Gram-Positive Bacterial Infections Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 13.28 Billion |

| Market Size (2031) | USD 16.89 Billion |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

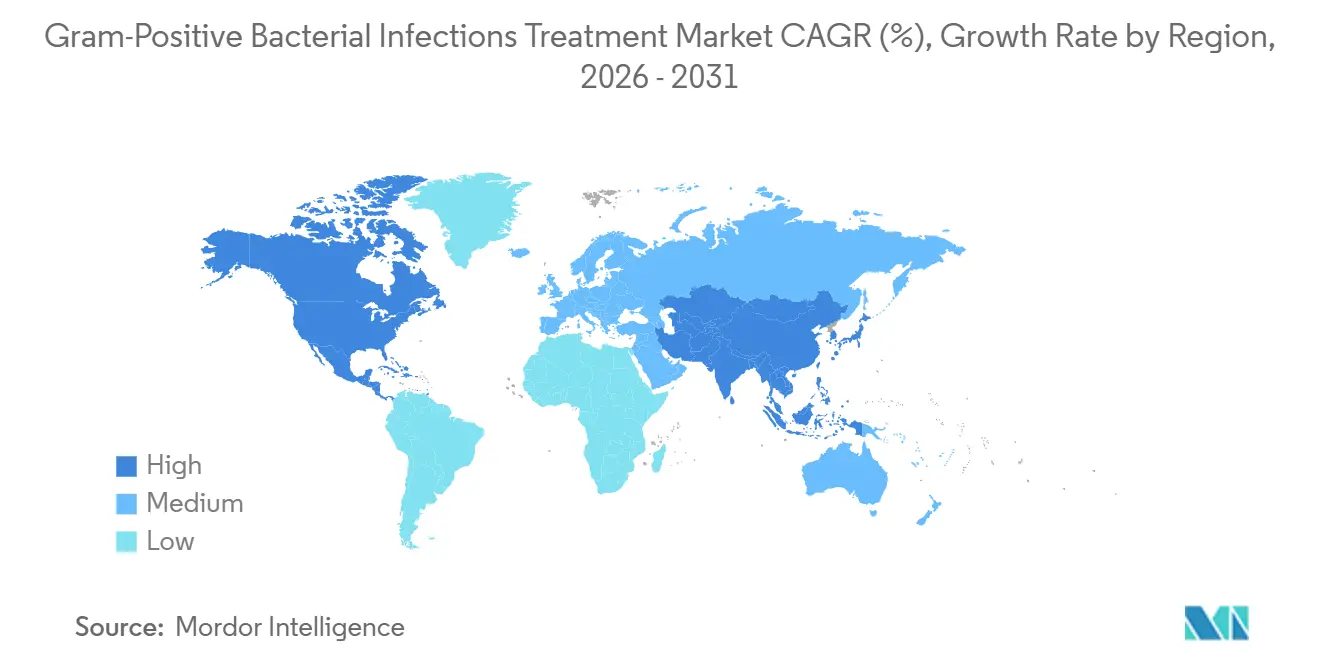

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

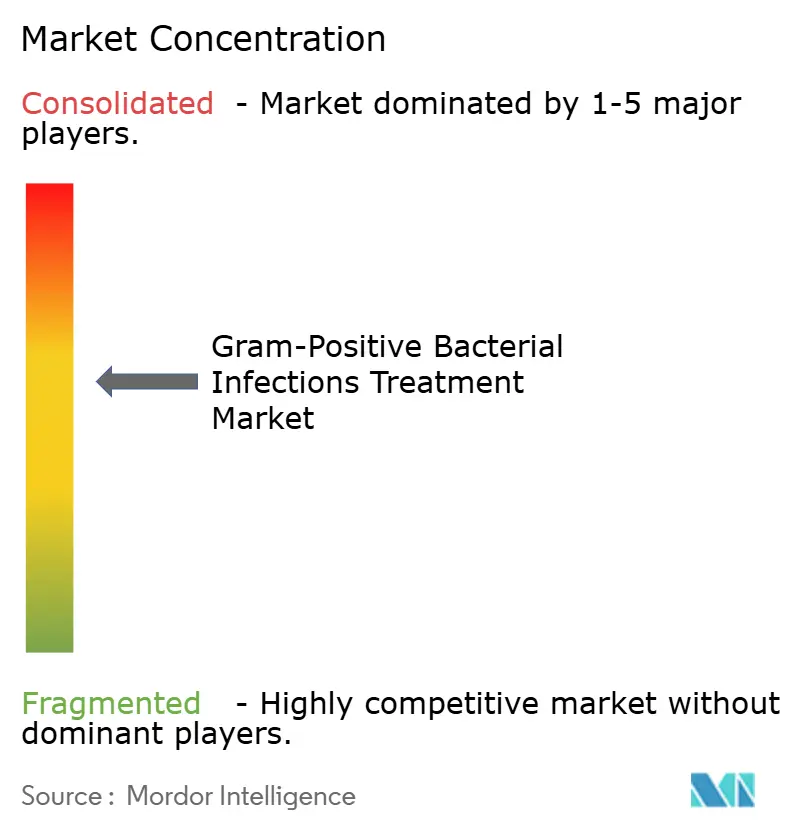

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gram-Positive Bacterial Infections Treatment Market Analysis by Mordor Intelligence

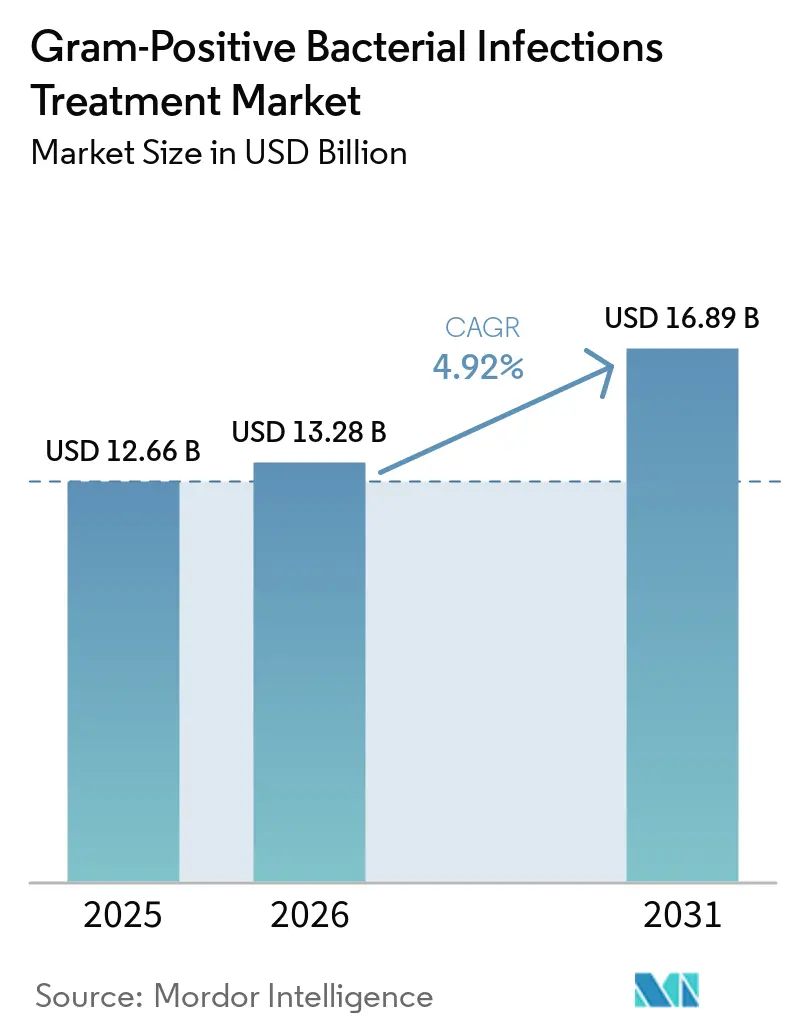

The Gram-Positive Bacterial Infections Treatment Market size is projected to expand from USD 12.66 billion in 2025 and USD 13.28 billion in 2026 to USD 16.89 billion by 2031, registering a CAGR of 4.92% between 2026 to 2031.

Rising methicillin-resistant Staphylococcus aureus (MRSA) infections, continued approvals of next-generation agents, and rapid molecular diagnostics sustain demand, even as antimicrobial-stewardship programs temper indiscriminate prescribing. Pharmaceutical leaders protect revenue streams by pairing life-cycle management of mature brands with pipeline investments that address vancomycin-resistant Enterococcus faecium and other WHO priority pathogens. Governments now treat antimicrobial supply as a national-security concern, launching stockpiling mandates and domestic manufacturing incentives that mitigate shortages. Meanwhile, AI-driven discovery partnerships, such as Eli Lilly’s collaboration with OpenAI, shorten lead-compound identification timelines and ease development economics.

Key Report Takeaways

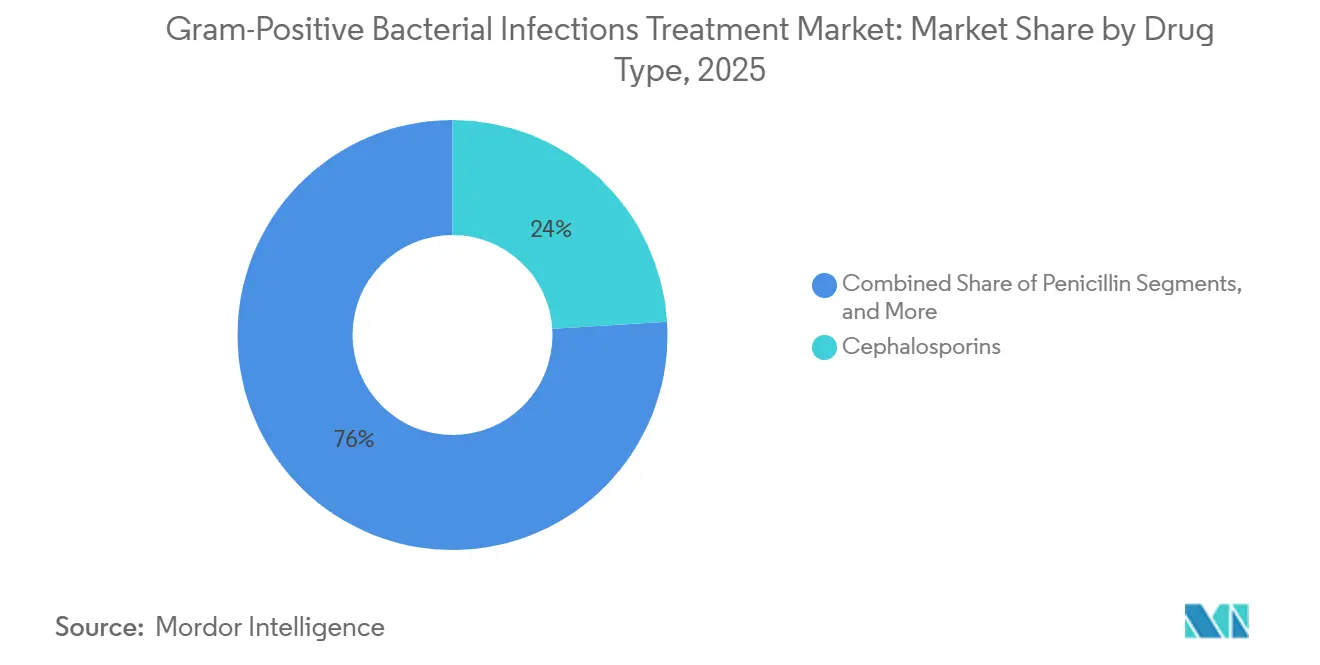

- By drug type, cephalosporins led the market share 25.20% for gram-positive bacterial infections in 2025, while oxazolidinones are forecasted to grow at a 9.26% CAGR through 2031.

- By disease, MRSA infections accounted for a 28.10% share of the gram-positive bacterial infections treatment market size in 2025 and are projected to expand at an 8.61% CAGR through 2031.

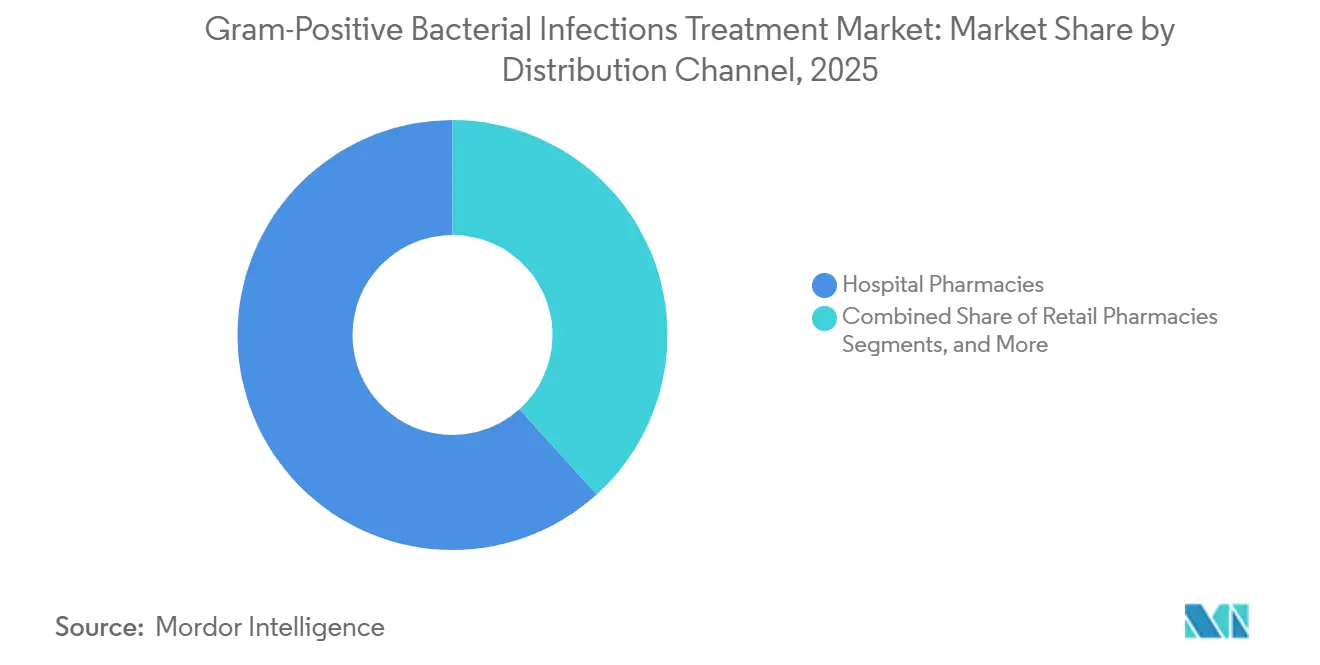

- By distribution channel, hospital pharmacies held a 61.70% revenue share in 2025; online pharmacies are projected to post the highest CAGR of 12.14% through 2031.

- By geography, North America dominated the market with a 38.40% revenue share in 2025, whereas the Asia-Pacific region is the fastest-growing, advancing at a 7.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Gram-Positive Bacterial Infections Treatment Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising prevalence of gram-positive infections | 1.20% | Global, strongest in Asia-Pacific and Sub-Saharan Africa | Medium term (2-4 years) |

| Increasing number of drug approvals and pipeline progression | 0.80% | North America & EU, spillover to emerging markets | Short term (≤ 2 years) |

| Growing healthcare expenditure in emerging economies | 0.60% | Asia-Pacific core, Latin America, Middle East | Long term (≥ 4 years) |

| Adoption of rapid molecular diagnostics enabling targeted therapy | 0.40% | North America & EU first, Asia-Pacific catching up | Medium term (2-4 years) |

| Resurgence of older narrow-spectrum antibiotics via stewardship programs | 0.30% | High-income countries worldwide | Short term (≤ 2 years) |

| Government subscription and pull-incentive models | 0.20% | OECD markets, selective emerging-market pilots | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Gram-Positive Infections

Healthcare-associated infections remain stubbornly high, and MRSA alone represented 121,000 AMR-related deaths annually.[1]World Health Organization, “Physician Density Database,” who.int Hospitals now screen high-risk admissions with PCR panels that deliver 93.3% detection accuracy within 88 minutes, allowing clinicians to start targeted therapy sooner and reserve broad-spectrum agents for confirmed need. Aging populations enlarge the pool of immunocompromised patients undergoing cancer therapy or organ transplantation, further boosting demand for effective gram-positive coverage. Hypervirulent strains with novel resistance elements add urgency to stewardship, although most currently affect gram-negative pathogens. Collectively, these dynamics lift baseline utilization of oxazolidinones, lipopeptides, and new-generation cephalosporins.

Increasing Number of Drug Approvals & Pipeline Progression

Between 2024 and 2025, the U.S. FDA cleared ceftobiprole for the treatment of MRSA bacteremia and acute skin infections, achieving a 68.9% success rate in bacteremia trials.[2]U.S. Food and Drug Administration, “FDA Approves drugs,” fda.gov Gepotidacin secured Priority Review as the first topoisomerase-inhibiting antibiotic in decades, while contezolid earned approval in China with fewer hematologic adverse events than linezolid. WHO counts 97 antibacterial candidates in clinical development, 32 of which target priority pathogens. QIDP and Fast-Track incentives extend exclusivity, partially offsetting development risk and attracting new capital into the market for gram-positive bacterial infections. This regulatory momentum underpins a steady launch cadence through the forecast period.

Growing Healthcare Expenditure In Emerging Economies

Vietnam’s public hospitals dedicate 28.6% of drug budgets to antimicrobials, and Shandong Province in China saw antibiotic spending grow 56% from 2012-2016 before stewardship slowed the trend.[3]American Journal of Medicine, “Primary-Care Screening Survey,” amjmed.com India’s tertiary centers still allocate one-third of treatment costs to infection control, illustrating how limited diagnostic capacity often drives empiric, multi-drug regimens. Regional policymakers increasingly view AMR containment as an economic imperative; Indonesia’s National AMR Strategy for 2025-2029 embeds reimbursement reforms aimed at channeling funds toward innovative therapies. As incomes rise and insurance coverage widens, spending elasticity supports uptake of premium-priced oxazolidinones and lipoglycopeptides.

Adoption Of Rapid Molecular Diagnostics Enabling Targeted Therapy

Next-generation panels reduce pathogen-ID time to under three hours with ≥95% concordance versus culture, shrinking hospital stays, and improving stewardship metrics. Blood culture-free PCR kits guide early de-escalation, trimming carbapenem exposure without harming outcomes. MALDI-TOF adoption reaches 75.8% species-level accuracy directly from blood culture, although gram-positive identification lags gram-negative performance. Real-time nanopore sequencing picks up low-abundance resistance plasmids that traditional tests miss, allowing earlier switch to active agents. Combined, these tools raise physician confidence in narrow-spectrum choices and limit resistance selection pressure.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Escalating antibiotic resistance among gram-positive pathogens | -1.10% | Global, highest in hospital-dense urban areas | Medium term (2-4 years) |

| Patent expiries driving generic erosion | -0.70% | North America & EU, emerging-market spillover | Short term (≤ 2 years) |

| Stringent stewardship limiting broad-spectrum use | -0.40% | High-income countries with mature programs | Medium term (2-4 years) |

| Fragile API supply chains for niche gram-positive agents | -0.30% | Global, concentrated in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Antibiotic Resistance Among Gram-Positive Pathogens

Linezolid resistance now appears in multiple regions via 23S rRNA mutation and cfr gene uptake, curbing therapy length and success. Cambodia’s surveillance logged 12.5% extensively drug-resistant Neisseria gonorrhoeae isolates in 2023, underscoring how resistance traits spread quickly even in lower-use settings. Global antibiotic consumption climbed 16.3% between 2016 and 2023, with forecasts of 52.3% growth by 2030 if unchecked, accelerating selection pressure. These patterns threaten current pipelines and require simultaneous investment in prevention, diagnostics, and novel mechanisms.

Patent Expiries Driving Generic Erosion

Generic fidaxomicin launched in 2024, cutting branded C. difficile revenue and signaling similar risks for linezolid, vancomycin, and lipoglycopeptides as patents lapse. The plazomicin case showed how small innovators struggle to recover costs when sales fail to meet expectations in a stewardship-constrained environment. While GAIN Act extensions add five years of exclusivity, they do not fully offset revenue compression once generics arrive, dampening R&D appetite within the Gram-positive antimicrobials industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: Oxazolidinones Extend Momentum

Cephalosporins held 24.20% of the gram-positive bacterial infections treatment market share in 2025, anchored by broad empirical use and inclusion in surgical prophylaxis guidelines. FDA approval of ceftobiprole for MRSA bacteremia adds premium-priced volume and supports cephalosporin revenue resilience; however, stewardship directives and growing cephalosporin resistance in some geographies moderate long-term growth. Oxazolidinones, led by linezolid, posted the fastest expansion, with a 9.26% CAGR projected through 2031. Contezolid’s approval in China and promising Phase 3 data for tedizolid-analogue agents enhance safety perceptions and widen prescriber comfort. Long-acting lipopeptides such as dalbavancin hold niche utility for outpatient parenteral therapy but rely on reimbursement alignment to offset high single-dose prices. Glycopeptides face sustained pressure from vancomycin-resistant enterococci; developers respond with dosing-optimized formulations that lower nephrotoxicity risk and prolong clinical relevance. Pipeline-stage combination agents, for example, beta-lactam plus β-lactamase inhibitor pairings, mainly target gram-negative organisms, yet cross-labeling potential may expand coverage in mixed infections. Vaccinology advances, particularly against Group B Streptococcus, could gradually reshape demand by preventing infections that currently require prolonged intravenous treatment.

By Disease: MRSA Stewardship Drives Formulary Priority

MRSA infections accounted for 28.10% of the gram-positive bacterial infections treatment market size in 2025, reflecting the pathogen’s prevalence across surgical wards and intensive-care units. Despite stringent prevention programs, hospital-onset MRSA rates have plateaued, keeping demand for potent anti-MRSA drugs elevated. Pneumonia and sepsis contribute substantial pooled volume; the advent of rapid respiratory panels now guides earlier pathogen-directed therapy, which may curtail unnecessary dual coverage yet supports timely uptake of targeted agents. Pharyngitis, traditionally managed with narrow-spectrum penicillins, benefits only marginally from new drug launches, aligning with stewardship emphasis on Access-group antibiotics. Endocarditis and meningitis maintain steady but specialized demand, often requiring prolonged intravenous courses of combined agents. Trials investigating single-dose lipoglycopeptide regimens for uncomplicated bacteremia aim to reduce inpatient days, potentially freeing capacity in resource-limited centers.

By Distribution Channel: Digital Platforms Gain Traction

Hospital pharmacies retained a dominant 61.70% share in 2025 as complex infections still require inpatient administration and close monitoring. Integrated stewardship software recommends dose adjustments in real time, aligning inventory with susceptibility trends and minimizing wastage. Retail pharmacies cater to uncomplicated skin and respiratory infections; however, their share declines slowly as virtual visits redirect prescriptions to digital fulfillment partners. Online pharmacies, though starting from a small base, exhibit a 12.14% CAGR through 2031, fueled by telemedicine expansion and relaxed e-prescribing regulations. Same-day logistics networks and temperature-controlled packaging meet stringent stability requirements for high-value oxazolidinone courses, improving adherence and outcomes.

Geography Analysis

North America commanded 38.40% of global revenue in 2025, propelled by early regulatory approvals, high diagnostic penetration, and broad insurance coverage. The EQUIP-A-Pharma initiative adds domestic 3D-printed linezolid capacity, fortifying supply resilience while lowering transportation emissions. Canadian authorities now oblige manufacturers to file shortage-risk plans and hold safety stocks, steps that enhance predictability for hospital buyers. Mexico benefits from near-shoring trends and streamlined USMCA trade lanes that shorten lead times for critical inputs. However, fragmented stewardship enforcement still encourages empiric multi-drug regimens in some regions.

Europe preserves a sizeable share through cohesive AMR policy frameworks. The proposed Critical Medicines Act coordinates joint procurement, ensuring smaller member states can access novel agents without price inflation. Surveillance data from ECDC confirm that broad-spectrum consumption tracks resistance evolution closely, reinforcing pay-for-performance models that reward narrow-spectrum adherence. Western European markets secure advance-purchase agreements for pipeline candidates, whereas Eastern Europe faces reimbursement delays that slow uptake. Pan-regional clinical societies publish emergency-department guidelines emphasizing biomarker-guided initiation and rapid de-escalation, harmonizing practice patterns across disparate health systems.

Asia-Pacific registers the fastest growth at a 7.78% CAGR to 2031, buoyed by expanding universal health coverage schemes and domestic innovation pipelines. Singapore incubates bacteriophage and antimicrobial-peptide startups, positioning itself as a translational hub. China’s National Medical Products Administration approved carrimycin and contezolid, demonstrating regulatory agility and rising innovation capacity. Japan achieved sizable consumption cuts for third-generation cephalosporins, yet the MRSA burden remains high, sustaining premium agent demand. India contends with affordability gaps that limit access to branded oxazolidinones, encouraging generic substitution and parallel importation when domestic supply falters. Australia’s stockholding mandate and supplier price uplifts underpin stable supplies despite long supply chains.

Competitive Landscape

The gram-positive bacterial infections treatment market shows moderate concentration, with multinational firms leveraging decades-old fermentation assets and lobbying experience to shape reimbursement frameworks. GSK, Pfizer, Merck, and Johnson & Johnson maintain leading portfolios but must offset impending patent cliffs for linezolid, dalbavancin, and fidaxomicin. They respond by investing in long-acting formulations, combination tablets, and pediatric indications that extend the brand arc. Emerging biotechnology players introduce differentiated mechanisms; Acurx’s ibezapolstat targets DNA polymerase IIIC and achieved 96% Phase 2 cure in C. difficile, attracting Fast-Track status. Such niche innovators often partner with large distributors to access global sales networks.

Strategic alliances intensify. Eli Lilly committed USD 100 million to the AMR Action Fund and teamed with OpenAI to apply generative models that propose novel scaffolds within days rather than months. Shionogi’s acquisition of Qpex Biopharma secures β-lactamase-inhibitor know-how, expanding its gram-negative and gram-positive combined franchise. Contract-development and manufacturing organizations scale continuous-manufacturing lines that cut batch times, enabling rapid surge capacity during outbreak spikes. Digital-regulatory sandboxes run by DARPA simulate process changes in silico, trimming qualification cycles and lowering barriers for smaller entrants.

Gram-Positive Bacterial Infections Treatment Industry Leaders

Novartis AG

Pfizer Inc.

GSK Plc

Merck & Co.

Cipla

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Acurx Pharmaceuticals, Inc. announced presentation of a scientific poster at the 35th Congress of ESCMID Global (European Society of Clinical Microbiology and Infectious Diseases) held in Munich, Germany from April 17-21, 2026. Using microbiome profiling shotgun metagenomics (MetaPhlAn) the authors concluded that DNA pol IIIC compounds represent a targeted strategy to treat resistant Gram-positive infections while preserving microbiome structure, minimizing downstream complications associated with antibiotic-induced dysbiosis.

- February 2025: Resilience won USD 17.5 million in HHS funding to upscale domestic API output for shortage-prone drugs.

- February 2025: FDA approved Emblaveo (aztreonam-avibactam) for complicated intra-abdominal infections, expanding options against multi-resistant organisms.

Global Gram-Positive Bacterial Infections Treatment Market Report Scope

As per the scope of the report, gram-positive bacterial infections treatment involves using specific antibiotics such as penicillins, glycopeptides (vancomycin), and macrolides, which target the thick peptidoglycan cell walls characteristic of these bacteria. Treatments aim to destroy bacteria or inhibit their growth to resolve conditions like pneumonia, skin infections, and bacteremia.

The gram-positive bacterial infections treatment market is segmented by drug type, disease, distribution channel, and geography. By drug type, the market includes beta-lactam antimicrobials, cephalosporins, penicillins, fluoroquinolones, lipopeptides, oxazolidinones, glycopeptides, vaccines, and combination therapies & others. By disease, the market is categorized into pneumonia, sepsis, pharyngitis, MRSA infections, endocarditis, meningitis, and other diseases. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Beta-Lactam Antimicrobials |

| Cephalosporins |

| Penicillins |

| Fluoroquinolones |

| Lipopeptides |

| Oxazolidinones |

| Glycopeptides |

| Vaccines |

| Combination Therapies & More |

| Pneumonia |

| Sepsis |

| Pharyngitis |

| MRSA Infections |

| Endocarditis |

| Meningitis |

| Other Diseases |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Type | Beta-Lactam Antimicrobials | |

| Cephalosporins | ||

| Penicillins | ||

| Fluoroquinolones | ||

| Lipopeptides | ||

| Oxazolidinones | ||

| Glycopeptides | ||

| Vaccines | ||

| Combination Therapies & More | ||

| By Disease | Pneumonia | |

| Sepsis | ||

| Pharyngitis | ||

| MRSA Infections | ||

| Endocarditis | ||

| Meningitis | ||

| Other Diseases | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current market size?

The market size was USD 13.28 billion in 2026 and is projected to reach USD 16.89 billion by 2031, growing at a 4.92% CAGR.

Which drug class is growing fastest?

Oxazolidinones are the fastest-growing, with a 9.26% CAGR through 2031, driven by safer next-generation approvals like contezolid.

Why does MRSA remain the largest disease segment?

MRSA infections accounted for 28.10% of the market in 2025 due to high hospital-acquired infection rates, sustaining demand for potent anti-MRSA agents.

How are online pharmacies affecting market dynamics?

Online pharmacies are expanding rapidly with a 12.14% CAGR to 2031, fueled by telemedicine adoption and same-day logistics improving access to therapies.

Which region offers the highest growth potential?

Asia-Pacific is the fastest-growing region with a 7.78% CAGR, supported by expanding healthcare coverage and domestic approvals of novel agents.

Page last updated on: