Meningitis Diagnosis and Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

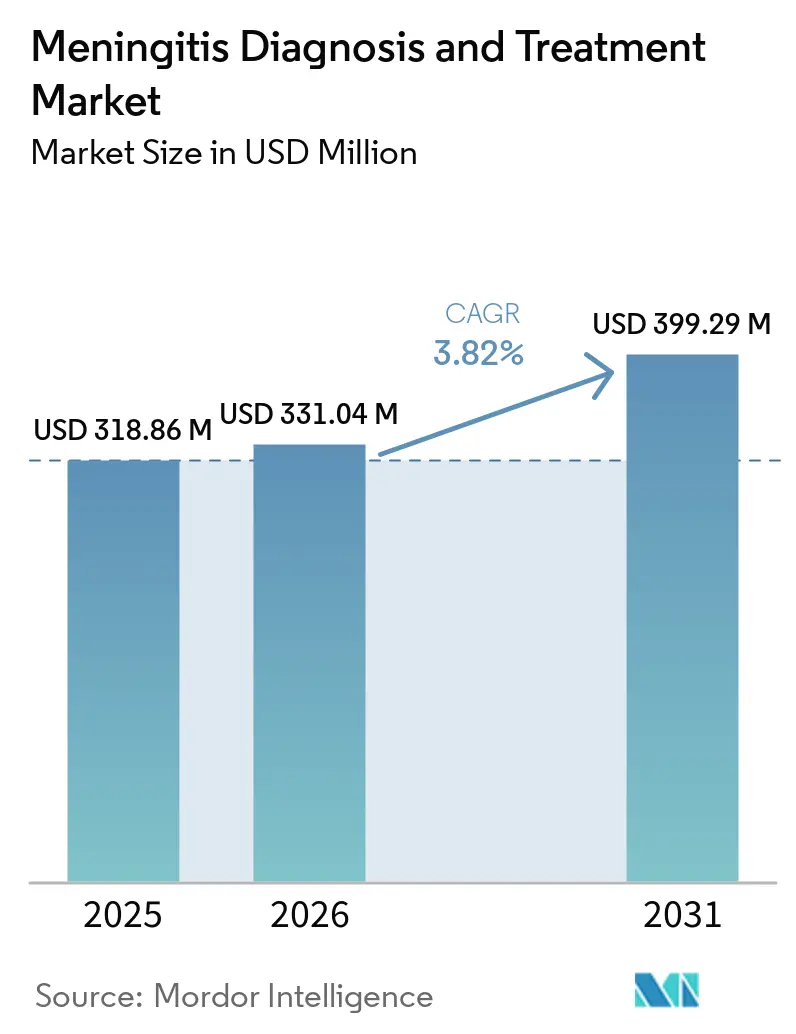

| Market Size (2026) | USD 331.04 Million |

| Market Size (2031) | USD 399.29 Million |

| Growth Rate (2026 - 2031) | 3.82% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Meningitis Diagnosis and Treatment Market Analysis by Mordor Intelligence

The Meningitis Diagnosis And Treatment Market size is projected to be USD 318.86 million in 2025, USD 331.04 million in 2026, and reach USD 399.29 million by 2031, growing at a CAGR of 3.82% from 2026 to 2031.

The growth path stays firm because meningitis remains a medical emergency, and hospitals continue to buy diagnostics and therapies on the basis of clinical need rather than discretionary spending. The 2025 WHO guidelines on meningitis diagnosis, treatment, and care set rapid lumbar puncture, syndromic PCR panels, and immediate antibiotic initiation as the standard approach, which strengthened compliance-led demand for instruments, assays, and treatment pathways in the meningitis diagnosis and treatment market. The disease burden also remains high, with the Global Burden of Disease Study 2023 reporting 2.54 million incident cases and 259,000 deaths in 2023, which keeps diagnosis, treatment, and vaccination demand structurally intact across the forecast period. Wider vaccination and surveillance programs, faster molecular testing, and reimbursement support in high-income health systems are supporting steady expansion in the meningitis diagnosis and treatment market, while post-vaccination monitoring is also creating recurring demand for confirmatory testing. The main constraint is still the cost of molecular infrastructure in lower-income settings, which limits adoption in the highest-incidence geographies and keeps the meningitis diagnosis and treatment market centered on access and execution rather than broad affordability.

Key Report Takeaways

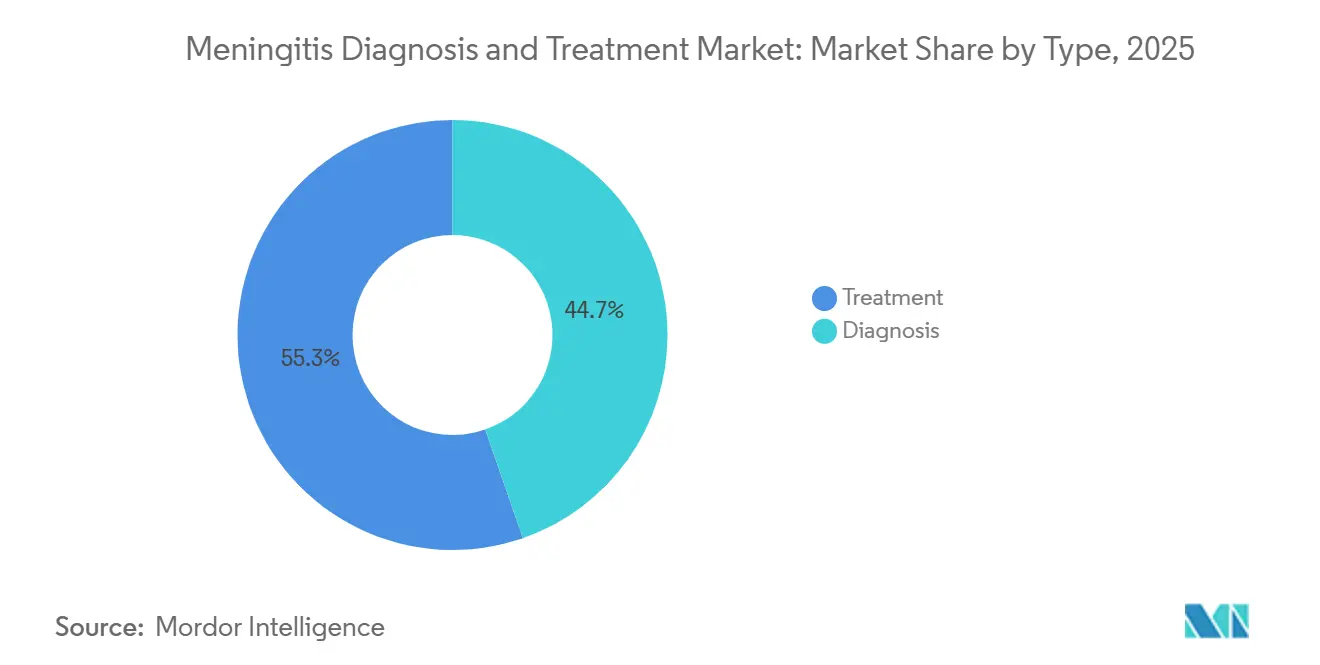

- By type, treatment held 55.31% revenue share in 2025, while diagnosis is forecast to grow at a 4.38% CAGR through 2031.

- By type of meningitis, bacterial meningitis accounted for 45.24% of revenue in 2025, while viral meningitis is projected to expand at a 4.52% CAGR through 2031.

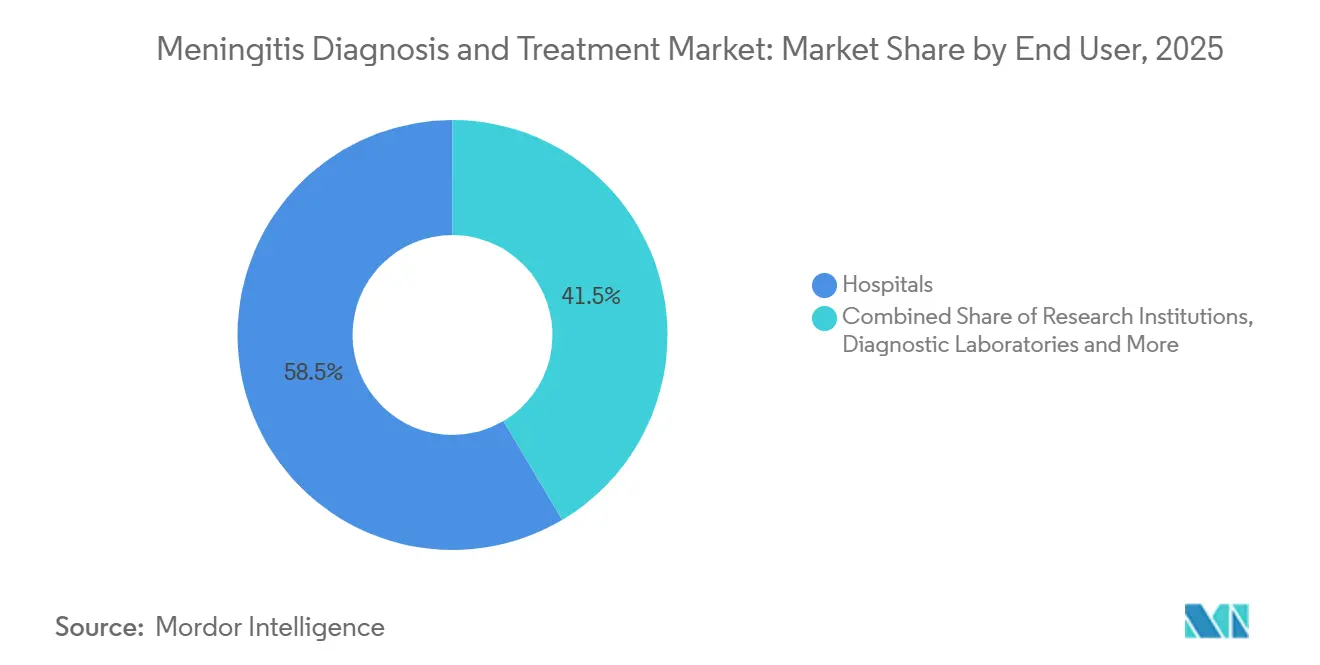

- By end user, hospitals held 58.52% revenue share in 2025, while research institutions recorded the highest projected CAGR at 5.25% through 2031.

- By geography, North America held 38.22% of meningitis diagnosis and treatment market share in 2025, while Asia-Pacific is forecast to grow at a 5.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Meningitis Diagnosis and Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Meningitis and Outbreak Recurrence | +1.1% | Global, with acute concentration in sub-Saharan Africa, North America, and Southeast Asia | Short term (≤ 2 years) |

| Shift Toward Rapid Rule-Out Testing in Emergency and Stewardship Pathways | +0.8% | North America and Europe, with spillover to upper-middle-income APAC | Medium term (2-4 years) |

| Expanding Vaccination and Post-Vaccination Surveillance Programs | +0.6% | Global, with highest near-term leverage in the African meningitis belt, Europe, and South America | Long term (≥ 4 years) |

| Molecular Syndromic Panels Improving Diagnostic Yield | +0.7% | North America, Western Europe, and urbanized APAC including China, Japan, South Korea, and Australia | Medium term (2-4 years) |

| Reimbursement Support for Fast Diagnostics in High-Income Markets | +0.4% | North America and Western Europe | Short term (≤ 2 years) |

| Low-Resource, Heat-Stable Assays Unlocking Underserved Access | +0.3% | Sub-Saharan Africa, South Asia, and South America, with broader relevance across MEA and the rest of APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Meningitis and Outbreak Recurrence

The recurrence of meningitis outbreaks remains a direct growth force for the meningitis diagnosis and treatment market because the global case load has stayed materially high. The Global Burden of Disease Study 2023 reported 2.54 million incident cases and 259,000 deaths in 2023, and it also showed that the 4 preventable pathogens alone caused 594,000 cases and 98,700 deaths. In the United States, bacterial meningitis cases reached their highest levels since 2014, which underlined that recurrence pressure is not limited to lower-income countries. France also recorded a sharp rise in invasive meningococcal infections in early 2025, and the government responded by intensifying the national vaccination strategy and rolling out MenACWY vaccination for adolescents aged 11 to 14 years in the 2025 to 2026 school year[1]Ministère de la Santé, “Méningite, Infections Invasives à Méningocoques,” Ministère de la Santé, sante.gouv.fr. Even markets with established vaccine programs still face serogroup shifts and waning immunity, which keeps both booster procurement and diagnostic demand active in the meningitis diagnosis and treatment market. Public health budgets are also funding more surveillance activity, which helps protect laboratory panel volumes from normal hospital capital spending cycles.

Shift Toward Rapid Rule-Out Testing in Emergency and Stewardship Pathways

Rapid rule-out testing is becoming a structural demand driver in the meningitis diagnosis and treatment market because antibiotic decisions now need to be made within a much shorter clinical window. Updated German clinical guidance published in February 2025 endorsed procalcitonin as a serum biomarker to help distinguish bacterial from viral meningitis and also recognized PCR panel diagnostics as core diagnostic evidence. bioMérieux states that the BioFire FilmArray ME Panel delivers results in around 1 hour and is the only FDA-cleared syndromic panel that includes all 5 relevant herpes virus targets tied to antiviral treatment decisions[2]bioMérieux, “The BIOFIRE FILMARRAY ME Panel Is the Most Aligned FDA-Cleared and CE Marked Syndromic Panel to Meet the 2025 World Health Organization Guidelines,” bioMérieux, info.biomerieux.com. In the United States, the MolDX policy effective January 1, 2025 provides reimbursement criteria for meningitis molecular panels in critically ill patients, which lowers a major adoption barrier for hospital systems. Faster testing also supports antimicrobial stewardship because it helps clinicians de-escalate broad-spectrum antibiotics sooner and narrow therapy with greater confidence. That combination of shorter turnaround time, better stewardship, and lower use of legacy culture workflows is helping the meningitis diagnosis and treatment market move toward panel-based diagnostics more quickly.

Expanding Vaccination and Post-Vaccination Surveillance Programs

Vaccination programs are supporting the meningitis diagnosis and treatment market not only through product uptake but also through the surveillance work that follows every rollout. GSK received FDA approval for PENMENVY on February 14, 2025, which added a first pentavalent meningococcal vaccine option for people aged 10 to 25 years and replaced the need for 2 separate vaccines in that group. The WHO Defeating Meningitis by 2030 roadmap targets a 50% reduction in vaccine-preventable bacterial meningitis cases and a 70% reduction in deaths, and those goals require countries to strengthen surveillance capacity and diagnostic confirmation. That requirement raises demand for CSF culture, PCR confirmation, and serotyping work even when vaccines are already in use. Each new vaccine launch also creates a practical need to distinguish vaccine-breakthrough infections from unvaccinated clusters, which means health systems often need more testing per episode rather than less testing. This dynamic keeps surveillance-linked diagnostic demand tied closely to the longer-term expansion of the meningitis diagnosis and treatment market.

Molecular Syndromic Panels Improving Diagnostic Yield

Molecular syndromic panels are changing the meningitis diagnosis and treatment market because they compress what was once a sequential workflow into a near-simultaneous multi-pathogen result. QIAGEN received FDA clearance for the QIAstat-Dx Meningitis and Encephalitis Panel on November 4, 2024, and the same panel later obtained CE-IVDR certification in July 2025, which expanded access across regulated European hospital networks. QIAGEN had already received Health Sciences Authority approval for the panel in Singapore in January 2024, which gave the company an early reference point for broader APAC rollout. A peer-reviewed evaluation published in Diagnostics reported 96.43% sensitivity and 95.24% specificity for the QIAstat-Dx ME Panel across bacterial, viral, and fungal CSF targets, with an estimated run time of around 1 hour. These performance and access gains improve the value of rapid pathogen identification in emergency and ICU settings, where treatment decisions cannot wait. They also support a clearer split inside the meningitis diagnosis and treatment market between cartridge-based systems built for urgent care and broader multiplex platforms used in reference laboratories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Instrument and Reagent Cost of Molecular Testing | -1.2% | Global, with the strongest pressure in Sub-Saharan Africa, South Asia, and lower-income APAC health systems | Long term (≥ 4 years) |

| Limited CSF Sampling and Pediatric Specimen Constraints | -0.7% | Global, with acute relevance in pediatric and neonatal care settings across all income levels | Medium term (2-4 years) |

| Reimbursement Gaps for Rapid Point-of-Care Tests | -0.6% | Middle-income markets including Southeast Asia, MEA, and Latin America, along with non-covered indications in high-income systems | Medium term (2-4 years) |

| Supply Chain Concentration in Critical Reagent Inputs | -0.4% | Global, with higher exposure in markets dependent on single-source reagent suppliers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Instrument and Reagent Cost of Molecular Testing

High test cost remains the biggest structural brake on the meningitis diagnosis and treatment market because the most advanced platforms are still priced far above the levels needed for broad public health use. The WHO target product profile for a low-cost bacterial meningitis diagnostic set a target list price below USD 8 per test for use in outbreak response and surveillance in low- and middle-income countries. Commercial syndromic panels from leading suppliers sit far above that threshold, which keeps the fastest-growing diagnostic category out of reach for many hospitals in the African meningitis belt and parts of South Asia. This pricing gap creates a split between the commercial market, which is driven by higher-income health systems, and the donor-backed global health market, which depends more heavily on public procurement and subsidy support. A 2024 study in Annals of Clinical Microbiology and Antimicrobials showed that a CRISPR and Cas12a-based LAMP lateral flow assay could detect N. meningitidis without thermocycling equipment, which points to a lower-cost path but does not solve the near-term commercialization gap. Additional compliance demands under frameworks such as EU IVDR and FDA Class II device rules add more cost layers for new entrants and keep the meningitis diagnosis and treatment market tilted toward established players.

Limited CSF Sampling and Pediatric Specimen Constraints

Specimen access is another hard restraint on the meningitis diagnosis and treatment market because lumbar puncture remains central to diagnosis and cannot always be performed safely. Clinical guidance from the German neurology community states that antibiotic treatment must begin before imaging in suspected bacterial meningitis when delay would increase risk, even if CSF cannot be obtained immediately. This means treatment often starts without pathogen confirmation, which naturally limits the number of cases that move through a full molecular diagnostic workflow. Pediatric and neonatal care adds a separate constraint because available CSF volume can be 0.2 mL or less, and that reduces the practical use of multiplex panels in the age group with some of the highest risk. A 2025 PLOS One study reported that children aged 1 to 5 months still recorded incidence rates of 1,185 per 100,000, which made them the hardest patients to test and among the most exposed to treatment delay. Because this challenge depends on procedural training, clinical protocols, and specimen collection realities, it is not a limitation that product innovation alone can remove from the meningitis diagnosis and treatment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Diagnosis Outpaces Treatment in Growth as Rapid Testing Reshapes Clinical Protocol

Treatment accounted for 55.31% of the meningitis diagnosis and treatment market size in 2025, which reflected the combined demand for antibiotics, corticosteroids, vaccines, supportive care, and antiviral therapy. This leadership was rooted in the emergency nature of bacterial meningitis, where empirical antibiotics are expected within 1 to 3 hours of presentation and therefore create a dependable treatment volume. Corticosteroids, especially dexamethasone in pneumococcal cases, remain a stable adjunct because their use is tied to established clinical practice rather than optional prescribing patterns. The vaccine portion of treatment is also becoming more commercially active as broader meningococcal coverage enters the market, especially after GSK received approval for PENMENVY in February 2025. In the meningitis diagnosis and treatment market, this keeps treatment as the larger revenue base even while newer diagnostic technologies gain momentum.

Diagnosis is projected to grow at a 4.38% CAGR through 2031, which makes it the faster-moving side of the meningitis diagnosis and treatment market. PCR-based methods, especially syndromic multiplex panels, are replacing single-pathogen tests and culture-led workflows in high-income systems where faster results can reduce ICU stay and narrow unnecessary therapy. Frontiers in Medical Technology noted in 2025 that syndromic panels with around 1-hour result times can detect bacterial, viral, and fungal pathogens together, and that the BioFire FilmArray ME Panel remained the only FDA-approved multiplex CNS panel at that point while QIAGEN had already entered the field with FDA clearance in late 2024. Blood cultures and serology still matter in resource-constrained settings, and imaging continues to support triage rather than first-line pathogen identification. Across the meningitis diagnosis and treatment industry, ISO 15189 quality demands and FDA device rules keep growth concentrated among accredited platforms with the evidence, regulatory capacity, and installed-base advantage to scale.

By Type of Meningitis: Viral Meningitis Demands Clinical Attention as the Fastest-Growing Subtype

Bacterial meningitis accounted for 45.24% of revenue in 2025, which kept it as the largest disease subtype within the meningitis diagnosis and treatment market. Its lead came from the higher cost per episode, because severe cases often require rapid diagnostics, antibiotics, corticosteroids, and ICU-level supportive care within the same treatment pathway. Streptococcus pneumoniae and Neisseria meningitidis remain the main pathogens, and the recent shift toward W and Y serogroups in Europe is shaping vaccine use and surveillance priorities. The same burden study showed that the 4 WHO-defined preventable pathogens caused 594,000 cases and 98,700 deaths in 2023, which explains why bacterial meningitis still drives the heaviest value capture across diagnosis and treatment.

Viral meningitis is forecast to grow at a 4.52% CAGR through 2031, which makes it the fastest-growing subtype in the meningitis diagnosis and treatment market. Enteroviruses and herpesviruses such as HSV-1, HSV-2, and VZV account for a large share of viral cases, and the 2025 WHO guidance recommends early aciclovir when herpes-group viruses are suspected. That guidance increases the need for rapid molecular differentiation between viral and bacterial causes, which directly supports higher use of multiplex PCR panels. Fungal meningitis remains important in immunocompromised populations, especially in parts of sub-Saharan Africa where treatment access can still be inconsistent, while parasitic meningitis creates smaller but specialized diagnostic demand in endemic settings. Across the meningitis diagnosis and treatment industry, broad syndromic panels that cover bacterial, viral, fungal, and parasitic targets in a single run are supporting faster uptake outside the traditional bacterial core.

By End User: Research Institutions Lead Growth as Diagnostic Innovation Drives Capital Allocation

Hospitals held 58.52% of revenue in 2025, which made them the largest end-user group in the meningitis diagnosis and treatment market. This dominance follows the care pathway because most suspected cases first present in emergency departments, intensive care units, and inpatient neurology settings where testing and treatment begin immediately. Hospital procurement is also shaped by existing analyzer investments, since facilities that already use integrated systems for respiratory or gastrointestinal panels can add meningitis and encephalitis testing as a menu extension rather than a new platform purchase. Diagnostic laboratories remain relevant as outsourced confirmation centers for blood culture, PCR, and serology, especially where hospital-based molecular infrastructure is limited. That mix keeps hospitals at the center of the meningitis diagnosis and treatment market even as more specialized testing capacity spreads across external labs.

Research institutions are projected to grow at a 5.25% CAGR through 2031, which makes them the fastest-growing end-user segment in the meningitis diagnosis and treatment market. Their expansion is being driven by translational work on CRISPR-based and LAMP point-of-care assays, metagenomic next-generation sequencing for undiagnosed CNS infections, and adjunct therapy development aimed at neuroprotection after bacterial meningitis. This part of the market matters because it supports validation work, assay optimization, and the movement of advanced methods from research use into clinical settings. Other end users, including ambulatory facilities and public health agencies, are also gaining importance as surveillance obligations become more formal under WHO-aligned post-vaccination monitoring frameworks. Within the meningitis diagnosis and treatment industry, that wider surveillance role gives non-hospital demand a clearer place in long-term market expansion.

Geography Analysis

North America held 38.22% of meningitis diagnosis and treatment market share in 2025, which made it the largest regional contributor by a clear margin. The United States accounts for most of that position because it combines broad hospital access, reimbursement support for molecular panels under the MolDX framework, and a large installed base of integrated multiplex PCR systems[3]Blue Cross and Blue Shield of Texas and CMS, “CPCPLAB063 Identification of Microorganisms Using Nucleic Acid Probes,” Blue Cross and Blue Shield of Texas, bcbstx.com. The region also benefits from recent vaccine portfolio expansion, including GSK's FDA approval for PENMENVY in 2025, which widened the menu of meningococcal protection options for eligible age groups. Canada and Mexico contribute more modestly, with Canada leaning on publicly funded hospital diagnostics and Mexico showing stronger private laboratory adoption patterns. North America's diagnostic intensity per case remains high, which helps preserve a large revenue footprint for the meningitis diagnosis and treatment market even when disease incidence is lower than in Africa or parts of Asia.

Europe remains one of the most structurally important regions in the meningitis diagnosis and treatment market because regulation is actively reshaping supplier access and procurement predictability. The EU IVDR framework has raised the compliance bar, and QIAGEN's CE-IVDR certification for the QIAstat-Dx Meningitis and Encephalitis Panel in July 2025 shows how approval under that regime can expand access to hospital networks while constraining weaker entrants. Germany, France, the United Kingdom, Italy, and Spain remain the main country markets, with Germany's updated 2025 guidance giving PCR and panel diagnostics a stronger place in routine practice and France's early 2025 meningococcal surge creating a clear near-term vaccine catalyst. Smaller European markets still benefit from harmonized procurement conditions, which helps extend platform standardization across the region.

Asia-Pacific is forecast to expand at a 5.65% CAGR through 2031, making it the fastest-growing region in the meningitis diagnosis and treatment market. China is supporting that trajectory through Healthy China 2030, which is funding hospital laboratory automation and wider deployment of next-generation sequencing and multiplex PCR capacity. India's Ayushman Bharat program is widening neonatal and pediatric screening access, which is increasing bacterial culture and PCR testing at secondary care facilities. QIAGEN's January 2024 approval from Singapore's Health Sciences Authority also shows a staged route into Southeast Asia, with Singapore serving as a gateway market for broader adoption. In contrast, the Middle East and Africa and South America carry heavy disease pressure but a smaller commercial base, since dependence on emergency vaccine stockpiles and cold-chain PCR logistics still limits scale, although WHO's low-cost test profile points to a future effort to build a more commercially viable access segment.

Competitive Landscape

The meningitis diagnosis and treatment market has a bifurcated structure, with diagnostics more concentrated among a small group of platform vendors and treatment spread across a broader set of pharmaceutical and vaccine suppliers. In diagnostics, bioMérieux through BioFire, QIAGEN, and Roche remain the most visible companies because clinical evidence, regulatory reach, and analyzer installed base all matter at the same time. bioMérieux states that the BioFire ME Panel aligns strongly with the 2025 WHO guidance and is supported by more than 190 peer-reviewed publications, while meta-analyses cited by the company reported mean sensitivity of 92.1%. QIAGEN narrowed the field with 4 FDA clearances in 2024, including the QIAstat-Dx Meningitis and Encephalitis Panel, and then extended that platform into Europe through CE-IVDR certification in 2025. That combination means the meningitis diagnosis and treatment market remains competitive, but competitive strength is still tied closely to evidence depth and platform integration rather than to price alone.

White space in the meningitis diagnosis and treatment market sits at both ends of the technology spectrum. One gap is ultra-low-cost point-of-care testing for the African meningitis belt and other underserved settings where current molecular platforms remain too expensive for broad use. The other gap is pathogen-agnostic next-generation sequencing for hard-to-diagnose CNS infections in high-income settings, where clinicians need broader answers after routine panels fail to identify a cause. On the vaccine side, Sanofi reported that its SP0230 5-valent ACWY+B meningococcal vaccine candidate was in Phase 2 as of late 2025, which could make the competitive field tighter if it progresses successfully against the first marketed pentavalent entrants.

Several recent strategic moves also show how the meningitis diagnosis and treatment market is evolving through investment, portfolio positioning, and corporate restructuring. Roche announced in April 2025 that it would invest USD 50 billion in pharmaceuticals and diagnostics in the United States over 5 years, which supports a broader manufacturing and R&D base relevant to its diagnostics operations. BD announced in February 2025 that it intended to separate its Biosciences and Diagnostic Solutions business, a move that could temporarily alter the ownership context around its diagnostic assets and procurement relationships. GSK's PENMENVY approval and QIAGEN's phased regulatory expansion from the United States to Singapore and Europe also show that the meningitis diagnosis and treatment market is being shaped by targeted product launches and sequenced geographic scaling rather than by one broad competitive model.

Meningitis Diagnosis and Treatment Industry Leaders

Pfizer Inc.

GlaxoSmithKline plc

Sanofi S.A.

Roche Holding AG

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The UK Health Security Agency taken an important step by expanding its Meningitis B vaccination program. Anyone receiving preventative antibiotic treatment during the outbreak can get the vaccine. This effort is focused on protecting those most at risk, especially individuals who may have been in close contact with confirmed or suspected cases, ensuring they receive long-term protection as soon as possible.

- September 2025: QIAGEN secured CE-IVDR certification for its QIAstat-Dx Meningitis/Encephalitis Panel, paving the way for its commercial rollout in EU hospitals adhering to the updated IVDR standards, thereby broadening the panel's potential market in Europe.

Global Meningitis Diagnosis and Treatment Market Report Scope

As per the scope of the report, meningitis diagnosis involves clinical assessment and laboratory tests, primarily cerebrospinal fluid analysis. Treatment includes antibiotics, antivirals, and others, along with supportive care to reduce complications.

The meningitis diagnosis and treatment market is segmented by type into diagnosis, which includes lumbar puncture, blood cultures, polymerase chain reaction, serological tests, and imaging techniques. The treatment segment comprises antibiotics, corticosteroids, vaccines, supportive care, and antiviral medication. By type of meningitis, the market is categorized into bacterial meningitis, viral meningitis, fungal meningitis, and parasitic meningitis. By end user, the market is divided into hospitals, diagnostic laboratories, research institutions, and other end users. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Diagnosis | Lumbar Puncture |

| Blood Cultures | |

| Polymerase Chain Reaction | |

| Serological Tests | |

| Imaging Techniques | |

| Treatment | Antibiotics |

| Corticosteroids | |

| Vaccines | |

| Supportive Care | |

| Antiviral Medication |

| Bacterial Meningitis |

| Viral Meningitis |

| Fungal Meningitis |

| Parasitic Meningitis |

| Hospitals |

| Diagnostic Laboratories |

| Research Institutions |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Diagnosis | Lumbar Puncture |

| Blood Cultures | ||

| Polymerase Chain Reaction | ||

| Serological Tests | ||

| Imaging Techniques | ||

| Treatment | Antibiotics | |

| Corticosteroids | ||

| Vaccines | ||

| Supportive Care | ||

| Antiviral Medication | ||

| By Type of Meningitis | Bacterial Meningitis | |

| Viral Meningitis | ||

| Fungal Meningitis | ||

| Parasitic Meningitis | ||

| By End User | Hospitals | |

| Diagnostic Laboratories | ||

| Research Institutions | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current and forecast value of the meningitis diagnosis and treatment space?

It stands at USD 331.04 million in 2026 and is projected to reach USD 399.29 million by 2031, growing at a 3.82% CAGR from 2026 to 2031.

Which product group holds the largest revenue base?

Treatment led with 55.31% of revenue in 2025 because antibiotics, corticosteroids, vaccines, and supportive care are tied directly to emergency clinical need.

Which disease subtype is expanding the fastest through 2031?

Viral meningitis is the fastest-growing subtype with a 4.52% CAGR through 2031, supported by the need for rapid molecular differentiation from bacterial cases.

Which end user is growing the fastest?

Research institutions are forecast to expand at a 5.25% CAGR through 2031 as work on CRISPR assays, mNGS, and adjunct therapies continues to scale.

Which region leads global revenue and which region grows the fastest?

North America held 38.22% of global revenue in 2025, while Asia-Pacific is projected to post the fastest growth at a 5.65% CAGR through 2031.

What is the main barrier to wider molecular test adoption?

High instrument and reagent cost remains the biggest barrier, especially in lower-income settings where the WHO target profile called for a price below USD 8 per test.

Page last updated on: