Hospital Acquired Infection Control Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.59 Billion |

| Market Size (2031) | USD 5.52 Billion |

| Growth Rate (2026 - 2031) | 3.72% CAGR |

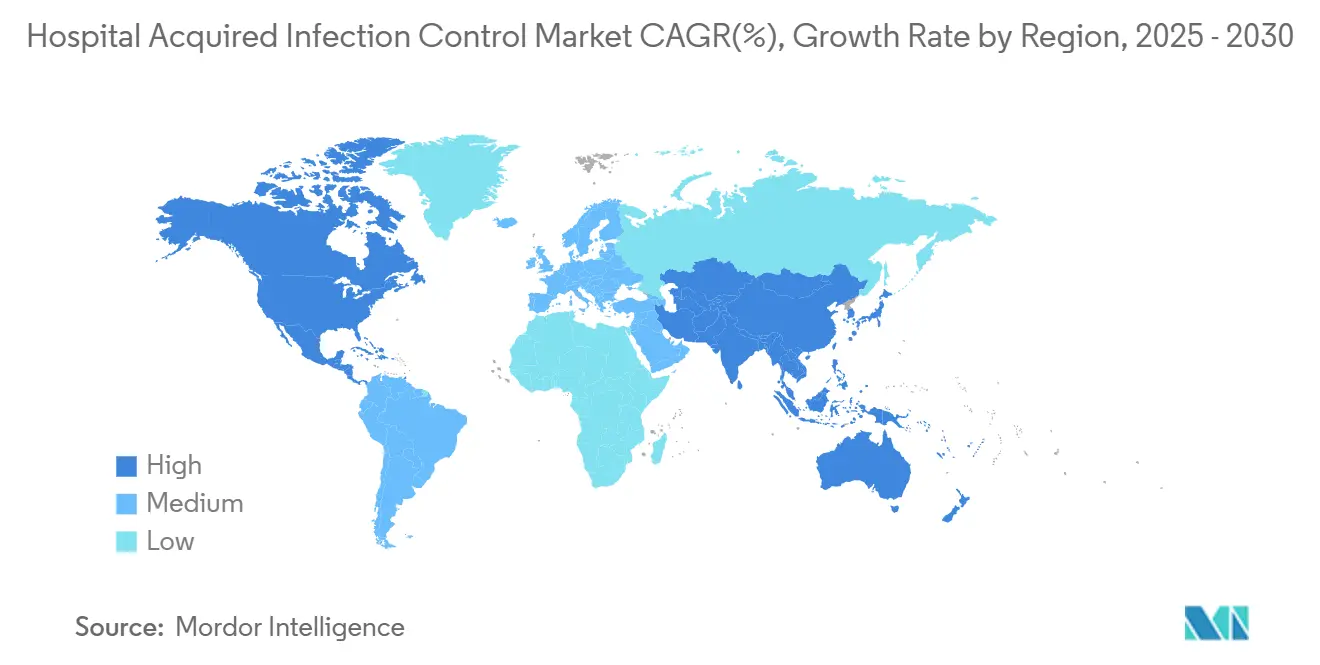

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hospital Acquired Infection Control Market Analysis by Mordor Intelligence

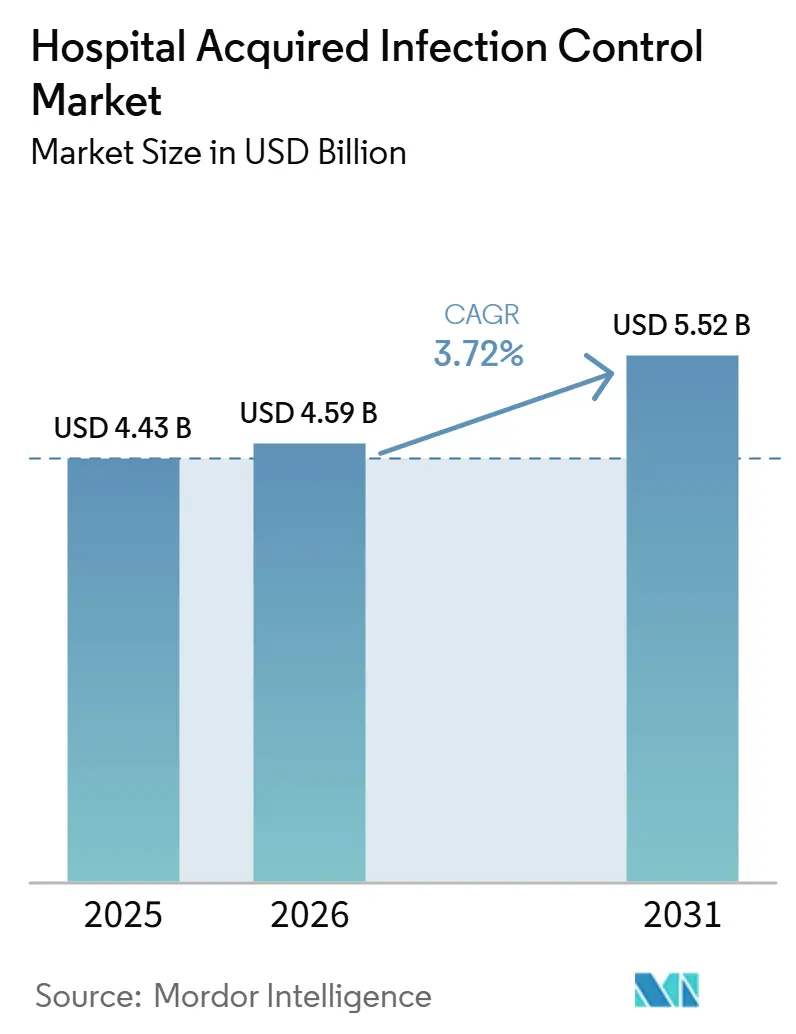

The Hospital Acquired Infection Control Market size is projected to be USD 4.43 billion in 2025, USD 4.59 billion in 2026, and reach USD 5.52 billion by 2031, growing at a CAGR of 3.72% from 2026 to 2031.

Demand is being driven by mandatory infection-reporting rules, expanding surgical volumes, and the growing financial penalties tied to high infection rates. Hospitals are broadening prevention programs to cover the entire patient pathway, which is lifting purchases of both single-use supplies and outsourced service contracts. UV-C robots, hydrogen-peroxide sterilizers, and data-rich hand-hygiene trackers are moving from pilot projects to routine procurement, encouraged by evidence of double-digit reductions in infection incidence. Vendors are also responding to litigation risk in markets like Australia by supplying traceable, audit-ready processes that help facilities prove compliance.

Key Report Takeaways

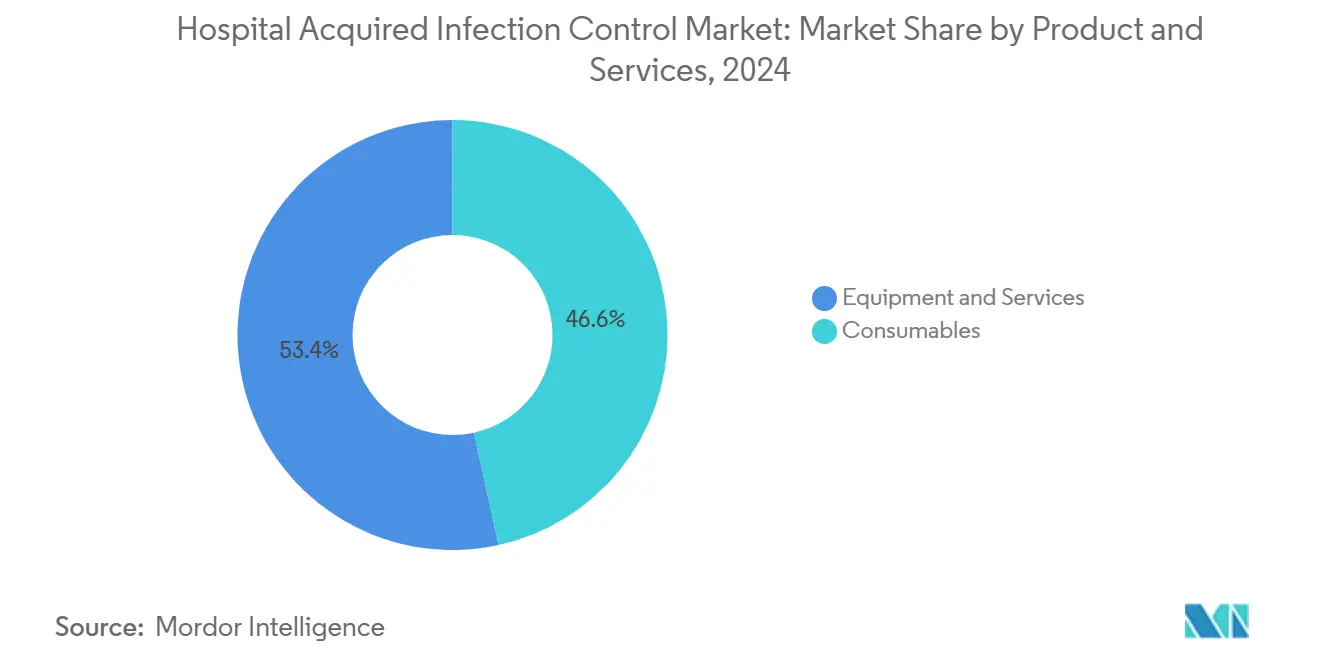

- By type, consumables led with 45.98% of hospital-acquired infection control market share in 2025, while services are projected to expand at a 5.05% CAGR to 2031.

- By end user, hospitals and ICUs commanded 62.12% of the hospital-acquired infection control market in 2025; ambulatory surgical centers are advancing at a 5.78% CAGR through 2031.

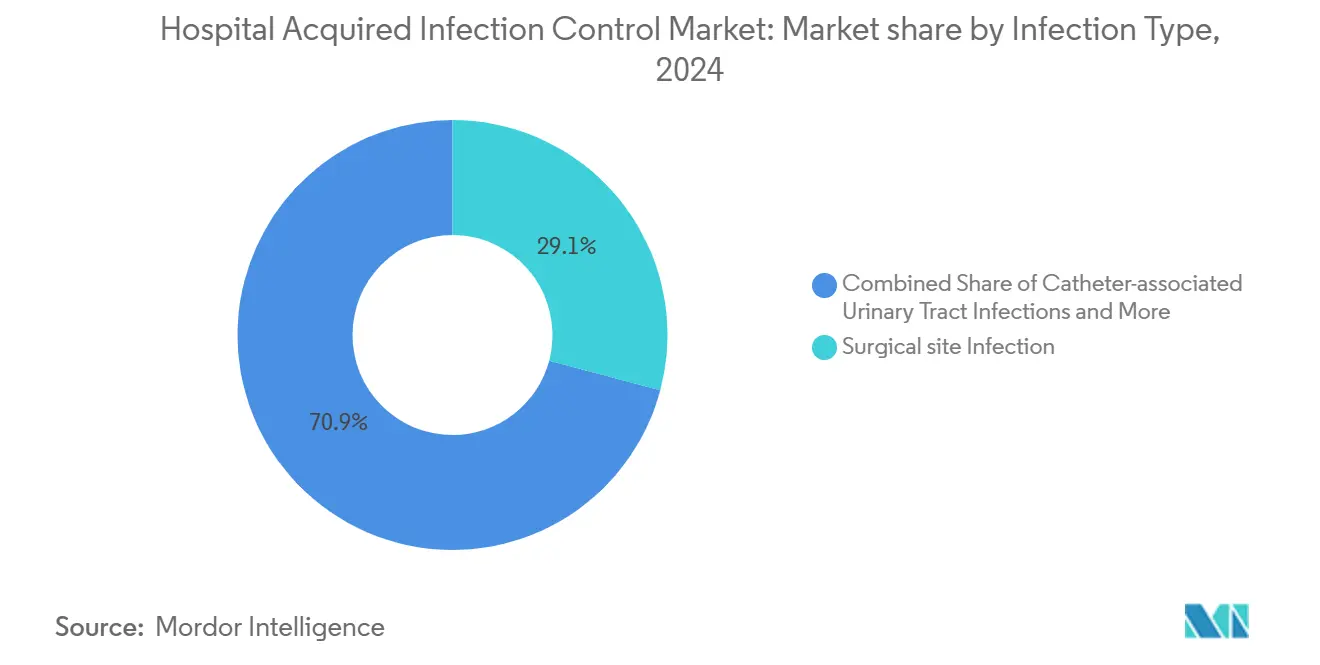

- By infection type, surgical site infections accounted for 28.74% of the hospital-acquired infection control market in 2025, whereas CLABSI prevention is set to grow at a 6.62% CAGR between 2026 and 2031.

- By geography, North America held 39.08% of the hospital-acquired infection control market share in 2025; Asia-Pacific is on track for a 6.43% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Hospital Acquired Infection Control Market*

| Driver | ~% Impact on CAGR | Geographic Relevance | Peak Impact |

|---|---|---|---|

| Rising Surgical Volumes and ICU Admissions | +1.2% | Global, with emphasis on North America & Europe | Medium term (~ 3-4 yrs) |

| Mandatory Reporting of HAIs in U.S. & Select EU Nations | +0.8% | North America & EU | Short term (≤ 2 yrs) |

| Rise in the Incidences of Different Types of Hospital Acquired Infections | +1.0% | Global | Medium term (~ 3-4 yrs) |

| Innovative Technologies Implemented in Devices that Control Infection | +1.5% | North America, Europe, developed APAC | Long term (≥ 5 yrs) |

| Rapid Expansion of Ambulatory Surgery Centers in North America | +0.6% | North America | Medium term (~ 3-4 yrs) |

| Growing Adoption of Low-temperature H₂O₂ Sterilizers in Europe | +0.4% | Europe | Short term (≤ 2 yrs) |

| Source: Mordor Intelligence | |||

Rising Surgical Volumes and ICU Admissions Drive Prevention Needs

Surgical caseloads are climbing with aging populations and improved access to elective procedures. Roughly 1 in 31 inpatients acquires at least one infection each day, lengthening stays by 17 days and prompting a 42% readmission rate within 30 days. The financial impact is acute: surgical site infections alone cost USD 3 billion to USD 5 billion annually. These pressures reinforce continuous purchasing of disinfectants, sterile wraps, and barrier devices across the hospital-acquired infection control market.

Mandatory Reporting Requirements Reshape Compliance Landscape

The United States and several EU states tie Medicare, Medicaid, or national reimbursement to demonstrated infection-control performance, compelling hospitals to fund robust surveillance programs [1]Centers for Disease Control and Prevention, “CDC's Core Infection Prevention and Control Practices for Safe Healthcare Delivery in All Settings,” cdc.gov.Electronic dashboards that map hand-hygiene events or track central-line days help facilities defend payments and avoid penalties, stimulating demand for data-enabled solutions within the hospital-acquired infection control market.

Rise in Incidences of Different Types of Hospital-Acquired Infections

Central-line infections average 41,000 cases per year in the United States, while catheter-associated UTIs reach 500,000 cases. Preventive measures such as antimicrobial catheters and disinfecting access caps are seeing rapid adoption, reflected in segment growth that outpaces the overall hospital-acquired infection control market.

Innovative Technologies Transform Infection Control Landscape

UV-C disinfection robots can remove 99.9% of pathogens in 10 minutes, with studies showing a 30% decrease in overall infection rates after rollout. AI-driven analytics platforms flag potential outbreaks and guide antibiotic selection, enhancing stewardship efforts. These technologies lower labor demands and strengthen audit trails, positioning them as key growth catalysts.

Restraints Impact Analysis of Hospital Acquired Infection Control Market*

| Restraint | ~% Impact on CAGR | Geographic Relevance | Peak Impact |

|---|---|---|---|

| Lack of Awareness Regarding Hospital Acquired Infection | -0.7% | Emerging markets, rural healthcare settings globally | Medium term (~ 3-4 yrs) |

| Stringent Regulatory Requirement | -0.9% | Global, with highest impact in North America & Europe | Short term (≤ 2 yrs) |

| High Capital Cost of UV/HPV Disinfection Systems for Tier-2 Hospitals | -1.1% | Emerging markets, smaller hospitals globally | Medium term (~ 3-4 yrs) |

| Workforce Skill Gaps in Endoscope Reprocessing | -0.6% | Global, with emphasis on regions with rapid healthcare expansion | Long term (≥ 5 yrs) |

| Source: Mordor Intelligence | |||

Lack of Awareness Regarding Hospital-Acquired Infection

Many frontline staff still fall short of the WHO’s five-moment hand-hygiene protocol. Ecolab’s electronic monitoring system creates a virtual patient zone and delivers real-time reminders, lifting compliance and providing measurable returns. Yet adoption unevenness continues to dampen the hospital-acquired infection control market.

Stringent Regulatory Requirements Create Market Barriers

Validation studies, sterility assurance audits, and clinical-evidence dossiers extend product launch timelines. The EU MDR demands expanded post-market surveillance, while FDA guidance for high-level disinfectants requires multi-cycle microbiological testing. Smaller firms struggle with capital and expertise, limiting new-entrant flow and tempering growth in the hospital-acquired infection control market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Consumables Lead While Services Gain Momentum

Consumables accounted for 46.57% of hospital-acquired infection control market share in 2024, supported by daily use of disinfectants, sterile drapes, gloves, and wrap materials. The segment delivers predictable volume thanks to mandatory single-use policies and frequent product turn-over. Suppliers are adding color-coded packaging and QR-enabled traceability to help hospitals document compliance. The hospital-acquired infection control market size tied to consumables is expected to post steady mid-single-digit expansion in line with surgical procedure growth.

Services are projected to register a 5.25% CAGR from 2025 to 2030. Hospitals are outsourcing infection-prevention audits, staff training, and sterilizer maintenance to specialists who guarantee performance under outcome-based contracts. Digital dashboards that track infection metrics in real time underpin these offerings. This consultative approach differentiates providers and unlocks recurring revenue streams inside the hospital-acquired infection control market.

By End-User: Hospitals & ICUs Maintain Dominance as ASCs Gain Ground

Hospitals and intensive care units held 62.77% of hospital-acquired infection control market size in 2024, reflecting their high patient density and invasive-procedure mix. Infection-control teams in tertiary centers maintain sophisticated surveillance networks that drive steady procurement of PPE, biocidal agents, and tracking software. The push to eliminate ventilator-associated pneumonia and central-line infections keeps capital budgets intact for new automation systems.

Ambulatory surgical centers are growing at a 6.05% CAGR through 2030. Evidence shows ASC infection rates are about six times lower than hospital outpatient departments. Their reputation for cleanliness draws payers and patients, encouraging investment in point-of-use sterilizers and low-temperature reprocessors that fit compact footprints. As payers shift more elective procedures to outpatient settings, ASCs will represent a rising slice of the hospital-acquired infection control market.

By Infection Type: Surgical Site Infections Drive Market While CLABSI Prevention Accelerates

Surgical site infections accounted for a 29.13% share of hospital-acquired infection control market size in 2024. Their sizable clinical burden keeps antiseptic preps, antimicrobial drapes, and wound-closure technologies in high demand. Institutions are also adding prophylactic antibiotic-impregnated sutures and advanced incision protectors to protocols, reinforcing consumable throughput in the hospital-acquired infection control market.

CLABSI prevention is forecast to climb at a 6.98% CAGR. Disinfecting caps, antimicrobial lock solutions, and training modules for central-line insertion bundles are penetrating care workflows 2Source: National Center for Biotechnology Information, “Disinfecting Caps Reduce CLABSI Rates,” ncbi.nlm.nih.gov. Vendors that integrate catheter materials with digital reminder systems are well placed to capture this fast-growing pocket of the hospital-acquired infection control market.

Geographical Analysis

North America Hospital Acquired Infection Control Market

North America contributed 39.50% of hospital-acquired infection control market share in 2024. CMS reimbursement rules require documented infection-prevention plans cms.gov, while CDC guidelines provide detailed clinical roadmaps. Hospitals respond by funding UV-C robots and real-time location systems that verify protocol adherence. These spending patterns underscore the region’s leading role in the hospital-acquired infection control market.

Europe Hospital Acquired Infection Control Market

Europe follows with strong adoption in Germany, France, and the United Kingdom. Although the EU Medical Device Regulation has tightened evidence thresholds, national health services still finance large-scale sterilizer replacements and automated endoscope reprocessors. Informal divergence in infection-control standards complicates procurement but also drives consulting demand as hospitals seek to reconcile local and EU-wide rules. Vendors that can navigate multi-country compliance secure a durable advantage in the hospital-acquired infection control market.

APAC Hospital Acquired Infection Control Market

Asia-Pacific is the fastest-growing region at 6.77% CAGR. A pooled infection prevalence of 9.0% across Southeast Asian facilities reveals significant unmet need. Rapid expansion of private hospitals in China and India, together with aging demographics, is accelerating orders for sterilizers, isolation consumables, and hand-hygiene dispensers. Government grants are emerging for rural clinics to adopt low-temperature sterilization, widening the addressable base of the hospital-acquired infection control market.

LATAM and MEA Hospital Acquired Infection Control Market

Latin America and the Middle East & Africa remain smaller contributors but post steady gains as accreditation bodies adopt Joint Commission-style benchmarks. Regional distributors increasingly partner with global OEMs to assemble consumable kits locally, improving affordability and compliance reporting.

Competitive Landscape

The hospital-acquired infection control market features a blend of diversified giants and focused innovators. 3M, STERIS, Getinge, and Ecolab leverage scale, multi-category portfolios, and direct service networks to secure long-term supply contracts. Getinge’s 2025 acquisition of Healthmark Industries strengthened its sterile processing lineup and deepened distribution reach in the United States. Ecolab, after divesting its surgical solutions unit, is concentrating on digital hand-hygiene monitoring and instrument reprocessing assets.

Innovation remains a prime differentiator. STERIS’s integrated capital-plus-consumable bundles promise validated cycle outcomes and remote diagnostics sec.gov. Bactiguard’s antimicrobial endotracheal tube cut ventilator-associated pneumonia incidence in peer-reviewed studies. UV-C robot specialists deploy leasing models that lower capital hurdles, allowing mid-tier hospitals to adopt automation quickly.

Price competition is moderate because regulatory approval and clinician validation erect barriers. Service quality, uptime guarantees, and user-training programs often outweigh pure product cost considerations. Players that combine evidence-backed efficacy with workflow analytics are well placed to enlarge share in the hospital-acquired infection control market.

Hospital Acquired Infection Control Industry Leaders

3M Company

Steris PLC

Getinge AB

Ecolab Inc.

Advanced Sterilization Products (Fortive)

- *Disclaimer: Major Players sorted in no particular order

Hospital Acquired Infection Control Market Companies Covered in this Report

- Dentsply Sirono

- 3M

- STERIS

- Getinge

- Ecolab

- Advanced Sterilization Products

- STERIS

- Belimed

- Beckton Dickinson

- Olympus

- Matachana Group

- MMM Group

- Cardinal Health

- Halyard Health

- Ansell

- Metrex Research (Envista)

- HuFriedyGroup

- GAMA Healthcare

- Medline Industries

- Steelco

- Fedegari Autoclavi

- Tuttnauer

Read Analysis of Hospital Acquired Infection Control Companies

Recent Industry Developments in Hospital Acquired Infection Control Market

- January 2025: Getinge completed the acquisition of Healthmark Industries, expanding its infection control consumables portfolio and reinforcing its U.S. distribution network.

- January 2025: The American Hospital Association released its 2025 Environmental Scan, highlighting demographic and climate trends likely to influence infection-control strategies.

- April 2024: Getinge introduced the Aquadis Index washer-disinfector to boost throughput and traceability in CSSDs

- March 2024: The CDC issued revised clinical guidance for C. difficile prevention in acute-care facilities, advocating isolation protocols and antibiotic stewardship.

Hospital Acquired Infection Control Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the hospital-acquired infection (HAI) control market as the global sales of products, equipment, and onsite services that hospitals and intensive-care units deploy to prevent, monitor, or eradicate infections emerging >=48 hours after admission, within three days post-discharge, or up to thirty days after surgery. The scope spans sterilizers, disinfectant consumables, environmental monitoring devices, personal protective barriers, and outsourced decontamination services used by acute-care providers.

Scope Exclusion: Post-acute home-care kits and anti-infective drugs are outside the study.

Segments Covered in This Report

- By Product and Services

- By Equipment

- Sterilization

- Steam Sterilizers

- Low-temperature Hâ‚‚Oâ‚‚ Sterilizers

- Ethylene Oxide Sterilizers

- Radiation Sterilization

- Contract Sterilization Services

- Disinfection

- UV & Hydrogen-Peroxide-Vapor Devices

- Endoscopic Reprocessor Systems

- Others

- Sterilization

- Services

- Consumables

- By Equipment

- By End-user

- Hospitals & Intensive Care Units (ICUs)

- Ambulatory Surgical Centers (ASCs)

- Long-term Care Facilities

- Specialty Clinics & Dialysis Centers

- By Infection Type

- Surgical Site Infections (SSI)

- Catheter-associated Urinary Tract Infections (CAUTI)

- Central-line Associated Bloodstream Infections (CLABSI)

- Hospital-acquired & Ventilator-associated Pneumonia (HAP/VAP)

- Gastro-intestinal Infections & Others

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed infection-control nurses, biomedical engineers, procurement heads, and regional public-health officials across North America, Europe, and Asia-Pacific. These conversations confirmed workflow changes, realistic average selling prices, and adoption curves, helping us bridge gaps seen in desk research before final triangulation.

Desk Research

We gathered baseline figures from tier-1 public sources such as the World Health Organization, the US Centers for Disease Control and Prevention, Eurostat hospital discharge files, the European Centre for Disease Prevention and Control surveillance network, and peer-reviewed journals indexed in PubMed. Industry associations, including the Association for the Advancement of Medical Instrumentation and the International Federation of Infection Control, supplied procedure counts and device-utilization ratios. Company filings accessed through D&B Hoovers and news archives on Dow Jones Factiva enriched the dataset with pricing corridors, capacity additions, and product-mix shifts. This list is illustrative; many additional open sources informed data collection, validation, and narrative clarification.

Market-Sizing & Forecasting

We reconstruct demand top-down from global patient-days, surgical volumes, and catheter or ventilator device-days, which are then cross-checked with sampled supplier revenues for bottom-up sanity. Key inputs include catheter-days per bed, hand-hygiene compliance rates, sterilizer replacement cycles, average disinfectant spend per ICU bed, and penalty-linked infection scores. Values are projected with multivariate regression blended with step-wise ARIMA to capture policy shocks and seasonality, and any supplier data gaps are filled via region-specific ASP benchmarks validated during interviews.

Data Validation & Update Cycle

Outputs face variance checks against CDC scorecards, WHO burden estimates, and quarterly earnings of listed suppliers. Two analyst reviews follow, and any anomaly triggers fresh respondent calls. Reports refresh each year, with interim updates after major regulatory or technological shifts.

How Mordor Intelligence's Hospital Acquired Infection Control Market Size Compares to Other Published Estimates

Published estimates often diverge because firms pick wider product baskets, apply distinct ASP ladders, and refresh at different times. According to Mordor Intelligence, our disciplined definition and annual refresh keep numbers tightly tied to observable hospital practice.

Key gap drivers include the inclusion of home-care supplies, uniform ASP inflation without regional weights, and optimistic uptake assumptions for premium automation services.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.43 B (2025) | Mordor Intelligence | - |

| USD 20.98 B (2024) | Global Consultancy A | counts outpatient centers and retail disinfectants |

| USD 20.6 B (2025) | Industry Insights Group B | applies uniform ASP inflation without regional weighting |

| USD 38.51 B (2024) | Research Aggregator C | assumes full hospital compliance with automated UV systems |

The comparison shows that when scope creep and optimistic pricing are peeled away, Mordor's carefully triangulated baseline remains the most dependable starting point for strategic decisions.

Key Questions Answered in the Report

What is the current value of the hospital-acquired infection control market?

The market stands at USD 4.59 billion in 2026 and is projected to reach USD 5.52 billion by 2031.

Which product segment leads the hospital-acquired infection control market?

Consumables lead with 45.98% market share thanks to daily demand for disinfectants, wraps, and PPE.

Why are ambulatory surgical centers attracting attention in infection control?

They record infection rates about six times lower than hospital outpatient departments, driving a 5.78% CAGR for related solutions.

How are UV-C robots impacting infection rates?

Studies show these robots can cut overall healthcare-associated infections by 30% after deployment.

Which region is growing fastest in the hospital-acquired infection control market?

Asia-Pacific is advancing at a 6.43% CAGR due to hospital construction, rising surgical volumes, and stronger awareness campaigns.

What regulatory factors influence purchasing decisions in North America?

CMS reimbursement conditions and CDC guidelines require hospitals to document infection-control performance, motivating investment in validated technologies.

Page last updated on: