Folding Furniture Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

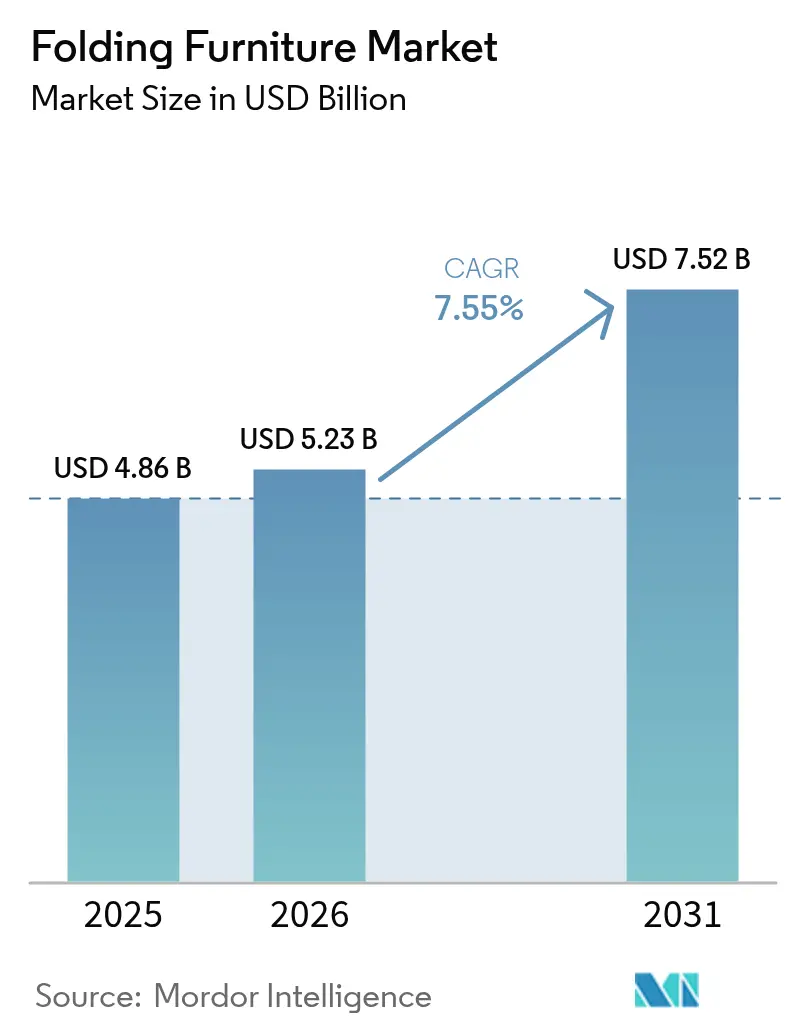

| Market Size (2026) | USD 5.23 Billion |

| Market Size (2031) | USD 7.52 Billion |

| Growth Rate (2026 - 2031) | 7.55% CAGR |

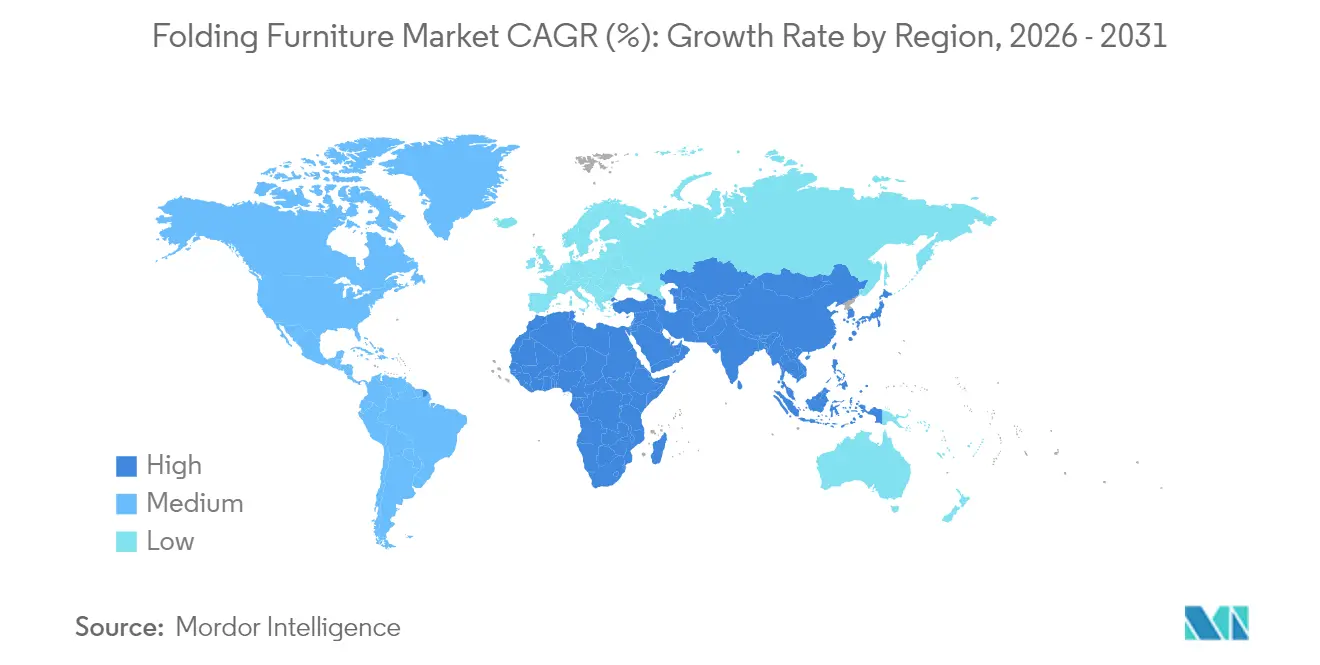

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Folding Furniture Market Analysis by Mordor Intelligence

Folding Furniture Market size in 2026 is estimated at USD 5.23 billion, growing from 2025 value of USD 4.86 billion with 2031 projections showing USD 7.52 billion, growing at 7.55% CAGR over 2026-2031.

Urban dwellers are trading aesthetics for utility as floor areas shrink, and the hybrid work wave has turned spare corners into home-office zones that require desks or benches able to vanish after hours. Retailers now report that 2025 buyers list versatility as a top decision factor, catapulting devices that can shift from seating to bedding or from workstation to shelving in a single motion. Metals are displacing heavier frames—unit weights are down since 2023—while maintaining ANSI/BIFMA load ratings, encouraging consumers who relocate often. Asia Pacific is expanding on the back of micro-apartment construction, public housing grants, and cost-competitive production hubs. Residential demand still drives sales, yet commercial buyers—hotels, schools, convention centers—accelerate faster as post-pandemic refurbishments call for reconfigurable layouts. Players wrestle with steel price swings and lingering durability concerns in upscale hospitality, but patented “one-touch” transformation mechanisms, integrated charging ports, and GREENGUARD certifications are widening premium margins and drawing affluent consumers.

Key Report Takeaways

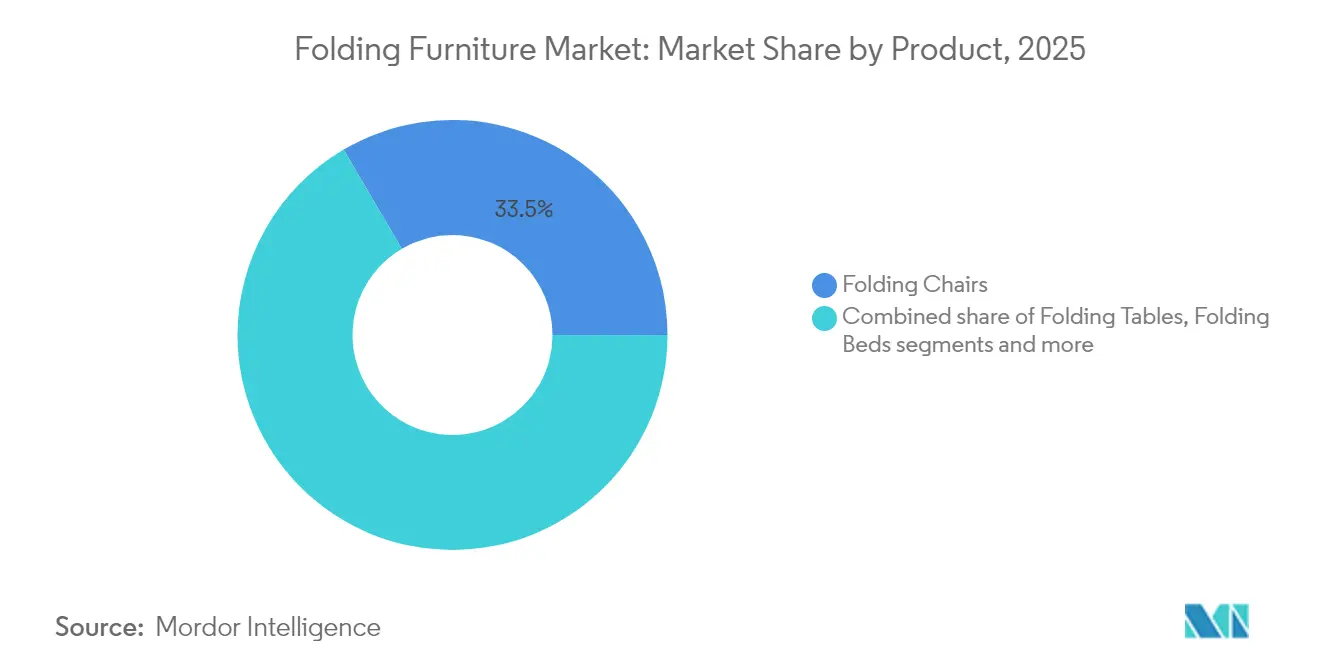

- By product category, folding chairs led with 33.45% of the folding furniture market share in 2025; folding beds are projected to record the fastest 7.6% CAGR through 2031.

- By material, wood secured a 35.60% revenue share in 2025, while metal products are forecast to expand at an 8.05% CAGR to 2031.

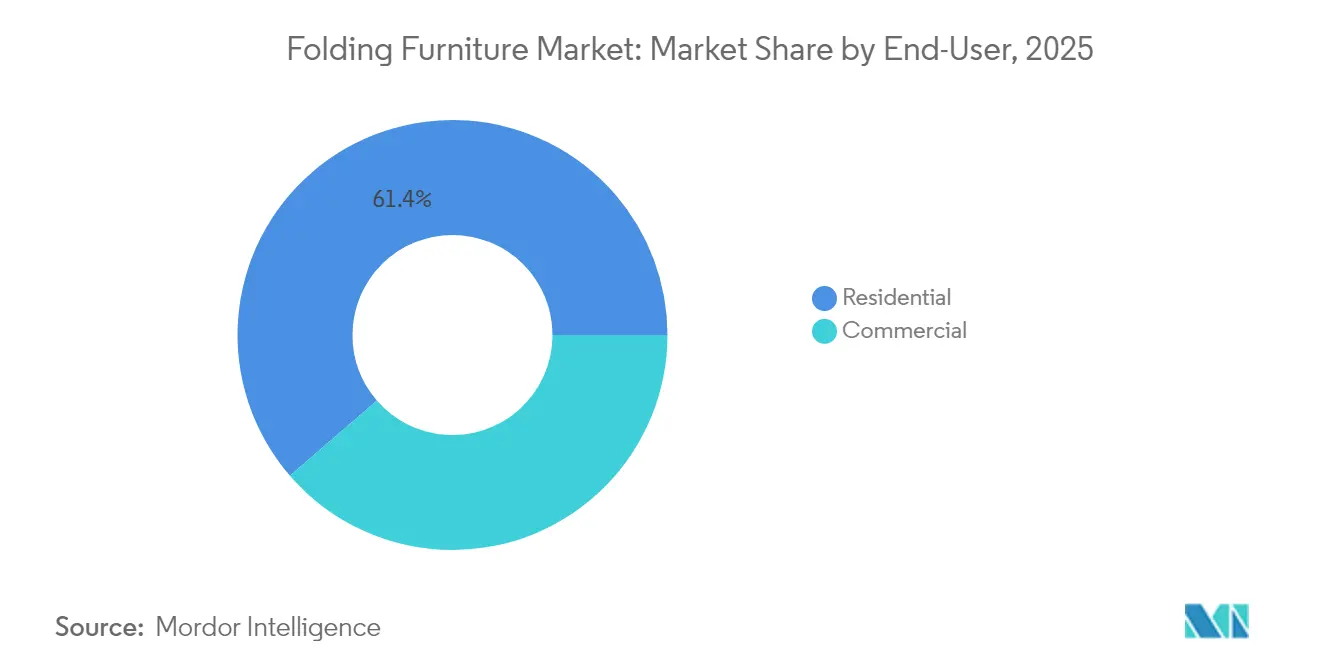

- By end user, the residential segment held 61.35% of the folding furniture market size in 2025, whereas commercial demand is advancing at a 7.9% CAGR.

- By distribution channel, B2C retail captured 78.40% sales in 2025; direct B2B procurement is growing with stronger margin resilience.

- By geography, Asia-Pacific dominated with 39.60% revenue in 2025 and is set to accelerate at a 7.7% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Folding Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Uptake of Micro-Apartments Requiring Space-Saving Furniture | +2.1% | Asia-Pacific, Europe, North America | Medium term (2-4 years) |

| Hybrid Work Culture Boosting Home-Office Folding Furniture | +1.8% | Global, with emphasis on North America & Europe | Short term (≤ 2 years) |

| Government Housing Subsidies Accelerating Multipurpose Furniture Adoption | +1.5% | North America, Europe, and emerging Asia-Pacific markets | Medium term (2-4 years) |

| Rising Demand for Multi-functional Furniture | +1.2% | Global | Long term (≥ 4 years) |

| Growing Commercial Applications | +0.8% | Global, with emphasis on Asia-Pacific & North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Uptake of Micro-Apartments Requiring Space-Saving Furniture

Penetration of folding furniture in urban dwellings under 500 ft² has increased, mirroring Asia-Pacific and European mega-cities where liveable floor plans shrink yearly. Residents prioritize transformability over décor, steering spend toward compact systems that turn kitchens into offices or bedrooms into lounges. Suppliers that engineer seamless, low-friction hinges and slimline frames now influence buying criteria more than color palettes. The folding furniture market, therefore, secures a recurring demand base that shows limited sensitivity to economic cycles and keeps replenishment sales elevated as micro-apartment turnover stays brisk.

Hybrid Work Culture Boosting Home-Office Folding Furniture

The 2024 JLL Global Future of Work survey, which captured input from 2,300 corporate real-estate leaders across 25 markets, indicates that 65% of companies intend to increase workplace flexibility by 2030 [1]JLL Research Team, “Global Future of Work Survey 2024,” JLL, jll.com. This shift is fuelling demand for fold-away desks and workstations that disappear once the workday ends. High-end models now include integrated cable channels, height-adjustable legs, and quick-lock latches that replicate the ergonomics of fixed office furniture. Manufacturers that have targeted this niche are earning stronger margins than their legacy ranges, pointing to a lasting profit pool as hybrid work solidifies.

Rising Demand for Multi-Functional Furniture

Urban residents increasingly want furniture that can change roles throughout the day, think a coffee table that rises into a dining surface or a wall unit that unfolds into a guest bed. This appetite goes beyond simple space-saving; it reflects a desire for flexible lifestyles that let the same square footage serve work, leisure, and rest without compromise. Makers that weave smart features, USB-C charging hubs, voice-activated lifts, or one-touch foldaway mechanisms into their designs are winning the affluent crowd and capturing fatter margins than standard lines. Expect the momentum to build as more people treat their homes as adaptable hubs rather than fixed layouts.

Growing Commercial Applications

Hotels, schools, and activity-based offices specify reconfigurable furniture to raise revenue per square foot and create adaptive classrooms. Corporate companies are shifting towards desk-sharing models stimulates bulk orders for durable, lightweight tables and nesting chairs. Commercial projects command larger order sizes and long-term maintenance contracts, stabilizing manufacturer capacity utilization and margin forecasts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Durability Concerns Limiting Premium Hospitality Procurement | -0.6% | Global, with emphasis on North America & Europe | Medium term (2-4 years) |

| Steel Price Volatility Compressing Manufacturer Margins | -0.4% | Global, with the highest impact in Asia-Pacific | Short term (≤ 2 years) |

| Price-Based Competition Eroding Brand Loyalty | -0.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Durability Concerns Limiting Premium Hospitality Procurement

High-end hotels still suspect that folding frames fatigue quicker than fixed alternatives, curbing adoption despite rigorous ANSI/BIFMA X5.1 certifications [2]Business and Institutional Furniture Manufacturers Association, “ANSI/BIFMA X5.1-2022 Office Seating,” BIFMA, bifma.org. Luxury operators demand multi-year stress-test data and silent hinges that protect guest sleep quality. Manufacturers that publish third-party load validation are slowly easing the perception gap, though sales cycles remain longer than mid-tier hospitality projects.

Steel Price Volatility Compressing Manufacturer Margins

Global steel spot prices jumped erratically in 2024-2025, squeezing mid-market producers that lack hedging sophistication or premium brand positioning[3]Jane Doe, “Steel Volatility Hits Furniture Manufacturers in 2025,” Furniture Today, furnituretoday.com. Many introduced aluminum-hybrid or composite frames that cut steel input by 30%, but retooling costs and learning curves temporarily trimmed EBITDA. Wider adoption of commodity futures and index-linked contracts should tame the threat over the coming years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Momentum Shifts from Chairs to Beds

Folding chairs contributed 33.45% revenue in 2025, anchoring the folding furniture market with a ubiquitous presence in homes, schools, and events. Upgraded lumbar contours, mesh backrests, and molded edges now mirror traditional task seating, enhancing perceived value. The segment’s installed base also fuels aftermarket cushion, glide, and replacement-bolt revenues. Folding beds, while smaller in volume, climb fastest at 7.6% CAGR through 2031. Demand roots in micro-apartments where wall-mounted frames reclaim daytime floor area, and in guest rooms transforming into home-office spaces overnight. Integrated strut-assist pistons shorten setup to seconds, a decisive buying hook cited by young professionals.

Manufacturers cross-pollinate design cues between these categories, spawning convertible chair-bed hybrids that slot into the premium tier. Meanwhile, folding tables hold a sizable share across conference venues and catering rentals, benefiting from powder-coated frames that resist denting during transport. Sofas, loveseats, and storage cubes represent nascent but promising subsegments that surf the same multifunctional living trend.

By Material: Wood Retains Charm While Metal Accelerates

Wood enjoys a 35.60% share of 2025 revenue, powering the fold-flat coffee tables, expandable dining sets, and bamboo laptop desks preferred by style-sensitive urbanites. Sustainably harvested rubberwood, bamboo, and reclaimed timber variants lift the eco profile without sacrificing rigidity. Metal, however, advances at an 8.05% CAGR as high-tensile steel and 6000-series aluminum alloys shave 30% off product weight yet sustain 250 lb static loads. These gains protect hinges from premature wear and enable slimmer silhouettes that fit in car trunks and apartment closets.

Composite innovations are reshaping the folding furniture market size trajectory for premium SKUs. Powder-bonded fiberboard cores wrapped in veneer deliver a wood feel while beating solid timber on warp resistance. Hybrid frames that sandwich an aluminum beam between plywood panels reinforce stress zones and pass BIFMA drop tests. The material arms race ultimately widens differentiation and lets brands command varied price ladders across channels.

By End User: Residential Dominates, Commercial Accelerates

Apartments and small homes still anchor 61.35% of the 2025 demand, making the residential tier the folding furniture market’s largest revenue pool. Penetration skews highest among units below 800 ft², where buyers juggle living, sleeping, and working zones in one open footprint. The segment’s digital-native shoppers embrace augmented-reality apps that confirm fit and demonstrate transformation animations in situ, lifting e-commerce conversion rates.

Commercial buyers fuel faster 7.9% CAGR growth through 2031. Hospitalities retrofit banquet halls into breakout rooms; classrooms add mobile desks for group activities; corporate hubs embrace huddle spaces for brainstorming, then fold tables away for yoga classes. Procurement teams weigh total-cost-of-ownership ratios, focusing on life-cycle durability, stacking efficiency, and extended warranties. Brands meeting ANSI/BIFMA and GREENGUARD standards often clinch multi-year framework deals, securing production visibility.

By Distribution Channel: Retail Commands, Direct B2B Gains

Retail outlets and pure-play e-commerce together moved 78.40% of the 2025 share, illustrating the folding furniture market’s consumer-driven DNA. Specialty marketplaces now eclipse generalist platforms for online purchases as shoppers seek niche SKUs and 3-D room-planning tools that visualize folding cycles. Home centers still move entry-level metal-frame chairs at volume, while boutique showrooms push coordinated modular systems at premium price points. Click-and-collect and rapid-ship options shorten delivery windows, an expectation codified by gig-economy tenants who relocate frequently.

Direct B2B distribution stakes a 21.60% slice of the folding furniture market size and draws higher gross margins. Manufacturers nurture vertical-specific teams for hospitality, education, and corporate fit-outs, bundling on-site training and maintenance kits. Quick-response OEM capabilities—cutting new molds within six weeks—encourage chain hotels and public-school districts to standardize specifications. Omnichannel overlap is advancing brand-run showrooms that double as trade portals, and large institutional buyers increasingly test demos in consumer pop-ups before bulk ordering.

Geography Analysis

Asia-Pacific anchors the folding furniture market with 39.60% revenue in 2025 and sustains a 7.7% CAGR to 2031 as megacities densify faster than infrastructure expansions. China leverages domestic demand and export-ready supply chains, while India’s booming middle class steers e-commerce platforms toward folding desks and beds that solve space headaches in tier-2 cities. Policy levers—Singapore’s Smart-Home Initiative and Malaysia’s MyHome rebates—explicitly reward compact furnishings, reinforcing mainstream uptake. Japan continues to debut space-efficient origami-inspired mechanisms adopted globally, and South Korea melds IoT sensors into frames that count fold cycles and flag maintenance needs.

North America ranks second by value, driven by the United States’ premium bias and Canada’s sustainability tilt. Urban lofts in New York, San Francisco, and Toronto treat folding dining sets as everyday essentials, while suburban homeowners purchase portable tables for seasonal gatherings and home gyms. The hybrid work surge sparks U.S. demand for fold-away sit-stand desks that vanish post-workday, maintaining mental boundaries in shared living spaces. Mexico's hospitality-led growth funnels government tourism incentives into flexible guest-room layouts that optimize occupancy rates.

Europe exhibits high design sophistication and stringent durability norms forged in centuries-old city footprints that demand creative use of square footage. The United Kingdom leads smart folding furniture adoption, integrating Bluetooth-linked motors and Alexa routines. Germany’s engineering culture prizes precision hinges crafted to micron tolerances, supporting premium pricing shields. France blends couture styling with functional bones, pioneering slimline wall beds disguised as art panels. Italy and Spain post above-average growth as boutique hotels refresh interiors for multipurpose events, while Eastern European capitals such as Warsaw and Bucharest open fertile ground for mass-market imports.

Competitive Landscape

The folding furniture market remains moderate, leaving room for agile challengers. IKEA capitalizes on vertically integrated sourcing and flat-pack logistics, reinforcing cost leadership and global reach. Resource Furniture LLC defends an upscale niche by patenting counterbalanced wall-bed mechanisms that users elevate with two fingers, carving a moat through intellectual property. Lifetime Products’ acquisition of Plastic Development Group broadens plastic-top table capacity, signaling consolidation momentum focused on scale economies.

Technology has shifted competitive battlegrounds. Zinus Inc. wins share via tool-free snap-lock connectors that cut assembly time to five minutes, delighting renters wary of landlord penalties from wall mounts. Hettich adds silent self-closing hinges into OEM collaborations, monetizing hardware expertise across desk, bed, and cabinet frames. ANSI/BIFMA certifications emerge as gating criteria in RFPs, prompting midsize factories to invest in cycle-test rigs and environmental chambers. GREENGUARD labels unlock procurement budgets in education and healthcare segments that prioritize indoor air quality.[4]John Smith, “Why BIFMA Certification Sets the Bar for Furniture Quality,” BIFMA, bifma.org

Price competition intensifies in the mid-market, where commoditized steel-tube chairs flood online channels. Yet premium and value segments see steadier margins—high end via design patents and smart integrations, low end via volume scale and austere feature sets. Direct-to-consumer newcomers deploy social-video tutorials to demystify wall-bed installation and sidestep retailer mark-ups. Incumbents respond by launching digital configurators and subscription upgrade bundles that swap worn panels for refreshed finishes.

Folding Furniture Industry Leaders

Leggett & Platt Inc.

Dorel Industries Inc.

IKEA

Lifetime Products Inc.

Meco Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Dorel Home consolidated residential operations into its Cosco division to sharpen its folding furniture focus.

- May 2025: MityLite reaffirmed GREENGUARD certification across folding product lines, underscoring low VOC emissions

- July 2024: Titus Group introduced the Set F450 Bi-Fold and Set P700 Hideaway folding door systems for wardrobes and bedrooms, adding smoother movement and better space efficiency to its hardware line.

- June 2024: Howe, working with Jones & Partners, unveiled Folding Surfaces, a mobile double-folding bench that broadens its portfolio of space-saving furniture for flexible environments.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the folding furniture market as new, factory-built tables, chairs, beds, sofas, desks, storage units, and related items designed to collapse, stack, or nest for compact storage and easy transport; values are expressed in USD at manufacturer selling price, inclusive of OEM and private-label production. According to Mordor Intelligence, demand spans residential micro-apartments, hospitality banqueting halls, classrooms, pop-up retail, and portable office kits.

Scope exclusion: knock-down "ready-to-assemble" furniture that cannot be repeatedly folded is outside the present scope.

Segmentation Overview

- By Product

- Folding Chairs

- Folding Tables

- Folding Beds

- Folding Sofas & Loveseats

- Folding Desks & Workstations

- Folding Storage Units

- Other Folding Furniture

- By Material

- Wood

- Metal

- Plastic

- Other Materials

- By End-User

- Residential

- Commercial

- By Distribution Channel

- B2C/Retail

- Home Centers

- Specialty Furniture Stores

- Online

- Other Distribution Channels

- B2B/Directly from Manufacturers

- B2C/Retail

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Middle East And Africa

- United Arab of Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Over multiple structured interviews and pulse surveys with furniture OEM executives, contract manufacturers, real-estate developers, institutional buyers, and specialty retailers across Asia-Pacific, North America, and Europe, we were able to verify penetration rates, discount structures, and emerging material preferences (powder-coated steel versus engineered wood). These conversations helped us stress-test growth drivers cited during desk work and resolve unit-conversion quirks before final modeling.

Desk Research

We initiated desk work by mapping production, trade, and consumption indicators available from tier-one public sources such as UN Comtrade shipment codes for metal and wooden furniture, UN-DESA urbanization data, Eurostat structural business statistics, US Census Current Industrial Reports, and national housing-completion bulletins. Company 10-Ks, patent filings captured through Questel, and price trackers within Dow Jones Factiva allowed us to benchmark average selling prices and raw-material sensitivity. Supplementary insights were drawn from trade associations, for example, BIFMA and the China National Furniture Association, plus periodic academic journals that test load-bearing performance of space-saving frames.

Mordor's paid access to D&B Hoovers enriched the desk phase with revenue splits for leading OEMs, while shipment micro-data from Volza clarified cross-border flow patterns of foldable chairs. The sources listed illustrate our evidence base; many additional references supported data checks, narrative context, and assumption vetting.

Market-Sizing & Forecasting

A top-down demand pool was first built from new housing completions, commercial floor additions, and average units installed per square meter, which are then multiplied by validated ASPs to derive the 2025 baseline. Selected bottom-up cross-checks, supplier roll-ups, and sampled online SKU sales provided reasonableness tests. Key variables tracked include urban dwelling size, e-commerce furniture share, mild-steel price index, hospitality capex cycles, and hybrid-work adoption. Multivariate regression married these drivers with historical sales to project CAGR through 2030, while scenario analysis bounded upside from rapid prefabricated housing rollouts. Gaps in producer counts inside fragmented emerging markets were bridged through regional proxy coefficients agreed during expert calls.

Data Validation & Update Cycle

Model outputs pass variance scans against historical trade values and independent customs tallies, followed by two-tier analyst review. Reports refresh annually; extraordinary events such as tariff shocks trigger interim recalibration, ensuring clients receive the latest vetted view at delivery.

Why Mordor's Folding Furniture Baseline Commands Reliability

Published estimates often diverge because analysts pick different product cutoffs, currency bases, and refresh cadences. Our disciplined scope choice and yearly model rebuild narrow those gaps for decision-makers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.86 B (2025) | Mordor Intelligence | - |

| USD 4.77 B (2025) | Global Consultancy A | Excludes fold-flat storage units and counts only household demand |

| USD 11.14 B (2025) | Industry Association B | Uses retail receipts, double-counting distributor margins and mixed ready-to-assemble stock |

The comparison shows that when definitions widen to retail or narrow to select SKUs, totals swing sharply. Mordor's balanced middle path, factory value basis, repeat-fold functionality, and transparent variable tracking deliver a stable baseline executives can replicate and challenge with confidence.

Key Questions Answered in the Report

What is the folding furniture market’s expected growth trajectory through 2031?

The market is projected to rise from USD 4.86 billion in 2025 to USD 7.52 billion by 2031, posting an 7.55% CAGR.

Which region offers the strongest growth outlook for folding furniture?

Asia-Pacific leads with 39.60% revenue in 2025 and the fastest regional CAGR of 7.7% through 2031, supported by rapid urbanization and housing incentives.

Which product categories are expanding the fastest?

Folding beds record the highest 7.6% CAGR as urban consumers seek multifunctional pieces, while folding chairs remain the largest revenue generator at 33.45% share.

How are materials trends shifting in the industry?

Wood holds the largest 35.60% share, but metal products are scaling faster on an 8.05% CAGR due to lightweight, high-strength alloys that ease transport and assembly.

Which challenges most affect manufacturers’ profitability?

Durability perceptions in premium hospitality and steel price volatility are trimming margins, prompting investment in composite materials and expanded BIFMA-certified testing.

Page last updated on: