Infectious Enteritis Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

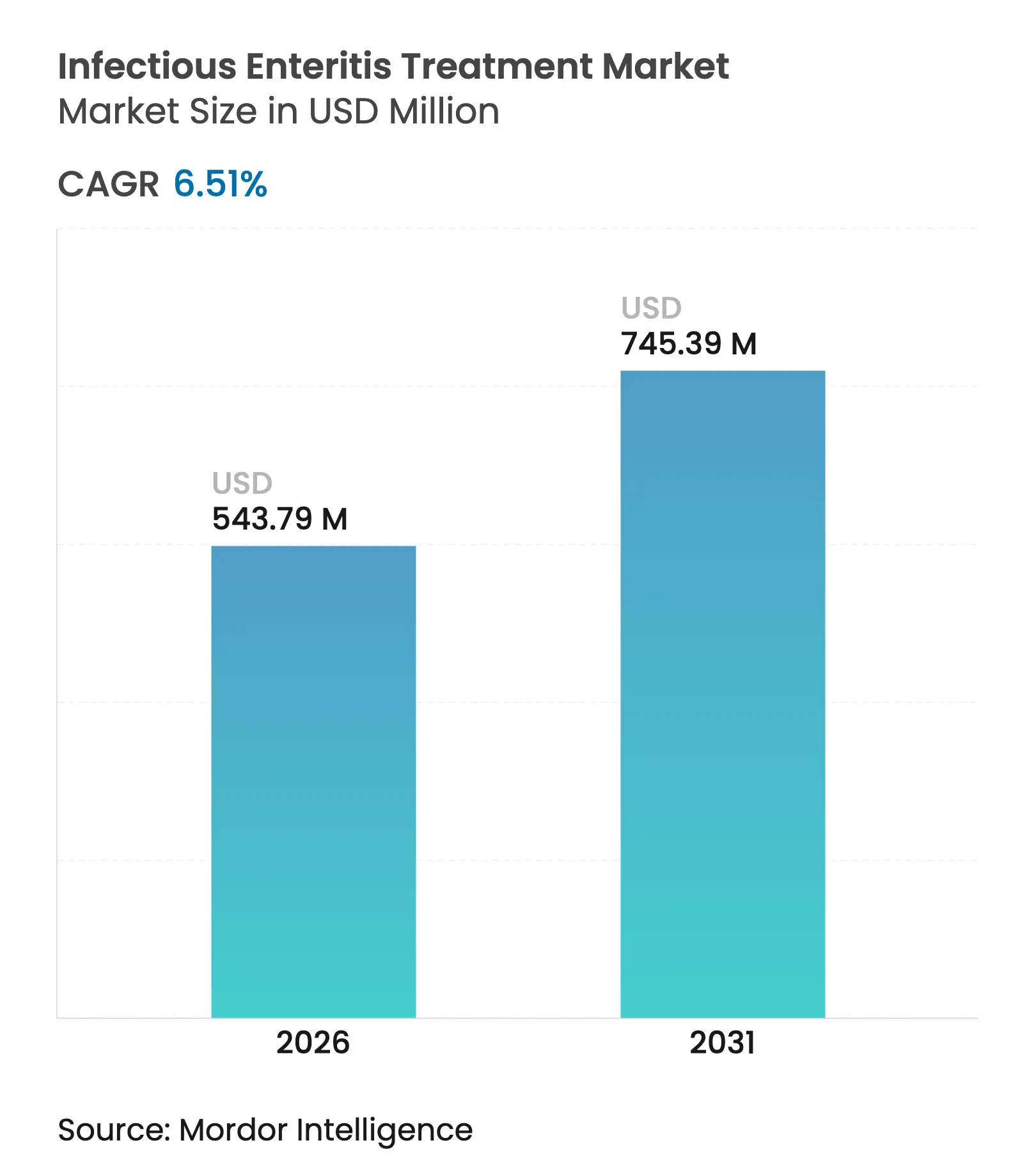

| Market Size (2026) | USD 543.79 Million |

| Market Size (2031) | USD 745.39 Million |

| Growth Rate (2026 - 2031) | 6.51 % CAGR |

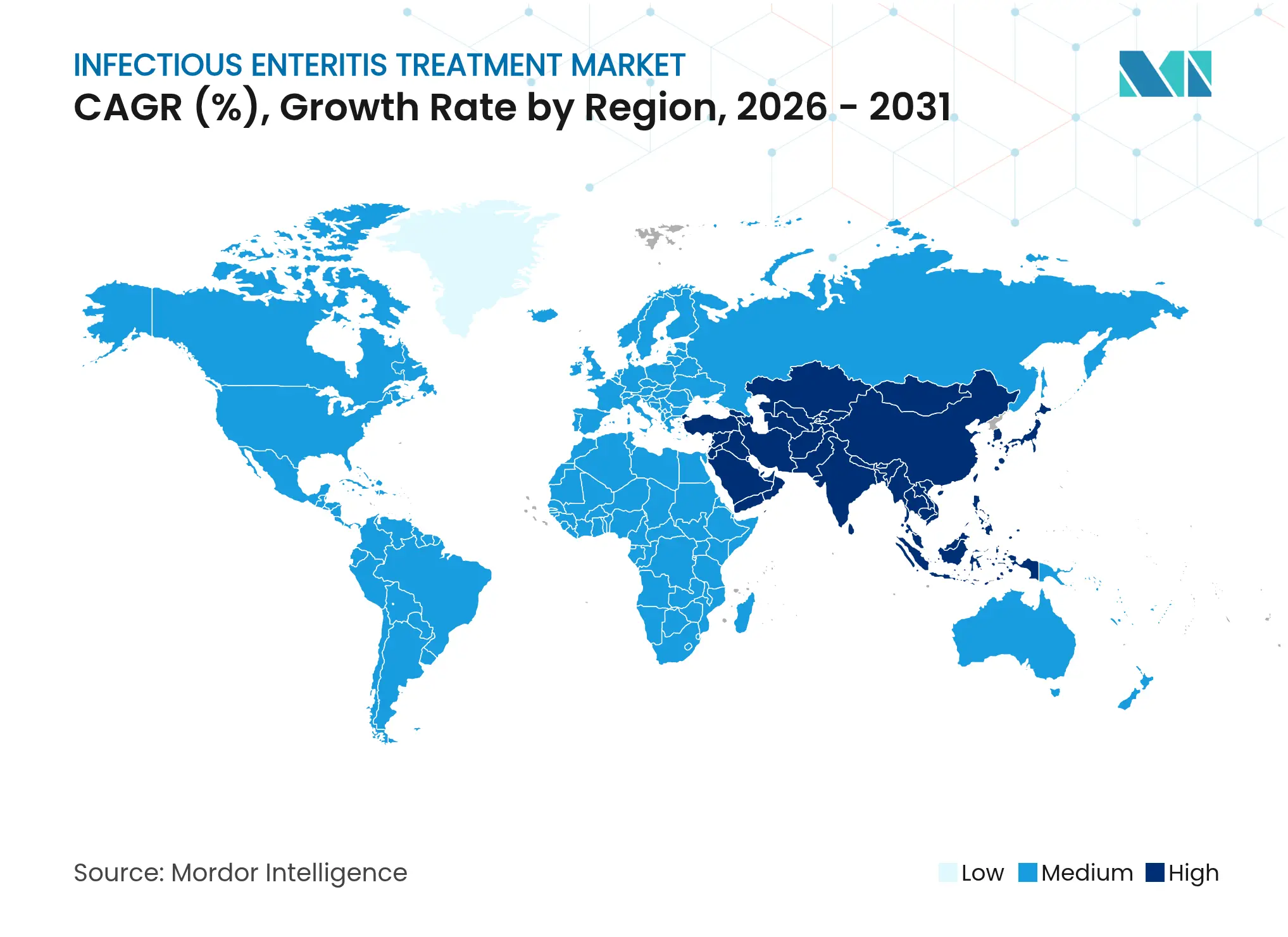

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

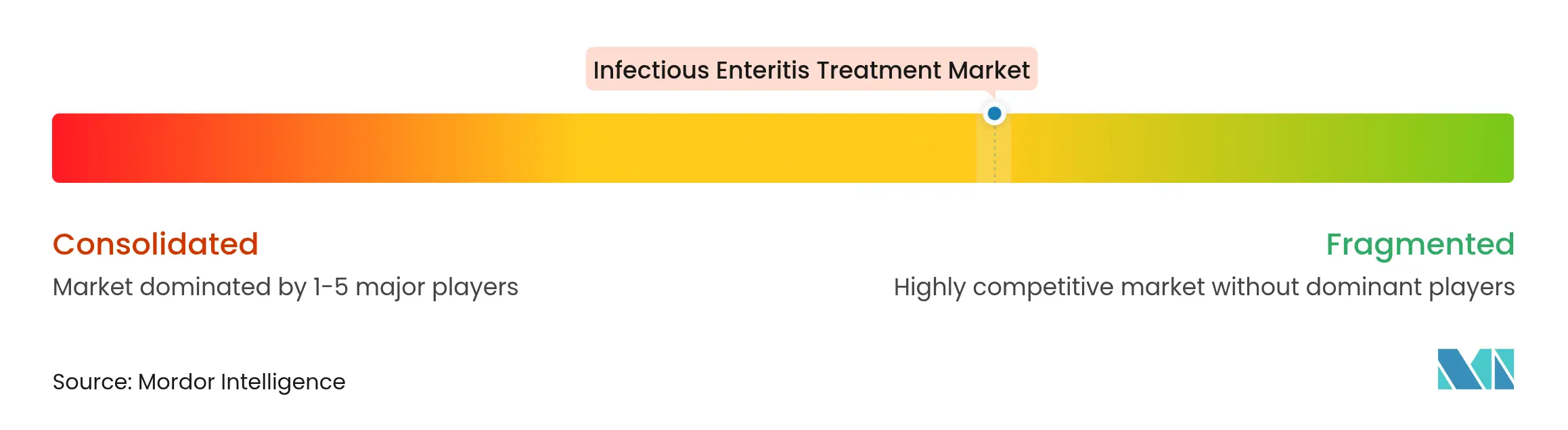

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Infectious Enteritis Treatment Market Analysis by Mordor Intelligence

Expanding demand stems from rising antimicrobial-resistant (AMR) pathogens, premium pricing acceptance for narrow-spectrum drugs, and greater adoption of live biotherapeutic products that restore the gut microbiome after antibiotic use. Wider rotavirus immunization roll-outs in emerging economies accelerate pediatric uptake, while online pharmacy penetration boosts patient access in digitally connected regions. Competitive differentiation increasingly hinges on AI-enabled drug discovery partnerships and regulatory pathways such as the FDA’s Limited Population Antibiotic Drug (LPAD) approvals, allowing faster commercial launches of precision antimicrobials. North America presently anchors revenue through sophisticated diagnostics and stewardship frameworks, but Asia-Pacific contributes the fastest incremental growth as healthcare infrastructure scales and vaccine coverage deepens.

Key Report Takeaways

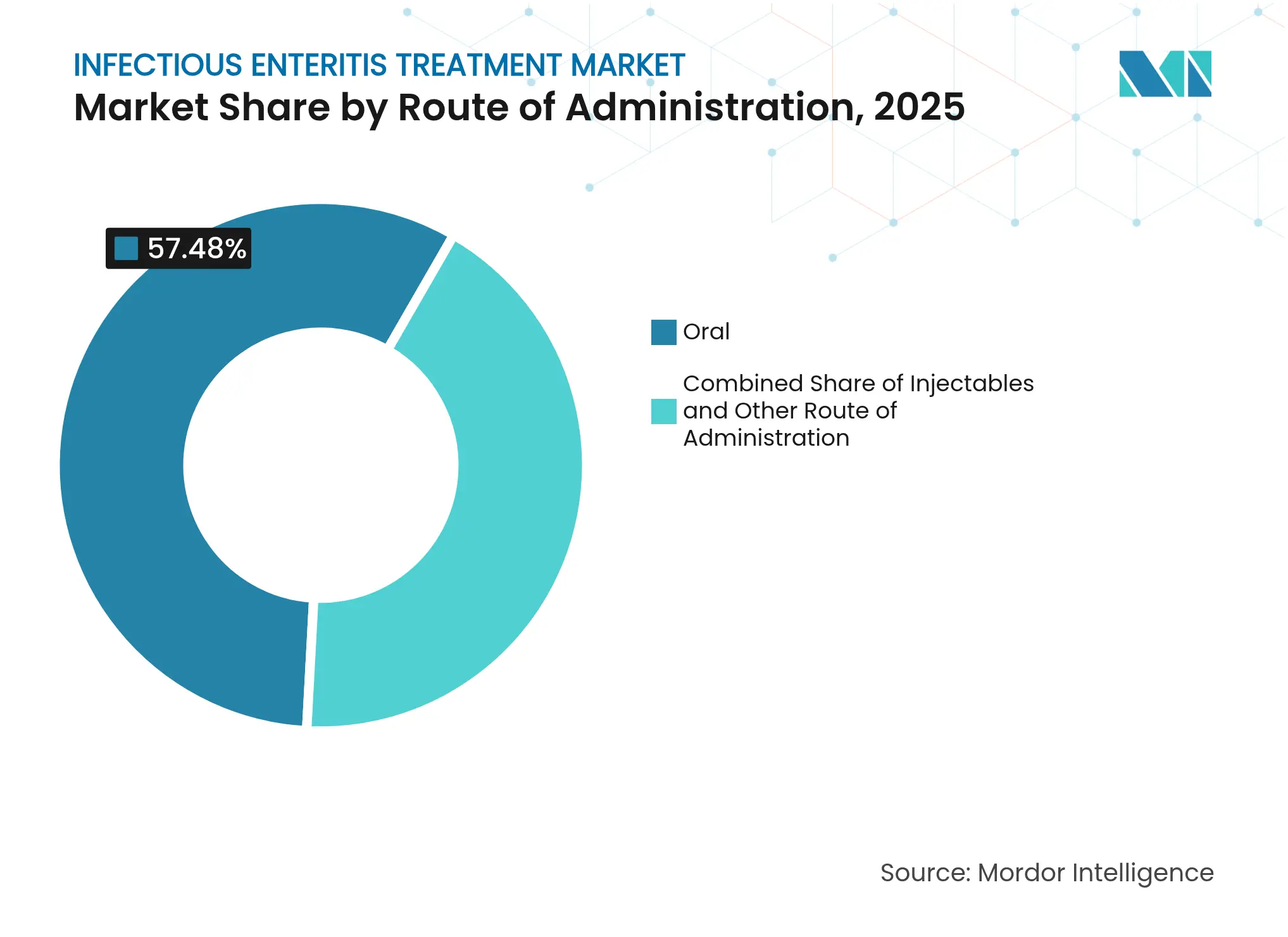

- By route of administration, oral formulations led with 57.48% revenue share in 2025, whereas injectable products are advancing at an 8.12% CAGR through 2031.

- By drug class, antibiotics accounted for 51.10% of the infectious enteritis treatment market share in 2025, while probiotics and microbiome therapeutics are expanding at a 8.96% CAGR.

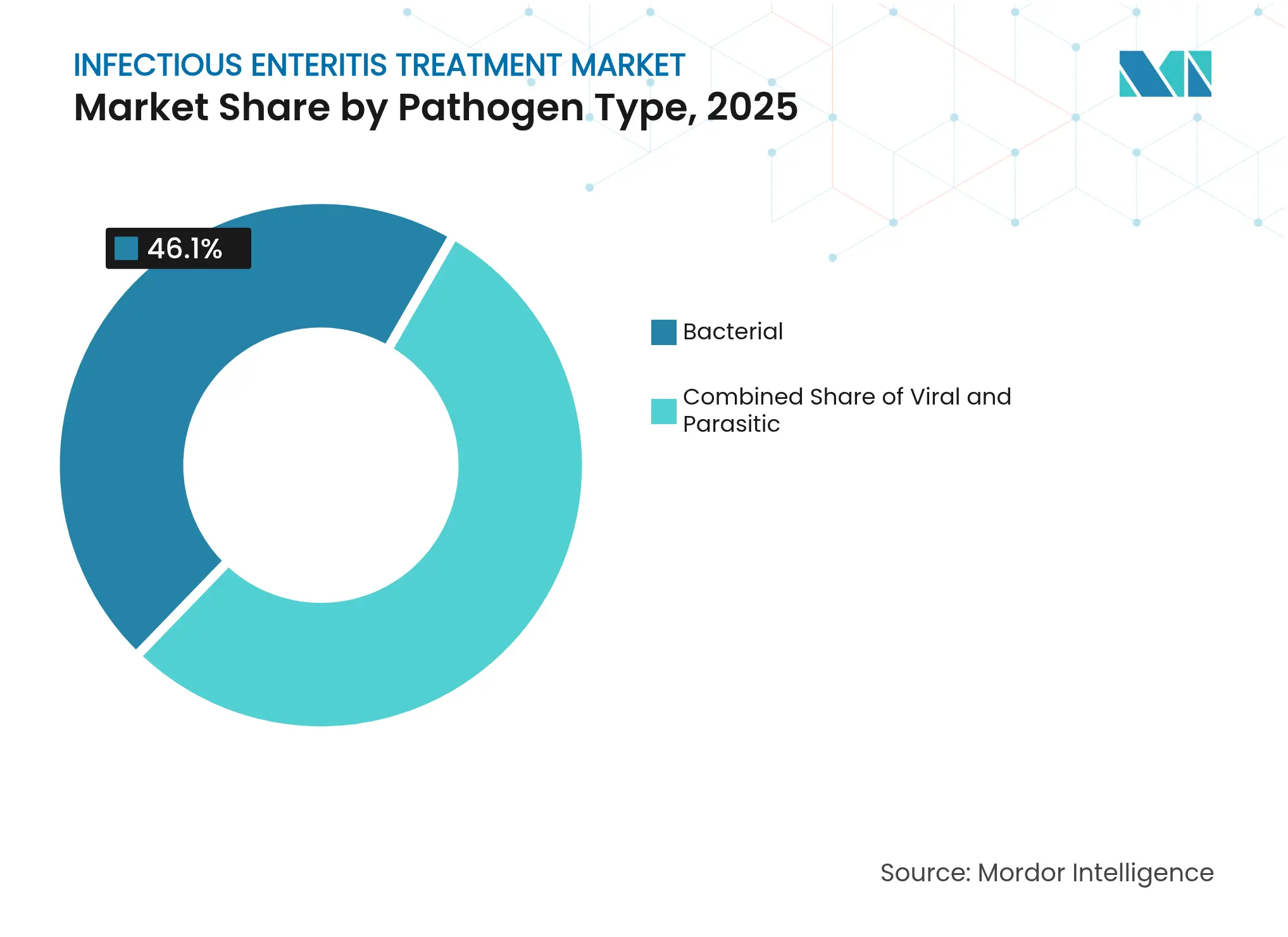

- By pathogen type, bacterial infections dominated with 46.10% share in 2025; viral pathogens are set to rise at a 9.41% CAGR.

- By patient age group, pediatrics commanded 48.93% of the infectious enteritis treatment market size in 2025 and is forecast to grow at a 10.10% CAGR to 2031.

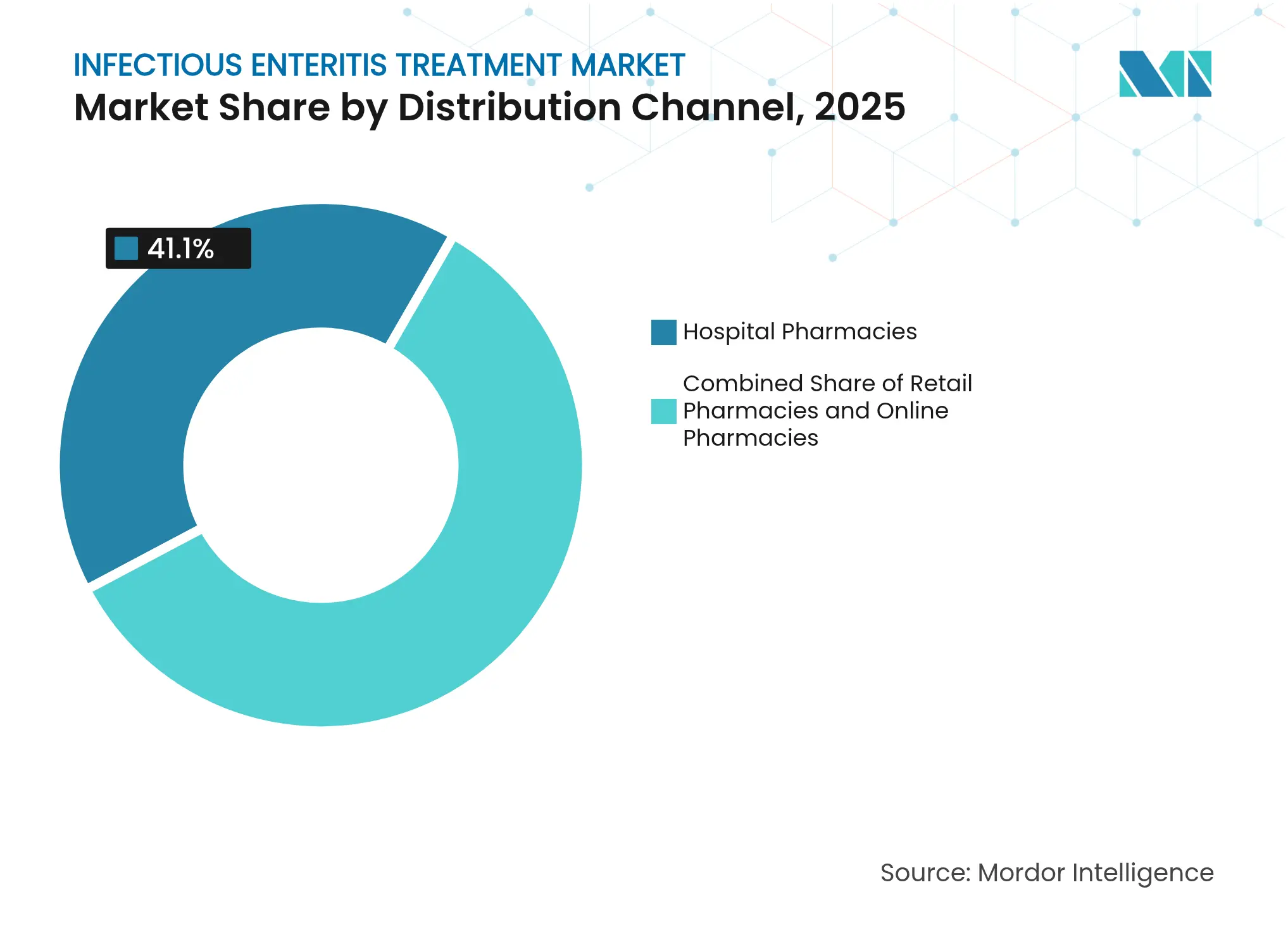

- By distribution channel, hospital pharmacies held 41.10% revenue share in 2025, whereas online pharmacies are pacing at an 8.45% CAGR.

- By geography, North America held 36.40% of infectious enteritis treatment market share in 2025, and Asia Pacific represents the fastest-growing region at a 10.21% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Infectious Enteritis Treatment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growing

AMR-resistant bacterial strains

Growing

AMR-resistant bacterial strains

| +1.8% | Global; concentrated in North America & EU | Medium term (2-4 years) |

(~) %

Impact on CAGR Forecast

:

+1.8%

|

Geographic

Relevance

:

Global;

concentrated in North America & EU

|

Impact

Timeline

:

Medium term

(2-4 years)

|

Uptake of

oral microbiome-restoration LBPs

Uptake of

oral microbiome-restoration LBPs

| +1.2% | North America & EU; expanding to APAC | Short term (≤ 2 years) | |||

Pediatric

rotavirus vaccine roll-outs

Pediatric

rotavirus vaccine roll-outs

| +0.9% | APAC core; spill-over to MEA & South America | Long term (≥ 4 years) | |||

Re-emergence

of travel-related enteritis

Re-emergence

of travel-related enteritis

| +0.7% | Global; peak in tourism-dependent regions | Short term (≤ 2 years) | |||

Accelerated

FDA LPAD approvals

Accelerated

FDA LPAD approvals

| +0.6% | North America; regulatory spillover to EU | Medium term (2-4 years) | |||

AI-enabled

drug-repurposing platforms

AI-enabled

drug-repurposing platforms

| +0.4% | Global; led by North America & EU | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Growing AMR-Resistant Bacterial Strains Spurring Premium Narrow-Spectrum Drugs

Escalating carbapenem-resistant Enterobacterales and fluoroquinolone-resistant Campylobacter species are pushing clinicians toward precision therapeutics that minimize microbiome disruption and curb resistance propagation. FDA approval of Zevtera (ceftobiprole medocaril sodium) in March 2024 for Staphylococcus aureus bloodstream infections signaled regulatory openness to advanced narrow-spectrum options.[1]U.S. Food and Drug Administration, “FDA Approves Zevtera,” fda.gov EMBLAVEO, cleared in February 2025, became the first marketed monobactam/β-lactamase-inhibitor combination, reinforcing premium pricing traction in niche anti-infective categories.[2]AbbVie, “EMBLAVEO Receives FDA Approval,” abbvie.com Dual-action macrolones that simultaneously impair protein synthesis and DNA supercoiling make bacterial resistance development up to 100 million times harder, underpinning a strategic shift to mechanism-intensive antibiotics. Healthcare payers increasingly prioritize resistance-sparing attributes over unit-cost considerations, widening commercial opportunities for innovators.

Rapid Uptake of Oral Microbiome-Restoration Therapeutics (LBPs) Post-Antibiotics

Live biotherapeutic products (LBPs) such as REBYOTA and VOWST deliver superior efficacy in preventing Clostridioides difficile recurrence, with VOWST lowering 8-week recurrence rates to 12.4% versus 39.8% for placebo. Vedanta Biosciences launched the Phase 3 RESTORATiVE303 trial for VE303 across 22 countries after Phase 2 data showed a 30.5% recurrence reduction. Randomized controlled trials of Lactiplantibacillus plantarum P9 reported a 20% drop in chronic diarrhea severity, validating strain-specific benefits. As clinical guidelines evolve, microbiome restoration is shifting from optional supplementation to standard-of-care adjunct therapy that complements antibiotics while mitigating dysbiosis.

Surge in Pediatric Rotavirus Vaccine Roll-Outs in Emerging Countries

Nigeria’s 2022 rotavirus introduction is expected to save nearly 100,000 children and reduce healthcare outlays by USD 28.5 million over the next decade.[3]Johns Hopkins IVAC, “Nigeria Rotavirus Vaccine Impact,” ivac.jhu.edu Vietnam expanded vaccination to 32 provinces in 2024 with nationwide coverage planned by 2026, reflecting broader Southeast Asian momentum. Injectable next-generation vaccines aim to overcome oral performance gaps in low-income settings, aided by heat-stable formulations that ease cold-chain constraints. Sustained procurement commitments from governments and multilaterals underpin predictable demand for pediatric formulations.

Re-Emergence of Travel-Related Enteritis Driving OTC Antidiarrheal Demand

International tourism recovery heightens travelers’ diarrhea cases, with enterotoxigenic Escherichia coli implicated in up to 82% of episodes among U.S. travelers. Bismuth subsalicylate halves incidence compared with placebo, establishing the compound as first-line prophylaxis. Phase 2 data released in January 2025 showed Travelan (IMM-124E) significantly reduced ETEC load and accelerated pathogen clearance, spotlighting passive immunotherapy potential. OTC brands are broadening point-of-sale distribution to airport pharmacies and travel clinics, reinforced by harmonized U.S. OTC antidiarrheal labeling under 21 CFR Part 335.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising

macrolide & fluoroquinolone resistance

Rising

macrolide & fluoroquinolone resistance

| -1.1% | Global; acute in APAC & MEA | Short term (≤ 2 years) |

(~) %

Impact on CAGR Forecast

:

-1.1%

|

Geographic

Relevance

:

Global; acute

in APAC & MEA

|

Impact

Timeline

:

Short term (≤

2 years)

|

Gut-microbiome

disruption curbing broad prescriptions

Gut-microbiome

disruption curbing broad prescriptions

| -0.8% | North America & EU; expanding globally | Medium term (2-4 years) | |||

Low

reimbursement for probiotic therapies

Low

reimbursement for probiotic therapies

| -0.5% | North America & EU; selective coverage gaps | Long term (≥ 4 years) | |||

Awareness

gaps in rural LMICs

Awareness

gaps in rural LMICs

| -0.4% | APAC, MEA & South America rural regions | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Macrolide & Fluoroquinolone Resistance Lowering First-Line Efficacy

European surveillance links excessive fluoroquinolone use to higher resistance in community pathogens, undermining enteritis protocols. U.S. emergency departments recorded 27.6% inappropriate antibiotic prescriptions, with 46% lacking infection indications. Broader stewardship efforts therefore push clinicians toward narrow-spectrum or reserve agents, compressing volume-driven revenues for legacy broad-spectrum drugs while opening premium niches for precision antimicrobials.

Adverse Gut-Microbiome Disruption Triggering Stewardship-Led Prescription Curbs

Antibiotic-associated dysbiosis is prompting tighter stewardship oversight, as evidence ties broad agents to prolonged microbiome recovery and secondary infections. Hospitals achieving 33% compliance across four stewardship criteria reported reduced mortality and shorter stays. AI-based decision support now guides empiric therapy to safeguard commensal flora, thereby elevating the bar for antibiotic selection and signaling greater demand for diagnostics that differentiate bacterial from viral enteritis.

Segment Analysis

By Route of Administration: Oral Dominance Driven by Patient Compliance

Oral products generated 57.48% of 2025 revenue, supported by outpatient convenience and rising adherence among pediatric and adult cohorts. The infectious enteritis treatment market size attributable to oral delivery is forecast to climb at an 7.92% CAGR through 2031 as companies invest in targeted capsules and pH-sensitive coatings that improve intestinal bioavailability. Injectable formulations remain indispensable for severe dehydration cases requiring rapid serum concentrations, accounting for the segment’s share of hospital spending. Innovations such as MIT’s bioinspired pumping capsule achieve injection-level tissue deposition via the GI tract without invasive administration.

In parallel, Harvard’s RNACap platform and University of Arkansas cellulose-nanocrystal microspheres showcase future oral delivery modalities that protect fragile payloads until intestinal release. Continued technology gains will likely sustain oral leadership, though parenteral advances will keep a foothold in critical-care settings where speed trumps convenience.

Note: Segment shares of all individual segments available upon report purchase

By Drug Class: Antibiotics Face Microbiome Therapeutic Challenge

Antibiotics still held 51.10% share in 2025, but rising resistance and stewardship pressures are shifting momentum toward probiotics and live microbiome therapeutics, the fastest-growing class at a 8.96% CAGR. The infectious enteritis treatment market share for vaccines is also expanding as next-generation rotavirus and norovirus candidates progress. FDA clearance of gepotidacin (Blujepa) in March 2025 the first novel oral antibiotic class for urinary infections in 30 years illustrates ongoing innovation yet underlines that new entrants must demonstrate resistance-mitigating benefits to gain formulary traction .

Symptomatic agents such as antispasmodics and oral rehydration solutions will persist as adjuncts, but investor focus is gravitating toward assets that balance pathogen eradication with microbiome preservation. This pivot aligns commercial strategies with payer priorities around long-term resistance management and healthcare-associated infection prevention.

By Pathogen Type: Bacterial Segment Pressured by Resistance

Bacterial pathogens commanded 46.10% of 2025 revenues, yet growth decelerates as stewardship cuts unnecessary antibiotic use and diagnostics partition viral and parasitic etiologies more precisely. Conversely, viral enteritis therapies are projected to post a 9.41% CAGR through 2031 thanks to expanded vaccine programs and better point-of-care detection tools.

AI-driven discovery platforms have uncovered nearly 900 000 antimicrobial peptide candidates, promising fresh options against priority bacterial threats. However, without simultaneous stewardship, bacterial resistance could erode value, underscoring the need for diagnostics and narrow-spectrum solutions that protect microbiome integrity while suppressing resistant strains.

Note: Segment shares of all individual segments available upon report purchase

By Patient Age Group: Pediatric Leadership Through Vaccine Innovation

Pediatrics contributed 48.93% of 2025 revenue and is forecast to grow at 10.10% CAGR, reflecting aggressive rotavirus immunization and tailored probiotic formulations. The infectious enteritis treatment market size uplift is accentuated by evidence that Bifidobacterium animalis subsp. lactis BLa80 cut diarrhea duration to 122.6 hours versus 148.4 hours for controls in children aged 0-3 years. High-dose Bacillus clausii spore probiotics shortened recovery by 3 days in infants 3-24 months old. Diagnostic biomarker use in emergency departments such as CRP and procalcitonin helps curb empiric antibiotic exposure, aligning pediatric protocols with stewardship aims.

Adults remain the largest volume segment due to population size, but lower growth reflects entrenched treatment patterns and fewer innovation triggers. Geriatric management complexity, including polypharmacy and immunosenescence, drives specialized research yet contributes modest revenue share compared with pediatric volumes.

By Distribution Channel: Online Pharmacies Surge Amid Digital Health Integration

Hospital pharmacies owned 41.10% of 2025 sales yet face share erosion as outpatient care shifts toward telemedicine and e-commerce. Online channels, climbing at an 8.45% CAGR, leverage virtual consultations and direct-to-consumer diagnostics to streamline therapy initiation. Community pharmacists demonstrate cost-effective management of uncomplicated infections, achieving lower revisit rates than conventional care models. Ambulatory pharmacy expansion in India underscores the critical role of pharmacists in antimicrobial stewardship and medication counselling. As digital platforms integrate prescription services with remote symptom monitoring, online pharmacies will capture a growing slice of the infectious enteritis treatment market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America held 36.40% revenue share in 2025, buoyed by advanced diagnostic capacity, reimbursement for premium therapeutics, and accelerated FDA pathways such as LPAD that shorten time-to-market. Robust venture funding fuels AI-guided discovery start-ups, reinforcing regional leadership in precision antimicrobials and microbiome-based solutions.

Asia-Pacific is the fastest-growing arena, tracking a 10.21% CAGR through 2031 as rotavirus vaccine coverage surges across Pakistan, Vietnam, and Nigeria-modeled programs. Rising healthcare spending, diagnostics expansion, and supportive government policies collectively enlarge patient access. Climate-change studies link temperatures above 30°C to 39% higher diarrhea risk, signaling sustained therapeutic need across tropical APAC geographies. Harmonizing antimicrobial policies remains a priority, given diverse Helicobacter pylori resistance patterns and variable gastric cancer burdens.

Europe records steady growth on the back of ESAC-Net surveillance and mandated stewardship, though aging populations and cost-containment render market expansion incremental. Middle East & Africa and South America present latent potential tied to limited infrastructure. Mobile outreach programs in Niger treated 12,004 patients in three months, demonstrating scalable care in conflict zones. Awareness studies show only one-third of Ghanaian respondents grasp AMR concepts, underscoring education as a prerequisite for effective market penetration.

Competitive Landscape

Market Concentration

The infectious enteritis treatment market is moderately fragmented. Multinational incumbents are partnering with AI specialists exemplified by Eli Lilly’s alliance with OpenAI to compress discovery timelines for novel antimicrobials. Consolidation continued when Shionogi acquired Qpex Biopharma to strengthen β-lactamase inhibitor pipelines ahead of U.S. commercialization. Live biotherapeutic developers such as Acurx Pharmaceuticals advance selective antibiotics like ibezapolstat that spare commensal flora while achieving 96% cure rates in CDI trials.

White-space innovation targets pediatric-specific dosing and rural distribution. Companies are engineering heat-stable vaccine formulations to eliminate cold-chain dependence, a key barrier in low-resource settings. AI-optimized peptide databases supply a reservoir of candidates able to bypass known resistance pathways, promoting pipeline diversity. Overall, strategic focus is converging on therapies that demonstrate clear microbiome protection and resistance-mitigating value rather than volume-driven antibiotic sales.

Infectious Enteritis Treatment Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: GSK received FDA approval for Blujepa (gepotidacin) tablets, the first new antibiotic class for uncomplicated urinary tract infections in nearly 30 years, targeting female patients aged 12 and older with novel mechanism reducing resistance development risk.

- February 2025: AbbVie announced FDA approval of EMBLAVEO (aztreonam and avibactam) for complicated intra-abdominal infections in adults with limited treatment options, representing the first monobactam/β-lactamase inhibitor combination with commercial availability planned for Q3 2025.

- January 2025: Immuron Limited reported positive Phase 2 results for Travelan (IMM-124E) passive immunotherapy, demonstrating statistically significant reduction in ETEC colony-forming units and faster pathogen clearance for travelers' diarrhea prevention.

- August 2024: FDA approved YORVIPATH (palopegteriparatide) for hypoparathyroidism treatment in adults, with Phase 3 studies showing 68.9% of patients achieving normal serum calcium levels and independence from conventional therapy.

Table of Contents for Infectious Enteritis Treatment Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Growing AMR-Resistant Bacterial Strains Spurring Premium Narrow-Spectrum Drugs

- 4.2.2Rapid Uptake of Oral Microbiome-Restoration Therapeutics (LBPs) Post-Antibiotics

- 4.2.3Surge in Pediatric Rotavirus Vaccine Roll-Outs in Emerging Countries

- 4.2.4Re-Emergence of Travel-Related Enteritis Driving OTC Antidiarrheal Demand

- 4.2.5Accelerated FDA LPAD Approvals Streamlining Niche Anti-Infective Launches

- 4.2.6AI-Enabled Drug-Repurposing Platforms Shortening Discovery Cycles

- 4.3Market Restraints

- 4.3.1Rising Macrolide & Fluoroquinolone Resistance Lowering First-Line Efficacy

- 4.3.2Adverse Gut-Microbiome Disruption Triggering Stewardship-Led Prescription Curbs

- 4.3.3Low Reimbursement for Probiotic-Based Therapies in Developed Markets

- 4.3.4Awareness Gaps in Rural LMICs Delaying Treatment Initiation

- 4.4Regulatory Landscape

- 4.5Technological Outlook

- 4.6Porter’s Five Forces Analysis

- 4.6.1Threat of New Entrants

- 4.6.2Bargaining Power of Buyers/Consumers

- 4.6.3Bargaining Power of Suppliers

- 4.6.4Threat of Substitute Products

- 4.6.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value in USD)

- 5.1By Route of Administration

- 5.1.1Oral

- 5.1.2Injectables

- 5.1.3Other Route of Administration

- 5.2By Drug Class

- 5.2.1Antibiotics

- 5.2.2Antivirals

- 5.2.3Probiotics & Microbiome Therapeutics

- 5.2.4Vaccines

- 5.2.5Other Drug Class

- 5.3By Pathogen Type

- 5.3.1Bacterial

- 5.3.2Viral

- 5.3.3Parasitic

- 5.4By Patient Age Group

- 5.4.1Pediatric

- 5.4.2Adult

- 5.4.3Geriatric

- 5.5By Distribution Channel

- 5.5.1Hospital Pharmacies

- 5.5.2Retail Pharmacies

- 5.5.3Online Pharmacies

- 5.6By Geography

- 5.6.1North America

- 5.6.1.1United States

- 5.6.1.2Canada

- 5.6.1.3Mexico

- 5.6.2Europe

- 5.6.2.1Germany

- 5.6.2.2United Kingdom

- 5.6.2.3France

- 5.6.2.4Italy

- 5.6.2.5Spain

- 5.6.2.6Rest of Europe

- 5.6.3Asia-Pacific

- 5.6.3.1China

- 5.6.3.2Japan

- 5.6.3.3India

- 5.6.3.4Australia

- 5.6.3.5South Korea

- 5.6.3.6Rest of Asia-Pacific

- 5.6.4Middle East & Africa

- 5.6.4.1GCC

- 5.6.4.2South Africa

- 5.6.4.3Rest of Middle East & Africa

- 5.6.5South America

- 5.6.5.1Brazil

- 5.6.5.2Argentina

- 5.6.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Johnson & Johnson

- 6.3.2Pfizer Inc.

- 6.3.3Novartis AG

- 6.3.4GlaxoSmithKline plc.

- 6.3.5Merck & Co.

- 6.3.6Bristol-Myers Squibb

- 6.3.7Teva Pharmaceuticals

- 6.3.8Mayne Pharma

- 6.3.9BioGaia

- 6.3.10RedHill Biopharma

- 6.3.11Seres Therapeutics

- 6.3.12Acurx Pharmaceuticals

- 6.3.13Ferring Pharmaceuticals

- 6.3.14Takeda Pharmaceutical

- 6.3.15Sanofi

- 6.3.16CSL Seqirus

- 6.3.17Bharat Biotech

- 6.3.18Abbott Laboratories

- 6.3.19Glenmark Pharma

- 6.3.20AstraZeneca

- 6.3.21Probi AB

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Infectious Enteritis Treatment Market Report Scope

As per the scope of this report, enteritis refers to the inflammation of the small intestine. Infectious enteritis is the most common type and includes bacterial and viral enteritis. Eating or drinking contaminated food or water causes bacterial enteritis. Viral enteritis also occurs through eating or drinking contaminated food or water and after contact with someone who has the virus. Viral enteritis usually goes away within a few days. The Infectious Enteritis Treatment Market is Segmented By Route of Administration (Oral and Injectables), Drug Type (Antibiotics, Antivirals, and Others), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.