Radiodermatitis Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

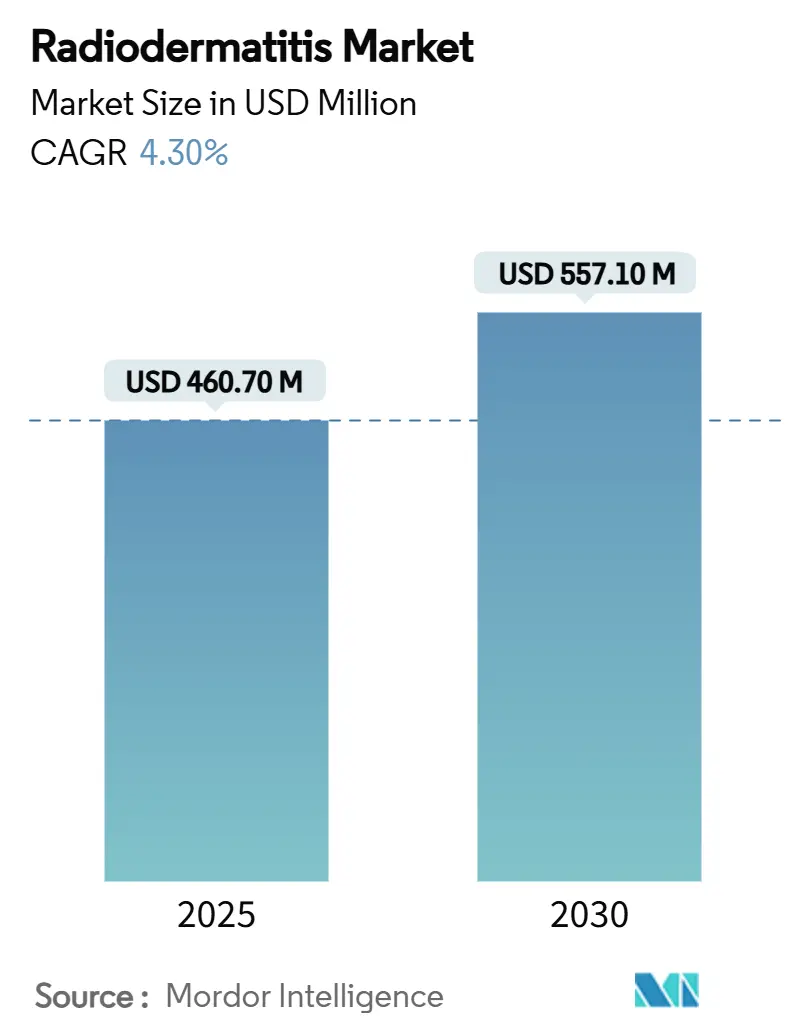

| Market Size (2025) | USD 460.70 Million |

| Market Size (2030) | USD 557.10 Million |

| Growth Rate (2025 - 2030) | 4.30% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Radiodermatitis Market Analysis by Mordor Intelligence

The radiodermatitis market size stands at USD 460.7 million in 2025 and is forecast to climb to USD 557.1 million by 2030, reflecting a 4.3% CAGR over the period. Demand is propelled by the expanding global cancer burden, rising radiotherapy utilization, and a gradual shift from reactive care to prevention-oriented protocols that emphasize AI-guided dosing dashboards and advanced barrier technologies. Increasing reimbursement for premium wound dressings, the broadening availability of over-the-counter (OTC) skin-care lines, and growing evidence for photobiomodulation therapy further support growth trajectories. At the same time, physician consensus gaps and raw-material supply risks temper near-term acceleration, leading to a moderately paced but structurally sound outlook for the radiodermatitis market. Competitive dynamics remain fragmented, yet consolidation is underway as large wound-care groups acquire niche innovators to secure next-generation dressings and drug-device combinations.

Key Report Takeaways

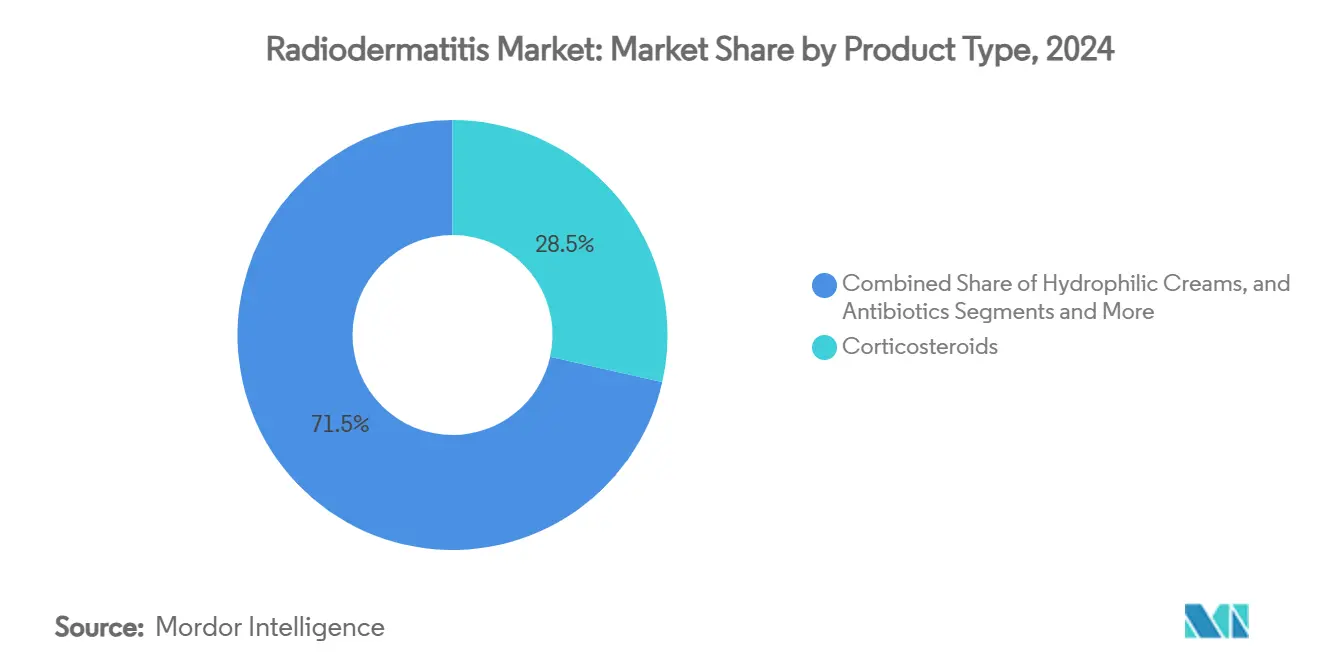

- By product category, corticosteroids retained a 28.5% share of the radiodermatitis market size in 2024, whereas no-sting barrier films are forecast to post an 8.2% CAGR through 2030.

- By distribution channel, retail pharmacies accounted for 33.7% revenue share in 2024, while online pharmacies show the fastest growth at 7.1% CAGR to 2030.

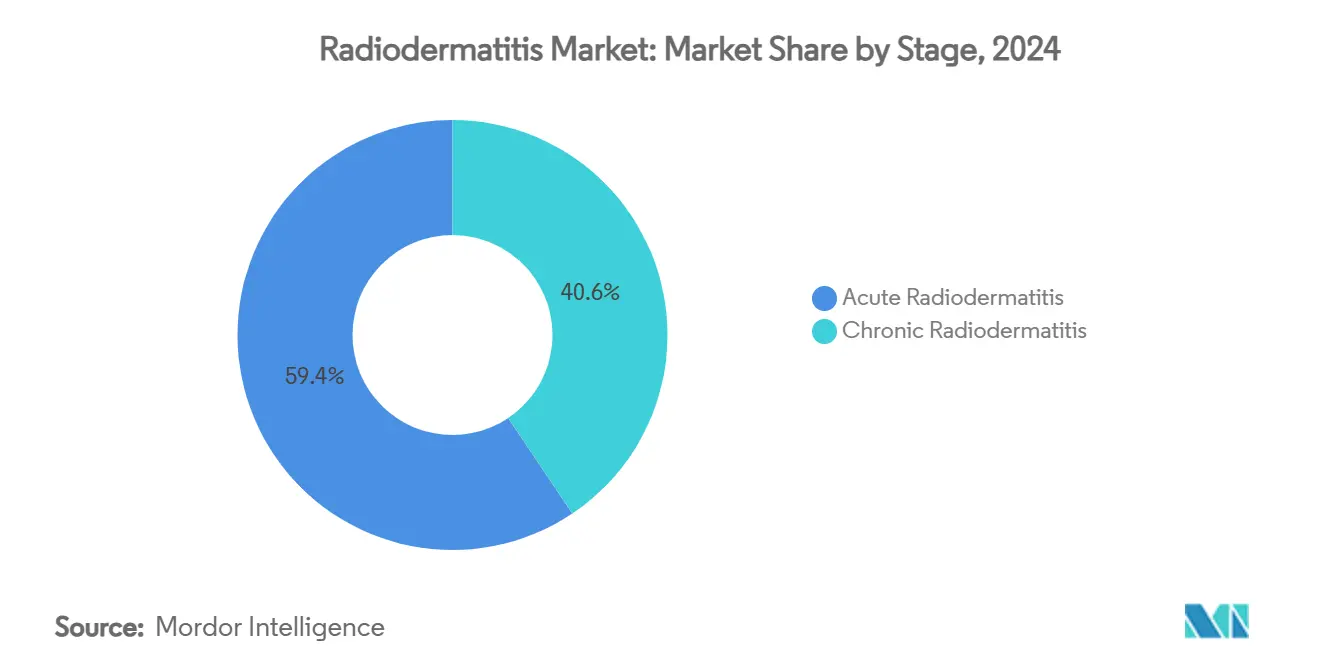

- By treatment stage, acute cases represented 59.4% of all episodes in 2024, yet chronic cases are advancing at a 7.3% CAGR to 2030.

- By end user, hospitals and cancer centers captured 39.4% share in 2024; home-care settings are set for 7.3% CAGR between 2025-2030.

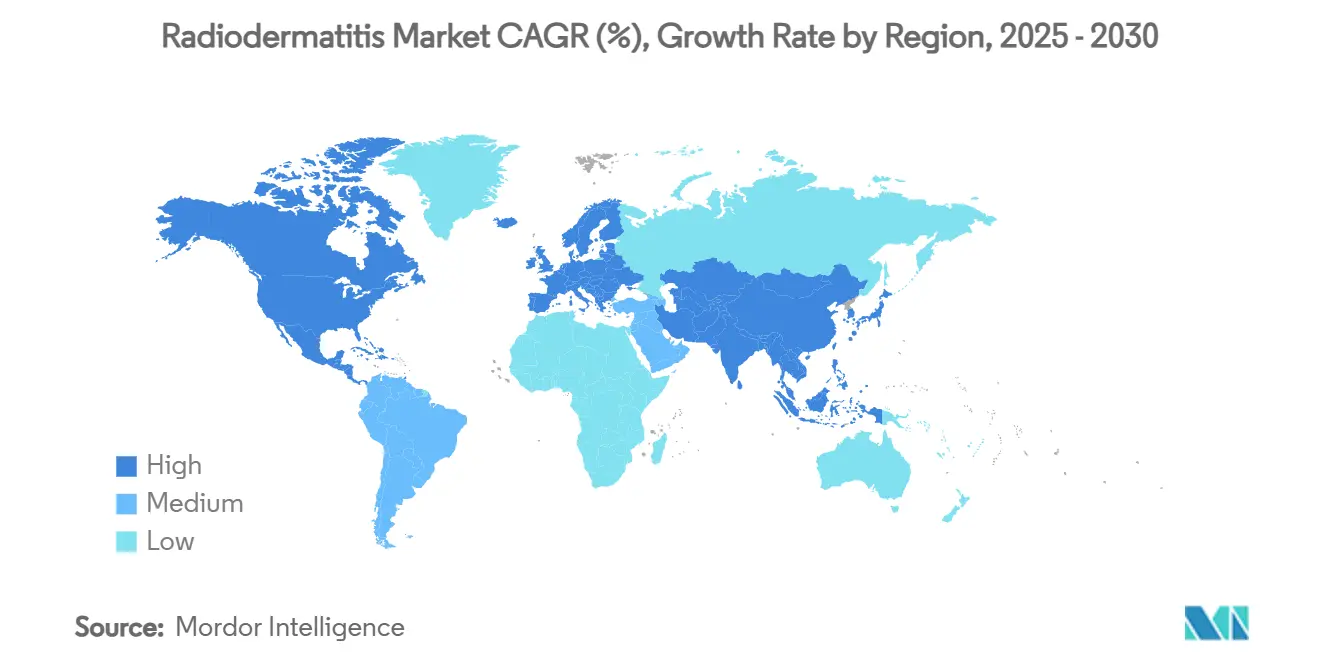

- By geography, North America led the radiodermatitis market with 32.6% of the share in 2024; Asia Pacific is projected to expand at a 7.4% CAGR to 2030.

Global Radiodermatitis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Cancer Prevalence And Radiotherapy Uptake | +1.20% | Global, with highest impact in APAC and MEA | Long term (≥ 4 years) |

| Growing Clinical Adoption Of Silicone-Based Barrier Films | +0.80% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Expansion Of Reimbursement For Advanced Wound Dressings | +0.60% | North America & EU core markets | Short term (≤ 2 years) |

| Nano-Fiber Drug-Loaded Patches Showing Phase II Success | +0.40% | North America & EU, early adoption markets | Long term (≥ 4 years) |

| AI-Driven Dosing Dashboards Reducing High-Dose Skin Hotspots | +0.30% | North America & EU, tech-advanced facilities | Medium term (2-4 years) |

| Increasing Availability Of OTC Radiodermatitis Skincare Lines | +0.20% | Global, with retail channel focus | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Global Cancer Prevalence and Radiotherapy Uptake

Cancer incidence continues to climb, and hypofractionated regimens—while shortening overall treatment time—concentrate doses that intensify skin toxicity. Proton-therapy patients in the United States tripled from 2012 to 2021, mirroring growth in Asia, where head-and-neck and breast indications account for therapy rates of 74% and 87% in India, respectively. The relationship between concentration and dermatitis risk places steady pressure on providers to upgrade prevention toolkits.[1]A. Renner et al., “Phase-III Barrier Film Trial,” ScienceDirect, sciencedirect.comAs radiotherapy suites expand in secondary cities, especially across China and India, demand for accessible yet clinically validated skin-care solutions accelerates, reinforcing the long-term pull on the radiodermatitis market.

Growing Clinical Adoption of Silicone-Based Barrier Films

Silicone-based barrier films such as Mepitel have moved swiftly from niche to routine practice. A Mayo Clinic cohort showed that 80% of breast cancer patients experienced materially lower dermatitis grades when films were applied from the first fraction. Randomized trials report recovery periods shrinking to 17 days versus 32 days under standard care, equating to a 47% improvement in healing velocity.[2]D. Keller, “Advanced Dressing Performance Metrics,” ScienceDirect, sciencedirect.comBroader protocol adoption is supported by reimbursement updates that now recognize single-use protective films as medically necessary, thus lowering out-of-pocket costs for patients and strengthening the radiodermatitis market.

Expansion of Reimbursement for Advanced Wound Dressings

In April 2025, the Centers for Medicare & Medicaid Services extended skin-substitute coverage from 12 to 16 weeks and doubled application limits to eight, materially improving the economic viability of advanced dressings for chronic cases.[3]CMS Policy Team, “Skin-Substitute Coverage Expansion,” cms.govThe policy acknowledges clinical evidence demonstrating faster closure rates for cellular and tissue-based products compared with traditional gauze. Coverage expansion also incentivizes hospital formularies to stock a broader range of premium solutions, which in turn lifts average selling prices and underpins healthy margins across the radiodermatitis market.

Nano-Fiber Drug-Loaded Patches Showing Phase II Success

Hierarchical nano-fiber matrices engineered to release antioxidants and antimicrobials have cleared Phase II efficacy hurdles, posting superior adhesion, moisture balance, and bacterial control relative to legacy foams. Cerium-oxide nanoparticles embedded within these patches mimic superoxide dismutase activity, neutralizing free radicals that drive chronic inflammation. Commercial launch would add a high-value option to clinician toolkits, further diversifying product portfolios in the radiodermatitis market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low Physician Consensus On Standard-Of-Care Protocols | -0.70% | Global, particularly in emerging markets | Medium term (2-4 years) |

| Supply Risk Of Medical-Grade Silver And Silicone | -0.50% | Global, with highest impact in APAC manufacturing | Short term (≤ 2 years) |

| Regulatory Uncertainty For Bioengineered Platelet Gels | -0.40% | North America & EU, regulatory-dependent markets | Long term (≥ 4 years) |

| Limited High-Level Clinical Evidence For Alternative Therapies | -0.30% | Global, with focus on evidence-based healthcare systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Low Physician Consensus on Standard-of-Care Protocols

Systematic reviews highlight limited high-quality randomized trials, leaving clinicians without definitive guidance and creating substantial variability in product selection. Inconsistent practice complicates payer assessments of medical necessity and dampens product uptake in emerging economies where cost controls are stringent. Professional societies are drafting consensus pathways, yet alignment remains a medium-term challenge, curbing rapid gains for the radiodermatitis market.

Supply Risk of Medical-Grade Silver and Silicone

The FDA lists 142 critical device categories at elevated shortage risk, including silver-based antimicrobial dressings and silicone films vital for radiodermatitis care. Raw-material volatility and geographic concentration of refining capacity expose manufacturers to price spikes and intermittent shortages. Although suppliers pursue dual-sourcing and vertical integration, significant diversification will likely take several production cycles, constraining short-term volume expansion across the radiodermatitis market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Corticosteroids Lead Despite Barrier Film Innovation

Corticosteroids preserved supremacy in 2024 with a 28.5% radiodermatitis market share, illustrating their entrenched role in mitigating acute inflammatory responses. Nevertheless, the no-sting barrier-film subsegment is accelerating at an 8.2% CAGR, evidencing a decisive pivot toward prophylaxis. The radiodermatitis market size for barrier films is set to reach USD 175.6 million by 2030, buoyed by clear healing benefits and user-friendly application protocols.

Advanced dressings such as hydrogels and hydrocolloids are gaining relevance owing to superior exudate management and enhanced patient comfort. Silicone-coated variants, supported by randomized study data, shorten average recovery times and lower dressing-related discomfort, reinforcing the shift toward patient-centric care. Honey-impregnated gauze retains a niche following among practitioners who favor natural antimicrobials, while growth-factor and platelet-rich formulations emerge as the next innovation frontier in the radiodermatitis treatment industry.

By Distribution Channel: Retail Dominance Challenged by Digital Growth

Retail pharmacies held a 33.7% revenue share in 2024, leveraging their brick-and-mortar presence to capture impulse and prescription-based traffic. Yet online platforms, expanding at a 7.1% CAGR, are reshaping buying habits as patients pursue discretion, competitive pricing, and subscription-based replenishment. The radiodermatitis market size attributable to e-commerce is projected to double by 2030 as telehealth platforms integrate ordering directly within virtual oncology consultations.

Hospital pharmacies remain critical for acute scenarios, where immediate access and clinician oversight are mandatory. Institutional purchasing benefits from bundled contracts that compress unit prices, although growth lags due to operational maturity. Digital channels add value-added services such as adherence alerts and interactive education modules, features unavailable in traditional outlets and increasingly favored by chronic-care patients.

By Stage: Acute Cases Drive Volume, Chronic Cases Drive Innovation

Acute radiodermatitis episodes accounted for 59.4% of treatments in 2024, underscoring the prevalence of skin reactions during active radiotherapy. Standard topical corticosteroids and barrier films dominate this stage, ensuring predictable procurement patterns. However, the chronic segment, advancing at 7.3% CAGR, fuels disproportionate revenue because care often involves multiple advanced products over extended durations.

Preventive regimens introduced during the acute window demonstrably cut chronic conversion rates, prompting oncology centers to embed skin-assessment checkpoints within every fraction schedule. Chronic presentations require complex combinations—advanced dressings, systemic antibiotics, and surgical debridement—that command premium pricing. Consequently, suppliers position high-margin drug-device hybrids toward this subpopulation, reinforcing the innovation tempo.

By End User: Hospitals Lead, Home Care Accelerates

Hospitals and cancer centers captured a 39.4% share in 2024, supported by integrated oncology pathways that deliver skin-care interventions alongside radiotherapy. Standardization efforts and multidisciplinary wound boards optimize product selection, sustaining institutional demand.

Home-care settings, projected to rise at 7.3% CAGR, mirror healthcare systems' objectives to contain costs and enhance quality of life. Remote monitoring apps allow nurses to supervise dressing changes while patients remain at home, extending the radiodermatitis market's reach beyond hospital walls. Dermatology clinics service complex refractory cases, providing specialized modalities such as laser resurfacing and platelet-rich plasma injections, thereby complementing hospital-led care continuums.

Geography Analysis

North America held 32.6% of global revenue in 2024, underpinned by robust reimbursement, extensive radiotherapy capacity, and early adoption of AI-enabled treatment planning. The United States drives regional leadership through large-scale cancer networks that embed evidence-based skin-care algorithms into electronic medical records, ensuring steady pull-through for high-value dressings. Canada contributes incremental growth via provincial funding expansions, while Mexico’s oncology-infrastructure upgrades stimulate import demand for premium barrier films.

The Asia Pacific radiodermatitis market is forecast to post 7.4% CAGR through 2030, fueled by large patient pools and rising radiotherapy installations across China, India, and Southeast Asia. Despite fragmented reimbursement and uneven access to advanced products, the region’s vast procedure volumes translate into significant aggregate opportunity. Japan and South Korea spearhead technological adoption, piloting nano-fiber dressings and photobiomodulation units, while Australia’s centralized procurement offers a springboard for new entrants seeking broader APAC penetration.

Europe maintains a mature yet resilient market, anchored by standardized treatment protocols across Germany, France, and the United Kingdom. Collaborative research grants facilitate rapid dissemination of best practices, sustaining steady uptake of novel therapies. Meanwhile, the Middle East & Africa and South America offer nascent potential: Gulf Cooperation Council states invest in comprehensive cancer centers, whereas Brazil and Argentina progress toward universal coverage for advanced wound dressings. However, currency volatility and healthcare-budget constraints temper near-term acceleration in these territories, moderating their contribution to the overall radiodermatitis market.

Competitive Landscape

The radiodermatitis market hosts a blend of diversified wound-care conglomerates and specialized dermatology innovators. 3M, ConvaTec, and Mölnlycke leverage global distribution and broad portfolios to secure institutional contracts, while smaller biotechnology firms carve niches with nano-fiber patches and growth-factor gels. Consolidation trends persist: larger players pursue bolt-on acquisitions to access proprietary delivery systems or AI-powered decision-support algorithms.

Technology differentiation is a focal battleground. ConvaTec’s InnovaMatrix launch, supported by 6.6% organic revenue growth during H1 2024, exemplifies evidence-backed product rollouts that resonate with formulary committees. Competitors invest in smart dressings embedded with pH-responsive indicators, enabling early infection detection and timely intervention. Concurrently, providers deploy AI dashboards that map radiation dose onto patient skin, predicting hotspot locations and allowing pre-emptive film placement—an approach that benefits both patients and device manufacturers.

Regulatory scrutiny shapes competitive dynamics. An FDA warning letter issued to Integra LifeSciences in January 2025 underscores the importance of rigorous quality-system adherence. Companies embracing robust compliance processes gain reputational advantages and smoother market access. Still, white-space opportunities remain: personalized combination kits bundling barrier films with antioxidant serums, or clinic-to-home service models integrating tele-dermatology, stand ready to redefine value propositions.

Radiodermatitis Industry Leaders

3M Company

Mölnlycke Health Care AB

ConvaTec Group Plc

Smith & Nephew plc

Medline Industries LP

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The FDA classified a device that detects bacterial protease activity in chronic wound fluid as Class II, paving the way for improved infection monitoring

- April 2025: CMS extended skin-substitute coverage to 16 weeks and raised application limits, enhancing patient access to advanced dressings

- February 2025: Phase II trial results showed that topical LUT014 met efficacy endpoints for radiation-induced dermatitis in breast-cancer patients.

- January 2025: The FDA issued a warning letter to Integra LifeSciences, citing manufacturing violations affecting wound-care devices

Global Radiodermatitis Market Report Scope

| Topical | Corticosteroids |

| Hydrophilic Creams | |

| Antibiotics | |

| Others | |

| Dressings | Hydrogel & Hydrocolloid Dressings |

| No Sting Barrier Films | |

| Honey Impregnated Gauze | |

| Silicone Coated Dressings | |

| Others | |

| Oral Systemic Drugs | |

| Emerging Therapies (growth-factor, platelet-based) |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Acute Radiodermatitis |

| Chronic Radiodermatitis |

| Hospitals & Cancer Centers |

| Dermatology Clinics |

| Home-care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Topical | Corticosteroids |

| Hydrophilic Creams | ||

| Antibiotics | ||

| Others | ||

| Dressings | Hydrogel & Hydrocolloid Dressings | |

| No Sting Barrier Films | ||

| Honey Impregnated Gauze | ||

| Silicone Coated Dressings | ||

| Others | ||

| Oral Systemic Drugs | ||

| Emerging Therapies (growth-factor, platelet-based) | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Stage | Acute Radiodermatitis | |

| Chronic Radiodermatitis | ||

| By End User | Hospitals & Cancer Centers | |

| Dermatology Clinics | ||

| Home-care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the radiodermatitis treatment market?

The radiodermatitis treatment market size is USD 460.7 million in 2025, with a projected rise to USD 557.1 million by 2030.

Which region leads global demand?

North America holds the largest share at 32.6%, supported by robust reimbursement and early technology adoption.

Which product category is growing the fastest?

No-sting barrier films record the highest CAGR at 8.2% through 2030 as clinicians shift toward prevention-focused care.

Why are online pharmacies gaining importance?

Online channels expand at 7.1% CAGR because patients value convenience, competitive pricing, and discreet delivery.

How is reimbursement policy affecting market growth?

CMS’s 2025 rule extending skin-substitute coverage to 16 weeks and doubling application limits directly boosts access to advanced dressings and underpins revenue growth.

What are the main challenges facing suppliers?

Physician consensus gaps on protocols and supply risks for medical-grade silver and silicone pose the most immediate hurdles to smoother expansion.

Page last updated on: