Sofa Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

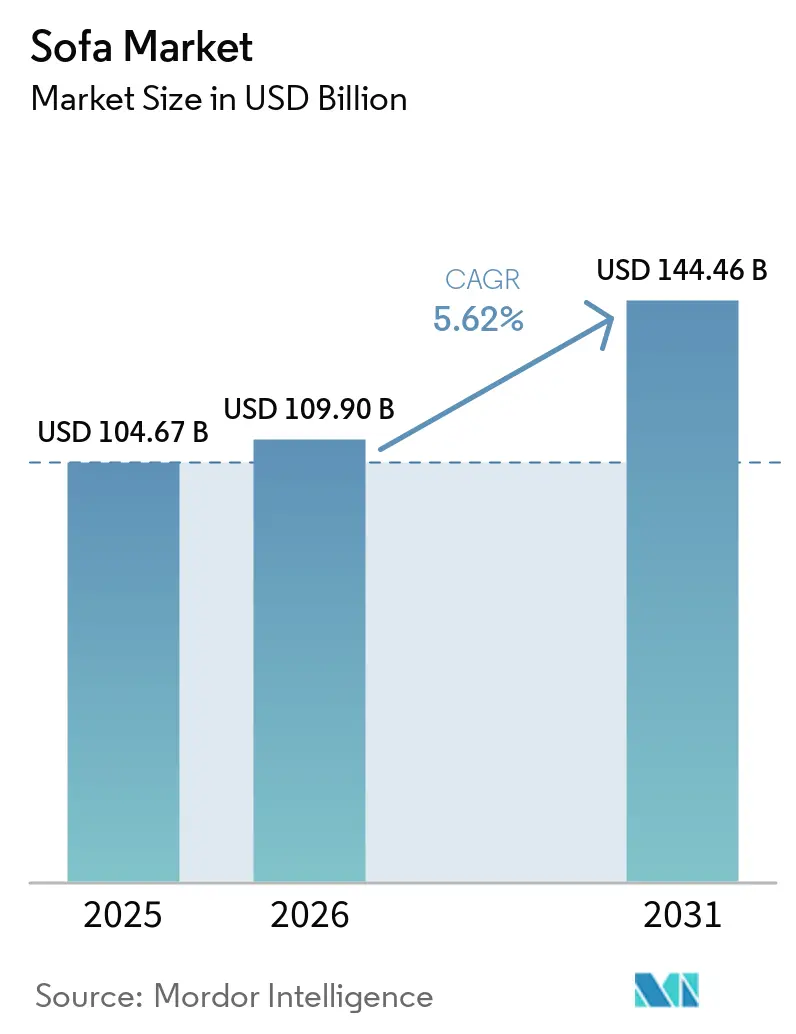

| Market Size (2026) | USD 109.90 Billion |

| Market Size (2031) | USD 144.46 Billion |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sofa Market Analysis by Mordor Intelligence

The sofa market size was valued at USD 104.7 billion in 2025 and estimated to grow from USD 109.9 billion in 2026 to reach USD 144.5 billion by 2031, at a CAGR of 5.6% during the forecast period (2026-2031). Growth reflects urbanization-led first purchases, recurring contract refurbishments, and better revenue per unit as premium and modular formats gain acceptance across the sofa market. Mature regions still face pressure from polyurethane foam cost swings, tariff escalation, and softer housing turnover in the United States and Europe, which keeps the upside measured rather than abrupt. Even so, the sofa market continues to benefit from apartment-led living patterns, digital buying tools, and renovation spending that support replacement demand across multiple buyer groups. New upholstery rules tied to PFAS-free and low-VOC materials are already changing sourcing decisions and could separate certified suppliers from manufacturers that still rely on older chemistries [1]California State Legislature, “AB 1817 Product Safety, Textile Articles Containing Regulated Perfluoroalkyl And Polyfluoroalkyl Substances,” California Legislative Information, leginfo.legislature.ca.gov . China may also add support on the demand side because the 15th Five-Year Plan targets stronger domestic consumption, which aligns with how major manufacturers are positioning product development for the sofa market.

Key Report Takeaways

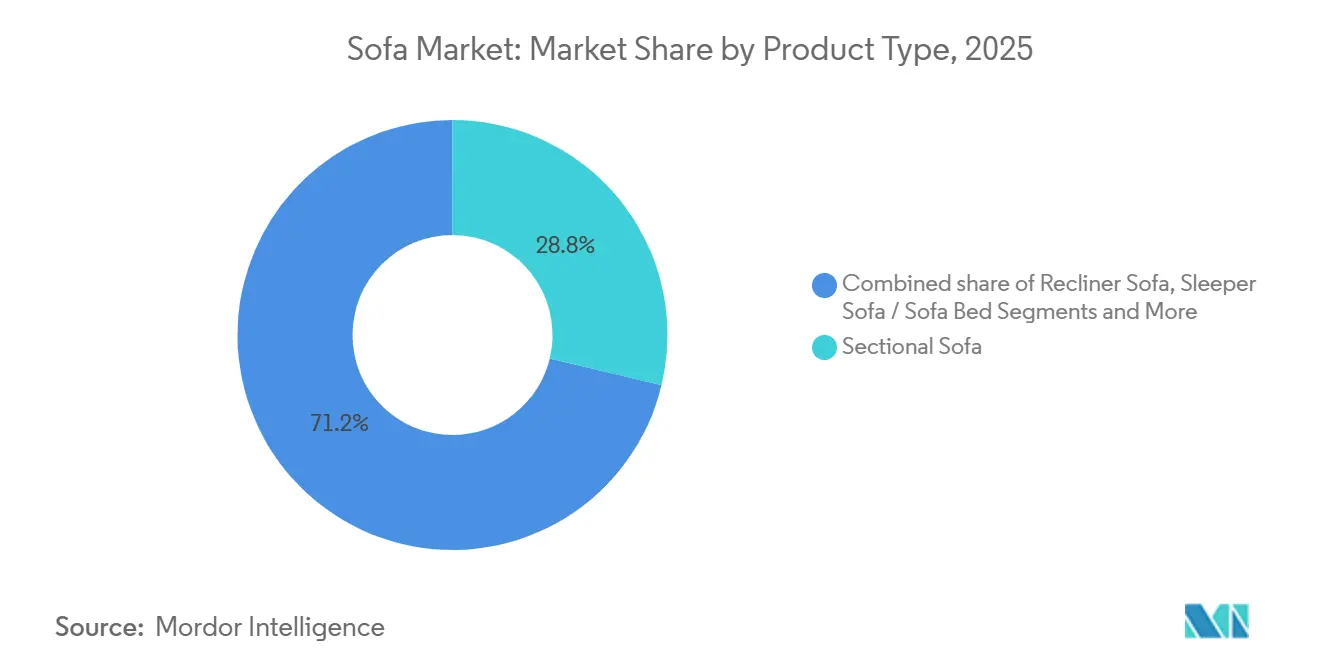

- By product type, sectional sofas led with 28.76% share in 2025 in the sofa market, while recliner sofas are forecast to grow at 6.11% CAGR through 2031.

- By price range, mid-range held 45.66% share in 2025 in the sofa market, while premium is projected to grow at 5.85% CAGR through 2031.

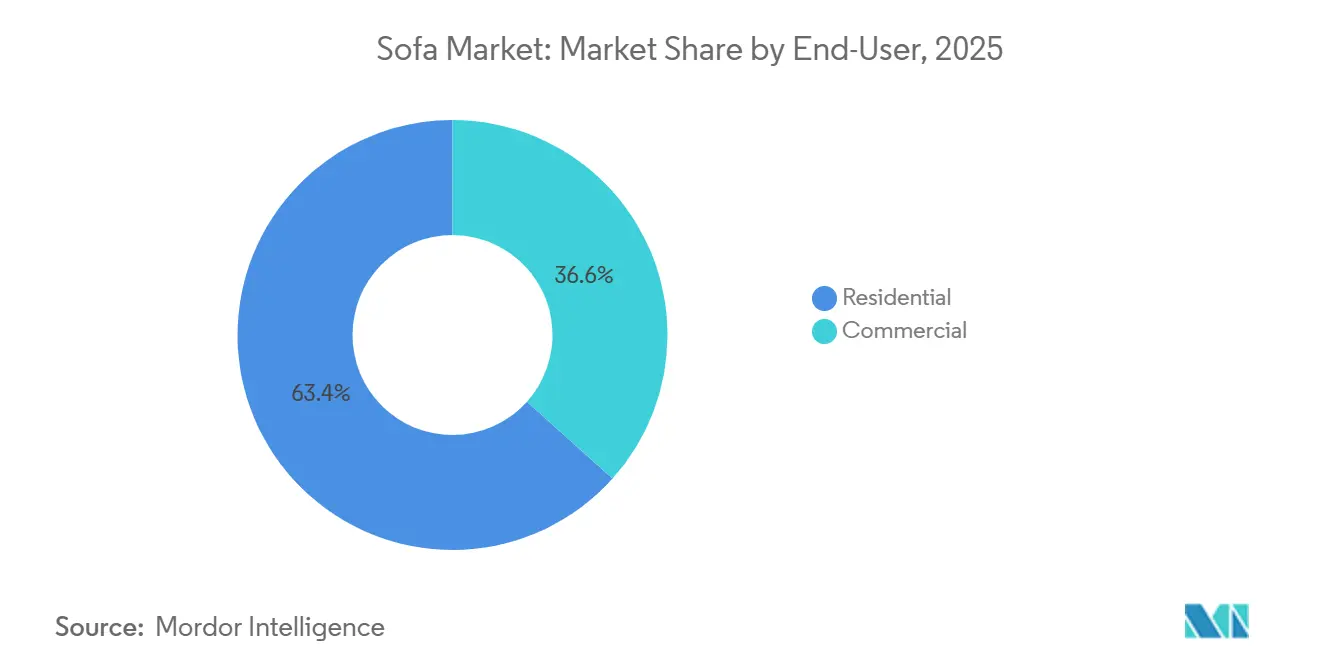

- By end-user, residential held 63.36% share in 2025 in the sofa market, while commercial is projected to expand at 6.61% CAGR through 2031.

- By distribution channel, B2C retail held 67.41% share in 2025 in the sofa market, while B2B project channels are forecast to grow at 6.54% CAGR through 2031.

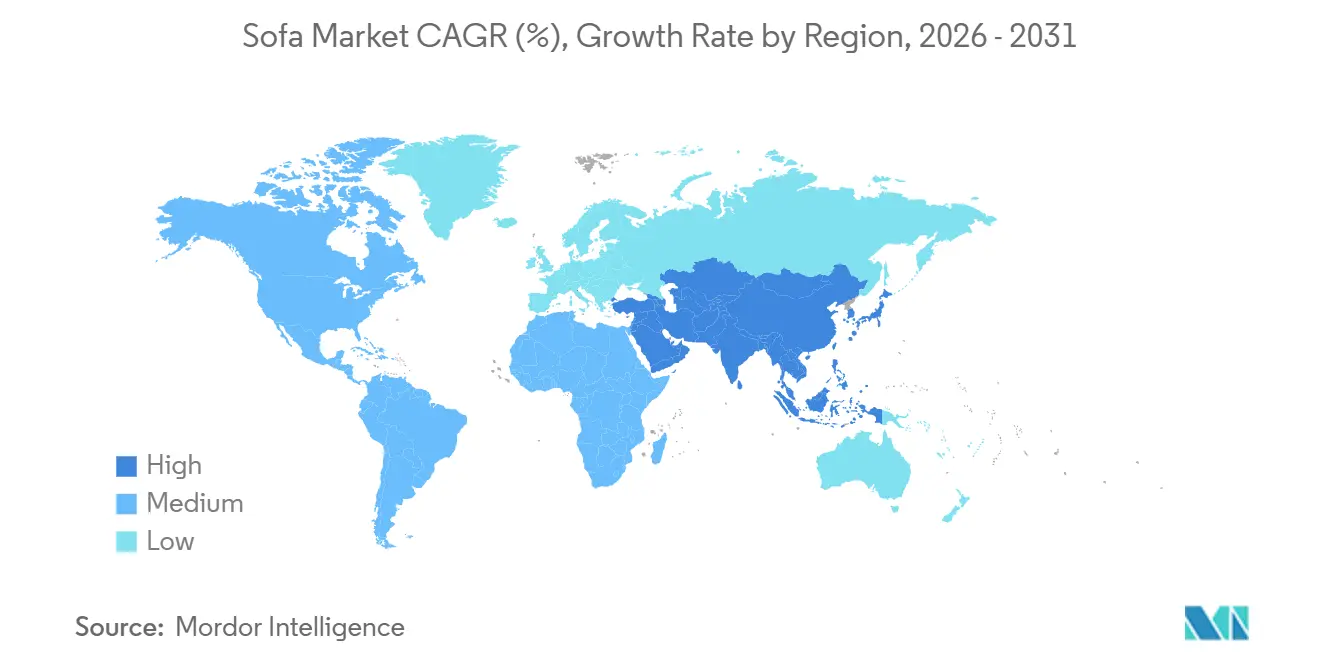

- By geography, Asia-Pacific held a 34.48% share in the sofa market in 2025, and is projected to expand at a 6.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sofa Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban Apartment Growth Lifting Sectional And Sofa-Bed Demand | +1.2% | Global, strongest in Asia-Pacific, South America, the Middle East, and Africa | Long term (≥ 4 years) |

| E-Commerce Visualization Reducing Big-Ticket Purchase Friction | +0.9% | Global, led by North America, Europe, and China | Medium term (2-4 years) |

| Home Renovation And Premium Interior Spending Supporting Replacement Demand | +0.8% | North America and Europe, with spillover to Gulf Cooperation Council countries and Oceania | Medium term (2-4 years) |

| Hospitality And Workplace Lounge Refurbishment Expanding Contract Demand | +0.7% | Global, concentrated in Asia-Pacific and the Middle East | Medium term (2-4 years) |

| PFAS-Free And Low-VOC Performance Upholstery Becoming A Purchase Trigger | +0.5% | North America and core Europe, extending to Asia-Pacific export markets | Short term (≤ 2 years) |

| Knock-Down Modular Engineering Easing Last-Mile And Stairwell Constraints | +0.6% | Global, strongest in high-rise urban markets across Asia-Pacific, Europe, and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Urban Apartment Growth Lifting Sectional and Sofa-Bed Demand

Urban densification is a structural driver of the sofa market rather than a short-cycle effect. As home sizes shrink across Asia, Latin America, and Southern Europe, households are choosing sectional sofas and sofa-beds because one purchase can cover seating, occasional sleeping, and room zoning. Inter IKEA said in its FY25 Annual Report that alternative sofa designs using renewable and recycled foam performed well in FY25, and that it would maintain wholesale price stability into FY26 to protect affordability [2]Inter IKEA Holding B.V., “Annual Report FY25,” Inter IKEA Group, inter.ikea.com . In India, rapid urban housing programs are creating more first-time apartment buyers in Tier-2 and Tier-3 cities, which supports demand for compact living room furniture. The sofa market is therefore finding new demand nodes outside the largest capitals, where new housing supply is growing faster than in saturated metros. This pattern matters because secondary cities generate new purchase occasions rather than solely replacement demand.

E-Commerce Visualization Reducing Big-Ticket Purchase Friction

Digital visualization is lowering purchase friction in the sofa market by reducing uncertainty around fit, layout, and style. Inter IKEA Systems launched the IKEA 3D Experience in February 2025, which lets customers scan rooms, place true-to-scale sofa models, and receive layout guidance through mobile devices. That move directly addresses the size and placement concerns that once kept many sofa transactions tied to physical showrooms. Mid-market retailers are also deploying 360-degree views, WebAR, and room planners, which shows that visualization tools are no longer limited to the largest chains. As this spreads, the sofa market can shift more product discovery into digital channels while retailers direct more spending toward fulfillment and white-glove delivery. The result is not the end of stores, but a different role for stores inside the buying journey.

Home Renovation and Premium Interior Spending Supporting Replacement Demand

Home renovation activity continues to support replacement purchases in the sofa market, especially at the higher end. Harvard University’s Joint Center for Housing Studies projects annual United States homeowner improvement spending at USD 518 billion by the end of 2026, even though growth moderates to 1.6% year over year by year-end as housing constraints persist. Spending plans remain more resilient among higher-income households, which helps explain why premium replacement demand is holding up better than broad consumer demand. FCI London’s 2025 renovation data also showed that living room spending, led by modular and premium sofas, captured a large share of luxury renovation budgets. Ashley Furniture responded to this shift in April 2026 with the Ashley Luxe launch, which introduced 5 premium collections built around upgraded materials and finishes at more accessible price points. The sofa market, therefore, benefits when renovation budgets remain active, even if housing turnover remains soft.

Hospitality and Workplace Lounge Refurbishment Expanding Contract Demand

The contract channel is the fastest-growing end-user path in the sofa market, and hospitality is the main reason. Hotel operators are still working through a backlog of pandemic-delayed property improvement plans, which keeps lounge and suite seating active in refurbishment budgets. This demand is increasingly tied to compliance because commercial buyers are placing greater emphasis on low-VOC interiors, traceable wood, and documented environmental practices. That shift gives suppliers an advantage to demonstrate ISO 14001 alignment and FSC chain-of-custody documentation during specification reviews. In France, the contract furniture market was valued at EUR 675 million (USD 742 million) in 2025 and accounted for 5% to 6% of total furniture revenue, supported by hotel repositioning, restaurant upgrades, and co-working projects. As a result, the sofa market is seeing contract procurement move closer to a recurring capital program rather than a short-term buying cycle.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Foam, Leather, And Freight Volatility Squeezing Gross Margins | -1.1% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Price Pressure From Low-Cost Imports And Unorganized Local Makers | -0.8% | Asia-Pacific and Latin America | Short term (≤ 2 years) |

| EPR, Deforestation, VOC, And Flammability Compliance Costs Rising | -0.6% | Europe and North America, gradually extending to the Asia-Pacific | Medium term (2-4 years) |

| Bulky-Item Returns And Reverse Logistics Eroding Online Unit Economics | -0.5% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Foam, Leather, and Freight Volatility Squeezing Gross Margins

Input volatility is the most immediate margin risk facing the sofa market in 2026. A major disruption at LyondellBasell’s Bayport Choate propylene oxide facility tightened supply and pushed domestic foam quotes higher in early 2026. The United States producer price index for furniture-grade polyurethane foam rose to 281.9 in April 2026, up from 267.6 in December 2025, indicating that cost pressure remained elevated well into the year [3]U.S. Bureau of Labor Statistics and Federal Reserve Bank of St. Louis, “Producer Price Index by Industry, Furniture-Grade Polyurethane Foam,” FRED, fred.stlouisfed.org . Leather adds another layer of strain, with the Yale Budget Lab projecting prices to remain 22% above pre-disruption levels for 1 to 2 years because of tariff exposure across major producing countries. Natuzzi’s 2025 revenue was USD 332.9 million, and its Q4 2025 gross margin fell to 30.2% from 38.1% as it shifted more Editions production from China to Italy to reduce tariff exposure. This shows how the sofa market can face higher costs even when companies take steps to reduce trade risk.

Price Pressure from Low-Cost Imports and Unorganized Local Makers

The sofa market remains exposed to price pressure from both industrial-scale exporters and informal local workshops. That pressure is amplified by fragmentation, as the top 5 players accounted for only 10.7% of global revenue in 2025, limiting broad pricing discipline. Man Wah sold 1.82 million sofa sets in FY2026, while its China revenue fell 6.8% to HKD 9.25 billion (USD 1.19 billion), as management cited industry overcapacity and stronger online price competition. The next challenge is that Chinese producers are expanding production in other countries, which means cost-competitive supply can continue even when tariffs target one origin. At the same time, local workshops keep price benchmarks low across South Asia, Latin America, and parts of Africa. Over time, PFAS rules and EPR obligations may raise the minimum compliance threshold enough to pressure some economy-tier producers. However, the near-term effect in the sofa market is still price compression.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Recliner Momentum Diversifying Beyond the Sectional Core

Sectional sofas held 28.76% of the sofa market share in 2025, keeping them at the center of the market by volume and room relevance. Their lead comes from the layout flexibility of apartments across Asia-Pacific and North America, where a single seating system often needs to support multiple uses. Recliner sofas are forecast to grow at 6.11% CAGR from 2026 to 2031, making them the fastest-moving product type in the sofa market. Man Wah reported sofa and ancillary products revenue of HKD 11.25 billion (USD 1.45 billion) in FY2026. In contrast, North America revenue rose 2.6% to HKD 4.54 billion (USD 583 million), on stronger average selling prices and the December 2025 Gainline acquisition.

That pattern shows that recliner growth is being supported by functionality and price mix, not just unit demand. Sleeper sofas also benefit from micro-apartments and short-term rentals, where a single product must serve as both seating and guest accommodation. IKEA widened this need set through the GRUNNARP sleeper sofa and its SALTMYRAN and LILLESÄTER seating additions across 2025 and 2026. Chaise, daybed, loveseat, and fixed-frame formats remain relevant in premium residential, boutique hospitality, entry-level residential, and commercial settings. Compliance costs are rising across all product groups, but they are most difficult for economy- and mid-range-upholstery, where older stain-repellent chemistry was more widely used.

By Price Range: Mid-Range Anchors Volume While Premium Captures Value Growth

Mid-range products accounted for 45.66% of the sofa market in 2025, keeping that tier as the main volume arena for scale players. IKEA, Ashley Furniture, and Man Wah’s CHEERS brand remain important here because affordability, broad assortment, and channel reach still shape buying decisions for much of the sofa market. Premium is projected to grow at a 5.85% CAGR through 2031, the fastest pace among price bands. Ashley Furniture’s April 2026 launch of Ashley Luxe shows how a company long associated with mid- to economy ranges is moving up to participate in that faster value pool.

Inter IKEA also said in FY25 that alternative sofa materials with renewable and recycled content performed well and were moving into pilot production, pointing to a more premium material mix even in mid-market offerings. Economy sofas still matter in emerging residential channels and value retail, but regulatory changes are raising the cost floor for producers that relied on legacy fluorinated finishes. California, Colorado, and Minnesota all moved forward with PFAS restrictions affecting upholstered furniture sold in major United States markets, which require reformulation of foam and fabric inputs. The premium ceiling is also widening because higher-income households continue to plan heavier home furnishings spending in 2026, providing the sofa market with a more resilient source of revenue at the top end.

By End-User: Commercial Momentum Outpacing Residential on a Per-Segment Growth Basis

Residential buyers represented 63.36% of the sofa market size in 2025, reflecting the category’s long-standing tie to household formation and home replacement cycles. Apartment purchases, living room refreshes, and renovation projects still make residential the largest use case in the sofa market. Commercial demand is forecast to grow at a 6.61% CAGR from 2026 to 2031, faster than any other end-user group. That growth comes from hotel refurbishment, co-working lounge expansion, and senior-living procurement, which often sit within multi-year capital plans rather than short retail cycles.

Harvard JCHS projects United States homeowner improvement spending at USD 518 billion in 2026. Still, it expects growth to slow to 1.6% by the end of the year, suggesting residential replacement will remain active but more measured. Commercial demand looks more durable in regions where hotel construction and renovation pipelines remain open. France’s contract furniture market reached EUR 675 million (USD 742 million) in 2025, supported by hotel repositioning, restaurant design, and coworking upgrades. Procurement standards are also becoming stricter, with ISO 14001-style environmental management and FSC chain-of-custody documentation gaining importance in supplier selection. That gives the sofa market a clearer compliance-based path to growth in contract channels than in price-sensitive consumer channels.

By Distribution Channel: B2B Project Velocity Challenges B2C Volume Dominance

B2C retail accounted for 67.41% of revenue in 2025, making it the dominant route to market for sofas. Home centers, specialty furniture stores, branded showrooms, and online platforms still capture most consumer purchase occasions. La-Z-Boy’s October 2025 acquisition of a 15-store network in Georgia, Florida, and Tennessee added around USD 80 million in annual sales. It lifted the number of company-owned stores to 220, or 60% of its franchise network, underscoring the value of tighter retail control. B2B project business is nevertheless growing faster, at a 6.54% CAGR through 2031, as hospitality groups and build-to-rent operators centralize procurement into larger contracts.

Online remains an important growth channel for the sofa market, but bulky-item returns and reverse logistics continue to weigh on unit economics. That is why retailers are investing in AR-led room planning before purchase and in knock-down modular engineering to reduce damage and shipping friction. Local workshop channels also remain relevant in countries where import duties and weaker last-mile infrastructure favor nearby production. In Europe, producer responsibility schemes such as Valobat are adding declaration and reporting obligations, increasing administrative complexity for importers serving multiple countries. The result is a channel structure where B2C still leads volume, while B2B offers cleaner visibility and faster growth for the sofa market.

Geography Analysis

Asia-Pacific held 34.48% of the sofa market share in 2025 and is projected to expand at 6.75% CAGR through 2031. China remains the largest national market in the region, even though Man Wah’s domestic revenue fell 6.8% to HKD 9.25 billion (USD 1.19 billion) in FY2026 amid saturation and online price pressure. The sofa market in China may still see policy support, as the 15th Five-Year Plan targets stronger domestic consumption, and leading manufacturers are aligning their product development in that direction. India follows a different path, with government-backed housing programs creating first-time apartment buyers in Tier-2 and Tier-3 cities who need compact living room solutions. Japan and South Korea add mature, design-led demand. At the same time, Southeast Asia supports both regional consumption and a large share of global upholstery manufacturing, keeping Asia-Pacific central to the sofa market.

North America is projected to grow at a 3.9% CAGR through 2031, reflecting a mature replacement cycle in the sofa market. United States homeowner improvement spending is projected at USD 518 billion in 2026, but remodeling growth slows to 1.6% by year-end, which tempers sofa replacement linked to housing turnover. IKEA United States plans 10 new stores in 2026, including urban formats in Chicago and Los Angeles, which shows that retailers are still targeting apartment-led demand despite the slower backdrop. Europe is expected to grow at 3.6% CAGR, with demand constrained by EPR obligations, VOC compliance costs, and cautious spending. At the same time, the Ecodesign for Sustainable Products Regulation will move furniture makers toward redesign for disassembly and recyclability [4]European Union, “Regulation (EU) 2024/1781 Ecodesign For Sustainable Products Regulation,” EUR-Lex, eur-lex.europa.eu .

South America is projected to grow at 4.4% CAGR through 2031, supported by urban household formation and wider organized retail penetration. The Middle East and Africa show a split pattern, with Western Asia benefiting from hospitality megaprojects and Sub-Saharan Africa growing more slowly because affordability keeps the mix weighted to economy and lower mid-range sofas. Roche Bobois reported Q1 2026 revenue of EUR 87.1 million (USD 95.8 million). They said March 2026 sales in Shanghai and Beijing rose 53.7% in volume, showing how quickly premium demand can recover when sentiment improves. Even with softer conditions in parts of Europe, hotel refurbishment and tourism-led projects across Southern Europe and the Gulf continue to support contract demand for sofas.

Competitive Landscape

The sofa market remains highly fragmented, with the top 5 players estimated to control only 10.7% of global revenue in 2025. That structure limits global pricing power and leaves room for regional specialists, premium niche brands, and material-led challengers. Strategy is split between scale-oriented manufacturers that focus on production efficiency and channel control, and design-led players that compete on craftsmanship, comfort systems, and brand heritage. Man Wah’s USD 32 million Gainline acquisition in December 2025 added Southern Motion and Fusion Furniture, plus 8 Mississippi facilities, reducing exposure to tariff-heavy export routes and expanding its United States manufacturing base. Inter IKEA also confirmed pilot production of sofas with renewable and recycled foam content, which supports both cost positioning over time and stronger compliance-readiness in the sofa market.

Premium players are responding differently. Natuzzi’s 2025 revenue declined to USD 332.9 million, and its margin came under pressure as the company shifted more Editions production from China to Italy, which lowered tariff risk but raised manufacturing cost. Ekornes reported Q1 2025 revenue of USD 104 million, up 14% year over year, which shows that patented comfort positioning can still support premium pricing even in a volatile input environment. Ashley Furniture’s move into accessible luxury with Ashley Luxe also shows that the sofa market is opening more space between mass pricing and ultra-premium design.

This landscape leaves a clear opening for suppliers that combine PFAS-free upholstery, recyclable knock-down engineering, and mid-premium pricing. Europe’s EPR systems and future ecodesign rules are likely to reward brands that can design for disassembly and document end-of-life handling more clearly. No single company has enough share to set the direction of the sofa market on its own, which means execution at the regional and channel level remains more important than scale alone. As compliance costs rise, the sofa market may stay fragmented at the top while becoming harder to enter at the low end.

Sofa Industry Leaders

IKEA

Ashley Furniture Industries

Man Wah Holdings

La-Z-Boy Incorporated

Natuzzi S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Ashley Furniture launched Ashley Luxe, a premium collection spanning five design lines, Bracken, Calden, Modero, Neo, and Whitehaven, featuring French oak, bouclé, marble-inlay finishes, and supple leather. The launch signals North America's largest mass-market furniture retailer's formal entry into the accessible-luxury sofa segment, expanding competitive overlap with Arhaus, RH, and West Elm.

- February 2026: IKEA United States announced plans to open 10 new stores in 2026, including urban-format locations in Chicago, Los Angeles, Tulsa, and Fort Collins, extending its geographic reach into high-density apartment markets where compact, modular sofa formats drive replacement cycles.

- December 2025: Man Wah USA Manufacturing Limited acquired Gainline Group, comprising Southern Motion (reclining furniture) and Fusion Furniture (stationary furniture), for USD 32 million, adding 8 manufacturing facilities in Mississippi. The acquisition deepens Man Wah's domestic United States production capability and mitigates tariff risk on exports from China and Vietnam.

- October 2025: La-Z-Boy completed the acquisition of a 15-store La-Z-Boy Furniture Galleries network in Georgia, Florida, and Tennessee from Atlanta Furniture Galleries LLC, adding approximately USD 80 million in annual sales and raising the number of company-owned stores to 220, 60% of the total franchise network.

Global Sofa Market Report Scope

The global sofa market covers revenue generated from the sale of sofas used in residential and commercial spaces worldwide. It includes upholstered seating products bought for homes, hotels, offices, co-working spaces, senior-living projects, restaurants, and other contract settings.

The Global Sofa Market Report is Segmented by Product Type (Sectional Sofa, Recliner Sofa, Sleeper Sofa/Sofa Bed, Chaise/Daybed Sofa, Other Sofa Types), Price Range (Economy, Mid-Range, Premium), End-user (Residential, Commercial), Distribution Channel (B2B/Project, B2C/Retail), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Sectional Sofa |

| Recliner Sofa |

| Sleeper Sofa / Sofa Bed |

| Chaise / Daybed Sofa |

| Other Sofa Types |

| Economy |

| Mid-Range |

| Premium |

| Residential |

| Commercial |

| B2B / Project | |

| B2C / Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Local Workshops | |

| Other Distribution Channels |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and the Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of the Middle East and Africa |

| By Product Type | Sectional Sofa | |

| Recliner Sofa | ||

| Sleeper Sofa / Sofa Bed | ||

| Chaise / Daybed Sofa | ||

| Other Sofa Types | ||

| By Price Range | Economy | |

| Mid-Range | ||

| Premium | ||

| By End-user | Residential | |

| Commercial | ||

| By Distribution Channel | B2B / Project | |

| B2C / Retail | Home Centers | |

| Specialty Furniture Stores | ||

| Online | ||

| Local Workshops | ||

| Other Distribution Channels | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and the Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of the Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the global sofa business, and how fast is it growing?

The sofa market size was USD 104.7 billion in 2025, rose to USD 109.9 billion in 2026, and is projected to reach USD 144.5 billion by 2031 at a 5.6% CAGR.

Which region leads global demand for sofas?

Asia-Pacific led with a 34.48% share in 2025 and is also the fastest-growing region, with a 6.75% CAGR through 2031.

Which sofa type is growing the fastest?

Recliner sofas are projected to grow at 6.11% CAGR through 2031, while sectional sofas remained the largest product type in 2025 with 28.76% share.

Why is commercial demand rising faster than residential demand?

Commercial demand is forecast to grow at a 6.61% CAGR, driven by hotel refurbishments, co-working lounges, and senior-living projects, which are creating more recurring contract procurement.

What are the main cost risks for manufacturers?

Foam, leather, and freight volatility remain the key risks. United States furniture-grade polyurethane foam prices stayed elevated in 2026, and leather prices are expected to remain above pre-disruption levels for 1 to 2 years.

How is regulation changing sofa manufacturing and sourcing?

PFAS, VOC, and EPR rules are pushing suppliers toward safer upholstery chemistry, better material traceability, and products designed for easier recycling and disassembly.

Page last updated on: