variety to defend their share in higher value segments where finish quality, documentation, and service carry weight. These structural factors support a measured growth path that complements the Asia-Pacific’s scale in the global wood furniture market.

Competitive Landscape

The global wood furniture market remains fragmented, with the largest global retailers’ wood-related sales representing a low single-digit percentage of worldwide market value and the top five firms holding well below a 30% combined share. Scale players are building advantage through portfolio breadth, integrated manufacturing, and nationwide distribution agreements, as seen in the announced all-stock combination of two major cabinet makers in 2025, which targets cost synergies and a comprehensive multibrand strategy across stock, semi-custom, and luxury. At the same time, mid-size and specialty firms compete on customization speed, craftsmanship, and sustainability credentials, facilitated by digital configurators, advanced scheduling, and CNC automation that reduce lead times while maintaining consistent quality.

Automation technologies are diffusing rapidly from large factories to smaller shops thanks to packaged software and machine solutions that make nested-based manufacturing accessible. Platforms that combine design, optimized nesting, and CNC execution help micro manufacturers reach 95% or higher panel utilization and reduce total production time, expanding the feasible range of custom projects at competitive price points. Robotics deployments and intelligent handling further reduce setup and transfer times, improving throughput for shops with limited floor space. On the product side, 2025–2026 launches in workplace and healthcare categories demonstrate how design and engineering upgrades support price integrity, specification wins, and channel expansion in contract furniture. These moves align commercial teams and dealer networks around assortments that balance aesthetics, function, and compliance documentation.

Sustainability and circularity continue to generate strategic moves, with investors building platforms around reclaimed wood that serve architects, designers, and builders with traceable supply and fabrication capacity. Peer-reviewed advances in wood and joint engineering suggest future pathways for lower-waste, high-performance components that could, over time, complement traditional methods in premium segments. As 2026 unfolds, the leaders in each segment tend to be those that combine documented sourcing, production agility, and consistent service, while challengers that lag in compliance or digital capabilities find it harder to compete at scale. This strategic pattern reinforces a wide field of viable competitors while concentrating momentum on brands that align engineering, sustainability, and omnichannel execution in the global wood furniture market.

Wood Furniture Industry Leaders

Inter IKEA Systems B.V.

Williams-Sonoma, Inc.

Ashley Furniture Industries, LLC

Nitori Holdings Co., Ltd.

RH (Restoration Hardware)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Old Hickory Furniture announced new ownership under President Beau Parsons, positioning for growth in hospitality and luxury residential segments, and introduced the Max Humphrey Lodge Collection while entering a reclaimed wood partnership with Nassar Development.

- February 2026: Williams‑Sonoma relaunched Dormify with a new e‑commerce platform targeting Gen Z and leveraging cross‑fulfillment from portfolio brands.

- January 2026: Knoll (MillerKnoll brand) launched Dividends Skyline, a workplace system with an expanded material palette, lounge modules, and coordinated finishes for hybrid offices, distributed through MillerKnoll dealers.

- January 2026: Beaubois Millwork completed the acquisition of Four Daughters Millwork to expand United States production capacity for complex architectural projects, with plans to invest in Northeastern Pennsylvania; the company retained the acquired workforce and broadened market access.

Global Wood Furniture Market Report Scope

| Home Furniture | Chairs |

| Tables (side tables, coffee tables, dressing tables, etc.) | |

| Beds | |

| Wardrobes | |

| Sofas | |

| Dining Tables/Dining Sets | |

| Kitchen Cabinets | |

| Other Home Furniture (bathroom furniture, outdoor furniture, etc.) | |

| Office Furniture | Chairs |

| Tables | |

| Storage Cabinets | |

| Desks | |

| Sofas and Other Soft Seating | |

| Other Office Furniture | |

| Hospitality Furniture | |

| Educational Furniture | |

| Healthcare Furniture | |

| Other Applications (public places, retail malls, government offices, etc.) |

| Solid Hardwoods (e.g., Oak, Walnut, Teak) |

| Softwoods (e.g., Pine, Spruce) |

| Engineered Wood Panels (Plywood, MDF/HDF, Particleboard) |

| Reclaimed/Salvaged Wood |

| Economy |

| Mid-Range |

| Premium |

| B2C/Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Local Workshops | |

| Other Distribution Channels | |

| B2B/Project |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and the Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of the Middle East and Africa |

| By Application | Home Furniture | Chairs |

| Tables (side tables, coffee tables, dressing tables, etc.) | ||

| Beds | ||

| Wardrobes | ||

| Sofas | ||

| Dining Tables/Dining Sets | ||

| Kitchen Cabinets | ||

| Other Home Furniture (bathroom furniture, outdoor furniture, etc.) | ||

| Office Furniture | Chairs | |

| Tables | ||

| Storage Cabinets | ||

| Desks | ||

| Sofas and Other Soft Seating | ||

| Other Office Furniture | ||

| Hospitality Furniture | ||

| Educational Furniture | ||

| Healthcare Furniture | ||

| Other Applications (public places, retail malls, government offices, etc.) | ||

| By Wood Type | Solid Hardwoods (e.g., Oak, Walnut, Teak) | |

| Softwoods (e.g., Pine, Spruce) | ||

| Engineered Wood Panels (Plywood, MDF/HDF, Particleboard) | ||

| Reclaimed/Salvaged Wood | ||

| By Price Range | Economy | |

| Mid-Range | ||

| Premium | ||

| By Distribution Channel | B2C/Retail | Home Centers |

| Specialty Furniture Stores | ||

| Online | ||

| Local Workshops | ||

| Other Distribution Channels | ||

| B2B/Project | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and the Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of the Middle East and Africa | ||

Key Questions Answered in the Report

What is the global wood furniture market size and growth outlook to 2031?

The global wood furniture market size was USD 401.38 billion in 2025 and is projected to reach USD 433.76 billion by 2031 at a 4.48% CAGR over 2026-2031.

Which region leads the global wood furniture market in 2026?

Asia-Pacific leads by value and momentum, with 38.11% share in 2025 and the fastest regional CAGR of 6.23% through 2031.

Which application grows the fastest through 2031 in the global wood furniture market?

Hospitality furniture is growing at a 5.98% CAGR as renovations and modular contract systems scale across hotels and mixed-use properties.

How do regulations affect suppliers in the global wood furniture market?

United States TSCA Title VI requires third‑party certification for composite wood emissions, and EU rules require deforestation‑free due diligence with geolocation, which raises documentation and testing workloads.

Which wood types are gaining share in the global wood furniture market?

Engineered wood panels are forecast to expand at a 5.78% CAGR as nesting optimization, scheduling, and automation improve yield and lead times.

What channel dynamics matter most in 2026 for the global wood furniture market?

B2C remains dominant by value, while B2B and project channels accelerate, driven by hospitality and office fit-outs, supported by omnichannel investments and verified sourcing.

Page last updated on: